Italy Organic Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

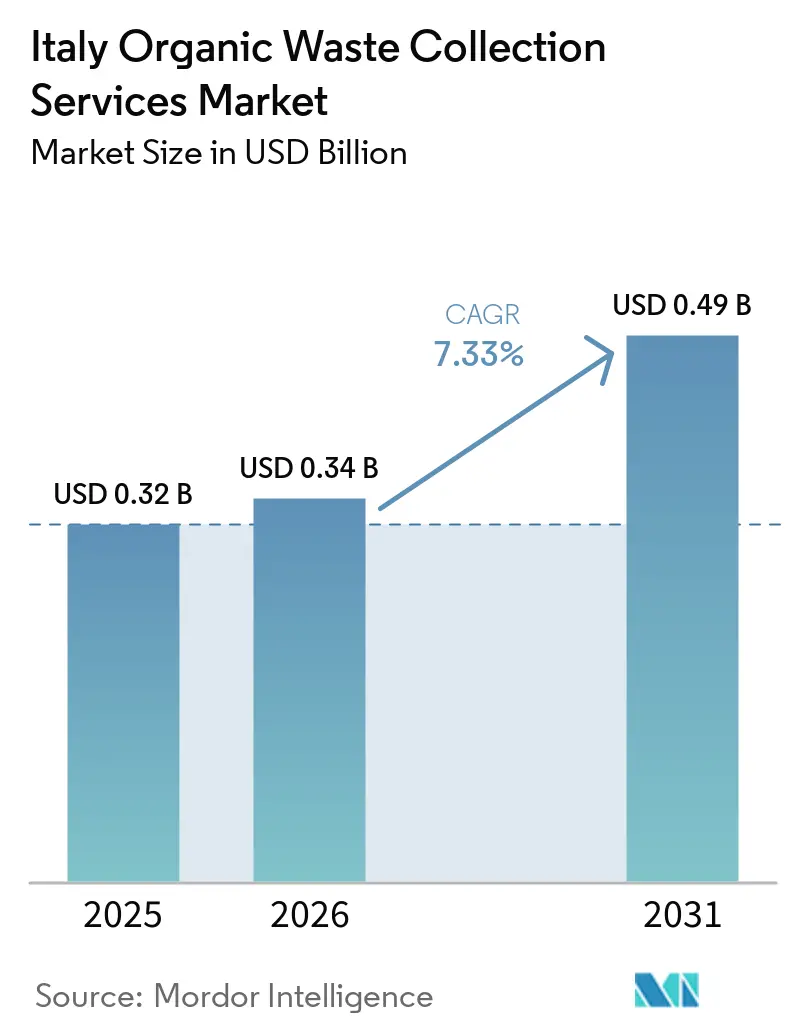

| Base Year Market Size (2025) | USD 0.32 Billion |

| Market Size (2026) | USD 0.34 Billion |

| Market Size (2031) | USD 0.49 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

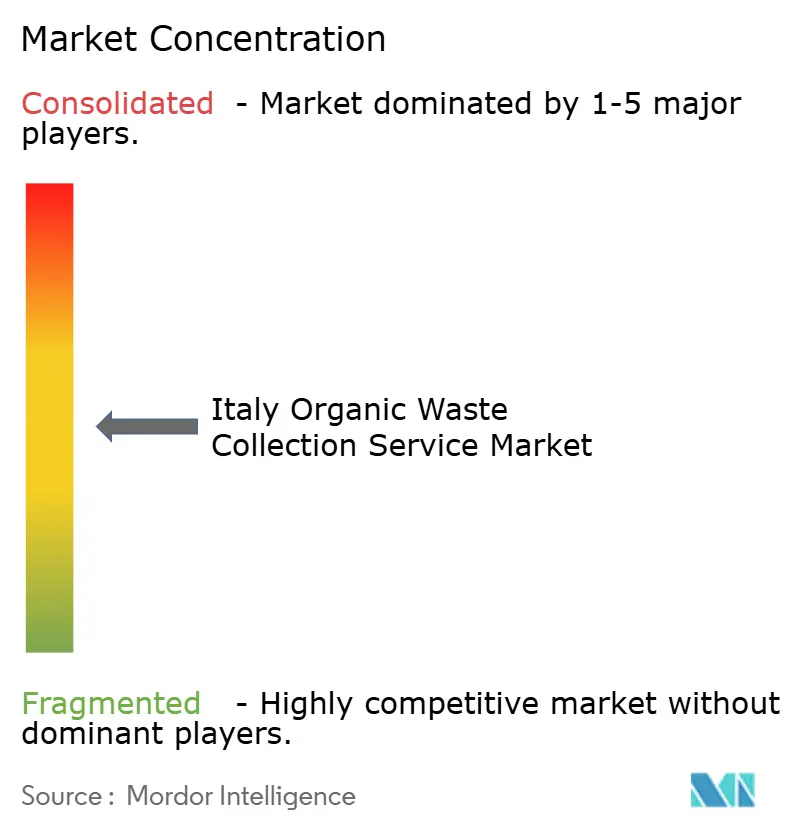

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Organic Waste Collection Services Market Analysis by Mordor Intelligence

The Italy Organic Waste Collection Services Market size was valued at USD 0.32 billion in 2025 and is estimated to grow from USD 0.34 billion in 2026 to reach USD 0.49 billion by 2031, at a CAGR of 7.33% during the forecast period (2026-2031).

Growth reflects policy-driven shifts in municipal service design, with national rules that prioritize separate collection, landfill diversion, and feedstock valorization through anaerobic digestion and composting. Tariff modernization under Italy’s regulatory framework is encouraging the adoption of traceability technologies that support pay-as-you-throw programs and transparent service quality metrics. The investment pipeline for biomethane and co-located composting capacity is accelerating, enabled by national recovery funding for circular economy projects and by multi-utilities that integrate collection with treatment and energy recovery. Collection economics continue to diverge across regions, as Northern territories operate denser biological treatment networks than the South, raising transport intensity and unit costs for municipalities with infrastructure gaps. Operators are responding with door-to-door models backed by RFID, route optimization, and AI-enabled purity monitoring to protect margins while meeting quality standards for compost and biomethane feedstock.

Key Report Takeaways

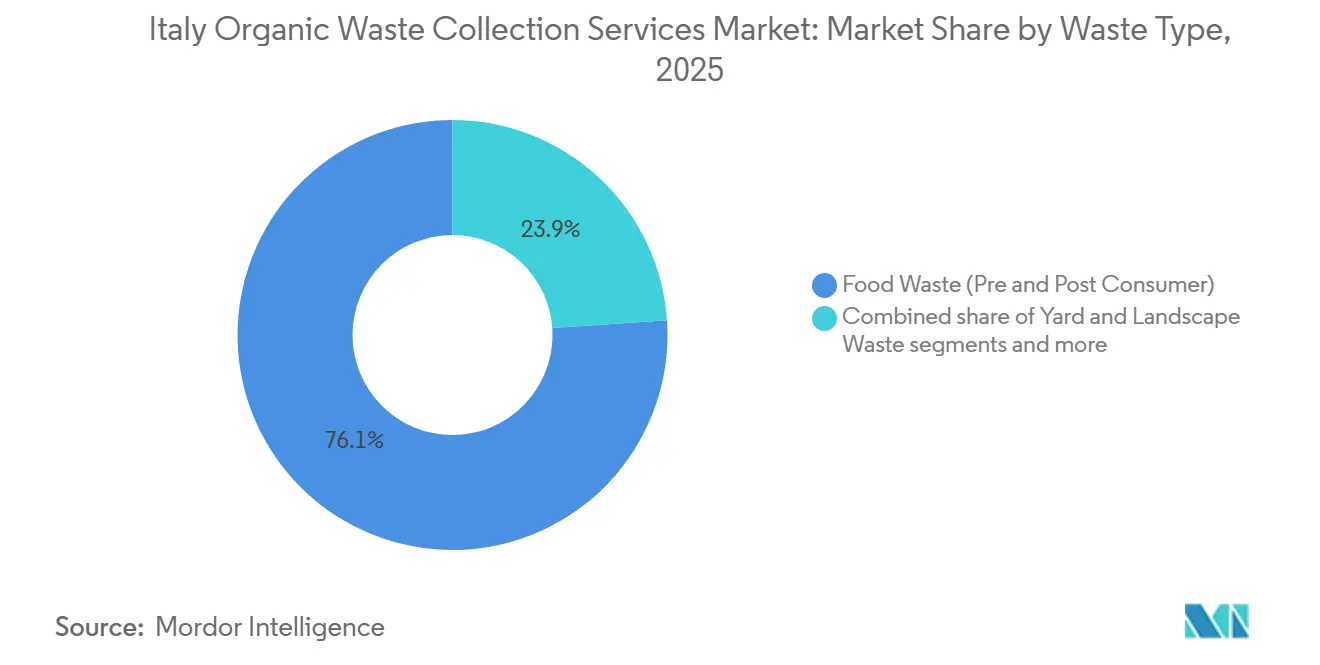

- By waste type, food waste (pre- and post-consumer) dominated the Italy organic waste collection services market share with 76.1% in 2025 and is projected to remain the fastest-growing segment at 8.21% CAGR through 2031, driven by mandated separate collection and biomethane incentives.

- By end-user, residential users held the largest share at 68.9% in 2025 in the Italy organic waste collection services market size, while commercial food service is expected to grow fastest at 7.86% CAGR through 2031 due to HoReCa diversion initiatives.

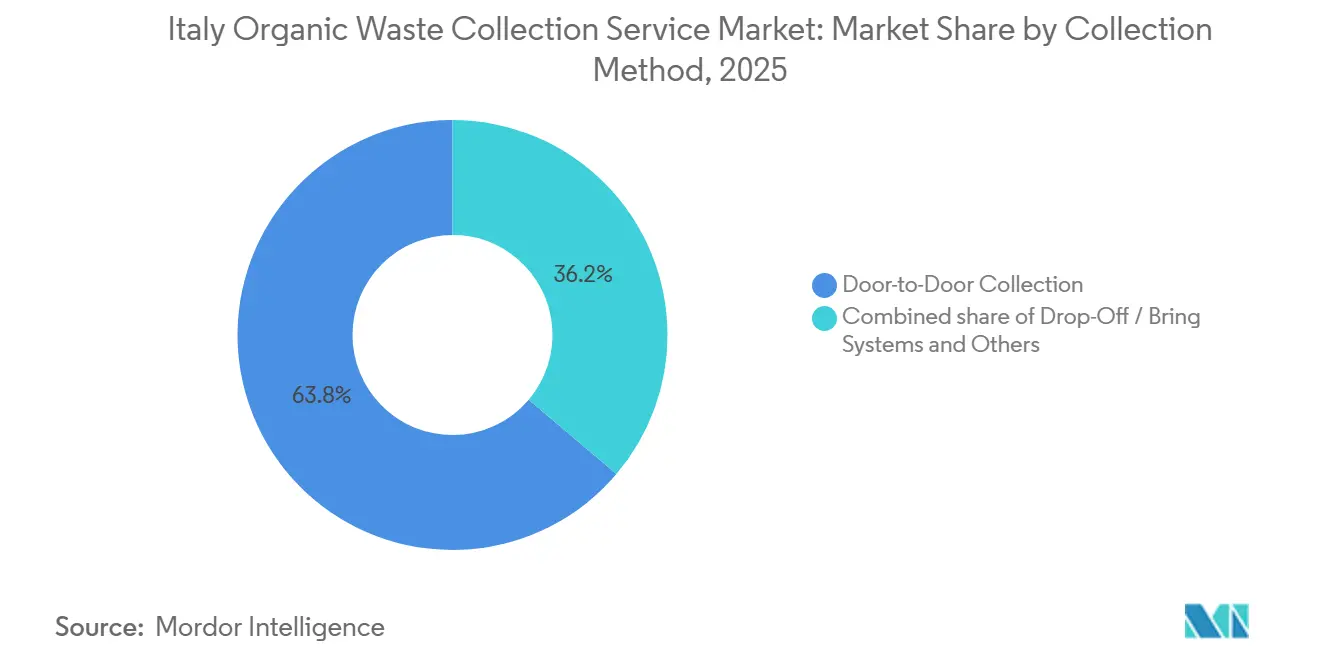

- By collection method, door-to-door led with a 63.8% share in 2025 and is projected to maintain the highest CAGR of 8.48% through 2031, supported by technology-enabled traceability and regulatory standards.

- By technology and equipment, semi-automated systems captured a 54.2% share in 2025, while fully automated systems are poised for the fastest growth at an 8.78% CAGR through 2031, driven by AI sorting and IoT integration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Organic Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Municipal Compliance with Italy’s “Raccolta Differenziata” Targets | +1.8% | National, outperformance in Emilia‑Romagna and Veneto | Short term (≤ 2 years) |

| Expansion of Composting Infrastructure in Northern Italy | +1.5% | North, with a spill‑over to Southern build‑outs | Medium term (2‑4 years) |

| Landfill Diversion Targets Driving Organic Waste Segregation | +1.3% | National, with acceleration in Central and Southern regions | Long term (≥ 4 years) |

| Pay‑As‑You‑Throw (PAYT) Adoption by Italian Municipalities | +1.2% | Highest penetration in the North‑East, expanding nationally | Medium term (2‑4 years) |

| EU Circular Economy Targets Accelerating Organic Waste Valorization | +1.0% | EU‑wide, with national implementation | Long term (≥ 4 years) |

| Biomethane Incentives Boosting Organic Waste Collection | +0.9% | National, with momentum in Lombardy, Emilia‑Romagna, Piedmont | Medium term (2‑4 years) |

| Source: Mordor Intelligence | |||

High Municipal Compliance with Italy’s “Raccolta Differenziata” Targets

Italy reached a 67.7% national separate collection rate in 2024, consolidating progress toward higher diversion of organic streams within differentiated collection systems. Regional leaders such as Emilia-Romagna and Veneto maintained performance levels above the national average, which enhances the quality and quantity of organic feedstock available for composting and anaerobic digestion. These outcomes are reinforced by long-term integrated service contracts that standardize door-to-door protocols and embed feedstock quality controls, which improve the operating environment for collection firms in high-compliance zones. In large cities where collection density and complexity are high, pairing infrastructure with user-facing tools and RFID helps reduce residual fractions while improving traceability of organic bins. Regions that combine higher-than-average separate collection with investment in digestion assets tend to host more biomethane plants, which tightens the link between upstream service design and downstream energy valorization. The cumulative effect is a more resilient base of captured organic material for operators in the Italy organic waste collection services market, which supports scale economics and revenue diversity across collection and treatment.[1]ISPRA Editorial Team, “Rifiuti Urbani 2024: Produzione e Raccolta Differenziata in Crescita,” ISPRA, isprambiente.gov.it

Expansion of Composting Infrastructure in Northern Italy

Northern regions operate more biological treatment sites than Southern territories, resulting in lower per-capita collection and transfer costs. In contrast, Central Italy records the country's highest per-capita management costs due to infrastructure gaps and longer transport distances, while Southern regions face similar cost pressures alongside lower treatment capacity. The current build-out trajectory reflects a continued shift from standalone composting toward integrated anaerobic digestion with aerobic stabilization, which increases energy revenues while preserving compost outputs from the same feedstock. A recent capacity expansion in Liguria illustrates the direction of travel, with a biodigester doubling its throughput, injecting biomethane into the national grid, and producing certified compost for agriculture. Strategic siting near agro-industrial clusters supports co-digestion of residues, boosting biogas yields and stabilizing plant economics year-round. As the North continues to lead on infrastructure density, service operators can plan collection routes around nearer facilities, which lowers unit costs and mitigates transport risks, a dynamic that remains a priority for municipalities in the Italy organic waste collection services market. Over the medium term, new digestion and composting projects in underserved provinces are positioned to rebalance regional flows of organics and reduce long-haul transfers.

Landfill Diversion Targets Driving Organic Waste Segregation

Landfill disposal declined to 14.8% of total municipal waste in 2024, yet further progress is required to meet EU ceilings by 2035, with organics recognized as a priority due to their biodegradability and the availability of valorization technologies. Legislative Decree 116/2020 continues to anchor separate collection requirements that steer organic material away from disposal and toward composting and anaerobic digestion. Regions deploying upgraded mechanical-biological treatment and modern composting networks are demonstrating tangible progress in closing cycles locally and avoiding legacy penalties linked to over-reliance on disposal. Collection operators benefit from this policy environment because steady diversion targets translate into predictable feedstock volumes and quality programs that reduce contamination at the source. As landfill diversion advances across Central and Southern territories, contract structures increasingly incorporate performance terms that link collection outcomes to treatment booking and energy yields, which is shaping competitive behavior in the Italy organic waste collection services market. Over the long term, new energy-from-residuals capacity in key provinces will further stabilize system flows by processing material unsuitable for composting.

Pay-As-You-Throw (PAYT) Adoption by Italian Municipalities

Municipalities are scaling pay-as-you-throw to align tariffs with actual residual volumes, a shift that requires reliable traceability of bin set-outs and route-level performance data. As examples, Teramo documented rapid gains in separate collection and reductions in residual waste within weeks of launching RFID-tagged bins for households, with transparent billing linked to measured disposals. Similar results have been achieved in dense urban contexts, where door-to-door pay-as-you-throw, coupled with resident apps, improved capture performance and accountability for organic fractions. Technology suppliers in the value chain are enabling municipalities to scale through hands-free vehicle readers, mobile scanners for pedestrian zones, and cloud platforms that compile disposal events for tariff computation and contamination alerts. As regulatory quality standards and tariff methods promote punctual measurement in new tenders, a larger share of collection contracts is embedding RFID and IoT prerequisites into technical specifications. These requirements are creating competitive advantages for operators with mature data systems, which feed back into route optimization and purity monitoring across the Italy organic waste collection services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Contamination Levels in Collected Organic Waste Streams | -1.1% | National, heightened risks in large metropolitan areas | Short term (≤ 2 years) |

| Rising Operational Costs | -0.9% | Higher in Central and Southern regions than in the North | Medium term (2‑4 years) |

| Limited Processing Capacity in Southern Regions | -0.8% | South and Islands, including Sicily and parts of Campania | Long term (≥ 4 years) |

| Limited Standardization of Collection Practices Across Municipalities | -0.6% | National, fragmented service models across thousands of comuni | Medium term (2‑4 years) |

| Source: Mordor Intelligence | |||

High Contamination Levels in Collected Organic Waste Streams

Despite Italy's 67.7% separate collection rate, variations in purity remain a challenge. Industry monitoring indicates persistent contamination of the organic fraction with plastic films, glass fragments, and metals, particularly in large metropolitan areas where resident compliance varies. These impurities add pre-processing stages such as sieving, magnetic separation, and optical sorting, which raise energy inputs per tonne and reduce net compost yields for operators. AI-enabled monitoring is emerging as a practical response at sorting plants and along collection routes, where computer vision flags contamination types and patterns that can be acted on operationally and through targeted resident communications. Deployments at large facilities demonstrate how real-time compositional analysis improves fiber quality for paper grades, illustrating the step-change AI and sensors can deliver across multiple material streams, including organics. Point-of-disposal cameras and route-level analytics from industry suppliers are also demonstrating higher purity in corporate settings, which signals broader applicability as municipalities aim to scale variable tariffs and contamination fee adjustments. Over time, capital availability will determine the pace of adoption of contamination-control technologies in smaller municipalities, thereby influencing cost recovery and pricing in the Italian organic waste collection service market.

Rising Operational Costs

Average per-capita costs for urban waste management increased in 2024, with Central and Southern regions recording higher levels than the North due to infrastructure gaps, long-haul transfers, and differences in service models. Door-to-door collection for organics requires more labor and more frequent rotations during warm months, which puts pressure on unit costs even as quality outcomes improve. Decarbonizing logistics through biofuels and electrification reduces lifecycle emissions but entails near-term capital outlays that must be amortized over multi-year contracts, a trade-off that large multi-utilities are actively managing. Digital route optimization and IoT-enabled billing platforms are helping curb mileage and improve traceability, enabling operators to trim logistics overhead in municipalities that adopt data-rich scheduling and customer engagement. Over the medium term, Southern regions that complete planned composting and digestion plants should see lower reliance on inter-regional shipment of organics, which can ease pressure on per-capita costs in the Italy organic waste collection services market. Persistent inflation in wages, consumables, and energy underscores the importance of contract structures that recognize quality incentives and technology investments when pricing services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Municipal Organic Waste Commands Market Leadership While Food Waste Registers the Fastest Growth

Food waste accounted for 76.1% of collection service revenues in 2025, driven by mandated separation of household and commercial organics and strong capture rates in municipalities with door-to-door programs. Regulatory obligations under D.Lgs. 116/2020 continue to anchor the primacy of the organic fraction of municipal solid waste, with certified compostable bags and resident education sustaining participation in curbside programs. As the largest segment, food waste is also projected to grow fastest among major waste types, with an 8.21% CAGR through 2031, reflecting ongoing expansion of separate collection mandates and biomethane incentives that increase captured volumes. Treatment pathways increasingly favor integrated anaerobic digestion followed by downstream composting to maximize energy output while meeting agronomic criteria for soil products, an approach now widespread across leading regions. Plants such as the expanded biodigester at Cairo Montenotte demonstrate how municipal organic fraction of municipal solid waste and green waste are converted into biomethane and compost, creating dual revenue streams and more resilient processing economics that support collection contract stability. Food service establishments generate dense organic loads that benefit from daily collection during peak seasons, and tariff structures recognize their higher waste intensity by aligning costs with waste-generation profiles. The Italy organic waste collection services market is therefore anchored in the organic fraction of municipal solid waste, where routing, bin design, and contamination control have the largest impact on feedstock quality and contract performance.

Green pruning and landscape waste represent the second-largest stream, characterized by seasonal fluctuations that challenge logistics and service levels in parks and residential neighborhoods. Composting-only facilities remain important for high-lignin fractions, with co-digestion reserved for blends that achieve more favorable carbon-nitrogen balances in anaerobic digestion tanks. Policies encourage the co-digestion of agro-industrial by-products to diversify feedstock sources and stabilize energy output profiles throughout the year. National bioeconomy planning designates support for anaerobic digestion in Southern regions, which may accelerate integration of farm-level residues into municipal collection frameworks where contracts and logistics permit. Collection service revenues for agricultural residues are projected to expand as new digestion sites secure guaranteed feed-in channels and strengthen local cooperatives' participation in organics management. Niche streams such as market waste can command premium gate fees when sorted to high purity, creating selective opportunities for municipalities that enforce robust contamination and set-out standards.

By End-User: Residential Dominates, Commercial Gains Momentum

Residential users accounted for the largest share of 68.9% in 2025, reflecting the wide reach of separate collection programs and door-to-door service in many municipalities within the Italy organic waste collection services market. Pay-as-you-throw pilots confirm that households respond to clear variable charges by shifting residual fractions into organics and recyclables, improving capture rates in a matter of weeks when the program is paired with RFID-tagged bins and communications. Multi-family buildings often require tailored solutions, including controlled-access communal containers with user authentication that manage throughput and reduce contamination risks. Domestic composting adds a complementary channel that diverts a portion of household organics from collection programs to local soil benefit, with industry monitoring estimating meaningful tonnage savings at the municipal level. In high-performing provinces, the growth pace moderates as programs approach saturation, which shifts focus to contamination control and route efficiency. Overall, residential organics remain the bedrock of captured volumes that underpin treatment bookings and biomethane production plans across the Italy organic waste collection services market.

Commercial food service is set to grow faster than the residential base, registering a CAGR of 7.86% over the forecast period, as tariff coefficients align costs with waste intensity and as municipalities expand dedicated circuits for restaurants and catering. Programs that meter customer set-ups with RFID and IoT achieve greater accountability, enabling variable tariffs to be translated directly into operating adjustments at the site level. EU-funded demonstrations show that introducing pay-as-you-throw for commercial users can increase separate collection rates and reduce residual waste, validating the business case for segment-specific contracts. Industrial generators in agro-food processing are increasingly integrated into co-digestion frameworks, where plants partner with producers to secure steady streams of organic residues. For operators, these end-user niches expand the Italian organic waste collection service industry footprint into more complex accounts that require tighter scheduling and quality control against contamination. Stronger data systems and clearer contractual clarity on contamination fees are key to protecting margins as programs scale.

By Collection Method: Door-to-Door Leads, Drop-Off Faces Decline

Door-to-door collection held the largest share in 2025, accounting for 63.8% of the Italy organic waste collection services market, supported by higher capture performance, greater accountability, and rapid expansion of RFID-enabled traceability. Municipal case studies show consistent improvements when pay-as-you-throw and individualized bins are deployed, with measurable reductions in residual waste and higher participation in organics programs. Industry suppliers have standardized on UHF readers for vehicles and hands-free scanners for pedestrian-only areas, reducing manual input per collection and improving data quality for billing. Fleet decarbonization through advanced biofuels and electrification is gaining traction, with large operators reporting material reductions in emissions intensity that align with wider climate commitments. Although labor intensity per route is higher than communal bin systems, route optimization algorithms and predictive service using on-board vision are mitigating mileage and pickup frequency. These elements reinforce door-to-door as the primary growth engine for the Italy organic waste collection services market through 2031, with the segment also recording the fastest growth at a CAGR of 8.48% over the forecast period.

Drop-off / bring systems remain important in rural and alpine territories where dispersed settlement patterns raise the cost of individualized service. However, they face structural headwinds from higher contamination rates and weaker accountability. Smart bring points with controlled access, authentication, and on-board cameras are improving hygiene and user responsibility, while fill-level sensors enable demand-based pickup, easing overflow risks. Trials with smart locks and volumetric monitoring demonstrate that technology can close the gap with door-to-door on a subset of metrics, though average pure capture performance remains lower. Episodic mobile collections for seasonal green waste surges complement routine service, with GPS-tracked roll-off containers improving rotation efficiency. Over the forecast period, modernization of bring systems will likely focus on contamination prevention and user authentication, while door-to-door will continue to capture a larger share of the Italian organic waste collection market due to stronger performance incentives.

By Technology & Equipment: Semi-Automated Dominates, Full Automation Ascends

Semi-automated systems held the largest share in 2025, accounting for 54.2% of the Italy organic waste collection services market, as municipalities and operators scaled RFID-tagged bins, vehicle-mounted readers, and crew-led quality checks that balance automation with legacy fleets. Retrofit economics favor this pathway because upgrading trucks with readers costs far less than procuring new fully automated equipment, allowing smaller communities to introduce traceability without large capital programs. These systems suit Italy's heterogeneous urban forms, where narrow streets and historical centers limit the maneuverability of robotic arms, while delivering reliable data for pay-as-you-throw billing and contamination monitoring. As national tariff and quality rules reinforce punctual measurement in new tenders, semi-automated deployments are expected to extend to more municipalities over the medium term. The Italian organic waste collection service industry will therefore continue to rely on hybrid architectures that balance local constraints with data collection to support tariffs and quality assurance.

Fully automated systems are expected to record the fastest growth through 2031, expanding at a CAGR of 8.78%, driven by advancements in AI-enabled sorting, smart bin technologies, and IoT-integrated operations that improve precision, efficiency, and labor optimization across waste streams. Vision-guided optical sorters installed at major facilities already achieve high accuracy in real-time compositional control, increasing output purity and revenue per tonne for premium fiber and recyclable grades. AI-powered mobile tools are speeding up the identification and classification of complex waste types, with pilots showing sizable reductions in processing time and improved compliance with coding requirements. Capital intensity remains the main barrier to full automation, which makes large multi-utilities better placed to amortize systems across large customer bases and multi-decade asset plans. Even so, European green-funding alignment is favorable for high-efficiency systems, which supports near-term deployment waves in the Italy organic waste collection services market as municipalities and operators tap dedicated programs. Manual collection will persist in morphologically constrained areas such as islands and pedestrian centers, although its relative share is expected to decline steadily over the forecast horizon.

Geography Analysis

Regional asymmetries are pronounced, with Northern territories operating more biological treatment infrastructure and processing more organic waste per capita than Southern regions, which contributes to lower unit costs and steadier feedstock flows for collection operators. Northern Italy serves as the anchor of the Italy organic waste collection services market, thanks to mature pay-as-you-throw penetration and integrated digestion-composting networks that tie collection outcomes directly to energy valorization. Emilia-Romagna has maintained leading separate collection performance and benefits from integrated service contracts that entrench door-to-door organic pickup and quality safeguards at scale. Veneto’s long-standing consortium models and early adoption of pay-as-you-throw for commercial users underscore the region’s high diversion profile, translating into robust organics capture and quality levels. Lombardy pairs strong separate collection outcomes with large-scale circular economy investment programs from integrated utilities, which sustain capacity additions in waste treatment and bolster route economics for contracted collectors.

Central Italy contributes a sizable share of the Italy organic waste collection services market but also carries the country’s highest per-capita management costs, reflecting transport burdens stemming from infrastructure deficits in large metropolitan areas. The capital area remains a focal point for system upgrades and for new energy-from-residuals capacity that will absorb material unsuitable for composting, which should reduce exports and stabilize tipping dynamics in the mid-term. Marche and Tuscany illustrate how integrated platforms and targeted expansions can lift collection quality and treatment self-sufficiency, improving the foundation for pay-as-you-throw and service quality metrics. As more Central territories finalize investments, routing distances should decrease, and contamination management should improve, both of which support margin protection for operators. Over the forecast period, Central Italy’s progress will depend on the pace of plant commissioning and the breadth of data-enabled tariffs across municipalities.

Southern Italy and the Islands present the largest medium-term growth vector for the Italy organic waste collection services market, starting from a lower base of treatment infrastructure and lower average separate collection rates than the North. Ongoing build-outs of composting and digestion plants are designed to eliminate dependence on out-of-region treatment, thereby increasing resilience and lowering transport-related costs as facilities enter service. Island regions like Sardinia have demonstrated that early investment and tariff alignment can deliver high levels of separate collection while capitalizing on seasonal organics to optimize energy output. Provinces adopting pay-as-you-throw across broader geographic footprints are reporting rapid gains in diversion measures, which strengthens the case for scaling controlled-access bins and user authentication in complex residential contexts. As Southern municipalities absorb recovery funding and finalize procurement, operators that can navigate permitting and deploy robust data systems stand to gain share as organic feedstock becomes easier to treat locally.

Competitive Landscape

The Italy organic waste collection services market is moderately consolidated in nature. The competitive field comprises integrated multi-utilities and a long tail of municipal and regional operators, with consolidation trends favoring players that control both collection and treatment assets in the Italy organic waste collection services market. Herambiente, A2A, Iren, and Acea illustrate the vertical model that pairs door-to-door service and pay-as-you-throw with digestion, composting, and energy-from-residuals to capture the full value chain. Financial disclosures show that large platforms process multi-million-tonne volumes and generate sizable EBITDA from waste businesses, supported by high separate collection in served territories and by ongoing deployment of RFID smart bins.[2]Strategic Plan Update 2024‑2035,” A2A S.p.A., gruppoa2a.it Strategic plans to 2035 confirm large investment envelopes for the circular economy, with targets for expanded waste treatment capacity and integrated business units that align waste, water, district heating, and efficiency services.[3] Investor Relations Team, “Hera Group Approves FY2024 Results,” Hera Group, gruppohera.it These strategies favor bidders with balance-sheet depth and proven track records in plant construction, which influences outcomes in new tenders where technology prerequisites are explicit.

Recent acquisitions highlight the focus on geographic reinforcement and industrial waste platforms that complement municipal organics. Herambiente increased its stake in SEA in Ancona, strengthening its node in the Marche region to process industrial residues aligned with local food manufacturing. Hera also finalized the acquisition of Sostelia Group to integrate water treatment capabilities, creating cross-sell opportunities for sludge and organics processing. Iren expanded digestion capacity in Liguria, reinforcing local management of organics while producing biomethane for injection into the grid. Acea is strengthening digital and network capabilities relevant to integrated resource management, which supports coordination across water and waste functions as large metropolitan systems modernize. These moves create defensible positions where integrated contracts value quality assurance, energy recovery, and robust reporting.

Disruptive potential is also evident in the technology layer, where AI vision and IoT providers license their systems to multiple operators rather than competing for collection tenders. AI vision systems are being deployed to enable continuous compositional analysis, elevating material revenues and reducing manual inspections. IoT platforms from sector suppliers enable vehicle- and asset-level tracking, fill-level monitoring, and data-driven billing, strengthening pay-as-you-throw readiness and optimizing collection routes. Corporate pilots demonstrate improved purity and assisted disposal in closed environments, indicating replicability for municipalities pursuing contamination-fee enforcement and variable tariffs. The Italy organic waste collection services market thus rewards integration and data leadership, with regional white space in the South offering expansion potential for firms able to navigate permitting and engage local communities as plants come online.

Italy Organic Waste Collection Services Industry Leaders

Gruppo Hera

A2A Group

Gruppo Iren

Waste Management, Inc.

Acea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Gruppo Hera finalized the acquisition of Sostelia Group, adding water treatment capabilities that create synergies with organic waste and sludge processing portfolios across multiple Italian regions.

- March 2026: Herambiente Servizi Industriali increased its stake in SEA in Ancona to 83%, reinforcing an industrial treatment platform that serves food manufacturing clusters in Central Italy.

- February 2026: NANDO and Capgemini Italia concluded a 10-month AI computer-vision pilot across six sites, reporting 71% recycling purity and zero-error assisted disposal, indicating potential for broader municipal deployments.

- January 2026: Gruppo Hera presented its 2026-2029 Business Plan, allocating significant capital to shared-value projects that include RFID smart bin deployments and biomethane plant expansions in Northern regions.

Italy Organic Waste Collection Services Market Report Scope

The Italy Organic Waste Collection Services Market is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and more), by End-User (Residential, Commercial, Industrial, and Others), by Collection Method (Door-to-Door, Drop-Off / Bring Systems, and Others), by Technology and Equipment (Manual, Semi-Automated, and more), and by Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste |

| Agricultural Residues |

| Others |

| Residential |

| Commercial (HoReCa, Retail) |

| Industrial (Food Processing & Manufacturing) |

| Others (Agri-waste) |

| Door-to-Door Collection |

| Drop-Off / Bring Systems |

| Others |

| Manual Collection Systems |

| Semi-Automated Systems |

| Fully Automated Systems |

| Others |

| By Waste Type | Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste | |

| Agricultural Residues | |

| Others | |

| By End-User | Residential |

| Commercial (HoReCa, Retail) | |

| Industrial (Food Processing & Manufacturing) | |

| Others (Agri-waste) | |

| By Collection Method | Door-to-Door Collection |

| Drop-Off / Bring Systems | |

| Others | |

| By Technology & Equipment | Manual Collection Systems |

| Semi-Automated Systems | |

| Fully Automated Systems | |

| Others |

Key Questions Answered in the Report

What is the current size and growth outlook for the Italy organic waste collection services market?

The Italy organic waste collection services market size was USD 0.32 billion in 2025 and is projected to reach USD 0.49 billion by 2031 at a 7.33% CAGR over 2026‑2031.

Which waste type contributes the most to captured organics in Italy?

Food waste is the largest stream, supported by separate collection mandates and strong household and canteen capture, representing the majority of collected organics in 2025.

Why is door-to-door leading among collection methods in Italy?

Door-to-door delivers higher capture and accountability, aided by RFID and pay-as-you-throw, which improves diversion outcomes and underpins technology-ready contracts.

What factors raise operating costs for organic collection services?

More frequent pickups for bio-waste, higher labor intensity for door-to-door, and longer transport distances in regions with fewer plants push per-capita costs higher, especially in Central and Southern Italy.

How are Italian operators addressing contamination in organics?

Operators are installing AI-based vision systems and using route-level analytics to detect impurities and guide user feedback, which protects compost and biomethane yields.

Where are the strongest growth opportunities by geography?

Southern regions and islands show the greatest potential for new digestion and composting projects, which reduce reliance on out-of-region treatment and support pay-as-you-throw expansion.

Page last updated on: