Cysteine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

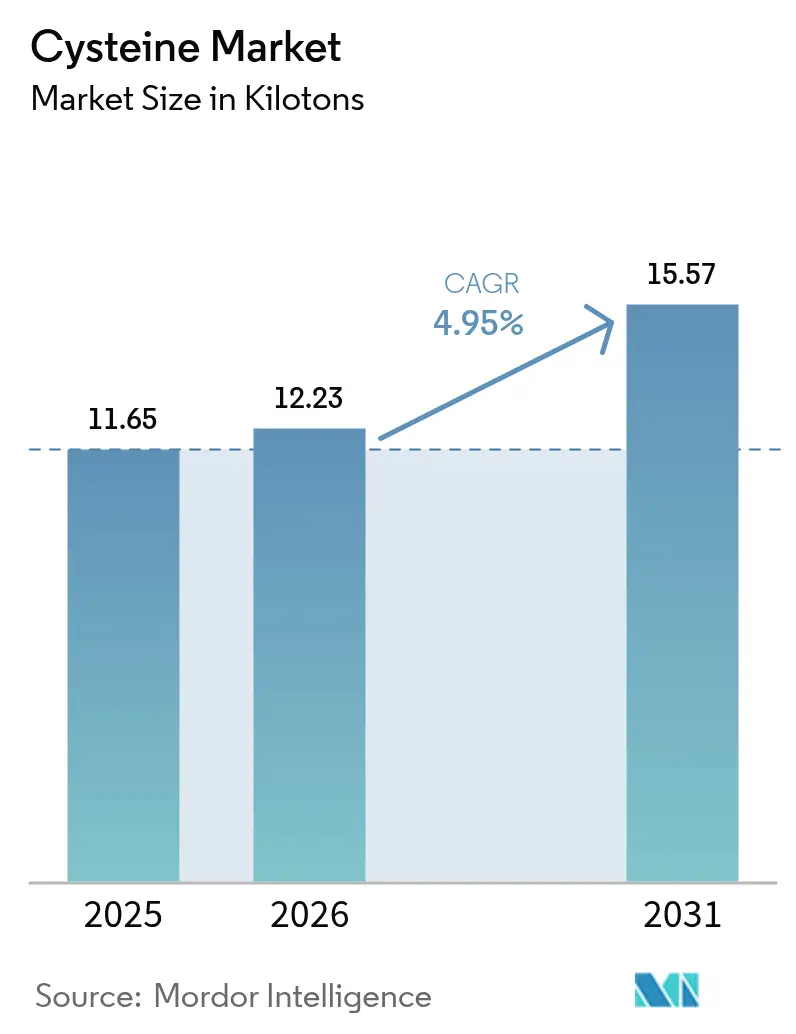

| Market Volume (2026) | 12.23 kilotons |

| Market Volume (2031) | 15.57 kilotons |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cysteine Market Analysis by Mordor Intelligence

The cysteine market size is expected to grow from 11.65 kilotons in 2025 to 12.23 kilotons in 2026 and is forecast to reach 15.57 kilotons by 2031 at 4.95% CAGR over 2026-2031. Moderate expansion continues as the amino acid’s sulfur chemistry underpins food processing, pharmaceutical, and personal-care applications that cannot be easily substituted. Bio-fermentation drives production realignment, enabling higher purity and vegan certification at competitive cost. Synthetic routes scale in parallel as producers seek additional flexibility. Demand is reinforced by the clean-label movement in packaged foods, pharmaceutical migration to plant-derived sources, and hair-care innovations that position cysteine as a safer alternative to formaldehyde-based treatments. Asia-Pacific retains its role as the supply hub, supported by large-scale fermenters, favorable feedstock economics, and expanding domestic consumption.

Key Report Takeaways

- By production process, natural fermentation held 68.34% of the cysteine market share in 2025, while the synthetic route is advancing at a 6.05% CAGR to 2031.

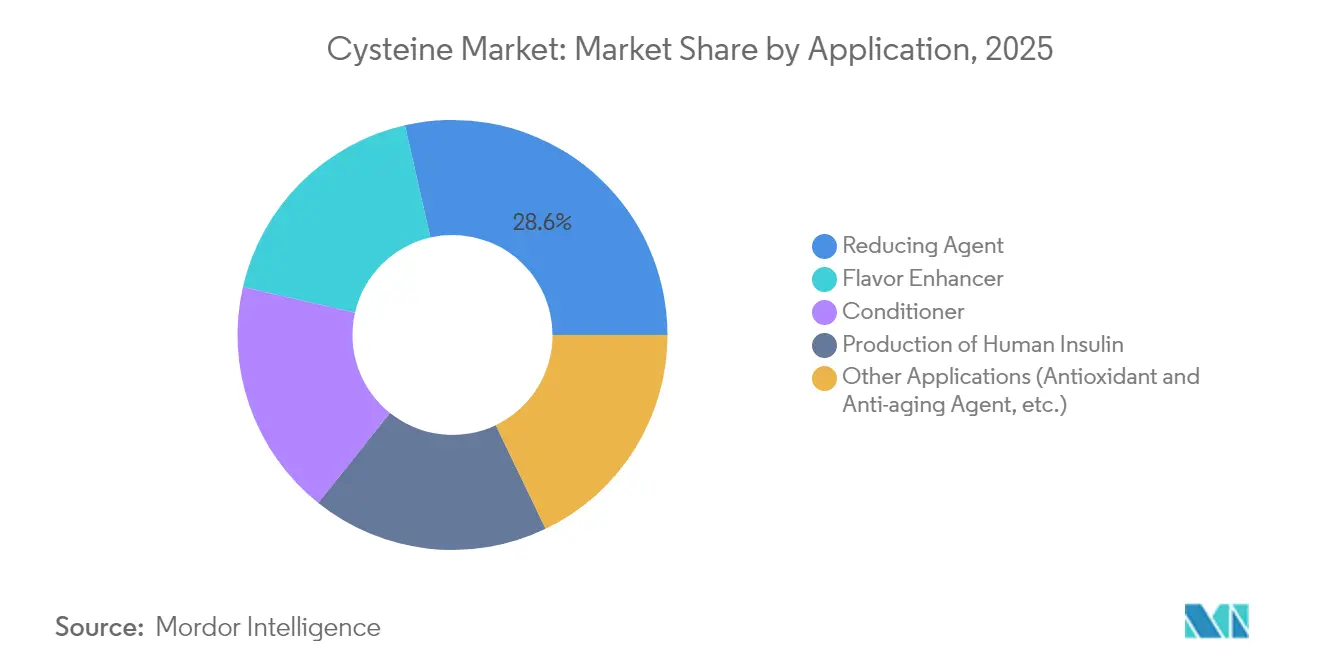

- By application, the reducing-agent segment captured 28.55% share of the cysteine market size in 2025; conditioner applications are expanding at a 6.12% CAGR through 2031.

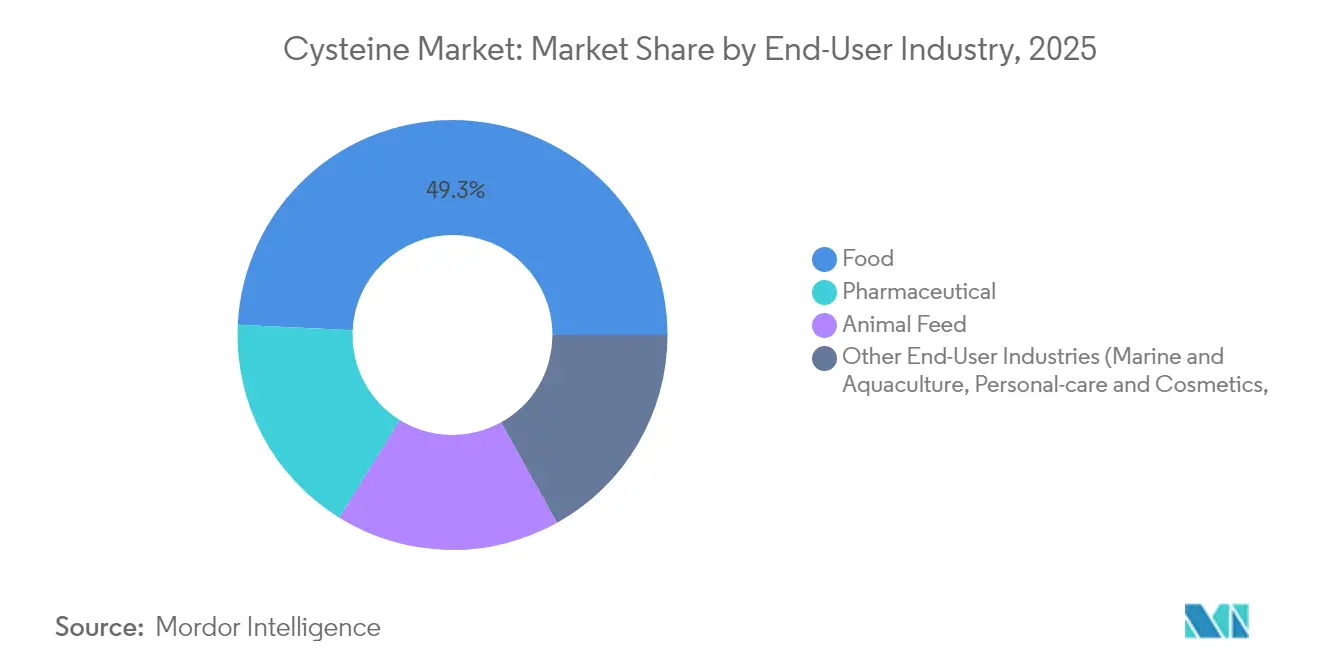

- By end user, the food sector accounted for 49.25% of the cysteine market size in 2025 and is progressing at a 5.91% CAGR to 2031.

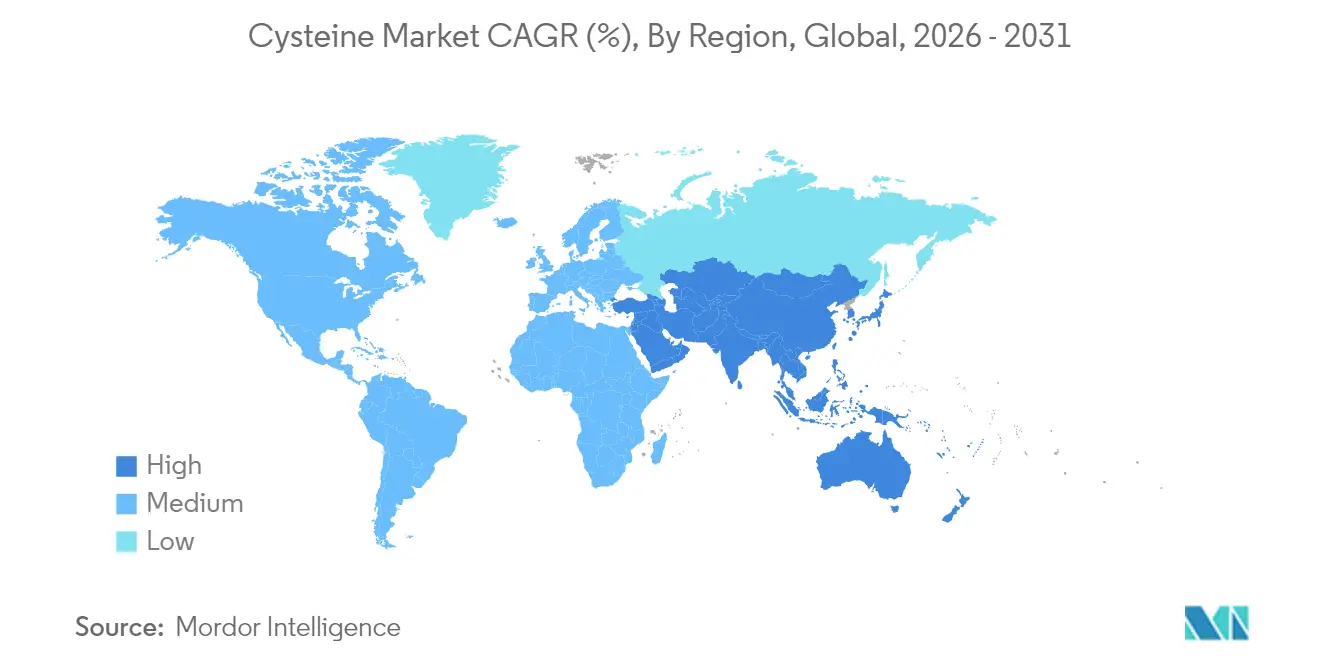

- By geography, Asia-Pacific led with 47.60% cysteine market share in 2025 and is on track for a 5.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cysteine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of bio-fermentation capacity | +1.2% | Global, APAC lead | Medium term (2-4 years) |

| Growing clean-label demand for natural flavor enhancers | +0.8% | North America & EU primary | Short term (≤ 2 years) |

| Pharmaceutical switch to plant-derived L-cysteine | +0.6% | Global, EU regulatory pull | Medium term (2-4 years) |

| Hair-care brands adopting high-dose cysteine kits | +0.4% | APAC core, LATAM spill-over | Long term (≥ 4 years) |

| Integration in green-hydrogen fuel-cell membranes | +0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Bio-Fermentation Capacity

Global producers continue to add fermenters that replace animal-hair extraction with microbial systems able to reach pharmaceutical-grade purity. Wacker Chemie’s FERMOPURE platform achieves this while cutting hydrochloric acid consumption and wastewater volumes. Engineering advances have lifted final L-cysteine titers to 33.8 g/L, a 37% improvement that lowers unit cost and widens pharmaceutical access. Fermentation aligns with vegan labeling requirements and preempts regulatory action against animal-derived inputs. New capacity in Spain, China, and India secures regional supply and hedges freight volatility. These investments raise baseline output, temper price spikes, and reinforce long-run growth for the cysteine market.

Growing Clean-Label Demand for Natural Flavor Enhancers in Processed Foods

Food formulators replace synthetic dough-conditioners and flavor boosters with amino acid alternatives that satisfy plain-language labeling rules. The U.S. Code of Federal Regulations grants GRAS status to L-cysteine monohydrochloride at 0.009 parts per 100 of flour, offering regulatory certainty for bakers[1]United States Government, “21 CFR § 184.1272 – L-Cysteine Monohydrochloride,” ecfr.gov. Thermal reaction trials confirm that cysteine enhances savory notes via sulfur-containing volatiles under Maillard conditions. CJ Food & Nutrition Tech’s FlavorNrich launch underscores commercial appetite for non-electrolytic grades that serve clean-label positioned snacks, sauces, and meat alternatives. As retailers tighten additive blacklists, natural amino acids gain shelf-life and sensory functions without regulatory friction, bolstering the cysteine market.

Pharmaceutical Switch from Animal- to Plant-Derived L-Cysteine for Parenteral Nutrition

Hospital demand for parenteral amino acids is shifting toward fermentation-origin inputs that eliminate bovine or porcine risk. Evonik’s cQrex KC dipeptide delivers 1,000-fold higher solubility than free L-cystine, streamlining high-density cell-culture feeds for healthcare[2]Evonik Health Care, "High-purity amino acids for various applications," healthcare.evonik.com. BioSpectra and other GMP suppliers follow suit, citing the regulator's preference for animal-free excipients. Parallel research links cysteine supplementation with improved redox balance in anxiety disorders, suggesting wider therapeutic utility. These trends support a durable uplift in pharmaceutical volumes in the cysteine market.

Hair-Care Brands Launching High-Dose Cysteine Smoothing Kits in Emerging Economies

Salons in India, Brazil, and Indonesia introduce formaldehyde-free smoothing services that rely on cysteine to realign disulfide bonds while limiting scalp irritation. Ingredient vendors combine plant-sourced amino acids with hydrolyzed keratin to extend treatment longevity to 4 weeks. Academic studies on lysine carboxymethyl cysteinate indicate parallel benefits in skin photoprotection, hinting at cross-category expansion. Rising disposable income and stricter cosmetic safety rules hasten substitution away from aldehyde-based straighteners. Consequently, conditioner formulations become the fastest-growing slice of the cysteine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of raw materials (sugar, corn steep liquor) | -0.7% | Global, with acute impact in APAC production hubs | Short term (≤ 2 years) |

| Increasing concerns related to animal-sourced cysteine | -0.5% | EU & North America regulatory pressure, APAC consumer shift | Medium term (2-4 years) |

| Harmful effects of cysteine on human body | -0.3% | Global, with regulatory scrutiny in pharmaceutical applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Raw Materials (Sugar, Corn Steep Liquor)

Fermentation margins tighten when feed corn and refined sugar spike, costs that mirror fertilizer and natural-gas swings. Bio-processors in Shandong and Gujarat report wider EBITDA variance when grain prices rise faster than amino acid spot values. Some producers trial molasses or upcycled starch waste to immunize cost curves, yet scale-up remains preliminary. Until substrate hedging tools mature, raw material inflation continues to temper the cysteine market’s growth pace.

Increasing Concerns Related to Animal-Sourced Cysteine

Regulators and consumers increasingly question the allergenicity and traceability of cysteine derived from hog hair or duck feathers. The UK Food Standards Agency calls for enhanced protein authentication protocols, reinforcing demand for DNA- or isotope-based origin testing. Quick-service restaurant chains react by specifying vegan-certified dough improvers, sidelining animal-origin material. The trend accelerates the pivot to bio-fermentation but also triggers short-term reformulation costs, applying moderate drag on the cysteine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Natural Fermentation Outpaces Synthetic Uptake

Natural fermentation commands 68.34% of the cysteine market share in 2025, translating into the largest contribution to overall volume. The segment benefits from consumer alignment with vegan and halal standards, strengthening its position as the default source for pharmaceutical and food producers. Synthetic pathways are smaller yet notable for a 6.05% CAGR, reflecting corporate initiatives to secure dual-sourced supply and circumvent fermentation capacity bottlenecks.

Recent investments have lifted fermenter yields through metabolic-pathway engineering that shortens reaction cycles and raises titers. As installed stainless-steel capacity ramps in China, Spain, and the Midwestern United States, fermentation retains cost leadership at full load factors. Chemical synthesis remains advantageous in niche derivative production where complex thiocarbonylation offers purity benefits. The interplay keeps both routes active but leaves natural fermentation as the anchor of the cysteine market.

By Application: Reducing Agents Lead While Conditioners Accelerate

The reducing-agent category captured 28.55% of the cysteine market size in 2025 due to extensive use in dough softening, injectable drugs, and industrial redox systems. Its dominance reflects longstanding formulation standards and predictable purchasing cycles across bakeries and pharmaceutical fill-finish lines. Conditioner applications, however, post a 6.12% CAGR, as cosmetic brands market plant-based smoothing lotions and shampoos in Asia-Pacific malls and Latin American salons.

Flavor enhancer volumes tick upward as snack and broth manufacturers seek natural savory tonalities. Niche adoption in fuel-cell membrane fabrication remains early but signals longer-run optionality. Overall, broadening personal-care use balances the maturity of food and pharma staples, sustaining healthy diversity within the cysteine market.

By End-User Industry: Food Sector Remains Growth Engine

Food processors accounted for 49.25% of the cysteine market size in 2025 and are forecast to grow 5.91% annually to 2031. The segment relies on cysteine for dough elasticity, flavor development, and antioxidant function, with clean-label claims enabling price premiums. Pharmaceutical producers follow a mid-single-digit expansion as plant-based parenteral nutrition and peptide synthesis absorb more volume.

Animal feed integrators and aquaculture farms add incremental demand by supplementing sulfur amino acids to boost weight gain and immunity. Personal-care formulators inject further upside through skin-care antioxidants and hair-bond builders. The composite picture illustrates how diversified demand anchors the cysteine market against any industry's cyclical downturns.

Geography Analysis

Asia-Pacific generated 47.60% of the cysteine market size in 2025, underpinned by integrated sugar refining, low-cost labor, and government-supported biotech parks. Regional producers benefit from captive demand within China’s bakery, instant-noodle, and generics sectors, while export lanes serve price-sensitive users in Africa and the Middle East. Growth remains strongest at 5.82% CAGR as India’s injectable-nutrition manufacturers and Korea’s cosmetic giants widen procurement volumes.

North America ranks second, propelled by well-defined FDA pathways and abundant corn substrates that lower feedstock costs. Fermentation investments cluster around the Midwest, where ethanol by-products feed amino acid lines, reducing inbound logistics. Regulatory emphasis on animal-free sourcing further redirects domestic buyers to fermentation grades, lifting the regional cysteine market.

Europe contributes steady mid-single-digit growth, anchored by Germany and Spain’s pharmaceutical-grade facilities that operate under stringent GMP and sustainability codes. Carbon-neutral production targets attract premium buyers in medical nutrition and infant formula. EU labeling laws restrict animal-hair origin inputs, consolidating demand around plant-based supply. Collectively, these dynamics place Europe as an innovation node that cross-pollinates process advances throughout the cysteine market.

Regulatory Landscape

Regulatory oversight for L-cysteine in food, pharma, and feed is shaped by additive authorizations and by labeling and traceability expectations around animal-derived inputs. In the United States, FDA listings for L-cysteine monohydrochloride in the Food Substances database and its status under 21 CFR provisions, including 21 CFR 184.1272, provide a clear compliance pathway for bakery and processed-food use, supporting continued use as a dough improver and flavor precursor.

In the European Union, recent feed-additive actions expanded formal permissions: Commission Implementing Regulation (EU) 2026/1012 (May 2026) authorized L-cysteine, L-cysteine hydrochloride monohydrate, and L-cysteine hydrochloride for all animal species, based on an EFSA opinion issued in September 2025. Parallel EU measures for cystine include Commission Implementing Regulation (EU) 2026/402 (February 2026) authorizing a specific fermentation-derived L-cystine produced with Escherichia coli DSM 34232, and Commission Implementing Regulation (EU) 2025/272 (February 2025) renewing L-cystine authorization. Together, these updates reinforce a compliance environment that increasingly recognizes defined microbial production systems alongside ingredient identity and safety requirements. Trade classification also shapes cross-border movement, with cysteine and cystine commonly aligned to HS code 29309013 and subject to periodic tariff schedule updates in major importing markets.

Value Chain Analysis

The cysteine value chain starts with agricultural and industrial inputs used as fermentation substrates, notably plant-derived glucose streams, plus nutrients and trace elements, along with utilities, solvents, and process chemicals for pH control and downstream recovery. Production has been shifting from animal-based protein hydrolysis, such as hair and feather keratin extraction, toward microbial fermentation. This move improves traceability and supports vegan and halal procurement requirements across food and pharmaceutical supply chains. Producers then purify to meet end-use specifications, with food-grade material focused on consistent assay and sensory neutrality, while pharmaceutical-grade supply requires tighter impurity profiles and GMP-aligned documentation.

Downstream processing commonly uses crystallization and redox conversion steps. In some routes, L-cysteine is converted to L-cystine for crystallization and then reduced back to L-cysteine for final isolation, which increases equipment and energy intensity for high-purity output. Distribution runs through ingredients distributors and direct supply contracts to large food processors, pharma manufacturers, and personal-care formulators. Supply risk is concentrated where capacity is geographically clustered, particularly in China, where concentrations are noted in Hubei and Zhejiang. This creates chokepoints tied to local logistics, environmental compliance, and feedstock price volatility for corn- and sugar-derived inputs, while integrated producers with in-house fermentation and purification, such as Wacker Chemie using its FERMOPURE platform, are positioned to manage quality, continuity, and sustainability requirements across stages.

Competitive Landscape

The cysteine market features moderate consolidation, with a handful of integrated chemical and nutrition players controlling key patents, strains, and customer relationships. Wacker Chemie extends its FERMOPURE range to specialty derivatives that satisfy ICH Q7 pharmaceutical guidelines, leveraging multi-continent production to guarantee continuity[3]Wacker Chemie, “FERMOPURE Sustainable L-Cysteine,” wacker.com.

Process innovation remains the primary differentiation lever. Evonik pioneers dipeptide solutions that unlock high-density cell culture, securing long-term supply contracts with vaccine developers, healthcare.evonik.com. Smaller firms explore waste-to-value feedstocks to cut operating costs and carbon footprints. Patent filings in palladium-mediated S-arylation and solvent-assisted peptide folding illustrate ongoing chemistry breakthroughs that spawn new niches inside the cysteine market.

Cysteine Industry Leaders

-

Wacker Chemie AG

-

Merck KGaA

-

Ajinomoto Co., Inc.

-

CJ CHEILJEDANG CORP

-

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is additional substitution away from animal-sourced cysteine in applications where provenance documentation, allergen and contaminant control, and vegan positioning shape procurement decisions. EU regulatory actions that broaden and reaffirm feed-additive permissions for L-cysteine forms, including Commission Implementing Regulation (EU) 2026/1012 (May 2026), expand the addressable compliance-permitted use cases for producers that can supply consistent, traceable material. The market also has a visible need for high-purity grades aimed at sensitive pharma and bioprocessing uses, where supplier qualification and consistent downstream purification are decisive differentiators.

On technology, fermentation performance and cost competitiveness continue to be driven by strain and process engineering, with 2026 academic work reporting systematic engineering approaches in Corynebacterium glutamicum (Metabolic Engineering, May 2026) and E. coli (Chinese Journal of Chemical Engineering, June 2026) to address L-cysteine yield constraints related to redox and sulfur metabolism. This technical progression supports a pipeline of higher-titer, lower-waste manufacturing tied to sustainability and wastewater reduction goals already emphasized by established suppliers. Commercial activity also points to product-market expansion beyond traditional food uses, with companies emphasizing cysteine in personal-care and bioprocessing value pools. Ingredient makers that pair fermentation-origin supply with application support, including formulation, stability, and documentation, are positioned to capture demand in these higher-value segments.

Recent Industry Developments

- April 2026: Wacker Chemie AG announced a collaboration with Amyris to develop bio-based functional ingredients for personal care, drawing on fermentation know-how linked to its amino-acid platform. The collaboration strengthens the positioning of fermentation-derived building blocks, including cysteine-related inputs, in premium personal-care formulations where origin and sustainability claims are central.

- March 2026: Ajinomoto CELLiST Korea highlighted the use of AminoSupplement Cys1 and Cys2 in a bioprocessing-focused webcast discussing upstream productivity constraints in cell culture. This highlights cysteine solutions as performance enablers in biomanufacturing workflows and supports demand for stable, application-specific cysteine formats rather than commodity-only grades.

- March 2024: Researchers from Xi'an Jiaotong-Liverpool University and Nanyang Technological University reported a method to produce cysteine-rich peptides at substantially faster rates than traditional approaches. Faster peptide manufacturing improves the feasibility of cysteine-rich sequences in pharmaceutical R&D and can increase pull-through demand for high-purity cysteine inputs used in synthesis and process development.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cysteine market is defined as the global supply and demand for pure L-cysteine sold across end uses such as food, pharmaceuticals, personal care, animal feed, and selected industrial applications, measured consistently across the value chain.

Scope exclusions: Derivative molecules such as N-acetyl-cysteine and cystine are not counted in the market size totals, even if they are discussed for context.

Segmentation Overview

-

By Production Process

- Natural (Fermentation)

- Synthetic (Hydrolysis)

-

By Application

- Flavor Enhancer

- Reducing Agent

- Conditioner

- Production of Human Insulin

- Other Applications (Antioxidant & Anti-aging Agent, etc.)

-

By End-user Industry

- Food

- Pharmaceutical

- Animal Feed

- Other End-User Industries (Marine & Aquaculture, Personal-care & Cosmetics, etc.)

-

By Geography

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Nordic Countries

- Rest of Europe

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East and Africa

-

Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean map of where cysteine is made, traded, and consumed, because the market has clear signals in production and cross-border movement. We referenced public sources such as UN Comtrade trade statistics, USITC and EU TARIC customs guidance for product mapping, FAOSTAT livestock and meat output indicators, and United States Pharmacopeia monographs and FDA reference materials for pharma-related use conditions.

To connect volumes to demand drivers, we reviewed peer-reviewed journals on amino acids and fermentation, association websites for food ingredients and feed, and selected company annual reports and investor decks to understand capacity, utilization direction, and pricing commentary. A paid subscription for shipment level import and export checks and a separate company financials and intelligence database were used only to validate a few key assumptions where public data was thin. The desk sources named above are illustrative only, and many other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what grades are actually moving in the cysteine trade, how contract pricing tends to reset by quarter, and how demand differs between food, pharma, and feed buyers. We spoke with a mix of producers, distributors, formulators, and downstream procurement teams across APAC, EMEA, and the Americas, and then the inputs were used to close gaps in desk findings and to sanity check conversion factors and growth assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 52% |

| Mid tier: 48% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 19% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach where production, trade flows, and end-use pull are reconstructed into an annual volume total for L-cysteine, and then aligned to a consistent market definition. To keep the model practical, we rely on observable inputs like estimated regional production and capacity moves, import and export momentum, typical grades used by end industries, and end market activity indicators such as processed food output, pharma formulation demand signals, and animal feed production trends.

Once the top line volume is built, selective bottom-up checks are run to see whether the total makes sense, including sampled supplier capacity rollups, distributor channel checks, and indicative price bands to ensure volumes and implied values are reasonable. For forecasting, scenario analysis is used because demand can shift with regulation and with raw material and energy cost changes, and then the scenarios are narrowed using what interviewees expect on capacity additions, utilization, and application mix. Where data gaps exist for smaller consuming countries, we extrapolate using trade intensity and end-use indicators, and then adjust after review so the regional split remains realistic.

Data Validation & Update Cycle

Results are validated through triangulation across independent signals, so the modeled totals are compared against trade balance logic, capacity-based supply ceilings, and downstream consumption reasonableness checks. Any large variances trigger a second pass on product mapping, unit conversions, and the assumed share of food versus pharma and feed grades, and then the team recontacts selected experts if the variance cannot be explained.

Before sign-off, the model goes through multi-step analyst review where assumptions are checked for internal consistency and for alignment with recent events such as plant expansions, regulatory actions, or sudden price swings. Reports refresh annually, and interim updates are made when a material event changes the market outlook. Right before delivery, a final review is run so clients receive the most current version available.

Mordor Intelligence's Cysteine Market Size Measured Against Other Published Estimates

Published cysteine market sizes often do not match because different studies measure different things, and the label cysteine gets used loosely across grades, derivatives, and use cases. The year selection can also change the picture, especially when pricing and trade flows move quickly.

A common gap driver is whether the estimate is volume based for pure L-cysteine, or revenue based and expanded to include adjacent molecules, which pushes totals upward. Other differences come from how conversion is handled between assay purity and sellable product, how average selling prices are updated across regions, and whether trade statistics are cleaned for re-exports and double counting. When derivative molecules like N-acetyl-cysteine and cystine are kept outside scope and the sizing stays on pure L-cysteine trade and production signals, the spread versus broader revenue builds becomes easier to explain for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.23 M (2026) | |

| Industry Publisher A | USD 441.10 M (2025) | Reported on a revenue basis with broader coverage that can mix product types and application driven price differences, and the year and currency conversion timing can shift the headline value versus a tonnage-led build. |

| Global Consultancy B | USD 462.13 M (2024) | Uses a value model with its own segmentation of production methods and applications, and it may treat pricing progression and inclusion of non-food uses differently, which can expand the market compared with a pure L-cysteine volume scope. |

The spread across publishers mostly comes from mixing value and volume measures and from how strictly the product definition is enforced. When the model is tied to clear trade and production signals and then checked with realistic grade level demand splits, the result is easier to follow and to repeat for future updates.

Key Questions Answered in the Report

How big is the Cysteine Market?

The Cysteine Market size is valued at 12.23 kilotons in 2026 and and is projected to reach 15.57 kilotons by 2031.

Which region leads the cysteine market?

Asia-Pacific leads with 47.60% market share in 2025 and shows the fastest growth at a 5.82% CAGR through 2031.

Why is bio-fermentation important for cysteine supply?

Bio-fermentation is crucial for cysteine production because it offers a renewable and sustainable alternative to traditional methods like keratin extraction, which have safety and environmental concerns.

Which application segment is expanding the fastest?

Conditioner formulations used in haircare and personal-care products are advancing at a 6.12% CAGR to 2031.

How are raw material prices affecting cysteine producers?

Volatile sugar and corn-steep liquor prices compress fermentation margins, posing a -0.7% drag on forecast CAGR.

Page last updated on: