Syringe and Needle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

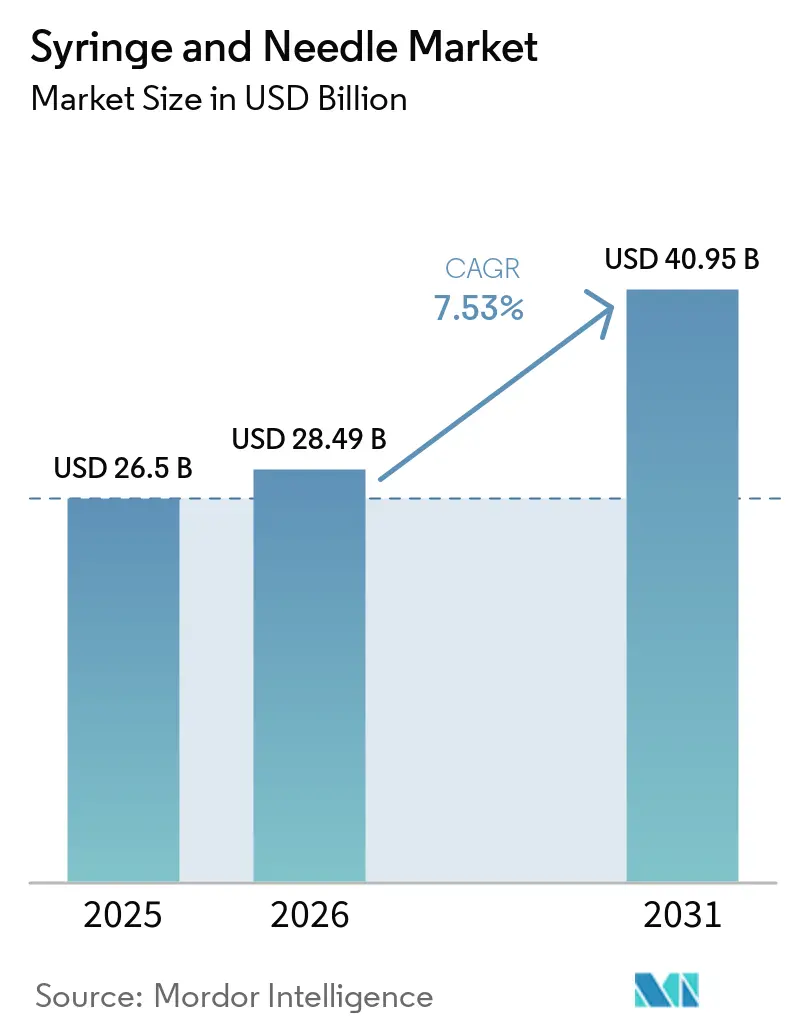

| Market Size (2026) | USD 28.49 Billion |

| Market Size (2031) | USD 40.95 Billion |

| Growth Rate (2026 - 2031) | 7.53% CAGR |

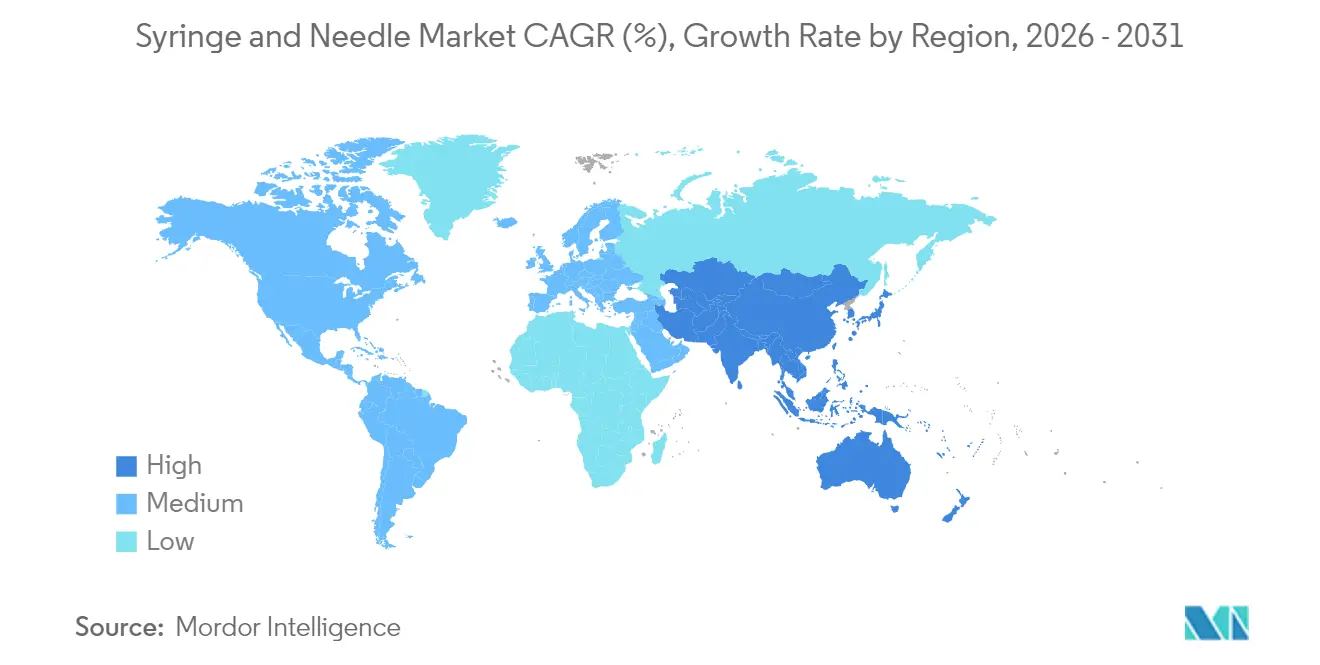

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Syringe and Needle Market Analysis by Mordor Intelligence

The syringe and needle market size is expected to grow from USD 26.50 billion in 2025 to USD 28.49 billion in 2026 and is forecast to reach USD 40.95 billion by 2031 at 7.53% CAGR over 2026-2031. Demand accelerates as GLP-1 biologics, large-volume subcutaneous therapies and year-round adult booster programs lift global injection volumes. Growth also reflects a structural shift toward self-administration and point-of-care diagnostics, both of which elevate the need for user-friendly, safety-engineered devices. Outpatient models now dominate chronic disease management, while hospital purchasing policies increasingly favor high-quality, traceable devices following regulatory warnings on sub-standard imports.

Key Report Takeaways

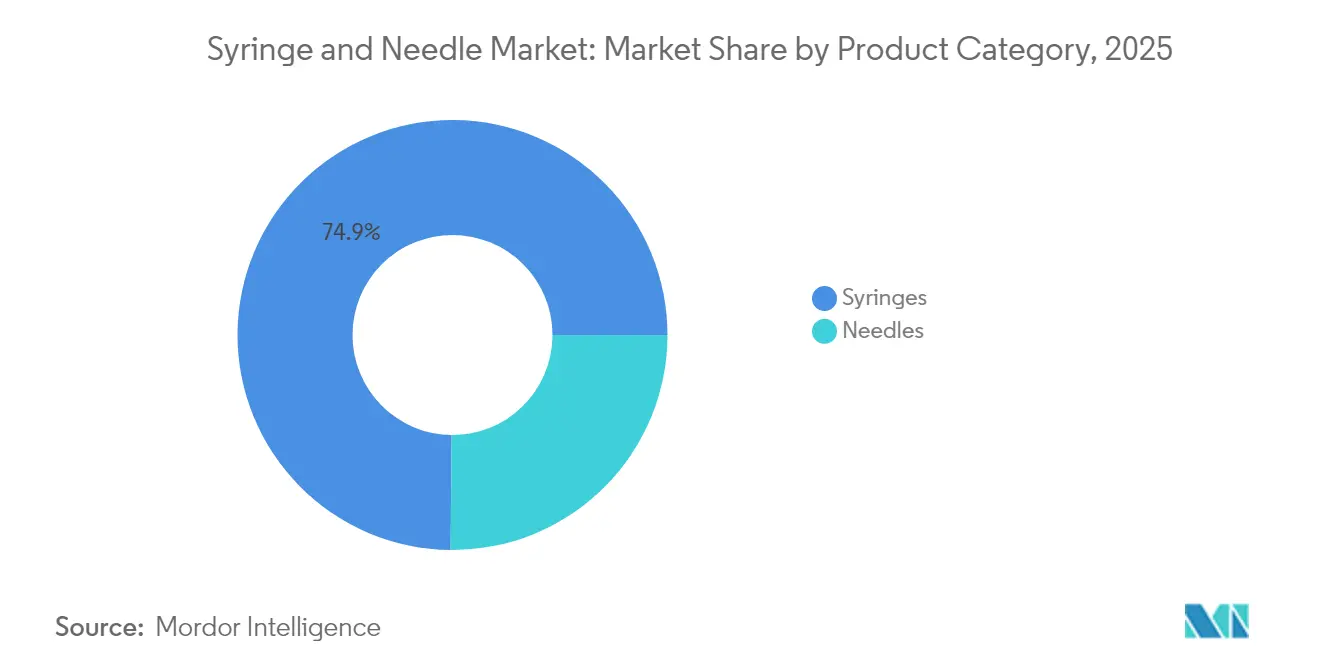

- By product category, syringes led with 74.86% revenue share in 2025; needles record the fastest 8.12% CAGR through 2031.

- By material, plastic held 52.05% of the syringe and needle market share in 2025, while stainless-steel devices expand at an 8.01% CAGR to 2031.

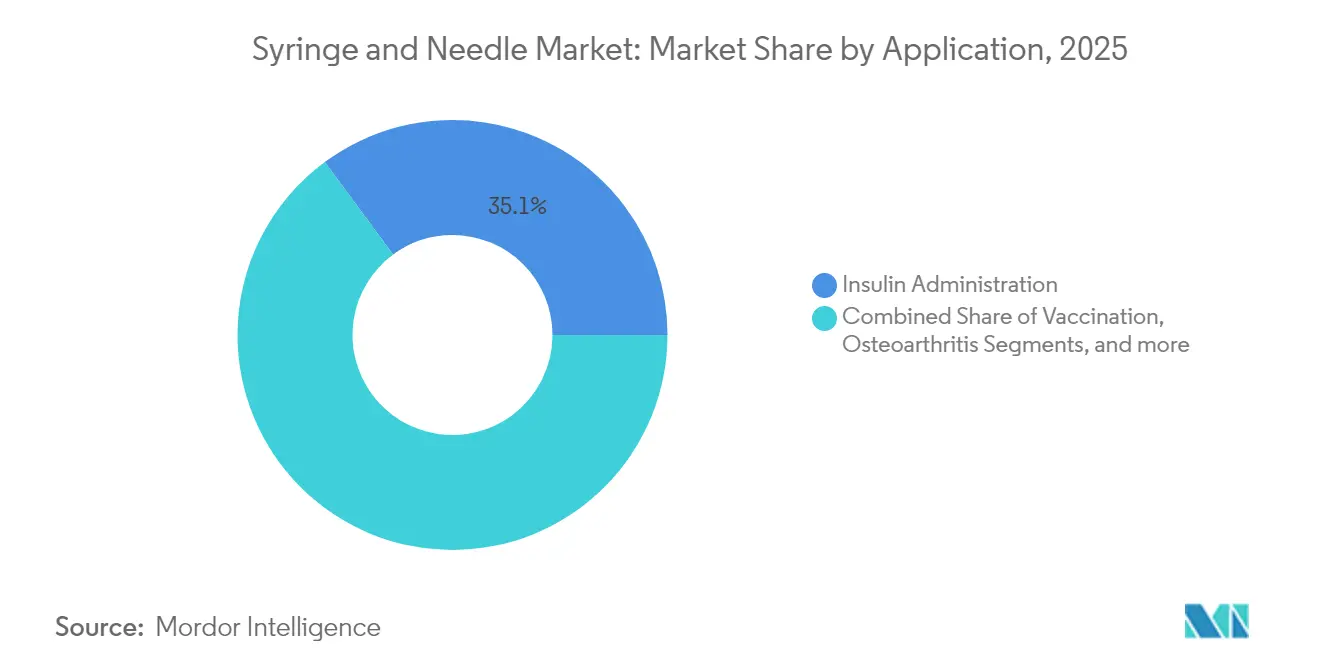

- By application, insulin administration accounted for 35.12% share of the syringe and needle market size in 2025; blood collection is advancing at an 8.27% CAGR to 2031.

- By end user, hospitals and clinics represented 52.74% share in 2025; home-healthcare settings post the strongest 8.31% CAGR.

- By geography, North America led with 39.18% revenue share in 2025; Asia-Pacific is projected to grow at 8.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Syringe and Needle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging GLP-1 & other biologic injectables | +1.8% | North America & Europe lead; global diffusion | Medium term (2-4 years) |

| Mass adult booster immunization programs | +1.2% | Higher compliance in developed markets | Short term (≤2 years) |

| High and rising burden of chronic diseases | +1.5% | APAC fastest growth; global relevance | Long term (≥4 years) |

| Adoption of injectables in out-patient care | +1.1% | Starts in North America & Europe, broadening to APAC | Medium term (2-4 years) |

| Antimicrobial resistance spurring safety | +0.9% | Hospitals worldwide | Medium term (2-4 years) |

| Expansion of point-of-care diagnostic testing | +0.7% | Rural and underserved areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surging GLP-1 & Other Biologic Injectables Pipeline

The shift toward high-viscosity biologics pushes manufacturers to develop syringes that can withstand pressures created by formulations up to 30 mL. BD’s Neopak XtraFlow glass platform integrates thinner-wall cannulas to maintain glide force within patient-acceptable ranges [1]Becton Dickinson, “Neopak XtraFlow Technology Brief,” bd.com. Pharmaceutical firms favor prefilled formats because they improve dose accuracy; as a result, the global prefilled syringe segment is on track to double by 2027. Autoinjector demand also rises, with the category forecast to hit USD 19.67 billion by 2028 on the back of chronic disease self-care. The combination of biologic R&D pipelines and monthly dosing regimens enlarges the syringe and needle market far beyond historical insulin-focused volumes.

Mass Adult Booster Immunization Programs

Influenza and COVID-19 booster uptake among U.S. adults reached 34.7% and 17.9% respectively in November 2024, creating recurring annual demand spikes for injection devices [2]Centers for Disease Control and Prevention, “COVID-19 Vaccination Coverage, United States,” cdc.gov . Advisory bodies now recommend routine RSV vaccination for adults ≥75 years, locking in baseline global syringe volumes each respiratory season. High-throughput immunization settings favor safety-engineered, prefilled devices that cut preparation time and reduce worker exposure to sharps.

High and Rising Burden of Chronic & Infectious Diseases

Rising diabetes and autoimmune incidence anchors steady syringe consumption because many first-line biologics remain parenteral. Home-based care models accelerate as connected monitoring tools let clinicians oversee therapy adherence remotely. This decentralization fuels steady demand for ready-to-administer syringes that minimize preparation errors and simplify patient training.

Increased Adoption of Injectable Drugs for Out-Patient Care

Subcutaneous delivery is displacing intravenous infusions for oncology and immunology regimens, trimming hospital chair time and lowering payer costs. Device makers respond with audible-cue autoinjectors that guide patients through insertion, dose completion and needle retraction. These features enlarge the syringe and needle market as non-clinical users require premium ergonomics and fail-safe design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Needle-stick injuries & cross-contamination | −0.8% | Highest in hospital-dense regions | Short term (≤2 years) |

| Needle-free delivery technology progress | −1.1% | Starts in North America & Europe, spreading globally | Medium term (2-4 years) |

| Extended-producer-responsibility rules | −0.6% | Europe core; expanding to North America & APAC | Medium term (2-4 years) |

| Volatile medical-grade resin prices | −0.4% | APAC manufacturing hubs most exposed | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Cases of Needle-Stick Injuries & Risk of Cross-Contamination

OSHA estimates 600,000 needle-stick injuries occur annually in U.S. hospitals despite mandated safety devices. Outbreaks linked to contaminated syringes underscore patient-to-patient transmission risks, elevating costs tied to post-exposure prophylaxis and litigation [3]Maria Papagianni, "An Outbreak of Serratia marcescens in a Cardiothoracic Surgery Unit Associated with an Infected Solution of Pre-Prepared Syringes," MDPI, mdpi.com.

Availability & Rapid Progress of Needle-Free Delivery Technologies

Needle-free jet injectors and micro-array patches enter mainstream vaccine programs, eliminating sharps waste and easing logistics. BD’s fingertip blood collection device demonstrates comparable accuracy to venous draws while bypassing phlebotomy skill requirements. As manufacturing scales, total cost of ownership narrows versus conventional syringes, limiting future growth in selected segments of the syringe and needle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Needles Drive Innovation Despite Syringe Dominance

Syringes captured 74.86% of the syringe and needle market share in 2025, underlining their indispensability across therapeutic areas. Disposable syringes predominate because infection-control protocols favor single-use devices. Reusable syringes persist only where sterilization controls are economically justified. Needles, though smaller in revenue today, post an 8.12% CAGR to 2031 as hospitals adopt passive safety mechanisms that shield the tip immediately after use.

Technological variety within the needle subsegment fuels this performance. Hypodermic models remain workhorses for vaccination and drug administration, whereas intravenous needles accelerate on the back of outpatient infusion growth. Ophthalmic and dental specialists demand ultra-fine gauges for precision procedures, creating niche premium-price categories. Manufacturers overlay RFID tags on high-value syringes, enabling real-time inventory visibility for hospital pharmacies and reducing wastage from expired stock.

By Material: Plastic Dominance Faces Stainless-Steel Resurgence

Plastic retained 52.05% share of the syringe and needle market in 2025 as polypropylene, polyethylene and COC blends provided low-cost moldability and gamma-sterilization compatibility. Glass continues to rule premium prefilled formats because it minimizes drug-container interaction for biologics with high surface sensitivity. Yet stainless-steel barrels re-enter the mainstream, growing at 8.01% CAGR through 2031, buoyed by the need for rugged delivery systems that handle viscous GLP-1 formulations without barrel flex. Raw-material inflation and resin supply shocks illustrate why device firms diversify material portfolios and on-shore strategic inventory.

Glass investments reinforce confidence: Gerresheimer allocated EUR 100 million to scale syringe capacity at its Skopje plant, while Nipro upgraded German lines for dual-flange (D2F) formats that pair seamlessly with autoinjectors. Such projects broaden geographical redundancy, a priority after pandemic-era freight bottlenecks.

By Application: Blood Collection Surges Past Traditional Leaders

Insulin administration remained the largest single application at 35.12% of the syringe and needle market in 2025, reflecting the diabetes burden and expanded GLP-1 usage for metabolic syndrome. Blood collection, however, races ahead at an 8.27% CAGR as hospitals and community labs ramp post-pandemic diagnostics. Demand for capillary-micro-sampling devices reduces patient pain while delivering lab-grade accuracy, positioning the syringe and needle market size for this application at USD 4.19 billion by 2031.

Vaccination retains steady momentum through adult booster programs, while osteoarthritis injections and intravitreal ophthalmic therapies contribute incremental share. Advanced silicone-free barrel coatings mitigate particle generation that can undermine biologic stability during chronic retinal treatments. Cross-category demand ensures balanced growth even as specific segments plateau.

By End User: Home Healthcare Transforms Care Delivery

Hospitals and clinics commanded 52.74% revenue in 2025, yet home-healthcare posts the briskest 8.31% CAGR. The trend reflects payers’ drive to shift infusion and biologic maintenance therapy to living rooms, reducing overhead and infection risk. Ready-to-administer devices shorten nurse visit times, while connected autoinjectors upload adherence data to cloud dashboards, enabling proactive intervention.

Ambulatory surgery centers also benefit from device miniaturization that supports same-day discharge pain control. Diagnostic labs sustain steady uptake as point-of-care platforms multiply in rural clinics, each requiring single-use safety needles to prevent cross-patient contamination.

Geography Analysis

North America led the syringe and needle market with 39.18% share in 2025. Domestic producers capitalized on FDA safety communications that curtailed certain Chinese imports, elevating demand for compliant, traceable alternatives. BD’s USD 10 million expansion added 40% safety-engineered syringe capacity and 50% conventional syringe output across Connecticut and Nebraska, fortifying regional supply resilience.

Europe remained a stronghold owing to stringent quality norms and aging populations that boost chronic-care injections. Investments such as Gerresheimer’s glass line scale-up and Nipro’s D2F upgrades underscore the region’s role in premium biologic delivery solutions. Sustainability rules, especially extended-producer responsibility mandates, spur innovation in recyclable components and low-waste packaging.

Asia-Pacific is the fastest-growing zone at 8.43% CAGR. India aims for a USD 50 billion medical-device economy by 2025 and has aligned domestic regulations with ISO standards to attract foreign OEM partnerships. Chinese manufacturers pivot from volume to value, investing in class-III device certification and building joint ventures in Southeast Asia to diversify market exposure. Large patient pools needing chronic therapy, coupled with public-hospital modernization, sustain a rising baseline for syringe and needle market demand across the region.

Competitive Landscape

The competitive field is fragmented. Becton Dickinson remains the anchor player, leveraging vertical integration and domestic capacity to buffer clients against supply disruptions. Its 2024 investment strategy coupled infrastructure upgrades with R&D on silicone-free and RFID-enabled syringes aimed at biologic innovators. Terumo and Smiths Medical emphasize pre-filled safety systems, while Gerresheimer and Schott focus on high-precision glass barrels that withstand high-viscosity fills.

Strategic collaboration defines current competition. BD partnered with Ypsomed to pair XtraFlow glass barrels with autoinjector platforms optimized for 1-mL-plus doses, locking in dual-sourcing assurances for pharma clients. Smaller disruptors target needle-free niches and biodegradable resin formulations, offering hospitals cost avoidance on sharps disposal.

Regulatory headwinds also reshape share. FDA warning letters to low-cost importers create white-space for quality-centric vendors, while the EU’s Medical Device Regulation raises compliance thresholds that smaller manufacturers struggle to meet. Market participants thus differentiate through certified quality management and lifecycle logistics support.

Syringe and Needle Industry Leaders

-

B. Braun Melsungen AG

-

Terumo Medical Corporation

-

Smiths Medical, Inc

-

Becton, Dickinson and Company

-

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BD expanded syringe and needle production capacity in Nebraska and Connecticut facilities to meet rising U.S. demand.

- January 2025: BD announced intent to separate its Biosciences and Diagnostic Solutions divisions, sharpening focus on core medication-delivery technologies.

- June 2024: Cardinal Health expanded a recall of Monoject syringes after detecting compatibility issues.

- April 2024: Cardinal Health received an FDA warning for marketing unapproved Luer-lock and enteral feeding syringes.

Global Syringe and Needle Market Report Scope

As per the scope of this report, the syringe is a device used by medical professionals to transfer liquids into or out of the body. A needle is a thin, hollow tube with a sharp tip that contains a small opening at the pointed end, used to transfer fluids from the syringe. The Syringes and Needles Market is segmented by Type (Syringes (Sterilizable/Reusable Syringes and Disposable Syringes ) and Needles(Hypodermic, Intravenous, Intramuscular, and Others)), Application (Syringes (Insulin administration, Botox, Osteoarthritis, Human Growth Hormone, and Other Applications) and Needles (Blood Collection, Ophthalmic Procedures, Dental, and Other Applications)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Syringes | Disposable |

| Reusable | |

| Needles | Hypodermic |

| Intravenous | |

| Intramuscular | |

| Others |

| Plastic |

| Glass |

| Stainless Steel |

| Insulin Administration |

| Vaccination |

| Osteoarthritis |

| Botox |

| Blood Collection |

| Ophthalmic Procedures |

| Dental |

| Other Applications |

| Hospitals and Clinics |

| Ambulatory Surgery Centers |

| Diagnostic Laboratories |

| Home Healthcare Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Category | Syringes | Disposable |

| Reusable | ||

| Needles | Hypodermic | |

| Intravenous | ||

| Intramuscular | ||

| Others | ||

| By Material | Plastic | |

| Glass | ||

| Stainless Steel | ||

| By Application | Insulin Administration | |

| Vaccination | ||

| Osteoarthritis | ||

| Botox | ||

| Blood Collection | ||

| Ophthalmic Procedures | ||

| Dental | ||

| Other Applications | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgery Centers | ||

| Diagnostic Laboratories | ||

| Home Healthcare Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the syringe and needle market?

The global syringe and needle market is valued at USD 28.49 billion in 2026 and is forecast to grow at a 7.53% CAGR to USD 40.95 billion by 2031.

Which product category is growing the fastest?

Needles exhibit the fastest growth, expanding at an 8.12% CAGR through 2031 as hospitals adopt safety-engineered and specialty designs.

Why are stainless-steel syringes gaining traction?

Stainless-steel barrels better handle high-viscosity biologics such as GLP-1 formulations, driving an 8.01% CAGR for the material segment.

Which region shows the highest growth potential?

Asia-Pacific leads in growth with an 8.43% CAGR due to expanding healthcare infrastructure and large patient pools requiring chronic injections.

How are regulatory actions affecting competitive dynamics?

FDA warnings against non-compliant imports and stringent EU regulations shift market share toward quality-certified manufacturers with robust traceability systems.

What technological trends will shape future demand?

Prefilled syringes, RFID tagging, and connected autoinjectors will dominate as self-administration and supply-chain transparency become standard buyer requirements.

Page last updated on: