Industrial Enzymes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.65 Billion |

| Market Size (2031) | USD 13.02 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

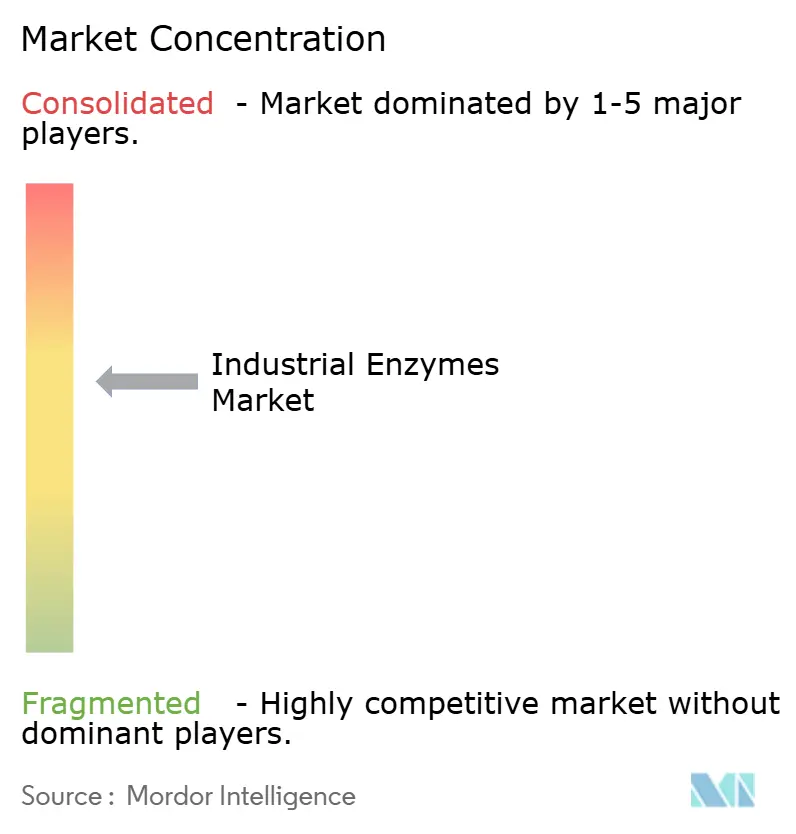

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Enzymes Market Analysis by Mordor Intelligence

The Industrial Enzymes Market size is projected to expand from USD 9.09 billion in 2025 and USD 9.65 billion in 2026 to USD 13.02 billion by 2031, registering a CAGR of 6.17% between 2026 to 2031. Growth stems from food, biofuel, detergent, and healthcare producers that replace chemical catalysts with bio-based enzymes, cutting hazardous by-products and energy use. Precision-fermentation advances have lowered production costs, enabling economical small-batch enzyme customization. North American and European biofuel mandates are spurring demand for high-efficiency cellulase and amylase blends. Clean-label regulations in the European Union and the United States accelerate enzyme uptake in bakery, dairy, and beverage plants. Competitive positioning centers on rapid strain-engineering, shorter development cycles, and integrated fermentation–purification platforms that enhance margins while meeting stricter environmental standards.

Key Report Takeaways

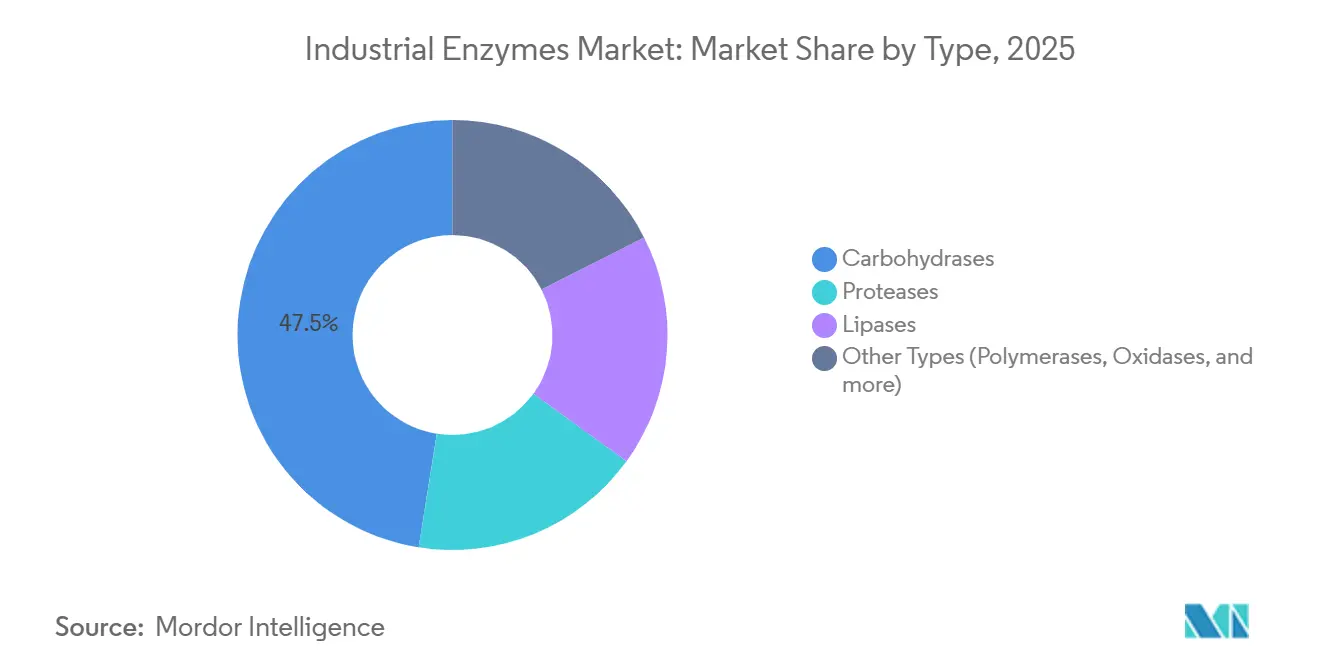

- By type, carbohydrases led with 47.50% of the Industrial Enzymes market share in 2025. Moreover, they are poised to grow with the fastest CAGR of 6.96% during the forecast period (2026-2031).

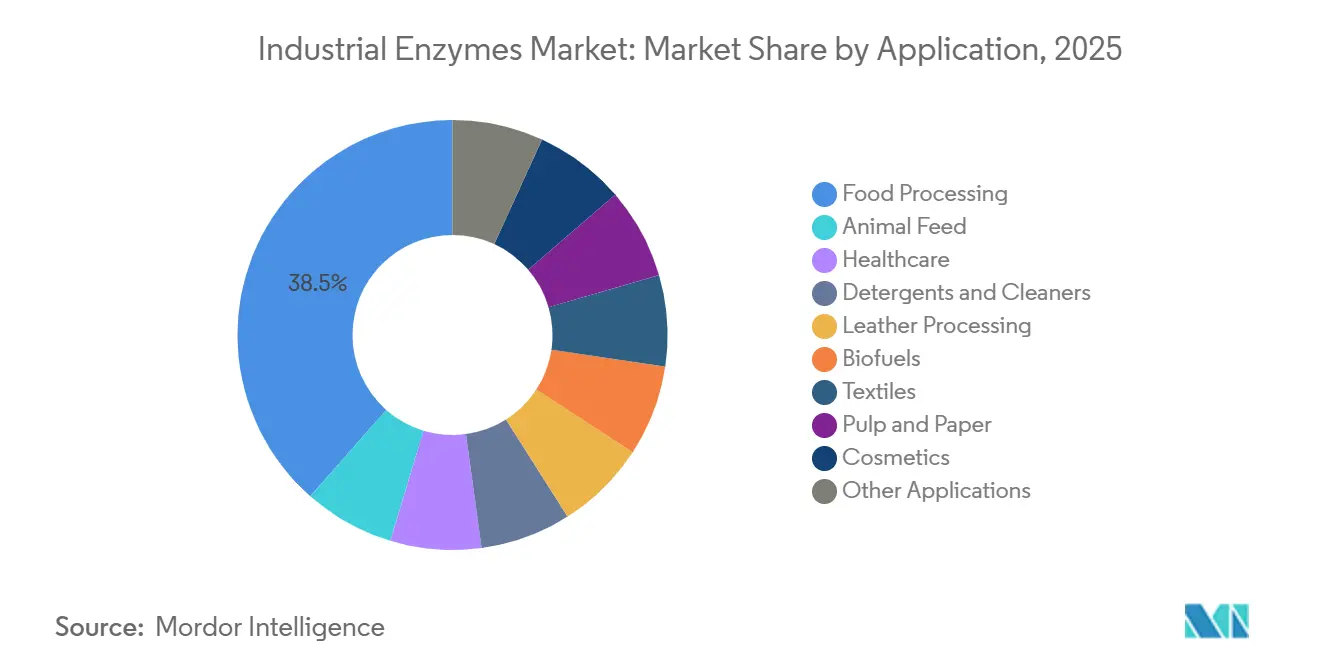

- By application, food processing accounted for 38.46% of the industrial enzymes market size in 2025 and is advancing at a 7.82% CAGR to 2031.

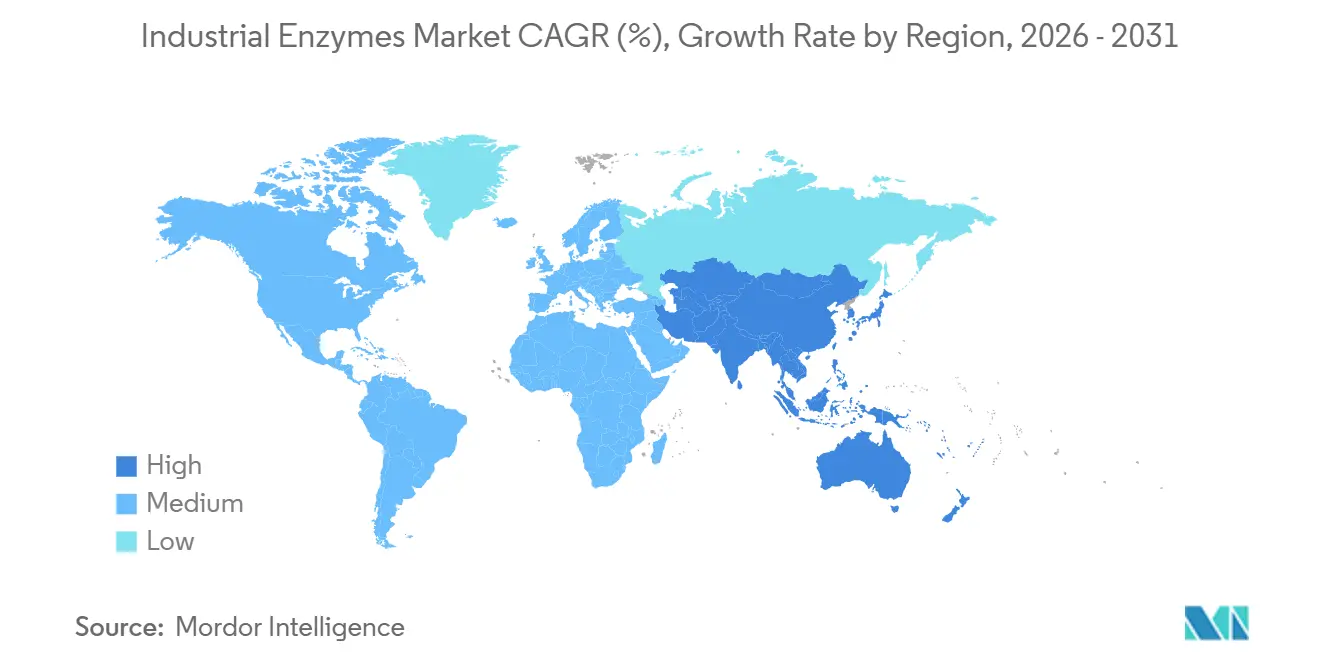

- By geography, North America accounted for 35.91% of the market share in 2025, and Asia-Pacific is expected to grow at the fastest CAGR of 6.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biofuel mandates boosting demand, especially in starch and cellulosic ethanol | +1.8% | North America, Europe, Brazil | Medium term (2-4 years) |

| Increasing adoption for industrial enzymes in food processing | +1.5% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| Stricter environmental regulations favouring bio-based processing aids | +1.2% | Europe, North America, APAC coastal regions | Long term (≥ 4 years) |

| Precision-fermentation cost breakthroughs enabling smaller-batch customised enzymes | +1.0% | Global, early adopters in North America & Western Europe | Medium term (2-4 years) |

| Healthcare shift to multi-enzymatic cleaners for infection-control compliance | +0.7% | Global, accelerated in North America, EU, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Biofuel Mandates Boosting Demand, Especially in Starch and Cellulosic Ethanol

Legislation such as the U.S. Renewable Fuel Standard targets 36 billion gallons of renewable fuel by 2027, of which 16 billion must be cellulosic, driving multi-enzyme cocktails that push glucose yields beyond 85%[1]U.S. Environmental Protection Agency, “Renewable Fuel Standard,” epa.gov. Brazil’s RenovaBio program rewards ethanol plants that cut lifecycle emissions, encouraging enzyme formulations that lower pretreatment severity. The International Energy Agency expects global biofuel output to climb 28% between 2024 and 2030, keeping enzymes at 10–15% of conversion costs. U.S. Corn Belt producers already dose thermostable alpha-amylases that tolerate ≥95 °C, trimming enzyme spend per gallon. Consolidated bioprocessing initiatives aim to halve enzyme costs by 2028, supporting wider cellulosic rollout.

Increasing Adoption for Industrial Enzymes in Food Processing

The EU Food Information to Consumers Regulation obliges clear labeling of processing aids, nudging bakeries, breweries, and dairies toward “natural” enzyme solutions[2]European Commission, “Food Information to Consumers Regulation,” europa.eu. Amylases and xylanases appear in more than 70% of Western European bread recipes, extending shelf life by up to three days without emulsifiers. Pectinases shorten juice clarification times by 40%, easing capital on membrane equipment. Transglutaminase use in yogurt replaces carrageenan while preserving texture, meeting minimal-ingredient expectations. The US FDA granted GRAS status to 30 new enzyme preparations during 2024-2025, accelerating commercialization.

Stricter Environmental Regulations Favoring Bio-Based Processing Aids

The EU Circular Economy Action Plan targets 30% renewable content in industrial chemicals by 2030, steering textile, leather, and pulp producers toward enzyme-enabled processes. USDA’s BioPreferred Program awards procurement preference to enzyme-rich detergent blends that cut phosphate loading. China’s revised 2024 wastewater norms reduced allowable chemical oxygen demand by 25%, prompting mills in Zhejiang and Guangdong to adopt laccase bleaching and protease dehairing. Scandinavian pulp mills slashed chlorine dioxide by 30% with xylanase pretreatment while achieving brightness above 85 ISO. National Paris Agreement commitments reinforce demand for low-emission bio-intermediates.

Precision-Fermentation Cost Breakthroughs Enabling Smaller-Batch Customized Enzymes

Synthetic-biology toolkits, single-use bioreactors, and membrane-based purification have reduced viable batch sizes from 10,000 L to 500 L, opening specialty diagnostics and nutrition niches. Contract manufacturers now switch products within 48 hours, avoiding cross-contamination and slashing downtime. DOE’s 2025 modular enzyme-production grants support on-site units at ethanol plants, cutting logistics costs. Faster directed-evolution cycles deliver variants with 5–10 °C wider operating ranges in under six months, critical for detergents facing diverse wash temperatures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Narrow operating pH and temperature windows for most commercial enzymes | -1.0% | Global, acute in high-temperature textile and leather sectors | Medium term (2-4 years) |

| High upstream production and downstream purification costs | -0.8% | Global, more pronounced in regions with expensive fermentation substrates | Short term (≤ 2 years) |

| Feedstock-supply concerns across various geographies | -0.6% | North America, South America, vulnerable to climate variability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Narrow Operating pH and Temperature Windows for Most Commercial Enzymes

Proteases, lipases, and carbohydrases rapidly lose activity outside pH 4.5–8.5 and above 65°C, limiting use in cotton scouring at 100°C and leather pickling below pH 3. Textile mills forced to drop temperature extend cycle times and face higher energy bills when reverting to caustic soda. Directed evolution has produced enzymes with two-hour half-lives at 80°C, yet premiums of 30–50% over wild-type variants hinder uptake in price-sensitive plants. Immobilization extends enzyme life but adds reactor cost and 10–20% activity loss during bonding. Broader deployment awaits scale-neutral thermostable formulations that meet cost parity.

High Upstream Production and Downstream Purification Costs

Downstream steps absorb up to 70% of manufacturing expense, especially for pharma-grade enzymes requiring chromatography and ultrafiltration. Feedstock shocks magnify the burden; the Midwest drought pushed 2025 corn prices above USD 6 per bushel, squeezing fermenter margins. Chromatography resin prices have climbed 8% annually since 2024 amid specialty polymer shortages. Pharma-grade trypsin commands premiums exceeding USD 5,000 per kg due to stringent endotoxin limits. Continuous fermentation and aqueous two-phase extraction promise 20–30% cost cuts, but retrofitting legacy plants demands high capital and lengthy validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbohydrases Benefit From Biofuel and Bakery Demand

Carbohydrases represented 47.50% of 2025 revenue, the highest share within the industrial enzymes market, and will grow at a 6.96% CAGR to 2031. Thermostable alpha-amylase adoption in US ethanol facilities supports high-temperature liquefaction that lowers steam costs and contamination risk. Cellulase loadings of 15–25 FPU g⁻¹ dry biomass remain vital for second-generation biofuels, with on-site production forecasts aiming to halve costs by 2028. Bakery manufacturers rely on amylases, xylanases, and glucose oxidases to extend freshness and eliminate chemical emulsifiers, meeting clean-label rules in Europe where usage tops 70% of bread lines.

Proteases follow as the second-largest contributor to the industrial enzymes market. They drive premium detergent formulations and leather bating, while pharma-grade trypsin fills a lucrative niche at prices above USD 5,000 kg⁻¹. Lipases gain traction in biodiesel transesterification and structured-lipid production for infant formula. Smaller but rapidly expanding categories such as polymerases, laccases, and oxidases serve molecular diagnostics, pulp bleaching, and eco-friendly denim finishing, illustrating the segment’s diversification path.

By Application: Food Processing Rides Clean-Label Momentum

Food processing generated 38.46% of the 2025 industrial enzymes market value and leads growth with a 7.82% CAGR forecast to 2031. EU regulations that require explicit disclosure of processing aids steer bakers, brewers, and dairies toward enzyme systems that may be declared “natural” or omitted if deactivated during processing. Juice makers deploy pectinases for faster clarification, cutting filtration capital by 40%. Transglutaminase innovation enables yogurt texture without carrageenan, underpinning minimal-ingredient labels.

Animal-feed enzymes, chiefly phytases and xylanases, enhance nutrient availability and reduce phosphorus waste, supporting environmental compliance in North America and the EU. Detergent producers seek protease, lipase, and amylase blends that lift stains in cold water, aligning with energy-efficiency goals. Biofuel plants remain heavy enzyme consumers for starch and lignocellulosic conversions under escalating renewable-fuel quotas. Smaller sectors such as textiles, pulp, cosmetics, and healthcare apply enzymes to cut water use and improve product quality, broadening the customer base.

Geography Analysis

North America captured 35.91% of the Industrial Enzymes market revenue in 2025, led by US ethanol plants that alone absorb more than 40% of regional volume. The FDA’s expedited GRAS pathway saw 30 new enzyme approvals over 2024-2025, keeping the region at the forefront of novel launches. Canada’s pulp-and-paper mills and Mexico’s livestock producers contribute incremental demand, yet together remain below 10% of regional totals. USDA BioPreferred procurement preferences further nudge detergent reformulations toward enzyme systems.

Asia-Pacific is the fastest-growing region at 6.91% CAGR through 2031. China and India benefit from 20–30% lower enzyme production costs due to competitive feedstock and labor structures. China’s 2024 wastewater limits spurred enzyme adoption in the textile and leather sectors in Zhejiang and Guangdong. India’s push to cut post-harvest losses fosters enzyme use in dairy, bakery, and beverage plants. High per-capita consumption in Japan and South Korea stems from healthcare and premium detergent demand, while ASEAN nations grow through palm-oil processing and feed applications.

In Europe, Germany, France, and the United Kingdom lead detergent and bakery consumption, while Scandinavia pioneers pulp-bleaching enzymes that reduce chlorine dioxide by 30%. The EU Circular Economy Action Plan’s 30% renewable chemical target secures long-term demand signals. South America, driven by Brazil’s ethanol program, and the Middle East & Africa, anchored by South African food processing, round out the global landscape, though adoption levels vary with infrastructure and policy support.

Regulatory Landscape

Industrial enzymes operate under application-specific authorization regimes, with food and feed uses governed by safety assessments and listings, while technical and industrial uses must also meet chemical and worker-safety obligations. In the European Union, food enzymes move through EFSA evaluation toward inclusion in the Union framework, and the European Commission updated the food-enzyme register in February 2026 (including corrections to grouped application references) as the system continues to mature.

Feed enzymes in the EU continue to move via Implementing Regulations for zootechnical additives. These include an authorization effective May 27, 2026 for a 6-phytase produced with Aspergillus oryzae (DSM 33737) and an entry into force on January 8, 2026 for a high-concentration Bacillus subtilis and Bacillus amyloliquefaciens preparation for poultry. In the United States, enzymes used in food processing typically enter the market via the FDA GRAS pathway, with the GRAS Notice Inventory continuing to add and track submissions during 2026 (including pending evaluations). In the United Kingdom, transitional processes for food enzymes were adjusted under the Food and Feed (Regulated Products) Regulations 2025, under retained rules linked to Regulation (EC) No 1332/2008.

Value Chain Analysis

The industrial enzymes value chain starts with feedstocks (typically carbohydrate sources for fermentation), microbial strain libraries and engineering toolchains, and then scale-up into commercial fermentation. Downstream recovery and purification follow, using filtration, ultrafiltration, and in higher-purity cases chromatography. Finished enzyme formulations are stabilized and blended into application-ready products (for example, carbohydrase and protease blends for food processing, detergents, and biofuels), then distributed through direct sales to large industrial accounts and through distributors and formulators that serve regional food, feed, and industrial processors.

Competitive advantage tends to concentrate on integration across strain engineering, fermentation capacity, and downstream purification, since fermentation slot availability and purification throughput are common bottlenecks when moving new strains from pilot to commercial volumes. Documentation and compliance also shape the chain: technical enzymes need supply-chain dossiers aligned to chemical and safety frameworks (for example, EU REACH for relevant substances and the US TSCA inventory for industrial chemical applications), while food and feed enzymes require application-specific data packages and authorizations. Industry bodies such as AMFEP and the Enzyme Technical Association remain active in technical-regulatory engagement, including AMFEP input during 2026 related to the EU Biotech Act discussions.

Competitive Landscape

The Industrial Enzymes Market is moderately consolidated. Market leaders integrate strain engineering, fermentation, and purification to protect IP and offer bespoke solutions, while mid-sized firms license strains and use contract manufacturing to stay asset-light. Moreover, suppliers that maintain GRAS dossiers, EFSA approvals, and ISO 9001 certification secure faster market entry and lower customer-acquisition costs, reinforcing the importance of regulatory readiness.

Industrial Enzymes Industry Leaders

DuPont

Novozymes A/S

DSM-Firmenich N.V.

BASF

AB Enzymes GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and tighter integration of R&D with manufacturing are creating whitespace in high-volume dairy and specialty food processing, where consistent enzyme supply and tailored performance influence switching decisions. In April 2026, Kerry opened an expanded biotechnology manufacturing hub in Carrigaline, County Cork, Ireland to scale lactase production for lactose-free dairy, reinforcing an opportunity around lactase demand and localized biomanufacturing capability for global customers.

Opportunities also cluster around performance-led substitutions that reduce cost, energy, or water burdens, and where compliance pressures keep attention on bio-based processing aids. Examples include detergent reformulation to improve cleaning at lower wash temperatures, textile wet processing where water reductions are a key lever, and pulp and paper bleaching sequences that lower chemical inputs. Technology pull is concentrated on variants that widen operating windows (temperature and pH tolerance) to address a recurring limitation of many commercial enzymes, as well as shorter development cycles supported by computational methods and AI-enabled screening workflows discussed in the industrialization of microbial cell-factory approaches, highlighted in research published in July 2026.

Recent Industry Developments

- April 2026: Novonesis signed an agreement to acquire a fermentation production facility in Rayong, Thailand from Meihua for about USD 50 million. The acquisition expands Southeast Asian manufacturing footprint and adds fermentation capacity. It is intended to improve supply resilience for industrial enzyme demand while enabling more direct regional service for customers.

- November 2025: Novonesis and thyssenkrupp Uhde launched an enzymatic fat-splitting process using the Lipura Split enzyme for fatty acid production. The partnership offers an enzymatic alternative to conventional splitting routes. This change can alter the processing profile and economics for industrial oleochemical producers that use enzymes downstream.

- April 2024: dsm-firmenich announced EU regulatory approval for ProAct 360, a feed protease for use in poultry. The approval expands the company’s addressable market in regulated animal nutrition applications. It also underscores how authorizations act as a gatekeeper for scale in feed enzyme commercialization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the industrial enzymes market covers revenue earned from enzymes sold for industrial processing uses, where the enzyme acts as a catalyst in a production or treatment step, and the value is captured at the point of sale.

Scope exclusions: We exclude enzymes sold mainly for diagnostics, therapeutic use, and laboratory research, and we also exclude on-site generated enzymes not transacted commercially.

Segmentation Overview

- By Type

- Carbohydrases

- Amylases

- Cellulases

- Proteases

- Trypsins (API and Non-API)

- Other Proteases

- Lipases

- Other Types (Polymerases, Oxidases, etc.)

- Carbohydrases

- By Application

- Food Processing

- Animal Feed

- Healthcare

- Detergents and Cleaners

- Leather Processing

- Biofuels

- Textiles

- Pulp and Paper

- Cosmetics

- Other Applications

- By Geography

- Asia-Pacifc

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New-Zealand

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- Asia-Pacifc

Data Sources, Market Sizing, and Validation

Desk Research

To set the market boundaries and build an initial demand map, we start with public and official information that explains where enzymes are used and how volumes move across countries. Useful inputs include the Food and Agriculture Organization for agriculture and feed context, the US Geological Survey where mineral processing links matter, US EPA resources for environmental treatment references, and international trade statistics portals for cross-border patterns in enzyme-related product flows.

Alongside these, we review company annual reports, investor presentations, and press releases to understand capacity moves, product mix, and pricing commentary, which are then translated into sizing assumptions. Patent databases are also used to spot where activity is shifting by application area (for example, detergents, starch processing, or biofuels). For financial consistency checks, we selectively use paid subscriptions that provide standardized company financials and broader news and financials, and an import and export shipment-level database when trade signals are needed. The specific desk sources noted here are illustrative, and other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to turn the desk-built structure into a usable market model by stress-testing assumptions with people who touch pricing, formulation, and procurement decisions. We speak with manufacturers, distributors, and large end users across major consuming regions so that adoption rates, dosage ranges, and application-level splits can be corrected where secondary data is thin, and then the final totals are reconciled back to real operating conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 23% | EMEA: 31% |

| Smaller Players: 21% | Managers: 60% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enzyme demand is reconstructed from end-use output indicators and penetration assumptions, followed by conversions into value using application-appropriate pricing. In practice, we map demand to a set of use cases and then apply typical treat rates and dosage ranges (for example, in detergents and cleaning, food and beverage processing, animal feed, biofuel processing, and textiles and leather), which are then multiplied by an adjusted average selling price to reach revenue.

To keep totals realistic, the model is cross-checked with selective bottom-up approximations, such as sampling supplier revenues by application exposure, channel checks on regional pricing, and volume sanity checks using capacity announcements and utilization commentary. Where bottom-up views have gaps, the missing portion is handled through conservative scaling based on the share of the demand pool that is still uncovered, and the scaling factor is discussed with experts before being locked.

For forecasting, scenario analysis is used because industrial enzyme demand tends to move with end-use production cycles and cost-driven substitution. The key inputs we use include processed food output trends, detergent and cleaning product volumes, animal feed production and protein demand direction, biofuel blending targets and plant activity, and regional manufacturing activity signals that influence industrial throughput. Expert feedback is used to confirm which variables should lead the forecast in each region, and then assumptions are applied consistently through the forecast window.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and we look for mismatches that do not align with known end-use production patterns or price movements. Any large variance triggers a second pass on units, conversions, and currency timing, and follow-up questions are raised with interviewees where the gap is still not explained.

Before sign-off, the model and narrative go through multi-step analyst reviews so that assumptions are traceable and the math is consistent across regions and applications. The report is refreshed annually, and interim updates are made when material events occur, such as major capacity changes or sharp feedstock-driven pricing shifts. Right before delivery, a final update pass is completed so clients receive the latest consistent view.

Mordor Intelligence's Industrial Enzymes Market Size Versus Other Published Estimates

Published market sizes for industrial enzymes often do not line up because firms choose different scope lines, year labeling, and price and volume assumptions. Differences also come from how each study treats adjacent enzyme demand that sits close to industrial uses, and from how quickly the model is refreshed when end-use output shifts.

The main gap comes from whether enzyme revenue tied to non-industrial end uses is folded into the total, where Mordor Intelligence counts only commercially sold enzymes used in industrial processing steps and keeps diagnostics and therapeutic use out of scope. This tends to compress the total versus broader definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.65 B (2026) | |

| Global Consultancy A | USD 8.39 B (2025) | Uses a different base year and appears to anchor value on a 2025 estimate, which can understate the total if recent capacity additions and price resets are not carried into the starting point in the same way. |

| Industry Publisher B | USD 7.70 B (2024) | Starts from an earlier year and may apply broader average pricing and slower adoption assumptions across applications, which can reduce the sized value versus an application-mapped demand build with updated end-use output signals. |

The spread in the table is mostly explained by year choice and by how tightly industrial use is separated from nearby enzyme demand pools. When scope is kept consistent and the value build is linked back to end-use output, treat rates, and realistic pricing checks, the result becomes easier to replicate and to update as conditions change.

Key Questions Answered in the Report

How large is the industrial enzymes market in 2026?

The market is valued at USD 9.65 billion in 2026 with a 6.17% CAGR outlook to 2031.

Which enzyme type holds the largest share?

Carbohydrases led with 47.50% of 2025 revenue, driven by biofuel and bakery use.

What application segment is expanding fastest?

Food processing shows the quickest growth at a projected 7.82% CAGR to 2031.

Which region records the highest growth rate?

Asia-Pacific is forecast to grow at 6.91% CAGR through 2031 on the back of Chinese and Indian capacity additions.

Page last updated on: