Poland Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

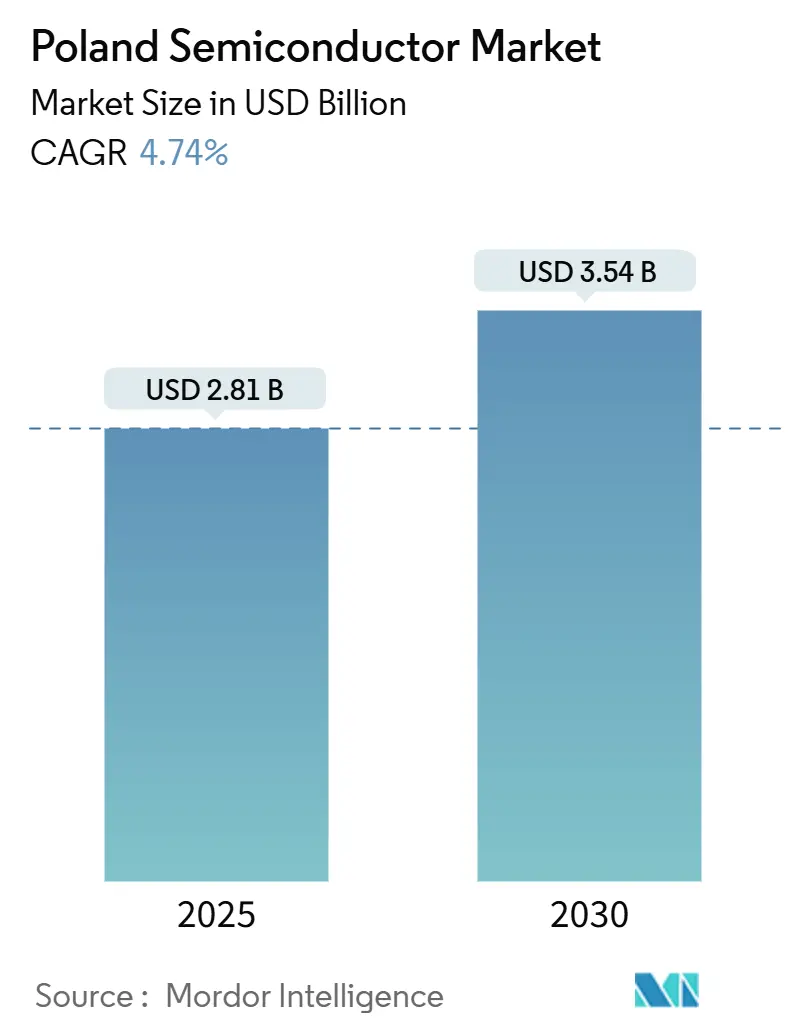

| Market Size (2025) | USD 2.81 Billion |

| Market Size (2030) | USD 3.54 Billion |

| Growth Rate (2025 - 2030) | 4.74% CAGR |

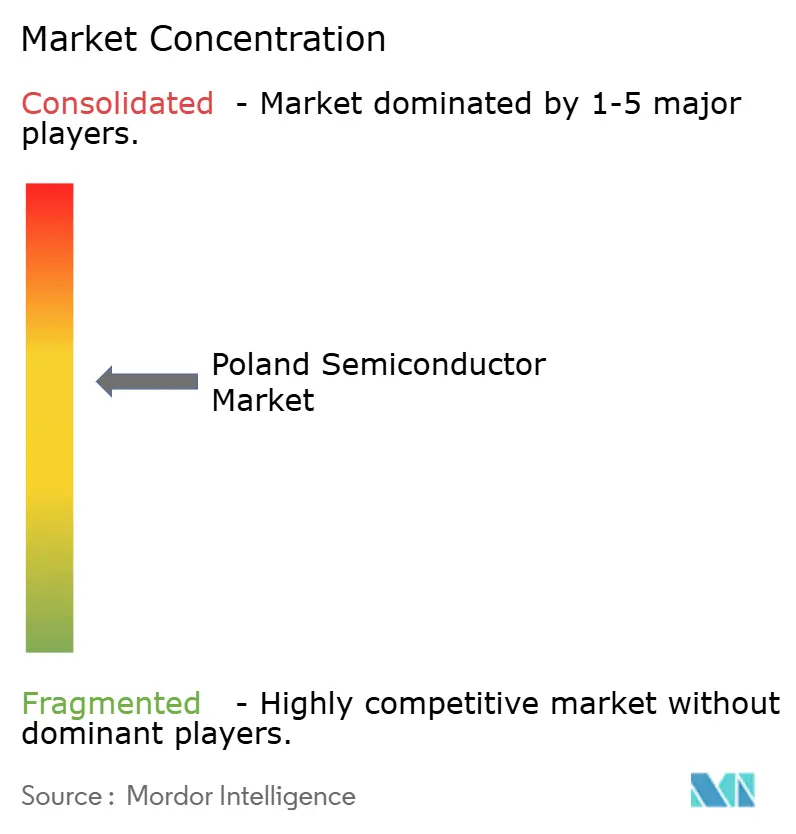

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Semiconductor Market Analysis by Mordor Intelligence

The Poland semiconductor market size stood at USD 2.81 billion in 2025 and is on track to reach USD 3.54 billion by 2030, translating into a 4.74% CAGR over the forecast period. This growth aligns with the European Union’s ambition to reclaim 20% of global chip production capacity through the EUR 80 billion Chips Act, positioning the Poland semiconductor market as a central pillar of Europe’s supply-chain sovereignty agenda. Strong domestic demand from electric-vehicle powertrains, surging advanced driver-assistance requirements, and accelerating Industry 4.0 adoption continue to create high-value opportunities for integrated-circuit vendors. Meanwhile, generous state-aid packages and a favorable renewable-energy cost base strengthen Poland’s attractiveness for capital-intensive manufacturing and R&D projects. Geopolitical stability, proximity to the German silicon hub, and a maturing talent pool further encourage multinational corporations to localize critical activities beyond traditional Asian centers.

Key Report Takeaways

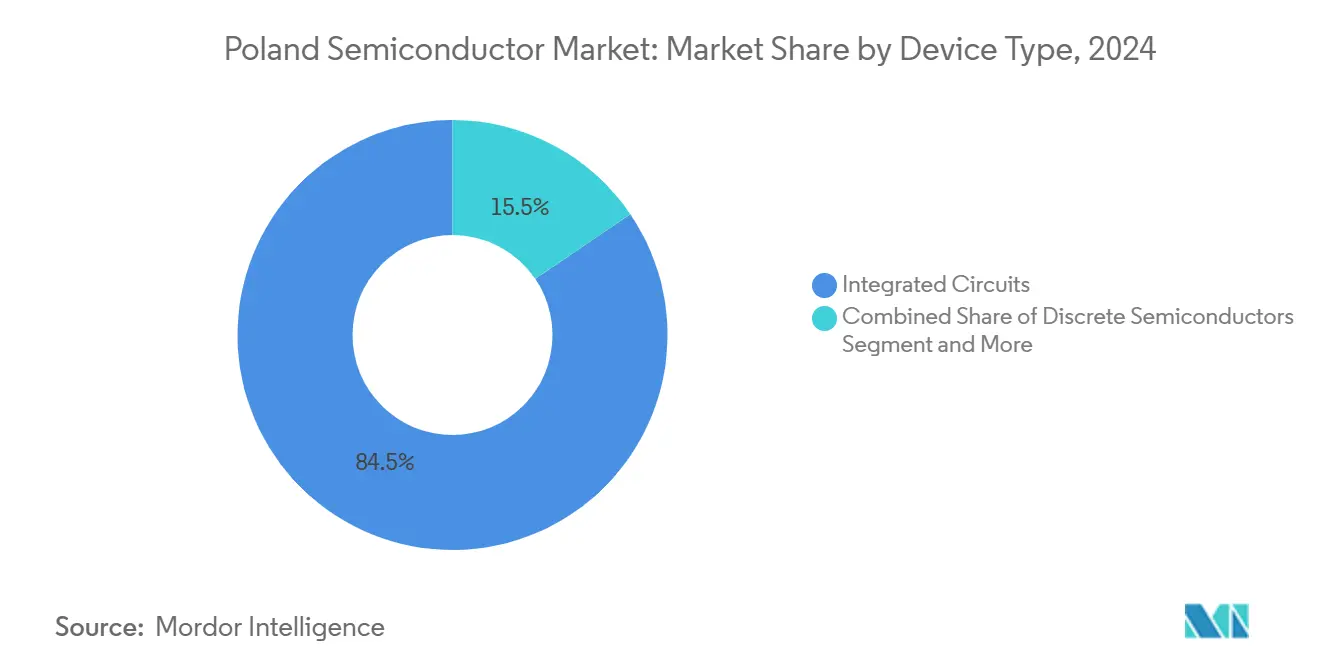

- By device type, integrated circuits secured 84.5% of Poland's semiconductor market share in 2024; the sensors and MEMS segment is projected to register the fastest 6.3% CAGR through 2030.

- By business model, IDMs accounted for a 61.3% share of the Poland semiconductor market size in 2024, while design/fabless vendors are forecast to grow at a 5.6% CAGR to 2030.

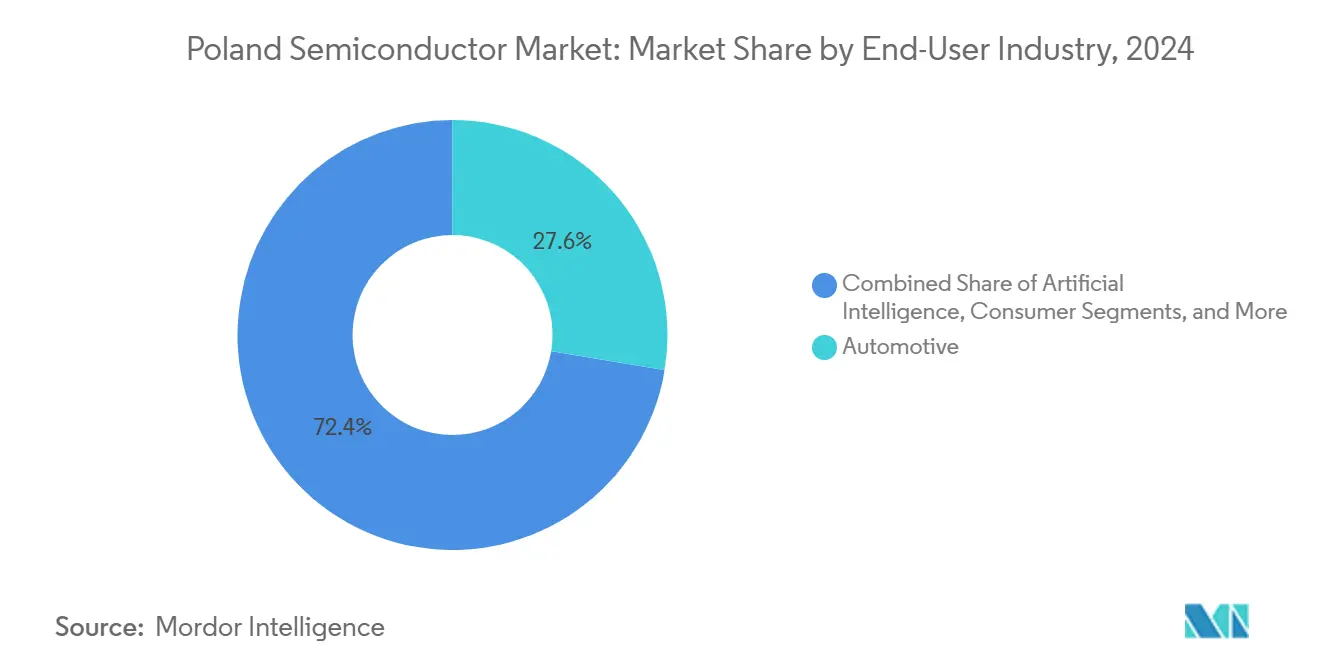

- By end-user industry, automotive held a 27.61% share of the Poland semiconductor market size in 2024, and artificial-intelligence deployments are expected to expand at a 6.5% CAGR through 2030.

Poland Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV and ADAS-driven power semiconductor demand surge | +1.2% | National, with concentration in Silesia and Pomerania regions | Medium term (2-4 years) |

| EU Chips Act subsidies and national incentive schemes | +0.8% | National, aligned with EU-wide initiatives | Long term (≥ 4 years) |

| Industrial IoT (Industry 4.0) uptake in Polish factories | +0.6% | National, strongest in manufacturing hubs | Medium term (2-4 years) |

| Expansion of global semiconductor R&D centers in Poland | +0.5% | National, concentrated in major cities | Long term (≥ 4 years) |

| Photonics sensor specialization for defense and space | +0.3% | National, defense sector focus | Long term (≥ 4 years) |

| Renewable-energy cost advantage for prospective fabs | +0.4% | National, particularly wind-rich regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV and ADAS-Driven Power-Semiconductor Demand Surge

Poland’s transition toward electromobility lifts per-vehicle semiconductor content from 700 units in conventional cars to nearly 3,000 units in battery-electric models, propelling the Poland semiconductor market well beyond its historical trajectory. Exports worth EUR 39.7 billion in 2022 generated a local supplier base that consumes power-management ICs, battery-management ASICs, and high-voltage discretes at scale. [1]PAIH, “Invest in Poland,” paih.gov.pl Government plans to deploy 1 million EVs by 2025 and expand public charging points from 5,000 to 100,000 by 2030, creating predictable pipeline visibility for chipmakers. Advanced driver-assistance mandates under the EU’s General Safety Regulation add radar, LiDAR, and sensor-fusion silicon to every vehicle platform, widening total addressable demand. Poland’s cost-competitive renewable-energy mix lowers fab operating expenses, reinforcing the country’s appeal for power-semiconductor back-end facilities. Consequently, automotive OEMs are pursuing long-term silicon sourcing agreements with both IDMs and local fabless houses, deepening the competitive moat of the Poland semiconductor market.

EU Chips Act Subsidies and National Incentive Schemes

The European Commission’s EUR 8.1 billion IPCEI approval in 2023 formalized a funding structure that rewards projects critical to resilience and innovation. [2]European Commission, “IPCEI Microelectronics II,” ec.europa.eu Poland’s share—illustrated by the PLN 7.4 billion (USD 1.9 billion) package earmarked for Intel’s since-cancelled facility—shows the government’s readiness to absorb execution risk for large semiconductor assets. The March 2025 formation of a EUR 43 billion Semicon Coalition among nine EU members adds a region-wide financial safety net that de-risks frontier-node R&D and specialty process rollouts. Domestic frameworks now bundle tax holidays, capex grants, and workforce training subsidies into single-window approvals, shortening investment lead times. These measures act as a structural growth lever, amplifying capital inflows and bolstering the Poland semiconductor market.

Industrial IoT (Industry 4.0) Uptake in Polish Factories

Manufacturing contributes almost 20% of Poland’s GDP, and recent policy efforts direct PLN 163.6 million to R&D that digitizes production lines. Early adopters in metals, chemicals, and food processing report double-digit quality improvements, validating payback models for edge AI controllers, secure microcontrollers, and low-power sensor arrays. Driven by the need to compete with Western European peers, plant managers increasingly standardize on modular automation platforms that demand higher semiconductor content per machine. Network effects develop as suppliers and service providers refit portfolios to plug into smart-factory ecosystems, expanding the addressable base for the Poland semiconductor market. Meanwhile, regulatory incentives around energy efficiency accelerate retrofit programs, locking in new silicon sockets for at least one equipment lifecycle.

Expansion of Global Semiconductor R&D Centers in Poland

Multinationals leverage Poland’s 80,000-plus STEM graduates per year and competitive salary levels to establish engineering campuses that design high-value automotive processors, RF front ends, and photonics sensors. NXP’s EUR 1 billion European Investment Bank loan specifically allocates R&D outlays across five countries—Poland among them—illustrating institutional confidence in local capability depth. Taiwan’s USI and MediaTek expansions add heterogeneous-integration know-how, fostering cross-pollination between Asian process leadership and European system requirements. Government-backed institutes like the Łukasiewicz Network supply pilot lines for advanced semiconductor packaging, shortening time-to-prototype for domestic fabless firms. These dynamics fortify the talent pipeline, stimulate patent activity, and embed Poland more deeply in EU supply-chain decision making, sustaining long-run momentum for the Poland semiconductor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce domestic wafer-fab capacity | -0.9% | Nationwide | Medium term (2-4 years) |

| Shortage of experienced chip-design engineers | -0.7% | Tech hubs | Short term (≤ 2 years) |

| Regional power-grid reliability concerns | -0.4% | Industrial zones | Medium term (2-4 years) |

| Competition for EU semiconductor funds | -0.3% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Domestic Wafer-Fab Capacity

The absence of a high-volume wafer fab forces Polish chip companies to queue at European foundries or outsource to Asia, increasing logistics costs and elongating lead times. [3]European Court of Auditors, “The EU’s Strategy for Microchips,” eca.europa.eu Intel’s July 2025 withdrawal erased a near-term path toward local back-end capacity, compelling automotive and industrial clients to hedge with suppliers outside Poland. Reliance on neighboring fabs also restricts access to reserved automotive process lines, risking production stoppages when allocations tighten. Niche players in photonics and RF see innovation cycles slow because mask-set iterations traverse multiple borders. Unless new fabs or shared pilot lines come online, the Poland semiconductor market faces structurally higher supply-chain risk that could temper its above-GDP growth premium.

Shortage of Experienced Chip-Design Engineers

Polish universities graduate ample electrical-engineering students, yet only a fraction specialize in advanced mixed-signal, RF, or power-management design. The European ambition to double regional chip output by 2030 magnifies the talent crunch, with Ireland’s experience showing that mature hubs still struggle to meet demand. Local firms frequently lose senior architects to higher-paying multinational design centers, widening project-delivery gaps. Government programs target a 20% engineering-talent increase by 2030, but curriculum modernization and faculty-development cycles take time. This bottleneck could cap the addressable workload for emerging fabless ventures, delaying revenue capture across the Poland semiconductor industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Drive Market Leadership

Integrated circuits dominated 2024 revenue with an 84.5% share of the Poland semiconductor market size, reflecting deep penetration into vehicle control units and industrial-automation controllers. Power-efficient microcontrollers and domain-specific system-on-chips increasingly replace discrete architectures as OEMs migrate toward software-defined vehicles. Sensors and MEMS, the fastest-expanding category at a 6.3% CAGR, are propelled by camera modules, radar transceivers, and environmental monitors that underpin ADAS and predictive-maintenance rollouts. Optoelectronics enjoys steady momentum through defense-grade IR detectors supplied by local champion VIGO System S.A., underlining Poland’s photonics niche.

The ascent of integrated circuits anchors Poland in the higher-margin layers of the value chain. Access to European open-foundry programs accelerates complex IC packaging and heterogeneous-integration pilots, giving national design houses a viable path to differentiated ASICs. As OEM roadmaps converge on centralized compute architectures, tier-1 suppliers pre-qualify Polish IC vendors for design-in opportunities spanning power-train inverters to zonal gateways. This keeps the Poland semiconductor market on a structural uptrend, even if discrete component volumes flatten alongside legacy platforms.

By Business Model: IDM Leadership Faces Fabless Challenge

IDMs retained 61.3% revenue in 2024 thanks to stringent automotive quality-assurance protocols that favor vertically integrated supply. Yet fabless firms compound at a 5.6% CAGR, taking advantage of European wafer-capacity build-outs that lower time-to-tape-out costs. The share shift captures a broader industry tilt toward asset-light models and underpins competitive churn within the Poland semiconductor market. IDM rationalization, such as NXP’s plan to close four 8-inch lines and pivot to 12-inch production, signals that even incumbents must recalibrate fixed-asset footprints.

Fabless growth leverages Poland’s engineering wage arbitrage and proximity to leading-edge process nodes in Dresden and Taiwan. Government innovation grants offset EDA licensing and MPW tape-out fees, leveling early-stage barriers. Meanwhile, OEMs diversify supply chains post-pandemic, awarding design wins to agile fabless houses that customize power-management ICs within accelerated cycles. As capital-expenditure intensity rises, the fabless camp is poised to erode additional share from legacy IDMs, reinforcing a mixed-model structure across the Poland semiconductor market.

By End-User Industry: Automotive Dominance Meets AI Disruption

Automotive accounted for 27.61% of 2024 revenue, underscoring Poland’s position as Europe’s third-largest vehicle producer and a regional e-mobility hub. Vehicle electrification, safety regulation, and domain-controller architectures create an expanding silicon bill of materials that anchors baseline demand for the Poland semiconductor market. Artificial-intelligence applications, however, exhibit the briskest 6.5% CAGR through 2030 as factories, data centers, and autonomous-infrastructure projects require edge accelerators and high-bandwidth memory.

Industrial clients adopt smart-factory solutions at scale, driving microcontroller, connectivity, and sensor deployments beyond pilot projects. Communication-equipment suppliers benefit from 5G node densification, while renewable-energy developers integrate SiC-based inverters co-designed with local chipmakers. The result is a widening spread of end-user exposure that buffers cyclicality and reinforces the overarching expansion arc of the Poland semiconductor market.

Geography Analysis

Poland’s central-European location links Western design hubs to Eastern manufacturing clusters, giving the country logistical reach that few EU peers share. Founding membership in the EUR 43 billion Semicon Coalition provides preferential access to cross-border pilot lines and guarantees priority wafers at the Dresden mega-fab once production ramps up in 2026. The Lower-Silesia region hosts several multinationals alongside a burgeoning photonics community, anchoring a technology corridor that shortens supply routes for automotive OEMs in nearby Slovakia and Czechia.

Pro-investor legislation allows rapid greenfield development, exemplified by the record-time permitting originally granted to Intel’s cancelled back-end facility. Renewables penetration near the Baltic coast reduces electricity tariffs for hypothetical fabs, while freight corridors to the German border expedite raw-wafer imports and finished-chip exports. However, competition intensifies as neighboring countries deploy their incentive schemes—Czechia secured a USD 2 billion SiC fab from ON Semiconductor in 2024, highlighting the zero-sum nature of EU funds allocation.

Despite funding rivalry, collaborative frameworks such as shared apprenticeship programs and cross-border IPCEI clusters mitigate talent bottlenecks. Poland’s resilience to geopolitical shocks further raises its strategic profile for firms hedging Asia risk, reinforcing demand pull throughout the Poland semiconductor market.

Competitive Landscape

Market structure remains moderately concentrated, with multinational subsidiaries and specialized domestic players sharing revenue pools across device types. Intel’s cancelled USD 4.6 billion plant preserved the status quo, preventing any single vendor from reaching dominant manufacturing scale. [4]CIJ Europe, “Intel Cancels Factory Plans in Poland,” cijeurope.com IDMs like Infineon, NXP, and Bosch secure long-term automotive contracts, while fabless challengers carve niches in sensors, power-management ASICs, and millimeter-wave radar.

Partnership networks become the primary route to differentiation. VIGO System S.A. teams with defense integrators to supply space-grade IR detectors, translating photonics know-how into high-margin programs. Meanwhile, Polish design houses co-develop zonal-controller reference boards with Western tier-1s, embedding their IP in next-generation EV architectures. Public-private R&D initiatives funnel grants into heterogeneous-integration RDL stacking, positioning local specialists for future packaging leadership.

The competitive equilibrium rewards ecosystem participation over vertical integration, allowing SME players to monetize proprietary IP without assuming wafer-fab capex. As IDMs restructure legacy assets and regional fabs ramp, share redistribution is likely, reinforcing the dynamic nature of the Poland semiconductor market.

Poland Semiconductor Industry Leaders

Intel Technology Poland Sp. z o.o.

Infineon Technologies Poland Sp. z o.o.

STMicroelectronics Polska Sp. z o.o.

NXP Semiconductors Poland Sp. z o.o.

Texas Instruments Poland Sp. z o.o.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Intel terminated its planned USD 4.6 billion assembly and test facility, halting 2,000 expected jobs.

- May 2025: Infineon obtained final German approval for its EUR 5 billion Smart Power Fab in Dresden, slated to employ 1,000 personnel from 2026.

- March 2025: Nine EU nations, including Poland, launched the EUR 43 billion Semicon Coalition under the Chips Act umbrella.

- February 2025: Infineon released its first 200 mm silicon-carbide products out of Villach, targeting renewable-energy inverters and EV drivetrains.

- January 2025: NXP secured a EUR 1 billion EIB loan to expand automotive-processor R&D footprints across Europe, Poland included.

Poland Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Poland semiconductor market in 2025?

It is valued at USD 2.81 billion, with forecasts pointing to USD 3.54 billion by 2030 at a 4.74% CAGR.

Which segment leads revenue in the Poland semiconductor market?

Integrated circuits command 84.5% revenue, driven by automotive control units and industrial-automation processors.

What funding mechanisms support chip manufacturing in Poland?

Companies tap EU IPCEI grants, national tax holidays, and the EUR 43 billion Semicon Coalition financing framework.

Why does automotive drive local chip demand?

Poland’s status as Europe’s third-largest vehicle producer and its EV transition multiply per-vehicle semiconductor content.

What risks could slow market expansion?

Limited domestic wafer-fab capacity and shortages of experienced chip-design engineers pose the most immediate growth restraints.

Page last updated on: