South Korea Organic Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

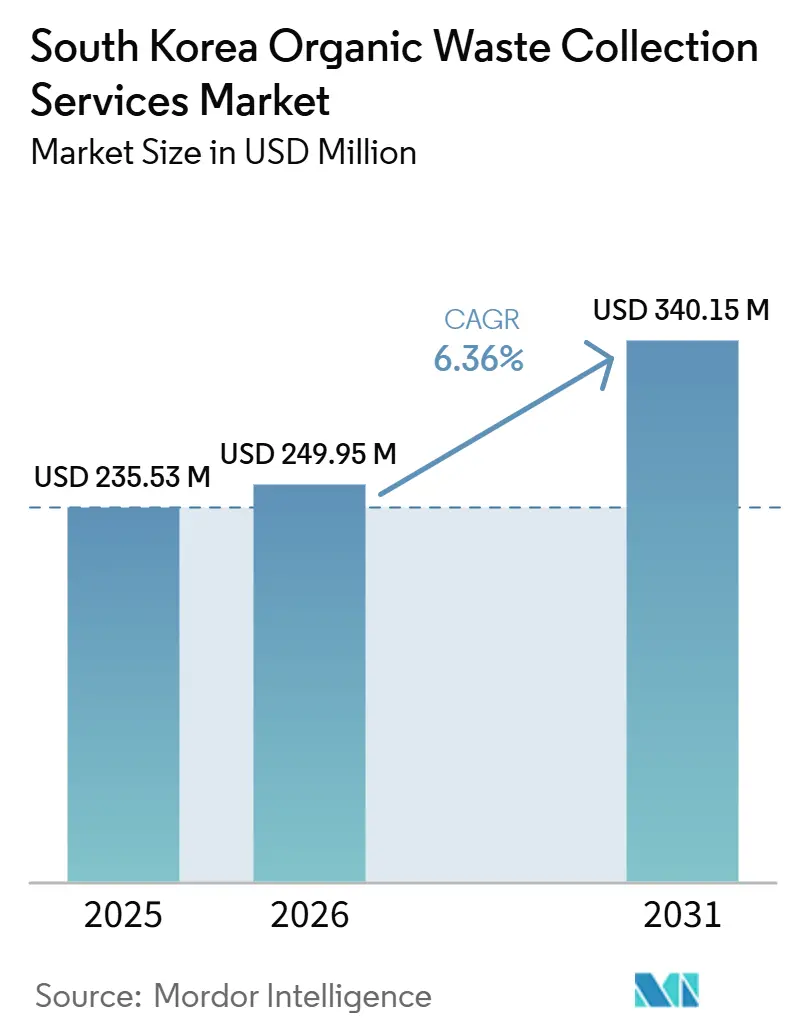

| Base Year Market Size (2025) | USD 235.53 Million |

| Market Size (2026) | USD 249.95 Million |

| Market Size (2031) | USD 340.15 Million |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

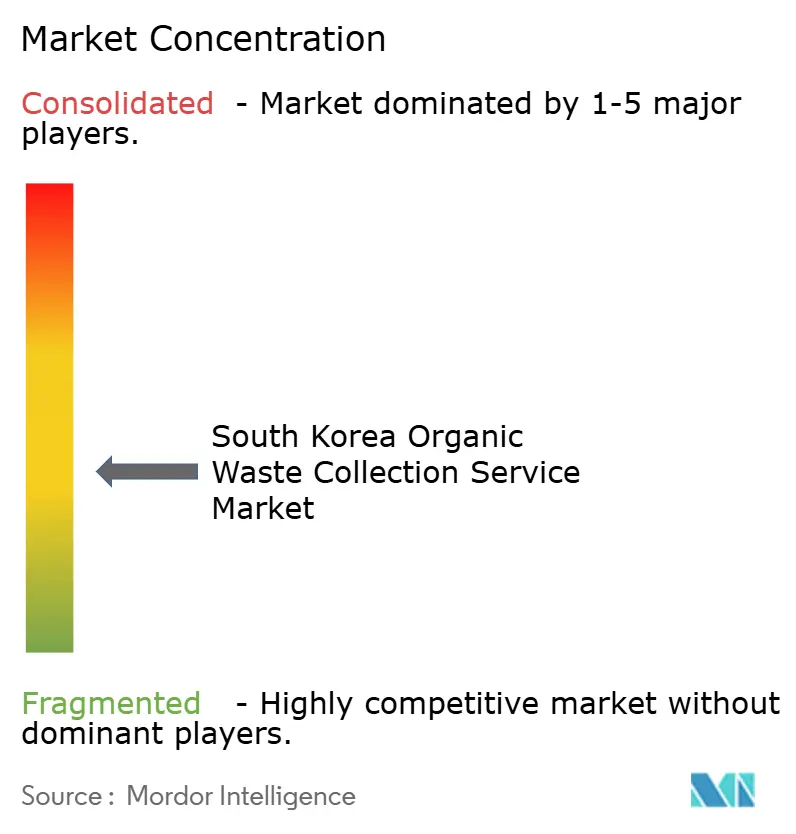

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Organic Waste Collection Services Market Analysis by Mordor Intelligence

The South Korea Organic Waste Collection Services Market size is expected to increase from USD 235.53 million in 2025 to USD 249.95 million in 2026 and reach USD 340.15 million by 2031, growing at a CAGR of 6.36% over 2026-2031.

Market demand is shifting from disposal to resource circulation, supported by national carbon-neutrality goals, rising sustainability requirements, and phased landfill restrictions across the Seoul capital region. The direct landfill ban in the Seoul metropolitan area, effective January 2026, is moving more waste into incineration pathways, tightening gate-fee dynamics, and increasing the importance of collection operators that can secure reliable downstream processing routes. This regulatory shift is also encouraging municipalities and service providers to improve segregation, optimize collection frequency, and expand partnerships with treatment and recovery facilities to reduce dependence on landfill capacity. RFID-enabled systems and pilot electrified fleets indicate a shift toward digital routing, behavioral incentives, and lower-emission operations, helping operators address labor constraints, fuel-price exposure, and cost volatility. These technologies also support better tracking of waste volumes, improved route efficiency, and stronger compliance with municipal waste-management requirements. Biogas targets further support growth by directing more organic feedstock into conversion pathways, including anaerobic digestion and other waste-to-energy applications, although policy ambition continues to outpace realized production in several regions due to infrastructure gaps, feedstock-quality issues, and delays in project execution.

Key Report Takeaways

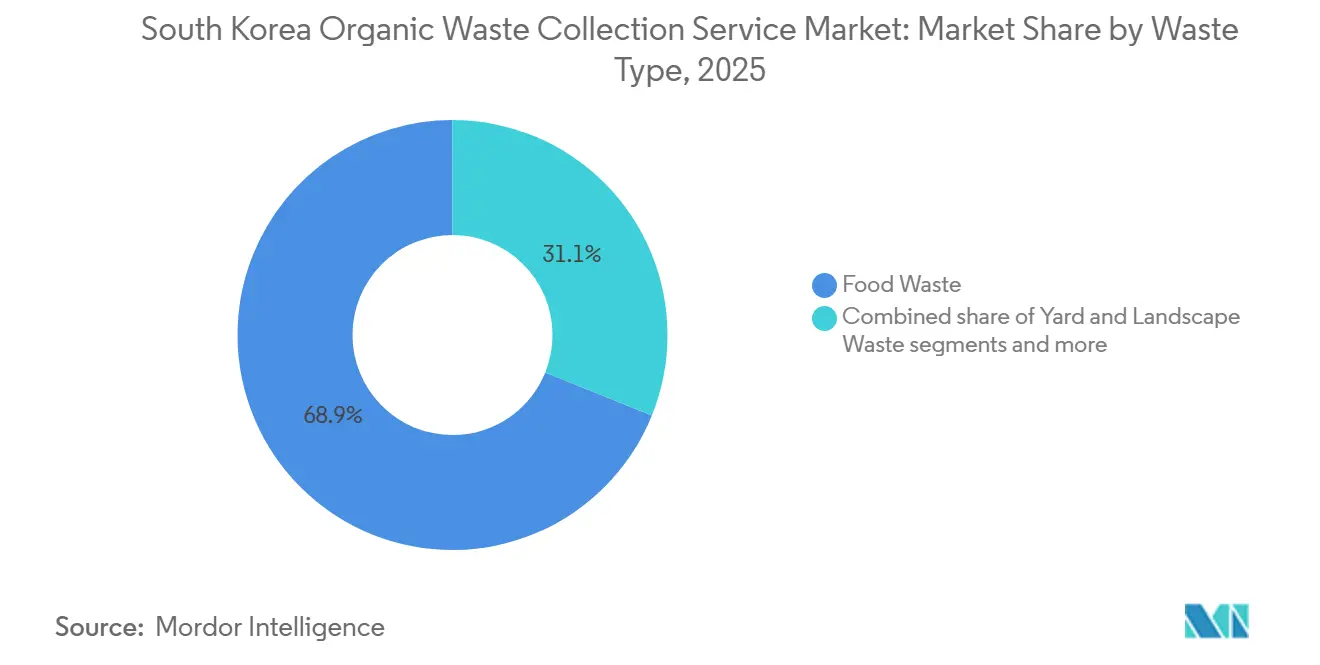

- By waste type, food waste led with a 68.9% of the South Korea organic waste collection service market share in 2025 and is also the fastest-growing, with a 7.21% CAGR through 2031.

- By end-user, residential accounted for 53.9% of the South Korea organic waste collection service market size in 2025, while commercial is projected to advance at a 7.67% CAGR through 2031.

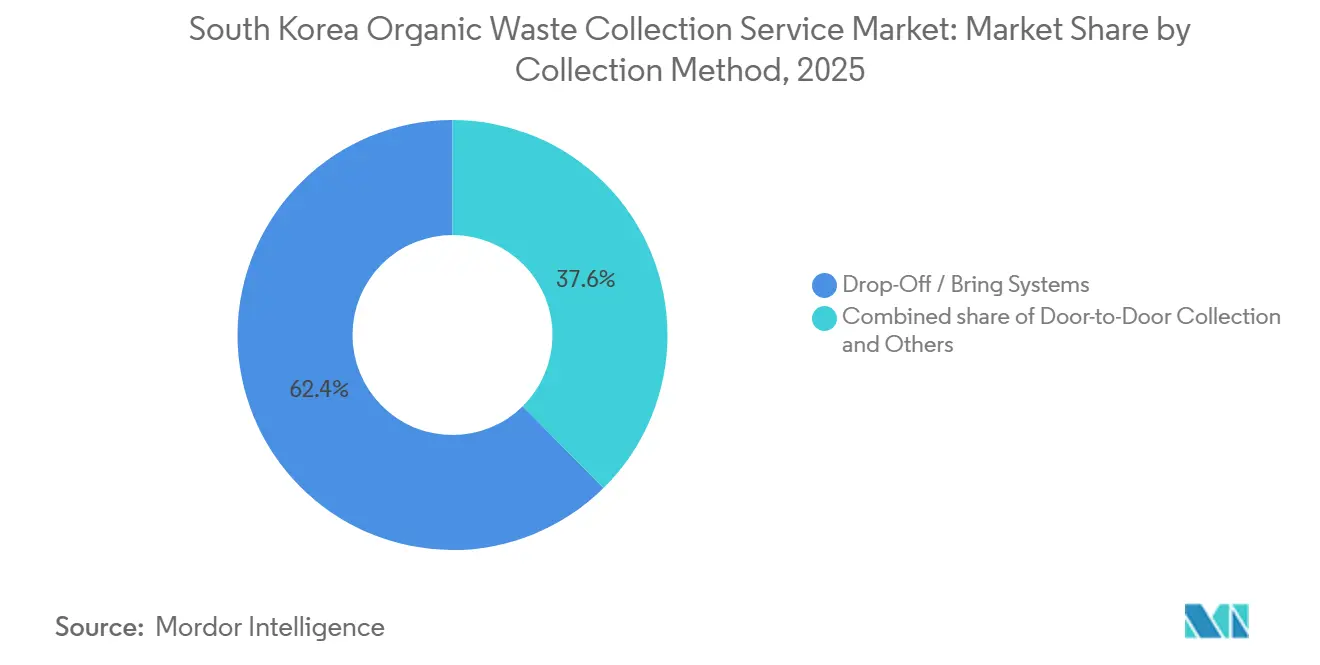

- By collection method, drop-off or bring systems held 62.4% share in 2025, while door-to-door collection is forecast to grow at an 8.21% CAGR through 2031.

- By technology and equipment, semi-automated Systems held 49.2% share in 2025, while fully automated systems are expected to expand at an 8.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Organic Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RFID-Based Smart Waste Bins Adoption Increases Collection Efficiency | +1.8% | Seoul, major metropolitan cities | Medium term (2-4 years) |

| Advanced Food Waste Recycling Infrastructure With 95%+ Diversion Rate from Landfills | +1.5% | South Korea, with concentration in urban cores | Long term (≥ 4 years) |

| Growing Demand for Biogas and Bio-Fertilizer Production From Organic Waste | +1.4% | Asia-Pacific core, spill-over to national regions | Medium term (2-4 years) |

| The Government's Green New Deal and Carbon Neutrality By 2050 Targets | +1.0% | National | Long term (≥ 4 years) |

| High Urbanization Rates and Dense Apartment Complexes Require Organized Collection Services | +0.5% | Seoul, Busan, and Incheon metropolitan areas | Short term (≤ 2 years) |

| Zero Food Waste Policy Initiatives at the National And Municipal Levels | +0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RFID-Based Smart Waste Bins Adoption Increasing Collection Efficiency

Seoul deployed 27,289 RFID (Radio Frequency Identification) food waste disposal units by December 2025, covering a large share of apartment complexes, while penetration across single-family homes remained lower due to higher per-household costs. Field results across several districts reported meaningful reductions in food waste after RFID installation, reflecting improved segregation accuracy and increased route efficiency in multi-unit dwellings. Incentive programs launched in early 2026 that award points to households for reducing food waste are designed to drive incremental improvements beyond the baseline set by volume-based fees. Nationwide, rollout covers millions of households, though adoption remains concentrated in capital regions where route density supports better returns. Over the medium term, data integration from RFID networks is expected to support dynamic pricing and predictive maintenance, strengthening unit economics for the market.

Advanced Food Waste Recycling Infrastructure with 95%+ Diversion Rate from Landfills

Recycling rates for food waste in South Korea exceed 95%, supported by a multi-decade infrastructure buildout and layered policy instruments such as pay-as-you-throw systems and disposal restrictions. Newer multi-stream bioenergy assets, including large-scale bioenergy centers with high daily processing capacity, show how next-generation plants can combine throughput with revenue from biogas sales. National plans through 2030 outline further expansion of biogas facilities, with pilots already selected to increase daily processing capacity and feed more renewable gas into local grids. Private operators are also upgrading throughput and efficiency, including through on-site renewable energy that helps reduce power costs. Authorities continue to acknowledge that compost and feed channels do not absorb all processed output, which is directing more municipal and private stakeholders toward biogas conversion to stabilize offtake.[1]Veolia, “Dongyang Green Bio Facility Update,” Veolia, veolia.com

Growing Demand for Biogas and Bio-Fertilizer Production from Organic Waste

The Biogas Act, which takes effect for public organic waste in 2025 and phases in for larger private generators in 2026, underpins conversion targets that lift feedstock demand and create more stable offtake frameworks for organic waste generators. Policy tools include compliance thresholds for high-volume producers and financing support for integrated plants that handle multiple organic feedstocks, such as food waste, manure, and sludge.[2]Ministry of Environment, “Biogas Conversion Roadmap and Methane Reduction,” Ministry of Environment, me.go.kr Plant-level strategies are also diversifying revenue through combined energy and fertilizer outputs, with several projects reporting stronger capacity utilization and sales growth after upgrades. South Korea’s methane reduction roadmap complements biogas policy and targets structural emissions declines through 2030, reinforcing demand for reliable organic waste collection to secure feedstock volumes. For the market, contracted flows into biogas plants help hedge landfill and incineration pricing volatility and support longer-term planning for both public and private operators.

The Government's Green New Deal and Carbon Neutrality by 2050 Targets

Transport decarbonization targets, including rising goals for EV and hydrogen vehicle adoption through 2035, are beginning to influence municipal fleet procurement strategies. Busan’s staged deployment of hydrogen-powered waste-collection trucks demonstrates early-scale-up of zero-emission assets in frontline sanitation operations. In Seoul, pilot projects with electric commercial vehicles adapted for narrow, hilly zones are testing route viability, charging performance, and body types suitable for collection duties. Government budgets in 2026 designate funds for low- and zero-emission vehicles and charging infrastructure, lowering barriers to adoption for municipal agencies and contracted operators. Despite supportive policy tailwinds, biogas supply remains modest in the national energy mix, highlighting the implementation gap that collection players must navigate as they scale new fleets and automate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages in the Waste Collection Sector are Due to an Aging Workforce | -1.2% | National, acute in rural districts | Medium term (2-4 years) |

| Fluctuating Gate Fees at Treatment Facilities are Affecting Service Profitability | -0.9% | Seoul metropolitan area, Incheon, Busan | Short term (≤ 2 years) |

| Saturation in Major Metropolitan Markets is Limiting Growth Opportunities | -0.6% | Seoul, Busan, and Incheon core districts | Long term (≥ 4 years) |

| Illegal Dumping and Improper Disposal in Cost-Sensitive Households | -0.3% | Peri-urban and cost-sensitive communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages in the Waste Collection Sector Due to an Aging Workforce

South Korea’s working-age population is entering a structural inflection point, with super-aging and a rising share of residents over 65 tightening labor supply for physically demanding collection roles. National labor agencies project sectoral imbalances through the early 2030s, drawing workers toward social welfare and healthcare and increasing competition for recruitment in waste collection. Municipalities are responding with electrified and hydrogen fleets that reduce noise and vibration, potentially improving operator retention and ergonomics on stop-and-go collection routes. Trials with compact electric trucks in hill-dense Seoul districts are also testing whether right-sized vehicles can reduce physical strain and improve access to routes where large trucks face constraints. City-level inspections of private contractors are intensifying to uphold service quality during periods of staff turnover and maintain transparency in weighing and handling as labor shortages raise operational risk.

Fluctuating Gate Fees at Treatment Facilities are Affecting Service Profitability

A post-ban shift toward incineration in the Seoul metropolitan area has exposed operators to pricing bands that vary by facility ownership and maintenance schedules, creating bid-to-bid swings in net disposal costs. Municipalities and private plants continue to publish different fee structures for household and food waste. At the same time, staged increases are planned in some cities to narrow projected deficits and fund asset upgrades. Industry bodies have contested claims of high private incineration premiums, noting bid data that suggest average costs can be closer to those of public channels once ash treatment responsibilities and effective rates are adjusted. Contract instability is an added factor, as some private processors have terminated agreements before service initiation, forcing districts to seek redundant capacity or intergovernmental sharing arrangements. In response, adjacent cities have started cooperative agreements to cross-process during maintenance windows at public plants, reducing exposure to volatile private gate fees and strengthening continuity planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Pre and Post Consumer Food Dominates Through Kitchen-to-Curb Ecosystems

Food Waste accounted for 68.9% of the South Korea organic waste collection service market share in 2025 and is also the fastest-growing category, with a 7.21% CAGR through 2031. The concentration of residents in dense metropolitan clusters supports consistent generation and collection schedules that align well with food waste processing cycles and conversion pathways.[3]Ministry of Environment, “Biogas Conversion Roadmap and Methane Reduction,” Ministry of Environment, me.go.kr Policy-backed growth in biogas infrastructure targets municipalities prioritized for integrated plants, which anchor offtake commitments and strengthen price visibility for contracted feedstock. Yard and landscape waste accounts for a smaller share due to housing density and limited green space in the largest cities. At the same time, agricultural residues often pose seasonal and logistical hurdles that do not align with the economics of daily routes. Co-feeding approvals for select organic by-products also indicate that regulators are encouraging technology combinations that can broaden input flexibility at digestion facilities over the medium term.

The market continues to rely on established segregation rules and RFID-enabled practices that have driven measurable waste reduction in apartment complexes, improving upstream purity for food waste streams. Expansion in conversion capacity aligns with food waste’s shorter processing cycle, which is attractive for biogas operations that need reliable, high-moisture inputs to manage methane yields and uptime. Private plants that have upgraded to higher throughput and better operational efficiency form a complementary layer under long-term policy, helping steady the pipeline from collection to digestion. The industry is also likely to see a longer runway for food waste than for diffuse green waste or seasonal farm residues, given collection economics and compliance oversight in high-density districts.

By End-User: Commercial Outpaces Residential on Hospitality Recovery Dynamics

Residential end-users accounted for 53.9% share of the South Korea organic waste collection service market size in 2025, while Commercial is forecast to grow at a 7.67% CAGR through 2031. Dining, hospitality, and retail venues are returning to normalized operations and remain subject to strict segregation requirements, which concentrate food waste volumes and support route density. Larger private generators face compliance thresholds under the biogas conversion policy timeline, reinforcing contracted collection volumes linked to digester throughput and offtake agreements. Private operators are expanding capacity and performance at co-digestion plants, strengthening the reliability of downstream processing for commercial customers with consistent organic streams. The shift away from direct landfilling has also increased the strategic importance of reliable alternative processing capacity for commercial generators that cannot absorb service interruptions.

For residential flows, municipalities continue to refine behavioral incentives through point-based programs linked to RFID machines, complementing long-standing volume-based fees by rewarding measured reductions. Apartments remain a stronghold for residential compliance due to convenient access to RFID machines in common areas, which lowers contamination and supports route efficiency. Commercial generates more frequent collection needs, often requiring off-peak pickups and aligned routing during maintenance at public plants, which drives interest in bundled service models that secure processing capacity. As compliance for larger private generators tightens, commercial volumes are expected to remain a key growth lever because contracted biogas routes can absorb more feedstock at predictable pricing.

By Collection Method: Door-to-Door Gains on Illegal Dumping Deterrence and Apartment Density

Drop-Off or Bring Systems held 62.4% share of the South Korea organic waste collection service market size in 2025, while Door-to-Door Collection is projected to grow at an 8.21% CAGR through 2031. Drop-Off remains entrenched where volume-based fee infrastructure has been established for years, supported by widespread RFID units at fixed locations in large apartment complexes. Door-to-Door is expanding faster due to the priority placed on convenience, which supports higher compliance in dense neighborhoods and reduces diversion to improper disposal pathways. Electric pilot fleets are targeting narrow or hilly districts where right-sized vehicles can safely navigate and reach buildings that are not well served by large trucks. Municipal oversight has also raised the bar for vendor quality controls to prevent unattended waste and ensure transparent weighing practices.

Cooperation among districts that share specialized facilities shows how Door-to-Door variants can be coordinated to direct specific material types to regional hubs during maintenance windows. Adoption of niche systems, such as pneumatic transfers in premium housing and smart machines for other recyclables, remains limited due to their capital intensity. However, these pilots still inform a broader automation roadmap. The market benefits from Door-to-Door expansion because it helps stabilize segregation quality while municipalities continue to calibrate fees and incentives. Over the forecast period, Door-to-Door is likely to expand its role in hill-dense, access-constrained environments where convenience is essential for compliance.

By Technology & Equipment: Fully Automated Systems Surge Despite Semi-Automated Incumbency

Semi-Automated Systems held 49.2% share of the South Korea organic waste collection service market size in 2025, while Fully Automated Systems are forecast to grow at an 8.61% CAGR through 2031. Semi-automated setups such as RFID card-swipe machines support pay-as-you-throw billing and enable foundational data collection without end-to-end automation. Fully automated deployments integrate analytics for dynamic scheduling, behavior-based incentives linked to reduction points, and predictive maintenance to lower downtime and improve asset utilization. City pilots are advancing vehicle-mounted AI recognition to locate and photograph waste, prioritize response, and suggest optimal routes while applying privacy filters. Downstream plants are also introducing AI-assisted sorting to improve processing yields and stabilize output rates.

Manual systems remain common in less-dense areas, where the return on investment for automation is harder to achieve, and staffing remains the primary cost driver. Decarbonized fleets and route automation both address labor and noise constraints, helping municipalities improve job quality and maintain service reliability under tight headcount conditions. Grant-backed pilots for unmanned collection of other recyclables demonstrate how different materials can leverage shared AI capability stacks that may later be portable to organic waste. As the market scales automation, integration with policy incentives and data platforms will be key to achieving consistent performance gains across districts with varied density profiles.

Geography Analysis

Gangnam District alone processed 67,642 tons of household waste in 2025 and planned to process 71,268 tons in 2026, prompting early contracts with private incinerators to cover scheduled maintenance of the public facility. Incheon split processing between public and private plants in early 2026 and advanced modernization for key facilities while progressing long-term plans to replace aging assets. The market will continue to rely on spare capacity and cross-district contracting in the capital region as new public plants are built and legacy units are overhauled.

Busan is a high-growth pocket where fleet modernization through hydrogen trucks is now underway, supporting lower-emission collection across broad service areas. Industry groups have proposed longer-term contracting and fee caps to stabilize treatment costs in secondary cities, helping buffer short-term spikes during maintenance or system upgrades. Gyeonggi Province has confirmed spare private incineration capacity and is planning new and expanded public plants that will add thousands of tons per day by 2030, which should gradually reduce the cost premium over landfilling that existed before the ban. These additions will help align route density with firm processing slots, reducing rollover risks during peak maintenance periods.

In rural provinces, the pace of RFID and AI adoption is slower due to lower density and different waste priorities, including coastal cleanups where marine debris can dominate. Select counties are piloting AI-driven machines for other recyclable streams, building digital familiarity that may later be applied to organics as route economics improve. National policy staggers implementation across regions, with 2026 milestones for the capital area and 2030 for non-metropolitan zones, which sequences capital planning and upgrades around mandated deadlines. The geographic profile of the market is therefore likely to remain bifurcated in the near term, with tier-one cities front-loading investment and tier-two or tier-three municipalities pacing commitments to policy timetables.

Competitive Landscape

The South Korea organic waste collection service market is moderately fragmented, with public facilities and private consignment models coexisting and evolving under the capital region’s landfill ban and shifting gate-fee dynamics. Competition plays out across cost, technology, and access to processing capacity, with incumbents retrofitting existing drop-off infrastructure while challengers pursue AI-enabled automation to gain routes and support compliance. Operators that secure multi-year incineration or digestion capacity can reduce fee volatility and present bundled service proposals to cities and commercial customers that value predictability. Over the forecast period, electric and hydrogen fleets are likely to differentiate bids where local governments weigh climate funding and job quality targets alongside per-ton cost metrics.

Several strategic moves highlight these shifts. Busan’s scaled hydrogen truck procurement sets a benchmark for large-city fleet transition within tight urban corridors. Seoul’s pilots with compact electric collection vehicles test solutions for hill-dense neighborhoods where access, safety, and noise are critical to service continuity. AI-enabled routing and recognition initiatives in local governments are a step toward data-first collection planning that blends visual inputs and historical patterns to target timely pickups. Inter-municipal agreements in the capital region also demonstrate a path to reduce reliance on private plants during maintenance at public facilities without causing service lapses.

Price transparency has improved as municipal bidding portals and industry groups publish or challenge rate claims. At the same time, ash-treatment adjustments are increasingly used to compare public and private options on an equivalent basis. Public facility modernization plans through 2030 indicate continued competition for volume and a gradual rebalancing of public-private mixes in the capital region. Meanwhile, private investments in digestion efficiency, solar self-generation, and system redundancy point to long-term strategies anchored in reliable offtake and lower operating costs. The market is likely to reward operators that can align routing technology, zero-emission fleets, and contracted processing into an integrated service package.

South Korea Organic Waste Collection Services Industry Leaders

Reencle

Veolia

OCI SE Co., Ltd.

Envac

DOOBIWON CO., LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Seoul Gangnam District signed contracts with five private incineration plants through nationwide competitive bidding to secure alternative disposal capacity during a major overhaul of the Gangnam Resource Recovery Facility. This proactive contracting reflected a preference for private incineration partnerships over reliance on landfills, despite higher costs.

- December 2025: Hanwha Corporation’s construction division was selected as the preferred bidder for the Busan Suyeong Sewage Treatment Plant modernization project. This large-scale private investment will expand sewage and sludge treatment capacity and strengthen the company’s position in environmental infrastructure.

South Korea Organic Waste Collection Services Market Report Scope

The South Korea Organic Waste Collection Service Market Report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and more), by End-User (Residential, Commercial, and more), by Collection Method (Door-to-Door Collection, Drop-Off / Bring Systems, Others), by Technology (Manual Collection Systems, Semi-Automated Systems, and more). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste |

| Agricultural Residues |

| Others |

| Residential |

| Commercial (HoReCa, Retail) |

| Industrial (Food Processing & Manufacturing) |

| Others (Agri-waste) |

| Door-to-Door Collection |

| Drop-Off / Bring Systems |

| Others |

| Manual Collection Systems |

| Semi-Automated Systems |

| Fully Automated Systems |

| Others |

| By Waste Type | Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste | |

| Agricultural Residues | |

| Others | |

| By End-User | Residential |

| Commercial (HoReCa, Retail) | |

| Industrial (Food Processing & Manufacturing) | |

| Others (Agri-waste) | |

| By Collection Method | Door-to-Door Collection |

| Drop-Off / Bring Systems | |

| Others | |

| By Technology & Equipment | Manual Collection Systems |

| Semi-Automated Systems | |

| Fully Automated Systems | |

| Others |

Key Questions Answered in the Report

What is the size and growth outlook for the South Korea organic waste collection service market to 2031?

The market was USD 235.53 million in 2025 and is projected to reach USD 340.15 million by 2031 at a 6.36% CAGR over 2026-2031.

Which end-user segment is growing fastest in South Korea’s organic waste collection?

Commercial is the fastest, projected at a 7.67% CAGR through 2031, while residential held 53.9% share in 2025.

How is the 2026 landfill ban in the capital region reshaping collection service operations?

The ban redirected an estimated 4,000 tons daily to private incineration, increasing the importance of contracted capacity and exposing operators to gate-fee volatility.

Which collection method is likely to gain share in South Korea?

Door-to-door collection is expanding fastest with an 8.21% projected CAGR, driven by convenience, compliance, and deterrence of illegal dumping.

What technologies are setting the pace for efficiency in collection services?

Fully automated systems are leading growth at an 8.61% projected CAGR, supported by RFID analytics, AI-enabled routing, and behavior incentives that cut waste volumes.

How do biogas policies affect organic waste collection in South Korea?

The biogas act phases in conversion requirements from 2025 for public waste and 2026 for larger private generators, creating stable offtake and contracted feedstock flows for collection operators.

Page last updated on: