Czech Republic Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

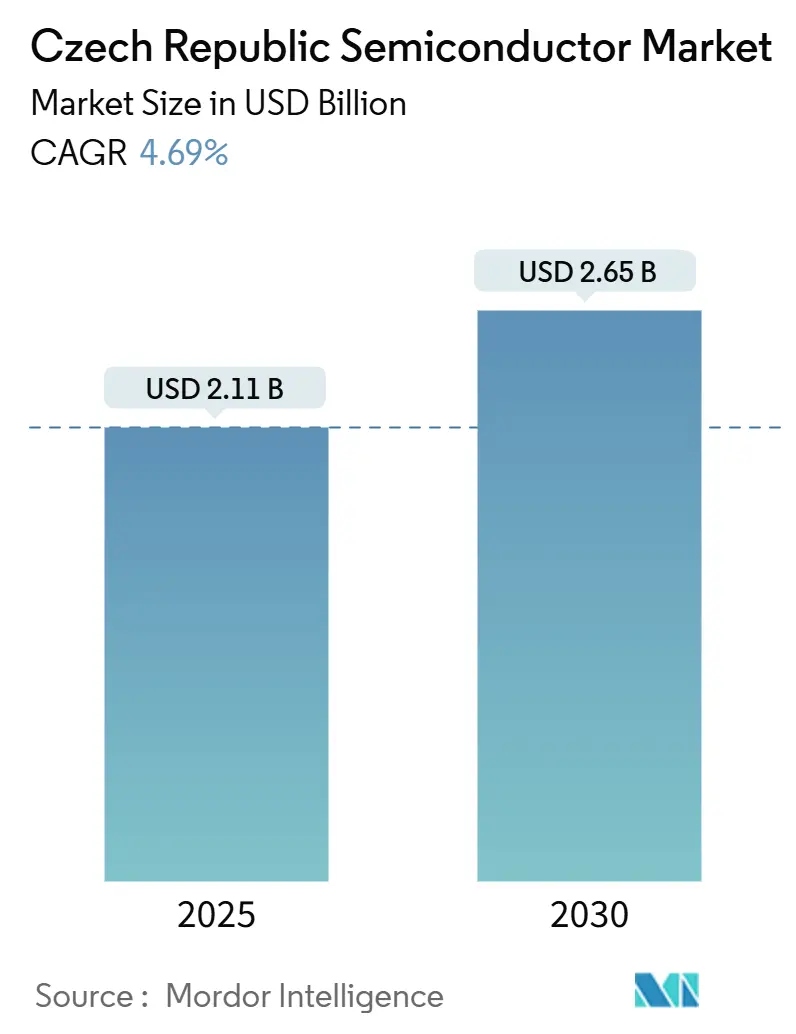

| Market Size (2025) | USD 2.11 Billion |

| Market Size (2030) | USD 2.65 Billion |

| Growth Rate (2025 - 2030) | 4.69% CAGR |

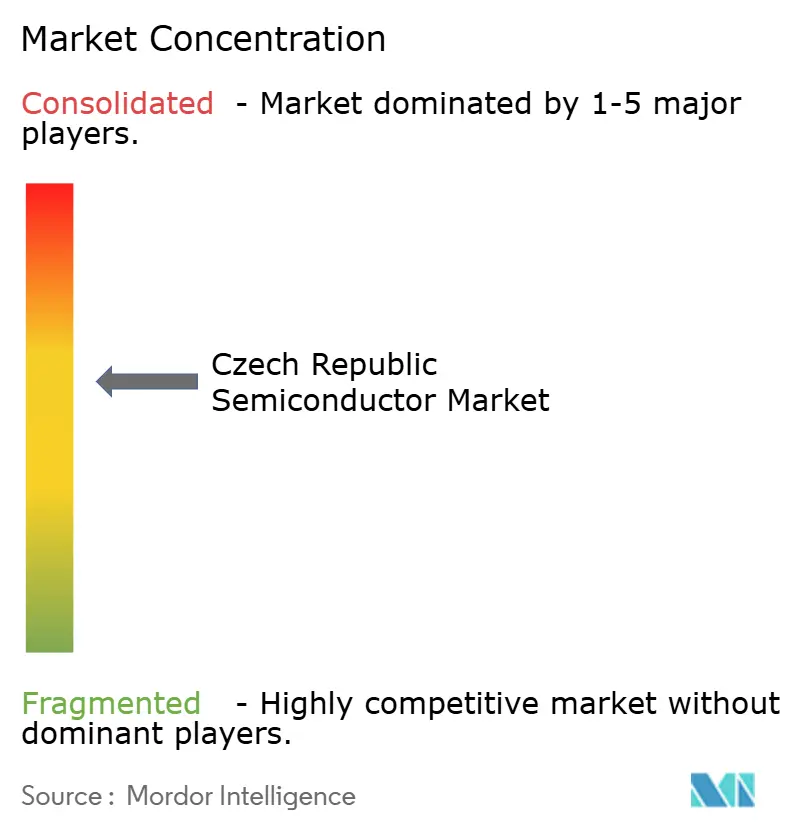

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic Semiconductor Market Analysis by Mordor Intelligence

The Czech Republic semiconductor market size reached USD 2.11 billion in 2025 and is forecast to climb to USD 2.65 billion by 2030, reflecting a 4.69% CAGR. This steady trajectory signals that the Czech Republic's semiconductor market is moving from a niche regional base toward a core pillar of the European Union’s drive for chip sovereignty. Demand from vehicle electrification, factory automation, and silicon-carbide (SiC) power devices anchors near-term growth, while deep-tech funding and international partnerships extend the opportunity set into artificial intelligence and advanced packaging. End-to-end SiC production by onsemi, an expanding processor-IP startup scene in Prague, and Brno’s new Taiwan-Czech design center together tighten the local value chain. Persistent shortages of senior engineers and energy-price volatility remain limiting factors, yet coordinated state aid and university-industry alliances are closing these gaps and elevating national competitiveness.

Key Report Takeaways

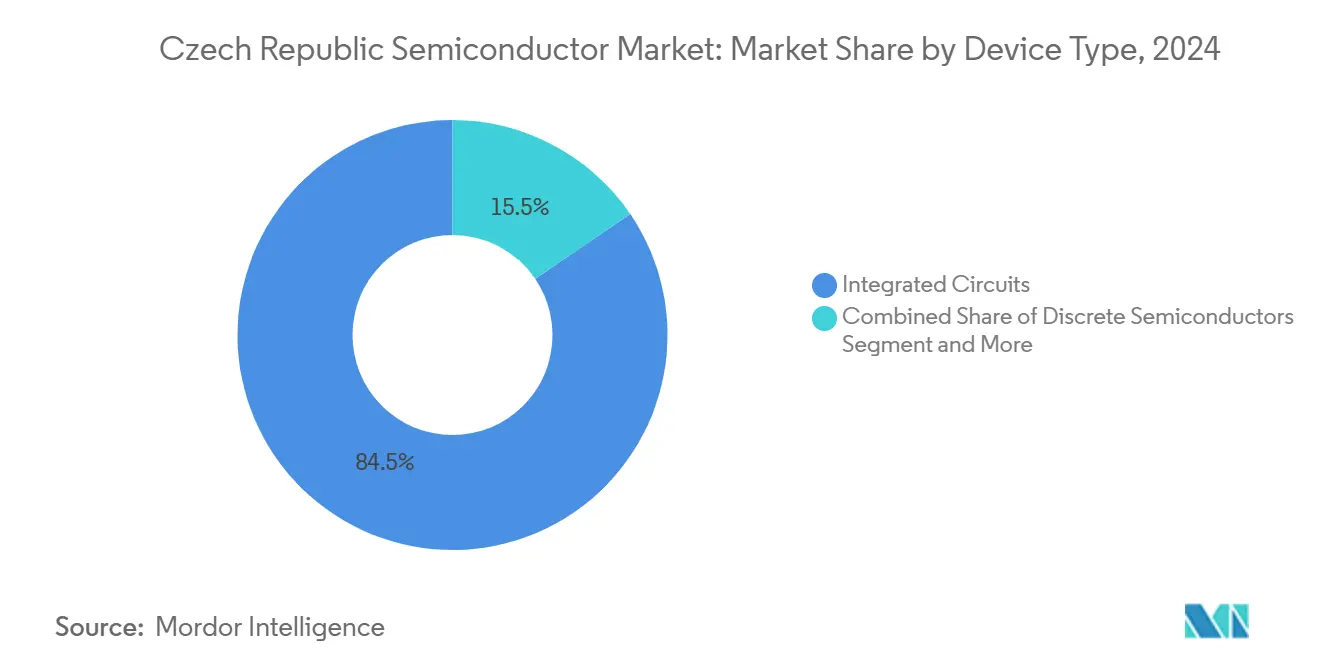

- By device type, Integrated Circuits led with 84.52% revenue share of the Czech Republic semiconductor market in 2024; Sensors and MEMS are projected to expand at a 6.0% CAGR to 2030.

- By business model, the IDM segment held 72.3% of the Czech Republic semiconductor market share in 2024, while Design/Fabless vendors record the highest projected CAGR at 5.7% through 2030.

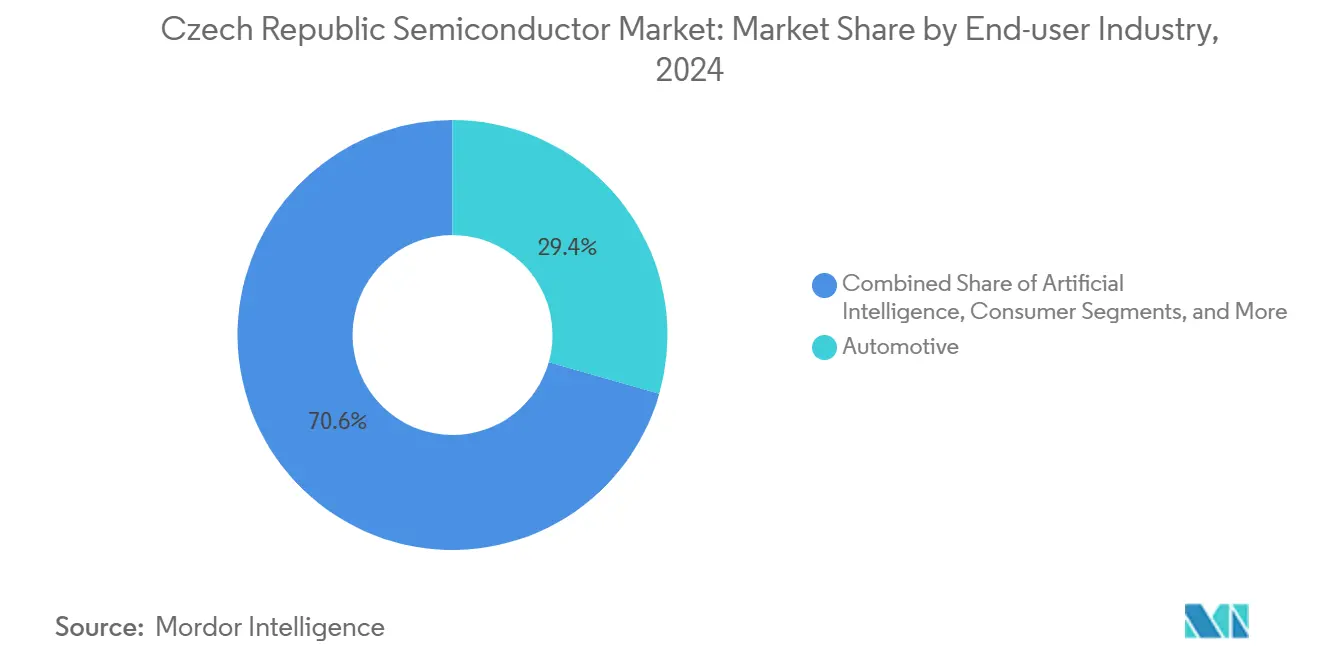

- By end-user industry, automotive applications accounted for 29.41% of the Czech Republic's semiconductor market size in 2024, and artificial intelligence is advancing at a 6.1% CAGR through 2030.

Czech Republic Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive-electronics push by Czech vehicle OEMs | +1.2% | National, concentrated in Mladá Boleslav, Kvasiny, Vrchlabí | Medium term (2-4 years) |

| EU Chips Act-backed R&D funding inflows | +0.8% | National, with focus on Brno research corridors | Long term (≥ 4 years) |

| Industrial automation sensor demand surge | +0.7% | National, with spillover to Central European supply chains | Short term (≤ 2 years) |

| Onsemi Rožnov SiC capacity expansion | +0.6% | Regional, centered in Moravian-Silesian region | Medium term (2-4 years) |

| University–industry RF-IC consortia (Brno) | +0.3% | Regional, Brno metropolitan area | Long term (≥ 4 years) |

| Rise of Prague-based processor-IP start-ups | +0.2% | Regional, Prague innovation ecosystem | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive-electronics push by Czech vehicle OEMs

Škoda Auto’s rebound to 925,164 vehicles in 2024 has restored line-side semiconductor consumption, and each new battery-electric model raises SiC power-device content per car. [1]“Production and Logistics | Škoda Annual Report 2024,” Škoda Auto, reporting.skoda-auto.com Vitesco Technologies’ EUR 188 million plant in Ostrava accelerates local sourcing of high-voltage inverters, tightening links with onsemi’s Rožnov SiC wafer supply. Vehicle makers are piloting 5G shop-floors that rely on robust RF front-ends and edge AI chips to orchestrate autonomous logistics. Multi-year purchasing deals between onsemi and Volkswagen Group further secure offtake, locking in mid-decade demand visibility. These moves together position the Czech Republic semiconductor market as a preferred Tier-1 supply hub for Central European auto OEMs.

EU Chips Act-backed R&D funding inflows

A CZK 3 billion DEEP TECH grant line and the EUR 960 million Czech state-aid envelope channel capital directly into chip design, packaging, and pilot-line projects. Brno’s Advanced Chip Design Research Center blends Taiwanese foundry know-how with local RF-mixed-signal expertise, giving domestic teams early access to advanced-node PDKs. NXP’s EUR 1 billion EIB loan earmarks a share for Czech lab expansion, ensuring volume customers for home-grown IP blocks. [2]“NXP Secures €1 Billion EIB Loan to Advance Semiconductor Innovation,” NXP Semiconductors, nxp.com Universities in Prague, Brno, and Ostrava run AI testbeds that integrate custom accelerator silicon, seeding design skills among graduate engineers. Collectively, these measures lift long-term innovation intensity and attract private co-investment.

Industrial automation sensor demand surge

Manufacturing still contributes 35% of Czech GDP, and labor scarcity drives rapid robot adoption. Each collaborative robot, machine-vision cell, or predictive-maintenance loop requires a dense mix of pressure, magnetic, optical, and motion sensors. Joint projects between FEKT VUT and more than 200 factories funnel sensor prototypes from lab benches to production lines within a year. Škoda’s campus-wide EV-charger optimization illustrates how sensor arrays feed big-data engines that, in turn, refine layout, energy draw, and throughput. The accelerating rollout keeps the Czech Republic's semiconductor market firmly aligned with Industry 4.0 demand curves.

Onsemi Rožnov SiC capacity expansion

A USD 2 billion outlay upgrades Rožnov into Europe’s first fully integrated SiC line, spanning crystal growth, 150 mm wafering, and advanced power module assembly. The plant is forecast to add USD 270 million to the Czech GDP per year and raise local semiconductor employment to roughly 3,000 staff. Volkswagen’s next-generation EV platform locks in a multiyear SiC supply deal that back-stops fab utilization. Although 170 positions were trimmed in 2025 for cost alignment, engineering headcount continues to expand in epitaxy and device-prototyping roles. The project cements a regional cluster for power electronics, feeding both auto and renewable-energy inverters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic wafer-fab scale | -0.9% | National, affecting all semiconductor segments | Medium term (2-4 years) |

| Import-dependency for process equipment | -0.6% | National, with particular impact on advanced node production | Long term (≥ 4 years) |

| Scarcity of senior semiconductor engineers | -0.5% | National, concentrated in Prague and Brno tech hubs | Short term (≤ 2 years) |

| Energy-price volatility for high-power fabs | -0.4% | National, with disproportionate impact on energy-intensive processes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited domestic wafer-fab scale

Onsemi’s 6-inch line covers legacy bipolar, CMOS, and power MOSFET flows but falls short of 300 mm volumes or sub-28 nm logic nodes. Prague’s fabless startups must tape-out at overseas foundries, stretching lead times and eroding margin capture. The Dresden ESMC mega-fab in neighboring Germany may siphon both projects and senior engineers, widening the capacity gap. Without a second mid-volume fab, the Czech Republic semiconductor market stays reliant on cross-border capacity, limiting economies of scale.

Energy-price volatility for high-power fabs

Electricity still costs measurably more in Czechia than in Germany, a spread that hits crystal-growth furnaces and backend anneal ovens hardest. Trade bodies cite energy inflation as a core reason some assemblers reverted to Asian component sourcing in 2024 and 2025. [3]“Zhodnocení Roku 2024 a Výhled na Českou Ekonomiku 2025,” Svaz průmyslu a dopravy ČR, spcr.cz Onsemi and other power-device makers push for renewable subsidies or long-term price contracts to maintain cost parity with Western European peers. Until price stability arrives, expansion decisions carry higher financial risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor Revenue and Sensors Accelerate

Integrated Circuits contributed 84.52% of 2024 revenue, equal to USD 1.78 billion of the Czech Republic's semiconductor market size. Automotive-grade power-management ICs and mixed-signal drivers dominate because domestic OEMs demand high reliability and extended temperature ranges. The pipeline now includes domain-controller SoCs co-designed with Prague IP startups, signaling a shift into higher-value compute devices.

Sensors and MEMS deliver the swiftest uplift with a projected 6.0% CAGR. Factory-floor digitization triggers steep unit growth for pressure, magnetic, and optical sensors integrated into robot arms and test rigs. Local design teams leverage CEITEC nano-fab facilities for quick prototyping, while established IDM lines at onsemi supply mature Hall-effect sensors. Discrete power devices, optoelectronics, and RF front-ends keep steady momentum, ensuring balanced product breadth in the Czech Republic semiconductor market.

By Business Model: IDM Scale Meets Fabless Creativity

IDMs controlled 72.3% of the Czech Republic semiconductor market share in 2024, translating to roughly USD 1.53 billion of sales. Vertical integration reassures automotive clients on traceability and lifecycle support. Onsemi’s Rožnov complex and NXP’s regional power-train IC lines exemplify this scale advantage.

Fabless design houses post a 5.7% CAGR as venture capital and EU grants lower entry barriers. Codasip raised USD 2.8 million to commercialize RISC-V processor cores, while Neuronix’s AI-edge IP won acquisition by Microchip, validating exit pathways. Access to Taiwan-Czech PDK stacks further boosts design throughput. Together, the dual-track model enlarges the talent pool and diversifies revenue streams in the Czech Republic semiconductor market.

By End-user Industry: Vehicles Lead, AI Outruns

Automotive captured 29.41% of 2024 demand, or nearly USD 620 million of the Czech Republic semiconductor market size, thanks to EV power modules, ADAS radar MMICs, and infotainment processors. Škoda, Hyundai, and Toyota plants all raised semiconductor content per vehicle through 2025.

Artificial intelligence chips register the fastest 6.1% CAGR as Czech corporates deploy edge inferencing in logistics, utilities, and medical imaging. Brno’s AI design center rolls out low-power accelerators, while data-center operators install GPU clusters that rely on high-bandwidth memory modules. Industrial automation, communication infrastructure, and data-storage segments each sustain mid-single-digit growth, broadening the application mix.

Geography Analysis

Moravian-Silesian county anchors manufacturing scale through onsemi’s SiC hub, now slated to push out 150 mm epi-ready wafers for both internal and merchant sales. Annual output capacity is expected to exceed 200,000 wafers by 2027, cementing the region’s export orientation. An adjacent advanced-packaging park readies ground for substrate, molding, and test vendors, knitting a complete back-end corridor.

Prague forms the nation’s design nucleus. Processor-IP ventures, security ASIC houses, and RF front-end integrators cluster around technical universities and shared EDA cloud farms. Access to seed capital, international accelerators, and multilingual engineering graduates draws in cross-border project mandates. As a result, the Czech Republic semiconductor market radiates value beyond physical wafers into IP royalties and design services.

Brno sits at the intersection of academia and prototype fabrication. CEITEC’s class-100 cleanroom supports MEMS die runs, while the new Advanced Chip Design Research Center feeds tape-outs into Asian and European foundries. Local start-ups sprint from tape-out to packaged samples in under nine months, shortening commercialization cycles. Coordinated investment-park rollout by SIRS links these three hubs with modern logistics and redundant power, ensuring that geographic dispersion does not hinder supply-chain velocity.

Competitive Landscape

The top five semiconductor suppliers together command roughly 48% of national revenue, indicating moderate concentration. Onsemi alone holds the largest single-player position through captive SiC, Hall-sensor, and power-MOSFET lines. NXP and Infineon stress automotive MCUs and micro-power ICs; STMicroelectronics’ pending takeover of NXP’s sensor unit further consolidates motion-sensing know-how on Czech soil. [4]“STMicro to Buy Part of NXP’s Sensor Business for up to $950 Million,” Reuters, reuters.com Texas Instruments maintains a mixed-signal design center servicing European car OEMs.

Domestic newcomers sharpen focus on niche compute or metrology gaps. Codasip offers configurable RISC-V cores for domain-specific acceleration, while TESCAN adapts electron-beam inspection for advanced packaging lines. University-spin-outs license RF-MEMS switches and sub-6 GHz power amplifiers, broadening product diversity. Partnership models predominate: fabless firms rely on global foundry alliances, whereas IDMs prefer long-term power-module contracts with automotive Tier-1s.

Government policy shapes rivalry. Grants under the EU Chips Act tilt capex toward power devices, where Czechia already enjoys a labor-cost edge. However, energy-price disparities with Germany expose fabs to cost shocks, nudging players to invest in rooftop solar and long-term power-purchase agreements. Overall, strategy orbits around marrying local engineering depth with multinational capital to lift the Czech Republic semiconductor market toward higher-margin layers.

Czech Republic Semiconductor Industry Leaders

onsemi Czech Republic, s.r.o.

NXP Semiconductors Czech Republic s.r.o.

Infineon Technologies Czech Republic s.r.o.

STMicroelectronics Design and Application s.r.o.

Renesas Design Czech s.r.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Onsemi confirmed a USD 2 billion end-to-end SiC facility in Rožnov, the nation’s largest private investment.

- July 2025: Onsemi posted Q2 2025 free-cash-flow gains of 72% year over year.

- July 2025: STMicroelectronics agreed to buy part of NXP’s sensor business for up to USD 950 million.

- March 2025: Onsemi announced a 170-employee Czech workforce adjustment amid cost streamlining.

- March 2025: The EU approved a EUR 960 million Czech aid scheme for strategic sectors including semiconductors.

- January 2025: Vitesco Technologies opened a EUR 188 million Ostrava plant for high-voltage EV modules.

- January 2025: Onsemi reported Q1 2025 revenue of USD 1,445.7 million and returned 66% of free cash flow to shareholders.

Czech Republic Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Czech Republic semiconductor market in 2025?

The Czech Republic semiconductor market size is USD 2.11 billion in 2025.

What is the forecast CAGR through 2030?

Market value is projected to rise at a 4.69% CAGR to reach USD 2.65 billion by 2030.

Which device category dominates revenue?

Integrated Circuits generate 84.52% of 2024 revenue, led by automotive power-management and mixed-signal chips.

Which end-user segment is expanding fastest?

Artificial intelligence applications show the quickest growth at a 6.1% CAGR through 2030.

What role does onsemi play in the local ecosystem?

Onsemi’s USD 2 billion Rožnov facility delivers end-to-end SiC production, anchoring power-device supply for European EV makers.

How supportive is government policy?

A EUR 960 million state-aid scheme and a CZK 3 billion DEEP TECH grant line under the EU Chips Act provide robust funding for R&D and pilot production.

Page last updated on: