Alpha Methylstyrene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 307.70 kilotons |

| Market Volume (2031) | 369.18 kilotons |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

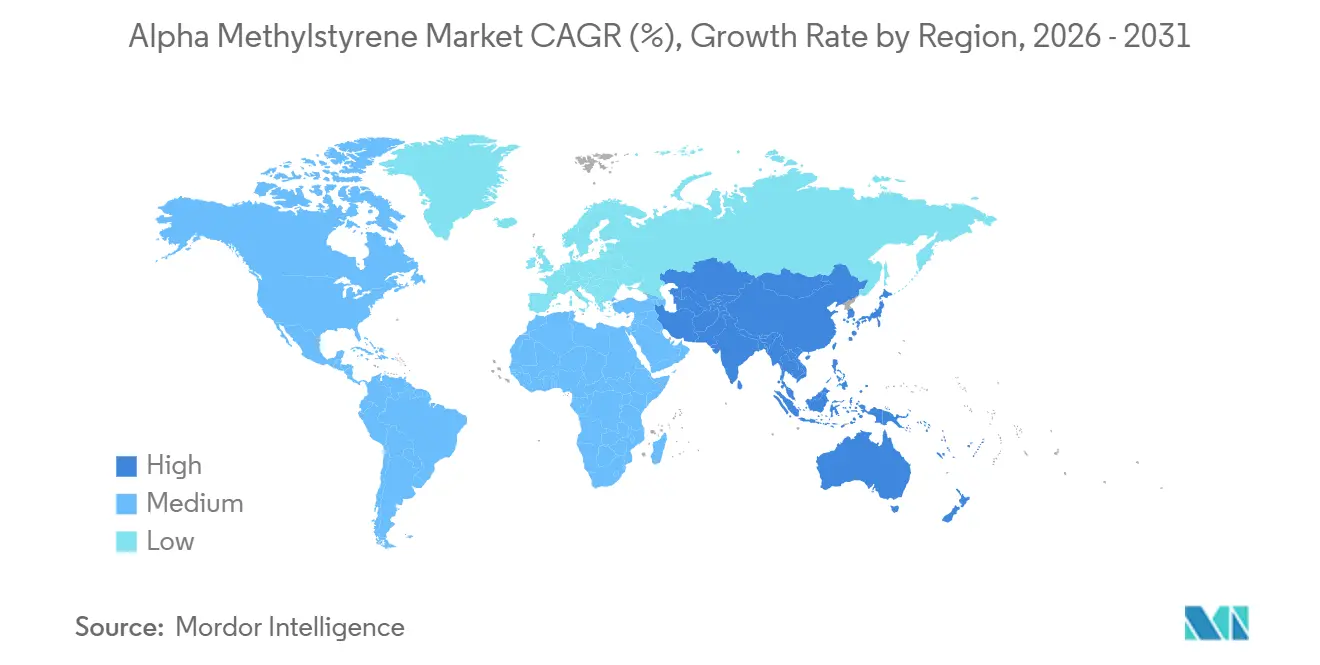

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

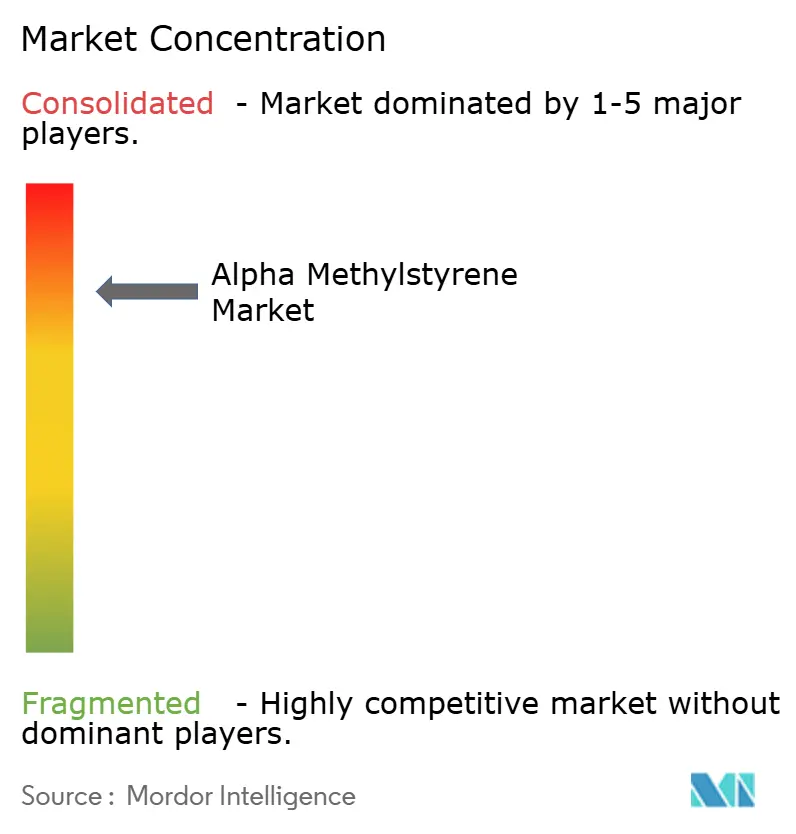

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alpha Methylstyrene Market Analysis by Mordor Intelligence

The Alpha Methylstyrene Market size is estimated at 307.70 kilotons in 2026, and is expected to reach 369.18 kilotons by 2031, at a CAGR of 3.71% during the forecast period (2026-2031). This growth rests on three structural pivots: Asia-Pacific refinery-to-chemicals integration, automotive lightweighting, and electronics miniaturization. Roughly 95% of global Alpha-Methylstyrene output remains tied to phenol economics, so supply swings more with phenol than with direct Alpha-Methylstyrene demand. Capacity rationalization in Japan and Europe has begun as integrated Chinese complexes push surplus volumes into export channels, while producers that control phenol, acetone, and Alpha-Methylstyrene in one site achieve clear cost advantages. High-purity grades are gaining momentum because downstream users now specify benzene-free and phenol-below-20 ppm limits, a trend most visible in electronics and medical devices.

Key Report Takeaways

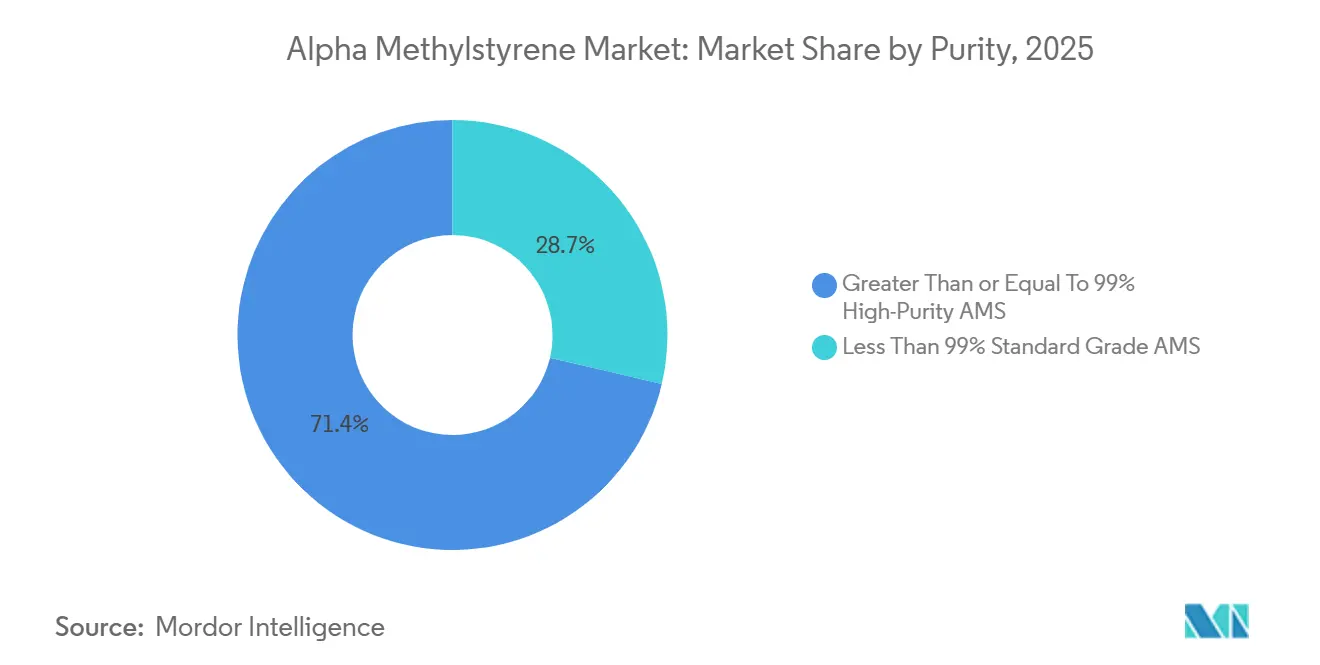

- By purity, high-purity (≥99%) grades commanded 71.35% of the alpha-methylstyrene market share in 2025, while the same category is forecast to expand at a 4.69% CAGR through 2031.

- By form, liquid bulk held 90.88% of the alpha-methylstyrene market size in 2025, yet solid flaked material is projected to grow at a 4.35% CAGR over the same period.

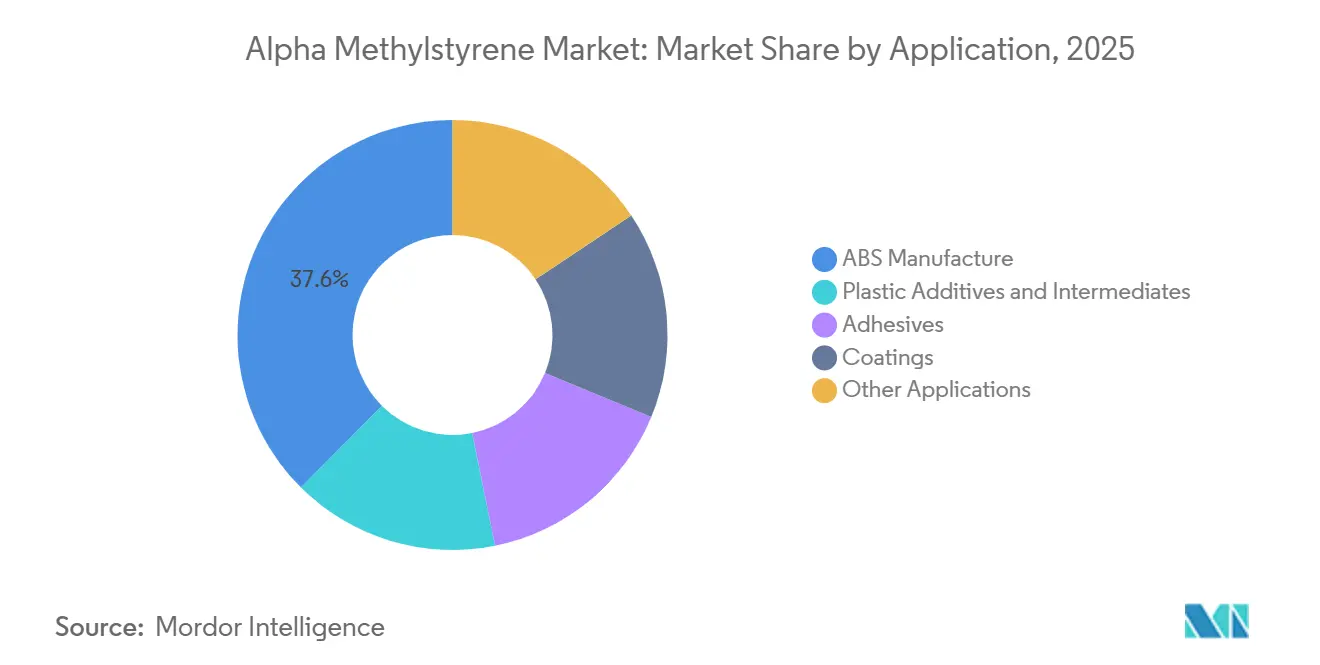

- By application, ABS manufacture led with 37.56% of the alpha-methylstyrene market size in 2025, whereas plastic additives and intermediates record the highest expected CAGR at 4.18% to 2031.

- By end user, the automotive segment accounted for 32.75% of the alpha-methylstyrene market share in 2025, and the tire segment is poised for a 5.22% CAGR to 2031.

- By geography, Asia-Pacific controlled 56.06% of 2025 volume and is forecast to advance at a 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alpha Methylstyrene Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand in lightweight automotive parts | +1.2% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Rising consumption in heat-resistant electronic encapsulants | +0.9% | Asia-Pacific, North America | Medium term (2-4 years) |

| Growing use in medical devices | +0.5% | North America, Europe, South and Southeast Asia | Long term (≥4 years) |

| Emergence of para-cumylphenol in battery electrolytes | +0.3% | Europe, Asia-Pacific EV hubs | Long term (≥4 years) |

| Closed-loop AMS recovery in caprolactam complexes | +0.4% | Europe, Japan, China | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surging Demand in Lightweight Automotive Parts

Automakers specify Alpha-Methylstyrene-modified ABS to push heat-deflection temperatures beyond 100 °C while trimming component weight by nearly one-fifth, an essential gain as battery packs crowd interior space. A 2020 patent from INEOS Styrolution documents ABS grades with up to 10 wt% Alpha-Methylstyrene that meet strict VOC and thermal targets for interior trims[1]INEOS Styrolution, “ABS Composition Patent WO2020064594,” patentscope.wipo.int. Strong electric-vehicle output in China keeps the throughput of such resins high, and North American suppliers are mirroring the formulation shift. Adoption should crest in the medium term as the EV mix accelerates and legacy internal-combustion programs sunset.

Rising Consumption in Heat-Resistant Electronic Encapsulants

Semiconductor packaging now requires polymers that survive 260 °C reflow without warping. High-purity Alpha-Methylstyrene meets this bar and complies with RoHS plus REACH, enabling its use in laptop, smartphone, and IoT housings produced across East Asia. The FDA permits indirect food contact under several CFR clauses, which further broadens appliance and packaging demand[2]U.S. Food & Drug Administration, “Indirect Food Additives Listings,” fda.gov. With Asia-Pacific responsible for more than 70% of global electronics assembly, the driver maintains a mid-term push.

Growing Use in Medical Devices Boosting Demand

Repeated steam-sterilization cycles and harsh disinfectants prompt device makers to favor Alpha-Methylstyrene-based polymers for housings and single-use components. The resin’s thermal stability and chemical inertness make it compatible with ISO 13485 and U.S. FDA quality frameworks. North America and Europe dominate early uptake, but Indian and ASEAN contract manufacturers are scaling output to serve cost-sensitive export markets.

Emergence of Para-Cumylphenol as Battery-Electrolyte Additive

Para-cumylphenol derived from Alpha-Methylstyrene improves the thermal stability of lithium-ion electrolytes used in high-energy nickel-rich cells. Recent peer-reviewed work on similar aromatic additives demonstrated reduced flammability at low concentration while maintaining 5.0 V electrochemical windows. Europe and key Asian EV hubs are piloting such formulations, setting the stage for long-term, niche but lucrative demand.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hazardous waste streams and stricter REACH/EPA limits on cumene | -0.8% | Europe, North America, global | Short term (≤2 years) |

| Volatility in crude-derived feedstock pricing | -0.6% | Europe, Southeast Asia, global | Short term (≤2 years) |

| Rise of bio-based styrenic analogues | -0.3% | North America, Europe, Asia-Pacific bio-hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hazardous Waste Streams and Stricter REACH/EPA Limits on Cumene

Cumene’s classification as a hazardous air pollutant drives capital spending on VOC abatement, while RCRA rules curb the storage time of Alpha-Methylstyrene wastes with a flash point of 53.9 °C. Smaller standalone producers struggle with the resulting compliance cost, accelerating consolidation.

Volatility in Crude-Derived Feedstock Pricing

Benzene and propylene, which form cumene, track crude oil swings. When phenol demand softens, but cumene costs stay high, merchant Alpha-Methylstyrene margins compress sharply. Import-dependent Europe faces the steepest exposure, prompting hedging and contract repricing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Purity: Higher Grades Capture Premium Margins

High-purity (≥99%) Alpha-Methylstyrene controlled 71.35% of 2025 volume and is forecast for a 4.69% CAGR to 2031, twice the pace of standard grades. Electronics and pharmaceutical buyers insist on benzene-free material with phenol below 20 ppm, allowing producers such as DOMO Chemicals to fetch 10-20% price premiums. The Alpha-Methylstyrene market size for high-purity volumes is therefore set to widen its lead as validation protocols tighten across printed-circuit and medical-device supply chains. Conversely, the commoditized standard grade remains burdened by Asian oversupply and has limited scope for differentiation.

ASTM’s dedicated D7977 test method now gives downstream buyers tighter control over polymer contaminants, reinforcing the bifurcation of the Alpha-Methylstyrene market. Integrated complexes that purify on-site can guarantee supply continuity, positioning themselves as partners of choice for high-spec applications in semiconductors, diagnostic probes, and thermoformed medical trays.

By Form: Liquid Bulk Prevails but Safety Concerns Aid Solids

Liquid Alpha-Methylstyrene dominates with 90.88% of 2025 shipments because continuous ABS and SAN polymerization plants depend on metered liquid feed. The Alpha-Methylstyrene market share for this form remains elevated, yet regulatory focus on VOC exposure is spurring a 4.35% CAGR in solid flakes.

Flaked material melts in sealed vessels, curbing vapor loss and easing compliance with tight workplace-exposure limits. EU guidelines for large-volume organic chemicals favor such approaches, giving solids momentum in Europe and Japan, where environmental permitting standards are strictest.

By Application: ABS Leads, Additives Gain Ground

ABS polymerization absorbed 37.56% of the 2025 demand, anchoring the alpha-methylstyrene market. Plastic additives and intermediates will, however, post a faster 4.18% CAGR to 2031 as formulators swap in Alpha-Methylstyrene to raise glass-transition temperatures in automotive interiors and appliance housings.

Patented graft-sheath blends show that modest Alpha-Methylstyrene loadings deliver elevated Vicat softening points without compromising impact strength, a balance valued by tier-1 suppliers. Para-cumylphenol, synthesized from the monomer, further broadens reach into battery electrolytes and specialty polycarbonates, reinforcing the additive segment’s upbeat outlook.

By End User: Automotive Dominates, Tires Accelerate

Automotive captured 32.75% of 2025 volume, relying on alpha-methylstyrene-modified ABS for dashboards, door panels, and under-hood parts. The tire segment will log the fastest 5.22% CAGR through 2031 as SBR compounders deploy Alpha-Methylstyrene-influenced tackifiers that cut rolling resistance in electric-vehicle tires.

Regulatory tire-labeling schemes in the EU and upcoming U.S. rules elevate wet-grip and efficiency metrics, both of which benefit from Alpha-Methylstyrene chemistry. Electronics, building materials, and personal-care absorb steady volumes, but none match the automotive and tire thrust that now shapes investment decisions across the alpha-methylstyrene industry.

Geography Analysis

Asia-Pacific held 56.06% of global volume in 2025 and is projected to grow at a 5.62% CAGR to 2031 on the back of mega complexes in China that pair 20 million tons/year refineries with aromatics units churning out benzene, phenol, and ultimately Alpha-Methylstyrene. The hubs of Zhejiang Petroleum & Chemical and Hengli Petrochemical epitomize this integrated model, forcing older Japanese and European plants offline.

North America, while losing some volume share, specializes in high-purity output for electronics and healthcare. INEOS Phenol’s 2023 takeover of Mitsui Phenols Singapore underscores the region’s drive to secure Asian customer proximity and diversify feedstock risk. Europe grapples with tighter REACH rules, yet its producers invest in zeolite alkylation and VOC capture that elevate product quality and cut emissions, maintaining a premium foothold.

The Middle East and Africa and South America represent nascent pockets that import most of their needs. Low-cost naphtha in the Gulf could anchor future Alpha-Methylstyrene units, but the absence of downstream ABS and SAN clusters dilutes short-term prospects. Overall, the three established regions will continue to account for more than 90% of Alpha-Methylstyrene market transactions to 2031.

Competitive Landscape

The Alpha Methylstyrene market is highly consolidated, with the top five players accounting for a significant market share. INEOS Phenol’s USD 330 million acquisition of Mitsui Phenols Singapore in 2023 boosted its Asian presence and signaled a broader consolidation trend. Mitsui Chemicals, meanwhile, elected to shutter its aging Ichihara unit by 2026 and co-opt logistics with Mitsubishi Chemical to defend domestic supply reliability. DOMO Chemicals leverages its caprolactam chain to deliver ≥99.6% purity Alpha-Methylstyrene, capturing high-margin electronics and pharma orders. Honeywell UOP’s technology packages, which fold in Alpha-Methylstyrene hydrogenation for up-cycle to cumene, give licensees a closed-loop edge that slashes waste and improves economics. Start-ups commercializing biosourced styrenic monomers represent a credible long-term threat, especially if carbon-pricing schemes reward lower-footprint feedstocks. For now, incumbents with deep integration and purification know-how retain the upper hand but must continue to invest in specialty grades to protect margins when commodity cycles soften.

Alpha Methylstyrene Industry Leaders

INEOS

Advansix

Eni S.p.A. (Versalis)

Moeve (Cepsa)

Domo Chemicals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mitsui Chemicals and Mitsubishi Chemical began a joint study to pool storage and logistics for phenol-related products, Alpha-Methylstyrene included, aiming to trim greenhouse-gas emissions and safeguard supplies during turnarounds.

- January 2025: DOMO Chemicals published updated specifications guaranteeing ≥99.6% purity Alpha-Methylstyrene with cumene less than 0.1 wt%, reinforcing its high-purity positioning.

- April 2023: INEOS Phenol closed the USD 330 million purchase of Mitsui Phenols Singapore, adding 20,000 ton/year Alpha-Methylstyrene capacity and deepening its reach in Asian polycarbonate and ABS value chains.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the alpha-methylstyrene (AMS) market as the total supply of neat, newly produced AMS, regardless of purity grade, that is sold in bulk liquid or flake form for use as a co-monomer or intermediate in plastics, resins, waxes, adhesives, coatings, and related specialty chemicals.

Scope exclusion: finished ABS resin, para-cumylphenol, and other downstream derivatives are not sized within this baseline.

Segmentation Overview

- By Purity

- Greater Than or Equal To 99% High-Purity AMS

- Less Than 99 % Standard Grade AMS

- By Form

- Liquid (Bulk)

- Solid (Flaked)

- By Application

- ABS Manufacture

- Plastic Additives and Intermediates

- Adhesives

- Coatings

- Other Applications

- By End-user Industry

- Automotive

- Tire

- Plastics

- Electronics

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement managers at ABS converters across China, Germany, and the United States, spoke with phenol-acetone producers in the Gulf Cooperation Council, and ran an online pulse survey of specialty adhesive formulators in South-East Asia. These discussions validated regional demand drivers, typical contract prices, and purification yields that desk work alone could not reveal.

Desk Research

We began with trade statistics from UN Comtrade and China Customs to track global phenol-acetone co-product output, which anchors AMS availability. Supplemental context came from the U.S. EPA air-toxics database, Eurostat PRODCOM chemical codes, and industry association briefs such as PlasticsEurope's styrenics yearbooks. Company 10-K filings and investor decks clarified planned capacity additions, while news flows were screened via Dow Jones Factiva. Paid access to D&B Hoovers helped verify plant-level financials. This list is indicative; many other open and subscription sources assisted our evidence gathering.

Market-Sizing & Forecasting

A top-down reconstruction begins with phenol capacity, co-product acetone output, and historical AMS recovery rates; these generate a global supply pool that is adjusted for self-consumption and inventory changes. Results are cross-checked with selective bottom-up roll-ups of nameplate AMS units at 27 plants and average export prices from Korean and U.S. customs data. Key model fingerprints include ABS resin production, automotive build rates, Chinese electronics exports, refinery operating ratios, and AMS spot price spreads over acetone. A multivariate regression against these indicators projects demand, while ARIMA bridges short-term shocks. Where plant data are missing, regional averages from primary calls backfill the gaps.

Data Validation & Update Cycle

Outputs pass three-layer reviews: analyst, domain lead, and quality team, before sign-off. Variances above ±5% against independent series trigger re-checks. We refresh every twelve months, issuing interim revisions when closures, start-ups, or regulation (e.g. the 2024 NESHAP update) materially shift the baseline.

Why Mordor's Alpha Methylstyrene Baseline Commands Reliability

Published estimates often differ because providers choose dissimilar product scopes, weighting methods, and refresh cadences.

Key gap drivers for AMS sizing include: a) whether low-purity recycle streams are counted as fresh supply, b) the treatment of captive ABS consumption inside integrated complexes, and c) the currency year and exchange rates applied to convert regional sales. Mordor reports both volume and value, uses current-year FX, and excludes captive recycle, which makes our figure more conservative yet repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 297.01 kt (2025) | Mordor Intelligence | - |

| USD 508.42 mn (2024) | Regional Consultancy A | Includes downstream para-cumylphenol, omits recycle adjustments |

| USD 555.8 mn (2025) | Trade Journal B | Uses list prices, not contract averages; assumes 100% plant utilization |

| USD 425.16 mn (2024) | Global Consultancy A | Stops at purity >=99.5%, only excludes emerging Asia micro-plants |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual-metric reporting, and annual refresh cycle deliver a balanced, transparent baseline that decision-makers can trace back to clear, verifiable variables.

Key Questions Answered in the Report

How large is the Alpha-Methylstyrene market in 2026?

The market is estimated at 307.70 kilotons in 2026 and is projected to expand at a 3.71% CAGR through 2031.

Which region drives most Alpha-Methylstyrene demand?

Asia-Pacific leads with 56.06% of global volume in 2025 and the fastest 5.62% growth outlook.

Why are high-purity grades gaining share?

Electronics, medical, and automotive customers now demand benzene-free material with phenol below 20 ppm, boosting ≥99% purity volumes.

What end-use segment is growing fastest?

The tire sector, fueled by electric-vehicle efficiency goals, is forecast to grow at a 5.22% CAGR to 2031.

How exposed is the market to feedstock volatility?

Highly exposed, since 95% of supply comes as a phenol co-product, tying margins to crude-linked benzene and propylene prices.

Are bio-based alternatives a real threat?

Yes, bio-refineries are piloting renewable styrenics that could erode 10-15% of specialty demand after 2030 if scale economics improve.

Page last updated on: