Dental Caries Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.58 Billion |

| Market Size (2031) | USD 8.83 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

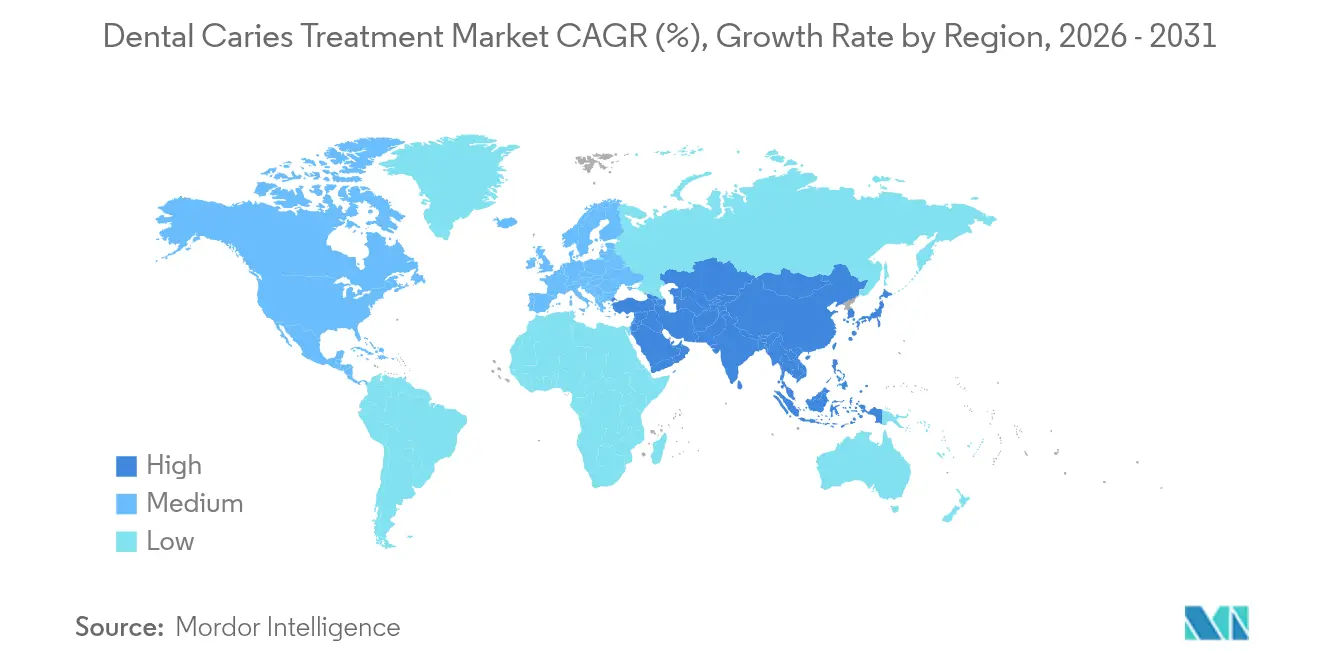

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

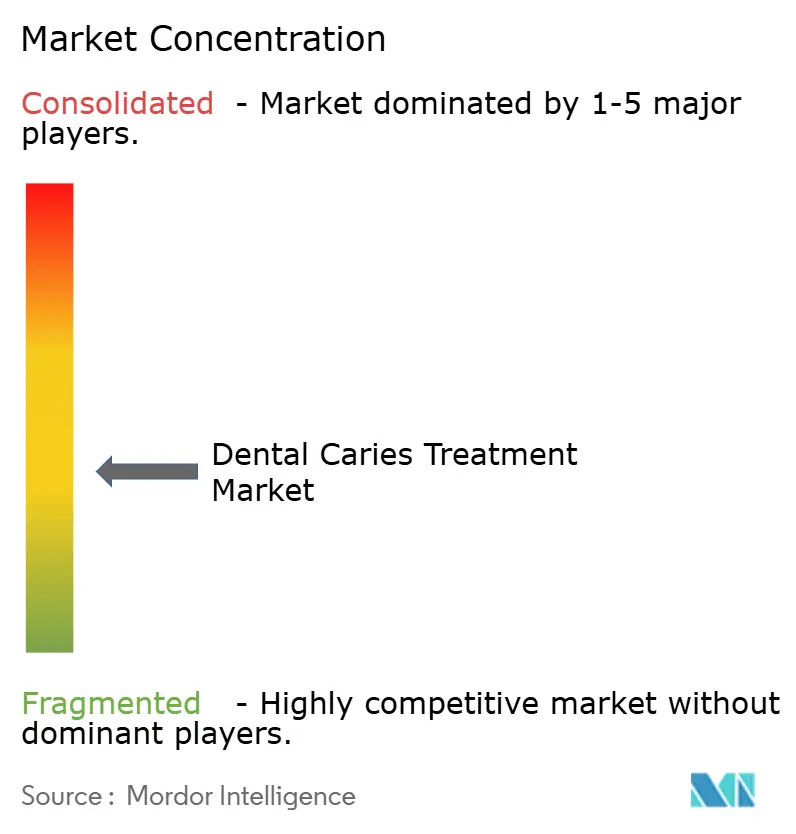

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Caries Treatment Market Analysis by Mordor Intelligence

The Dental Caries Treatment Market size is expected to grow from USD 7.35 billion in 2025 to USD 7.58 billion in 2026 and is forecast to reach USD 8.83 billion by 2031 at 3.12% CAGR over 2026-2031.

This measured growth indicates a maturing competitive field in high-income economies, while emphasizing the new patient throughput now visible in emerging territories that have recently incorporated oral care into universal-coverage charters.[1]World Health Organization, “Oral Health,” who.int Momentum also stems from artificial-intelligence diagnostic suites that achieve 73-98% accuracy, compared to 45% for manual radiographic reading, thereby reducing misdiagnosis and expanding the addressable restorative pool.[2]B. Ekert et al., “Artificial Intelligence for Radiographic Imaging Detection of Caries Lesions,” BMC Oral Health, bmcoralhealth.biomedcentral.com At the same time, population ageing—by 2034, one in four U.S. residents will be older than 65 —shifts volume toward multi-surface restorations and vital-pulp therapies that carry higher per-procedure value. Clinical preference now tilts toward minimally invasive protocols; selective caries removal delivers 94% procedural success and reduces pulp-exposure risk from 27.5% to 2%. National fluoride programs, early screening mandates, and dental tourism bundles in the Asia-Pacific further widen access, ensuring a durable patient funnel for the dental caries treatment market.

Key Report Takeaways

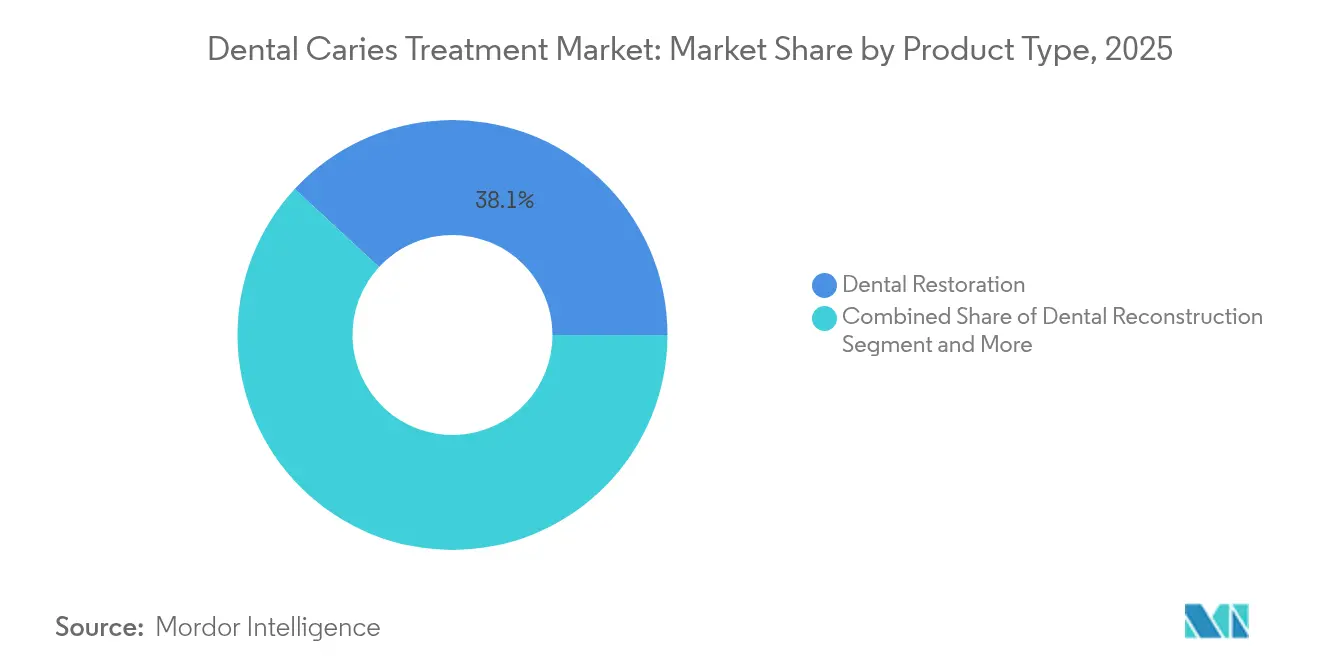

- By product type, dental restoration accounted for 38.12% of the revenue in 2025, while endodontic products are projected to rise at a 3.75% CAGR through 2031.

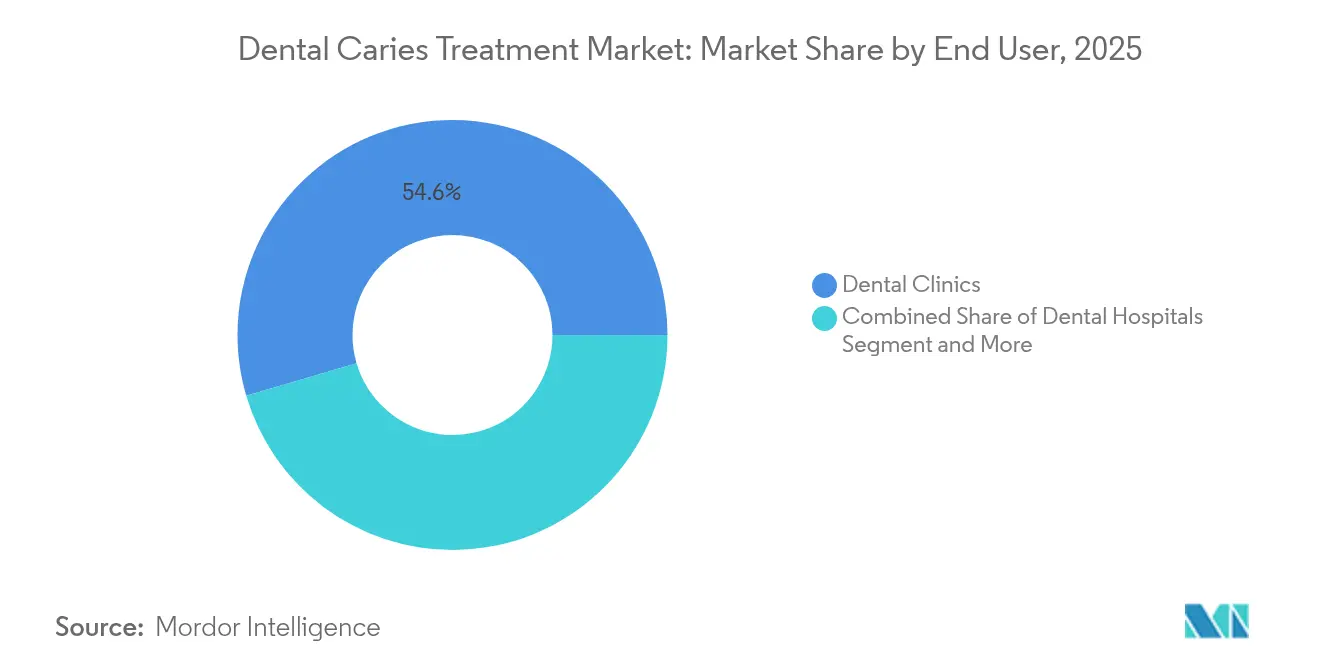

- By end user, dental clinics accounted for 54.55% of the dental caries treatment market share in 2025. In contrast, dental hospitals are expected to show the highest CAGR of 4.05% from 2025 to 2031, underscoring a gradual shift toward more complex case centers.

- By geography, North America represented 34.52% of global revenue in 2025, while the Asia-Pacific region is expected to advance at a 4.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Caries Treatment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Dental Caries Worldwide | +1.0% | Global, with highest impact in developing regions | Long term (≥ 4 years) |

| Growing Geriatric Population Needing Restorative Care | +0.8% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Technological Advances in Minimally-Invasive Caries Removal | +0.6% | Developed markets initially, global adoption | Medium term (2-4 years) |

| AI-Enabled Early Detection Tools Adoption | +0.5% | North America & Europe, selective Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of Dental-Tourism Packages for Caries Treatment | +0.4% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Universal-Health Coverage Schemes Adding Oral Health Benefits | +0.3% | Global, with priority in emerging economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries Worldwide

Untreated decay affects 2 billion adults and 514 million children, making caries the planet’s most common disease. Rapid urbanization increases access to sugar-dense snacks, potentially overwhelming the benefits of water fluoridation. In many low-income regions, public clinics often have multi-month waiting lists for simple fillings, allowing lesions to progress into costly endodontic cases that fuel the dental caries treatment market. Governments respond with community fluoride-varnish drives, yet workforce shortages persist. The net effect perpetuates a structural demand floor that shields the dental caries treatment market from broader economic cycles.

Growing Geriatric Population Needing Restorative Care

By 2030, more than 20% of EU residents will surpass 65 years, with similar ratios emerging across East Asia. Polypharmacy-induced xerostomia and reduced dexterity heighten root-surface decay, shifting treatment toward multi-surface restorations, partial pulpotomies, and root-caries sealants. Many seniors lack dental insurance, prompting policymakers to debate the expansion of Medicare dental coverage in the United States. Long-term-care facilities are now installing in-house operatories, further embedding restorative workflows into geriatric care and reinforcing demand for the dental caries treatment market.

Technological Advances in Minimally Invasive Caries Removal

Selective excavation, chemomechanical gels, and self-limiting burs preserve healthy dentin, achieving a 94% success rate and reducing pulp exposure to 2%. Chairside adoption lowers anaesthetic need, shortening visits and raising patient satisfaction. European insurers already reimburse conservative codes, encouraging further uptake. In the dental caries treatment market, product innovations that align with stricter infection control standards are helping vendors enhance their pricing strategies while supporting broader value-based care objectives.

AI-Enabled Early Detection Tools Adoption

Convolutional neural networks increase diagnostic accuracy to 98%, surpassing the 45% benchmark for manual reading. Early discovery supports resin-infiltration treatments that intercept decay before cavitation, creating new billing opportunities. The U.S. FDA clarified performance criteria in 2024, accelerating clearances. Subscription pricing models reduce capital hurdles for smaller practices, promoting wider installation of AI platforms and deepening data feedback loops that benefit the dental caries treatment market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Restorative Materials & Devices | -0.6% | Global, with highest impact in price-sensitive markets | Medium term (2-4 years) |

| Limited Reimbursement for Dental Procedures | -0.4% | Global, particularly acute in developing economies | Long term (≥ 4 years) |

| Antimicrobial Resistance Reducing Cariostatic Efficacy | -0.3% | Global, with emerging hotspots in antibiotic-overuse regions | Long term (≥ 4 years) |

| Sustainability Scrutiny of Amalgam Alternatives | -0.2% | Europe & North America primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Restorative Materials & Devices

Nanoparticle-reinforced composites and AI scanners can cost three times as much as conventional options. EU Medical Device Regulation paperwork raises overhead, squeezing smaller firms and nudging prices upwards. Latin American public payers cap reimbursements well below premium material costs, slowing the conversion to bioactive products.

Limited Reimbursement for Dental Procedures

Seventy percent of U.S. seniors lack dental coverage because Medicare does not cover routine care. Out-of-pocket spending exceeds 65% of dental spending in several low-income nations. Patients, therefore, delay early treatment until pain forces emergency extraction, a pattern that undercuts conservative therapy volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Restorative Materials Lead Innovation

The dental restoration segment captured 38.12% of the revenue in 2025, cementing its role as the cornerstone of the dental caries treatment market. Nano-hybrid composites compete on polish retention, wear resistance, and polymerisation shrinkage, while glass ionomers win in moisture-challenged cervical lesions with sustained fluoride release. Mercury amalgam phase-down under the Minamata Convention accelerates resin conversion, even in cost-sensitive clinics. Bioactive glass fillers that stimulate apatite formation expand premium price bands. Meanwhile, bulk-fill formulations that cure in 4 mm increments cut chair time, pleasing high-volume public clinics and solidifying throughput for the dental caries treatment industry. Manufacturers also develop shade-adaptive resins that reduce inventory complexity and cross-shade mismatch risk, strengthening brand stickiness across the dental caries treatment market.

Endodontic products are projected to grow at the fastest 3.75% CAGR through 2031, reflecting a global shift from extraction to pulp-vitality conservation. Bioceramic sealers bond chemically to dentin and resist micro-leakage, improving long-term outcomes. Rotary nickel-titanium files with regressive tapers reduce the risk of fracture and decrease the total number of instrumentation steps. Cone-beam CT guidance refines working-length estimation, curbing retreatment rates. Public health programmes in middle-income economies now reimburse pulpotomy for deciduous molars, delaying premature exfoliation and safeguarding occlusal development. These trends expand procedure counts and unit sales for obturators, sealers and irrigation solutions, reinforcing the dental caries treatment market trajectory.

By End User: Clinics Dominate Through Accessibility

Dental clinics accounted for 54.55% of the global revenue in 2025, underscoring consumer preference for local, relationship-based care pathways within the dental caries treatment market. Chain clinics backed by private equity roll out digital practice-management platforms that integrate intraoral scanning, chairside CAD/CAM, and AI lesion detection, thereby optimally lifting revenue per hour. Tele-triage portals triage pain cases and funnel patients to clinics, adding incremental restorative openings. Together, these service innovations keep the dental caries treatment market anchored in community-oriented settings.

Dental hospitals, although fewer in absolute number, are expected to clock a 4.05% CAGR through 2031. They manage medically complex patients with oncology therapy, anticoagulation, and severe systemic disease who require integrated anaesthesiology and emergency support. Multidisciplinary rounds coordinate cardiac clearance before root canal therapy, thereby reducing the risk of adverse events. Hospitals serve as training grounds for postgraduate residencies, giving them early access to prototype biomaterials and AI platforms. As population ageing accelerates, the prevalence of comorbidities increases, prompting referrals of high-risk restorative cases to hospital settings, thereby adding specialized volume to the dental caries treatment market.

Geography Analysis

North America accounted for 34.52% of the revenue in 2025, driven by employer-funded insurance enrollment, clinician density, and the rapid adoption of diagnostic AI solutions. Yet Medicare still excludes routine dentistry, limiting growth among retirees and influencing public hearings for benefit expansion. Corporate dental support organisations bulk-buy composites and liners, negotiating steep rebates that maintain margin resilience in the dental caries treatment market. Tele-dentistry pilots in remote Canada and Alaska expand fluoride-varnish coverage, increasing preventive caseloads and enhancing the rural reach of the dental caries treatment market.

Europe remains innovation-minded while managing tight budgets. Scandinavia subsidises fissure sealants and resin infiltration for schoolchildren, front-loading material usage early in life. The Medical Device Regulation introduces significant compliance costs, prompting consolidation and giving well-capitalized suppliers a competitive advantage. Germany trials bundled reimbursement for minimally invasive therapy, and France expands public-clinic fluoride-varnish programs, each generating steady revenue for the dental caries treatment market. Southern Europe is experiencing pent-up demand as economic recovery boosts private dental spending, helping to offset the maturity of the northern market.

The Asia-Pacific region charts the fastest growth at 4.30% CAGR, driven by rising disposable income, universal coverage expansion, and dental tourism inflows to Thailand, Vietnam, and Cambodia. Thailand reimburses atraumatic restorative treatment under its national scheme, fueling demand for glass hybrids. China’s Healthy Mouth Initiative doubles dental-school seats and mandates community-clinic quotas in underserved provinces, boosting workforce supply. Smartphone-based booking apps, popular among urban millennials, translate latent cosmetic interest into actual restorative appointments, adding volume to the dental caries treatment market. Simultaneously, local production of composites in India and Indonesia mitigates import duties, but quality-control discrepancies keep premium imports relevant for high-end clinics.

South America’s progress ties to Brazil’s public insurer, which extends fluoride-varnish coverage and builds demand for follow-up operative care. Currency volatility tempers premium import growth, encouraging regional suppliers to produce cost-optimised composites. The Middle East & Africa trail in absolute numbers, yet record high-value consumption in Gulf states, where expatriate professionals expect Western-grade restoratives and CBCT imaging. Sub-Saharan projects utilize mobile clinics for silver-diamine fluoride applications to school populations, providing early-stage interventions that funnel future restorative cases into the dental caries treatment market once disposable income increases.

Competitive Landscape

The dental caries treatment market is moderately concentrated, with the five largest companies accounting for over half of the aggregate revenue, while specialized challengers continue to thrive. Solventum, Dentsply Sirona, GC Corporation, and Colgate-Palmolive utilize a global scale to refresh composite chemistry, develop AI-integrated workflows, and distribute through direct sales footprints spanning more than 120 countries. Solventum’s spin-off from 3M sharpened its healthcare focus and accelerated launch cycles for 3D-printed aligner attachments now cleared in North America. Dentsply Sirona equips dental faculties with scanners and simulation units, locking in early-career brand preference.

AI software pioneers license diagnostic algorithms to imaging OEMs on a pay-per-scan basis, side-stepping hardware risk and tapping recurring revenue. Composite makers acquire syringe-tip specialists, ensuring ergonomic exclusivity that cements brand ecosystems within the dental caries treatment market. At the same time, regional suppliers address cost-sensitive segments with mercury-free glass ionomers and moisture-tolerant bioceramics. Venture funds inject capital into nanotechnology start-ups that explore peptide-functionalized fillers, promising genuine dentin remineralization. Regulatory stringency filters out undercapitalised entrants yet incentivises strategic alliances as a shortcut to compliance, keeping the dental caries treatment market dynamic and technologically progressive.

Supplier bargaining power rises as consolidation reduces competing bids, yet purchaser clout strengthens via group practices and dealer conglomerates. Pricing therefore remains stable; differentiation pivots on ease-of-use kits, digital workflow compatibility and evidence-backed clinical longevity. Marketing narratives spotlight value-based care materials that lower retreatment incidence over commodity discounting, a positioning that sustains gross margins even as reimbursement ceilings tighten. Consequently, the dental caries treatment market rewards firms that fuse science, software and service into integrated care pathways rather than isolated products.

Dental Caries Treatment Industry Leaders

Institut Straumann AG

Coltene Group

ZimVie Inc.

3M

Dentsply Sirona Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Solventum launched 3M Clarity Precision Grip Attachments, the first 3D-printed aligner accessories tailored to tooth anatomy.

- August 2024: Perceptive demonstrated the world’s first fully automated AI-guided restorative procedure, cutting crown placement to 15 minutes.

Global Dental Caries Treatment Market Report Scope

Dental caries is a biofilm disease that results in the localized destruction of tooth tissues by acids produced in the mouth from the bacterial fermentation of dietary carbohydrates. Dental caries treatment procedures are used to remove or treat the condition. The Dental Caries Treatment Market is Segmented by Product Type (Dental Restoration, Dental Reconstruction (Abutments, Bridges, Crowns, Dentures, and Implants), and Endodontic (Files, Obturator Devices, Permanent Sealers, and Others)), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (In USD Million) for the above segments.

| Dental Restoration | |

| Dental Reconstruction | Abutments |

| Bridges | |

| Crowns | |

| Dentures | |

| Implants | |

| Endodontic Products | Files |

| Obturator Devices | |

| Permanent Sealers | |

| Others |

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| Product Type | Dental Restoration | |

| Dental Reconstruction | Abutments | |

| Bridges | ||

| Crowns | ||

| Dentures | ||

| Implants | ||

| Endodontic Products | Files | |

| Obturator Devices | ||

| Permanent Sealers | ||

| Others | ||

| By End User | Dental Hospitals | |

| Dental Clinics | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the dental caries treatment market in 2026?

It stands at USD 7.58 billion and is projected to reach USD 8.83 billion by 2031, giving a 3.12% CAGR.

Which product group generates the most revenue?

Restorative materials lead with 38.12% of global revenue in 2025.

What is the fastest-growing product segment?

Endodontic procedures grow at a 3.75% CAGR, driven by pulp-preservation therapies.

Which region shows the quickest expansion?

Asia-Pacific grows at a 4.30% CAGR, propelled by universal-coverage schemes and dental tourism.

How does artificial intelligence influence treatment?

AI improves lesion detection to 98% accuracy, enabling earlier, less invasive interventions and boosting clinic productivity.

What reimbursement gap limits access?

Most national plans lack comprehensive dental benefits, so seniors and low-income populations often self-pay, delaying early care.

Page last updated on: