Europe Bulky Waste Collection Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

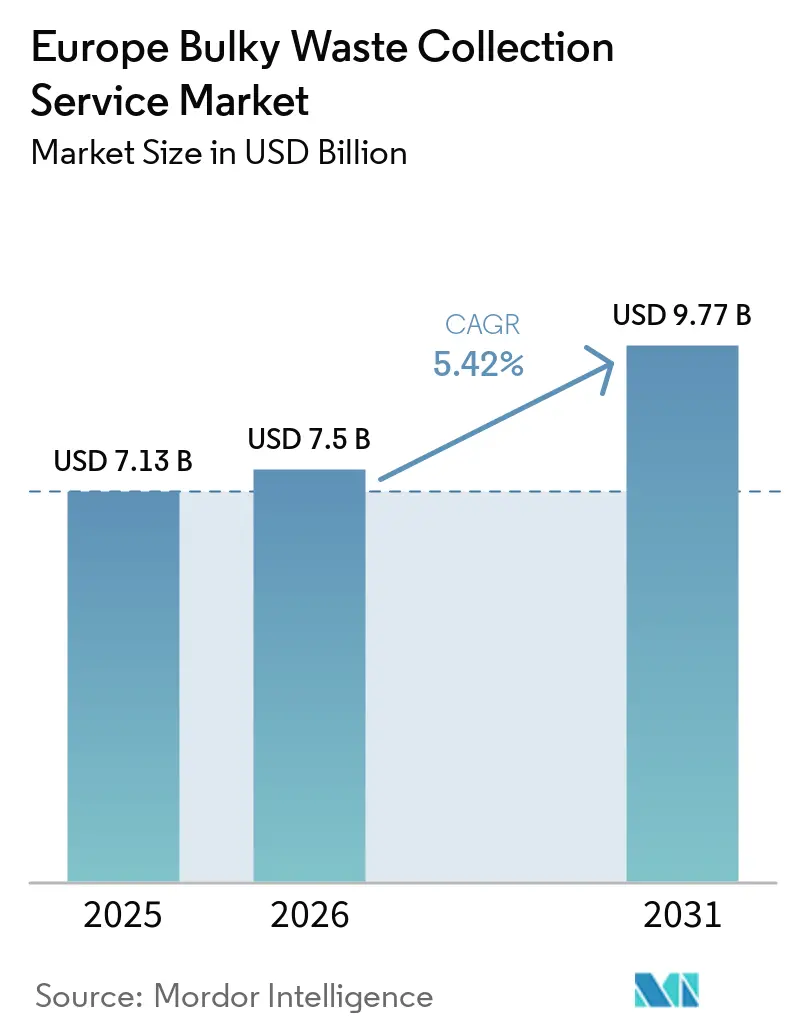

| Base Year Market Size (2025) | USD 7.13 Billion |

| Market Size (2026) | USD 7.5 Billion |

| Market Size (2031) | USD 9.77 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

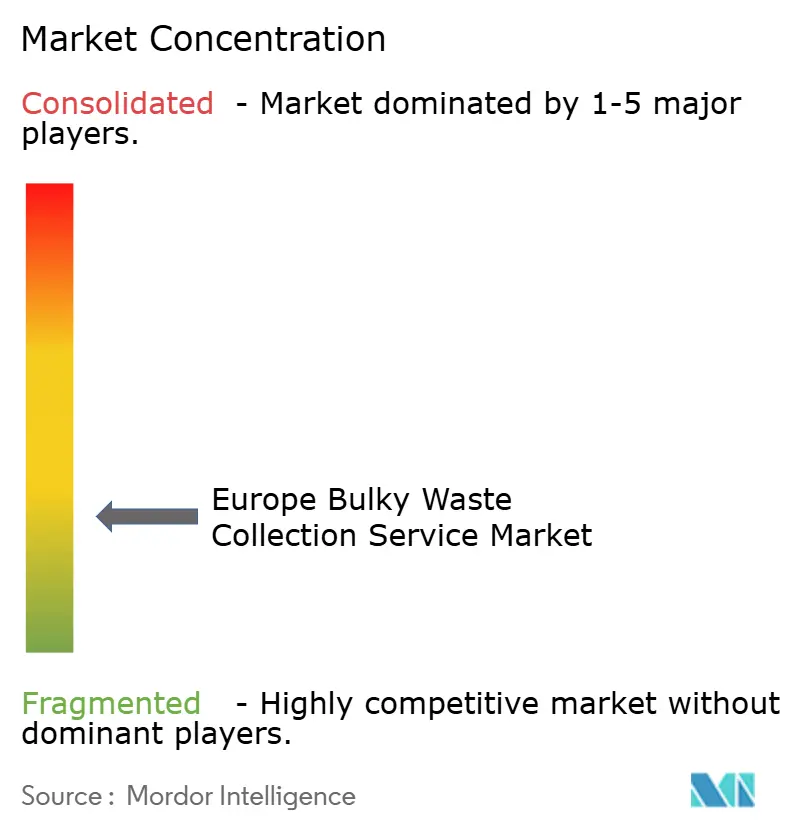

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bulky Waste Collection Service Market Analysis by Mordor Intelligence

The Europe Bulky Waste Collection Service Market size is projected to expand from USD 7.13 billion in 2025 and USD 7.5 billion in 2026 to USD 9.77 billion by 2031, registering a CAGR of 5.42% between 2026 to 2031.

Tightening European Union circular-economy policies and real-time digital tracking requirements are shifting cost curves and rewarding operators that invest in compliance-grade technology. Municipalities are aligning budgets and procurement to drive higher landfill diversion, while large private operators pursue route optimization, fleet electrification, and data-led service models to protect margins. Platform-based, on-demand models are scaling across dense urban clusters to meet rising expectations for convenience and speed. Adjacent value creation in reuse, recycling, and energy recovery is becoming integral as the Europe bulky waste collection service market shifts from simple haulage to integrated resource management.

Key Report Takeaways

- By source, residential accounted for a 60.23% share in 2025 and is advancing at a 6.21% CAGR through 2031.

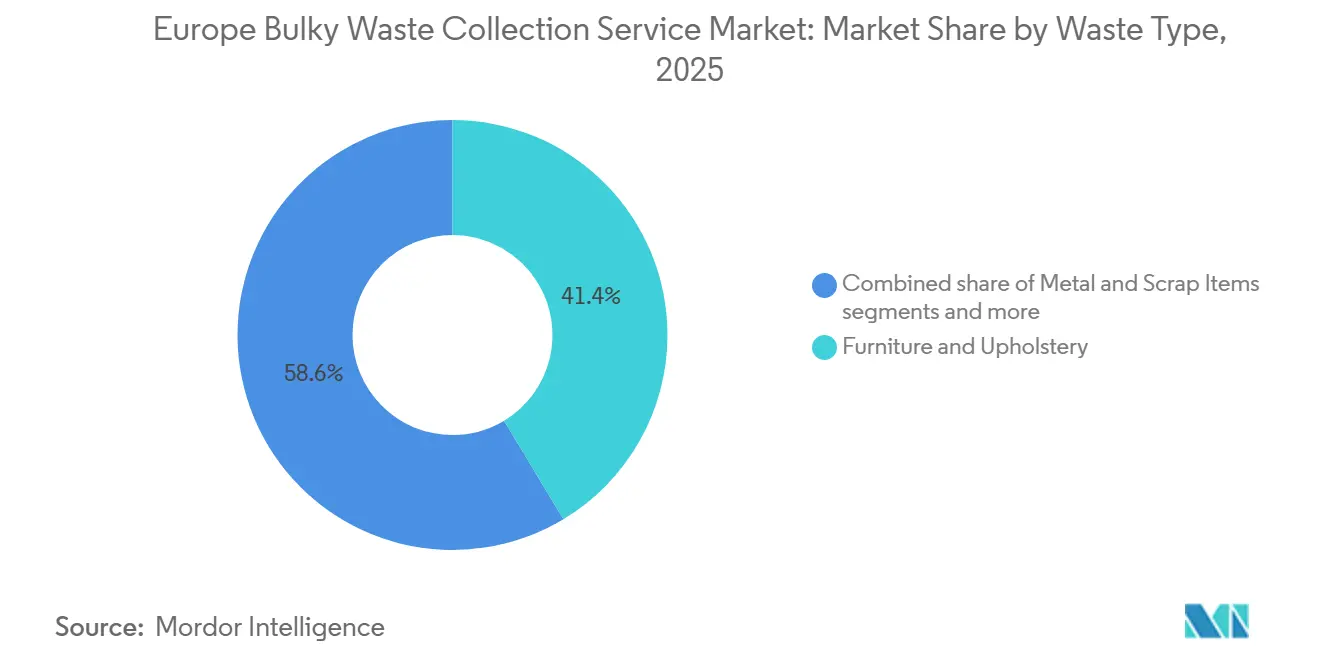

- By waste type, furniture and upholstery accounted for 41.37% of the Europe bulky waste collection service market size in 2025 and are growing at a 6.41% CAGR through 2031.

- By geography, Germany held 20.62% of the Europe bulky waste collection service market share in 2025, while Spain recorded the highest projected CAGR at 6.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Bulky Waste Collection Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing renovation and refurbishment activities across residential and commercial sectors | +1.7% | Germany, France, Netherlands, Italy, and Spain; expanding across EU-27 | Short to medium term (1-3 years) |

| Stringent European Union waste management regulations and circular economy policies | +1.5% | European Union-wide, harmonized across member states | Long term (≥ 4 years) |

| Rising adoption of smart waste management technologies | +1.2% | Western Europe core, expanding to CEE | Medium term (2-4 years) |

| Increasing urbanization and household waste generation | +0.9% | Urban hubs in Germany, the United Kingdom, France, and Spain | Long term (≥ 4 years) |

| Expansion of municipal waste collection programs | +0.6% | Southern and Eastern Europe, rural catchment areas | Medium term (2-4 years) |

| Growing environmental awareness among European consumers | +0.4% | The Nordic countries, Germany, and the Netherlands are spread across the European Union. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Renovation and Refurbishment Activities Across Residential and Commercial Sectors

The European bulky waste collection service market is growing significantly, driven by increased renovation and refurbishment activities in residential and commercial properties. Post-COVID-19, home improvement spending has surged, with countries such as France, Germany, Spain, and Italy reporting 15-20% annual growth in renovation permits driven by remote work trends and energy-efficiency upgrades. Residential renovations generate 2-5 tons of bulky waste per project, including old fixtures, flooring, appliances, and furniture, requiring specialized disposal services. EU energy efficiency initiatives, such as the Energy Performance of Buildings Directive (EPBD), and subsidy programs in Germany, France, and the Netherlands have further boosted renovation rates, thereby contributing to increased bulky waste volumes. Commercial refurbishments, driven by hybrid work models and redesigns in offices, retail, hotels, and restaurants, add to this waste, including partition walls, fixtures, and outdated equipment. With 35% of European buildings constructed before 1970, aging properties require ongoing maintenance, sustaining demand for waste collection services. Municipalities and private operators are expanding services such as on-demand pickups and sorting facilities to manage mixed bulky waste, driven by regulatory pressures, demographic trends, and the lifecycle of Europe’s built environment.

Stringent European Union Waste Management Regulations and Circular Economy Policies

The European Union is implementing the most comprehensive waste reforms in years, with provisions that reshape roles across the chain from producers to collectors. The revised Waste Framework Directive entered into force in October 2025 and includes requirements such as Extended Producer Responsibility for textiles on a set timetable and targets to reduce food waste, creating upstream pressure that ultimately affects sorting and collection practices. The Digital Waste Shipment System requires near real-time tracking for intra-European Union waste movements from May 2026, enabling better enforcement and closing gaps that previously allowed misclassification to avoid recycling obligations. Packaging reforms continue to advance toward recyclability grading and domain-specific obligations that will accelerate material redesign and downstream separation. These changes reward operators who can manage data integrity, certification, and sorting quality across bulky waste streams. They also set a higher baseline for compliance that will influence bids, pricing, and technology adoption in the Europe bulky waste collection service market.

Rising Adoption of Smart Waste Management Technologies

Digitization is scaling from pilots to mainstream deployment in major municipalities and private networks. Evidence from European deployments shows that fill-level sensors and analytics-led route optimization can reduce unnecessary trips and road use, supporting measurable cost savings and emissions reductions for operators and city clients. SUEZ’s use of real-time monitoring across its collection networks illustrates how data can trigger pickups when bins approach capacity, rather than on fixed schedules. Smart access systems, incentive-based tariffs, and integrated fleet management are being bundled as comprehensive platforms through strategic partnerships that support municipal modernization agendas. Adoption curves remain steeper in Western Europe than in parts of Central and Eastern Europe, where capital constraints are a barrier. As more public tenders require digital reporting and performance metrics, technology capability is increasingly a prerequisite in the Europe bulky waste collection service market.

Increasing Urbanization and Household Waste Generation

Rising household consumption and denser living patterns are concentrating bulky waste in urban corridors where collection windows and curb space are limited. Municipal solid waste generation reached 517 kg per capita in 2024 across the European Union, up 8% from 2014, with high-income countries such as Denmark and Austria at the upper end of the distribution. Cities face recurring mismatches between fixed collection schedules and the actual disposal timing of items such as sofas and appliances, which drive demand for on-demand services that can respond quickly. The Europe bulky waste collection service market is adapting to these behavioral patterns through hybrid scheduling, improved communication, and more granular service tiers. Regions with advanced pay-as-you-throw schemes show that economic signals can reduce residual waste, yet bulky item turnover linked to housing churn continues to challenge capacity planning. These urban dynamics increasingly shape resource allocation decisions, fleet profiles, and yard operations among public and private operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Illegal dumping and non-compliance issues | -0.9% | CEE, Southern Europe, pockets in the United Kingdom | Short term (≤ 2 years) |

| High operational costs of specialized collection equipment | -0.6% | European Union-wide, acute in high-cost labor markets | Short term (≤ 2 years) |

| Budget constraints faced by municipal authorities | -0.5% | CEE, peripheral regions in Southern Europe | Medium term (2-4 years) |

| Limited infrastructure in rural and remote areas | -0.3% | Rural Spain, Romania, Poland, and the Scottish Highlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Illegal Dumping and Non-Compliance Issues

Waste crime and non-compliance erode legitimate operators’ pricing and undermine environmental goals. In England, authorities have documented significant financial losses from waste crime and introduced a multi-year plan that funds digital waste tracking and expands enforcement tools to deter illegal activity.[1]Government of the United Kingdom, “Waste Crime Action Plan,” GOV.UK, gov.uk The plan includes measures to improve data, surveillance, and permitting oversight, signaling an enforcement shift toward data-driven deterrence and earlier intervention. At the global level, multilateral bodies have highlighted the scale and complexity of waste trafficking, which complicates accountability along the supply chain and imposes additional compliance costs on lawful collectors.[2]United Nations Office on Drugs and Crime, “Waste Crime and Trafficking,” UNODC, unodc.org These patterns create near-term pricing pressure in regions with persistent enforcement gaps. Over time, digital tracking requirements and coordinated cross-border action can improve baseline compliance, which should benefit aligned operators in the Europe bulky waste collection service market.

High Operational Costs of Specialized Collection Equipment

Bulky waste handling requires vehicles and equipment capable of safely and efficiently handling irregular, heavy items, which increases capital and operating expenses. In high-income regions, operating costs per tonne are structurally higher, and specialized bulky waste services add additional layers of cost linked to manual handling and lower payload utilization. Local authority data show budget sensitivity to even limited service additions, which can challenge contract economics if inflation or fuel volatility persists.[3]North London Waste Authority, “Finance Update,” NLWA, nlwa.gov.uk Infrastructure constraints also matter, since not all facilities accept certain pre-treated bulky fractions if they alter throughput performance or emissions profiles. Operators are investing in in-cab technology and smaller vehicles suited for narrow urban streets, often tied to climate commitments in local tenders, which can raise upfront costs even as they improve long-run efficiency. These cost realities shape pricing, capex cycles, and rollout decisions in the Europe bulky waste collection service market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

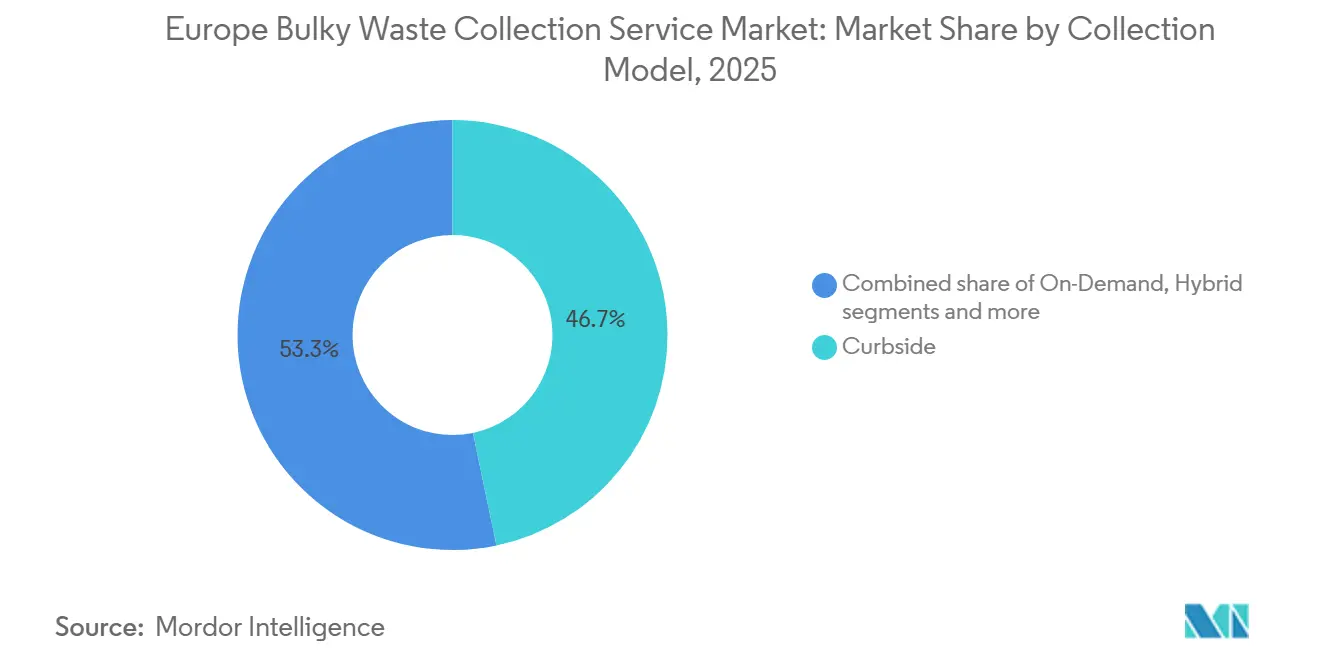

By Collection Model: Digital Platforms Disrupt Legacy Curbside Dominance

Curbside collection held 46.72% share in 2025, while on-demand services are projected to advance at a 5.82% CAGR through 2031 as convenience expectations rise in dense cities. This divergence reflects a broader shift in service design, where app-based booking and shorter response times are no longer optional in metropolitan areas. Hybrid models that blend fixed routes with on-call capacity are gaining favor because they protect route density while enabling flexible surge response. Digital capabilities, including GPS tracking and dynamic scheduling, are becoming a baseline requirement in large municipal tenders in the Europe bulky waste collection service market. Operators that standardize data capture and proof-of-service improve billing accuracy, audit readiness, and customer satisfaction.

Curbside’s resilience stems from network effects in established corridors, where optimized routes lower unit costs at scale. Tender specifications increasingly embed sustainability and reporting clauses, and recent public contracts illustrate the shift toward electric or right-sized vehicles and advanced in-cab systems to meet local climate goals. App-based platforms compete through service granularity and transparent pricing, with the most durable gains in high-density neighborhoods. Municipal drop-off networks and access-controlled sites can complement curbside by relieving pressure during peak disposal periods. As compliance and performance reporting converge, selection of the collection model in the Europe bulky waste collection service market will balance cost, responsiveness, and data integrity.

By Source: Residential Surge Outpaces Commercial Maturity

Residential sources accounted for 60.23% of total volume in 2025 and are the fastest-growing segment at a 6.21% CAGR, reflecting steady increases in per-capita municipal waste and shorter replacement cycles for home goods. Higher turnover in urban rental markets and e-commerce-enabled purchasing drive increased bulky-item disposal, especially for mattresses, sofas, and white goods. Commercial and industrial sources show more measured growth, supported by waste minimization programs and circular procurement that slow asset obsolescence. Public facilities add episodic surges tied to refurbishment and seasonal maintenance. As households remain the anchor of demand, residential service design is becoming the reference point for routing, communications, and capacity planning across the Europe bulky waste collection service market.

Geographic differences are visible in household waste patterns, with some countries demonstrating stronger diversion and prevention through pay-as-you-throw policies and deposit-return systems. Commercial generators increasingly require tailored pickups for retail fixtures and equipment governed by WEEE rules, which adds complexity to scheduling and treatment. Municipal and government sources, while smaller in share, often dictate operating parameters for mixed urban networks through funding and infrastructure. The Europe bulky waste collection service industry is adapting by introducing tighter service tiers that align pickup windows, vehicle selection, and fee structures with source-specific needs. Over the forecast period, operators that integrate residential and commercial demand on shared, data-optimized routes will improve asset utilization and service quality.

By Waste Type: Furniture Dominance Masks Shifting Material Composition

Furniture and upholstery accounted for 41.37% in 2025 and are projected to grow at a 6.41% CAGR, driven by fast-furniture dynamics that shorten product life cycles. This category requires specialized handling and pre-treatment, especially when composite materials and foams are involved, which raises processing costs relative to single-material streams. Large appliances are significant contributors and require dedicated handling under WEEE obligations, which shape collection design and cost allocation. Metal and scrap items deliver higher salvage value in markets with secondary buyers, creating offset opportunities that can improve unit economics. As product designs evolve to meet recyclability thresholds, collectors will face new sorting demands and opportunities in the Europe bulky waste collection service market.

Evidence from country profiles shows significant material recovery potential when infrastructure and reuse ecosystems are in place, including the repair, refurbishment, and resale of furniture. Textiles-related rules under the revised Waste Framework Directive will further separate certain soft goods from mixed bulky streams, adding operational steps and reporting needs for compliant collectors. Over time, design-for-disassembly will help downstream processing, but interim complexity will persist as legacy items continue to flow into the stream. Leading operators are building capabilities in sorting and baling, and are partnering with recyclers and refurbishes to capture material value. These moves position the Europe bulky waste collection service market to evolve from a disposal-centric to a value-recovery model.

Geography Analysis

Germany accounted for 20.62% of demand in 2025, supported by high per-capita waste generation and a mature network spanning dense urban areas and rural regions. Spain is projected to be the fastest-growing market, with a 6.78% CAGR, as regions invest in selective collection systems and modernization programs supported by European Union funds. France is scaling separate sorting and smart platform deployments that integrate access control, fill monitoring, and optimized routing, which is likely to increase performance expectations in new contracts. The United Kingdom is channeling producer fees to improve local services and increase investment in sorting and processing capacity over the decade.

Regional policies and enforcement signal different paths to improved performance. Digital waste-tracking rules from May 2026 aim to strengthen intra-Union shipment oversight, supporting quality and transparency across borders. Authorities are pairing infrastructure funding with clear compliance expectations for sorting and reporting in municipal services. The Europe bulky waste collection service market is likely to see stronger bid requirements on data visibility and environmental reporting in Germany, France, Spain, Italy, and the United Kingdom. Operators that meet these criteria will be better positioned to renew contracts and expand into adjacent services. Overall, market development remains linked to public investment, enforcement capability, and the diffusion of proven digital practices across regions.

Nordic and Benelux countries continue to set higher benchmarks in separate collection and prevention outcomes, driven by economic incentives and consumer participation. Private consolidation in the Nordics, including acquisitions that add AI-enabled treatment capacity in metropolitan areas, points to a direction of travel toward technology-led performance gains. Central and Eastern Europe remain diverse, with some cities advancing quickly while rural areas face structural infrastructure gaps that affect service viability. In the United Kingdom, authorities are increasing enforcement resources to shift compliance dynamics and improve public trust, with implications for contractor selection and service models. Over the forecast period, these geographic contrasts will shape where the Europe bulky waste collection service market grows most quickly and where digitization presents the largest catch-up opportunities.

Competitive Landscape

The Europe bulky waste collection service market is moderately fragmented, with a mix of multinational operators, strong regional players, and municipalities that perform services in-house. Competition is intensifying around data capabilities, compliance readiness, and cost-to-serve in dense urban areas. SUEZ demonstrates how sensor-enabled collection and platform integration can reduce unnecessary trips and improve service quality for public clients. In the United Kingdom, a recent contract award highlighted right-sized electric fleets and in-cab technology as part of the climate and performance commitments sought by local authorities. As reporting and transparency become pervasive requirements, digital maturity is a differentiator in renewals and new bids.

Strategic acquisitions are adding capabilities and accelerating region-specific growth strategies. A 2026 agreement by large infrastructure funds to acquire a major integrated operator reflects investor confidence in long-term, compliance-led waste services, including municipal and industrial segments focused on circular outcomes. Reconomy’s 2026 purchase of a German specialist expanded its reach across complex industrial streams and strengthened a broader European partner network. In the Nordics, acquisitions that integrate AI- and robotics-based treatment capacity position operators to capture value from higher-purity secondary materials and to support advanced sorting mandates. These moves show how private capital and operators are aligning portfolios with policy direction and client expectations.

Public programs and enforcement actions are also redistributing advantage. The United Kingdom’s Extended Producer Responsibility for packaging is designed to shift collection cost burdens upstream, supporting investments in local services that will affect contract scope and performance clauses. The European Union's digital shipment tracking requirements raise compliance expectations for any operator handling cross-border flows, favoring those with robust data systems and certifications. Municipalities remain influential buyers and operators, supporting a wide range of vendors while raising the bar on transparency and environmental performance. Over time, players that combine route density, electrified fleets, and material recovery partnerships will be best positioned to capture share in the Europe bulky waste collection service market.

Europe Bulky Waste Collection Service Industry Leaders

Clearabee

AnyJunk Limited

Veolia Environnement S.A.

SUEZ S.A.

Biffa plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NG Nordic acquired Kuljetusrinki Oy, adding AI- and robotics-based waste treatment capacity serving the Helsinki metropolitan area.

- February 2026: EQT Infrastructure and Blackstone Infrastructure agreed to acquire Urbaser, a global integrated waste management platform serving municipal and industrial customers, with plans to expand industrial segments and strengthen municipal operations.

- July 2025: The United Kingdom Government announced a GBP 1.1 billion boost from Extended Producer Responsibility for Packaging to improve local recycling services, with industry estimating significant annual investment from packaging producers to support jobs and infrastructure.

- July 2025: The European Commission adopted a key legal act to digitalize waste shipments within the European Union, enabling near-real-time tracking of intra-EU waste movements.

Europe Bulky Waste Collection Service Market Report Scope

The Europe Bulky Waste Collection Service Market Report is Segmented by Collection Model (Curbside, On-Demand, Hybrid, Contracted B2B, Others), Source (Residential, Commercial, Industrial, Municipal/Government, Others), Waste Type (Furniture & Upholstery, Metal & Scrap Items, White Goods/Appliances, Construction & Demolition, Others), and Geography (United Kingdom, Germany, France, Italy, Spain, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others (Event-specific Waste, Biomedical/Institutional) |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Collection Model | Curbside |

| On-Demand | |

| Hybrid | |

| Contracted B2B | |

| Others | |

| By Source | Residential |

| Commercial | |

| Industrial | |

| Municipal/Government | |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | |

| By Waste Type | Furniture & Upholstery |

| Metal & Scrap Items | |

| White Goods/Appliances | |

| Construction & Demolition | |

| Others (Event-specific Waste, Biomedical/Institutional) | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe bulky waste collection service market size outlook through 2031?

The Europe bulky waste collection service market size was USD 7.13 billion in 2025, USD 7.50 billion in 2026, and is forecast to reach USD 9.77 billion by 2031 at a 5.4% CAGR from 2026 to 2031.

Which collection models are gaining traction in Europe bulky waste collection service?

Curbside remains the largest model, with a 46.72% share in 2025, while on-demand services are growing faster at a 5.82% CAGR through 2031 as urban customers seek app-based booking and rapid pickups.

Which sources drive most volumes in Europe bulky waste collection service?

Residential sources accounted for 60.23% of volumes in 2025 and are the fastest-growing segment, with a 6.21% CAGR, driven by higher per-capita waste and shorter replacement cycles for home goods.

What waste types are included in the bulky waste collection service in Europe?

Furniture and upholstery led with a 41.37% share in 2025 and a 6.41% CAGR to 2031, followed by white goods and metal items that require specific collection and treatment flows.

Which European countries are most influential in the field of bulky waste collection services?

Germany holds the largest share at 20.62% in 2025, and Spain posts the fastest projected growth at a 6.78% CAGR through 2031, while the United Kingdom, France, and Italy shape standards through funding, enforcement, and digitalization.

How are regulations shaping the Europe bulky waste collection service market?

European Union rules on recyclability and digital waste tracking, coupled with national enforcement actions, are raising compliance requirements and pushing the adoption of smart collection technologies.

Page last updated on: