Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

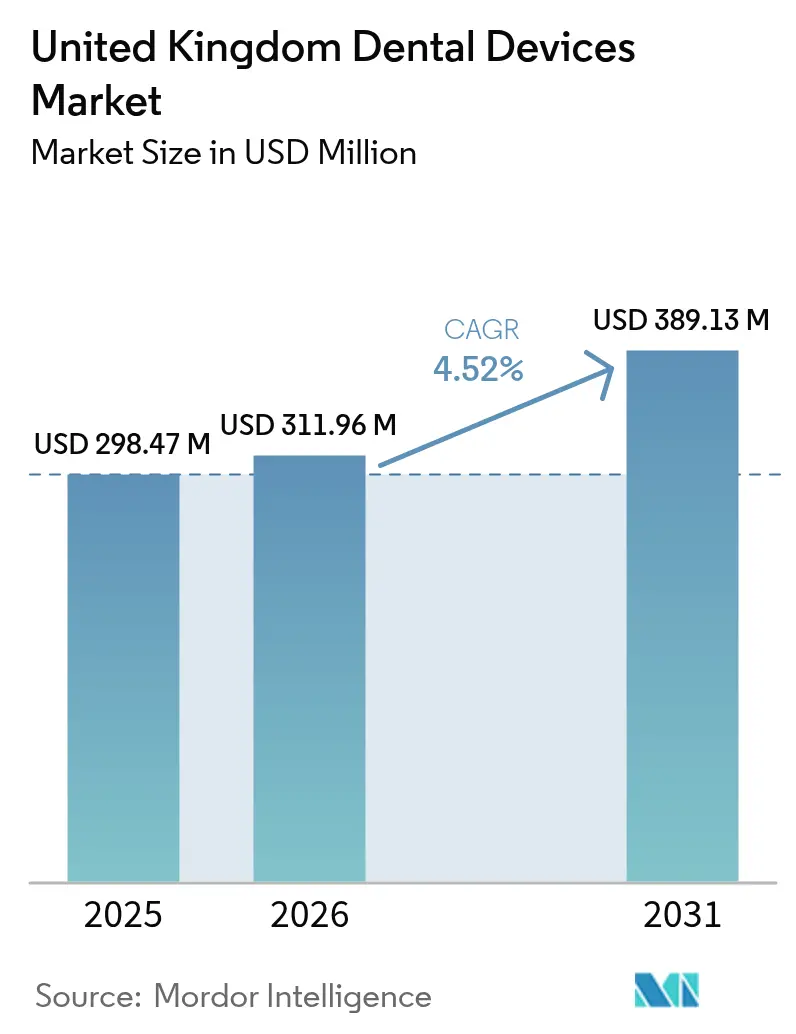

| Base Year Market Size (2025) | USD 298.47 Million |

| Market Size (2026) | USD 311.96 Million |

| Market Size (2031) | USD 389.13 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Dental Devices Market Analysis by Mordor Intelligence

The United Kingdom dental devices market size is expected to grow from USD 298.47 million in 2025 to USD 311.96 million in 2026 and is forecast to reach USD 389.13 million by 2031 at 4.52% CAGR over 2026-2031. Demand is accelerating as digital workflows, policy incentives such as the Super-Deduction Capital Allowance, and a demographic tilt toward older patients redefine investment priorities. England anchors the market, but Scotland is gaining momentum through targeted workforce initiatives. Dental consumables remain the revenue backbone, yet the equipment category is outpacing overall growth due to the rapid uptake of CAD/CAM, 3-D printing, and AI-enabled imaging. Independent practices are regaining ownership share from corporate groups, reshaping purchasing patterns and supply-chain relationships. Meanwhile, the NHS Dental Recovery Plan is catalyzing digital adoption even as workforce shortages restrain service capacity and delay equipment upgrades[1]Source: UK Parliament, “NHS Dentistry Recovery and Reform,” hansard.parliament.uk .

Key Report Take Aways

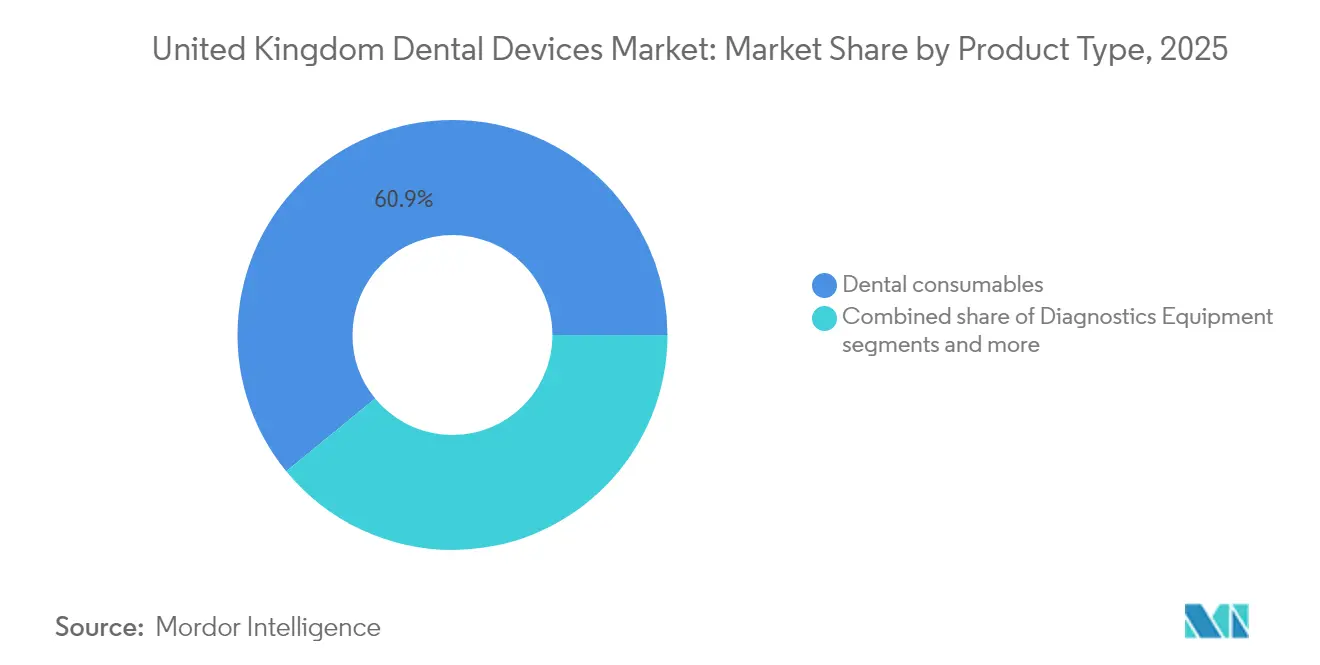

- By product type, dental consumables commanded 60.93% of the United Kingdom dental devices market share in 2025, while dental equipment is advancing at a 5.18% CAGR through 2031.

- By treatment, prosthodontics accounted for a 33.28% share of the United Kingdom dental devices market size in 2025; orthodontics is expanding at a 5.78% CAGR to 2031, led by clear aligners.

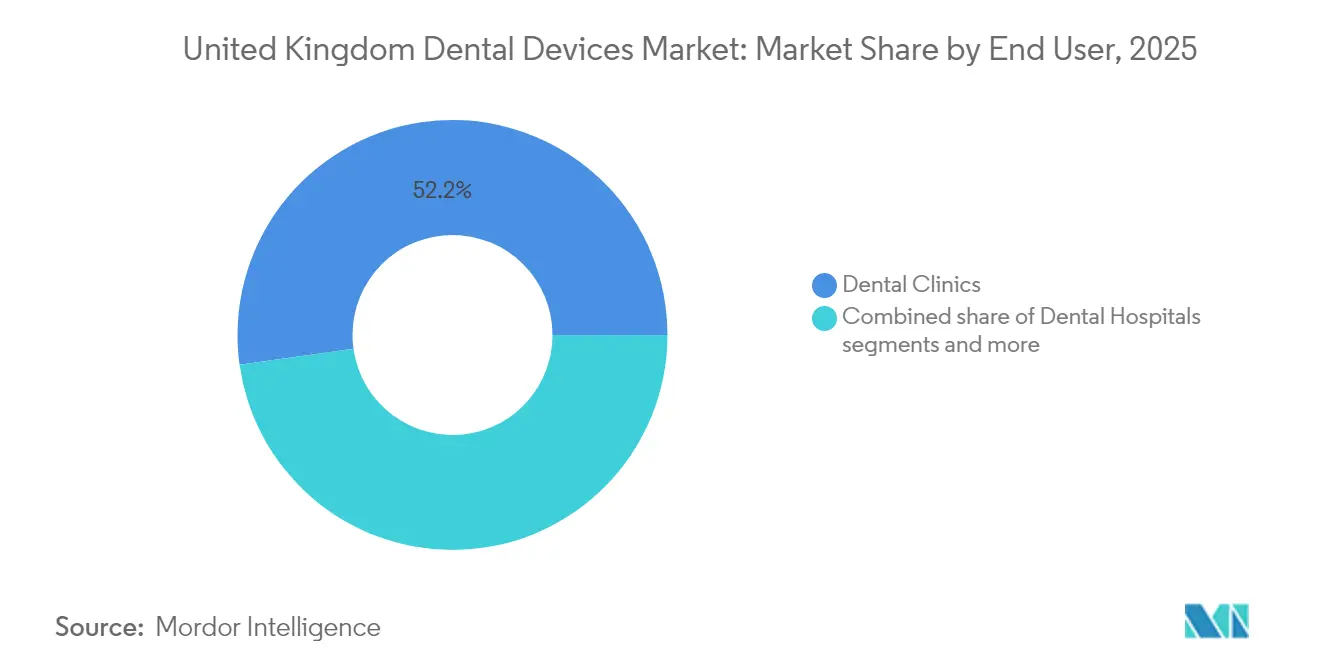

- By end user, dental clinics held 52.21% of the United Kingdom dental devices market in 2025, whereas academic and research institutes are growing fastest at 5.09% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Dental Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing U.K. Population Accelerating Demand for Prosthodontic & Implant Devices | +1.1% | National, with higher impact in England and Scotland | Long term (≥ 4 years) |

| NHS Dental-Contract Reform Driving Digital Equipment Adoption Across England | +0.9% | England, with spillover to Wales | Medium term (2-4 years) |

| Expansion of Private Dental Insurance (e.g., Denplan) Boosting High-value Cosmetic Devices | +0.8% | National, with concentration in urban centers | Medium term (2-4 years) |

| Super-Deduction Capital Allowance (2021-26) Catalysing Clinic Investment in CAD/CAM & 3-D Printing | +0.7% | National, with higher impact in England | Short term (≤ 2 years) |

| Post-Brexit UKCA Transition Deadlines Favouring CE-Marked Device Replacement Cycles | +0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing U.K. Population Accelerating Demand for Prosthodontic & Implant Devices

Adults aged ≥65 will represent 25% of the national population by 2050, pushing long-term demand for durable, biocompatible prosthodontic and implant solutions. Clinics are shifting toward zirconia-hybrid implants that blend titanium cores with zirconium-dioxide ceramic, reducing inflammatory response and addressing titanium hypersensitivity. Laboratory studies show these hybrids improve cell adhesion and osteogenic differentiation in human dental pulp stem cells compared with pure titanium. As a result, procurement teams are prioritizing suppliers able to guarantee consistent quality of advanced ceramic and composite implant lines. The driver’s influence is strongest in England and Scotland where geriatric dental infrastructure is most developed, and it underpins steady growth for the United Kingdom dental devices market through the forecast horizon.

NHS Dental-Contract Reform Driving Digital Equipment Adoption Across England

The NHS Dental Recovery Plan introduces financial incentives that reward higher treatment volumes and allocates a 40% lift in training places by 2031, prompting clinics to digitize workflows to meet throughput targets. Surveys show 99.3% of practitioners recognize digital benefits, yet capital costs remain the chief adoption barrier. Group practices in particular are scaling intraoral scanners and chairside milling to cut appointment times and align with preventive-care KPIs embedded in the reform. Although limited to England, the policy’s spillover into Wales is visible as suppliers report cross-border orders for UKCA-compliant scanners. This driver sustains above-market growth for digital equipment and cements its role in the United Kingdom dental devices market.

Expansion of Private Dental Insurance Elevating Device Sophistication

Private dental plans such as Denplan now cover 20% of Britons, and 61% of NHS patients would switch for faster care. Insured patients visit dentists more regularly, shortening replacement cycles for consumables and encouraging investment in premium restorative systems. The shift is most pronounced in urban centers where disposable income and aesthetic demand converge, fuelling orders for advanced composites, high-end implant kits, and cosmetic lasers. Consequently, device suppliers are tailoring portfolios toward higher-margin cosmetic lines, reinforcing value growth for the United Kingdom dental devices market.

Super-Deduction Capital Allowance Catalysing Clinic Investment in CAD/CAM & 3-D Printing

Until 2026, limited-company practices can deduct 130% of qualifying capital spend, translating a GBP 100,000 outlay into GBP 24,700 corporation-tax relief. Larger groups and well-capitalized independents are accelerating CAD/CAM chairside unit purchases and lab 3-D printers, compressing payback periods to under three years. Vendors report spike orders as practices race to secure equipment before the incentive lapses, temporarily lifting shipment volumes and inflating the equipment sub-segment’s contribution to the United Kingdom dental devices market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHS Workforce Shortage Constraining Equipment Replacement Cycles | -1.4% | National, with severe impact in rural and deprived areas | Medium term (2-4 years) |

| Import-led Inflation Raising ASPs of High-tech Devices Post-Brexit | -0.8% | National, with higher impact on equipment-intensive practices | Medium term (2-4 years) |

| UKCA Certification Uncertainty Deterring SME Product Launches | -0.5% | National, with concentration in England and Scotland | Short term (≤ 2 years) |

| Environmental Levies (Single-use Plastics Tax) Increasing Consumable Costs | -0.3% | National, with higher impact on high-volume practices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NHS Workforce Shortage Constraining Equipment Replacement Cycles

A documented gap of 5,500 dental professionals is widening “dental deserts,” particularly in coastal and deprived regions, with 95% of practices struggling to hire nurses and associates. Reduced chair capacity discourages capital outlays for advanced imaging and in-house milling, as owners question utilization rates. Associates are shifting toward private practice for higher remuneration, further throttling NHS throughput. Until expanded training cohorts graduate, staffing scarcity will dampen the pace of high-tech adoption, subtracting an estimated 1.4 percentage points from the base CAGR of the United Kingdom dental devices market.

Import-led Inflation Elevating Equipment Costs

Post-Brexit trade friction, sterling volatility, and lingering logistics bottlenecks have pushed up import prices for high-tech dental equipment, lifting average selling prices and lengthening pay-back periods on capital projects. Larger group practices and specialist clinics feel the squeeze most because digital scanners, 3-D printers, and implantology systems are sourced predominantly from continental Europe and North America, where suppliers have passed through higher production and shipping costs. With 82% of equipment items still imported, every 5% depreciation in sterling against the euro has added roughly GBP 2,700 to the ticket price of a typical chairside CAD/CAM unit, delaying upgrade cycles and suppressing order volumes. Many independents have responded by extending the useful life of existing assets or leasing refurbished systems, which tempers near-term penetration of next-generation digital workflows. Although some distributors are re-routing purchases through UKCA-ready stockpiles or negotiating hedged contracts, practices are unlikely to see meaningful price relief before 2027 when new bilateral trade accords and localized assembly lines are expected to stabilize costs

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Revolution Reshaping Equipment Segment

The equipment slice of the United Kingdom dental devices market recorded a 5.18% CAGR outlook to 2031, outstripping the consumables-dominated 60.93% revenue base in 2025. Practices cite chairside CAD/CAM and lab-grade 3-D printers as strategic investments that compress turnaround times and cut outsourcing fees. The CAD/CAM blocks and consumables niche is expanding in tandem with installed bases, locking clinics into proprietary supply chains that generate recurring revenue.

Intraoral scanners now permeate routine examinations, feeding STL data directly into cloud design portals. Meanwhile, three-dimensional printing is shifting complex restoration work from milling to additive, due to superior material efficiency and design freedom. AI-enabled sensors such as DEXIS Ti2 layer machine-learning analytics onto imaging, foreshadowing a diagnostic platform play rather than stand-alone hardware. These trends reinforce the value share of equipment and embed digital dependence throughout the United Kingdom dental devices market.

By Treatment: Orthodontics Disruption Through Clear Aligners

Prosthodontics retained the largest slice at 33.28% in 2025, yet orthodontics is the fastest-growing therapy line, advancing at 5.78% CAGR behind clear aligner acceleration. The April 2025 VAT ruling classifies aligners as “dental prostheses,” potentially delivering zero-rating that lowers patient cost and widens addressable demand. Adults drive much of the volume, seeking discreet aesthetics and remote monitoring apps that align with hybrid care models.

Restorative dentistry growth remains steady, buoyed by caries prevalence and the ageing population. Implantology benefits from zirconia-based materials that combine strength and biocompatibility, while periodontics and endodontics see incremental innovation via bioactive fillers. Collectively, these shifts broaden the therapeutic canvas and raise the average selling price across the United Kingdom dental devices market.

By End User: Academic Institutes Driving Innovation Ecosystem

Dental clinics captured 52.21% of 2025 revenue, but academic and research institutes are charting a 5.09% CAGR through 2031 on the back of expanded government funding that lifts the undergraduate dental tariff to GBP 36,041 for 2024-25. University laboratories are piloting AI-driven caries-detection algorithms and bio-printed graft scaffolds, creating early-adopter pathways for suppliers.

Hospitals hold a stable share, focusing on complex oral-maxillofacial surgeries, whereas dental laboratories are pivoting toward digital-first models, as illustrated by MediMatch’s management buy-out and 20% annual growth. The swing from solo to group practices, tempered by a resurgence of independent ownership, reshapes procurement cycles and underpins diversified demand across the United Kingdom dental devices market.

Geography Analysis

England leads the United Kingdom dental devices market, benefiting from dense practice networks and policy initiatives such as mobile dental vans and expanded training slots that aim to rebalance access in underserved locales. Yet the Public Dental Access Index reveals sharp intra-regional disparities, with many rural and coastal districts posting limited NHS appointment availability. Consequently, device vendors calibrate distribution strategies around metropolitan clusters while aligning service contracts to mobile units.

Scotland is growing above the national average, propelled by university intake quotas and retention incentives that address practitioner shortages. Procurement trends favor diagnostic and preventive devices that fit community-clinic deployment, aligning with health-inequality reduction programs. This focus widens the buyer base for portable X-ray and chairside screening units, reinforcing market expansion.

Wales is mid-overhaul of its General Dental Services contract, shifting from UDA volume metrics to care-package models that emphasize prevention. FY 2023-24 data show 1.4 million courses of treatment with 55.6% in Band 1 services such as fluoride varnish. Contract reform stimulates demand for diagnostic imaging that supports risk-stratified care, although overall device turnover remains below pre-pandemic peaks.

Northern Ireland maintains a steady trajectory supported by 1,195 dentists across 364 practices, with government spending of GBP 121.6 million on dental services in 2023-24. Patient co-payment increases prompt selective uptake of higher-value restorative devices, while laboratories invest in digital workflows to counter rising labor costs. Collectively, regional nuances shape channel strategies and incentive alignment across the United Kingdom dental devices market.

Competitive Landscape

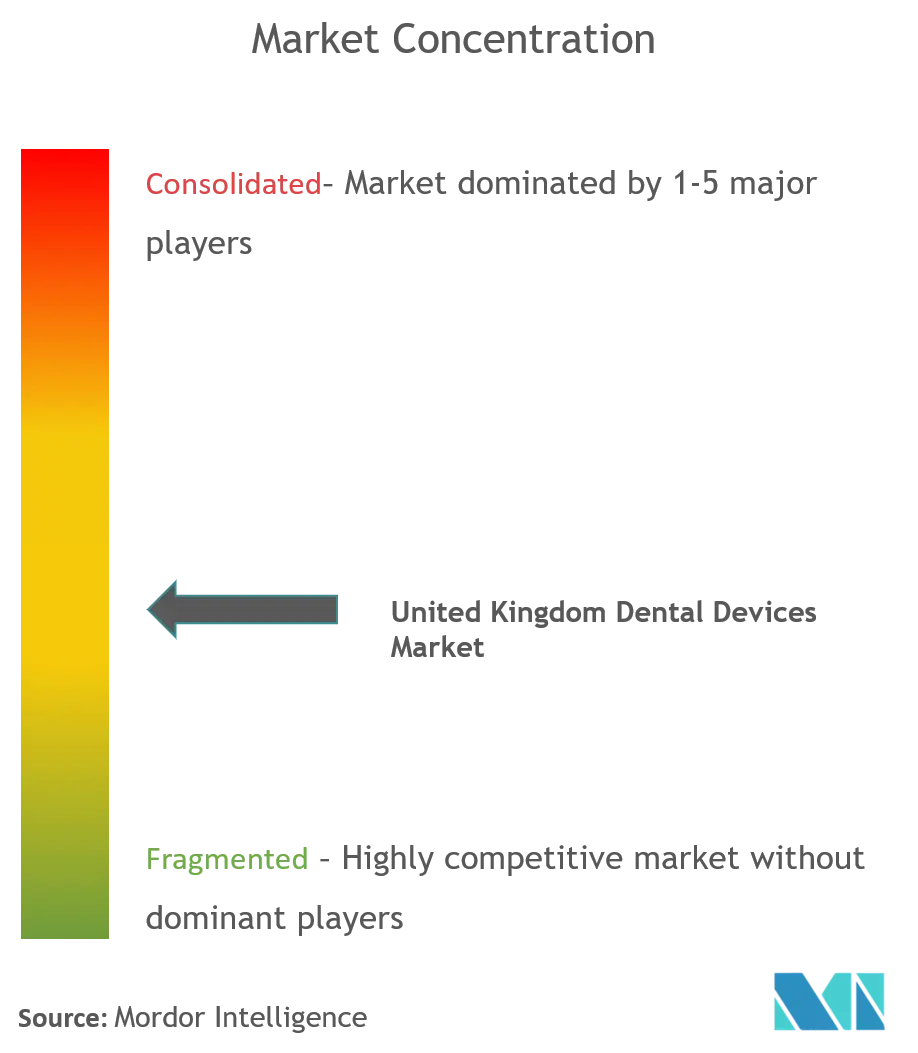

The United Kingdom dental devices market remains fragmented, with 12,583 predominantly independent practices generating continuous consolidation opportunities. Independent buyers accounted for over 80% of 2024 practice transactions as corporate groups trimmed portfolios in response to capital-cost pressures. Sale prices still climbed 8.6% amid a 24% jump in serious buyers, underscoring asset scarcity for profitable mixed practices.

Global manufacturers Dentsply Sirona, Straumann, and Henry Schein anchor the supply side. Dentsply Sirona dedicated roughly 4% of 2024 revenue to R&D, launching Primescan 2 and scaling its DS Core cloud platform across 39 countries. Henry Schein attracted a 12% equity injection from KKR, signalling confidence in vertical integration plays that knit distribution, software, and specialty manufacturing.

The UK Competition and Markets Authority scrutinizes dental roll-up acquisitions, compelling divestments where local competition risks arise. This oversight shapes investment pacing and preserves regional practice diversity, sustaining a competitive sourcing environment for the United Kingdom dental devices market.

United Kingdom Dental Devices Industry Leaders

Envista Holdings Corporation

Institut Straumann AG

Carestream Dental LLC.

Dentsply Sirona

3M Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EMS unveiled its next-generation GBT Machine with automated handpiece recognition at the Dentistry Show

- January 2025: MediMatch completed a management buy-out backed by Queen’s Park Equity to scale its digital-lab network

United Kingdom Dental Devices Market Report Scope

As per the scope of the report, dental devices are the tools that dental professionals use to provide dental treatment, which include various tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures.

The UK dental devices market is segmented by product type (general and diagnostics equipment [dental lasers, radiology equipment, dental chair and equipment, and other general and diagnostics equipment], dental consumables [dental biomaterial, dental implants, crowns and bridges, and other dental consumables], and other dental devices), treatment (orthodontic, endodontic, periodontic, and prosthodontic), and end user (hospitals, clinics, and other end users). The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Product Type (Value)

| Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra Oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair and Equipment | ||

| Therapeutic Equipment | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Equipments | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns and Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Peridontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product Type (Value) | Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra Oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair and Equipment | |||

| Therapeutic Equipment | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Equipments | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns and Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Peridontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current United Kingdom dental devices market size and growth outlook?

The market stands at USD 311.96 million in 2026 and is projected to reach USD 389.13 million by 2031, registering a 4.52% CAGR.

Which product category is expanding fastest?

Dental equipment is rising at 5.18% CAGR, driven by widespread adoption of CAD/CAM units and 3-D printers.

How do NHS workforce shortages affect device investment?

A deficit of 5,500 dental professionals suppresses chair utilization, delaying practice spending on high-tech equipment despite tax incentives.

What regional factors shape demand?

England dominates sales, Scotland posts above-average growth via targeted workforce schemes, while Wales and Northern Ireland focus on contract reform and steady service delivery.

Page last updated on: