Data Center RFID Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

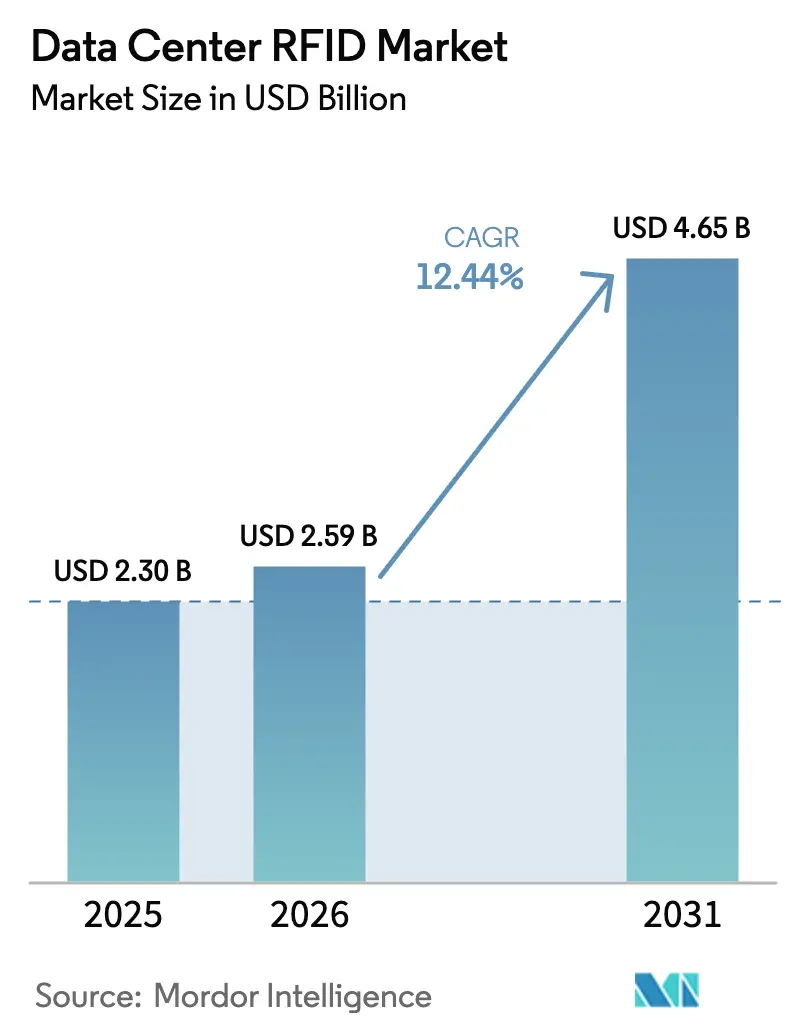

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 12.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Center RFID Market Analysis by Mordor Intelligence

Data center RFID market size in 2026 is estimated at USD 2.59 billion, growing from 2025 value of USD 2.3 billion with 2031 projections showing USD 4.65 billion, growing at 12.44% CAGR over 2026-2031. Capacity expansions at hyperscale facilities, which now double every four years to support racks drawing 40–140 kW, are the primary catalyst behind this growth trajectory DataCenterDynamics. Regulatory audits, sustainability mandates, and the need for real-time visibility over millions of distributed assets further reinforce adoption, pushing RFID from optional to essential in next-generation facilities. Integration with Data Center Infrastructure Management (DCIM) platforms is accelerating value creation by automating ticketing, thermal mapping, and predictive maintenance workflows, while falling UHF tag prices have removed the last meaningful cost barrier. Together, these forces position the data center RFID market as a core enabler of AI-driven, high-density infrastructure operations around the world.

Key Report Takeaways

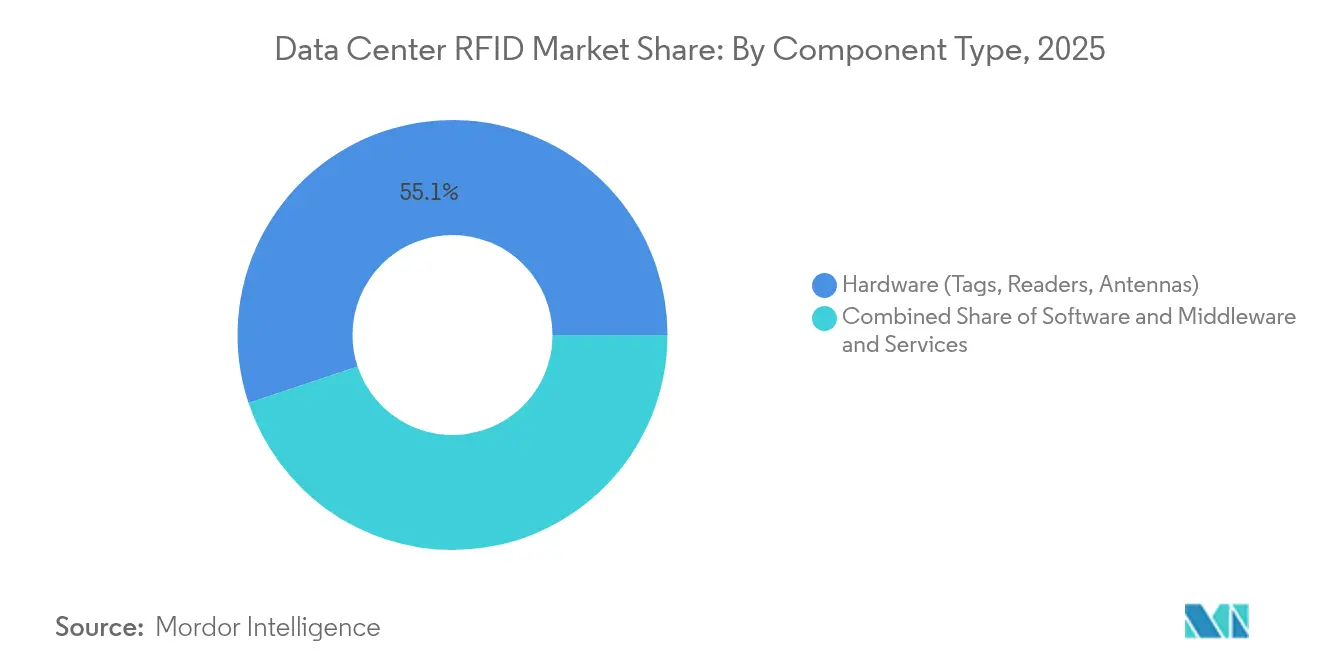

- By component, hardware captured 55.12% of data center RFID market share in 2025, while software and middleware is on track for the fastest CAGR at 13.39% through 2031.

- By tag type, passive tags led with 71.65% revenue share in 2025; active tags are projected to grow at 14.46% CAGR to 2031.

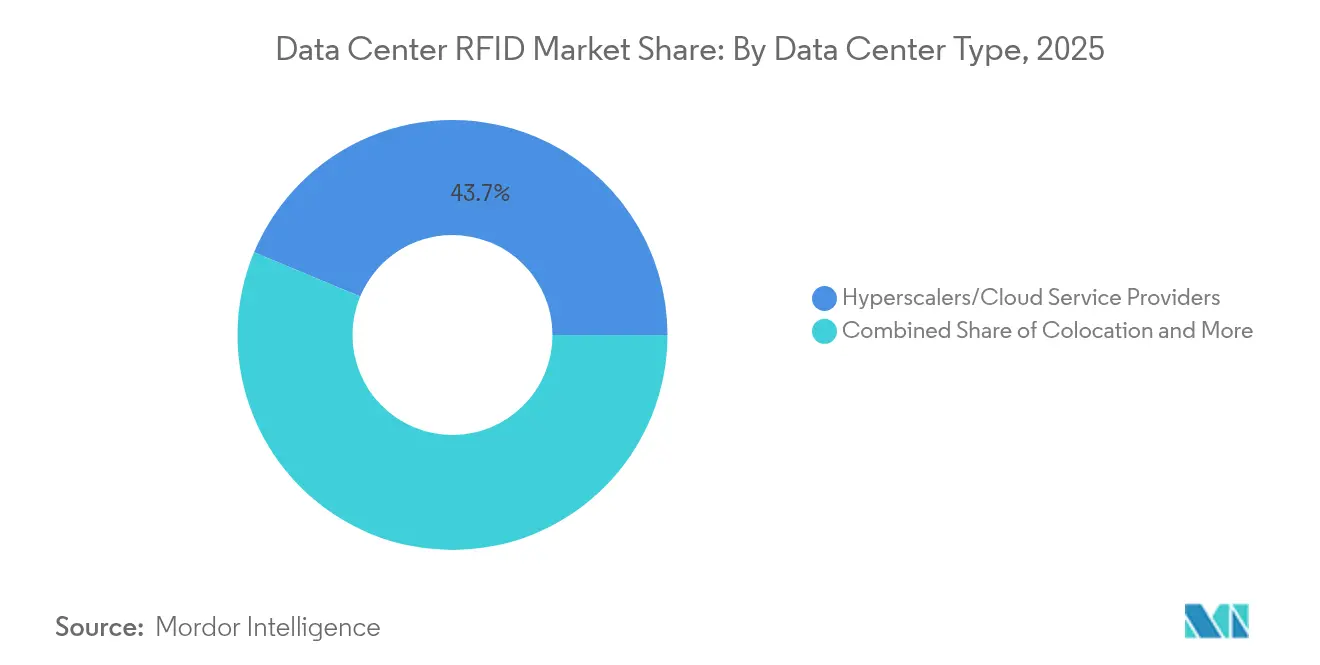

- By data-center type, hyperscalers held 43.72% share of the data center RFID market size in 2025 and are advancing at 14.55% CAGR through 2031.

- By application, asset tracking accounted for 45.86% of data center RFID market size in 2025, while environmental monitoring posts the quickest rise at 15.02% CAGR to 2031.

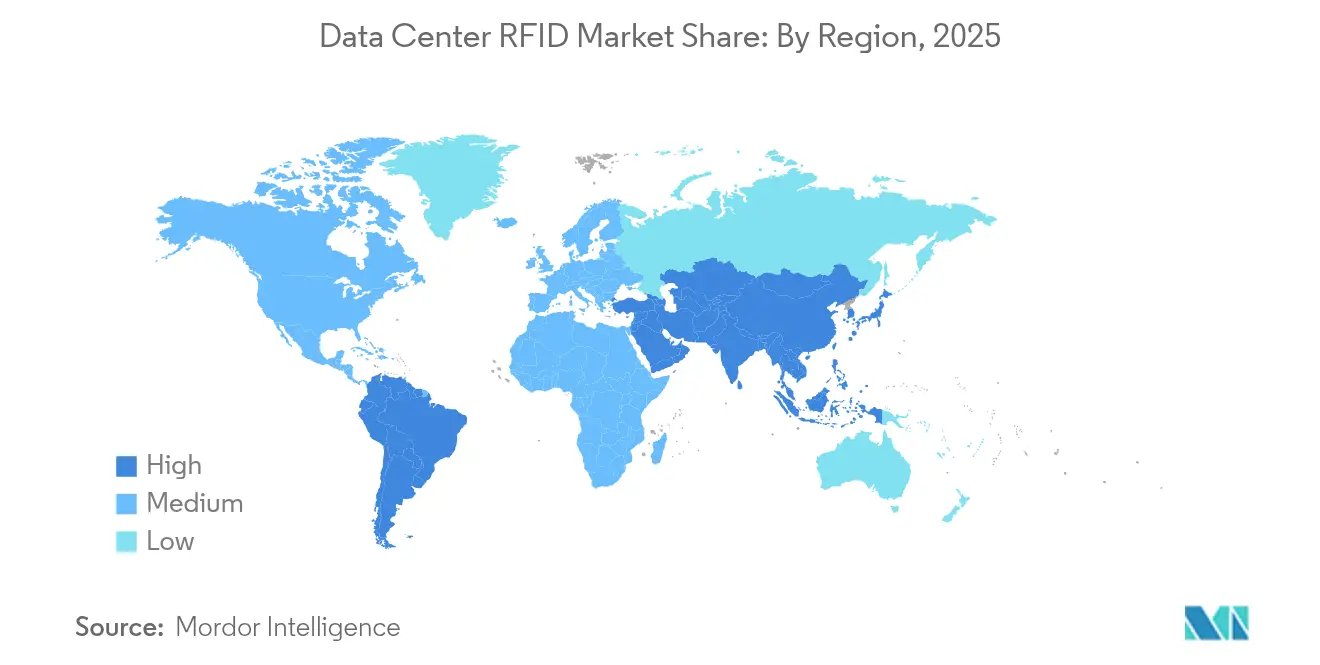

- By geography, North America retained 36.95% share of the data center RFID market in 2025; Asia-Pacific records the strongest 15.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Data Center RFID Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-time asset audit compliance pressure | 2.8% | Global, with early gains in North America, EU | Medium term (2-4 years) |

| Declining RFID tag cost curves | 2.1% | Global | Short term (≤ 2 years) |

| Integration with DCIM and ITSM stacks | 1.9% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Hyperscale and edge data-center build-outs | 3.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-enabled RFID thermal mapping | 1.4% | National, with early gains in hyperscale facilities | Long term (≥ 4 years) |

| Circular IT lifecycle buy-back tracking | 0.8% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Real-time Asset Audit Compliance Pressure Drives Market Acceleration

Persistent audit and governance demands oblige operators to maintain continuously updated inventories rather than occasional cycle counts, and RFID delivers near-perfect accuracy that barcode systems cannot match. The Social Security Administration’s RFID program achieved a 90% cut in labor hours while improving audit accuracy to 99%.[1]RFIDJournal — "The Social Security Administration’s RFID program achieved a 90% cut in labor hours while improving audit accuracy to 99%" Financial institutions reliant on Sarbanes-Oxley compliance have mirrored these outcomes, reporting inventory accuracy above 99% after RFID rollout. Continuous monitoring slashes remediation costs when assets go misplaced and enables real-time reporting to satisfy regulators. This dynamic amplifies spending among U.S. agencies and multinational banks, placing compliance as a top investment trigger for the data center RFID market.

Declining RFID Tag Cost Curves Enable Mass Deployment

Passive UHF tag pricing has slipped to USD 0.10–0.50 per unit as 300 mm wafer production and antenna material advances scale manufacturing efficiencies.[2]ScienceDirect — "Passive UHF tag pricing has slipped to USD 0.10–0.50 per unit as 300 mm wafer production and antenna material advances scale manufacturing efficiencies" Active tags have fallen to USD 15–50 each, opening budget headroom for dense sensor networks in large campuses. Capital injections such as Tageos’ USD 100 million U.S. plant and Avery Dennison’s Mexico line underscore industry confidence in rising volumes. As chip shortages ease by early 2025, predictable supply ensures operators can plan multi-year rollouts without price spikes. Lower unit economics now position data center RFID market adoption as a cost-saving initiative rather than a discretionary capital outlay.

Integration with DCIM and ITSM Stacks Enhances Operational Intelligence

RFID feeds directly into modern DCIM suites, turning static asset ledgers into real-time command centers. Sunbird’s platform processes over 10 billion daily datapoints to trigger automated alerts for thermal, humidity, and capacity deviations.[3]Sunbird Software — "Sunbird’s platform processes over 10 billion daily datapoints to trigger automated alerts for thermal, humidity, and capacity deviations" British Airways deploys dcTrack to allocate servers faster across six sites while ServiceNow connectors push location changes straight into enterprise workflows. This deep integration makes RFID indispensable for predictive maintenance and energy savings, accelerating the data center RFID market penetration in mature operations.

Hyperscale and Edge Data-Center Build-outs Fuel Demand

Roughly 120 new hyperscale halls open each year, and edge nodes proliferate even faster as AI inference workloads localize near users. AWS, Meta, and regional players like Sify are injecting billions into capacity, each site requiring thousands of tags, readers, and sensors. Distributed micro-centers with 3–10 kW cabinets depend on unattended, automated monitoring, pushing RFID right to the network edge. These construction pipelines lock in multi-year hardware and software demand, ensuring sustained double-digit growth for the data center RFID market.

Restraints Impact Analysis of Data Center RFID Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and skilled labor cost | -1.8% | Global | Short term (≤ 2 years) |

| RF interference inside dense racks | -1.2% | Global, particularly high-density facilities | Medium term (2-4 years) |

| Data-sovereignty limits on active-tag telemetry | -0.9% | EU, China, emerging markets | Long term (≥ 4 years) |

| Battery-waste concerns in active tags | -0.6% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Skilled Labor Cost Constraints

End-to-end deployments often start near USD 27,000 and require engineers versed in antenna physics and data-center protocols. The worldwide shortage of such talent extends project timelines and inflates consulting fees, especially for mid-tier operators. While long-run savings offset upfront expenses, smaller enterprises still label RFID as discretionary. Training programs and turnkey service bundles are emerging to ease adoption, yet the labor gap continues to shave points off the data center RFID market growth potential.

RF Interference Inside Dense Racks Creates Technical Challenges

Metal enclosures, power cables, and liquid-cooling lines generate multipath reflections that degrade read rates, as shown by Sandia National Laboratories where accuracy dipped to 93.9% in live server rooms. AI clusters topping 100 kW per rack intensify electromagnetic noise, requiring directional antennas and fine-tuned power levels. These engineering hurdles raise deployment complexity and sometimes necessitate hybrid tagging strategies, restraining immediate expansion in the densest compute halls of the data center RFID market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Data Center RFID Market Segment Analysis

By Component:

Hardware Dominance Driven by Infrastructure ScalingHardware retained 55.12% share of the data center RFID market in 2025 on the back of massive tag rollouts that accompany every new rack build. RF Code has shipped over 3 million tags into enterprise facilities, illustrating the scale of physical deployments. In revenue terms, readers and antennas represent the lion’s share of upfront spend, while middleware subscriptions drive recurring margins. Software and analytics, though smaller today, post the fastest 13.39% CAGR as operators demand AI-enabled insights. Services revenue follows hardware growth because integration, calibration, and ongoing optimization require specialized staff. Together, these spending patterns demonstrate why the data center RFID market size for hardware remains dominant even as value creation shifts toward data and automation layers.

Demand elasticity favors hardware even further because tag unit prices are falling, permitting operators to tag every blade, cable, and peripheral. As enterprises mature, they migrate from handheld readers to continuous fixed-reader grids, expanding antenna footprints in both white space and loading docks. This evolution guarantees multi-year hardware refresh cycles, keeping physical components at the center of procurement strategies. Meanwhile, recurring licenses for DCIM connectors, API feeds, and cybersecurity modules elevate total cost of ownership but also deepen vendor-client lock-in, supporting a balanced ecosystem across the data center RFID industry.

By Tag Type:

Passive Tags Lead Despite Active Growth MomentumPassive tags claimed 71.65% share in 2025 owing to minimal cost and battery-free longevity that stretches asset lifespans. In dense rack aisles where read distances span only centimeters, passive solutions meet audit requirements at the lowest possible budget. The data center RFID market size for passive tagging therefore remains unparalleled. Active tags, however, expand faster at 14.46% CAGR because real-time environmental sensing and 100 meter read ranges support thermal mapping and perimeter security. Modern active platforms integrate temperature, humidity, and even vibration sensors on a single tag, justifying higher unit prices in AI facilities that demand granular data.

Hybrid semi-passive designs have started bridging the gap by pairing passive read modes with battery-assisted sensor functions, enabling five-year lifecycles at mid-tier cost. As circular-economy regulations mandate cradle-to-grave tracking, demand for richer telemetry will likely narrow the lead passive tags hold today. Still, volume economics dictate that passive labels will dominate unit sales for the foreseeable future, underscoring their foundational role in the data center RFID market.

By Data-Center Type:

Hyperscalers Drive Market LeadershipHyperscale and cloud operators represented 43.72% of data center RFID market share in 2025 as single campuses often house over 250,000 tagged assets. Their standardized build templates streamline RFID design, and central purchasing delivers volume discounts that smaller entities cannot match. Double-digit facility growth planned by AWS, Google, and Microsoft ensures this segment also records the steepest 14.55% CAGR toward 2031. Colocation providers follow, requiring multi-tenant segregation that amplifies the need for precise asset location verification. Edge micro-data centers, though smaller individually, represent high-growth greenfield deployments, especially in telecom and retail sectors where thousands of sites roll out in parallel.

Economies of scale favor hyperscalers but also introduce challenges like RF zoning across millions of square feet. Consequently, these giants often implement layered RFID architectures mixing overhead antenna grids with rack-level readers. The resulting best practices trickle down to enterprise and edge clients, setting industry baselines and propelling the entire data center RFID market forward.

By Application:

Asset Tracking Dominates with Environmental Monitoring SurgeAsset tracking delivered 45.86% of data center RFID market size in 2025 because every operator must know what device sits in each rack at any moment. The shift from annual audits to real-time ledgers eliminates manual errors and satisfies auditors instantly. Environmental monitoring, however, captures the strongest 15.02% CAGR as AI clusters increase thermal risk. Sensors tied to RFID networks stream temperature and humidity readings at rack granularity, supporting dynamic cooling and energy savings that can lower PUE. Enhanced workflows such as automatic incident tickets or decommission flags now ride on asset location changes, illustrating the expanding scope of RFID beyond inventory into operational control.

Security integrations add further layers by matching employee badges with asset moves, thwarting insider threats. Workflow automation is emerging as the next wave, where AI engines predict spare-part demand or schedule maintenance windows based on RFID signals. These evolving use-cases enlarge the addressable footprint, ensuring application diversification continues to lift the data center RFID market.

Geography Analysis

North America Data Center RFID Market

North America held 36.95% of the data center RFID market in 2025, benefiting from mature hyperscale footprints, stringent audit laws, and aggressive AI adoption that demands accurate asset provenance. AWS’s USD 10 billion Mississippi plan and multi-site federal contracts ensure sustained tag volumes. Edge deployments across retail and telecom corridors further expand opportunities, especially as 5G coverage accelerates latency-sensitive compute needs. Regulatory convergence under frameworks like NIST SP-800 strengthens compliance drivers, reinforcing RFID as the de-facto standard for asset validation.

APAC Data Center RFID Market

Asia-Pacific is scaling even faster at 15.21% CAGR thanks to large-scale builds in China, Japan, India, and Southeast Asia. Sify Technologies alone earmarked USD 5 billion for AI data centers that will require millions of tags at inception. Japan’s construction cost surge underscores restricted land and power, pushing operators toward dense racks that magnify thermal management needs and accelerate sensor uptake. Local regulations tilt toward data sovereignty, prompting interest in passive or semi-passive tags that store data locally while limiting active telemetry.

EMEA and South America Data Center RFID Market

Europe combines significant installed base with complex data privacy statutes. Energy-efficiency directives mandate granular monitoring, making RFID vital for carbon accounting. Yet cross-border data flows remain constrained, shaping architectures that anonymize or locally process tag telemetry. Middle East and Africa show rising footprints in Gulf countries where renewable-powered campuses emerge, and South America gains traction through cloud-region rollouts in Brazil and Chile. Collectively, these diversification patterns assure the global data center RFID market remains on a structurally sound upward path.

Competitive Landscape

The market is moderately concentrated: the top five vendors account for roughly 65% of global revenue, granting mid-level bargaining power to buyers while leaving room for new entrants. RF Code anchors the active-tag niche via a 3 million-unit installed base linked to its CenterScape software, supplying hyperscalers like Vodafone that demand sub-meter accuracy. Zebra Technologies complements passive tagging with cloud analytics; its Asset Intelligence and Tracking unit recorded USD 462 million revenue in Q1 2025, up 18.4% year over year. Avery Dennison’s vertical factories in Mexico and U.S. guarantee supply resilience, an edge during recent semiconductor shortages.

Strategic alliances expand product scopes. Zebra and Merck’s M-Trust platform marries handheld readers with anti-counterfeiting features to secure pharmaceutical supply chains, a capability that has adjacent relevance in data-center spares management. Identiv and Novanta co-develop reader-inlay bundles for healthcare OEMs, illustrating a broader pivot toward turnkey offerings. Meanwhile, newcomers such as Acceliot leverage cloud-native architectures, boasting STARflex readers that operate in dense rack formations without performance drop-off. Their focus on AI-enabled analytics threatens incumbent software margins, spurring established firms to double down on predictive algorithms.

Capital markets fuel expansion. Vantage Data Centers secured USD 9.2 billion in equity to accelerate its build pipeline, automatically enlarging RFID hardware orders for each new hall . OEMs in reader, antenna, and middleware niches court these operators early to embed proprietary protocols before construction. As battery-free sensor innovations mature, the competitive field is expected to tilt toward vendors offering holistic energy-harvesting solutions. Continuous price erosion on tags ensures differentiation comes from software ecosystems, analytics, and integration depth, shaping future competitive moats in the data center RFID market.

Data Center RFID Industry Leaders

-

IBM Corporation

-

ZEBRA Technologies

-

Hewlett Packard Enterprise

-

GAO RFID

-

RF Code

- *Disclaimer: Major Players sorted in no particular order

Data Center RFID Market Companies Covered in this Report

- IBM Corporation

- Zebra Technologies Corp.

- Hewlett Packard Enterprise

- GAO RFID Inc.

- RF Code Inc.

- Alien Technology LLC

- Avery Dennison Corp.

- Omni-ID Ltd. (HID Global)

- Impinj Inc.

- NXP Semiconductors N.V.

- Honeywell International Inc.

- HID Global Corp.

- Vizinex RFID LLC

- InLogic Inc.

- Quanray Electronics Co. Ltd.

- SmartX Hub Inc.

- Invengo Information Tech. Co. Ltd.

- SATO Holdings Corp.

- Cisco Systems Inc.

- Johnson Controls (Cloudvue RFID)

- Tyco Integrated Security

Recent Industry Developments in Data Center RFID Market

- March 2025: Zebra Technologies and Merck KGaA introduced the M-Trust platform, integrating Zebra’s TC58 scanner with Merck’s authentication patents to enhance product verification

- February 2025: Identiv and Novanta partnered to provide all-in-one RFID reader-inlay solutions for medical device OEMs

- January 2025: Vantage Data Centers closed a USD 9.2 billion equity round led by DigitalBridge and Silver Lake to accelerate global build-outs

- January 2025: Honeywell and Verizon launched a bundled hardware-plus-5G package designed to streamline logistics and could spill into data-center workflows

- January 2025: Sify Technologies unveiled a USD 5 billion plan for AI data centers across India, expanding regional demand for RFID asset tracking

- December 2024: Avery Dennison displayed RFID innovations at NRF 2025, highlighting connected-product pilots with JD Sports

Data Center RFID Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the data-center RFID market as all hardware, software, and related services that use radio-frequency identification to locate, monitor, and secure any IT or facilities asset housed within a data-center's physical perimeter, regardless of ownership or tier classification. Coverage spans tags, readers, antennas, middleware, and integration services deployed across enterprise, colocation, edge, and hyperscale sites worldwide.

Scope Exclusion: Tracking solutions applied outside the data-center fence line (for example, warehouse or inbound logistics RFID) are excluded.

Segments Covered in This Report

-

By Component

- Hardware (Tags, Readers, Antennas)

- Software and Middleware

- Services (Integration, Support)

-

By Tag Type

- Passive

- Active

-

By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

-

By Application

- Asset Tracking and Inventory

- Environmental and Thermal Monitoring

- Security and Access Control

- Workflow Automation

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Chile

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Singapore

- Australia

- Malaysia

- Rest of Asia-Pacific

-

Middle East

- United Arab Emirate

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Primary Research

Telephone and online interviews with data-center operations managers, RFID integrators, tag OEM product leads, and regional auditors across North America, Europe, Asia-Pacific, and the Gulf validated adoption thresholds, average tags per rack, service pricing, and payback expectations that were unclear in secondary material.

Desk Research

Our analysts collated capacity and asset-base fundamentals from tier-one public sources such as Uptime Institute's annual data-center census, AFCOM State of the Data Center reports, U.S. Energy Information Administration power-use files, European Data Centre Association capacity trackers, and Singapore's IMDA colocation registry. Trade association white papers, company 10-Ks, and patent counts accessed via Questel and Dow Jones Factiva rounded out adoption and pricing cues.

Shipment-level hardware trends were then sampled using Volza customs data, while research articles from IEEE Xplore and ASHRAE clarified tag performance inside high-density racks. This illustrative list is not exhaustive; numerous additional open and subscription sources informed data checks and context.

Market-Sizing & Forecasting

A top-down rebuild started with installed rack counts by region, converted to potential tag pools via primary-confirmed penetration rates and adjusted for replacement cycles. Select bottom-up roll-ups sampled ASP multiplied by yearly shipments from supplier disclosures were overlaid to reconcile totals. Key model drivers include global data-center white-space growth, average tags per rack, tag price deflation, share of racks requiring environmental sensors, regulatory audit frequency, and hyperscale build-out pipelines. Multivariate regression, benchmarked against three years of historical values, generated the 2025-2030 forecast. Scenario analysis stress-tested energy-efficiency mandates and AI server density shifts.

Data Validation & Update Cycle

Outputs pass anomaly screens, peer review, and a senior analyst sign-off. Models refresh every twelve months or sooner when mergers, tariff shifts, or silicon shortages move inputs materially, so clients always receive the latest calibrated view.

How Mordor Intelligence's Data Center RFID Market Size Compares to Other Published Estimates

Published figures often diverge because firms favor different asset boundaries, tag pricing curves, and refresh cadences.

Our disciplined scope alignment, dual-sided modeling, and annual updates limit such variance. Key gap drivers elsewhere include hardware-only counting, aggressive CAGR stacking from adjacent IoT markets, or unvetted ASP assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.30 Billion (2025) | Mordor Intelligence | - |

| USD 1.49 Billion (2024) | Global Consultancy A | Excludes services, applies mid-sized data-center ceiling |

| USD 2.27 Billion (2023) | Industry Analyst B | Uses legacy tag prices, omits edge facilities, triennial refresh |

These contrasts show that Mordor's balanced, variable-traced approach yields a dependable baseline clients can replicate and defend when budget, capacity, or compliance decisions are on the line.

Key Questions Answered in the Report

What is the current size of the data center RFID market?

The data center RFID market is valued at USD 2.59 billion in 2026 and is projected to reach USD 4.65 billion by 2031.

Which component holds the largest share within the data center RFID market?

Hardware items such as tags, readers, and antennas lead with 55.12% revenue share because every deployment begins with physical tagging.

Why are hyperscale operators the largest adopters of RFID in data centers?

Hyperscale facilities manage millions of distributed assets, so they rely on RFID to maintain real-time visibility and comply with stringent audit requirements.

How fast is the Asia-Pacific region growing in the data center RFID market?

Asia-Pacific is currently expanding at a 15.21% CAGR, driven by large-scale investments in China, Japan, and India.

What technical hurdle most commonly limits RFID performance in dense server racks?

Metallic enclosures and high electromagnetic interference create RF shadows that reduce read accuracy, often requiring specialized antenna placement.

How does integrating RFID with DCIM platforms benefit data-center operators?

DCIM integration automates ticketing, thermal mapping, and predictive maintenance, allowing operators to cut labor costs and improve uptime.

Page last updated on: