Dental Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

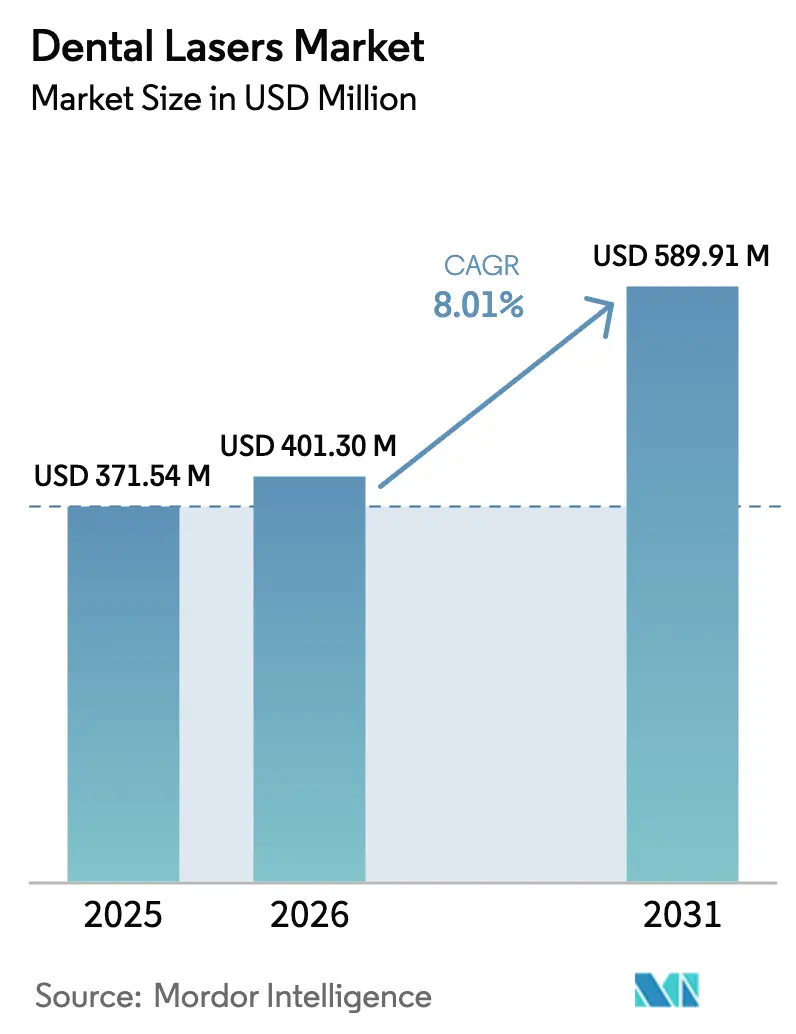

| Market Size (2026) | USD 401.30 Million |

| Market Size (2031) | USD 589.91 Million |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Lasers Market Analysis by Mordor Intelligence

The dental lasers market size is expected to grow from USD 371.54 million in 2025 to USD 401.30 million in 2026 and is forecast to reach USD 589.91 million by 2031 at 8.01% CAGR over 2026-2031. Momentum stems from consolidation among dental service organizations (DSOs), which deploy capital equipment across large practice footprints to standardize minimally invasive care and raise procedure throughput. Elevated periodontal and peri-implant disease prevalence, currently affecting about 19% of adults worldwide, increases the volume of cases that benefit from laser-assisted treatment. Lasers also align with the profession’s shift toward tissue-preserving techniques, which shorten chair time and recovery, thereby increasing patient acceptance. Ongoing product refinements such as shorter pulse widths and dual-wavelength consoles are broadening the range of clinical indications, while chair-side CAD/CAM compatibility positions lasers as integral components of same-day restorative workflows. Although upfront costs and limited reimbursement temper uptake among solo practices, DSOs and hospitals continue to build installed bases, tilting the competitive landscape toward larger, well-financed operators.

Key Report Takeaways

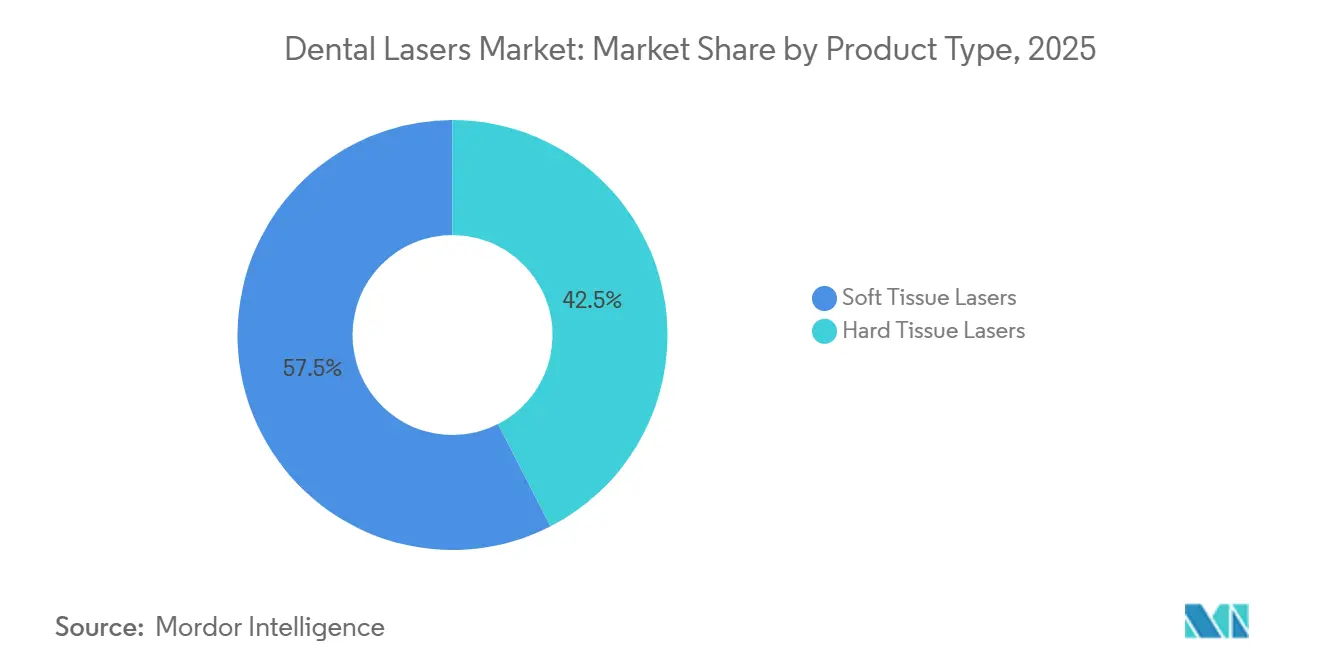

- By product type, soft tissue lasers led with 57.54% revenue share in 2025; hard-tissue-capable systems are projected to expand at a 10.43% CAGR through 2031.

- By 2025, diode platforms are expected to hold 36.54% of the dental lasers market share, while erbium:YAG units are anticipated to post the fastest growth, with a 10.65% CAGR from 2026 to 2031.

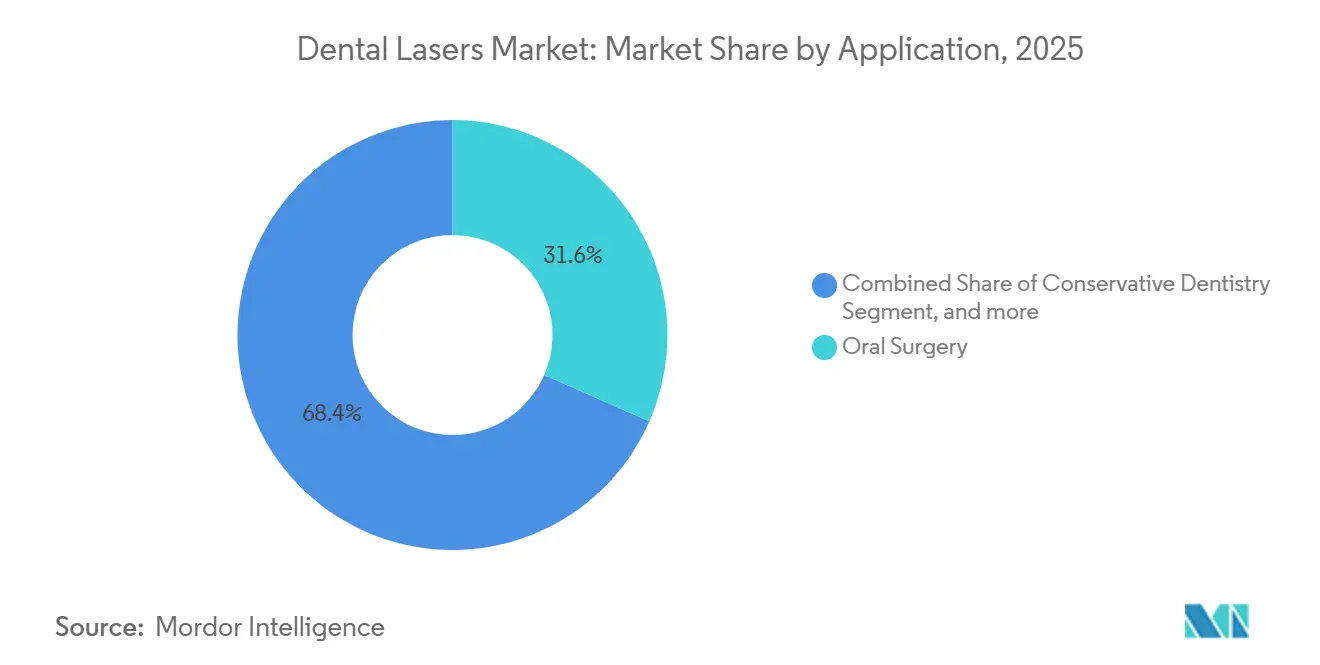

- By application, oral surgery accounted for 31.56% of the dental lasers market size in 2025, whereas implantology is poised to register an 11.67% CAGR from 2026 to 2031.

- By end user, clinics and DSOs accounted for 55.67% of demand in 2025; however, hospitals are expected to record an 11.45% CAGR through 2031.

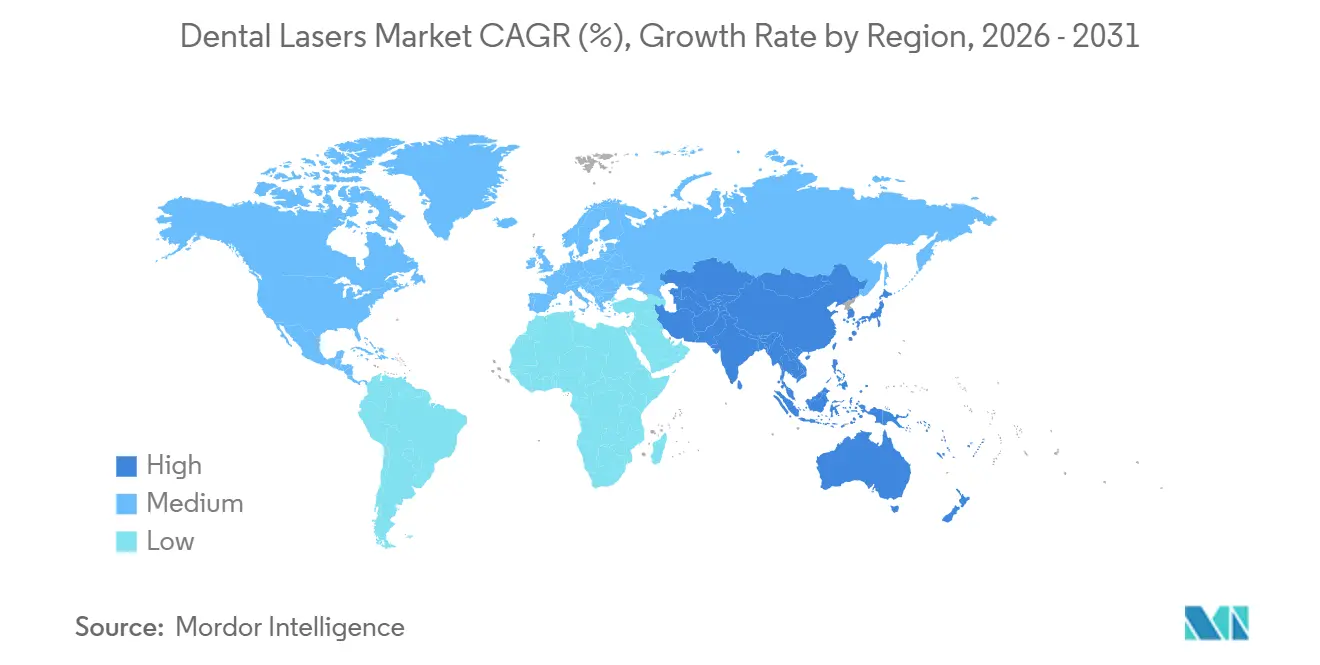

- By geography, North America retained 40.34% share in 2025; Asia-Pacific is forecast to advance at a 9.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Lasers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Periodontal & Peri-Implant Diseases | +1.8% | Global, acute in North America, Europe, aging APAC | Medium term (2-4 years) |

| Growing Adoption of Minimally Invasive Dentistry | +1.5% | North America, EU, expanding urban APAC | Short term (≤ 2 years) |

| Rapid Technological Advances (Short-Pulse, Dual-Wavelength) | +1.3% | Early adoption in Germany, United States, Japan | Medium term (2-4 years) |

| Expansion of Chair-Side CAD/CAM Compatibility | +0.9% | North America, Western Europe, South Korea | Medium term (2-4 years) |

| Increasing DSO-Led Investments in High-ROI Equipment | +1.2% | Core in North America, spillover to UK, Australia | Short term (≤ 2 years) |

| Emerging Dental Tourism Clusters | +0.7% | Mexico, Thailand, Turkey, Costa Rica, UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Periodontal & Peri-Implant Diseases

Severe periodontitis afflicts roughly 1 billion adults and climbs sharply after age 50[1]World Health Organization, “Global Oral Health Status Report,” who.int. Peri-implantitis adds a recurrent clinical burden, as conventional debridement risks scratching titanium. Erbium:YAG lasers vaporize biofilm while sparing implant surfaces, and diode units coagulate inflamed soft tissue. Evidence-based protocols such as laser-assisted new attachment procedures gain traction because they avoid flap surgery and encourage faster healing. Aging populations in the United States, Germany, and Japan ensure a steady influx of complex periodontal cases that are well-suited for laser therapy. Practices adopting these protocols report higher treatment acceptance because patients associate lasers with lower pain and quicker recovery.

Growing Adoption of Minimally Invasive Dentistry

Patient demand for gentle care accelerates the shift away from scalpels and burs. Soft tissue lasers complete gingivectomy and frenectomy with limited bleeding, enabling same-day discharge. Hard-tissue erbium:YAG systems can excise caries while preserving enamel, thereby reducing postoperative sensitivity. DSOs capitalize on this preference by marketing laser procedures as premium offerings and implementing standardized protocols across their extensive networks. In dense urban markets, the ability to advertise no-shot cavity removal differentiates practices and drives elective case volume. The trend integrates seamlessly with digital scanning and on-site milling, enabling practitioners to complete restorations in a single visit.

Rapid Technological Advances (Short-Pulse, Dual-Wavelength Systems)

Manufacturers now bundle short-pulse erbium:YAG and neodymium:YAG beams in a single console, covering both hard-tissue ablation and soft-tissue coagulation without requiring the use of different handpieces. Pulse durations under 100 microseconds restrain heat diffusion, protecting the pulp during enamel cutting. Manufacturers add photobiomodulation settings that use low-level output to accelerate wound closure and minimize edema. Software interfaces guide parameter selection through preloaded procedure libraries, supporting clinicians new to lasers. These advances collectively widen the range of billable indications and lower the skill barrier, persuading general practitioners that lasers are no longer niche equipment.

Expansion of Chair-Side CAD/CAM Workflow Compatibility

Digital dentistry thrives on single-visit efficiency. Laser-prepared margins create clean, blood-free fields that optical scanners capture accurately, eliminating the need for retrofitting steps. Labs or in-office mills can then fabricate ceramic inlays that seat precisely, shortening total chair time. For DSOs, the integration underpins a high-throughput restorative model, while hospitals use laser-CAD/CAM combinations for complex oncologic resections followed by immediate prosthetic rehabilitation. The workflow synergy lifts overall equipment utilization, strengthening the return on laser investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition & Maintenance Costs | -1.4% | Global, acute for solo practices in North America, Europe | Short term (≤ 2 years) |

| Limited Reimbursement Across Major Payers | -1.1% | United States, Western Europe; lower impact in cash-pay APAC, MEA | Medium term (2-4 years) |

| Steep Learning Curve & Training Deficits | -0.8% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Regulatory Uncertainty for Class IV+ Lasers | -0.5% | United States, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty for New Laser Classes (Class IV+)

High-power or multi-wavelength devices may be classified into stricter regulatory categories, thereby prolonging clearance cycles under FDA 510(k), EU MDR, or China’s NMPA regimes[2]U.S. Food and Drug Administration, “Dental Lasers: Premarket Notification 510(k) Guidance,” fda.gov. Extended approval timelines can increase development costs and delay market entry by 12-18 months. Manufacturers hedge by releasing incremental upgrades rather than breakthrough configurations, modestly slowing the pace of innovation available to clinicians.

Limited Reimbursement Across Major Payer Systems

Most U.S. and European insurers bundle laser procedures with conventional codes, eliminating incremental fees that might offset the cost of the equipment. Clinicians must rely on patient out-of-pocket payments, a viable strategy only in affluent or cosmetic-oriented markets. In contrast, cash-pay regions such as parts of Asia-Pacific experience fewer reimbursement barriers, but widespread adoption still hinges on household disposable income. Without payer recognition of clinical benefits, the financial incentive to invest in lasers stays muted for insurance-dependent practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soft Tissue Volume Masks, Hard Tissue Upside

Soft tissue lasers accounted for 57.54% of the dental lasers market size in 2025, driven by lower price points and their broad applicability in gingival contouring, frenectomy, and periodontal debridement. Their ease of integration delivers quick payback, especially in high-throughput DSO branches that perform large volumes of cosmetic reshaping. Hard-tissue-capable erbium:YAG systems, though more expensive, are gaining visibility as evidence mounts for painless caries excavation and peri-implantitis management. Over the forecast period, rising clinician proficiency and the introduction of bundled dual-wavelength consoles will gradually shift the product mix toward platforms that address both tissue types within a single workflow. DSOs already deploy soft tissue units system-wide and concentrate premium hard-tissue models at specialty hubs where procedure complexity justifies higher capital allocation.

Soft tissue dominance reflects the financial calculus of independent practices that often start with a diode laser to gain surgical flexibility and patient marketing appeal. Once utilization stabilizes, some practices trade up to dual-wavelength devices that unlock restorative indications and expand revenue streams. Continued refinement of pulse modulation and fiber delivery will further broaden the indications for soft tissue. Yet, the comparative clinical value of hard-tissue capability suggests a measured but steady shift toward full-spectrum systems as amortization barriers ease.

By Technology: Erbium Momentum Signals Hard-Tissue Pivot

Diode platforms held 36.54% of the 2025 dental lasers market share because they address everyday soft tissue cases at entry-level pricing. However, erbium:YAG units are projected to post the highest 10.65% CAGR through 2031 as clinicians seek single-visit hard-tissue treatments that preserve tooth structure. Carbon dioxide lasers, once favored for excisional biopsy and vaporization, face share erosion due to higher cost and competitive diode upgrades. Neodymium:YAG remains niche for deep tissue coagulation and photobiomodulation, often bundled as a secondary wavelength in multi-mode consoles.

Technological convergence is accelerating. Short-pulse erbium modules achieve enamel ablation with negligible thermal spread, while software-guided parameter libraries simplify setup. Manufacturers now combine diode and erbium beams in a single chassis, allowing practitioners to transition from gingivectomy to cavity preparation without switching equipment. These hybrid systems reduce operatory clutter and strengthen the overall value proposition, positioning erbium as the logical next-round investment for practices already comfortable with diode workflows.

By Application: Implantology Growth Outpaces Established Oral Surgery

Oral surgery captured 31.56% of revenue in 2025 because lasers reliably perform tissue excision and hemostasis with less bleeding and faster wound closure. Implantology, however, is set to expand at an 11.67% CAGR as protocols for laser-mediated peri-implantitis decontamination gain scientific backing. Clinicians appreciate that erbium:YAG beams remove microbial biofilm without scratching titanium, extending implant lifespan, and reducing revision rates. Periodontal procedures, including LANAP, continue to generate consistent volume, while conservative dentistry gains traction as patients embrace vibration-free cavity preparation.

Emerging indications illustrate the modality’s versatility. Endodontic disinfection benefits from laser-activated irrigants that penetrate complex canal anatomy, though adoption remains confined to technology-forward practices. Pediatric dentistry also shows promise because lasers permit caries removal with minimal anesthesia, a compelling proposition for anxious children and parents alike. As clinical literature expands, referral patterns are likely to favor laser-enabled practitioners, further widening the usage gap between equipped and unequipped offices.

By End User: Hospital Demand Climbs Alongside Case Complexity

Clinics and DSOs generated 55.67% of purchases in 2025, reflecting their dominance in routine restorative and periodontal care. Hospitals are on track for an 11.45% CAGR because maxillofacial and oncologic teams require precision cutting with minimal collateral damage. Teaching hospitals pioneer dual-wavelength research protocols, accelerating the translation of evidence into mainstream practice. Academic sites validate safety profiles that bolster insurance negotiations and inform regulatory approvals.

DSOs utilize uniform training curricula and centralized procurement to scale adoption rapidly. Their data platforms capture utilization metrics that tighten return-on-investment models, reinforcing further capital allocation. Conversely, adoption in single-owner clinics remains patchy; without group purchasing power or internal mentors, many dentists defer investment, perpetuating market bifurcation.

Geography Analysis

North America retained 40.34% share in 2025, anchored by the United States, where DSO expansion and high disposable income underpin equipment upgrades. Mature CAD/CAM penetration creates natural integration points for lasers, while continuing education ecosystems sustain clinician competency. Canada mirrors these trends on a smaller scale, with provincial variations in scope-of-practice regulations shaping uptake. Mexico’s border clinics exploit dental tourism by advertising laser-assisted veneers and implant placement to U.S. patients seeking price relief.

Asia-Pacific is forecast to grow fastest at 9.43% CAGR through 2031. China’s rising middle class drives the opening of private clinics, which view lasers as a modern brand signal. Japan’s high implant prevalence drives demand for erbium units suitable for peri-implant maintenance, whereas South Korea’s well-established medical tourism sector positions dual-wavelength consoles as standard amenities. India exhibits early-stage adoption, primarily in urban areas where competitive differentiation is crucial. Thailand and the Philippines, on the other hand, bank on laser-branded packages to attract overseas clientele.

Europe exhibits mixed dynamics. Germany benefits from selective insurance reimbursement for periodontal laser therapy, fostering penetration among periodontists. The United Kingdom sees strong private-sector interest, but reimbursement gaps within the National Health Service limit broader deployment. France and Italy maintain a moderate level of adoption, focusing on urban cosmetic clinics. In the Middle East, Gulf countries invest in cutting-edge equipment to build regional centers of excellence. South Africa’s private market pilots laser units in Johannesburg and Cape Town, but broader diffusion is hindered by currency volatility and limited access to training. Brazil leads South America through private dental chains that equip high-volume sites with diode systems to cater to cosmetic surgery travelers.

Regulatory Landscape

Dental lasers are generally regulated as moderate-risk medical devices in key markets. In the United States, laser surgical instruments for dental use are commonly classified as Class II devices under FDA product codes such as GEX, which typically require 510(k) clearance. Manufacturers and providers also need to meet radiation and electrical safety expectations that flow into labeling, protective eyewear guidance, and facility controls, which can become more complex as systems add higher power and multi-wavelength modes.

In Europe, dental lasers fall under the EU Medical Device Regulation (MDR) 2017/745, where classification and clinical evidence requirements shape Notified Body review and post-market obligations. Guidance continues to develop through standards and technical documents used in conformity assessment, including the publication of CEN/TR 12401:2025 (April 2025), which provides updated classification guidance for dental devices under the MDR framework and affects how manufacturers justify intended purpose, claims, and risk class for laser platforms.

Value Chain Analysis

The dental lasers value chain starts with specialized component sourcing, including laser diodes, solid-state laser modules, optics, fibers, handpieces, control electronics, and cooling subsystems. It then moves through OEM design, software development (procedure libraries and presets), system integration, and quality management. Compliance and test activities, including alignment to laser and medical electrical safety standards (commonly IEC 60601-2-22 and IEC 60825-1), are built into development and manufacturing because they affect clearance dossiers, labeling, and service procedures.

Commercialization depends on multi-tier distribution and service networks, since installation, calibration, maintenance, and clinical training influence utilization and renewal of consumables or service contracts. Trade associations and channel bodies (e.g., Dental Trade Alliance, ADDE, BDIA) support market access through guidance, training ecosystems, and standards awareness, while manufacturers and specialist distributors manage regional regulatory documentation and after-sales coverage. In the United States, FDA Laser Notice No. 56 (effective by March 2025) supports use of harmonized IEC standards to demonstrate compliance, which can streamline multi-market submissions and reduce duplicative test burdens across the chain.

Competitive Landscape

Market concentration remains moderate, with global incumbents defending their share through incremental upgrades that refine pulse shapes, fiber ergonomics, and software presets, rather than radical hardware leaps. Integration with digital dentistry ecosystems enables manufacturers to bundle scanners and milling units, thereby deepening account penetration. Subscription service contracts and proprietary consumables secure recurring revenue streams that cushion price competition.

While niche entrants target specific wavelengths or lightweight form factors, limited service coverage restricts their appeal in hospital and DSO tenders. Geographic expansion features prominently in strategic roadmaps, especially toward the Asia-Pacific and the Middle East, where first-mover installations anchor long-term consumables sales. Several leaders partner with DSOs to create co-branded training centers, ensuring that clinician proficiency dovetails with equipment rollouts. Regulatory complexity raises barriers for newcomers, subtly favoring companies that maintain in-house compliance expertise and clinical education teams.

Industry observers anticipate selective consolidation as smaller firms struggle to finance multi-region distribution and sustained R&D. Acquisitions that fold specialist players into larger portfolios can deliver complementary wavelength technologies and bolster after-sales networks. Competitive intensity may rise if reimbursement codes finally differentiate laser procedures, but for now, product ecosystems and training depth outweigh pure hardware specifications in purchasing decisions.

Dental Lasers Industry Leaders

Dentsply Sirona

Fotona D.D.

Gigaalaser

MegaGen Implant

Convergent Dental Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An actionable opportunity lies in pairing multi-indication capability with adoption that fits general practitioners. Consoles that combine soft-tissue throughput (diode) with hard-tissue and peri-implant workflows (erbium-capable), while also embedding guided presets, workflow integrations, and standardized training, reduce the operational lift required to expand beyond a single clinical niche. Evidence of this shift toward broader functionality appears in regulatory activity and product roadmaps that extend beyond cutting and coagulation, including FDA 510(k) clearances tied to laser fluorescence-based caries detection technology (for example, Dentsply Sirona Primescan 2 receiving 510(k) clearance in August 2025).

A second opportunity is scaling utilization, not only placements, through structured clinical education and protocol standardization that supports more consistent outcomes across DSOs and hospitals. Professional bodies and laser dentistry organizations continue to formalize education pathways, and company initiatives emphasize workflow-enabled therapy packages, such as the LANAP AI workflow integration launched in May 2025 that bundles devices with operatory productivity tools. As more 510(k) clearances are granted for soft-tissue diode systems in 2026, differentiation increasingly shifts toward service footprint, training depth, and end-to-end digital dentistry compatibility rather than wavelength alone.

Recent Industry Developments

- March 2026: Fotona launched its FotonaSMILE campaign to support comprehensive laser-assisted smile enhancement and increase practitioner awareness of aesthetic dentistry applications. The campaign reinforces demand-generation beyond core periodontal and surgical use-cases, supporting higher utilization of multi-application laser platforms among cosmetic-oriented practices.

- May 2025: Millennium Dental Technologies launched the LANAP AI Workflow, integrating the PerioLase MVP-7 Nd:YAG laser with the Zyris Isolite Pro system. By packaging a clinical protocol with workflow components, the release targets chair-time efficiency and standardization, which is particularly relevant for multi-site operators seeking consistent periodontal outcomes.

- April 2025: Convergent Dental launched Solea Perioguide for minimally invasive periodontal therapy as an application for the Solea all-tissue CO2 dental laser. The launch expands procedure-specific positioning for existing installed bases, supporting broader periodontal adoption and increasing the addressable set of billable indications for CO2 laser users.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The dental lasers market covers revenue from laser systems used in dental procedures, together with related accessories when sold as part of the laser offering. It is sized using equipment demand across key dental care settings and the mix of procedures where lasers are clinically used.

Scope exclusions: Cosmetic spa lasers and general medical or surgical lasers not intended for dental use are excluded.

Segmentation Overview

- By Product Type

- Soft Tissue Lasers

- Hard Tissue Lasers

- By Technology

- Diode Lasers

- Nd:YAG Lasers

- Er:YAG Lasers

- CO? Lasers

- By Application

- Conservative Dentistry

- Endodontic Treatment

- Oral Surgery

- Periodontics

- Implantology

- By End User

- Dental Clinics & DSOs

- Hospitals

- Academic & Research Institutions

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting demand picture and to ensure assumptions follow real world clinical and regulatory patterns. We referenced public sources such as CDC oral health statistics, WHO oral health facts, World Bank population and income indicators, OECD health data, and FDA device databases and safety notices (as examples of what was checked).

On the supply side, annual reports, investor decks, and reputed press were reviewed to understand product positioning, launch timing, and broad regional exposure. We also used paid subscriptions for company financials and intelligence, plus patent database access, to track technology focus and the pace of new filings that may influence adoption. The desk sources listed here are not exhaustive, and many other public references were also consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating where lasers are actually being used in dentistry, and what is changing purchase decisions year to year. We spoke with a mix of clinic operators, procurement and biomedical teams, distributors, and dental academics across APAC, EMEA, and the Americas, which helped us confirm procedure-level adoption, typical replacement cycles, and the real spread between list price and transacted pricing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 45% |

| Mid tier: 58% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 15% | Managers: 52% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the dental equipment demand pool is reconstructed using dental procedure volumes and the penetration of laser-assisted dentistry by care setting, and then the totals are allocated by region using service capacity indicators. To keep the totals realistic, we corroborate the outcome with selective bottom-up approximations, such as sampled average selling prices multiplied by estimated unit shipments, distributor channel feedback, and replacement-driven demand checks when new placements are hard to observe.

The model uses a practical set of inputs that can be tracked over time, including the mix of soft tissue and hard tissue procedures, adoption in DSOs versus solo practices, average system pricing by laser type (for example, diode versus erbium), equipment replacement cycles, and regional dentist and clinic density. Where gaps exist, assumptions are filled using interview-based ranges and then stress-tested against what clinics say they can budget for in a typical year.

For forecasting, scenario analysis is used, with inputs adjusted based on how quickly chair-time savings and patient acceptance translate into purchasing, and how training availability and reimbursement climates evolve. The forward view is also anchored by expert consensus on the pace of diode uptake, the growth of implantology and oral surgery volumes, and the likely timing of product refreshes that can trigger upgrades.

Data Validation & Update Cycle

Validation is done by checking the model against independent signals, and then rechecking any large variances before sign-off. We compare the derived totals with region-level procedure growth, observed pricing bands, and interview feedback on ordering patterns, and then unusual jumps are reviewed to confirm they are linked to a known driver like a product cycle or a demand shock.

Each report goes through multi-step internal review where assumptions, calculations, and year-to-year movements are challenged and corrected when needed. Reports are refreshed annually, and interim updates are triggered when there is a material event such as a major regulatory action, a notable change in clinic purchasing behavior, or a meaningful pricing shift. Before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Dental Lasers Market Estimate Compared With Other Published Estimates

Published market values for dental lasers often do not match because scope and counting rules vary, and those choices change the final number more than many people expect. Differences usually come from what is treated as dental-only revenue, how pricing is averaged across laser types, and whether the year shown is a base year or the first forecast year.

A common gap driver is whether adjacent laser revenues get folded in, where Mordor Intelligence counts dental laser systems by defined dental use and excludes broader medical laser sales even if the technology is similar. Other spreads also come from how procedure growth is translated into equipment demand, since some estimates assume faster penetration into smaller practices without checking training capacity and purchase cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 401.30 M (2026) | |

| Industry Publisher A | USD 371.50 M (2025) | Uses a different reference year and a type split that can shift the weighted average price by emphasizing all-tissue systems versus procedure-specific systems, which changes the starting value before forecasting. |

| Industry Publisher B | USD 316.20 M (2024) | Uses an earlier base year with a slower assumed adoption path, and the link between procedure demand and device purchases is less explicit, which can understate replacement-led buying in mature regions. |

The table shows that most of the spread is explained by year selection and by how pricing and adoption are averaged across laser types and care settings. By tying demand to procedure usage, care-setting penetration, and realistic replacement timing, we keep the estimate traceable to clear inputs that can be rechecked and updated as new signals appear.

Key Questions Answered in the Report

How large is the dental lasers market in 2026?

The dental lasers market size reaches USD 401.30 million in 2026 and is positioned for steady 8.01% annual expansion to 2031.

Which laser technology is growing fastest?

Erbium:YAG platforms lead growth with a projected 10.65% CAGR through 2031, reflecting rising demand for hard-tissue capability.

Why are DSOs important to dental laser adoption?

DSOs centralize purchasing and training, enabling rapid, cost-efficient rollout of lasers across large practice networks.

What restrains laser uptake in independent practices?

High acquisition costs, bundled reimbursement codes, and limited formal training delay investment among solo offices.

Which region will expand most quickly?

Asia-Pacific is expected to advance at a 9.43% CAGR to 2031, driven by income growth, dental tourism, and government oral-health initiatives.

What clinical application shows the highest future growth?

Implantology should rise fastest, at an 11.67% CAGR, as erbium:YAG lasers prove effective for peri-implantitis decontamination.

Page last updated on: