Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.09 Billion |

| Market Size (2031) | USD 37.03 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

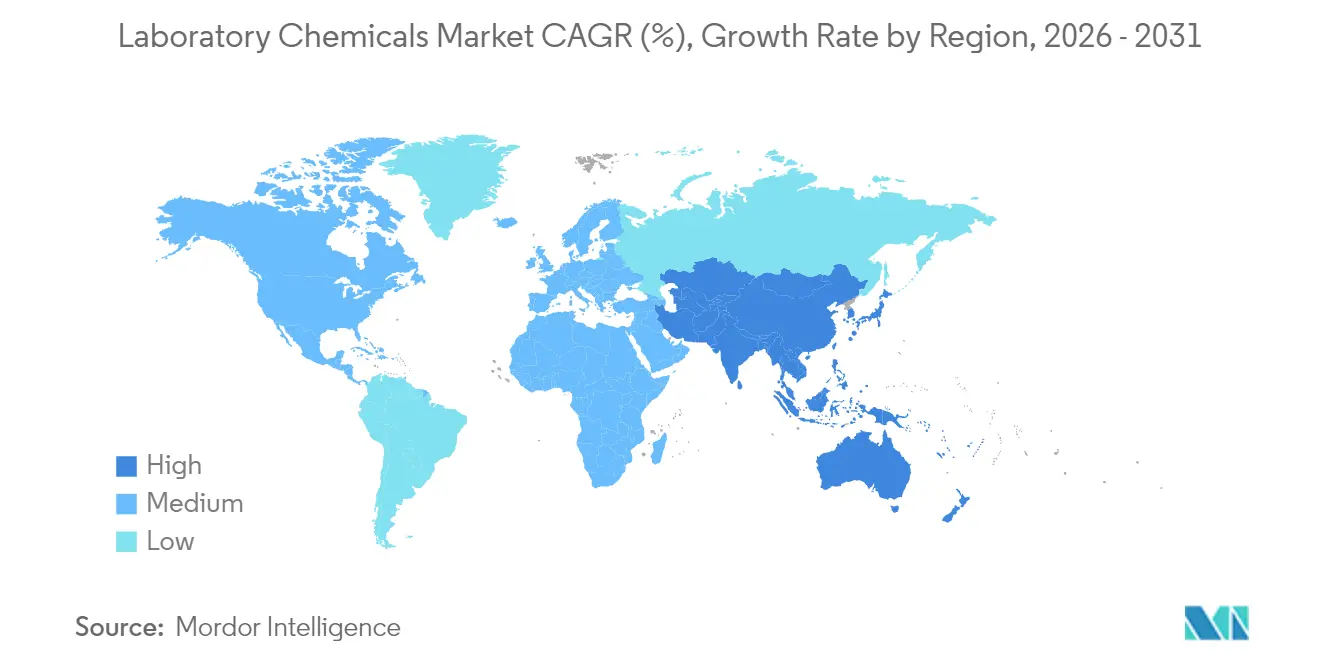

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

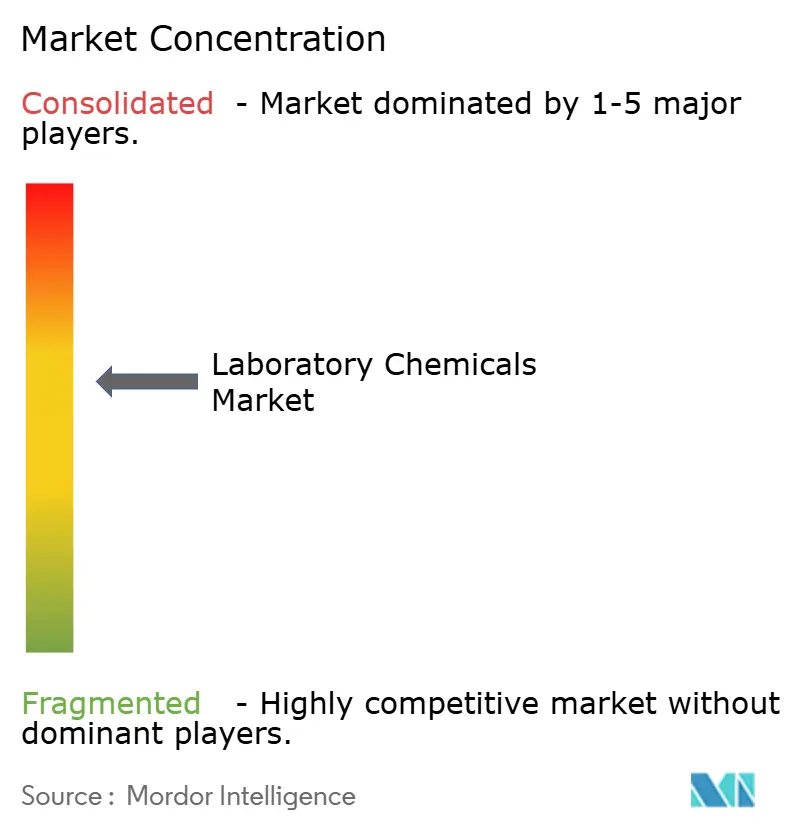

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Chemicals Market Analysis by Mordor Intelligence

The Laboratory Chemicals Market size in 2026 is estimated at USD 30.09 billion, growing from 2025 value of USD 28.87 billion with 2031 projections showing USD 37.03 billion, growing at 4.24% CAGR over 2026-2031. Sustained investment in life-science research, tighter analytical standards, and the gradual switch to greener chemistries form the bedrock of this steady trajectory. Pharmaceutical developers, now channeling more than USD 200 billion each year into R&D, remain the largest single demand node for high-purity reagents. Laboratories are also re-engineering workflows around automation, which raises consumption of pre-formatted liquid standards that cut handling steps. Parallel environmental regulations are pushing end users toward certified reference materials and bio-based solvents that meet emerging sustainability scorecards.

Key Report Takeaways

- By type, biochemistry led with 27.12% of laboratory chemicals market share in 2025 while healthcare/pharmaceutical reagents recorded the fastest 4.93% CAGR through 2031.

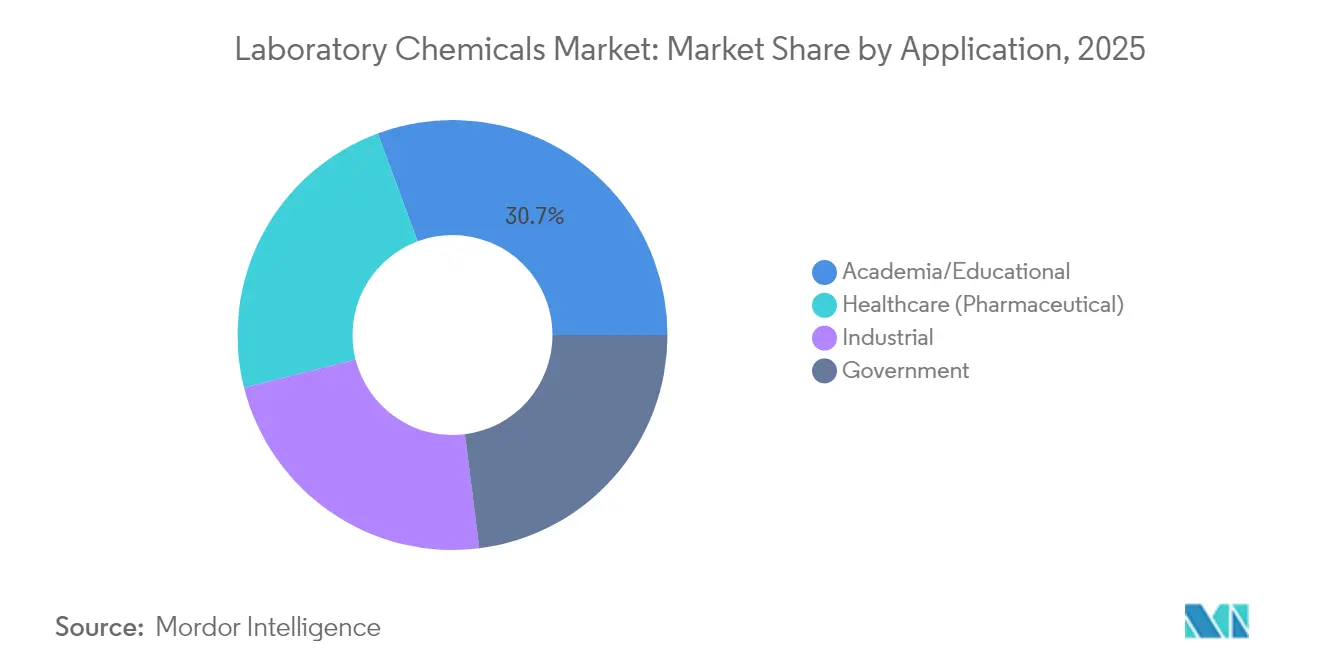

- By application, academia/educational institutions accounted for 30.66% of the laboratory chemicals market size in 2025, whereas cell/tissue culture reagents are on track for a 4.58% CAGR between 2026 and 2031.

- By geography, North America commanded 29.60% revenue in 2025; Asia-Pacific is projected to grow the quickest at a 4.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laboratory Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing RandD Spending in Life-Science and Pharma Sectors | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expanding Biopharmaceutical Manufacturing Capacity Worldwide | +0.9% | Global, led by Asia-Pacific and North America | Long term (≥ 4 years) |

| Rising Demand for High-Purity Reagents In Environmental and Food Testing | +0.7% | Global, with regulatory emphasis in EU and North America | Short term (≤ 2 years) |

| Digitization and AI-Enabled High-Throughput Lab-Of-The-Future Initiatives | +0.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Shift Toward Sustainable/Green Solvents and Bio-Based Reagents | +0.6% | EU-led, expanding to North America and developed APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing R&D Spending in Life-Science and Pharma Sectors

Major drugmakers allocated 15-20% of 2024 revenue to discovery programs, sustaining demand for chromatographic solvents, enzyme substrates, and isotope-labeled standards that underpin precision biology. Universities remain active buyers by leveraging industry alliances and foundation grants that shield research pipelines from public-funding volatility. The expansion of self-driving laboratories, built on robotic liquid handlers and AI-guided experiment design, tilts reagent consumption toward ready-to-use liquid stocks carrying bar-coded metadata. Suppliers able to deliver automation-compatible packaging and digital documentation are seeing elevated order volumes. The trend establishes a flywheel: richer data feeds better algorithms, which in turn heightens throughput and reagent requirements.

Expanding Biopharmaceutical Manufacturing Capacity Worldwide

A greater than 20% jump in global biologics capacity during 2024 opened a sizeable tailwind for process buffers, chromatography resins, and release-testing standards used in GMP environments. Contract development and manufacturing organizations rely on platform processes that multiply reagent needs across clients, cementing a predictable offtake profile. Asia-Pacific captures the lion’s share of new bricks-and-mortar investment as competitive cost structures attract multinationals and biosimilar firms alike. Continuous-manufacturing paradigms rooted in quality-by-design frameworks intensify demand for real-time analytical reagents that ensure batch integrity[1]U.S. Food & Drug Administration, “Process Analytical Technology Guidance,” fda.gov . Suppliers offering validated PAT chemistries are securing multi-year agreements tied to long-term commercial supply.

Rising Demand for High-Purity Reagents in Environmental and Food Testing

Updated U.S. EPA methods for PFAS monitoring now require ultra-trace detection limits that only premium-grade solvents and isotope-labeled standards can meet. EU drinking-water directives add further harmonization, creating a de facto global baseline that lifts purity specifications worldwide. Food-safety laboratories must support rapid screening of pesticides and mycotoxins, fueling uptake of certified multianalyte kits. Accreditation bodies under ISO/IEC 17025 mandate full traceability, favoring suppliers with complete lot-to-lot documentation and uncertainty budgets. As these standards climb, mid-tier reagents cede share to high-conformity products priced on value rather than volume.

Digitization and AI-Enabled High-Throughput "Lab-of-the-Future" Initiatives

Automation adoption accelerated in 2024 as researchers sought consistent data and relief from skilled-labor shortages. Cloud labs such as Emerald Cloud Lab centralize instrument fleets, enabling pooled procurement agreements for reagents, consumables, and calibration standards. These models prefer bottle-ready formats and validated SDS archives that interface with electronic lab notebooks via APIs. AI-driven design of experiments demands vast, well-annotated chemical libraries to train predictive models, opening niches for data-rich reagent catalogs. Vendors that integrate ordering portals with laboratory information management systems are displacing traditional distributors that rely on fragmented manual workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Feedstock Prices for Key Solvents and Acids | -0.8% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Stringent Hazardous-Waste and Chemical-Safety Regulations | -0.5% | EU and North America leading, expanding globally | Medium term (2-4 years) |

| Availability of Functional Substitute Kits and Automation Platforms | -0.4% | Developed markets with high automation adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Feedstock Prices for Key Solvents and Acids

Sharp swings in crude-oil and naphtha benchmarks cascade into acetone, acetonitrile, and sulfuric-acid supply, destabilizing budgeting for high-consumption labs. Suppliers risk margin compression as tender-driven customers resist price pass-throughs. Geographic clustering of specialty chemical production in East Asia magnifies exposure when maritime bottlenecks or trade friction arise. Dual-sourcing strategies offset risk but incur qualification costs that stretch timelines and tie up working capital. Academic institutions, already coping with grant uncertainties, feel the pinch most acutely in the near term.

Stringent Hazardous-Waste and Chemical-Safety Regulations

The newest REACH updates expand the Substances of Very High Concern list, forcing expensive reformulation or discontinuation of longstanding reagents[2]European Chemicals Agency, “Candidate List of SVHCs,” echa.europa.eu. Waste-disposal levies are rising as local authorities reclassify previously benign mixtures into higher-fee categories. Suppliers must now furnish extensive exposure-scenario documentation, multilingual SDS, and digital traceability records that strain regulatory teams. Smaller niche manufacturers without global compliance infrastructure face exit decisions, nudging the laboratory chemicals market toward higher concentration among well-capitalized players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biochemistry Leads Amid Proteomics Expansion

Biochemistry captured 27.12% of laboratory chemicals market share in 2025, underscoring its pivotal role in enzyme kinetics, metabolomics, and proteome-scale analyses. Proteomics labs routinely consume high-purity buffers, reducing agents, and mass-spectrometry grade solvents that command price premiums. Within this category, the laboratory chemicals market size for healthcare/pharmaceutical reagents is expected to compound at 4.93% CAGR through 2031 as drug manufacturers upscale biologics pipelines.

Molecular-biology reagents trail closely behind, buoyed by CRISPR and next-generation sequencing workflows that require fidelity-centric polymerases and nucleotide mixes. Cell/tissue-culture media are shifting toward serum-free, chemically defined formulations, aligning with regulatory guidance for advanced therapies. Environmental-testing chemicals continue steady uptake as governments widen contaminant-screening mandates. Across these subdomains, suppliers win share by offering data-rich certificates of analysis and flexible batch sizes that minimize customer inventory costs.

By Application: Academia Dominates Despite Funding Pressures

Academia/educational users retained 30.66% of the laboratory chemicals market in 2025, benefiting from diversified funding sources even as federal appropriations tightened. Bulk purchases span everything from basic acids for first-year teaching labs to high-grade reagents for cross-disciplinary research clusters. Industry buyers drive the second-largest slice of demand as in-house QC and process-development teams fortify analytical depth in response to stricter regulatory audits.

Cell/tissue culture emerged as the quickest-growing application, clocking a 4.58% CAGR from 2026 onward on the back of cell-therapy and organoid programs. Government laboratories remain stable consumers as they expand environmental-surveillance networks. The laboratory chemicals market size within healthcare/pharmaceutical applications is also expanding in lockstep with biologics capacity build-outs, cementing long-term offtake for GMP-grade consumables.

Geography Analysis

North America anchored 29.60% of 2025 revenue, fueled by GSK’s USD 30 billion and Eli Lilly’s USD 5 billion investments in U.S. manufacturing facilities. Federal bodies such as the FDA and EPA sustain consistent reagent requisitions for compliance and research mandates. Canada’s specialty-chemicals ecosystem adds regional supply resilience, further entrenching the laboratory chemicals market across the continent.

Asia-Pacific is on course for the most rapid expansion at a 4.66% CAGR. China’s push for biotech self-sufficiency spurs heavy procurement of chromatography media, cell-culture supplements, and analytical standards. India leverages its API leadership to source validation reagents domestically while exporting surplus supply worldwide. Japan and South Korea contribute high-end materials science and genomics demand, underpinning a sophisticated buyer base that prizes traceability and automation compatibility. The laboratory chemicals market size in Asia-Pacific thus benefits from both volume and value-added product mixes.

Europe retains a robust foothold underpinned by strict environmental legislation and advanced pharma clusters centered in Germany and Switzerland. Green-chemistry adoption is accelerating as public funding channels reward low-carbon lab operations. Brexit has nudged some ordering hubs from the UK to mainland EU, but trans-Atlantic and intra-European trade flows remain largely intact. Emerging regions such as South America and the Middle East and Africa are increasingly commissioning public-health labs, signaling future incremental uplift even though current shares stay modest.

Competitive Landscape

The laboratory chemicals market is moderately concentrated. Thermo Fisher Scientific’s USD 4.1 billion purchase of Solventum’s purification unit in September 2024 broadened its consumables span and fortified end-to-end workflow coverage. Merck KGaA, Agilent, and Sartorius continue to scale through targeted bolt-ons that add niche capabilities in filtration, chromatography, and bioprocess single-use systems.

Technology remains the chief battleground. Leaders are embedding AI into formulation design, enabling customers to model reagent interactions digitally before bench work. Patent filings around self-driving laboratory interfaces and smart packaging are ramping, hinting at future differentiation anchored in data services rather than commoditized chemicals.

Sustainability is the parallel axis of competition. Early movers offering carbon-accounted solvent alternatives and recyclable containers are securing preferred-supplier status on ESG-constrained tenders. New entrants include cloud labs that negotiate bundled reagent contracts, compressing margins but boosting volume visibility for accepted suppliers.

Laboratory Chemicals Industry Leaders

ITW Reagents Division

Merck KGaA

Avantor, Inc.

Thermo Fisher Scientific Inc.

Agilent Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Shanghai Bid Pharmaceutical Technology Co., Ltd. and two investment funds acquired Combi-Blocks for USD 215 million. This acquisition aims to integrate Combi-Blocks' global supply of laboratory chemicals with Shanghai Bid Pharmaceutical Technology Co., Ltd.'s existing business.

- May 2023: Calibre Scientific announced the acquisition of Chemos GmbH & Co. KG. Chemos manufactures laboratory chemicals and supplies raw materials to the chemical, food, and pharmaceutical industries

Global Laboratory Chemicals Market Report Scope

Laboratory chemicals are all chemicals used for laboratory tests and experiments. Most are standard chemical reagents, or simple chemicals that serve as building blocks for synthesizing more complex chemicals. The scope of the laboratory chemicals market report includes segmentation by type, application, and geography. The market is segmented by type into molecular biology, cytokine and chemokine testing, carbohydrate analysis, immunochemistry, cell/tissue culture, environmental testing, biochemistry, and other types. The market is segmented by application into industrial, academia/educational, government, and healthcare (pharmaceutical). The report also covers the market size and forecast for the market in 16 countries across major regions. The report offers market size and forecast for laboratory chemicals in terms of revenue (USD) for all the above segments.

By Type

| Biochemistry |

| Molecular Biology |

| Cytokine and Chemokine Testing |

| Carbohydrate Analysis |

| Immunochemistry |

| Cell/Tissue Culture |

| Environmental Testing |

| Other Types |

By Application

| Academia/Educational |

| Industrial |

| Government |

| Healthcare (Pharmaceutical) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Biochemistry | |

| Molecular Biology | ||

| Cytokine and Chemokine Testing | ||

| Carbohydrate Analysis | ||

| Immunochemistry | ||

| Cell/Tissue Culture | ||

| Environmental Testing | ||

| Other Types | ||

| By Application | Academia/Educational | |

| Industrial | ||

| Government | ||

| Healthcare (Pharmaceutical) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the laboratory chemicals market be by 2031?

Value is projected to reach USD 37.03 billion under a 4.24% CAGR forecast.

Which product category currently holds the highest revenue share?

Biochemistry commands 27.12% of revenue thanks to its central role in proteomic and metabolomic assays.

Which application segment is expanding fastest through 2031?

Cell/tissue culture reagents are expected to post a 4.58% CAGR, reflecting growth in cell therapies.

Why is Asia-Pacific the most attractive growth region?

Why is Asia-Pacific the most attractive growth region?

Page last updated on: