Triacetin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

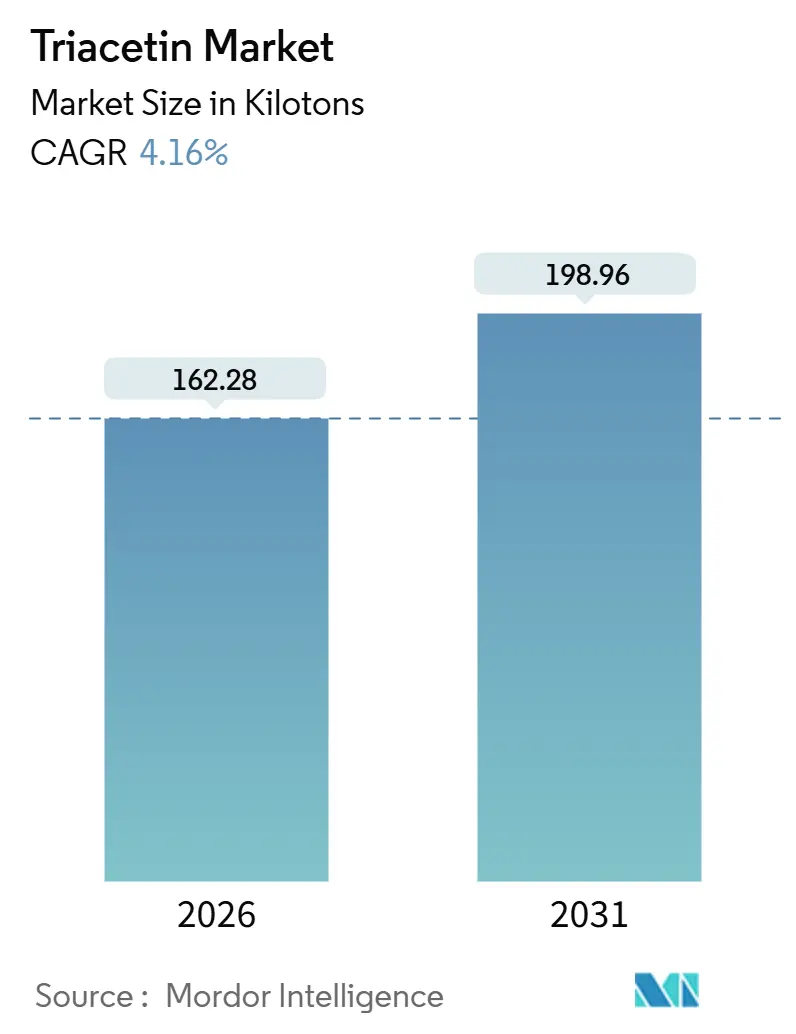

| Market Volume (2026) | 162.28 kilotons |

| Market Volume (2031) | 198.96 kilotons |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Triacetin Market Analysis by Mordor Intelligence

The Triacetin Market size is estimated at 162.28 kilotons in 2026 and is expected to reach 198.96 kilotons by 2031, at a CAGR of 4.16% during the forecast period (2026-2031). Strong demand for triacetin-plasticized cellulose-acetate filters in Asia, rising usage in nutraceutical soft-gel capsules, and emerging solvent roles in high-solid ink-jet inks are the principal growth engines. Process-intensification technologies, notably continuous reactive distillation, are compressing production costs and widening the adoption window for bio-based glycerin feedstocks. Meanwhile, tightening European Union purity rules and sporadic acetic-anhydride price spikes inject compliance and margin risk. Competitive strategies now revolve around vertical acetyl-chemical integration, sustainability-certified offerings, and long-term offtake deals with cigarette majors, while diversified opportunities in cosmetics and flexible packaging begin to offset a maturing tobacco segment.

Key Report Takeaways

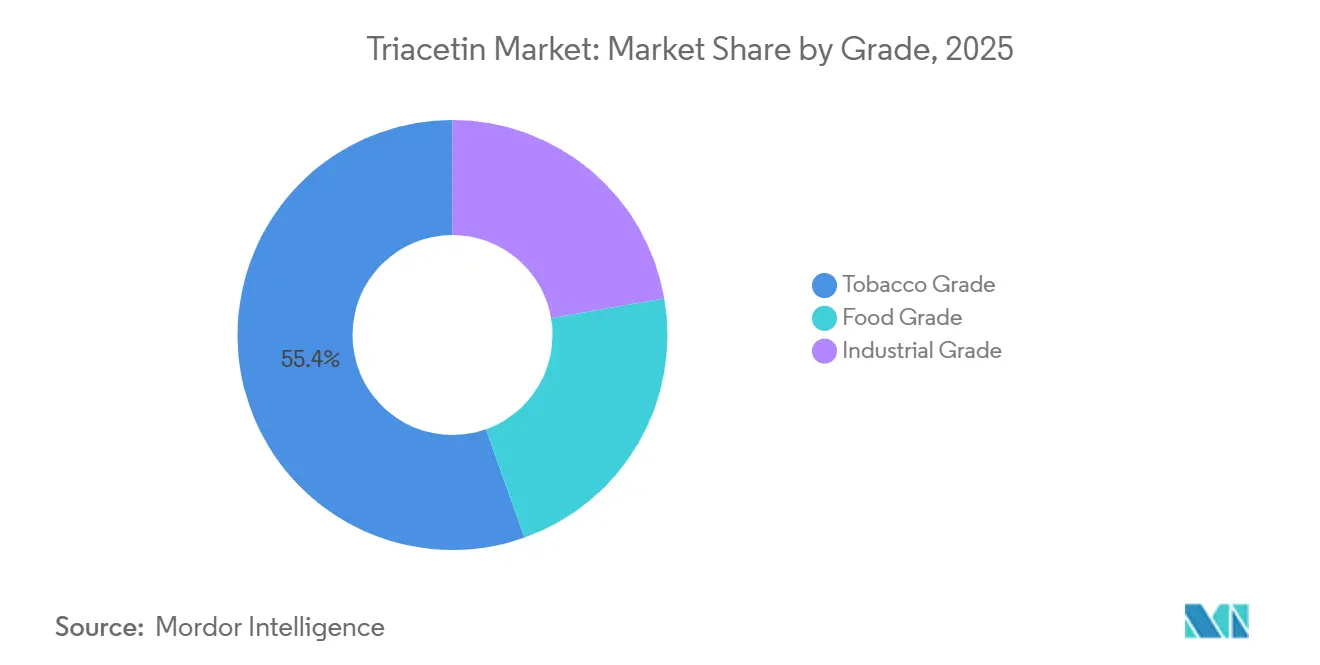

- By grade, tobacco grade led with 55.45% of 2025 volume; food grade is advancing at a 5.56% CAGR to 2031.

- By product type, plasticizers contributed 45.32% of 2025 demand, whereas solvents are forecast to grow at a 6.61% CAGR through 2031.

- By source, synthetic-glycerin routes supplied 60.65% of output in 2025, while vegetable-glycerin sourcing expanded at a 6.69% CAGR through 2031.

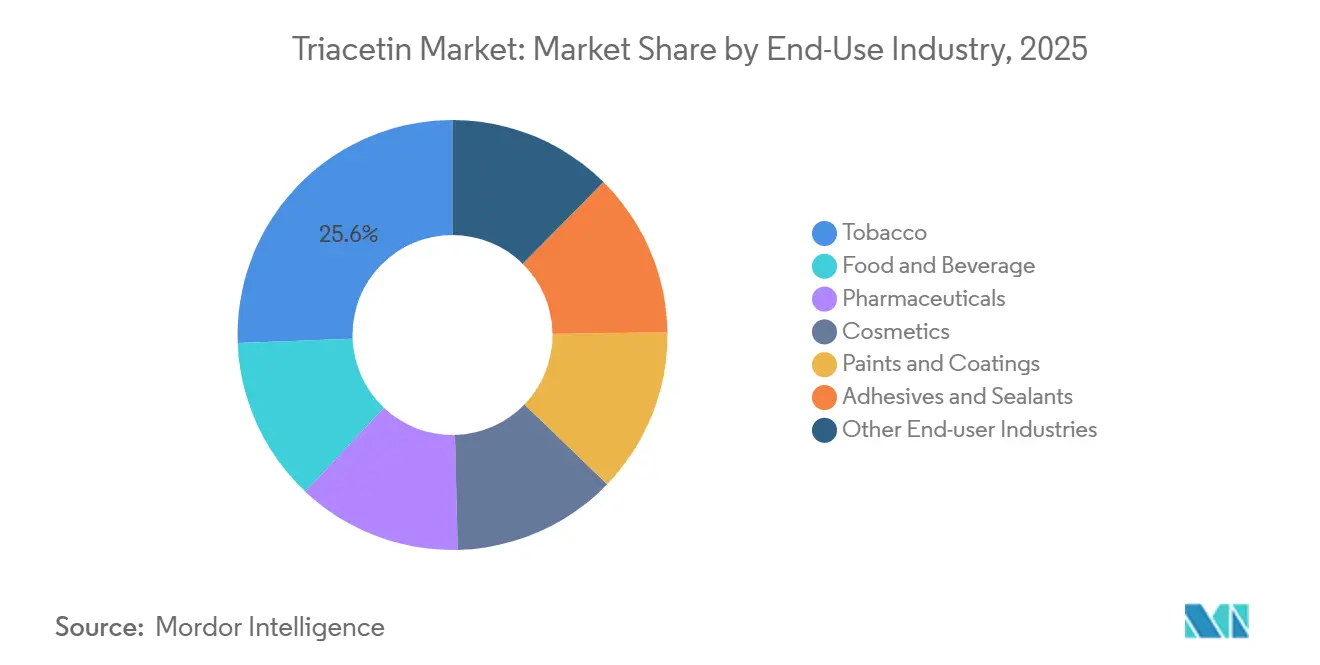

- By end-use industry, tobacco captured 25.59% of demand in 2025; cosmetics head the growth league at 6.18% CAGR to 2031.

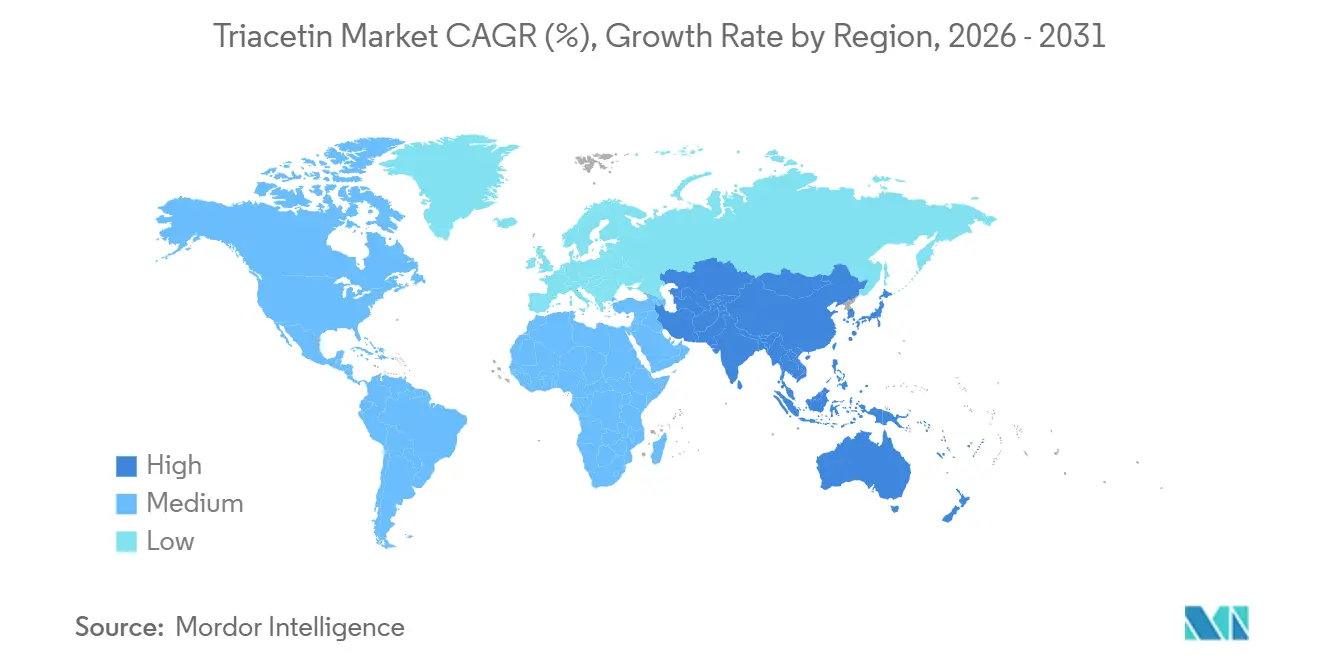

- By geography, Asia-Pacific commanded 55.71% of volume in 2025 and is set to post a 5.22% CAGR, the strongest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Triacetin Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing implementation of triacetin-plasticized cellulose-acetate tow in Asian cigarette filters | +1.2% | China, India, Indonesia, Middle East | Medium term (2–4 years) |

| Surging demand for gel-caps in nutraceuticals | +0.9% | North America, Europe, global spillover | Long term (≥4 years) |

| Shift toward bio-based plasticizers under Europe’s paints and coatings regulations | +0.7% | Germany, France, United Kingdom, North America | Long term (≥4 years) |

| Emergence of triacetin as carrier solvent in high-solid ink-jet inks for flexible packaging | +0.5% | Asia-Pacific, North America | Medium term (2–4 years) |

| Adoption of continuous reactive-distillation units lowering production cost and carbon footprint | +0.6% | China, Europe, global early adopters | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Implementation of Triacetin-Plasticized Cellulose-Acetate Tow in Asian Cigarette Filters

China’s filter-rod lines operating at 400–800 m/min require a stable plasticizer to control tow density at 1.28–1.32 g/cm³; triacetin delivers the needed migration profile, locking it into cigarette specifications. Daicel’s two-band patent quantifies typical triacetin dosing at 6–8 wt%, translating into repeat purchases with every rod formed. Eastman’s Fibers unit logged USD 1,318 million sales in 2024, 60% of which came from the ten largest cigarette manufacturers, underscoring volume certainty but also concentration risk[1]Eastman Chemical Company, “2024 Annual Report,” eastman.com. India and Indonesia continue to shift smokers toward filtered formats, lengthening rods to cut tar yields and pushing per-stick triacetin demand upward. Regulatory traceability requirements from the FDA and the EU’s Tobacco Products Directive elevate the barriers for low-cost suppliers, reinforcing incumbent dominance.

Surging Demand for Gel-Caps in Nutraceuticals

Soft-gel capsules rely on plasticizers to curb shell brittleness during high-speed encapsulation; triacetin’s dual hydrophilic and lipophilic miscibility tailors release profiles in both gelatin and carrageenan systems[2]PharmaCompass, “Triacetin – Excipient Profile,” pharmacompass.com. BASF’s Kollisolv GTA positions triacetin as a film-forming excipient compliant with Ph.Eur. and USP/NF monographs, lending regulatory confidence to contract manufacturers. Vegetarian soft-gel capacity additions in Bahrain and India intensify pharmaceutical-grade pull. FDA GRAS affirmation and the presence of multiple Type IV Drug Master Files bolster adoption in liability-sensitive nutraceuticals. Limited comparative data on polysaccharide shells present a research and development gap, yet early evidence favors triacetin’s hydrophilicity for carrageenan formulations.

Shift Toward Bio-Based Plasticizers Under Europe’s Paints and Coatings Regulations

REACH lists triacetin at 10,000–100,000 tons/year with 23 active registrants; the February 2025 high-purity amendment to Regulation (EU) 10/2011 tightens migration thresholds to 0.05 mg/kg, spurring demand for certified bio-routes. Eastman’s Triacetin Renew 59 uses mass-balance to deliver 59% recycled plus 41% bio-based content, satisfying brand sustainability scorecards. Academic work confirms triacetin’s effective plasticization of PVC up to 200 °C while avoiding phthalates, supporting uptake in wire and cable coatings. A Danish EPA survey pegged triacetin at EUR 1.50/kg in 2010, a 150% premium over DEHP; although no 2026 update is available, purity overheads likely keep a price delta in place. Incremental demand emerges from architectural paint formulators seeking non-phthalate solutions.

Emergence of Triacetin as Carrier Solvent in High-Solid Ink-Jet Inks for Flexible Packaging

Triacetin’s boiling point of 258 °C and viscosity of 21–24 mPa·s enable high-solid pigment loads while curbing VOC emissions during industrial printing runs. Eastman markets the molecule for “inks on plastics,” signaling acceptance across graphic-arts lines. Its refractive index of 1.4305 aids droplet precision in piezo heads, while a 138 °C flash point maintains plant safety margins. Flexible packaging converters in Asia are early adopters that value print-speed gains without solvent-recovery retrofits. Forthcoming REACH revisions could add testing costs, yet the solvent’s non-listed toxicity profile keeps it competitive against ketones and glycol ethers.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in acetic-anhydride prices linked to methanol supply constraints | -0.5% | Global, acute in China coal-to-methanol clusters | Short term (≤2 years) |

| Regulatory scrutiny on plasticizers in Europe | -0.3% | Europe, North America spillover | Medium term (2–4 years) |

| Anti-smoking policies targeting single-use cellulose filters | -0.8% | EU, Australia, Canada, global echo | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Acetic-Anhydride Prices Linked to Methanol Supply Constraints

Triacetin producers dependent on acetic anhydride endure feedstock swings tied to natural-gas and coal markets; a 2024 Renewable Energy simulation flagged route-2 economics (acetic anhydride) as uncompetitive under recent price decks. Eastman hedges 75% of raw-material exposure yet still devotes 45% of operations cost to feedstocks, illustrating systemic sensitivity. Coal-gasified methanol hubs in China amplify volatility during power rationing or safety inspections. Hedging and dual-feed strategies partially mitigate, but regional cost gaps persist.

Regulatory Scrutiny on Plasticizers in Europe

Regulation (EU) 2025/351 now forces documentation of non-intentionally added substances down to 0.05 mg/kg migration, raising analytical spend for every food-contact triacetin batch. REACH’s forthcoming overhaul could impose authorization barriers, adding lead times and risk premiums. UK e-liquid rules call for toxicological data in both heated and unheated states, and peer-reviewed aerosol tests linked triacetin to elevated acrolein levels at 3–6 wt%, fuelling precautionary bans in some vaping segments. Compliance budgets now form a competitive moat for incumbents with QC laboratories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Tobacco Dominance Amid Food Acceleration

Tobacco grade anchored 55.45% of 2025 volume, benefiting from entrenched filter specifications in China’s 400-billion-stick output. The triacetin market size for tobacco grade is projected to inch forward at low single-digit rates, constrained by anti-smoking drives. By contrast, food grade is expanding at 5.56% CAGR, propelled by flavor-solvent roles in confectionery and dairy, where GRAS status eases formulation. Pricing power remains higher in food and pharma channels that demand USP/NF documentation and lot traceability. The shift underscores a gradual pivot toward regulated, high-purity niches that cushion volatility in tobacco volumes.

Legacy acetyl-chemical integration grants incumbents a cost edge in commodity tobacco streams, yet the compliance premium in food-grade widens gross margins despite lower tonnage. Suppliers with dual capabilities—Eastman, BASF, Polynt—can arbitrage between grades, redirecting output as filter demand moderates. Start-ups chasing food-grade must absorb high analytical overheads and build brand trust, elongating break-even timelines.

By Product Type: Solvent Gains as Plasticizer Matures

Plasticizers accounted for 45.32% of 2025 demand on the back of filter rods, soft-gel shells, and PVC blends. However, the solvent segment is forecast to grow 6.61% CAGR, outpacing plasticizers as flexible-packaging printers shift to high-solid inks and pharma formulators exploit dual miscibility. The triacetin market share for solvents is set to widen as VOC caps tighten in major print hubs.

Humectant roles in food and topical pharma hold niche but steady slices, while explosive and foundry uses retreat amid safety and environmental audits. Process-intensified capacity keeps supply agile, allowing producers to pivot volumes toward solvent buyers without major plant revamps. High-purity needs in inks intended for food wrappers weave regulatory synergy with food-grade requirements.

By Source: Vegetable Glycerin Gains on Sustainability Push

Synthetic glycerin still fed 60.65% of 2025 output thanks to predictable purity and global petrochemical supply chains. Yet vegetable-derived glycerin is charting a 6.69% CAGR, catalyzed by REACH purity demands and brand sustainability scorecards. The triacetin market size for vegetable routes is small but lucrative, leveraging ISCC plus mass-balance certifications such as Eastman’s Renew 59.

Biodiesel side-streams keep crude glycerol prices discounted, but upfront purification to pharma grade adds equipment and energy load. Reactive-distillation gains narrow that gap, enhancing the carbon narrative and supporting scope-3 emissions cuts for downstream users. Regional biofuel policy swings still dictate feedstock availability, urging multi-source procurement strategies.

By End-Use Industry: Cosmetics Outpaces as Tobacco Plateaus

Tobacco retained 25.59% of 2025 consumption, yet a flat outlook signals diminishing marginal utility from price hikes. Cosmetics is clocking 6.18% CAGR, with formulators abandoning phthalates in nail lacquers and fragrances, areas where triacetin offers biodegradability and film flexibility. The triacetin market size for cosmetics could surpass tobacco by value before 2031 if current price differentials persist.

Food and beverage leverage humectant and solvent roles, sustaining mid-single-digit growth underpinned by emerging-market confectionery demand. Pharmaceuticals absorb premium-priced volumes tied to soft-gel expansions and topical creams. Adhesives, sealants, and coatings remain price-sensitive adopters; bio-based certification could unlock future demand if cost gaps shrink.

Geography Analysis

Asia-Pacific commanded 55.71% of 2025 shipments, with China’s 35% share of global cigarette production anchoring basal demand. The triacetin market size in Asia-Pacific will expand at a 5.22% CAGR through 2031, buoyed by integrated acetate-tow supply chains and rising contract capsule output in India. Eastman supplies 100% acetate flake to its Chinese venture from Kingsport, illustrating trans-Pacific feedstock dependency.

North America contributes a significant share of Eastman’s fiber sales; vertical coal-to-acetyl integration ensures cost resilience, while mature smoking trends curb volume upside. Nevertheless, pharmaceutical-grade pull and bio-jet-fuel glycerol streams support modest growth. Europe, Middle East, and Africa face the most stringent plasticizer rules, forcing capacity upgrades or exit decisions among smaller players.

South America benefits from biodiesel-derived glycerin surpluses in Brazil and Argentina, offering feedstock leverage for local triacetin projects. The Middle East eye acetyl diversification in Saudi Arabia’s downstream push, though water scarcity and glycerol availability temper near-term scale. Overall, geographic diversification hedges policy and commodity risk, yet Asia remains the gravitational center.

Competitive Landscape

The triacetin market is moderately consolidated. Process innovation is the new battleground. Reactive-distillation license deals promise 70% cost savings, a threat to incumbents clinging to batch reactors. Eastman’s Triacetin Renew exemplifies sustainability branding, while Daicel defends tobacco niches with patented tow-band technologies. Indian CDMOs such as Mohini Organics exploit ISO and Kosher badges to carve pharma-grade export lanes. Potential entrants weigh purification capital against rising compliance hurdles. Feedstock control, particularly over bio-glycerin streams, and analytical-lab depth now delineate competitive moats. Strategic partnerships between biodiesel refiners and acetyl chemists could rewrite cost curves and regional power balances by 2030.

Triacetin Industry Leaders

Eastman Chemical Company

Daicel Corporation

LANXESS

Polynt S.p.A

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The European Commission released Regulation (EU) 2025/351, mandating “high degree of purity” proof and stringent migration limits for food-contact plasticizers, raising compliance overheads across the triacetin value chain.

- October 2024: BASF PETRONAS Chemicals doubled 2-ethylhexanoic acid capacity to 60,000 tons/year at its Kuantan site to strengthen Southeast Asian acetyl supply chains.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the triacetin market covers the global sale of neat glyceryl triacetate, manufactured from vegetable or synthetic-origin glycerin, for use as a plasticizer, solvent, humectant, and allied specialty functions within tobacco, food, pharmaceutical, cosmetic, coatings, and other industrial channels. Our study reports both volume and value; yet models are anchored first on traded kilotons.

Scope exclusion: formulated downstream blends such as ready-to-use e-liquid bases, nail polish, or bioplastic compounds containing triacetin lie outside this scope.

Segmentation Overview

- By Grade

- Tobacco Grade

- Food Grade

- Industrial Grade

- By Product Type

- Plasticizer

- Solvent

- Humectant

- Other Product Types

- By Source

- Vegetable-Glycerin-Based

- Synthetic-Glycerin-Based

- By End-Use Industry

- Tobacco

- Food and Beverage

- Pharmaceuticals

- Cosmetics

- Paints and Coatings

- Adhesives and Sealants

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews with acetate-tow producers, Southeast Asian formulators, pharmaceutical excipient buyers, and North American regulators validate grade splits, transacted prices, and substitution intent; closing information gaps uncovered during desk work.

Desk Research

Our analysts mine open datasets issued by the US Food and Drug Administration, Eurostat COMEXT, China Customs, and the World Bank, complemented by insights from the International Tobacco Growers Association, Food Chemicals Codex digests, and peer-reviewed glycerin ester studies. Company 10-Ks, investor decks, and chemical import permits expand the evidence pool. Mordor's access to D&B Hoovers and Dow Jones Factiva brings plant capacity, contract, and price spread details that public sources seldom reveal. The sources listed are illustrative; many additional repositories inform the model.

Market-Sizing & Forecasting

The model begins with a top-down apparent consumption build: national output and net trade flows are compiled, then reconciled with excise filings before selective bottom-up supplier shipment checks fine-tune anomalies. Key drivers, including acetate-tow production, flavored e-cigarette penetration, gelatin capsule output, vegetable glycerin availability, acetic anhydride cost swings, and regional disposable income trends, feed a multivariate regression that projects demand through 2030 while scenario analysis tests vaping or single-use plastic policy shocks.

Data Validation & Update Cycle

Analysts run variance and anomaly screens against historic ratios and external indicators. Findings pass dual review, and any swing beyond three percentage points triggers expert re-contact. Reports refresh yearly, with interim updates for material events, ensuring clients receive the latest baseline.

Why Mordor's Triacetin Baseline Commands Reliability

Published figures often diverge because providers mix derivatives, apply list rather than transacted prices, and refresh at uneven cadences. Our discipline, tracking neat chemical volumes, dual unit reporting, and annual reruns, tempers volatility and offers decision makers a reproducible anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 155.89 kt (2025) | Mordor Intelligence | - |

| USD 363.1 mn (2024) | Global Consultancy A | Includes downstream blends and packaging margins |

| USD 296.9 mn (2024) | Regional Consultancy B | Uses list prices, lacks trade reconciliation |

| USD 327.43 mn (2024) | Trade Journal C | Applies uniform CAGR from 2019 without end-use validation |

These comparisons show that by anchoring on audited production and customs data and validating every assumption with frontline users, Mordor delivers a balanced, transparent baseline that clients can trace and replicate with confidence.

Key Questions Answered in the Report

What volume is the triacetin market projected to reach by 2031?

The triacetin market is forecast to hit 198.96 kilotons by 2031, reflecting a 4.16% CAGR across the period.

Which region will add the most incremental triacetin demand through 2031?

Asia-Pacific is expected to register the strongest absolute increase, powered by cigarette filter production and expanding pharmaceutical capacity.

How fast is food-grade triacetin growing relative to tobacco grade?

Food grade is advancing at 5.56% CAGR, outpacing the mature tobacco grade that presently dominates volume.

What technological shift could lower triacetin production costs?

Continuous reactive-distillation technology can trim specific production costs by about 70%, as validated in a 2025 Scientific Reports study.

Which end-use segment is emerging as the fastest growth avenue?

Cosmetics, particularly nail lacquers and fragrances, is expanding at 6.18% CAGR due to the move toward non-phthalate, biodegradable plasticizers.

How stringent are new EU rules on triacetin purity?

Regulation (EU) 2025/351 enforces “high degree of purity” and migration limits of 0.05 mg/kg, compelling exhaustive analytical documentation for each batch.

Page last updated on: