Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

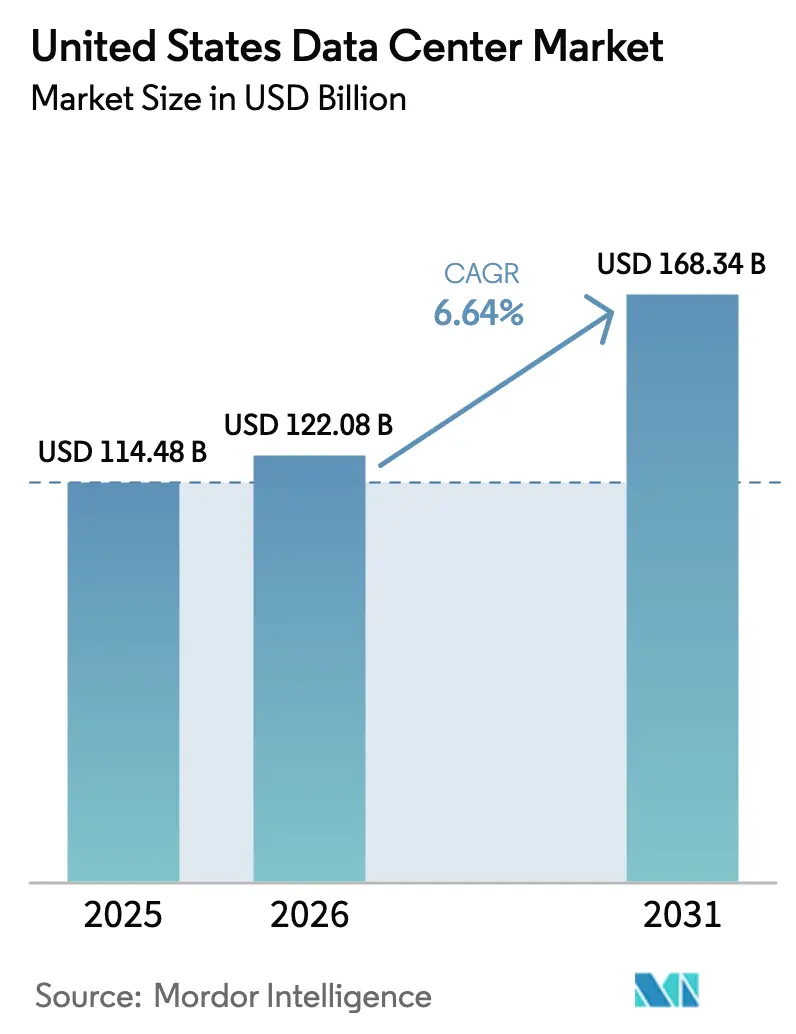

| Base Year Market Size (2025) | USD 114.48 Billion |

| Market Size (2026) | USD 122.08 Billion |

| Market Size (2031) | USD 168.34 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

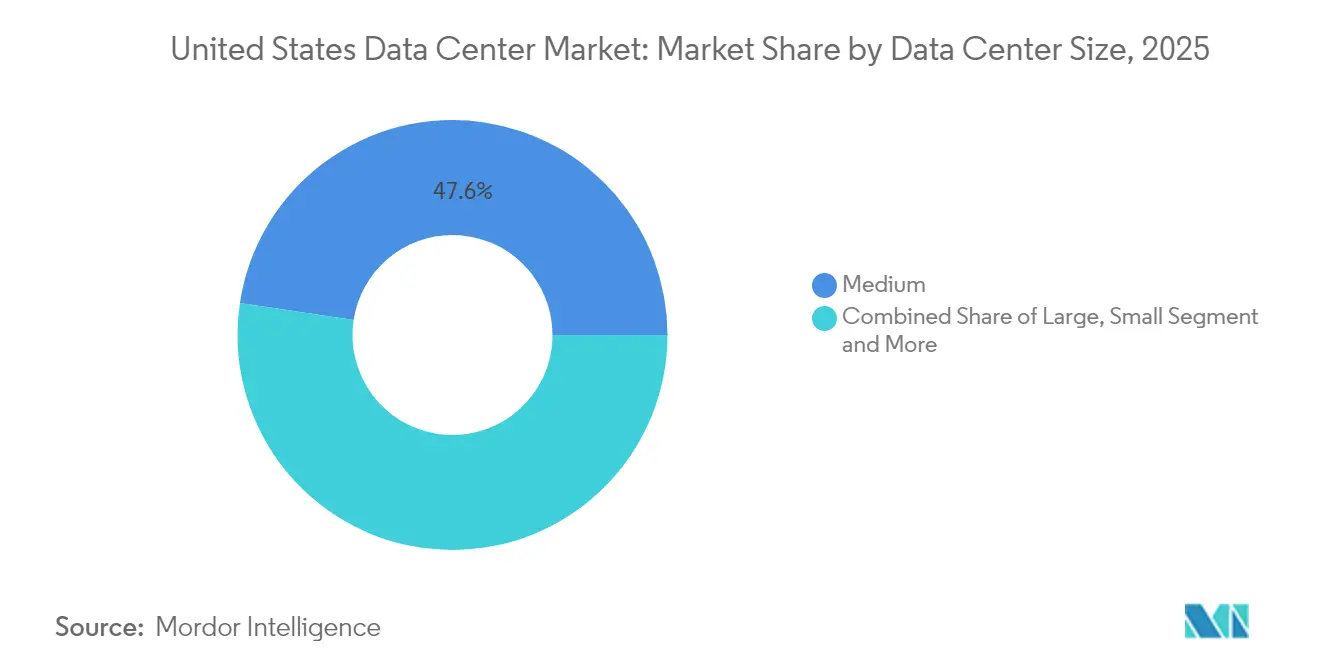

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Data Center Market Analysis by Mordor Intelligence

United States Data Center Market size in 2026 is estimated at USD 122.08 billion, growing from 2025 value of USD 114.48 billion with 2031 projections showing USD 168.34 billion, growing at 6.64% CAGR over 2026-2031. In terms of installed base, the market is expected to grow from 57.08 thousand megawatt in 2025 to 109.56 thousand megawatt by 2030, at a CAGR of 13.93% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. This expansion reflects unprecedented transformation driven by hyperscale operator demand and artificial intelligence infrastructure requirements, with record-breaking investment commitments exceeding USD 200 billion from major cloud providers. The market exhibits a stark regional concentration, with Atlanta holding the largest hotspot share at 21.68% in 2024, followed by Austin's emergence as the fastest-growing region, with a 5.21% CAGR through 2030. Power availability has emerged as the primary expansion constraint, with utilities reporting 5-7 year lead times for new capacity additions and transmission upgrades, creating development bottlenecks in core markets. Grid congestion and transmission limitations are reshaping site selection strategies, with secondary markets gaining traction as hyperscalers seek power-abundant locations beyond traditional hubs.

Key Report Takeaways

- By data center size, medium facilities led with 47.62% revenue share in 2025; large facilities are forecast to expand at a 6.78% CAGR to 2031.

- By tier standard, Tier 3 facilities held 68.12% of the United States data center market share in 2025, while Tier 4 recorded the highest projected CAGR at 6.83% through 2031.

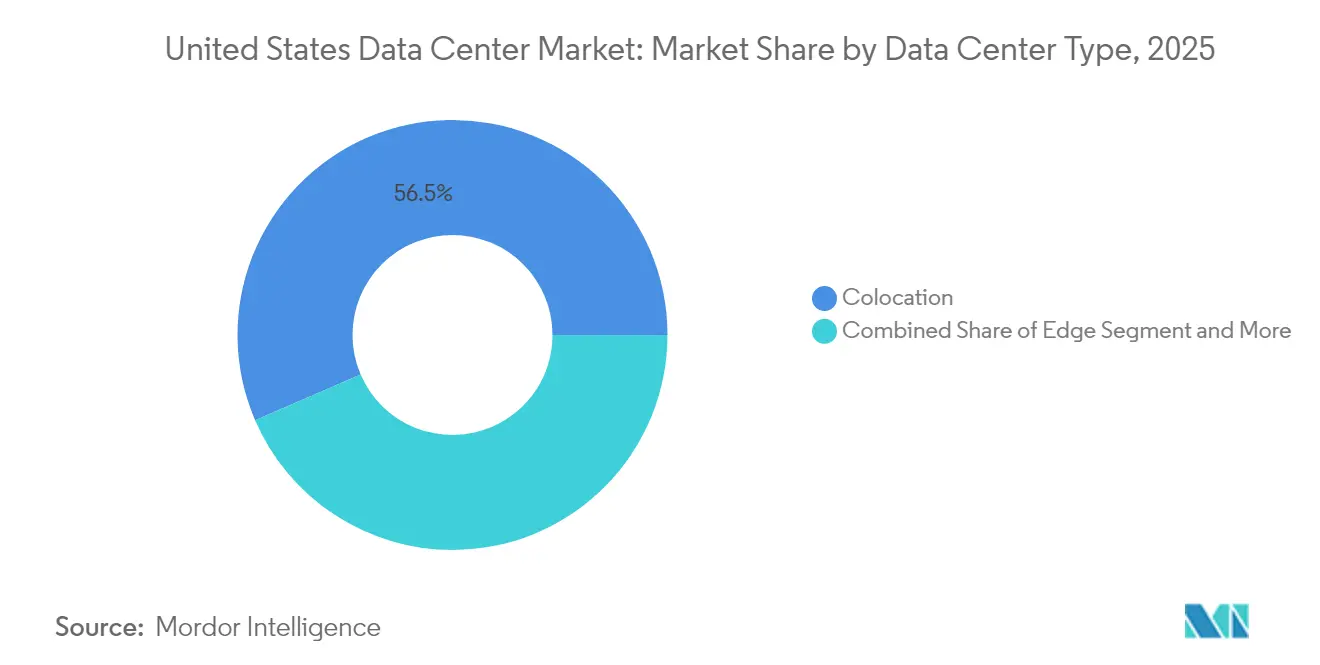

- By data center type, colocation accounted for a 56.48% share of the United States data center market size in 2025, and hyperscale self-built facilities are advancing at a 6.71% CAGR through 2031.

- By end user industry, the IT and telecom sectors collectively maintained 38.22% market share in 2025, with BFSI emerging as the fastest-growing segment at 6.92% CAGR driven by digital transformation and regulatory compliance requirements.

- By hotspot, Atlanta commanded 21.41% of the United States data center market share in 2025, while Austin is projected to grow at the highest CAGR of 6.86% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Data Center Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing hyperscale investments by cloud service providers | +1.2% | Global, concentrated in Northern Virginia, Dallas, Atlanta | Medium term (2-4 years) |

| Rising demand for AI and ML ready GPU clusters | +1.8% | Primary markets with robust power infrastructure, expanding to secondary metros | Short term (≤ 2 years) |

| Corporate sustainability commitments driving green colocation uptake | +0.7% | National, with early gains in renewable rich regions | Long term (≥ 4 years) |

| Edge deployments to support 5G and IoT latency requirements | +0.9% | Metropolitan areas and secondary cities, rural expansion following | Medium term (2-4 years) |

| Tax incentives in secondary and tertiary U.S. metros | +0.6% | Ohio, Indiana, Virginia, Texas, emerging in Wisconsin and Pennsylvania | Short term (≤ 2 years) |

| Under reported: Growth of sovereign cloud requirements for public agencies | +0.4% | National, with concentration near federal facilities and state capitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Hyperscale Investments by Cloud Service Providers

Hyperscale operators have committed unprecedented capital to United States infrastructure expansion, with Meta allocating USD 65 billion, Microsoft USD 80 billion, and Amazon USD 30 billion for 2025 data center investments.[1] Reuters, "Meta plans to spend up to USD65 billion on capex in 2025," reuters.com OpenAI's Stargate initiative represents the largest single commitment at USD 500 billion over four years, targeting AI optimized facilities across Texas, Louisiana, and Indiana. These investments are driving fundamental shifts in facility design, with new builds targeting 50-100 MW power capacities compared to traditional 10-20 MW deployments. The scale of commitment reflects hyperscalers' recognition that AI workloads require dedicated infrastructure rather than shared colocation environments, fundamentally altering demand patterns and site selection criteria.

Rising Demand for AI and ML Ready GPU Clusters

Artificial intelligence infrastructure requirements are reshaping data center specifications, with GPU clusters demanding 80-130 kW per rack compared to traditional 6-8 kW densities. NVIDIA's H100 systems require approximately 41 kW per rack, while next generation Blackwell GB200 configurations reach 130 kW per rack, necessitating liquid cooling architectures and upgraded power distribution systems. CoreWeave's USD 9 billion acquisition of GPU optimized facilities demonstrates the premium valuations for AI ready infrastructure. The transition from air cooled to liquid cooled environments requires fundamental architectural changes, with direct to chip cooling becoming standard for high density deployments and immersion cooling gaining adoption for extreme power densities exceeding 100 kW per rack.

Corporate Sustainability Commitments Driving Green Colocation Uptake

Enterprise sustainability mandates are accelerating renewable energy procurement, with data center operators securing over 120 GW of renewable capacity through corporate power purchase agreements.[2]Data Center Frontier, "The Eight Themes That Will Shape the Data Center Industry in 2024," Google's partnership with Fervo Energy for enhanced geothermal systems and Microsoft's Three Mile Island nuclear agreement exemplify innovative approaches to carbon free baseload power. Scope 2 carbon matching requirements are complicating procurement strategies, as enterprises demand hourly renewable energy matching rather than annual volume offsets. This shift is driving investment in hybrid renewable portfolios combining wind, solar, and storage to achieve 80% hourly matching at competitive costs, with near 100% matching requiring premium pricing structures that impact colocation rate negotiations.

Edge Deployments to Support 5G and IoT Latency Requirements

Edge computing infrastructure is expanding rapidly to support ultra low latency applications, with Verizon deploying edge nodes in over 30 metropolitan areas and AWS establishing Wavelength zones in major cities.[3]FS, "Forecasts for 2024 Fiber System: Two Key Trends in Broadband," fs.com The Federal BEAD program's USD 42.45 billion investment in broadband infrastructure is catalyzing edge facility development in underserved regions, creating opportunities for smaller scale data centers supporting rural connectivity. Edge deployments typically range from 1-10 MW capacity, focusing on compute intensive applications requiring sub 10 millisecond latency. The convergence of 5G network densification and autonomous vehicle deployment is driving edge infrastructure demand in metropolitan areas, with telecommunications providers increasingly partnering with data center operators to co locate edge computing resources at cell tower sites and central offices.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid congestion and sub 1 GW power availability in hot markets | -1.8% | Northern Virginia, Silicon Valley, Chicago, Dallas core counties | Short term (≤ 2 years) |

| Extended lead times for high capacity transformers and switchgear | -1.2% | National, with acute impact in high growth regions | Medium term (2-4 years) |

| Scope 2 carbon matching mandates complicating procurement | -0.6% | National, with early implementation in California and Northeast | Medium term (2-4 years) |

| Under reported: Scarcity of qualified controls engineers for hyperscale campuses | -0.4% | Primary markets with concentrated hyperscale development | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Sub 1 GW Power Availability in Hot Markets

Power transmission constraints have emerged as the primary growth limitation across major United States markets, with Northern Virginia requiring 5-7 year lead times for new utility capacity from Dominion Energy. The North American Electric Reliability Corporation reports that existing transmission infrastructure cannot support projected data center load growth without significant upgrades, creating bottlenecks in core markets where demand exceeds 1 GW annually. Silicon Valley faces particularly acute constraints, with some acquired sites lacking utility power access for over 10 years, forcing operators to consider fuel cells and on site generation alternatives. Grid congestion is driving geographic dispersion to secondary markets with available transmission capacity, fundamentally altering traditional site selection preferences and creating opportunities in previously overlooked regions with robust electrical infrastructure.

Extended Lead Times for High Capacity Transformers and Switchgear

Critical electrical equipment shortages are extending project timelines across the United States, with high voltage transformers requiring 18-24 months for delivery and switchgear lead times reaching 46-48 weeks. Generator and chiller procurement has extended to 30+ weeks, while copper feeders and busway systems face similar constraints due to global supply chain disruptions and surging demand from electrification initiatives. Equipment costs have increased 40-50% since Q3 2021, with some specialized components experiencing even steeper price escalation. These constraints are forcing developers to secure equipment commitments earlier in the development process and consider alternative sourcing strategies, including strategic partnerships with equipment manufacturers to guarantee supply continuity for large scale deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Medium Facilities Drive Market Foundation

Medium-sized data centers commanded 47.62% market share in 2025, reflecting enterprise preferences for balanced cost-performance infrastructure that supports diverse workload requirements without hyperscale complexity. Large facilities represent the fastest growing segment at 6.78% CAGR (2026-2031), driven by AI infrastructure demands requiring consolidated high density deployments. The United States data center market size for large facilities is projected to expand significantly as organizations consolidate computing resources to optimize operational efficiency and support increasingly complex workloads. Mega scale facilities continue expanding to accommodate hyperscaler campus strategies, while massive deployments serve specialized applications including cryptocurrency mining and high performance computing clusters. Small data centers maintain relevance for edge computing and local processing requirements, particularly in secondary markets where latency sensitive applications drive distributed architecture adoption.

The shift toward larger facility footprints reflects fundamental changes in workload characteristics, with AI training requiring clustered GPU resources that benefit from proximity and high bandwidth interconnection. Historical CAGR comparison reveals accelerating demand for large facilities, growing from 3.2% (2019-2024) to projected 6.78% (2026-2031), indicating sustained momentum in hyperscale infrastructure requirements. The United States data center market is experiencing this transformation as organizations recognize the efficiency advantages of consolidated operations. Regulatory compliance frameworks including SOC 2 Type II and FedRAMP requirements increasingly favor larger facilities with comprehensive security and operational controls, supporting the trend toward consolidated rather than distributed infrastructure deployment strategies.

By Tier Standard: Tier 3 Dominance with Tier 4 Acceleration

Tier 3 facilities maintained 68.12% market share in 2025, representing the optimal balance between uptime reliability and capital efficiency for enterprise workloads requiring 99.982% availability. Tier 4 infrastructure emerges as the fastest growing segment at 6.83% CAGR (2026-2031), driven by financial services and healthcare organizations demanding 99.995% uptime guarantees and fault tolerant architectures. The United States data center market share for Tier 4 facilities is increasing as mission critical applications require higher reliability standards and regulatory compliance mandates strengthen. Tier 1 and 2 facilities collectively serve cost sensitive applications and development environments where brief outages are acceptable, maintaining steady demand in secondary markets and edge deployments.

The acceleration in Tier 4 adoption reflects increasing enterprise recognition that downtime costs exceed infrastructure premiums for mission critical applications. Financial services regulations including Basel III and healthcare compliance requirements under HIPAA are driving demand for concurrent maintainable infrastructure with no single points of failure. The United States data center industry is responding with expanded Tier 4 capacity development across primary markets. Tier 4 facilities command premium pricing of 25-40% above Tier 3 equivalents, but deliver 99.6% fewer outage minutes annually, creating compelling value propositions for applications where availability directly impacts revenue generation and regulatory compliance.

By Data Center Type: Colocation Leadership Amid Hyperscale Growth

Colocation facilities dominated with 56.48% market share in 2025, serving enterprises seeking operational expertise and shared infrastructure economics without capital investment requirements. The segment divides between retail colocation serving smaller tenants with flexible space requirements and wholesale colocation providing dedicated suites for larger deployments. The United States data center market size for colocation facilities reached record levels as organizations increasingly outsource infrastructure management to specialized providers. Hyperscale self built facilities represent the fastest growing segment at 6.71% CAGR (2026-2031), as cloud providers prioritize control over power dense AI infrastructure and custom cooling architectures. Enterprise and edge facilities maintain steady growth supporting distributed computing requirements and local processing needs.

Utilized colocation space commands premium pricing due to supply constraints, with retail colocation rates increasing 20% year over year across primary markets. Non utilized inventory remains limited as pre leasing activity reaches record levels, with 83% of capacity under construction already committed to tenants. The United States data center market is experiencing unprecedented demand pressure as organizations accelerate digital transformation initiatives. The shift toward hyperscale self built reflects recognition that AI workloads require specialized infrastructure including liquid cooling, high density power distribution, and custom network architectures that standard colocation environments cannot efficiently accommodate.

By End User Industry: IT and Telecom Leadership with BFSI Acceleration

IT and telecom sectors collectively maintained 38.22% market share in 2025, reflecting core digital infrastructure requirements and cloud service provider expansion. Banking, Financial Services, and Insurance emerges as the fastest growing segment at 6.92% CAGR (2026-2031), driven by digital transformation initiatives, algorithmic trading infrastructure, and regulatory compliance requirements including stress testing and data residency mandates. The United States data center market size for BFSI applications is expanding rapidly as financial institutions prioritize technology infrastructure modernization. E commerce continues expanding to support omnichannel retail strategies and supply chain optimization, while government demand reflects modernization initiatives and cybersecurity infrastructure investments.

Manufacturing sector adoption accelerates as Industrial Internet of Things deployments require edge computing capabilities for real time process optimization and predictive maintenance applications. Media and entertainment demand grows with streaming service expansion and content delivery network requirements, while telecom infrastructure supports 5G network densification and edge computing deployment. The United States data center industry is responding with specialized solutions addressing sector specific requirements. The BFSI sector's growth acceleration reflects increasing recognition that competitive advantage depends on low latency trading systems, real time fraud detection, and customer experience optimization requiring dedicated high performance infrastructure rather than shared cloud environments.

By Hotspot: Atlanta Dominance with Austin Emergence

Atlanta commanded 21.41% market share in 2025, benefiting from robust fiber connectivity, competitive power costs, and strategic geographic positioning serving southeastern United States population centers. The market recorded 705.8 MW absorption in 2024, with AWS committing USD 11 billion for regional expansion and total inventory reaching 1,000.4 MW. Austin represents the fastest-growing hotspot at 6.86% CAGR (2026-2031), driven by technology sector concentration, renewable energy availability, and state tax incentives supporting digital infrastructure investment. Dallas maintains strong performance with projected market doubling by 2026, while Rest of United States encompasses emerging secondary markets gaining traction as primary regions face power constraints.

Austin's growth acceleration reflects Texas's favorable regulatory environment, with ERCOT's independent grid management enabling faster permitting and development timelines compared to interstate transmission coordination requirements. The region benefits from abundant renewable energy resources and semiconductor industry presence, creating synergies between chip manufacturing and data processing infrastructure. Secondary markets including Phoenix, Northern Indiana, and Boise are gaining hyperscaler attention due to available land, competitive power costs, and reduced natural disaster risk profiles, indicating geographic diversification trends that may reshape traditional hotspot concentration patterns over the forecast period.

Geography Analysis

The United States data center market demonstrates pronounced geographic concentration, with Atlanta leading national absorption at 705.8 MW in 2024 and commanding 21.41% market share in 2025 through strategic advantages including robust fiber infrastructure, competitive power costs averaging USD 0.065-0.07 per kWh, and positioning as the southeastern regional hub. AWS's USD 11 billion regional investment commitment underscores Atlanta's strategic importance, while total market inventory reached 1,000.4 MW with continued expansion planned across multiple campus developments. The United States data center market size in Atlanta continues growing as operators leverage the region's advantageous operating environment. The market benefits from Georgia Power's transmission infrastructure investments and favorable zoning policies that streamline development timelines compared to more restrictive jurisdictions.

Austin emerges as the fastest growing hotspot at 6.86% CAGR (2026-2031), leveraging Texas's independent ERCOT grid management system that enables accelerated permitting and development processes without interstate coordination requirements. The region's technology sector concentration, including major semiconductor facilities and corporate headquarters, creates natural demand synergies while abundant renewable energy resources support sustainability mandates. The United States data center market share in Austin is increasing rapidly as operators recognize these strategic advantages. Dallas Fort Worth maintains robust growth with market capacity projected to double by 2026, driven by ERCOT's reliable power supply and Oncor's distribution infrastructure that provides development advantages over constrained markets. Employment growth of 38% from 2018-2024 in the technology sector supports continued data center expansion, while strategic positioning enables efficient connectivity to both coasts.

Rest of United States encompasses emerging secondary markets gaining hyperscaler attention as primary regions face power transmission constraints and land scarcity. Northern Indiana attracted two major hyperscaler announcements in 2024, benefiting from available power capacity, competitive land costs, and strategic positioning within 300 mile radius of major Midwest metropolitan areas. Phoenix demonstrates supply constraints with less than 23 MW unleased inventory and 4.25% vacancy rates, while Boise, Idaho gains traction through favorable hydropower resources, abundant land availability, and low natural disaster risk profiles. The United States data center industry is increasingly exploring these emerging markets as geographic diversification becomes essential to growth strategies. These emerging markets represent geographic diversification strategies as hyperscalers seek power abundant locations beyond traditional coastal concentrations, supported by state and local tax incentive programs designed to attract digital infrastructure investment.

Competitive Landscape

The United States data center market exhibits moderate concentration with significant competitive intensity, as the top three global colocation providers account for approximately 30% of market share, led by Equinix at 11.1% and Digital Realty at 7.6%. Market dynamics reflect a bifurcated structure where established colocation operators compete for enterprise tenants while hyperscale cloud providers increasingly develop self-built facilities for proprietary workloads. The United States data center market is experiencing this dual-track development pattern as specialized infrastructure requirements drive divergent facility designs. Private equity participation has intensified, representing 80-90% of deal value from 2022-2024, with Blackstone's USD 16 billion AirTrunk acquisition exemplifying capital deployment strategies targeting high-growth infrastructure assets.

Strategic patterns emphasize vertical integration and power procurement capabilities, with operators pursuing utility partnerships, renewable energy development, and relationships with equipment manufacturers to secure supply chain continuity. Digital Realty's USD 7 billion joint venture with Blackstone and Equinix's USD 15 billion partnership with GIC and CPP demonstrate capital formation strategies enabling hyperscale expansion while maintaining operational control. The United States data center industry is adopting these innovative financing approaches to accelerate capacity development. Technology deployment focuses on liquid cooling architectures, advanced power distribution systems, and artificial intelligence optimized infrastructure, with companies leveraging proprietary cooling solutions and modular construction techniques to accelerate deployment timelines and reduce operational costs. White space opportunities exist in secondary markets with available power capacity, edge computing infrastructure, and specialized facilities supporting artificial intelligence workloads requiring custom cooling and network architectures that traditional colocation environments cannot efficiently accommodate.

United States Data Center Industry Leaders

-

Amazon Web Services, Inc

-

Google Inc

-

Microsoft Corporation

-

Digital Realty Trust, Inc

-

Equinix Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: OpenAI announced the Stargate initiative, a USD 500 billion artificial intelligence infrastructure project spanning four years with initial deployments planned across Texas, Louisiana, and Indiana, representing the largest single data center investment commitment in United States history and signaling unprecedented capital allocation toward AI optimized facilities.

- January 2025: Meta disclosed plans to invest up to USD 65 billion in capital expenditures for 2025, with the majority allocated to data center infrastructure supporting artificial intelligence research and development, marking a 25% increase from 2024 spending levels and reflecting accelerating AI infrastructure requirements.

- December 2024: Microsoft committed USD 80 billion to data center investments globally, with significant United States allocation, including the Three Mile Island nuclear power agreement to secure 835 MW of carbon-free baseload power for Pennsylvania operations, demonstrating innovative approaches to sustainable energy procurement.

- December 2024: Blackstone completed the acquisition of AirTrunk for approximately USD 16 billion, representing the largest single data center transaction in 2024 and highlighting continued private equity interest in high-growth infrastructure assets with global expansion potential.

United States Data Center Market Report Scope

By Data Center Size

| Large |

| Massive |

| Medium |

| Mega |

| Small |

By Tier Standard

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

By Data Center Type

| Hyperscale/Self-built | ||

| Enterprise/Edge | ||

| Colocation | Non-Utilized | |

| Utilized | Retail Colocation | |

| Wholesale Colocation | ||

By End User Industry

| BFSI |

| IT and ITES |

| E-Commerce |

| Government |

| Manufacturing |

| Media and Entertainment |

| Telecom |

| Other End Users |

By Hotspot

| Atlanta |

| Austin |

| Dallas |

| Rest of United States |

| By Data Center Size | Large | ||

| Massive | |||

| Medium | |||

| Mega | |||

| Small | |||

| By Tier Standard | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Type | Hyperscale/Self-built | ||

| Enterprise/Edge | |||

| Colocation | Non-Utilized | ||

| Utilized | Retail Colocation | ||

| Wholesale Colocation | |||

| By End User Industry | BFSI | ||

| IT and ITES | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

| By Hotspot | Atlanta | ||

| Austin | |||

| Dallas | |||

| Rest of United States | |||

Market Definition

- IT LOAD CAPACITY - The IT load capacity or installed capacity, refers to the amount of energy consumed by servers and network equipments placed in a rack installed. It is measured in megawatt (MW).

- ABSORPTION RATE - It denotes the extend to which the data center capacity has been leased out. For instance, a 100 MW DC has leased out 75 MW, then absorption rate would be 75%. It is also referred as utilization rate and leased-out capacity.

- RAISED FLOOR SPACE - It is an elevated space build over the floor. This gap between the original floor and the elevated floor is used to accommodate wiring, cooling, and other data center equipment. This arrangement assist in having proper wiring and cooling infrastructure. It is measured in square feet (ft^2).

- DATA CENTER SIZE - Data Center Size is segmented based on the raised floor space allocated to the data center facilities. Mega DC - # of Racks must be more than 9000 or RFS (raised floor space) must be more than 225001 Sq. ft; Massive DC - # of Racks must be in between 9000 and 3001 or RFS must be in between 225000 Sq. ft and 75001 Sq. ft; Large DC - # of Racks must be in between 3000 and 801 or RFS must be in between 75000 Sq. ft and 20001 Sq. ft; Medium DC # of Racks must be in between 800 and 201 or RFS must be in between 20000 Sq. ft and 5001 Sq. ft; Small DC - # of Racks must be less than 200 or RFS must be less than 5000 Sq. ft.

- TIER TYPE - According to Uptime Institute the data centers are classified into four tiers based on the proficiencies of redundant equipment of the data center infrastructure. In this segment the data center are segmented as Tier 1,Tier 2, Tier 3 and Tier 4.

- COLOCATION TYPE - The segment is segregated into 3 categories namely Retail, Wholesale and Hyperscale Colocation service. The categorization is done based on the amount of IT load leased out to potential customers. Retail colocation service has leased capacity less than 250 kW; Wholesale colocation services has leased capacity between 251 kW and 4 MW and Hyperscale colocation services has leased capacity more than 4 MW.

- END CONSUMERS - The Data Center Market operates on a B2B basis. BFSI, Government, Cloud Operators, Media and Entertainment, E-Commerce, Telecom and Manufacturing are the major end-consumers in the market studied. The scope only includes colocation service operators catering to the increasing digitalization of the end-user industries.

| Keyword | Definition |

|---|---|

| Rack Unit | Generally referred as U or RU, it is the unit of measurement for the server unit housed in the racks in the data center. 1U is equal to 1.75 inches. |

| Rack Density | It defines the amount of power consumed by the equipment and server housed in a rack. It is measured in kilowatt (kW). This factor plays a critical role in data center design and, cooling and power planning. |

| IT Load Capacity | The IT load capacity or installed capacity, refers to the amount of energy consumed by servers and network equipment placed in a rack installed. It is measured in megawatt (MW). |

| Absorption Rate | It denotes how much of the data center capacity has been leased out. For instance, if a 100 MW DC has leased out 75 MW, then the absorption rate would be 75%. It is also referred to as utilization rate and leased-out capacity. |

| Raised Floor Space | It is an elevated space built over the floor. This gap between the original floor and the elevated floor is used to accommodate wiring, cooling, and other data center equipment. This arrangement assists in having proper wiring and cooling infrastructure. It is measured in square feet/meter. |

| Computer Room Air Conditioner (CRAC) | It is a device used to monitor and maintain the temperature, air circulation, and humidity inside the server room in the data center. |

| Aisle | It is the open space between the rows of racks. This open space is critical for maintaining the optimal temperature (20-25 °C) in the server room. There are primarily two aisles inside the server room, a hot aisle and a cold aisle. |

| Cold Aisle | It is the aisle wherein the front of the rack faces the aisle. Here, chilled air is directed into the aisle so that it can enter the front of the racks and maintain the temperature. |

| Hot Aisle | It is the aisle where the back of the racks faces the aisle. Here, the heat dissipated from the equipment’s in the rack is directed to the outlet vent of the CRAC. |

| Critical Load | It includes the servers and other computer equipment whose uptime is critical for data center operation. |

| Power Usage Effectiveness (PUE) | It is a metric which defines the efficiency of a data center. It is calculated by: (𝑇𝑜𝑡𝑎𝑙 𝐷𝑎𝑡𝑎 𝐶𝑒𝑛𝑡𝑒𝑟 𝐸𝑛𝑒𝑟𝑔𝑦 𝐶𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛)/(𝑇𝑜𝑡𝑎𝑙 𝐼𝑇 𝐸𝑞𝑢𝑖𝑝𝑚𝑒𝑛𝑡 𝐸𝑛𝑒𝑟𝑔𝑦 𝐶𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛). Further, a data center with a PUE of 1.2-1.5 is considered highly efficient, whereas, a data center with a PUE >2 is considered highly inefficient. |

| Redundancy | It is defined as a system design wherein additional component (UPS, generators, CRAC) is added so that in case of power outage, equipment failure, the IT equipment should not be affected. |

| Uninterruptible Power Supply (UPS) | It is a device that is connected in series with the utility power supply, storing energy in batteries such that the supply from UPS is continuous to IT equipment even during utility power is snapped. The UPS primarily supports the IT equipment only. |

| Generators | Just like UPS, generators are placed in the data center to ensure an uninterrupted power supply, avoiding downtime. Data center facilities have diesel generators and commonly, 48-hour diesel is stored in the facility to prevent disruption. |

| N | It denotes the tools and equipment required for a data center to function at full load. Only "N" indicates that there is no backup to the equipment in the event of any failure. |

| N+1 | Referred to as 'Need plus one', it denotes the additional equipment setup available to avoid downtime in case of failure. A data center is considered N+1 when there is one additional unit for every 4 components. For instance, if a data center has 4 UPS systems, then for to achieve N+1, an additional UPS system would be required. |

| 2N | It refers to fully redundant design wherein two independent power distribution system is deployed. Therefore, in the event of a complete failure of one distribution system, the other system will still supply power to the data center. |

| In-Row Cooling | It is the cooling design system installed between racks in a row where it draws warm air from the hot aisle and supplies cool air to the cold aisle, thereby maintaining the temperature. |

| Tier 1 | Tier classification determines the preparedness of a data center facility to sustain data center operation. A data center is classified as Tier 1 data center when it has a non-redundant (N) power component (UPS, generators), cooling components, and power distribution system (from utility power grids). The Tier 1 data center has an uptime of 99.67% and an annual downtime of <28.8 hours. |

| Tier 2 | A data center is classified as Tier 2 data center when it has a redundant power and cooling components (N+1) and a single non-redundant distribution system. Redundant components include extra generators, UPS, chillers, heat rejection equipment, and fuel tanks. The Tier 2 data center has an uptime of 99.74% and an annual downtime of <22 hours. |

| Tier 3 | A data center having redundant power and cooling components and multiple power distribution systems is referred to as a Tier 3 data center. The facility is resistant to planned (facility maintenance) and unplanned (power outage, cooling failure) disruption. The Tier 3 data center has an uptime of 99.98% and an annual downtime of <1.6 hours. |

| Tier 4 | It is the most tolerant type of data center. A Tier 4 data center has multiple, independent redundant power and cooling components and multiple power distribution paths. All IT equipment are dual powered, making them fault tolerant in case of any disruption, thereby ensuring interrupted operation. The Tier 4 data center has an uptime of 99.74% and an annual downtime of <26.3 minutes. |

| Small Data Center | Data center that has floor space area of ≤ 5,000 Sq. ft or the number of racks that can be installed is ≤ 200 is classified as a small data center. |

| Medium Data Center | Data center which has floor space area between 5,001-20,000 Sq. ft, or the number of racks that can be installed is between 201-800, is classified as a medium data center. |

| Large Data Center | Data center which has floor space area between 20,001-75,000 Sq. ft, or the number of racks that can be installed is between 801-3,000, is classified as a large data center. |

| Massive Data Center | Data center which has floor space area between 75,001-225,000 Sq. ft, or the number of racks that can be installed is between 3001-9,000, is classified as a massive data center. |

| Mega Data Center | Data center that has a floor space area of ≥ 225,001 Sq. ft or the number of racks that can be installed is ≥ 9001 is classified as a mega data center. |

| Retail Colocation | It refers to those customers who have a capacity requirement of 250 kW or less. These services are majorly opted by small and medium enterprises (SMEs). |

| Wholesale Colocation | It refers to those customers who have a capacity requirement between 250 kW to 4 MW. These services are majorly opted by medium to large enterprises. |

| Hyperscale Colocation | It refers to those customers who have a capacity requirement greater than 4 MW. The hyperscale demand primarily originates from large-scale cloud players, IT companies, BFSI, and OTT players (like Netflix, Hulu, and HBO+). |

| Mobile Data Speed | It is the mobile internet speed a user experiences via their smartphones. This speed is primarily dependent on the carrier technology being used in the smartphone. The carrier technologies available in the market are 2G, 3G, 4G, and 5G, where 2G provides the slowest speed while 5G is the fastest. |

| Fiber Connectivity Network | It is a network of optical fiber cables deployed across the country, connecting rural and urban regions with high-speed internet connection. It is measured in kilometer (km). |

| Data Traffic per Smartphone | It is a measure of average data consumption by a smartphone user in a month. It is measured in gigabyte (GB). |

| Broadband Data Speed | It is the internet speed that is supplied over the fixed cable connection. Commonly, copper cable and optic fiber cable are used in both residential and commercial use. Here, optic cable fiber provides faster internet speed than copper cable. |

| Submarine Cable | A submarine cable is a fiber optic cable laid down at two or more landing points. Through this cable, communication and internet connectivity between countries across the globe is established. These cables can transmit 100-200 terabits per second (Tbps) from one point to another. |

| Carbon Footprint | It is the measure of carbon dioxide generated during the regular operation of a data center. Since, coal, and oil & gas are the primary source of power generation, consumption of this power contributes to carbon emissions. Data center operators are incorporating renewable energy sources to curb the carbon footprint emerging in their facilities. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms