Dental Mirrors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

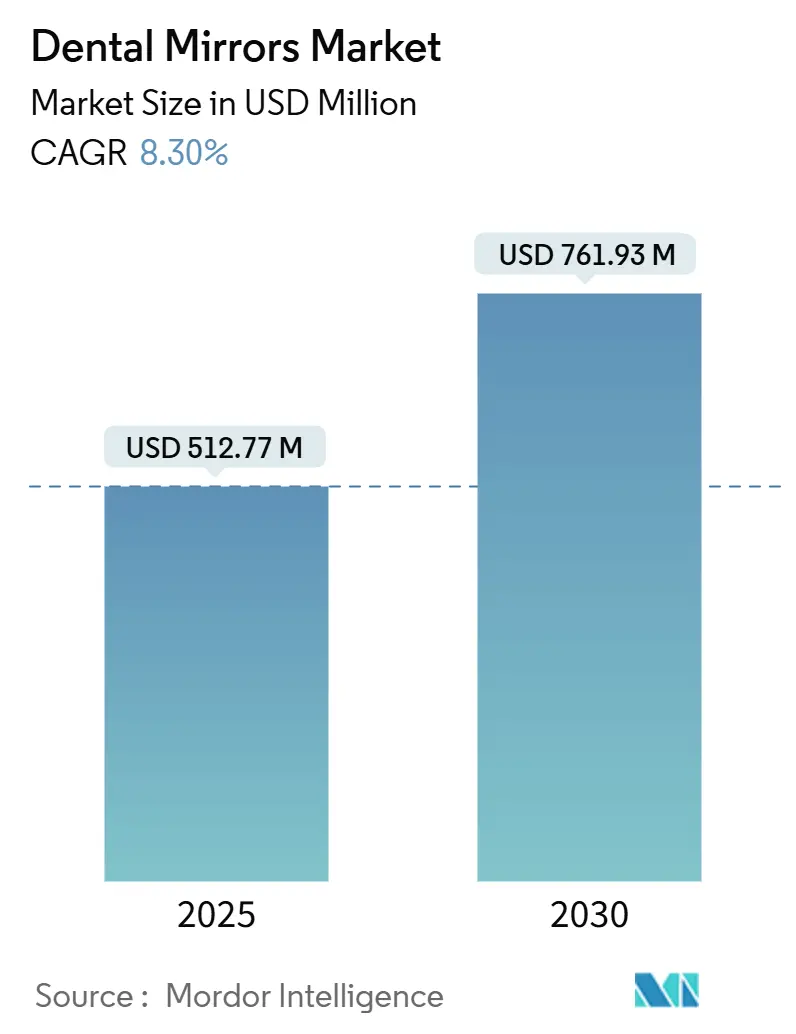

| Market Size (2025) | USD 512.77 Million |

| Market Size (2030) | USD 761.93 Million |

| Growth Rate (2025 - 2030) | 8.30% CAGR |

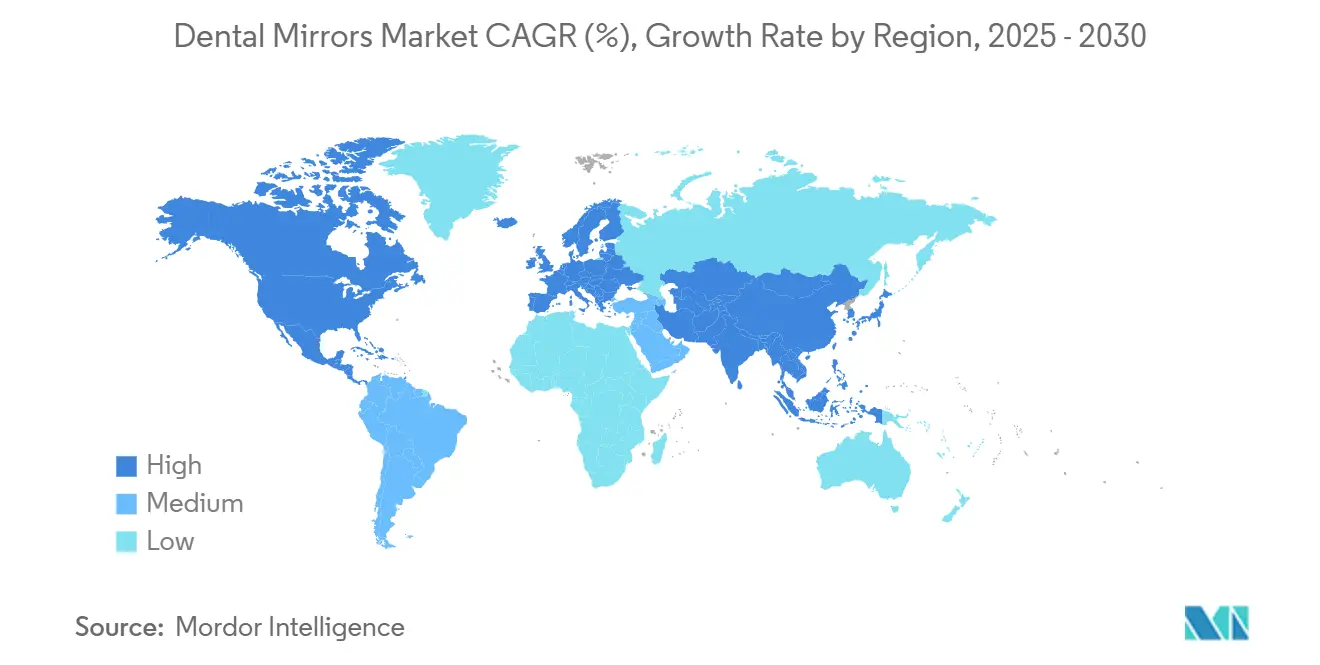

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

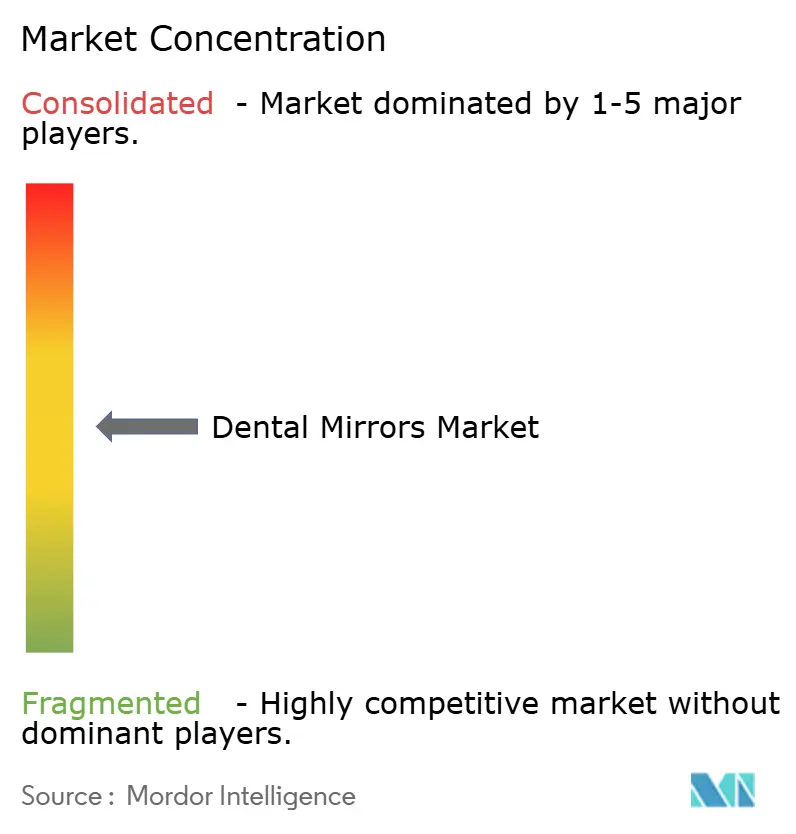

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Mirrors Market Analysis by Mordor Intelligence

The dental mirrors market size stands at USD 512.77 million in 2025 and is forecast to reach USD 761.93 million by 2030, reflecting an 8.30% CAGR. This sustained expansion is anchored in the indispensable role mirrors play across virtually every diagnostic and restorative procedure, a dynamic reinforced by global oral-disease prevalence and stricter infection-control protocols. The dental mirrors market benefits from rapidly rising procedure volumes, a surge in cosmetic dentistry, and steady private-practice expansion. At the same time, integrated digital/smart mirrors signal a future in which optical clarity converges with imaging connectivity. Competitive rivalry remains moderate as established suppliers protect share through product refresh cycles, material innovations, and selective acquisitions that broaden manufacturing depth. Regionally, North America retains leadership through high treatment penetration, yet Asia Pacific delivers the most compelling growth run-rate, powered by middle-class consumption and clinic build-out programs.

Key Report Takeaways

- By product type, reusable dental mirrors led with 61.4% of the Dental Mirror market share in 2024; integrated digital/smart mirrors are projected to expand at a 13.4% CAGR through 2030.

- By material, stainless-steel accounted for 46.8% of the Dental Mirror market size in 2024, while rhodium-coated variants are expected to grow at an 11.2% CAGR to 2030.

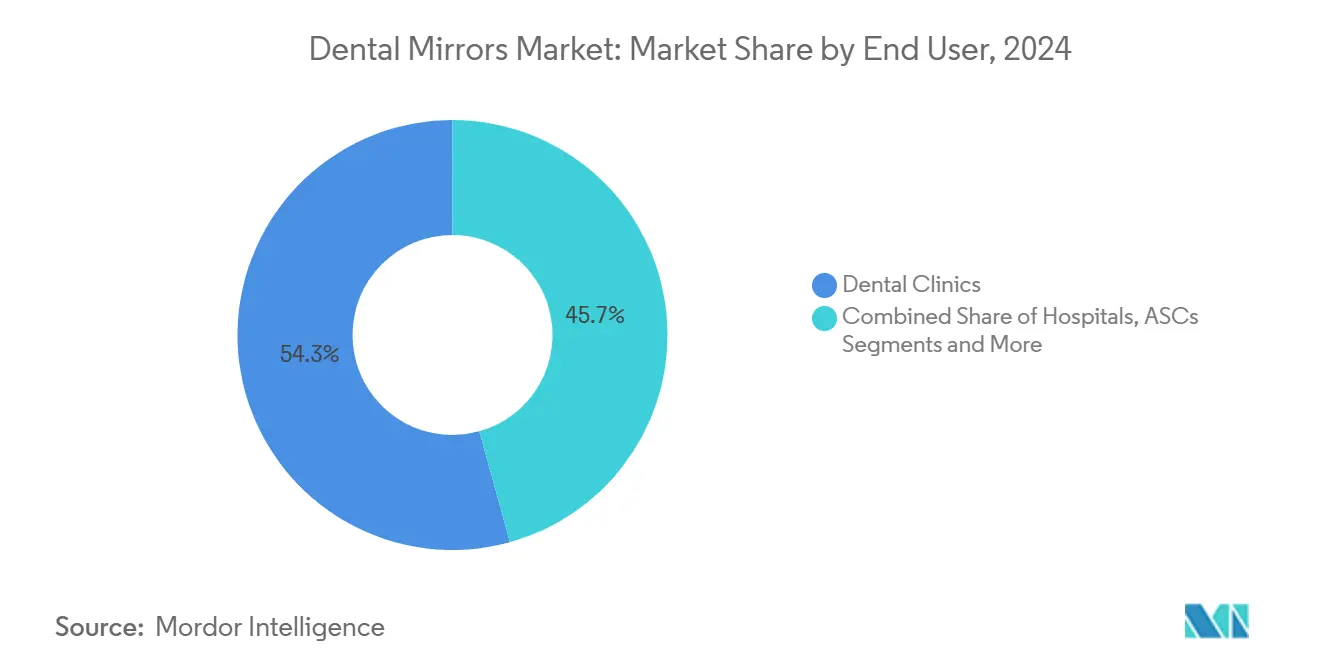

- By end user, dental clinics held 54.3% of the Dental Mirror market size in 2024; ambulatory surgical centers are advancing at a 9.1% CAGR through 2030.

- By geography, North America commanded 32.4% revenue share of the Dental Mirror market in 2024, whereas the Asia Pacific is forecast to deliver a 7.2% CAGR to 2030.

Global Dental Mirrors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Dental Caries & Periodontal Disease | +1.20% | Global, with highest burden in Asia and low-middle SDI regions | Long term (≥ 4 years) |

| Growth In Cosmetic Dentistry Procedures | +1.00% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Expansion Of Private Dental Clinics & Practitioner Base | +0.80% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Infection-Control Focus Boosting Single-Use Mirrors | +0.70% | Global, with regulatory emphasis in developed markets | Short term (≤ 2 years) |

| AR-Assisted Training Requiring High-Reflectivity Mirrors | +0.50% | North America & EU, early adoption in urban APAC | Long term (≥ 4 years) |

| Demand For Rhodium-Coated Mirrors For Digital Impressions | +0.40% | Global, concentrated in technologically advanced practices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries & Periodontal Disease

Global oral conditions afflict billions, creating a dependable stream of examinations that keep the dental mirrors market entrenched in day-to-day practice.[1]World Health Organization, “Oral Health,” who.int Approximately 2.37 billion people suffered from untreated caries and 951.3 million faced periodontal disorders in 2024, ensuring mirrors remain fundamental for diagnostics throughout the forecast window.[2]GBD 2021 Oral Disorders Collaborators, “Trends in the Global Burden of Oral Conditions 1990-2021,” lancet.com World Health Organization reduction targets heighten short-term screening activity, while demographic aging and sugary-diet penetration extend long-term demand. Asia’s particularly high burden, coupled with expanding public-health budgets, signals a structural growth pillar. Uniform diagnostic guidelines promote standardized mirror use, securing a resilient baseline for manufacturers.

Growth in Cosmetic Dentistry Procedures

Elective aesthetic treatments propel the premium tier of the dental mirrors market as practitioners rely on enhanced optics to evaluate veneer margins, shade matching, and smile symmetry. The United States therapeutic-esthetic segment continues a multibillion-dollar climb, buoyed by aging cohorts seeking restorative and cosmetic corrections, thereby lifting demand for distortion-free rhodium mirrors that excel under intense operatory lighting. Social-media influence amplifies patient expectations, translating to higher procedural counts and recurring mirror replacements in both consultation and follow-up phases. Europe and mature Asia Pacific clinics similarly pivot toward cosmetic menus, reinforcing global mirror volume.

Expansion of Private Dental Clinics & Practitioner Base

Rapid clinic proliferation in China, India, and Southeast Asia introduces thousands of new chairside operators annually, each needing full mirror inventories. Group practice models and dental service organizations institutionalize bulk procurement, favoring suppliers with stable production and standardization prowess. International manufacturers establish regional warehouses and training centers to lock in early loyalty, strengthening the dental mirrors market’s foothold in emerging metros. Regulatory pushes for accreditation in developing nations further elevate instrument-quality thresholds, benefiting premium brands that comply with FDA and ISO standards.

Infection-Control Focus Boosting Single-Use Mirrors

Post-pandemic vigilance accelerates the adoption of disposable variants that eradicate cross-contamination risk. U.S. CDC guidelines categorically prohibit reprocessing of single-use devices, compelling practices to stock a steady flow of cost-efficient plastic or polymer mirrors for high-risk procedures. Labor and sterilizer depreciation analyses increasingly reveal economic parity between reusable-cycle costs and disposables, especially in ambulatory surgical centers where turnover is rapid. Manufacturers responding with recyclable or bioplastic disposables align with both compliance and sustainability agendas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure from low-cost local manufacturers | −0.7% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Substitution by intraoral scanners & camera systems | −0.5% | North America & EU core, expanding into tech-forward APAC | Medium term (2-4 years) |

| Ergonomic injury concerns driving alternative tools | −0.4% | North America & Europe | Medium term (2-4 years) |

| Environmental limits on chromium-plated instruments | −0.3% | EU core, spreading to eco-conscious markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Low-Cost Local Manufacturers

Asian producers leverage wage advantages and lighter regulatory oversight to undercut premium brands, challenging margin defense in the dental mirrors market. Stainless-steel reusable mirrors face commoditization as cost-focused buyers negotiate bulk discounts. To maintain positioning, global incumbents automate plants and add antibacterial coatings that justify pricing differentials. The squeeze is pronounced in publicly funded clinics where purchasing committees impose strict ceiling bids.

Substitution by Intraoral Scanners & Camera Systems

High-definition cameras increasingly capture occlusal surfaces once viewed solely through mirrors, reducing reliance on select diagnostic steps. Early evidence shows digital impressions trimming chair time and enhancing lab communication, encouraging affluent practices to pivot. Nonetheless, mirrors remain indispensable in emergency, hygiene, and basic restorative contexts where direct visualization is fastest. The dental mirrors market, therefore, faces partial, not wholesale, substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Integration Drives Innovation

Reusable mirrors dominate the dental mirrors market with 61.4% revenue in 2024, a position anchored in affordability and universal clinical compatibility. Their familiarity and broad sterilization acceptance keep turnover brisk, particularly in multi-chair clinics. Disposable variants capture growing share as infection-control rules tighten; supply contracts with ambulatory centers underpin volume growth. Integrated digital/smart mirrors, though holding a modest base, post a 13.4% CAGR as LED lighting, magnification, and Bluetooth image transfer converge with teledentistry platforms. Manufacturers target premium pricing tiers by bundling mirrors within digital workflow kits, a strategy that further elevates the dental mirrors market.

Second-generation smart mirrors debut in 2025 with on-board sensors measuring fogging and surface temperature, signaling a shift toward data-rich operatory tools. Double-sided and front-surface designs retain niche importance in orthodontics and cosmetic restorations where angle flexibility and true-reflection accuracy are vital. Across categories, FDA Class I clearance remains a low regulatory hurdle, yet ISO sterilization documentation drives tangible differentiation, reinforcing brand reputations inside academic purchasing committees.

By Material: Advanced Coatings Command Premium

Stainless-steel mirrors held 46.8% of the dental mirrors market size in 2024, their dominance rooted in durability and cost-value alignment. They remain the preferred option for routine examinations and are favored in government tenders. Rhodium-coated models, by contrast, advance at an 11.2% CAGR on the strength of heightened brightness, scratch immunity, and compatibility with intraoral photography. As cosmetic and digital workflows expand, rhodium’s performance premium gains clinical justification, spurring volumes in urban Asia and private U.S. practices. Titanium variants, lighter and inherently biocompatible, appear in surgical and pediatric kits where reduced operator fatigue matters.

Advanced antibacterial coatings—such as titanium nitride layers that cut bacterial adhesion by nearly 90%—emerge as differentiators in high-risk procedural suites, pointing to a future where antimicrobial efficacy becomes a purchase criterion.[3]Yongcun Bao et al., “Corrosion Resistance and Antibacterial Activity of Ti-N-O Coatings,” sciencedirect.com Polymer mirrors fill the single-use niche, increasingly sourced through biodegradable blends that meet eco-procurement policies in Europe. Ongoing R&D into plasma-oxidized surfaces suggests a pipeline of mirrors able to maintain sterility over longer intervals, reinforcing the premiumization arc within the dental mirrors market.

By End User: Clinics Lead Adoption

Dental clinics generated 54.3% of global revenues in 2024, reflecting their role as frontline care providers; routine hygiene, restorative, and cosmetic workflows collectively draw heavy mirror consumption. Multi-location groups standardize procurement, often signing multi-year supply frameworks with top manufacturers. Hospitals, though smaller in share, maintain steady purchasing for emergency oral surgery suites and integrated head-and-neck service lines. Ambulatory surgical centers outpace all others at a 9.1% CAGR, propelled by procedural migration from inpatient to outpatient settings and strict single-use mandates that double mirror volume per case.

Academic and research institutes sustain demand for premium, true-reflection mirrors used in simulation labs and trials assessing novel coatings. Residency programs further elevate consumption as each cohort requires complete instrument sets. Cross-discipline integration under health-system umbrellas accelerates volume buying, reinforcing the dental mirrors market’s resilience even when elective demand moderates.

Geography Analysis

North America led the dental mirrors market with 32.4% revenue in 2024. Intense insurance penetration supports twice-yearly hygiene visits, each requiring fresh examination mirrors. Heightened infection-control scrutiny post-COVID drives clinics toward rhodium and single-use polymer options. U.S. practices also invest in smart mirrors that interface with imaging software to streamline documentation. Canada’s provincial health benefits supply baseline demand; private offices layer premium volume on top, especially in cosmetic hubs like Toronto and Vancouver.

Asia Pacific posts the steepest curve, delivering a 7.2% CAGR through 2030. China’s hospital and private-clinic build-outs create thousands of new operatories annually, while India’s dental-college system graduates a vast practitioner cohort that immediately buys entry-level kits. Japanese clinics, known for early tech uptake, adopt high-reflectivity rhodium mirrors to optimize scanner workflows. South Korea’s medical-tourism ecosystem amplifies demand for premium optics. Regional manufacturing clusters in Shenzhen and Mumbai integrate vertically, delivering cost-competitive yet standards-compliant products that feed both domestic and export streams, further fortifying the dental mirrors market.

Europe’s mature base grows steadily, undergirded by state reimbursement that guarantees preventive checkups. German and Swiss brands sustain export reputations for precision engineering, while EU environmental directives phase down chrome plating, nudging demand toward recyclable polymers and titanium. Southern Europe’s cosmetic surge bolsters rhodium mirror sales, while Nordic tenders emphasize sustainability, favoring suppliers with life-cycle assessments. Eastern Europe, catching up in clinic density, extends geographic upside for mid-priced reusable mirrors.

Competitive Landscape

The dental mirrors market remains moderately concentrated. HuFriedyGroup, Dentsply Sirona, and KaVo Kerr leverage long-standing catalogs, multi-channel distribution, and continuing-education initiatives that deepen brand lock-in. HuFriedyGroup’s 2024 acquisition of SS White Dental broadened its manufacturing platform and strengthened specialty instrument depth. Dentsply Sirona expanded its Essential Dental Solutions unit, capturing stocking orders tied to new product launches. KaVo Kerr channels mirror innovation through its DEXIS imaging arm, emphasizing smart-mirror integration with intraoral cameras slated for 2025 release.

Second-tier players—LM-Dental, Carl Martin, and Brasseler—compete on craftsmanship and niche innovations such as ergonomic handles that reduce wrist strain. Contract manufacturers in India and Pakistan supply private-label stainless-steel mirrors to distributors like Henry Schein, intensifying price competition in basic categories. FDA quality-system citations, such as the 2024 warning to Integra LifeSciences, illustrate regulatory hurdles newcomers must clear. Despite incremental substitution threats, mirrors remain a foundational consumable, keeping the sector attractive for investors, as evidenced by KKR’s USD 4.1 billion minority stake in Henry Schein in 2025.

Dental Mirrors Industry Leaders

HuFriedyGroup

KaVo Dental GmbH

Integra LifeSciences

LM-Dental

Carl Martin GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Henry Schein announced a USD 4.1 billion strategic investment by KKR, with proceeds earmarked for accelerated product expansion and digital-capability enhancement.

- December 2024: The FDA issued a warning letter to Integra LifeSciences outlining device manufacturing shortcomings that must be rectified to maintain market access.

- October 2024: HuFriedyGroup acquired SS White Dental, adding carbide and diamond burs that complement its mirror portfolio while expanding global manufacturing reach.

Global Dental Mirrors Market Report Scope

| Reusable Dental Mirrors |

| Disposable Dental Mirrors |

| Front-Surface Mirrors |

| Double-Sided Mirrors |

| Integrated Digital/Smart Mirrors |

| Stainless-Steel |

| Rhodium-Coated |

| Titanium |

| Polymer/Plastic |

| Other Alloys |

| Hospitals |

| Dental Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Reusable Dental Mirrors | |

| Disposable Dental Mirrors | ||

| Front-Surface Mirrors | ||

| Double-Sided Mirrors | ||

| Integrated Digital/Smart Mirrors | ||

| By Material | Stainless-Steel | |

| Rhodium-Coated | ||

| Titanium | ||

| Polymer/Plastic | ||

| Other Alloys | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Dental Mirror market in 2025?

The Dental Mirror market size is USD 512.77 million in 2025.

Which product category is growing fastest?

Integrated digital/smart mirrors lead with a projected 13.4% CAGR to 2030.

Why are rhodium-coated mirrors gaining share?

They offer superior reflectivity and scratch resistance, making them ideal for digital workflows and cosmetic procedures.

What region shows the strongest growth outlook?

Asia Pacific posts the highest regional CAGR at 7.2% through 2030, fueled by clinic expansion and rising disposable income.

How is infection control shaping demand?

Stricter CDC guidelines are accelerating adoption of single-use disposable mirrors, especially in outpatient and high-risk settings.

Who are the main industry leaders?

HuFriedyGroup, Dentsply Sirona, and KaVo Kerr dominate through broad portfolios, global distribution, and ongoing product innovation.

Page last updated on: