AdBlue Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

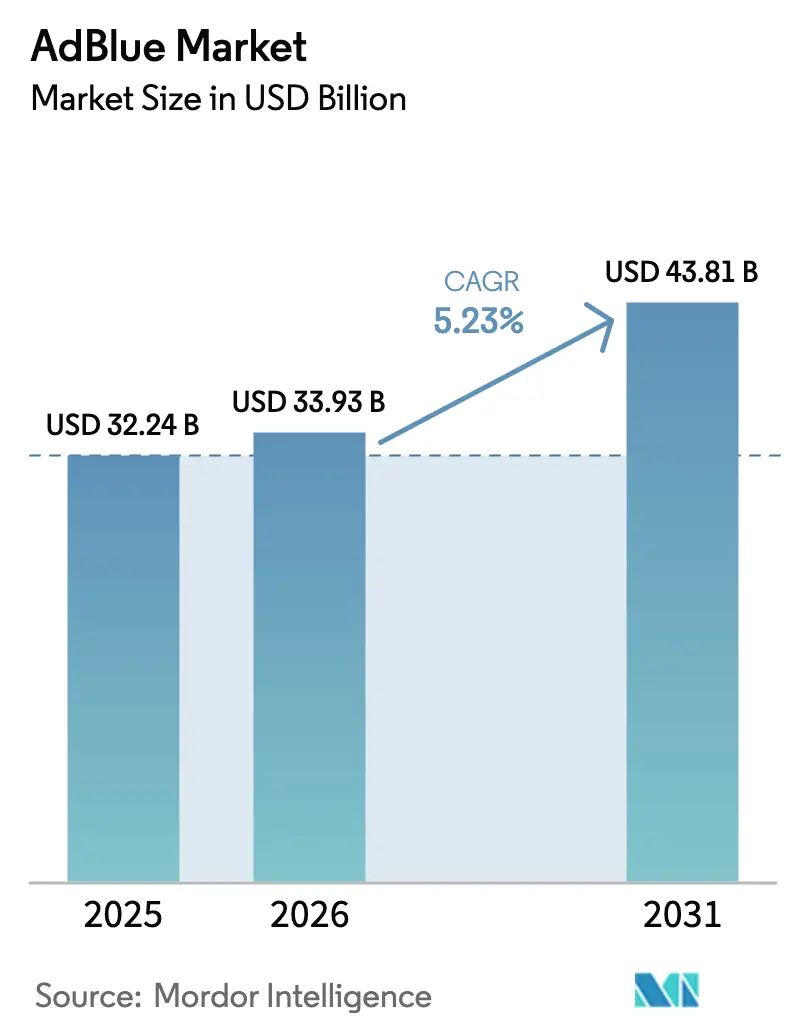

| Market Size (2026) | USD 33.93 Billion |

| Market Size (2031) | USD 43.81 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AdBlue Market Analysis by Mordor Intelligence

The AdBlue market size is expected to grow from USD 32.24 billion in 2025 to USD 33.93 billion in 2026 and is forecast to reach USD 43.81 billion by 2031 at 5.23% CAGR over 2026-2031. Continuing reliance on diesel powertrains in heavy-duty transport anchors near-term demand even as e-truck registrations trend higher, because selective catalytic reduction remains mandatory for the vast diesel fleet on the road. Progressive NOx rules in Europe, China, and India lift fluid consumption per vehicle by requiring tighter ammonia-slip controls and longer durability periods. The rapid roll-out of dispensing infrastructure in emerging markets enhances refill convenience and reduces system derate incidents, thereby supporting uptake among first-time users. Telematics-enabled dosing cuts unnecessary injections by linking urea flow to real-time NOx data, lowering operating cost while safeguarding compliance margins. Volatile urea feedstock prices and the gradual shift to zero-emission vehicles pose headwinds; however, these risks are partly offset by the expanding use in non-road machinery and retrofit programs in regions that tighten local ordinances.

Key Report Takeaways

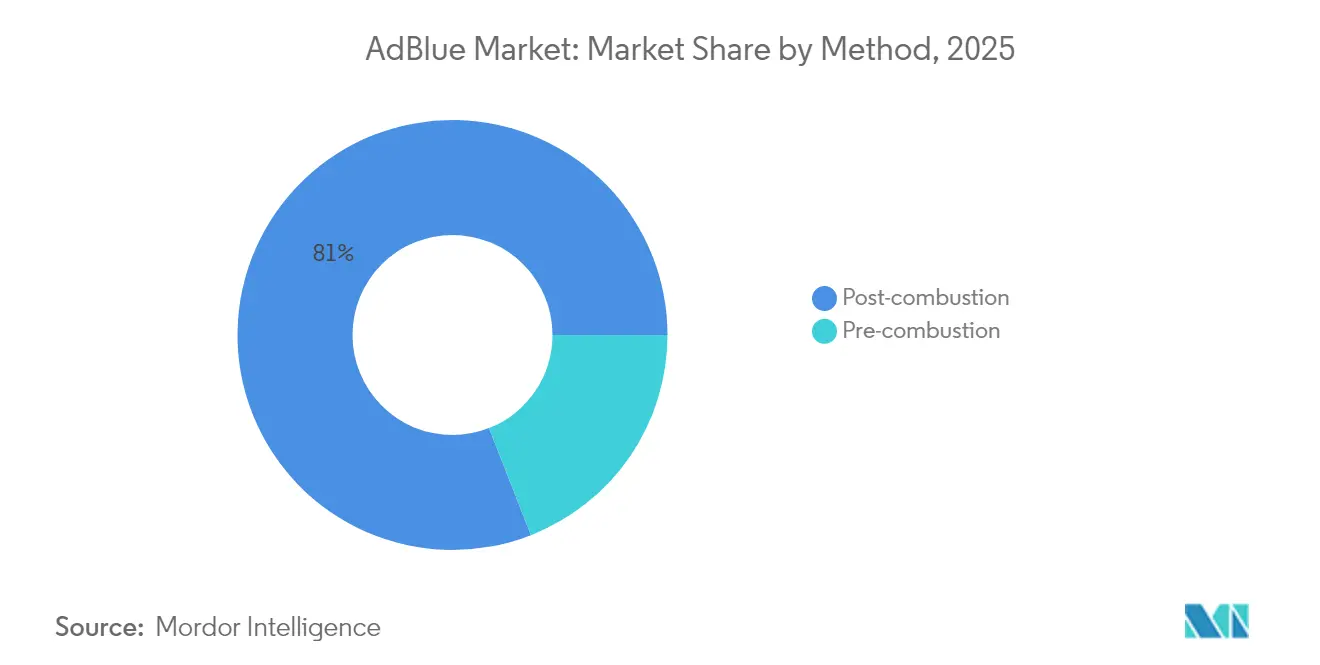

- By method, post-combustion selective catalytic reduction led with an 80.95% AdBlue market share in 2025, while pre-combustion dosing is forecast to expand at a 5.58% CAGR through 2031.

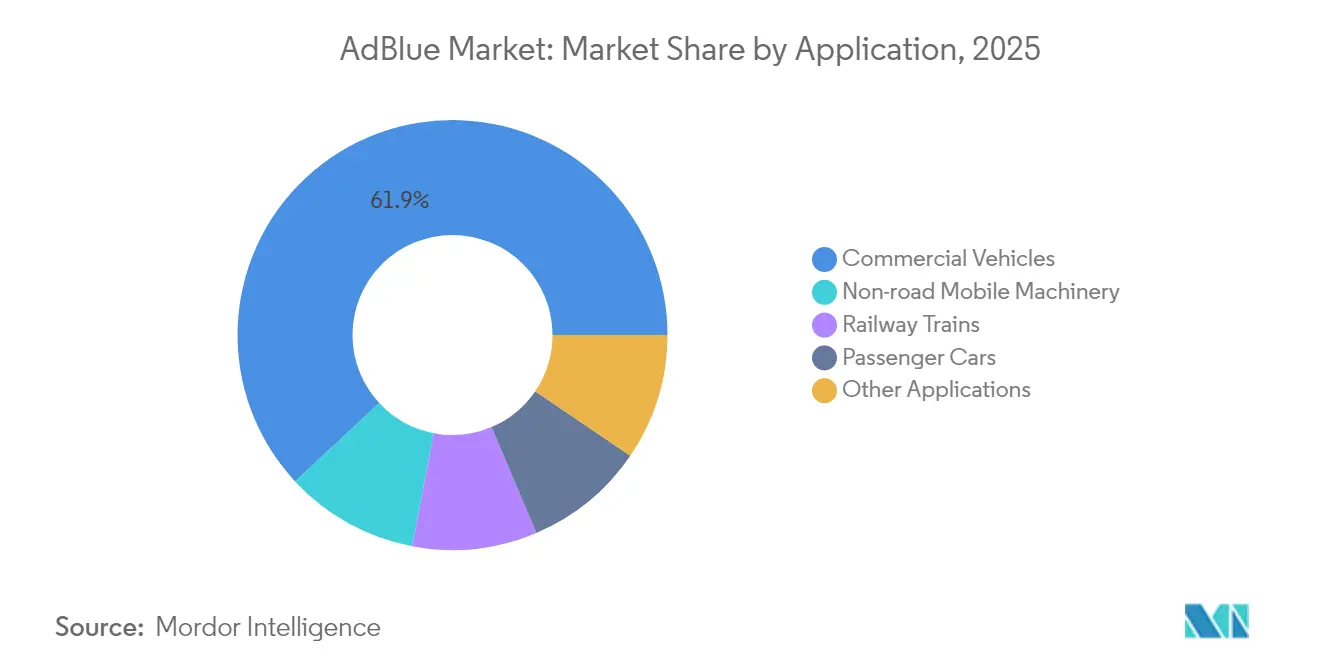

- By application, commercial vehicles accounted for 61.92% of the AdBlue market size in 2025, and non-road mobile machinery is projected to advance at a 5.96% CAGR through 2031.

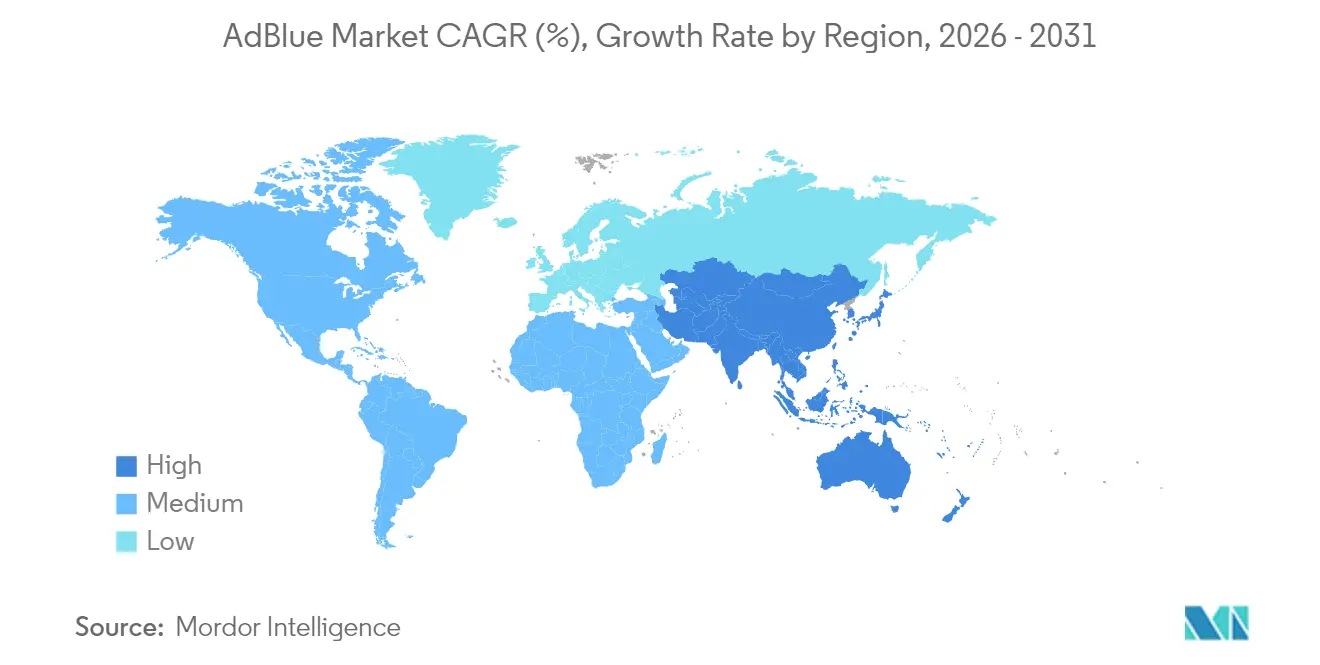

- By geography, Europe captured 38.12% of the AdBlue market share in 2025, whereas Asia-Pacific is projected to grow fastest at a 6.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global AdBlue Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global NOx-Emission Regulations | +1.8% | EU, China, India | Medium term (2-4 years) |

| Rapid SCR Uptake Across Non-Road Machinery | +1.2% | EU, North America, China | Medium term (2-4 years) |

| Expansion of AdBlue Retail Infrastructure in Emerging Markets | +0.9% | APAC, Middle East, Africa | Long term (≥4 years) |

| Surge in E-Commerce Logistics Diesel Mileage | +0.7% | North America, EU, China | Short term (≤2 years) |

| Telematics-Driven Dosing and Fleet Analytics | +0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Global NOx-Emission Regulations

Euro 7 limits effective from 2026 for light-duty vehicles and 2028 for heavy-duty trucks tighten real-driving NOx caps to 60 mg/km and introduce ammonia-slip ceilings, obligating manufacturers to integrate NH3 sensors and larger urea tanks[1]European Commission, “Proposal for Euro 7 Standards,” europa.eu. China’s National VI rule mandates on-board monitoring that uploads SCR data to provincial servers, discouraging underdosing to save fluid. India’s BS-VI Phase 2 introduces real-driving-emissions tests, which accelerate the roll-out of highway dispensers by state fuel retailers. The United States finalizes EPA 2027 requirements, demanding a 90% NOx cut by 2031, which pushes engine makers toward dual-dosing architectures. ASEAN economies trail, but Vietnam’s Euro 5 adoption signals regional tightening that widens the addressable AdBlue market.

Rapid SCR Uptake Across Non-Road Machinery

EU Stage V rules require SCR-plus-DPF systems on engines exceeding 56 kW, including excavators, wheel loaders, and tractors, where refill intervals remain a significant operational challenge. North America’s Tier 4 Final drives are similar to those in agricultural and construction fleets, with telematics alerts preventing mid-shift derates. Mining haul trucks in Canada and Chile validate low-temperature formulations to prevent crystallization at high altitudes. China’s move to National IV in non-road engines spurs Sinopec to market a dedicated low-biuret grade for urban equipment. These developments collectively lift AdBlue intensity per machine and diversify demand beyond on-road vehicles.

Expansion of AdBlue Retail Infrastructure in Emerging Markets

Indian Oil, Bharat Petroleum, and Hindustan Petroleum plan to install 500 new dispensers by 2026, targeting Tier 2 and Tier 3 corridors where BS-VI fleets operate. Petronas and PTT expand coverage along pan-ASEAN routes, although Indonesia and Vietnam still rely on more costly drum supply. In the Middle East, Saudi Aramco and ADNOC are rolling out highway dispensers to support Euro 5-compliant imports, aiming to reach 200 sites by 2026. South Africa’s network primarily grows around Gauteng and the Western Cape, yet rural gaps persist, limiting the uptake of Euro 5 trucks. Better availability helps trim system derates and supports the AdBlue market in first-time adopter regions.

Surge in E-Commerce Logistics Diesel Mileage

Last-mile delivery pushes diesel vans and light trucks to higher annual mileage, sustaining demand for fluid despite the parallel electrification of dense urban routes. China’s express-delivery sector used approximately 12 million tonnes of diesel in 2024, translating to roughly 0.5–0.6 million tonnes of AdBlue at 4–5% dosing rates. European parcel carriers report an 8–10% yearly growth in mileage, offsetting per-vehicle efficiency gains. North American LTL fleets shift toward larger Class 8 trucks, which consume more AdBlue per ton-mile. The logistics boom, therefore, underpins steady baseline demand through the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Light-Duty EV Penetration | -1.1% | EU, China, North America | Medium term (2-4 years) |

| Volatile Urea Feedstock Prices | -0.6% | Global | Short term (≤2 years) |

| Counterfeit / Contaminated AdBlue Risk | -0.4% | APAC, Middle East, Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Light-Duty EV Penetration

Battery-electric trucks achieved total cost parity with diesel in several urban duty cycles by 2024, accelerating electrification in delivery and regional haul segments[2]Nature Energy, “Total Cost Parity for Electric Trucks,” nature.com. California’s Advanced Clean Trucks rule demands up to 75% zero-emission Class 7–8 sales by 2035, shrinking diesel’s addressable base in the state that holds 12% of U.S. heavy-duty registrations. China mandates 100% electric buses and taxis in key cities, eroding demand for AdBlue in the 3.5–7.5 t bracket. Europe’s CO2 standards push OEMs toward battery and fuel-cell options for urban distribution vehicles. Although long-haul diesel remains prevalent, these urban shifts modestly alter the trajectory of the AdBlue market.

Volatile Urea Feedstock Prices

Urea trades about 45% above pre-2022 averages due to gas supply fragility, export quotas, and geopolitical tensions. Regional divergence is pronounced, with the Middle East FOB up 30.3% in 2025, while China FOB fell 12.6%, complicating procurement for global distributors. Producers under long-term fleet contracts often struggle to pass through cost spikes, which squeezes their margins and deters new entrants. Integrated fertilizer majors absorb volatility better, consolidating supply in the AdBlue market. Persistent feedstock swings therefore shave growth momentum, especially for independent blenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: Post-Combustion Dominance Anchors Baseline Demand

Post-combustion method captured 80.95% of the AdBlue market share in 2025, reflecting near-universal use in on-road diesel engines where urea is injected into the exhaust stream to convert NOx. This layout is embedded in Euro 7, EPA 2027, and China National VI, making it the industry baseline well past 2030. Pre-combustion dosing is forecast to grow at a rate of 5.58% as specialized sectors, such as marine diesel and stationary generators, pursue fuel efficiency gains. Railway locomotives and hybrid EGR-SCR setups in mining equipment strike a balance between durability and fluid consumption, ensuring ongoing relevance after combustion. Passenger cars carry 10–20 l tanks aligned with oil-change intervals, while commercial vehicles use 40–80 l tanks monitored by telematics that warn operators before derate thresholds activate.

Pre-combustion approaches inject ammonia directly into the cylinder, lowering peak combustion temperature and cutting NOx at the source. Technical hurdles include higher thermal stress and the risk of NH3 slip, yet 2–3% fuel-efficiency gains appeal to marine and fixed-plant operators. IMO Tier III stimulates trials on coastal vessels that cannot accommodate bulky SCR reactors. China’s industrial zones cap stack NOx at 50 mg/Nm³, prompting power plants to test pre-combustion dosing that circumvents retrofit space constraints. Even so, the AdBlue market remains anchored by post-combustion SCR, which offers proven compliance across the broadest range of mobile engines.

By Application: Commercial Vehicles Lead, Non-Road Machinery Accelerates

Commercial vehicles accounted for 61.92% of the AdBlue market size in 2025, underpinned by the heavy-duty truck fleet that consumed 16.8 million barrels per day of oil in 2023 at dosing ratios of 4–5%. Long-haul tractors, regional haul rigs, and intercity buses rely on fluid availability along highway corridors, prompting retailers to integrate dispensers at service stations in Europe and North America. Delivery vans sustain demand in last-mile logistics despite partial electrification, because suburban and rural routes still favor diesel. Engine makers introduce predictive dosing, which reduces consumption without compromising compliance, marginally moderating per-vehicle fluid growth while improving fleet economics.

Non-road mobile machinery is advancing at a 5.96% CAGR, lifted by EU Stage V and EPA Tier 4 Final requirements on equipment above 56 kW. Construction, mining, and agricultural segments integrate 20–50 l tanks, supplemented by telemetry that guides operators on refill timing. China transitions to National IV in non-road engines, creating the world’s largest incremental pool for AdBlue suppliers. Passenger-car demand softens in Europe, where diesel registrations fade, yet remains stable in India and parts of ASEAN, where fuel economics favor diesel. Rail and marine applications add a smaller but steady contribution, supported by long equipment life and retrofit mandates.

Geography Analysis

Europe commanded a 38.12% market share of the AdBlue market in 2025, largely due to the implementation of the Euro 7 rules and a vast long-haul truck fleet. Germany, France, and the United Kingdom maintain high per-vehicle dosing due to strict ammonia-slip limits and extended durability testing. Nordic fleets test cold-weather dual-dosing to secure compliance at sub-20 °C, illustrating regional engineering adaptations. Spain and Italy face gaps in rural dispensers that TotalEnergies and Shell aim to close along the Mediterranean freight corridors. Post-Brexit divergence obliges fleets to navigate separate EU and UK rules; however, both regimes maintain SCR obligations, preserving a baseline of fluid demand.

The Asia-Pacific region is the fastest-growing, with a 6.05% CAGR to 2031, driven by China’s OBM enforcement and India’s BS-VI Phase 2 RDE testing. Sinopec’s nationwide network of 30,000 stations alleviates refill anxiety and fosters domestic brand loyalty. Indian Oil and peers expand infrastructure along the Golden Quadrilateral, yet rural gaps encourage fleet stockpiling. Japan’s mature market stabilizes as diesel share in passenger cars shrinks, while South Korea posts modest growth tied to trucking and construction. ASEAN’s fragmented standards delay uniform uptake, but Vietnam and Malaysia show early momentum as Euro 5 rules take hold.

North America held a mid-teens share in 2024. EPA 2027 pushes engine builders toward higher-efficiency SCR, sustaining fluid use per vehicle. California’s zero-emission sales mandates tighten long-term diesel prospects, yet the multi-year phase-in keeps the existing fleet reliant on AdBlue. Canada’s demand concentrates along the Trans-Canada Highway, with Petro-Canada and Shell hosting the largest dispenser networks. Mexico’s cross-border operators adopt SCR to meet U.S. entry rules, prompting Pemex to bolster supply in northern states. Brazil leads South America after PROCONVE P8 enforcement, yet vast interior regions remain underserved. Saudi Arabia and the UAE invest in highway networks that underpin early Euro 5 truck adoption, while South Africa’s mining logistics maintain demand around Gauteng and the Western Cape.

Competitive Landscape

The AdBlue Market is fragmented. Integrated fertilizer majors BASF, Yara, and CF Industries combine captive urea production with broad distribution, enabling them to better absorb feedstock volatility than independent blenders. Sinopec dominates China with projected consumption exceeding 25 million tons in 2025 under National VI truck subsidies. TotalEnergies and Shell lead the European retail sector, embedding fluid dispensers at service stations and introducing RFID-enabled traceability to mitigate the risk of counterfeit products. Cummins and Bosch differentiate themselves through predictive dosing, which reduces consumption by up to 5%, appealing to cost-sensitive fleets.

AdBlue Industry Leaders

Shell plc

BASF

Yara

CF Industries Holdings, Inc.

GreenChem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mitsui Chemicals, Inc. and Sankyu Inc. announced that Sankyu has adopted Bio AdBlue, manufactured and sold by Mitsui Chemicals, made from bio-based urea using the mass balance method, in a number of its chemical tanker trucks.

- April 2024: OCI Global commenced production of AdBlue at the Chemelot industrial complex in Geleen, Netherlands. OCI’s facility has the capacity to produce up to 300,000 tonnes of AdBlue per year, with the capability to expand production in line with market demand.

Global AdBlue Market Report Scope

AdBlue, commonly known as diesel exhaust fluid, is a type of liquid used to minimize pollutants produced by diesel engines. It is made up of 32.5% urea and 67.5% deionized water and is used in selective catalytic reduction (SCR), which reduces the concentration of nitrogen oxides in engine exhaust emissions. The AdBlue market is segmented by application and geography. By application, the market is segmented into commercial vehicles, passenger cars, railway trains, non-road mobile machinery, and other applications. The report also covers market sizes and forecasts in 19 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Pre-combustion |

| Post-combustion |

| Commercial Vehicles |

| Passenger Cars |

| Railway Trains |

| Non-road Mobile Machinery |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Method | Pre-combustion | |

| Post-combustion | ||

| By Application | Commercial Vehicles | |

| Passenger Cars | ||

| Railway Trains | ||

| Non-road Mobile Machinery | ||

| Other Applications | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the AdBlue market in 2026?

The AdBlue market size stands at USD 33.93 billion in 2026.

What growth rate is expected for AdBlue between 2026 and 2031?

The market is forecast to grow at a 5.23% CAGR, reaching USD 43.81 billion by 2031.

Which region leads AdBlue consumption today?

Europe leads with 38.12% share thanks to stringent Euro emission rules.

Where is the fastest growth expected?

Asia-Pacific is projected to expand at a 6.05% CAGR through 2031 as China and India tighten NOx standards.

Which application segment dominates AdBlue demand?

Commercial vehicles contribute 61.92% of global demand, driven by long-haul trucks and buses.

Page last updated on: