Dental Caries Detector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

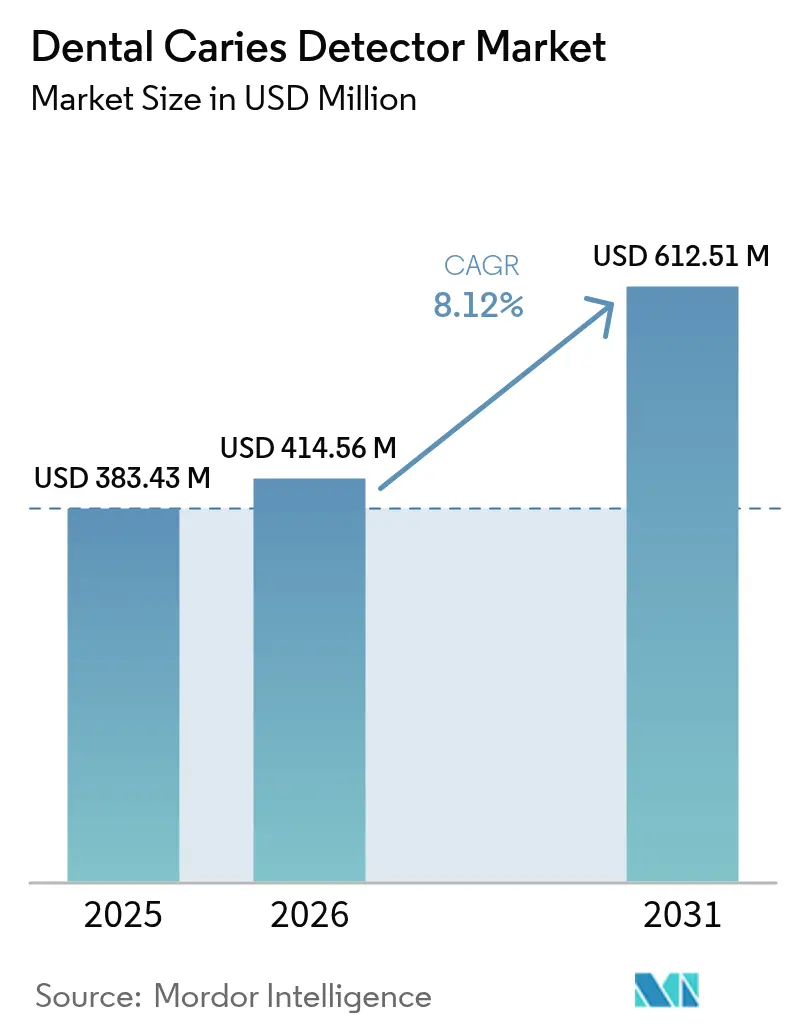

| Market Size (2026) | USD 414.56 Million |

| Market Size (2031) | USD 612.51 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Caries Detector Market Analysis by Mordor Intelligence

The Dental Caries Detector market size is expected to grow from USD 383.43 million in 2025 to USD 414.56 million in 2026 and is forecast to reach USD 612.51 million by 2031 at 8.12% CAGR over 2026-2031.

Momentum comes from the convergence of artificial intelligence (AI), laser fluorescence, and supportive regulatory pathways that prioritize preventive care over reactive treatment. Roughly 3.5 billion people now live with dental caries, and health systems are moving rapidly toward early-stage detection that can identify demineralization before cavitation sets in . Technology providers respond with integrated platforms that pair intraoral scanners, AI-based pattern recognition, and cloud analytics, yielding workflow efficiencies that raise treatment acceptance rates and shorten chair time. Venture capital keeps pouring into diagnostic start-ups underscoring sustained investor confidence in scalable, software-oriented solutions. Despite high acquisition costs in emerging economies, equipment leasing, mobile diagnostic services, and government oral-health campaigns temper price sensitivity and extend market outreach.

Key Report Takeaways

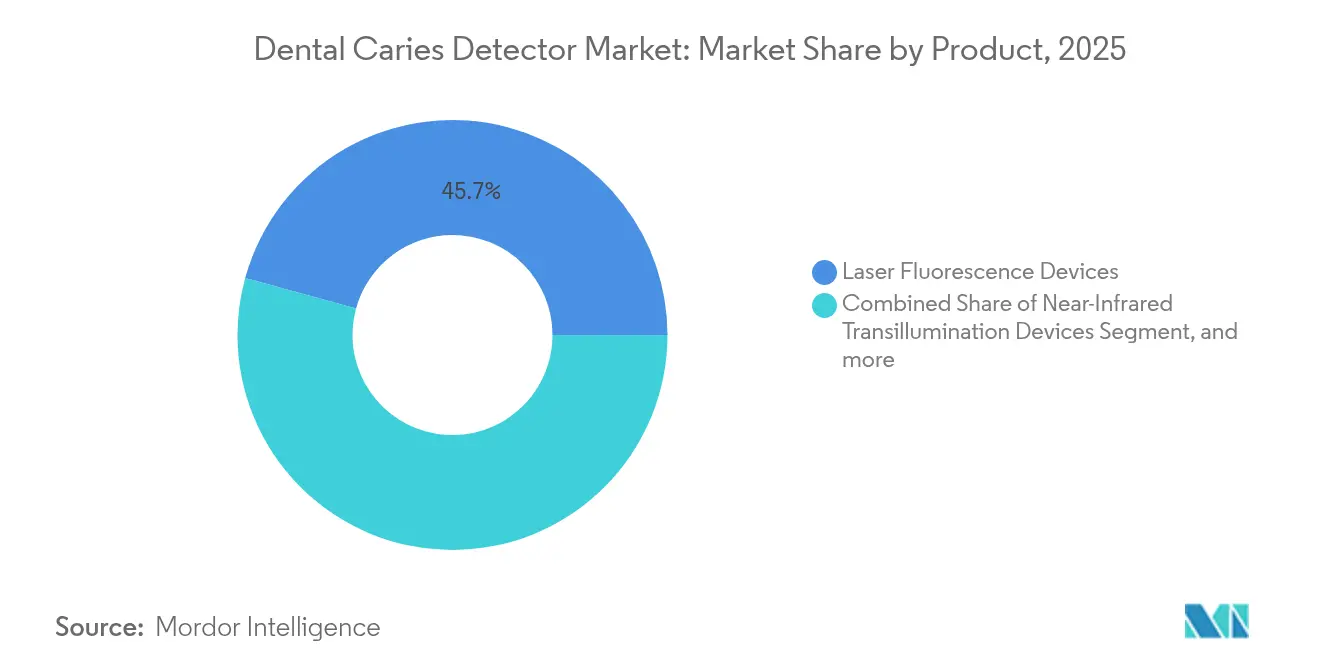

- By product category, laser fluorescence devices held 45.73% of the dental caries detector market share in 2025, while AI-based imaging platforms are forecast to rise at 10.98% CAGR through 2031.

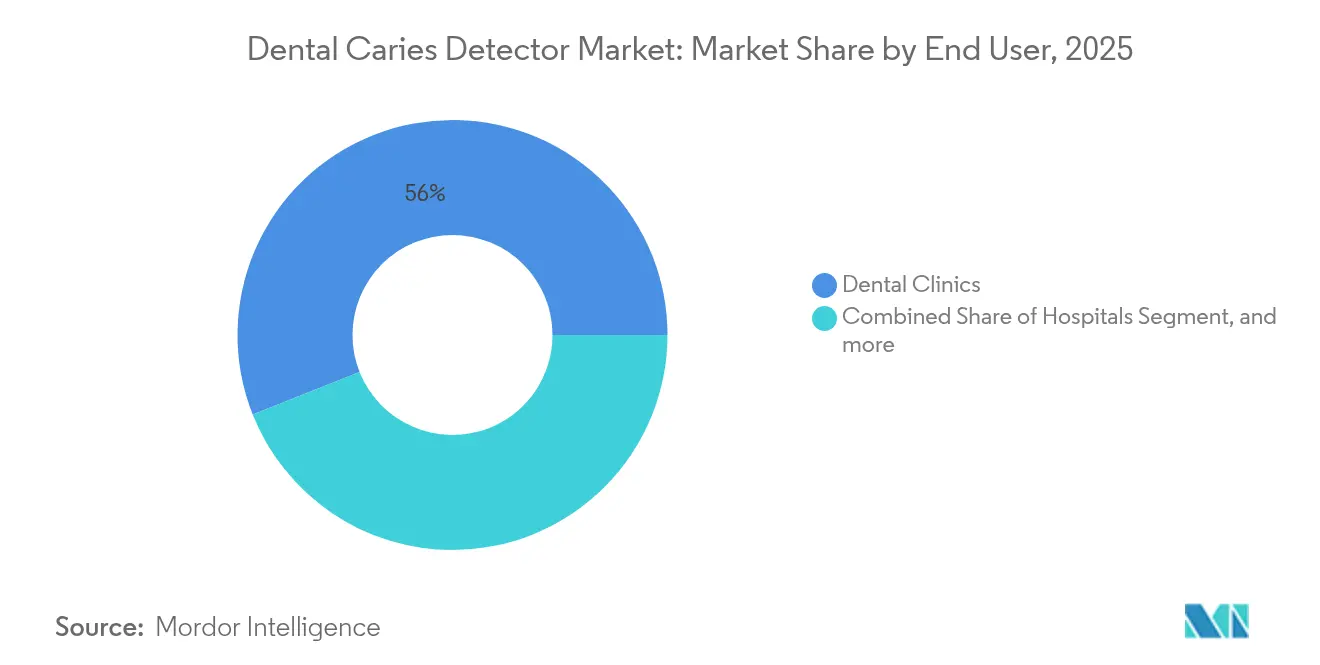

- By end user, dental clinics commanded 56.02% share of the dental caries detector market size in 2025, whereas ambulatory surgical centers are expanding at 12.15% CAGR to 2031.

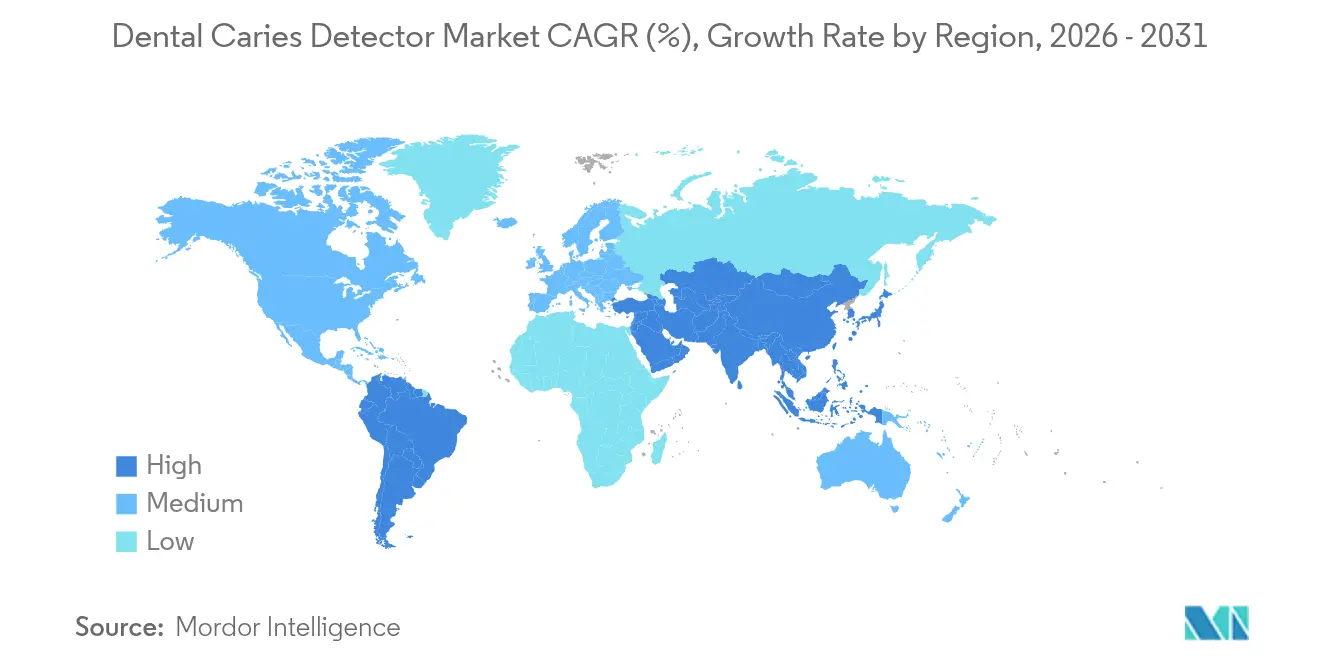

- By geography, North America led with 41.18% revenue share in 2025; Asia-Pacific is projected to register the fastest 11.74% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Caries Detector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries | +2.1% | Global, highest in Asia-Pacific | Long term (≥ 4 years) |

| Adoption of advanced diagnostic devices | +1.8% | North America, EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Demand for minimally invasive chairside diagnostics | +1.5% | Developed markets | Medium term (2-4 years) |

| AI-powered image analysis with intraoral scanners | +1.3% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| At-home salivary biosensor kits | +0.9% | Developed markets first | Long term (≥ 4 years) |

| Government oral-health initiatives | +0.7% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries

Roughly 3.5 billion people now face untreated oral disease, making early detection solutions a global necessity.[1]World Health Organization, “Oral Health Fact Sheet 2025,” who.int Health ministries increasingly pivot toward preventive care, budgeting for mass screening programs that hinge on portable fluorescence or AI-aided imaging. Untreated caries can escalate into complex interventions that consume scarce healthcare resources, so payers are incentivizing early diagnosis to curb downstream costs. Portable detectors that run on battery power gain popularity in outreach clinics and school-based programs across Asia-Pacific. Population-level epidemiological data feed machine-learning models that help providers stratify risk and allocate resources precisely. This systemic shift from reactive fillings to proactive demineralization monitoring underpins a sizeable slice of the dental caries detector market.

Increasing Adoption of Advanced Diagnostic Devices

Traditional visual-tactile exams often miss incipient lesions, so clinicians turn to laser fluorescence, near-infrared transillumination, and AI decision-support to raise diagnostic sensitivity. Intraoral scanners have reached a 57% adoption rate among U.S. practices, now bundling AI modules that flag demineralization otherwise overlooked on 2-D radiographs.[2]3Shape, “Annual Dental Market Survey 2024,” 3shape.com Practices adopting AI report 22% higher patient treatment acceptance and up to USD 78,000 in additional annual production per location. Workflow upgrades pose short-term training burdens, yet early adopters find competitive differentiation in faster diagnoses and richer patient communication. Vendors are consequently embedding tutorials and real-time decision aids into software updates, lowering the learning curve for late adopters.

Growing Demand for Minimally-Invasive Chairside Diagnostics

Minimally invasive dentistry calls for tools that spot lesions when remineralization is still viable. Devices such as the DIAGNOdent pen post about 90% reliability for early-stage caries, supporting micro-invasive treatment strategies that preserve enamel.[3]KaVo, “DIAGNOdent Product Brochure 2024,” kavo.com Chairside feedback loops allow immediate counseling, reducing the psychological barrier for patients who dread traditional drilling. Parents in particular favor laser-based diagnostics for children, as the method is contact-free and painless. Integration with practice-management software simplifies record-keeping, speeds insurance submissions, and ties diagnoses directly to restorative planning. The patient experience improves, lifting Net Promoter Scores and repeat visit probabilities for practices.

AI-Powered Image Analysis Integration with Intraoral Scanners

VideaHealth’s Caries 3.0 model cut diagnostic variability by 70% and false positives by 65%, demonstrating clinical gains that resonate in multisite dental service organizations. FDA clearance for patients aged 3 years and older enables cradle-to-lifetime applicability, de-risking adoption for family practices. AI integration also automates clinical note-taking and cross-links radiographs to CDT codes, reducing administrative overhead. Over 30,000 clinicians currently rely on at least one AI-powered detection platform, a figure projected to double by 2027. Smaller practices hesitate due to subscription fees and IT requirements, but cloud-hosted models and tiered pricing are narrowing the affordability gap. Uniform diagnostic standards also support insurers’ push toward value-based reimbursement, further catalyzing uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative diagnostic techniques | -1.2% | Global, higher in cost-sensitive markets | Medium term (2-4 years) |

| High device cost & limited reimbursement | -1.8% | Asia-Pacific emerging, MEA, South America | Long term (≥ 4 years) |

| Practitioner scepticism over specificity | -0.9% | Global, traditional settings | Short term (≤ 2 years) |

| Data-privacy and cybersecurity concerns | -0.7% | North America, EU (GDPR) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Limited Reimbursement in Emerging Markets

Advanced detectors run between USD 15,000 and USD 50,000 per unit, and annual maintenance or software subscriptions can add 25% to operating costs. Many public and private insurers in emerging economies classify these devices as elective, pushing the financial burden onto patients. Out-of-pocket payments often surpass average monthly income, restricting uptake to affluent urban centers. Leasing schemes and revenue-sharing partnerships have begun mitigating capital constraints, while mobile diagnostic vans bring portable units to rural communities on rotational schedules. National oral-health programs in India, Brazil, and Egypt now pilot reimbursement bundles that include preventive diagnostics, yet wide-scale inclusion in basic coverage remains years away.

Practitioner Scepticism Over Variable Device Specificity

Studies catalogue specificity variation among fluorescence systems, with some units dipping to 50% in identifying certain lesion types. Seasoned clinicians worry false positives may trigger unnecessary interventions, undermining patient trust. Workflow adjustments, including extra imaging steps and additional data entry, can lengthen appointment slots in already compressed schedules. Peer-reviewed guidelines from professional bodies like the American Dental Association now outline evidence-based protocols, but widespread comfort will take time. Continuing-education credits linked to AI and fluorescence training help bridge knowledge gaps and foster confidence in quantitative thresholds for treatment decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: AI Platforms Drive Innovation

Laser fluorescence devices retained the largest 45.73% slice of the dental caries detector market in 2025, thanks to established clinical familiarity and diagnostic reliability. These hardware-centric solutions remain staples for practices seeking immediate, chairside confirmation without major IT overhauls. However, AI imaging platforms are expanding at 10.98% CAGR, propelling a structural pivot toward software subscriptions that decouple diagnostic power from fixed equipment purchases. AI modules continuously learn from new radiographs, so diagnostic accuracy improves throughout the product life cycle. Near-infrared transillumination and fiber-optic systems fulfill niche preferences for radiation-free imaging, especially in pediatric and pregnant cohorts. Optical coherence tomography stretches into premium territory, offering micrometer-resolution cross-sections valuable for research and complex restorative planning.

Hardware and software convergence blurs category boundaries as fluorescence wands embed AI firmware and intraoral scanners bundle caries algorithms. Vendors secure FDA approvals not just for devices but for cloud-based engines spanning multiple imaging modalities, elevating value propositions beyond point solutions. Integrated product ecosystems synchronize detection data with digital treatment-planning suites, enhancing restorative accuracy and cementing customer lock-in. Vendors with modular upgrade paths such as firmware downloads that unleash new algorithms win favor among cost-conscious practices. Competitive differentiation increasingly hinges on cybersecurity credentials, uptime guarantees, and user-experience design rather than just hardware optics or laser wavelengths.

By End User: Ambulatory Centers Lead Growth

Dental clinics accounted for 56.02% of the dental caries detector market size in 2025, supported by broad patient bases and steady replacement cycles. Clinics rely on easy-to-operate fluorescence pens and plug-and-play AI packages that integrate with existing imaging suites. Hospitals sustain stable demand through trauma and oncology departments that need precise lesion mapping ahead of maxillofacial surgeries. Yet ambulatory surgical centers log the swiftest 12.15% CAGR, mirroring healthcare’s migration to outpatient venues that promise cost savings and faster scheduling. Ambulatory facilities integrate high-throughput scanners and AI dashboards to manage volume-driven models, shortening patient turnover while upholding diagnostic rigor.

Dental service organizations scale technology across multi-state footprints, leveraging centralized IT teams to manage AI updates and analytics dashboards. Academic institutes continue to incubate novel detection concepts, validating performance through randomized clinical trials that feed regulatory dossiers. Teledentistry platforms extend diagnostic reach to care deserts by funneling intraoral images from mobile hygiene units to centralized AI hubs for instant triage. Across all settings, the embrace of evidence-based preventive care aligns with insurers’ pay-for-performance programs, creating financial incentives to adopt technologies that reduce restorative burden downstream.

Geography Analysis

North America delivered 41.18% of 2025 sales, anchored by abundant private insurance, favorable reimbursement codes, and early FDA clearances for AI platforms. Dental-technology clusters around Boston, New York, and Silicon Valley funnel capital and talent into continuous product upgrades. Cross-border collaboration between U.S. device makers and Canadian dental service organizations accelerates rollout in both countries. The dental caries detector market share for North America remains resilient as group practices and DSOs deploy standardized diagnostics across hundreds of rooms.

Europe exhibits steady uptake despite stringent EU Medical Device Regulation (MDR) compliance costs. Germany, France, and the United Kingdom account for most regional orders, propelled by academic-industry partnerships that validate AI specificity under evidence-based protocols. Public health services in Scandinavia and the Netherlands reimburse for fluorescence-based preventive exams, nudging private practitioners toward similar tech stacks. Although MDR raises entry barriers for small manufacturers, it enhances patient confidence and reduces counterfeit imports, solidifying market baseline quality. The region’s focus on cross-border data privacy requires end-to-end encryption and GDPR-aligned cloud storage, influencing vendor selection criteria.

Asia-Pacific is the fastest-growing arena with a projected 11.74% CAGR. Urbanization in China and India unleashes middle-class demand for modern cosmetic and preventive dentistry. Government oral-health drives provide screening buses equipped with portable fluorescence devices that roam rural provinces. Japan spearheads technology adoption, while South Korean manufacturers export cost-effective transillumination units tailored for price-sensitive Southeast Asian clinics. Innovative financing leasing, pay-per-scan, and micro-loans facilitates adoption among smaller practitioners. Middle East & Africa and South America trail but show accelerating uptake as economic diversification funnels resources into primary healthcare and preventive dentistry infrastructure.

Competitive Landscape

The dental caries detector market features moderate fragmentation. Incumbents such as Dentsply Sirona, KaVo, Planmeca, and BIOLASE leverage large installed bases, but AI-centric disrupters like VideaHealth, Pearl, and Overjet chip away with subscription revenue models that scale rapidly. Hardware manufacturers respond by embedding partner AI engines, creating symbiotic alliances that marry optics to algorithms. In 2024, 3Shape integrated third-party AI modules into its TRIOS scanners, reporting a 53% surge in usage among digital dentistry adopters.

Competitive positioning is increasingly won on user-experience and regulatory readiness rather than raw technical specs. Firms with ISO-certified manufacturing, HIPAA-compliant clouds, and MDR class-IIb approvals attract institutional buyers in group practice and hospital networks. Patent arsenals remain strategic; BIOLASE maintains 266 active patents covering laser-tissue interaction and photoacoustic detection pathways, raising entry barriers for newcomers. Start-ups compensate by crowding into white-space niches at-home salivary biosensors, pediatric-specific AI datasets, and teledentistry APIs that incumbents find difficult to prioritize. Mergers and acquisitions are likely as established players seek to shore up portfolios before software-only providers capture outsized margin.

Strategic moves in 2024-2025 underscore the shift. VideaHealth deepened distribution via Dentalcorp and Henry Schein One, widening its footprint across multi-clinic networks. Pearl’s USD 58 million Series B fueled expansion into 120 countries, and Overjet’s rollout inside Dental Care Alliance’s 400 clinics signaled enterprise-level confidence in AI diagnostics. Hardware players pivot: KaVo announced a roadmap to integrate cloud analytics into its Spectra fluorescence line, while Planmeca unveiled chairside transillumination units designed for AI plug-ins. Competitive intensity therefore migrates from equipment price wars to ecosystem stickiness, recurring software revenue, and data stewardship.

Dental Caries Detector Industry Leaders

AdDent, Inc

Centrix, Inc.

Dentsply Sirona

DentLight, Inc.

Air Techniques, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: VideaHealth launched Caries 3.0 model featuring 65% reduction in false positives and 70% reduction in diagnostic variability, setting new standards for AI-powered caries detection accuracy and clinical reliability.

- November 2024: VideaHealth expanded partnerships with Dentalcorp Holdings and Henry Schein One to deploy AI diagnostic solutions across dental networks, enhancing patient care and practice performance through comprehensive detection capabilities and streamlined workflows.

- July 2024: Pearl secured USD 58 million in Series B funding, representing the largest investment in dental AI sector and enabling expansion of FDA-cleared diagnostic platforms across 120 countries.

- July 2024: Dental Care Alliance launched comprehensive rollout of Overjet's AI technology across over 400 dental practices, implementing FDA-cleared platform for detecting and quantifying oral diseases with enhanced patient education capabilities.

Global Dental Caries Detector Market Report Scope

As per the scope of this report, dental caries detectors are devices used for an early examination of any oral ailments, such as dental caries, enabling an effective treatment plan for the patient. The Dental Caries Detector Market is Segmented by Product (Laser Fluorescent Caries Detector, Fiber Optic Trans-illumination Caries Detector), End-user (Hospitals, Dental Clinics, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD million) for the above segments.

| Laser Fluorescence Devices |

| Near-Infrared Transillumination Devices |

| Fiber-Optic Transillumination Devices |

| Optical Coherence Tomography Systems |

| Photothermal Radiometry & Modulated-Luminescence Devices |

| AI-Based Imaging Software & Platforms |

| Hospitals |

| Dental Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Laser Fluorescence Devices | |

| Near-Infrared Transillumination Devices | ||

| Fiber-Optic Transillumination Devices | ||

| Optical Coherence Tomography Systems | ||

| Photothermal Radiometry & Modulated-Luminescence Devices | ||

| AI-Based Imaging Software & Platforms | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the dental caries detector market?

The dental caries detector market size stands at USD 414.56 million in 2026 and is forecast to reach USD 612.51 million by 2031.

How fast is growth expected over the forecast period?

The market is projected to expand at an 8.12% CAGR between 2026 and 2031, driven by AI integration, fluorescence advances, and preventive-care policies.

Which product segment leads in revenue?

Laser fluorescence devices hold the largest 45.73% share, buoyed by clinical familiarity and immediate chairside usability.

Which end-user segment is expanding the quickest?

Ambulatory surgical centers are growing at a 12.15% CAGR as dental services decentralize into outpatient settings.

Why is Asia-Pacific considered the most promising region?

Rising middle-class populations, public oral-health campaigns, and creative financing models support a projected 11.74% regional CAGR.

How do AI platforms improve diagnostic outcomes?

AI reduces diagnostic variability by up to 70% and cuts false positives by 65%, boosting patient trust and treatment acceptance rates.

Page last updated on: