Lanolin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

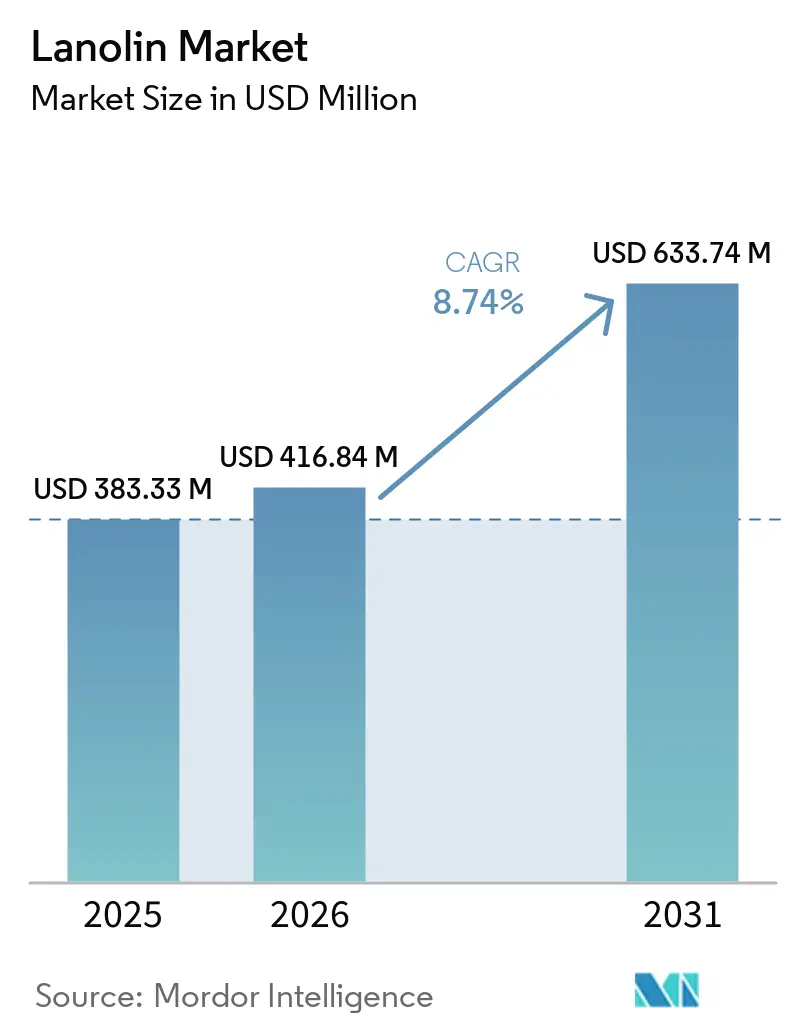

| Market Size (2026) | USD 416.84 Million |

| Market Size (2031) | USD 633.74 Million |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lanolin Market Analysis by Mordor Intelligence

The Lanolin Market size is expected to grow from USD 383.33 million in 2025 to USD 416.84 million in 2026 and is forecast to reach USD 633.74 million by 2031 at 8.74% CAGR over 2026-2031. The expansion reflects a pivot toward highly purified anhydrous (HPA) grades that balance natural-origin claims with allergen-control, even as plant-based emollients encroach on vegan segments. Lanolin’s unique ability to absorb up to 400% of its weight in water and reduce transepidermal water loss by 20-30% underpins its resilience in leave-on cosmetics and topical pharmaceuticals. Regulatory standing further supports demand; the ingredient retains active-drug status in the US FDA OTC skin-protectant monograph M016, giving it a compliance edge over many plant alternatives. Meanwhile, global wool-grease supply tightens as Australian shorn-wool output drops 12.6% in 2025/26, encouraging processors to lock in long-term offtake and invest in ultra-refinement to secure premium margins. Quality-oriented suppliers able to deliver pesticide totals below 40 ppm and lead under 10 ppm are now capturing the highest price points, whereas commodity producers face substitution by synthetic esters and shea-butter unsaponifiables.

Key Report Takeaways

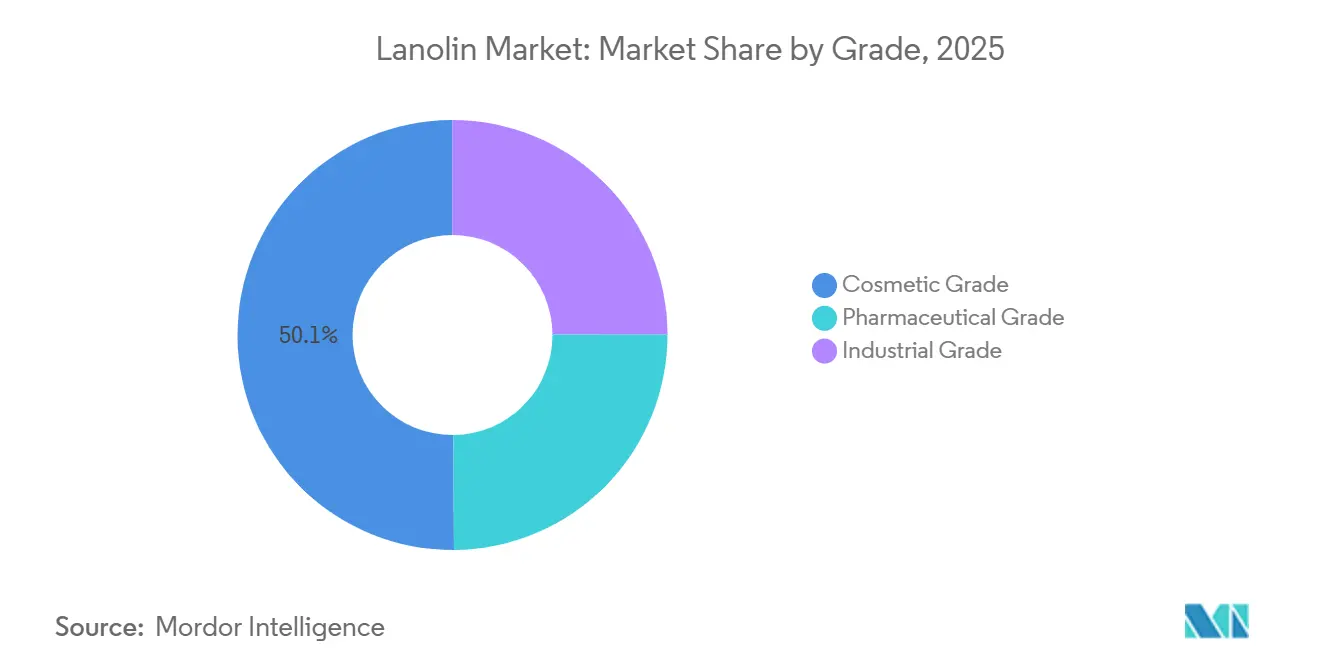

- By grade, cosmetic grade captured 50.12% of the Lanolin market share in 2025, while the pharmaceutical grade is advancing at a 6.34% CAGR through 2031.

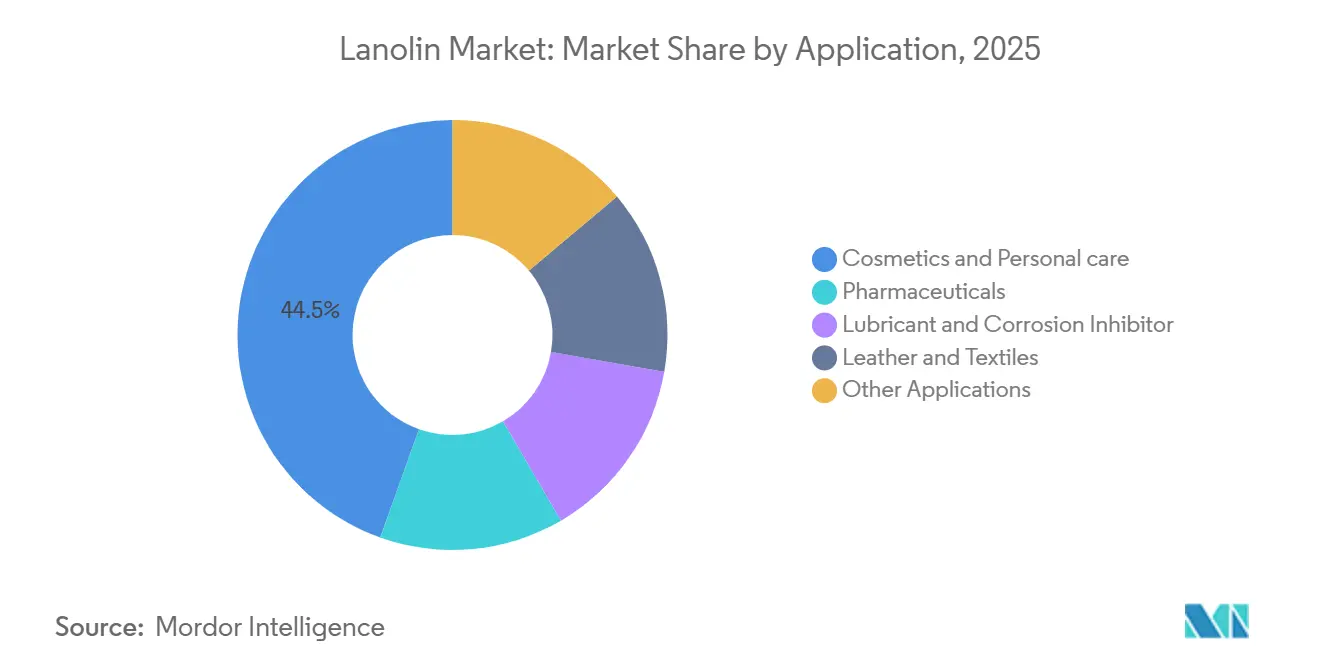

- By application, cosmetics and personal care accounted for 44.54% of the Lanolin market size in 2025; pharmaceuticals are projected to expand at a 6.62% CAGR to 2031.

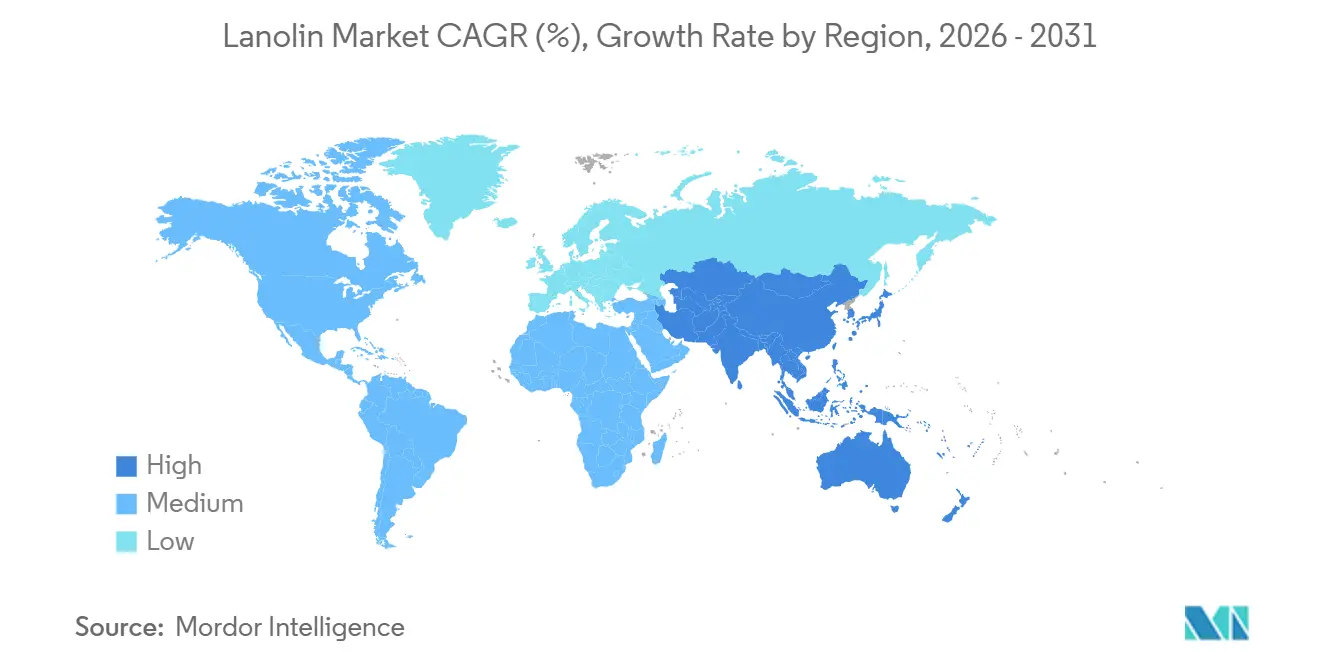

- By geography, Asia-Pacific held 36.22% revenue share in 2025 and is set to grow at a 6.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lanolin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural ingredients in cosmetics and personal care | +2.1% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing use in topical pharmaceuticals and medicated baby-care | +1.8% | North America, Europe, and Japan (regulatory-mature markets) | Long term (≥ 4 years) |

| Expansion of clean-label baby-care products | +1.5% | North America, Western Europe, and Australia/New Zealand | Medium term (2-4 years) |

| Advances in ultra-pure/low-allergen lanolin refining technologies | +1.3% | Global, led by suppliers in Europe and North America | Long term (≥ 4 years) |

| Niche uptake of lanolin-based biodegradable anti-corrosion coatings | +0.9% | Industrial clusters in Asia-Pacific, Middle East oil & gas, and North American automotive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Ingredients in Cosmetics and Personal Care

Consumers now scrutinize INCI decks and reward brands that showcase recognizable, animal-welfare-vetted inputs. Lanolin retains favor in premium lipsticks and balms because its sterol-rich matrix forms stable water-in-oil films that plant alternatives cannot fully match[1]Deanna Utroske, “Why Lanolin Persists in Premium Lipsticks,” cosmeticsandtoiletries.com. Formulators therefore split portfolios: mass-market SKUs adopt bis-diglyceryl polyacyladipate-2 or glyceryl rosinate blends, while luxury lines double down on HPA lanolin that contains less than or equal to 1.5% free lanolin alcohol, cutting hypersensitivity risk by about 96%. Concentration-of-use data confirm persistence at the high end; maximum lanolin levels in lipsticks remain 47%, unchanged since the prior Cosmetic Ingredient Review survey.

Growing Use in Topical Pharmaceuticals and Medicated Baby-Care

Lanolin’s inclusion in hospital formularies owes to a 2024 meta-analysis showing superior efficacy against nipple trauma versus routine care[2]David J. Lewis, “Lanolin Purification Cuts Hypersensitivity 96%,” ncbi.nlm.nih.gov. Active-ingredient status within the FDA (Food and Drug Administration) monograph M016 permits barrier-repair claims without a full New Drug Application, lowering regulatory hurdles for OTC (Over-the-Counter) ointments. Suppliers meet stringent specs, pesticides below detection, and alcohols less than or equal to 1.5%, via multi-residue HPLC-CAD protocols validated in 2025.

Expansion of Clean-Label Baby-Care Products

Parents expect minimal-processing and traceable sourcing. HPA lanolin, marketed as “no detectable pesticides,” now commands 20-30% price premiums in diaper-rash creams and nipple balms. Mixed clinical evidence on prophylactic use means brands target therapeutic relief, often pairing lanolin with mild antimicrobials. EU Regulation 2026/78 enforces impurity audits from May 2026, reinforcing demand for analytically certified lots.

Advances in Ultra-Pure/Low-Allergen Lanolin Refining Technologies

Analytical quality-by-design (AQbD) methods such as HPLC-QAMS (High-Performance Liquid Chromatography - Quantitative Analysis of Multi-Components by Single) quantify cholesterol, lanosterol, and 24,25-dihydrolanosterol with a single standard, slashing QC costs by up to 35%. Fractionation breakthroughs that isolate α-hydroxy fatty acids also unlock biofuel and polymer feedstock value, critical as wool supply contracts 12.6% year-on-year in Australia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of plant-based and synthetic emollient substitutes | -1.7% | Global, with highest substitution in North America and Western Europe vegan segments | Medium term (2-4 years) |

| Contact-allergy concerns and tightening cosmetic-safety regulations | -1.2% | Europe, North America, and regulatory-mature Asia-Pacific markets (Japan, South Korea) | Long term (≥ 4 years) |

| Raw-wool price volatility and supply-chain concentration | -0.8% | Global, with acute impact in Australia, New Zealand, and China processing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Plant-Based and Synthetic Emollient Substitutes

Shea unsaponifiables, glyceryl rosinate, and BDPA (1,3-bis(diphenylene)-2-phenylallyl) esters mimic lanolin’s gloss and adhesion at a lower cost while satisfying vegan claims. Comparative tests show parity on immediate feel but shorter moisturization longevity, leading premium brands to retain lanolin for performance-critical formats.

Contact-Allergy Concerns and Tightening Safety Regulations

Lanolin became the American Contact Dermatitis Society’s 2023 “Allergen of the Year,” pushing formulators toward highly purified anhydrous (HPA) grades. EU (European Union) Regulation 2026/78 now requires arsenic below 3 ppm (parts per million), mercury under 1 ppm, and total pesticides below 40 ppm, a compliance burden that smaller grease processors struggle to meet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharmaceutical Purity Commands Premium as HPA Specifications Tighten

Cosmetic grade, held 50.12% of the Lanolin market share in 2025, sees a gradual volume loss to vegan substitutes in mass cosmetics, yet preserves relevance in lipsticks, where concentration peaks at 47%. Pharmaceutical-grade lanolin is projected to expand faster than the overall lanolin market, growing at 6.34% CAGR to 2031 on the back of OTC skin-protectant demand and nipple-care protocols that insist on less than or equal to 1.5% lanolin alcohol. Industrial grade remains niche, but biodegradable anti-corrosion coatings using lanolin esters and cerium(III) nitrate achieve 26-fold higher charge-transfer resistance than neat lanolin, opening opportunities in automotive pipelines.

Quality variability is stark; cholesterol ranged 3.67-24.8% across ten industrial batches analyzed by HPLC-QAMS in 2024, pushing buyers to favor vertically integrated suppliers offering tight sterol specs. As a result, the lanolin market size for high-purity lines rises even amid flat overall tonnage.

By Application: Pharmaceuticals Outpace Cosmetics as Clinical Evidence Builds

Cosmetics and personal care still account for 44.54% of the Lanolin market size, owing to irreplaceable performance in lip and nail products. Yet pharmaceutical applications are expected to deliver the fastest gains at a 6.62% CAGR through 2031, driven by topical formulations and medicated baby-care products where clinical evidence and regulatory acceptance create moats against substitution. This growth is also because the FDA monograph pathways lower regulatory barriers. Lanolin-based OTC treatments leverage the ingredient’s 20-30% transepidermal water-loss reduction, validated in multiple 2024 trials. Industrial corrosion-inhibitor use remains niche but lucrative, supported by stricter VOC limits in oil & gas equipment coatings.

Geography Analysis

Asia-Pacific held 36.22% market share in 2025 and is forecast to expand at 6.87% CAGR through 2031, driven by China's dual role as a major wool-processing hub and a fast-growing consumer of natural cosmetic ingredients. China's retail cosmetics sales growth reflects urbanization, rising disposable incomes, and consumer preference for natural-origin ingredients in skincare and baby-care products. Japan and South Korea adopt EU-style impurity thresholds, supporting pharmaceutical-grade uptake. India grows from a low base but remains price-sensitive; substitution with plant esters is common in mid-tier creams.

North America blends mature pharma demand with polarized cosmetic attitudes. US premium skin-protection brands champion HPA lanolin, whereas mass retailers pivot toward BDPA and shea blends for vegan certification. Canada’s regulatory regime echoes the EU, reinforcing ultra-pure adoption. Mexico offers volume upside but is still dominated by cosmetic-grade imports.

Europe enforces the strictest impurity caps under Regulation 2026/78, driving vertical integration among processors able to certify pesticide totals less than 40 ppm. Germany and France dominate therapeutic lanolin demand, while Nordic countries prize clean-label baby-care balms. The United Kingdom retains strong cosmetic-lab skin-barrier research, supporting continued use in premium color lines.

Competitive Landscape

The Lanolin Market is moderately consolidated. Major players invest heavily in multi-residue analytics, allowing them to guarantee less than or equal to 10 ppm lead and undetectable organophosphates. Market entrants offering vegan substitutes pose a limited threat in high-regulation niches but win share in mainstream color cosmetics where cost and ethics trump performance.

Lanolin Industry Leaders

Nippon Fine Chemical

Croda International PLC

Zhejiang Garden Biochemical High-Tech Co. Ltd

NK Chemicals Pte Ltd

Lubrizol

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Effective May 1, 2026, the European Commission rolled out Regulation (EU) 2026/78. This new regulation introduced standardized classifications for substances deemed carcinogenic, mutagenic, or reprotoxic. Therefore, lanolin suppliers are now required to ensure their batches adhere to stringent limits.

- October 2025: Clae Skin launched Super Lanolin, a single-ingredient lip treatment. It was made from 100% pharmaceutical-grade, pesticide-free lanolin, ethically sourced from Merino sheep in New Zealand.

Global Lanolin Market Report Scope

Lanolin is a fatty substance found in sheep's wool. It is extracted as a yellowish viscous mixture of esters and used as a base for ointments and cosmetics.

The Lanolin market is segmented by grade, application, and geography. By grade, the market is segmented into cosmetic grade, pharmaceutical grade, and industrial grade. By application, the market is segmented into cosmetics and personal care, pharmaceuticals, lubricant and corrosion inhibitor, leather and textiles, and other applications. The report also covers the market size and forecast for the lanolin market in 16 countries across major regions. Each segment's market sizing and forecast are based on revenue (USD million).

| Cosmetic Grade |

| Pharmaceutical Grade |

| Industrial Grade |

| Cosmetics and Personal care |

| Pharmaceuticals |

| Lubricant and Corrosion Inhibitor |

| Leather and Textiles |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Cosmetic Grade | |

| Pharmaceutical Grade | ||

| Industrial Grade | ||

| By Application | Cosmetics and Personal care | |

| Pharmaceuticals | ||

| Lubricant and Corrosion Inhibitor | ||

| Leather and Textiles | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the lanolin market be by 2031?

The Lanolin market size is forecast to reach USD 633.74 million by 2031, expanding at an 8.74% CAGR from 2026.

Which lanolin grade is growing fastest?

Pharmaceutical-grade lanolin is projected to post a 6.34% CAGR through 2031, outpacing cosmetic and industrial grades.

Why are HPA specifications important?

Highly purified anhydrous lanolin with less than or equal to 1.5% free alcohol dramatically lowers allergy incidence and complies with EU impurity caps effective 2026.

Which region holds the largest demand?

Asia-Pacific leads with 36.22% share in 2025 and the strongest 6.87% CAGR outlook through 2031.

Page last updated on: