Croatia Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

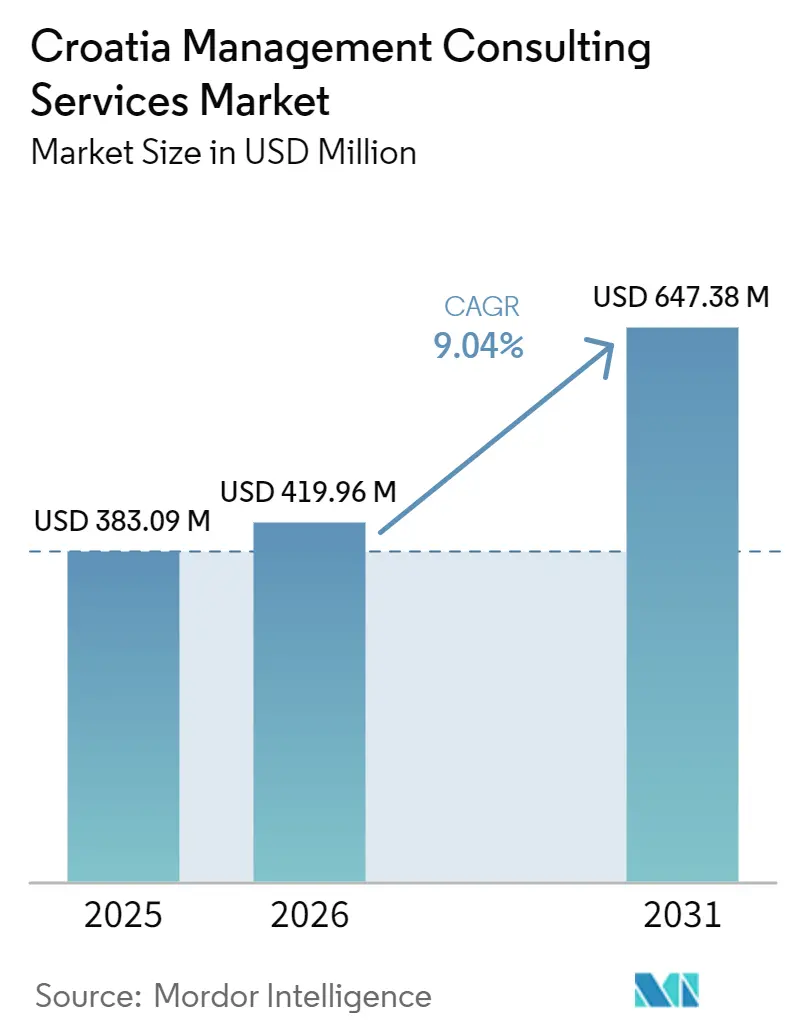

| Base Year Market Size (2025) | USD 383.09 Million |

| Market Size (2026) | USD 419.96 Million |

| Market Size (2031) | USD 647.38 Million |

| Growth Rate (2026 - 2031) | 9.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia Management Consulting Services Market Analysis by Mordor Intelligence

The Croatia management consulting services market size is projected to be USD 383.09 million in 2025, USD 419.96 million in 2026, and reach USD 647.38 million by 2031, growing at a CAGR of 9.04% from 2026 to 2031. Momentum stems from Croatia’s deepening alignment with European digital and regulatory frameworks after euro and Schengen entry, which lifted confidence among foreign investors and regional corporates. Mandatory Corporate Sustainability Reporting Directive compliance, expanding EU-funded digital-transformation grants and the new foreign direct investment screening regime together create a multi-year pipeline of high-value advisory mandates. Near-shore delivery advantages, supported by bilingual talent and cost competitiveness against Western European labor rates, continue to attract cross-border projects. At the same time, a fragmented consulting ecosystem allows both global firms and specialized boutiques to capture opportunity niches, especially in blue-economy and public-sector innovation programs.

Key Report Takeaways

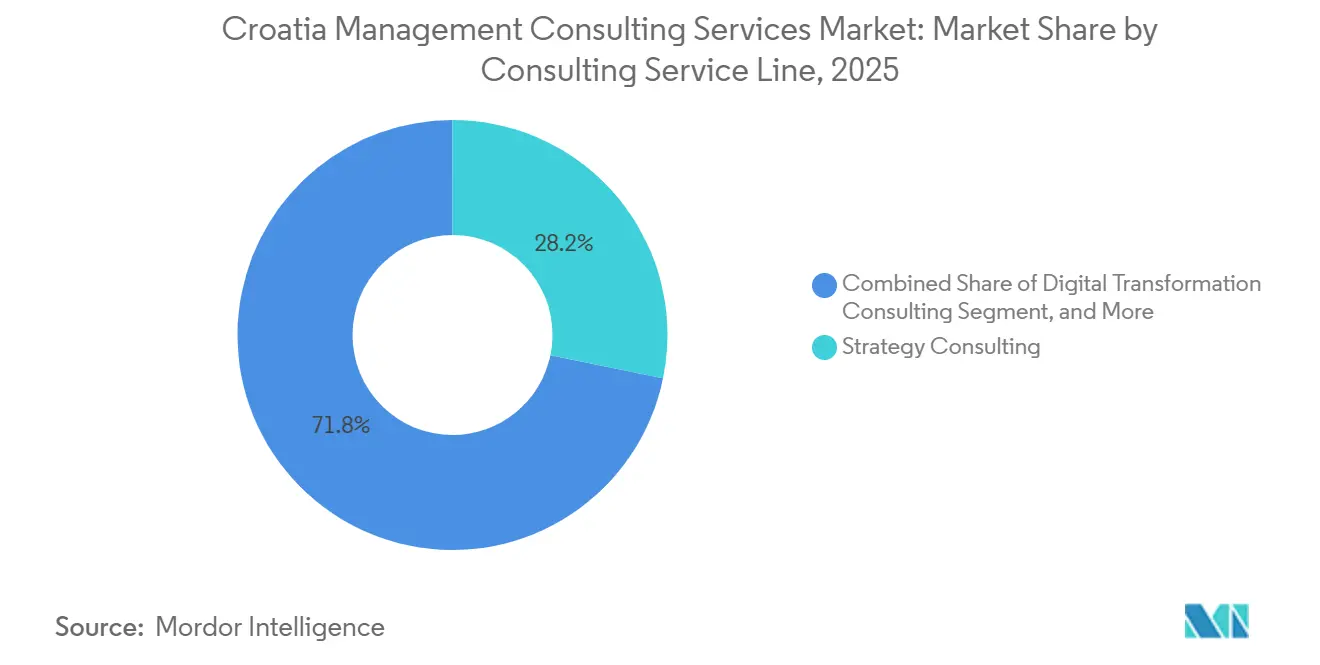

- By consulting service line, Strategy Consulting led with 28.23% of the Croatia management consulting services market share in 2025, while Digital Transformation Consulting is projected to advance at an 11.09% CAGR through 2031.

- By organization size, Large Enterprises accounted for 70.79% of the Croatia management consulting services market in 2025, whereas Small and Medium-Sized Enterprises are forecast to grow fastest at a 10.17% CAGR to 2031.

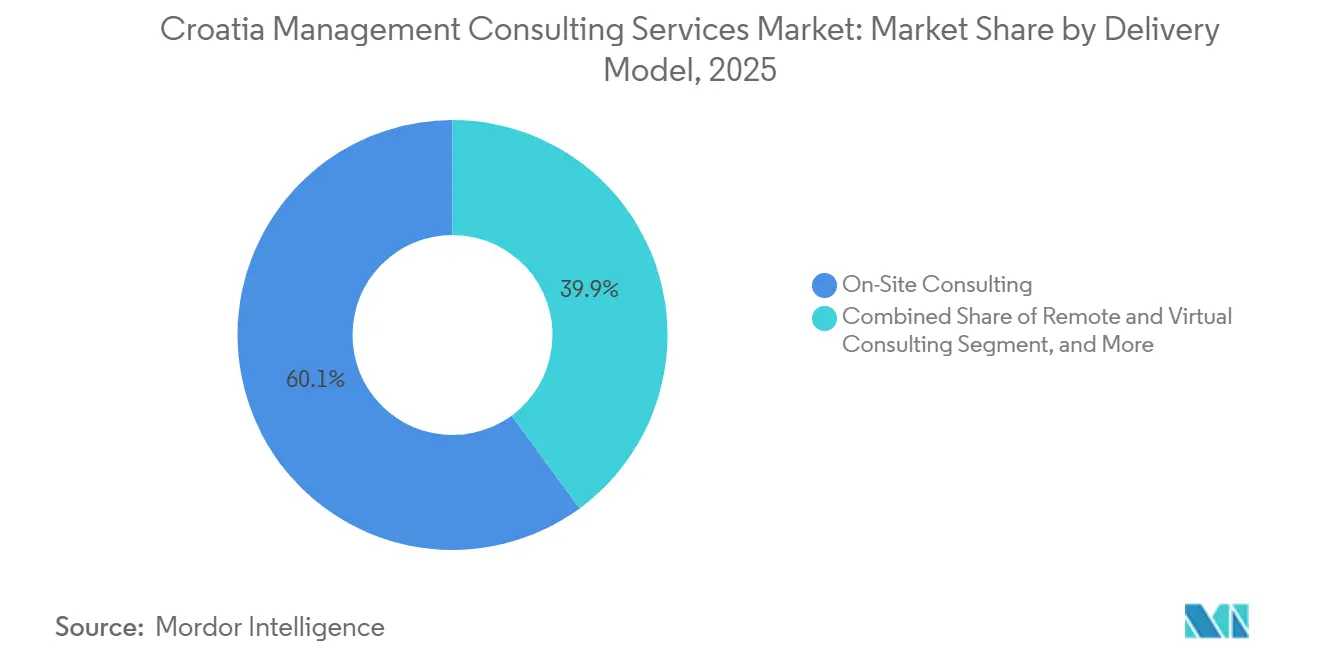

- By delivery model, On-Site Consulting retained 60.07% of the Croatia management consulting services market size in 2025, yet Remote and Virtual Consulting is expected to expand at a 9.76% CAGR during 2026-2031.

- By end-user industry, IT and Telecommunications captured 22.34% share of the Croatia management consulting services market in 2025, while Healthcare is poised for the highest growth at a 9.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Croatia Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Funded SME Digital-Transformation Grants Surge | +2.1% | National, concentrated in Pannonian, Adriatic and Northern Croatia | Short term (≤ 2 years) |

| ESG Reporting Mandates Under CSRD Intensify Compliance Spend | +1.8% | National, spillover to subsidiaries of EU-listed multinationals | Medium term (2-4 years) |

| FDI-Led M&A Pipeline Elevates Deal-Advisory Demand | +1.5% | National, focus on Zagreb and coastal urban centers | Medium term (2-4 years) |

| Near-Shore Delivery Growth After Euro Adoption | +1.3% | Zagreb and Split tech hubs | Long term (≥ 4 years) |

| Smart Islands and Blue Economy Initiatives Require Specialized Consulting | +0.9% | Adriatic Croatia, Dalmatian islands, coastal municipalities | Long term (≥ 4 years) |

| NATO Defense-Spending Ramp-Up Spurs Strategy Engagements | +0.7% | National, defense procurement centered in Zagreb | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-Funded SME Digital-Transformation Grants Surge

Croatia’s National Recovery and Resilience Plan and the Digital Europe Programme channel sizable capital into voucher schemes and innovation hubs that compel SMEs to seek external advisory support. Individual grants of EUR 30,000-120,000 (USD 33,300-133,200) cover cybersecurity, digital marketing and product development, with co-financing up to 80%, creating predictable demand for proposal writing, digital maturity assessments and implementation roadmaps.[1]Croatian Agency for SMEs, Innovation and Investments, “Supporting Business Development,” hamagbicro.hr The EDIH CROBOHUB++ consortium alone secured EUR 2.86 million (USD 3.18 million) to deliver test-before-invest and integration services that are executed primarily by consulting partners. A EUR 15 million (USD 16.65 million) DIGIT Challenge call further broadens project-design opportunities for multidisciplinary teams. Because disbursement rules mandate third-party expertise, consulting firms that master EU-fund navigation gain rapid access to a captive SME client base already pre-funded for advisory spend.

ESG Reporting Mandates Under CSRD Intensify Compliance Spend

The July 2024 transposition of CSRD into Croatian law imposes phased sustainability disclosure obligations that escalate from large public-interest entities to listed SMEs by 2027.[3]Luka Burilović, “Croatia’s Path to 2026: ESG, AI and Skills Shaping a Competitive Economy,” Bloomberg Adria, bloombergadria.com Double materiality analysis, supply-chain due diligence and XBRL tagging require integrated financial, legal and technical capabilities that most corporates lack internally. Monetary penalties and mandatory limited assurance heighten risk, prompting boards to allocate dedicated budgets for ESG advisory, data architecture and audit readiness. Croatia’s first domestic ESG rating system, launched by the Chamber of Economy, reinforces market pressure for credible reporting standards.[2]Wolf Theiss, “Key Insights on CSRD Reporting Requirements for Companies Operating in the Croatian Market,” wolftheiss.com As the EU’s February 2026 Omnibus amendments tighten thresholds, spend concentrates among Croatia’s largest companies and multinational subsidiaries, favoring firms able to deliver cross-border, multi-disciplinary solutions.

FDI-Led M&A Pipeline Elevates Deal-Advisory Demand

The Foreign Direct Investment Screening Act, effective November 2025, obliges non-EEA investors to notify any acquisition of 10% or more, extending review periods to as long as 150 days and granting retroactive authority for three years. This complexity adds valuation uncertainty and increases diligence workloads, driving demand for regulatory risk mapping, ownership tracing and committee liaison services. With cumulative FDI exceeding EUR 30 billion (USD 33.3 billion) from 2014-2025 and marquee deals such as Podravka’s EUR 333 million (USD 369.63 million) agricultural acquisition, Croatia remains an active transaction market. Consulting firms that combine legal, financial and policy expertise secure a differentiated advisory position, especially as investors seek structures that mitigate review delays and potential vetoes. European Investment Bank financing flows of EUR 536 million (USD 595.96 million) in 2025 further stimulate downstream project-preparation mandates linked to cross-border capital.

Near-Shore Delivery Growth After Euro Adoption

Eurozone entry eliminated currency risk while Schengen access simplified consultant travel, reinforcing Croatia’s proposition as a cost-effective near-shore hub for German, Austrian and Italian clients. Senior software architects in Zagreb earn about 70-80% of Western European peers, allowing consulting firms to price transformation projects competitively yet maintain attractive margins. English proficiency ranks among the world’s top-ten, and widespread German and Italian fluency improves cultural alignment with core client markets. Firms increasingly deploy hybrid delivery, splitting analytical work remotely and reserving on-site workshops for critical milestones, reducing travel cost without sacrificing relationship depth. Satellite offices in Split and other second-tier cities extend capacity and help mitigate Zagreb’s senior-talent bottleneck, sustaining the Croatia management consulting services market’s appeal for high-value, near-shore engagements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consultant Talent Drain to Western Europe | -1.4% | Zagreb and Split tech hubs | Short term (≤ 2 years) |

| Small Domestic Addressable Market and Fee Sensitivity | -0.8% | National | Long term (≥ 4 years) |

| Fragmented Public-Sector Procurement Framework | -0.6% | National, municipal and central tenders | Medium term (2-4 years) |

| Freelance Platforms Exert Downward Price Pressure | -0.4% | National, digital and IT consulting | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consultant Talent Drain to Western Europe

Croatia loses roughly 1,200 ICT professionals each year, and 40% of the top graduates from premier technical faculties immediately emigrate, mainly to Germany, Austria and Ireland where salaries can be triple domestic levels. Zagreb alone faces 7,500-9,000 unfilled ICT positions, driving fierce competition for senior cloud architects, AI engineers and cybersecurity experts. Foreign subsidiaries in Croatia often pay 30-40% premiums over domestic firms, further squeezing local consulting margins. Time-to-hire for niche senior roles now averages more than four months outside the capital, forcing firms to rely on offshore staffing or project delays.[4]KiTalent Research Team, “Split’s ICT Sector Is Growing Fast and Hiring Slowly: The Talent Bottleneck Behind Croatia’s Second Tech Hub,” kitalent.com Persistent talent leakage directly constrains delivery capacity, particularly for digital transformation and AI engagements that anchor the fastest-growing segments of the Croatia management consulting services market.

Small Domestic Addressable Market and Fee Sensitivity

Croatia’s economy of under USD 80 billion (USD 88.8 billion) limits the scale of private-sector consulting budgets, while SMEs remain highly price sensitive, often demanding success-based or heavily modularized fee structures. Public-fund support mechanisms such as vouchers lower entry barriers yet also cap billable hours per engagement. Domestic clients frequently compare global firm rates with freelance platform offerings, pressuring traditional firms to unbundle services or accept reduced scopes. Although near-shore demand helps offset local constraints, reliance on foreign clients exposes firms to exchange-rate fluctuations and external economic cycles. Together, these factors temper revenue expansion potential despite favorable growth drivers, moderating overall profitability across the Croatia management consulting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Ascends From a Lower Base

Digital Transformation Consulting is the fastest-growing line, advancing at an 11.09% CAGR through 2031, yet it still trailed Strategy Consulting, which held a 28.23% share of the Croatia management consulting services market in 2025. Mandatory e-invoicing starting in 2026, National Recovery and Resilience Plan funding and rising AI adoption all push clients toward end-to-end technology roadmaps. Strategy engagements retain boardroom relevance for market entry, post-merger integration and growth blueprints, but many now incorporate digital deliverables. Operations Consulting benefits from an Industry 4.0 readiness gap, as manufacturers seek lean programs and automation audits that bridge legacy processes with smart-factory ambitions. Financial Advisory and Risk and Compliance remain buoyed by the FDI screening act, CSRD audits and DAC8 data-exchange rules that demand complex valuations and governance redesign. Together, these dynamics redirect wallet share toward multidisciplinary teams that fuse strategy, technology and risk skills.

Despite the lower starting point, Digital Transformation’s momentum is large enough to re-shape overall revenue mix by 2031. The Croatia management consulting services market size flowing to pure strategic work will decline slightly in proportional terms, even as absolute spending rises, because clients bundle cloud migration, cybersecurity hardening and data-platform build-outs into their transformation budgets. Firms with proprietary accelerators or ecosystem partnerships capture outsized project scopes, while single-discipline boutiques risk relegation to subcontractor status. Advisory on conversational AI, prompted by recent agentic AI pilots, exemplifies how new service niches quickly gain traction. As a result, service-line boundaries blur and competitive differentiation pivots on the ability to orchestrate multidisciplinary teams at near-shore cost levels.

By Organization Size: SME Demand Outpaces Enterprise Budgets

Large Enterprises dominated with 70.79% of the Croatia management consulting services market in 2025 because they shoulder CSRD, FDI screening and multi-country compliance burdens that require integrated advisory. Their average engagement value frequently tops USD 1 million and spans multi-year transformation roadmaps, enabling firms to assign dedicated on-site teams. Board-level urgency around ESG reporting and global tax alignment preserves this segment’s spending resilience through economic cycles. However, procurement sophistication and rate benchmarking keep margin pressure high, encouraging vendors to deliver with blended on-shore and near-shore teams.

Small and Medium-Sized Enterprises expand their spending base faster, forecast at a 10.17% CAGR to 2031, fueled by voucher schemes, Urban Development Fund loans and EDIH CROBOHUB++ support that earmark consulting as an eligible cost. These subsidies ease fee sensitivity and create a predictable funnel of grant-compliant advisory mandates. The Croatia management consulting services market size attributable to SMEs remains smaller than the enterprise pool, yet its growth rate makes it a strategic priority for mid-tier and boutique firms seeking repeatable, template-based assignments. Engagement models often involve modular work-packages, success-based pricing and capacity-building workshops so SMEs can absorb new processes without large internal teams.

By Delivery Model: Hybrid Becomes the New Normal

On-Site Consulting held 60.07% share in 2025 because Croatian clients still prefer face-to-face collaboration for strategy definition, stakeholder alignment and change-management workshops. Cross-border European buyers also value periodic in-person sessions in Zagreb or Split when project milestones demand executive sign-off. Travel restrictions loosened after Schengen entry, keeping physical workshops viable while reducing administrative friction.

Remote and Virtual Consulting, projected to rise at a 9.76% CAGR, capitalizes on robust broadband, ubiquitous collaboration tools and client pressure to trim travel costs. Most new scopes adopt a hybrid structure that reserves key workshops for on-site delivery and shifts analytics, coding and documentation to virtual teams. This blend safeguards relationship depth yet lets firms unlock Croatia’s near-shore labor arbitrage for Western European clients. The Croatia management consulting services market share of fully virtual delivery remains modest, but its steady uptick pushes firms to invest in secure digital workspaces, remote-first project governance and asynchronous communication playbooks.

By End-User Industry: Healthcare Sets the Pace

IT and Telecommunications remained the largest client vertical with a 22.34% share of the Croatia management consulting services market in 2025, sustained by modernization of core networks, cloud migration and cybersecurity upgrades. Telcos also act as early adopters for AI-driven customer-experience pilots, creating multi-phase transformation roadmaps. Manufacturing keeps drawing lean and Industry 4.0 advisory as plants strive to elevate an average readiness score still below European peers.

Healthcare, forecast to post the fastest 9.92% CAGR, benefits from the e-Health Strategic Development Plan, telemedicine rollouts and electronic health-record interoperability efforts that demand process redesign and technology integration. Public-sector programs for affordable housing, maritime mobility and blue-economy skills funnel additional advisory mandates into coastal cities, widening the end-user mix. Banking and Insurance accelerate spending on digital banking platforms and regulatory compliance, while Tourism taps destination-marketing and sustainability consultants to upgrade visitor experiences. Collectively, these shifts diversify project pipelines and reduce overreliance on any single vertical, underpinning healthy growth for the Croatia management consulting services market.

Geography Analysis

Zagreb anchors demand, housing roughly 60% of the national ICT workforce and the headquarters of all major global consulting brands. Its dominance rests on the concentration of corporate head offices, ministries and financial regulators that commission high-value transformation and compliance programs. The city also hosts regional delivery centers where global firms co-locate data-analytics, finance and legal support units, reinforcing agglomeration effects.

Split ranks as the second tech hub with an ICT talent pool exceeding 4,800 professionals and double-digit annual growth. Local subsidiaries of international software firms and home-grown scale-ups increasingly outsource process-improvement and AI-design tasks to consulting partners, adding depth to regional pipelines. Coastal cities such as Rijeka, Pula and Dubrovnik generate specialized mandates tied to blue-economy, port infrastructure and tourism strategy, supported by EU military-mobility grants and smart-island pilots.

Inland Pannonian counties lean on manufacturing and agriculture, prompting Industry 4.0 audits and EU Common Agricultural Policy compliance work. Northern Croatia, with emerging tech clusters around university research projects, requests innovation roadmaps and spin-out commercialization advice. While uniform EU regulations apply nationwide, enforcement sophistication differs, keeping premium advisory demand centered in Zagreb. Nonetheless, electronic procurement thresholds introduced in early 2026 boost visibility of municipal tenders, gradually widening geographic participation in the Croatia management consulting services market.

Competitive Landscape

Global firms such as Deloitte Croatia, PwC Croatia, KPMG Adria and EY Croatia compete head-to-head with strategy specialists like McKinsey Croatia and sector-focused players including Horwath HTL Croatia. Big Four practices leverage regional delivery hubs and alliances, for example Deloitte’s March 2026 agreement with ElevenLabs, to embed agentic AI accelerators in client roadmaps, widening the technology gap over mid-tier rivals. KPMG’s 2024 merger of Croatian, Slovenian and Bosnian units into KPMG Adria pooled more than 400 professionals and met the parent network’s USD 300 million revenue threshold for advanced platform investment.

Boutique consultancies, among them Happtory and UHY Croatia, defend share in EU-fund application, SME capacity-building and blue-economy niches where relationship capital and local knowledge outweigh scale. Nevertheless, rising CSRD and FDI screening complexity pushes corporates toward firms that can field multidisciplinary teams across legal, tax and tech, concentrating marquee projects in the top tier. Freelance platforms and employer-of-record providers siphon commodity assignments by matching Western European buyers directly with Croatian experts, compressing price points for standard research, process mapping and basic system configuration.

Competitive intensity is greatest in digital transformation and ESG compliance, where mandatory timelines produce time-boxed demand spikes. Firms differentiate through proprietary accelerators, sector playbooks and near-shore talent pools rather than rate discounting alone. Mid-tier international brands lacking regional integration, illustrated by Roland Berger’s Croatian unit liquidation, risk exit unless they pivot to high-specialty offerings or join larger alliances. Overall, the Croatia management consulting services market rewards players that combine global tooling with local delivery economics and sector-specific insight.

Croatia Management Consulting Services Industry Leaders

Deloitte Croatia

PwC Croatia

EY Croatia

KPMG Croatia

McKinsey and Company Croatia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Deloitte Central Europe partnered with ElevenLabs to roll out agentic AI solutions that help enterprises build and govern omnichannel AI agents integrated with core systems, marking the region’s first Big Four–conversational-AI alliance.

- March 2026: HBOR received an S&P rating upgrade to “A” and unveiled new energy-efficiency financing lines with principal write-offs up to 50% for qualifying SME modernization projects.

- January 2026: Croatia enforced DAC8 and DAC9 through amendments to its administrative-cooperation act, triggering new tax-data exchange and crypto-asset reporting obligations.

- January 2026: Mandatory domestic B2B e-invoicing took effect, requiring companies to deploy compliant platforms and update VAT workflows.

Croatia Management Consulting Services Market Report Scope

The Croatia Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

How large is Croatia's management consulting services market today?

The market reached USD 383.09 million in 2025 and is expected to expand to USD 419.96 million in 2026 and USD 647.38 million by 2031.

Which consulting service line is growing fastest in Croatia?

Digital Transformation Consulting is projected to post the highest 11.09% CAGR between 2026 and 2031, outpacing all other service lines.

Why is SME consulting demand rising so quickly?

Voucher programs, Urban Development Fund loans and EU Digital Europe grants pre-finance advisory costs, lifting SME spending at a forecast 10.17% CAGR through 2031.

How does Croatia's euro and Schengen membership influence consulting delivery?

Currency-risk removal and seamless cross-border travel strengthen Croatia's position as a near-shore hub, enabling hybrid on-site and remote project models for Western European clients.

What are the main regulatory drivers of consulting spend?

CSRD sustainability reporting, the FDI screening act, DAC8 and DAC9 tax directives and mandatory B2B e-invoicing create sustained demand for compliance, risk and transaction advisory.

Which end-user industry will offer the strongest growth potential?

Healthcare, supported by the national e-Health Strategic Development Plan and telemedicine investments, is forecast to grow consulting spend at 9.92% CAGR through 2031.

Page last updated on: