Japan Organic Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

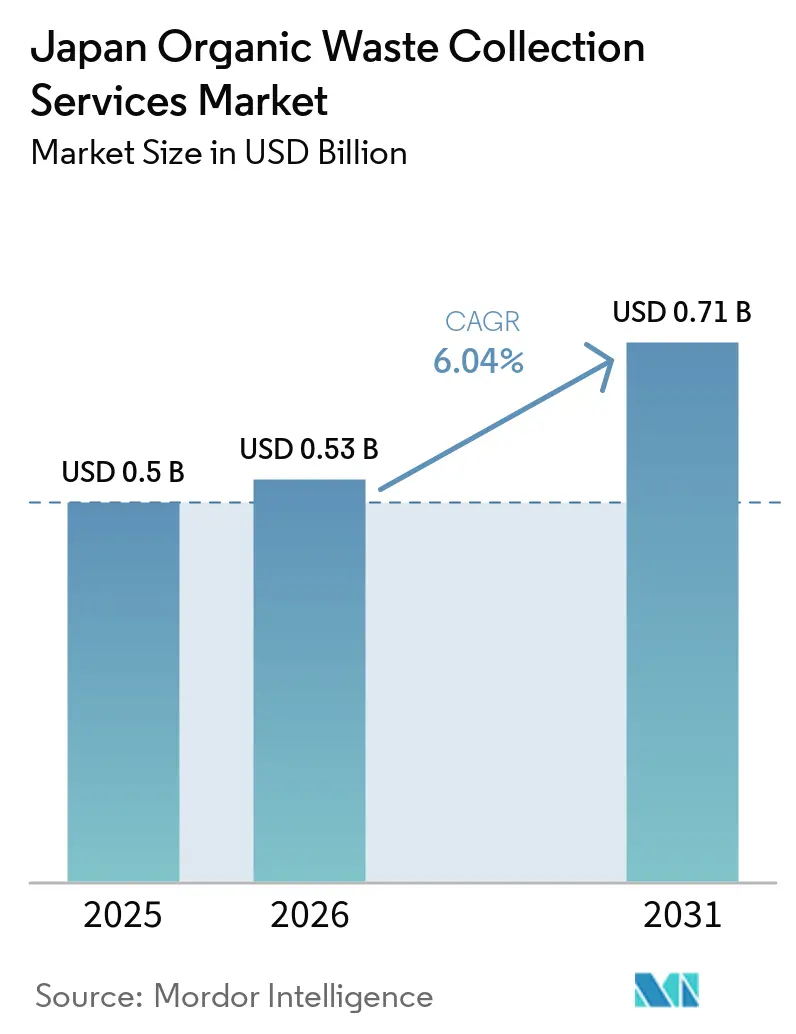

| Base Year Market Size (2025) | USD 0.5 Billion |

| Market Size (2026) | USD 0.53 Billion |

| Market Size (2031) | USD 0.71 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

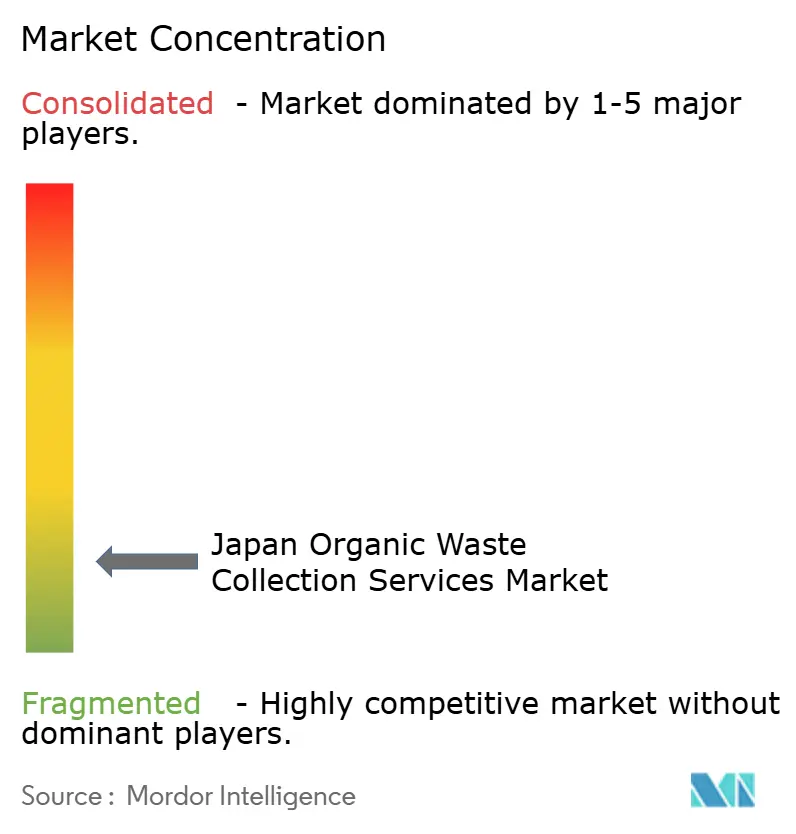

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Organic Waste Collection Services Market Analysis by Mordor Intelligence

The Japan Organic Waste Collection Services Market size is projected to be USD 0.5 billion in 2025, USD 0.53 billion in 2026, and reach USD 0.71 billion by 2031, growing at a CAGR of 6.04% from 2026 to 2031.

Growth reflects tighter policy direction, ongoing landfill constraints, and a steady shift toward biogas and compost pathways in municipal programs and public–private pilots. Regulatory attention has deepened through national circular-economy actions and legal updates that drive higher recycling rates and improved traceability. Municipal waste volumes declined in fiscal 2024 while the national recycling rate remained below 20%, underscoring the need to capture more organics for material or energy recovery. The market is also benefiting from innovations such as automated sorting, EV collection fleets, and IoT-enabled bins that improve route efficiency and reduce labor intensity. Limited final-disposal capacity in major metros further underscores the value of upstream segregation and dedicated collection systems for food waste streams.

Key Report Takeaways

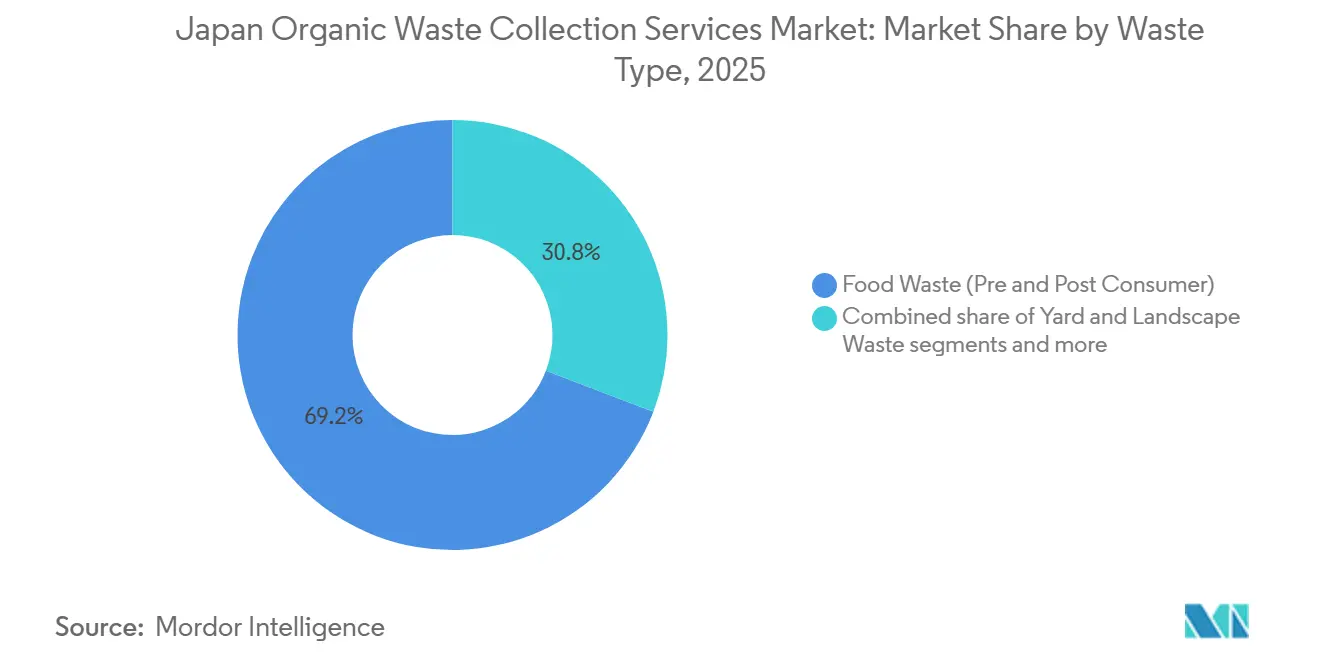

- By waste type, food waste (pre- and post-consumer) led with 69.2% of the Japan organic waste collection services market share in 2025 and is projected to grow at a 6.78% CAGR through 2031.

- By end-user, residential accounted for 54.7% of the Japan organic waste collection services market size in 2025, while commercial (HoReCa, retail) is forecast to expand at a 7.21% CAGR through 2031.

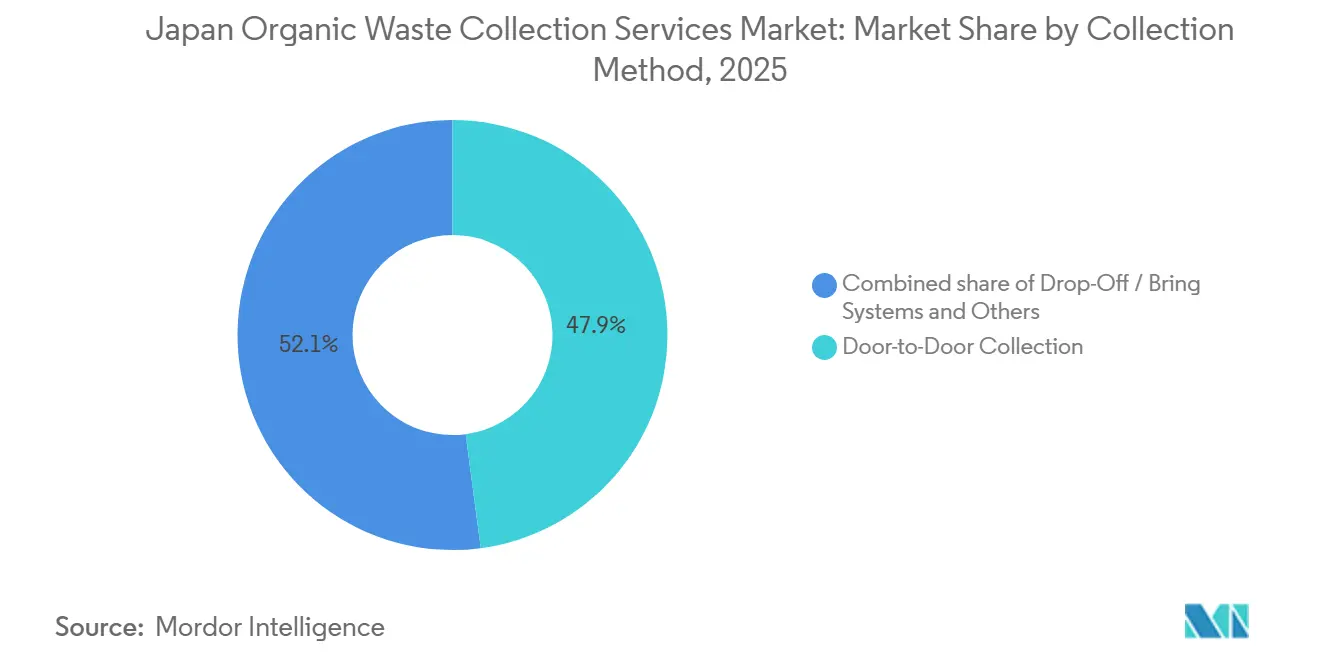

- By collection method, door-to-door collection held 47.9% share in 2025 and is expected to post the highest growth at a 7.42% CAGR through 2031.

- By technology and equipment, semi-automated systems dominated with 54.8% share in 2025, while fully automated systems are projected to grow at a 7.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Organic Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Government Regulations on Waste Segregation and Recycling | +1.8% | National, with early enforcement in Tokyo, Osaka | Medium term (2-4 years) |

| Growing Emphasis on Circular Economy Initiatives | +1.5% | National, pilot projects in Kitakyushu, Osaki Town | Long term (≥ 4 years) |

| Increasing Adoption of Biomass Energy Generation from Organic Waste | +1.2% | Japan core, led by Hokkaido, Kobe, and Sapporo | Medium term (2-4 years) |

| Expansion of Composting Facilities and Biogas Plants | +0.9% | National, concentrated in the Tohoku and Kansai regions | Medium term (2-4 years) |

| Government Subsidies and Incentives for Organic Waste Management | +0.5% | National | Short term (≤ 2 years) |

| Growing Corporate ESG Commitments and Sustainability Reporting Requirements | +0.4% | National, Prime Market firms focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations on Waste Segregation and Recycling

Policy momentum accelerated in 2024 and 2025 with new resource-circulation measures and related enforcement that require clearer reporting on recycling implementation and tighter controls on treatment outcomes. These measures pressure organic waste collectors and processors to improve segregation quality and document outcomes with more detailed manifests and auditable data trails. Planned updates scheduled to take effect around 2026 are also expected to broaden permit regimes for higher-risk materials, reducing mis-sorting and contamination risks in organics flows at the point of intake. In parallel, food-loss and food-recycling policy updates effective in 2025 are pushing enterprises to separate edible surplus from inedible streams and to disclose volumes more consistently, thereby improving upstream quality for separate collection. Together, these shifts translate into higher demand for telemetry, tagging, and container-level verification, enabling haulers to demonstrate segregation quality while lowering treatment risk and supporting national circularity goals.

Growing Emphasis on Circular Economy Initiatives

Japan has elevated the circular economy to a national strategic pillar, framing organics as a priority feedstock for renewable energy and soil health outcomes.[1]Prime Minister’s Office of Japan, “Ministerial Council on the Circular Economy,” Prime Minister’s Office of Japan, japan.kantei.go.jp Municipal case studies demonstrate that systematic separation, collection, and localized processing can scale when programs are designed around clear rules, stable offtake, and practical cost controls. These models favor defined organic pathways that return compost and digestate-derived nutrients to nearby farms, enabling short-haul logistics and more resilient agricultural loops. The Japan organic waste collection service market gains from this policy alignment because municipalities now have clearer targets, better precedent templates, and a stronger rationale for budget proposals tied to organics recovery projects.[2]Ministry of the Environment, “Cabinet Decision on Amendments to the Waste Management and Public Cleansing Law,” Ministry of the Environment, env.go.jp The Ministerial Council on the Circular Economy also signaled harmonization with global disclosure and recycling standards, which nudges enterprises to upgrade data capture across their waste chains. This convergence encourages standardized reporting from haulers and processors, in turn strengthening the investment case for specialized collection services for food waste.

Increasing Adoption of Biomass Energy Generation from Organic Waste

Biogas is taking a growing share within Japan’s renewable energy mix, with organics-to-power and organics-to-heat projects favored for local deployment. City-scale biogas facilities highlight repeatable models that process large daily volumes of food waste into electricity and fertilizer, creating a two-way loop aligned with local decarbonization goals. The market benefits from such anchor assets because they provide a stable offtake for segregated food scraps from commercial and residential districts. As more processors adopt end-to-end traceability, generators can link organics recovery to emissions accounting and energy claims under structured supply arrangements, strengthening demand for reliable, contamination-light organics streams that dedicated collection programs can deliver.

Expansion of Composting Facilities and Biogas Plants

Central and local programs are funding pilots and regional demonstrations to accelerate organics capture and processing, expanding the addressable volume for specialized collection. Municipal initiatives increasingly convert collected food waste into biogas and cycle it back into public infrastructure, supported by transparent tracking of operational and emissions outcomes. Smaller “zero food waste” style pilots also help dispersed generators test separate organics drop-offs and refine sorting, improving the quality and predictability of the collected fraction. Distributed solutions such as containerized micro-digesters for supermarkets or farms provide a bridge when land is tight, or volumes are small enough to be served by central plants. The market benefits from both centralized and distributed investment paths, as each increases the proportion of food scraps that are recoverable with minimal contamination and documented offtake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Investment Costs for Collection Infrastructure and Vehicles | -1.1% | National, acute in Tokyo and Osaka metro areas | Medium term (2-4 years) |

| Limited Land Availability for Waste Processing Facilities in Urban Areas | -0.8% | Tokyo Bay area, Kanto core cities | Long term (≥ 4 years) |

| Seasonal Variations in Organic Waste Generation Affecting Operational Efficiency | -0.4% | National, pronounced in agricultural regions | Short term (≤ 2 years) |

| Shortage of Skilled Workforce in the Waste Management Sector | -0.5% | Rural areas, Tohoku, and Kyushu municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment Costs for Collection Infrastructure and Vehicles

Capital requirements for new waste treatment and recycling facilities continue to strain municipal finances, even when subsidies are available. Large-scale energy recovery and recycling plants often create multi-decade debt service commitments after accounting for grants, bonds, and general revenue allocations. Site preparation, footprint constraints, and phasing requirements can add to procurement burden and extend payback periods. On the fleet side, EV refuse vehicles and modern compaction bodies can improve emissions performance and routing outcomes, but higher upfront costs increased reliance on leasing and phased deployments. As a result, adoption curves can diverge between cash-rich urban districts and smaller municipalities facing shrinking tax bases. Operators are responding by rolling out modular equipment in phases and prioritizing pilots that deliver quick wins in the organics fraction, building support for subsequent capital phases.

Limited Land Availability for Waste Processing Facilities in Urban Areas

Urban land scarcity raises project risk for siting or expanding compost and digester assets, especially where residential encroachment and safety buffers restrict options. Limited remaining landfill capacity in major metros increases pressure for upstream solutions that reduce final disposal volumes, keeping organics collection in focus. Planning and redevelopment constraints can complicate rebuilds or capacity additions, forcing longer construction phases and more complex staging to maintain service continuity. Additional screening criteria such as proximity to sensitive facilities and hazard zones can eliminate many candidates early, prolonging timelines and adding off-site utility and access costs. These realities push many municipalities toward upgrading existing footprints rather than pursuing new greenfield sites. Collection programs must therefore emphasize high-quality separation and stable offtake so that existing processing facilities can run at higher yields and lower contamination levels without requiring large land expansions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Food Waste Captures Two-Thirds of Kitchen Efficiency Gains

Food waste held 69.2% share in 2025 and is forecast to grow at a 6.78% CAGR through 2031, reflecting regulatory pressure and operational changes in how surplus is handled and disclosed. Policy updates are encouraging retailers and food-service operators to prioritize donating edible surplus, extend shelf life where feasible, and separate edible from inedible streams at source, thereby improving upstream quality for separate collection.[3]Ministry of Agriculture, Forestry and Fisheries, “Outline of the Revised Food Recycling Law Ordinance,” MAFF, maff.go.jp These dynamics favor urban curbside programs and contracted pickups for supermarkets, convenience chains, and cafeterias that can maintain high segregation standards and stable volumes. In parallel, projects that convert fermentation residue to fertilizer or other usable outputs strengthen offtake certainty, improving the economics of recurring organics routes.

Yard and landscape waste, as well as agricultural residues, follow distinct logistics patterns. Yard waste is seasonal and aligns with periodic collections and compost-site throughput constraints. In rural prefectures, crop residues may be integrated into digesters or compost systems that feed nutrients back to farms, often through circular-agriculture pilots. Miscellaneous organic streams, such as fish-processing byproducts or brewery residues, can also be captured where local operators have a reliable offtake for feed, compost, or biogas applications. While priorities vary by region, the overall direction remains consistent: more defined collection points, clearer contamination rules, and more predictable offtake especially for food waste, which accounts for most revenue.

By End-User: Commercial Surges as Restaurants Close the Loop

Residential generators accounted for 54.7% of demand in 2025 and continue to underpin base route density in cities and towns. Household incentives in select municipalities (such as subsidies for home processing containers) can reduce curbside volumes and contamination, improving routing and capacity planning. Commercial segments are expanding faster, at a 7.21% CAGR, as supermarkets, restaurant groups, and large canteens embed organic recovery into ESG programs and cost-control initiatives. Commercial contracts increasingly route food scraps to biogas plants and use structured arrangements to return electricity value to participating sites, strengthening long-term demand for scheduled pickups and contamination-light streams.

Industrial food processors show similar momentum as they pursue decarbonization milestones and seek credible emissions reductions through energy recovery and return-power models. Collection providers support these users by synchronizing pickups with production cycles and integrating weight-based audits that connect waste data to internal reporting dashboards. Residential volumes will remain important for route efficiency, while faster commercial growth signals deeper integration of organics capture into occupational kitchens and national retail chains. This trend is steering investments toward urban transfer points and stronger data systems to meet customer reporting expectations and improve benchmarking across multi-site operators.

By Collection Method: Door-to-Door Gains Digital Tracking Edge

Door-to-door Collection held a 47.9% share in 2025 and is also the fastest-growing method, with a 7.42% CAGR, supported by data-enabled containers and compactors that report fill levels and improve mileage efficiency. Municipal programs are increasingly pairing container tracking with analytics for route balancing, helping reduce missed pickups, improve driver safety, and enable predictive maintenance. Drop-off systems remain relevant in low-density areas and can be combined with surplus-food diversion initiatives that prevent edible items from becoming waste. Over time, grants and pilots are helping communities test low-cost collection points and scanning workflows that reduce contamination and enable batch transport to regional facilities.

Door-to-door growth is expected to continue as cities expand curbside organics bins and enforce clear contamination standards that keep downstream processing stable. More integrated data across trucks, containers, and receiving facilities will enable performance-based contracts that optimize collection frequency while reducing per-ton costs. Hybrid approaches combining scheduled routes with event-based or mobile collection can fill gaps in multi-family housing and mixed-use districts where access and storage constraints complicate standard curbside programs.

By Technology & Equipment: Fully Automated Systems Sprint Toward AI Parity

Semi-automated systems dominated with 54.8% share in 2025 due to broad utility across compactors, transfer points, and collection workflows that still require manual handling in many districts. As automation performance improves and costs trend down, fully automated systems are projected to grow at a 7.89% CAGR, supported by advances in AI-based recognition that reduce contamination and improve worker safety. Ongoing validation through extended pilots is helping operators benchmark automated outcomes against manual baselines and refine deployment requirements for different waste compositions and facility layouts.

Complementary technologies are also progressing, including advanced sensor-based sorting approaches that improve contaminant identification and material separation accuracy. Battery detection and hazard screening systems reduce fire risk and downtime at treatment facilities, improving safety and operational continuity. Over the forecast period, adoption will be strongest where contamination risk is high or where labor shortages make productivity gains essential. In the near term, semi-automated fleets will provide a base for gradual upgrades. At the same time, fully automated lines will expand in higher-volume hubs that can justify capital deployment tied to measurable safety and yield improvements.

Geography Analysis

The market shows earlier adoption in dense metropolitan areas, where waste volumes support strong route economics and policy pressure is typically highest. Tokyo and the broader Kanto region have led pilots of smart containers that compress waste and report fill levels, enabling reductions in collection frequency in high-traffic districts. Limited final-disposal runways in major metros highlight the need for upstream segregation, energy recovery, and reporting that validates diversion performance. As a result, large cities increasingly emphasize food-waste routes supported by processing assets that can return energy or fertilizer value to municipal operations and nearby partners.

Hokkaido and Tohoku are emerging as strongholds of biogas, combining organics-to-power with fertilizer use, supported by agricultural residues and municipal food scraps. City-scale plants provide anchor capacity for collection services, enabling them to schedule frequent pickups from schools, retailers, and food factories while maintaining a stable offtake. The fertilizer loop ties organic value to local farms, which can strengthen community support and permit approval. Distributed solutions that handle smaller loads at supermarkets or farms also help in areas with long distances to central sites, enabling stepwise capacity addition without large land acquisitions.

In Kansai and Chubu, industrial–academic partnerships and city utility projects are integrating organics into broader energy and resource-circulation plans. Municipal circular models that convert collected food waste into biogas power for local infrastructure demonstrate how public facilities can operate with higher shares of renewable electricity while improving diversion outcomes. Demonstration funding supports pilots for efficient organics collection and drop-off systems, strengthening data needed for scaling. In rural areas and parts of Kyushu, smaller tax bases can slow new facility development, but targeted subsidies and long-term offtake agreements can still support steady route expansion and rising capture of food scraps.

Competitive Landscape

The market remains fragmented, with municipal consortia, regional operators, and specialized processors forming localized ecosystems. Few players have national reach, and many projects are structured as partnerships that share investment and operational risk across public and private entities. This structure favors differentiation through technology, data capture, and circular service models that connect recovered organics to energy and soil products with traceable outcomes for customers.

Technology suppliers are also shaping competition as operators invest in automation, safety, and emissions reduction. Advances in unmanned and sensor-enabled sorting are improving performance, even where contamination remains a persistent bottleneck. Battery detection and hazard screening reduce fires and downtime at processing facilities, lowering operational disruption and improving worker safety. Fleet upgrades such as EV-capable refuse vehicles and more efficient compaction bodies support lower lifecycle emissions and can reduce fuel and maintenance exposure where routes are dense and predictable.

Digital transformation is accelerating along collection routes. Pilots that stream real-time vehicle status, location, and payload to dispatch teams are strengthening the case for wider adoption and for performance-based contracts. Smart compactor bins in high-traffic districts have demonstrated reductions in collection frequency while improving street cleanliness, supporting public acceptance of curbside organics programs. In parallel, municipal energy strategies increasingly align with waste objectives, reinforcing investment in systems that connect recovery performance to measurable energy and emissions outcomes.

Japan Organic Waste Collection Services Industry Leaders

ECOMMIT Co., Ltd.

Mitsuboshi Sangyo Ltd.

YAMAICHISHOJI, Inc.

Shirai Group

JERS Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: On April 1, 2026, Kobe City launched the "Biomass Acceptance Project" at its Higashinada Wastewater Treatment Plant, becoming Japan's first municipal wastewater facility to accept food waste (16.5 tons/day) for co-digestion with sewage sludge. Operated under a PPP model by KOBE Bioswedge Co., Ltd., the project runs through March 2044. It is expected to generate ~1.3 million kWh/year (electricity for ~400 households) and cut GHG emissions by ~3,100 tons-CO₂/year, serving as a model for other municipalities in Japan.

- February 2026: On February 23, 2026, Aeon Agri Create and Toyohashi Biomass Solutions opened the Kazo Circular Economy Research Base in Saitama Prefecture. Supported by Japan's Ministry of Agriculture, Forestry and Fisheries, the facility converts food and agricultural waste into biogas and liquid fertilizers for hydroponic cherry tomato cultivation, completing a closed-loop resource cycle for energy and nitrogen

- December 2025: Yokohama became the first Japanese city to municipally roll out automated "SDGs Locker" food waste collection stations at train stations, with each unit projected to divert over 12 tonnes of food waste annually, drawing replication interest from cities including Fukuoka and Sapporo under Japan's national target to halve household food waste by 2030.

- May 2025: J&T Recycling Corporation commenced operations of Hokkaido's largest food waste biogas power plant in Sapporo City, processing 100 tonnes of organic waste per day and generating approximately 16,420 MWh of electricity annually, while converting fermentation residue into fertilizer as part of a double recycling loop.

Japan Organic Waste Collection Services Market Report Scope

The Japan Organic Waste Collection Services Market Report is Segmented by Waste Type (Food Waste, Yard & Landscape Waste, and More), by End-User (Residential, Commercial, and More), by Collection Method (Door-To-Door Collection, and More), and by Technology & Equipment (Manual Collection Systems, Semi-Automated Systems, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste |

| Agricultural Residues |

| Others |

| Residential |

| Commercial (HoReCa, Retail) |

| Industrial (Food Processing & Manufacturing) |

| Others (Agri-waste) |

| Door-to-Door Collection |

| Drop-Off / Bring Systems |

| Others |

| Manual Collection Systems |

| Semi-Automated Systems |

| Fully Automated Systems |

| Others |

| By Waste Type | Food Waste (Pre and Post Consumer) |

| Yard & Landscape Waste | |

| Agricultural Residues | |

| Others | |

| By End-User | Residential |

| Commercial (HoReCa, Retail) | |

| Industrial (Food Processing & Manufacturing) | |

| Others (Agri-waste) | |

| By Collection Method | Door-to-Door Collection |

| Drop-Off / Bring Systems | |

| Others | |

| By Technology & Equipment | Manual Collection Systems |

| Semi-Automated Systems | |

| Fully Automated Systems | |

| Others |

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan organic waste collection services market?

The market stood at USD 0.50 billion in 2025 and is projected to reach USD 0.71 billion by 2031 at a 6.04% CAGR over 2026–2031.

Which waste type is leading demand today?

Food waste was the largest segment, with 69.2% share in 2025, supported by stricter food recycling practices and expanded separate collection by businesses and municipalities.

What collection method is expanding the fastest?

Door-to-door collection is the fastest-growing method, supported by container telemetry and route optimization that reduces mileage and labor intensity.

How are regulations shaping the Japan organic waste collection services market?

Recent policy and regulatory updates are raising expectations for greater recycling implementation, better disclosure, and tighter permitting, which, in turn, are increasing demand for traceable, high-quality organics collection and compliant downstream processing.

What technologies are improving safety and efficiency in organic handling?

AI-enabled sorting, battery and hazard screening, and EV-capable collection equipment are improving safety, uptime, and emissions performance across collection and preprocessing.

Which regions are setting the pace for adoption?

Greater Tokyo and Kanto are leading the adoption of smart containers and route analytics, while Hokkaido and Tohoku are scaling biogas loops that return fertilizer and energy value to local users.

Page last updated on: