Global Dental Floss Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

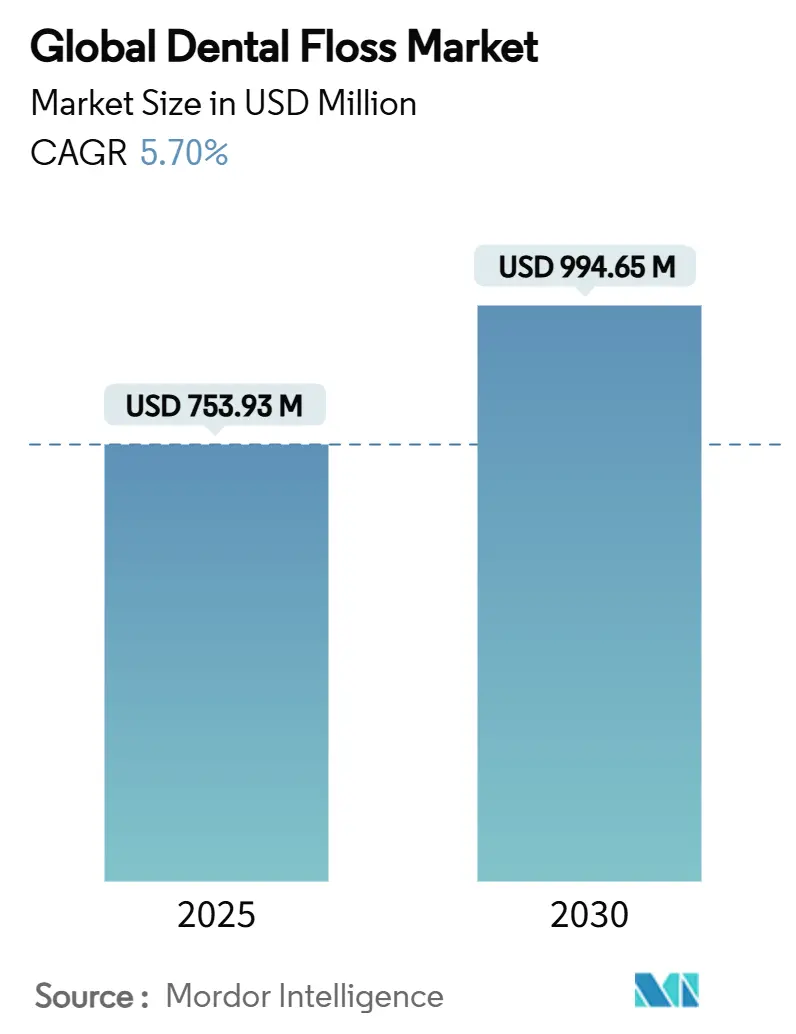

| Market Size (2025) | USD 753.93 Million |

| Market Size (2030) | USD 994.65 Million |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

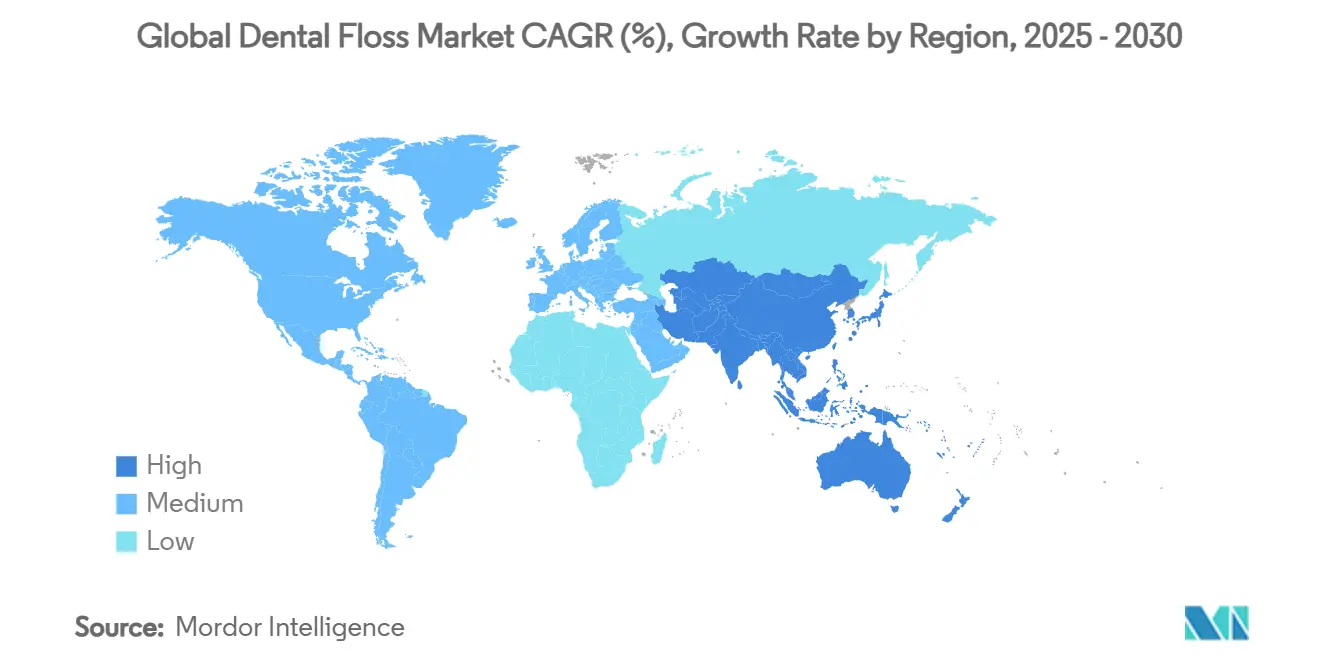

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Dental Floss Market Analysis by Mordor Intelligence

The dental floss market is valued at USD 753.93 million in 2025 and is forecast to reach USD 994.65 million by 2030, expanding at a 5.70% CAGR. The growth reflects resilient demand for preventive oral-care products despite regulatory scrutiny and shifting consumer preferences toward sustainable solutions. Escalating periodontal disease prevalence—now affecting more than 1 billion people—continues to anchor product adoption.[1]Sunstar, “The Global Burden of Periodontal Diseases,” sunstar.com Waxed floss remains the preferred format, but specialty designs such as super floss and orthodontic threaders are gaining momentum as orthodontic procedures rise. Materials innovation is accelerating as manufacturers replace PTFE with PLA, silk and other bioplastics in response to statewide PFAS bans in the United States. Digital buying behavior is transforming access; online platforms now represent the fastest-growing distribution route, supported by subscription services and social-commerce promotions. Regionally, the dental floss market benefits from stable demand in North America and rapid uptake across Asia-Pacific, where rising incomes and dental-tourism programs are widening prophylaxis awareness.

Key Report Takeaways

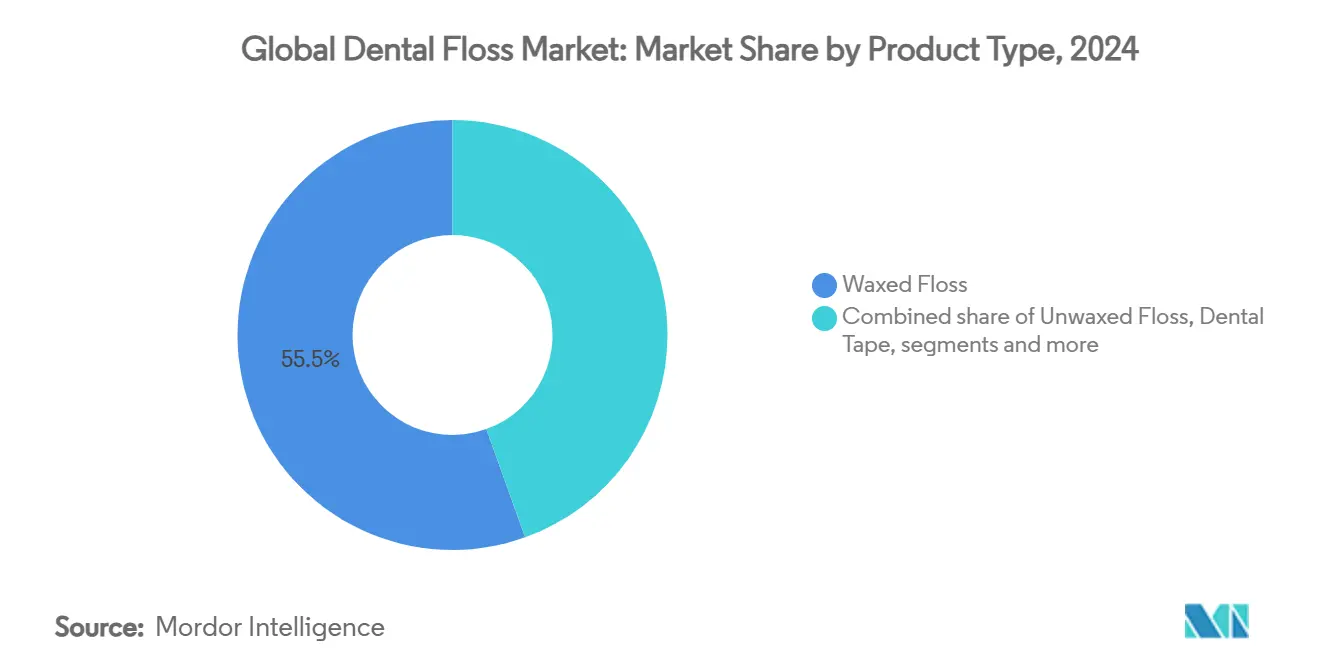

- By product type, waxed floss led with 55.48% of the dental floss market share in 2024, while the “Others” category is advancing at a 7.18% CAGR through 2030.

- By material, nylon held 32.42% of the dental floss market size in 2024, whereas PLA and other bioplastics are projected to expand at a 6.88% CAGR between 2025-2030.

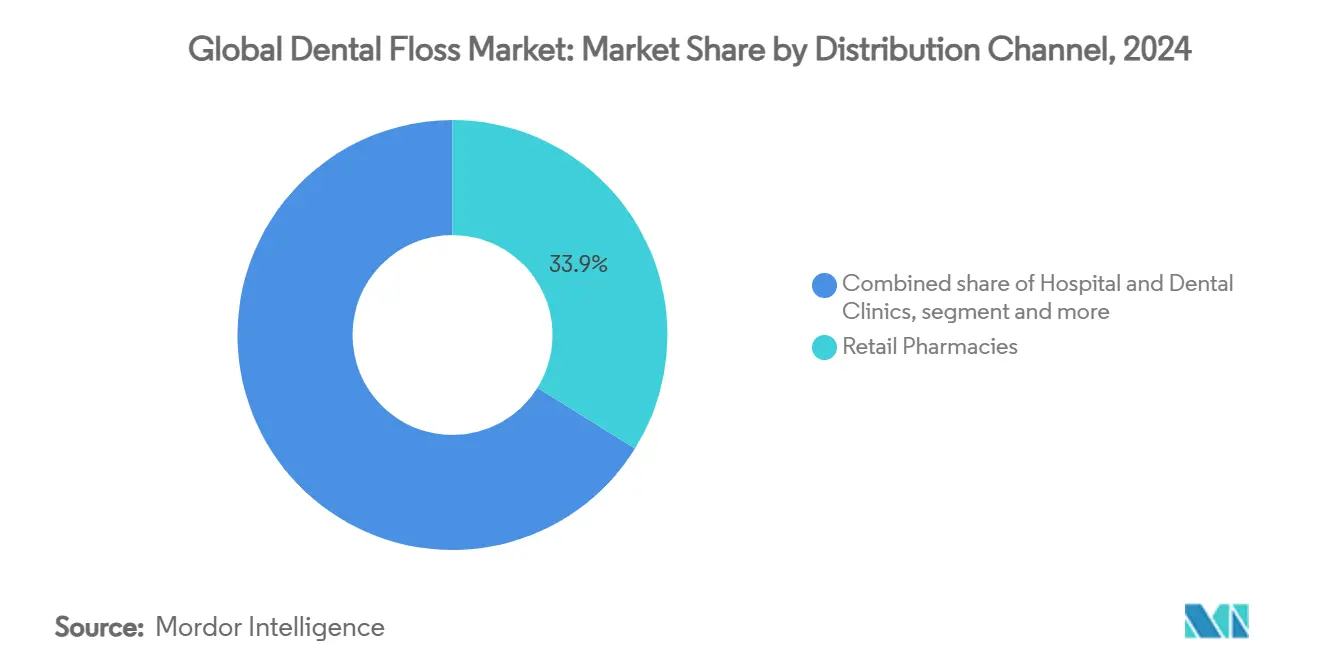

- By distribution channel, retail pharmacies accounted for 34.58% of revenue in 2024; online/e-commerce is forecast to post the highest CAGR at 7.32% to 2030.

- By age group, adults represented 54.74% of consumption in 2024, but the pediatrics segment is set to grow the fastest at 7.44% CAGR.

- By geography, North America commanded 39.33% of revenue in 2024, whereas Asia-Pacific is projected to record the strongest regional CAGR at 7.62% through 2030.

Global Dental Floss Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of oral hygiene | +1.2% | Global; higher in APAC & Latin America | Medium term (2-4 years) |

| Growing prevalence of periodontal diseases & cavities | +1.5% | Global; severe in South Asia & Sub-Saharan Africa | Long term (≥ 4 years) |

| Expansion of e-commerce & DTC oral-care brands | +0.8% | North America & Europe; fast adoption in APAC | Short term (≤ 2 years) |

| Innovative flavors & eco-friendly floss formats | +0.7% | North America & Europe; urban APAC | Medium term (2-4 years) |

| Preventive dental-care reimbursement policies | +0.5% | North America & Europe; expanding to APAC | Long term (≥ 4 years) |

| Growth in dental tourism boosting prophylaxis demand | +0.4% | APAC core; spill-over to MEA & Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness of Oral Hygiene

Seventy-four percent of American adults now follow complete oral-hygiene regimens that include interdental cleaning, underscoring a cultural shift from treatment to prevention. Emerging markets echo this trend: Malaysia’s National Oral Health Strategic Plan 2022-2030 addresses data showing 94% of adults experience gum issues, catalyzing educational initiatives.[2]International Trade Administration, “Malaysia Healthcare Outlook,” trade.gov Social-media health narratives have reframed flossing as a lifestyle practice tied to overall wellness and appearance. Younger consumers amplify this effect by sharing routines online, normalizing premium floss and accessory purchases. Institutional messaging from dental associations further reinforces daily flossing, tightening the link between public-health campaigns and retail demand.

Growing Prevalence of Periodontal Diseases & Cavities

Severe periodontitis affects 12.50% of the global population and is forecast to impact 1.56 billion people by 2050, heightening the urgency for interdental cleaning. In low-resource regions, diet changes and limited dental access accelerate disease incidence. Global dental-disorder cases among young adults rose 17.1% from 1990 to 2021, reaching 643.3 million. Medical research linking gum inflammation to systemic conditions such as diabetes drives clinicians to prescribe daily flossing, sustaining core demand in the dental floss market. Governments increasingly recognize the economic burden of oral disease, embedding flossing guidance into national health programs.

Expansion of E-commerce & DTC Oral-care Brands

Online sales channels are growing at a 7.32% CAGR, the fastest among all outlets. Direct-to-consumer pioneers demonstrate scale: one leading brand generated USD 1.04 million in single-month revenue during 2024, validating the channel’s profitability. Subscription models ensure replenishment consistency and encourage habitual use, while targeted ads personalize product discovery. Digital platforms also reduce entry barriers for niche eco-friendly brands, intensifying competitive variety. The outcome is a more fragmented yet vibrant dental floss market that rewards agility and community engagement.

Innovative Flavors & Eco-friendly Floss Formats

Product differentiation now hinges on sustainability credentials and sensory appeal. Silk, bamboo fiber and PLA filaments limit plastic exposure and comply with PFAS bans, attracting environmentally minded consumers. Flavor diversification moves beyond mint to include strawberry, orange and coconut, improving user experience and adherence. Research institutes add a technological dimension; a prototype smart floss measures cortisol in saliva, opening pathways for real-time health monitoring. The innovation pipeline positions premium, multifunctional floss as both a cleansing and diagnostic tool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of substitutes (interdental brushes, water flossers) | -1.1% | Global; higher in developed markets | Medium term (2-4 years) |

| Environmental concerns around plastic-based floss | -0.6% | North America & Europe; expanding to APAC | Long term (≥ 4 years) |

| Fluoropolymer regulation limiting PTFE supply | -0.8% | North America leading; Europe following | Short term (≤ 2 years) |

| Skepticism over clinical efficacy of flossing | -0.3% | Global; higher in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitutes (Interdental Brushes, Water Flossers)

Clinical trials show water flossers remove plaque up to 2 times more effectively than traditional string floss, intensifying competitive pressure. A 2025 randomized study confirmed superior outcomes for water-jet devices in reducing gingival bleeding, particularly for orthodontic patients and seniors. Convenience compounds their appeal; automated pulsation sidesteps the manual dexterity required for string floss. Some dental professionals now recommend brushes or irrigators as first-line tools, potentially diverting a portion of the dental floss market. Nevertheless, cost, portability and disposability still favor traditional floss for everyday users, containing but not eliminating the threat.

Environmental Concerns Around Plastic-based Floss

Minnesota’s Amara’s Law banned PFAS-containing dental floss on 1 January 2025, compelling nationwide manufacturers to pivot toward safer materials. Colorado enacted comparable measures in May 2025, with further state proposals under review. The legislative environment raises production costs and complicates supply chains as firms retool assets and validate alternative filaments. Consumer watchdog evaluations listing PFAS-free products amplify public scrutiny. Brands that fail to transition face reputational risk and lost shelf space, dampening overall category growth during the adjustment period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Waxed Dominance Faces Innovation Challenge

Waxed floss captured 55.48% of the dental floss market share in 2024, reflecting widespread familiarity and smooth gliding benefits for users with tight contacts. The segment retains strong momentum in pharmacies and supermarkets where incumbent brands maintain prominent shelf presence. At the same time, the “Others” group—covering super floss, threaders and electric picks—is projected to expand at a 7.18% CAGR. The dental floss market size for these specialty products is buoyed by rising orthodontic treatments and specific clinical needs. Manufacturers respond with hybrid constructions combining micro-textured strands and flavored coatings that improve plaque capture without sacrificing comfort. Technological breakthroughs such as embedded sensors hint at future product categories that integrate oral-health diagnostics, positioning innovation as the lever that could erode waxed floss hegemony.

Novel formats already claim mindshare among early adopters. Direct-to-consumer firms introduce compact rechargeable tools that reciprocate or vibrate at sonic frequencies, targeting users with limited dexterity. Dental professionals increasingly recommend differentiated floss for implants or bridges, broadening specialty uptake. As a result, waxed variants must innovate on sustainability or added functionality to preserve relevance. Premium line extensions featuring compostable coatings and natural flavors illustrate how legacy brands are repositioning within the evolving dental floss market.

By Material: Nylon Leadership Threatened by Sustainable Alternatives

Nylon accounted for 32.42% of the dental floss market size in 2024 thanks to proven strength and low unit costs. Supply chains are mature, allowing high-volume production for global distribution. Yet regulatory headwinds have intensified: fluoropolymer scrutiny limits PTFE coatings often paired with nylon, increasing compliance burdens. Bioplastic PLA and other plant-derived polymers are growing at a 6.88% CAGR, signaling a meaningful substitution trend. Silk and bamboo fibers, though smaller in volume, capitalize on plastic-free positioning and biodegradability to attract eco-conscious buyers.

Consumer Reports highlighted multiple silk and PLA floss products that meet efficacy benchmarks without detectable PFAS, accelerating retailer adoption. Subscription services emphasize compostable packaging to reinforce environmental credentials. To maintain share, nylon producers explore bio-nylon blends and solvent-free coatings, balancing performance with green claims. Long-term competitiveness hinges on securing PFAS-compliant supply and educating consumers on the recyclability of emerging materials.

By Distribution Channel: Digital Transformation Accelerates Pharmacy Disruption

Retail pharmacies held 34.58% of revenue in 2024, benefiting from in-store consultation and immediate product availability. However, online platforms exhibit the strongest momentum at a 7.32% CAGR, reflecting wider e-commerce adoption and convenience demand. The dental floss market now features influencer-driven launches timed to social-media events, propelling rapid sell-outs and waitlists. Subscription models lock in repeat sales while offering personalization features such as flavor variety packs and refill reminders.

Traditional retailers respond by integrating click-and-collect services and expanding private-label assortments that undercut premium online price points. Supermarkets bundle floss with toothpaste multipacks to defend impulse-buy share. Dental clinics, though smaller on absolute volume, exert outsized influence through chairside recommendations and post-procedure sample giveaways. Over the forecast horizon, omnichannel strategies blending pharmacist credibility with digital convenience are expected to define winning plays in the dental floss market.

By Age Group: Adult Stability Contrasts with Pediatric Acceleration

Adults comprised 54.74% of global volume in 2024, underpinned by routine purchasing habits and willingness to trade up to premium lines. Education campaigns highlighting links between gum health and systemic diseases sustain adult commitment to daily interdental cleaning. In contrast, the pediatric cohort is projected to rise at a 7.44% CAGR as schools and pediatric dentists reinforce early habits. Flavor innovation and kid-friendly packaging convert parental intentions into regular usage.

Lion Corporation’s strategy to lift floss adoption from 38% to 50% of the Japanese population by 2030 focuses heavily on youth outreach, illustrating the segment’s strategic value. Elderly users create parallel opportunities for ergonomic aids and gentler coatings that accommodate gum sensitivity. As life expectancy climbs, geriatric oral-care needs will further diversify product portfolios, sustaining multi-segment growth in the dental floss market.

Geography Analysis

North America led with 39.33% revenue share in 2024, anchored by high oral-health literacy, broad insurance coverage and sophisticated retail infrastructure. PFAS restrictions in Minnesota and Colorado elevate compliance costs but simultaneously push product upgrades that fuel premium pricing. The region’s consumer base demonstrates readiness to pay for sustainable innovations, reinforcing a trend toward high-margin launches. Competitive advertising and loyalty programs keep replacement rates stable even as water-flosser penetration climbs.

Asia-Pacific is the fastest-growing region at 7.62% CAGR through 2030. Rising disposable incomes, large untreated patient pools and flourishing dental-tourism hubs propel demand. Malaysia’s oral-care market, estimated to reach USD 2.8 billion by 2027, exemplifies regional momentum. China and India deliver scale through expanding middle classes, while South Korea and Japan shape premium niches with tech-centric products. Public-health drives, such as nationwide gum-disease screening campaigns, make floss an accessible and cost-effective preventive measure.

Europe maintains a sizable share, distinguished by stringent environmental regulation that accelerates uptake of biodegradable floss and refillable dispensers. Retailers prioritize eco-label accreditation, prompting rapid shelf turnover toward silk and PLA lines. South America and the Middle East & Africa offer emergent opportunities, though growth is tempered by economic volatility and uneven dental-care infrastructure. Nonetheless, high periodontal disease prevalence signals latent demand, positioning these regions as long-term contributors to dental floss market expansion.[3]SSRN, “Regional Variations in Periodontal Burden,” ssrn.com

Competitive Landscape

The dental floss market remains moderately fragmented. Procter & Gamble, Johnson & Johnson and Colgate-Palmolive command global reach and leverage cross-category brand equity to sustain front-of-shelf presence. In 2024 Procter & Gamble earmarked incremental R&D funding for premium oral-care innovations, citing floss as a priority category. Johnson & Johnson accelerates ingredient transparency programs to align with PFAS-free mandates, while Colgate-Palmolive bundles floss with smart toothbrush ecosystems to raise average transaction values.

Challenger brands such as Cocolab, The Humble Co. and Seek Bamboo capitalize on direct-to-consumer channels and sustainability narratives to attract younger, environmentally conscious buyers. Cocolab’s 2024 rebrand expanded flavor assortments and introduced a refill subscription that reduced plastic by 80%. Tech entrants heighten competitive pressure: the Proclaim Custom-Jet Oral Health System entered more than 700 dental practices in 2024, blurring lines between professional equipment and home use.

M&A remains a strategic lever. Large incumbents evaluate bolt-on acquisitions to access patented bioplastic technologies and DTC analytics capabilities. Partnerships with dental-practice networks facilitate clinical endorsements that sway consumer choice at point of care. Marketing spend increasingly shifts toward social commerce and micro-influencer collaborations, reflecting shifting media consumption habits.

Global Dental Floss Industry Leaders

Procter & Gamble

Colgate-Palmolive Company

Prestige Consumer Healthcare, Inc.

Johnson & Johnson Services, Inc

Perrigo Company plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tufts University researchers unveiled smart dental floss that detects cortisol in saliva for stress monitoring, using electropolymerized molecularly imprinted polymers with smartphone connectivity.

- May 2025: Colorado extended its PFAS ban to include dental floss, menstrual and cooking products, intensifying compliance demands.

- January 2025: Minnesota enacted a full PFAS prohibition on dental floss under Amara’s Law, the first U.S. state to implement such restrictions.

- April 2024: Slate Electric Flosser launched, featuring 12,000 sonic vibrations per minute and orthodontic attachments for users with dexterity challenges.

Global Dental Floss Market Report Scope

Dental floss is a cord of thin filaments used to remove food and dental plaque from between teeth in areas a toothbrush cannot reach. The dental floss market is segmented by product (waxed floss, unwaxed floss, and other products), sales channel (retail pharmacies, hospital pharmacies, and online), and geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report offers the value (in USD million) for the above segments.

| Waxed Floss |

| Unwaxed Floss |

| Dental Tape |

| Super Floss & Orthodontic Threaders |

| Others |

| Nylon |

| PTFE (Teflon) |

| Silk |

| UHMWPE |

| PLA & Other Bioplastics |

| Retail Pharmacies |

| Hospital & Dental Clinics |

| Supermarkets/Hypermarkets |

| Online/E-Commerce |

| Others |

| Adults |

| Pediatrics |

| Geriatrics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Waxed Floss | |

| Unwaxed Floss | ||

| Dental Tape | ||

| Super Floss & Orthodontic Threaders | ||

| Others | ||

| By Material | Nylon | |

| PTFE (Teflon) | ||

| Silk | ||

| UHMWPE | ||

| PLA & Other Bioplastics | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital & Dental Clinics | ||

| Supermarkets/Hypermarkets | ||

| Online/E-Commerce | ||

| Others | ||

| By Age Group | Adults | |

| Pediatrics | ||

| Geriatrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the dental floss market?

The dental floss market is worth USD 753.93 million in 2025 and is projected to reach USD 994.65 million by 2030 at a 5.70% CAGR.

Which product type leads the dental floss market?

Waxed floss leads with 55.48% share in 2024, though specialty products are expanding faster at a 7.18% CAGR.

Why are PFAS bans important to dental floss manufacturers?

State-level PFAS bans in Minnesota and Colorado require reformulation away from PTFE-coated floss, increasing R&D and compliance costs.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, expected to post a 7.62% CAGR through 2030 due to rising incomes and expanding dental tourism.

How is e-commerce impacting sales channels?

Online platforms are the fastest-growing channel, registering a 7.32% CAGR as subscription models and social commerce shift buying behavior.

Page last updated on: