Melatonin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 3.22 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

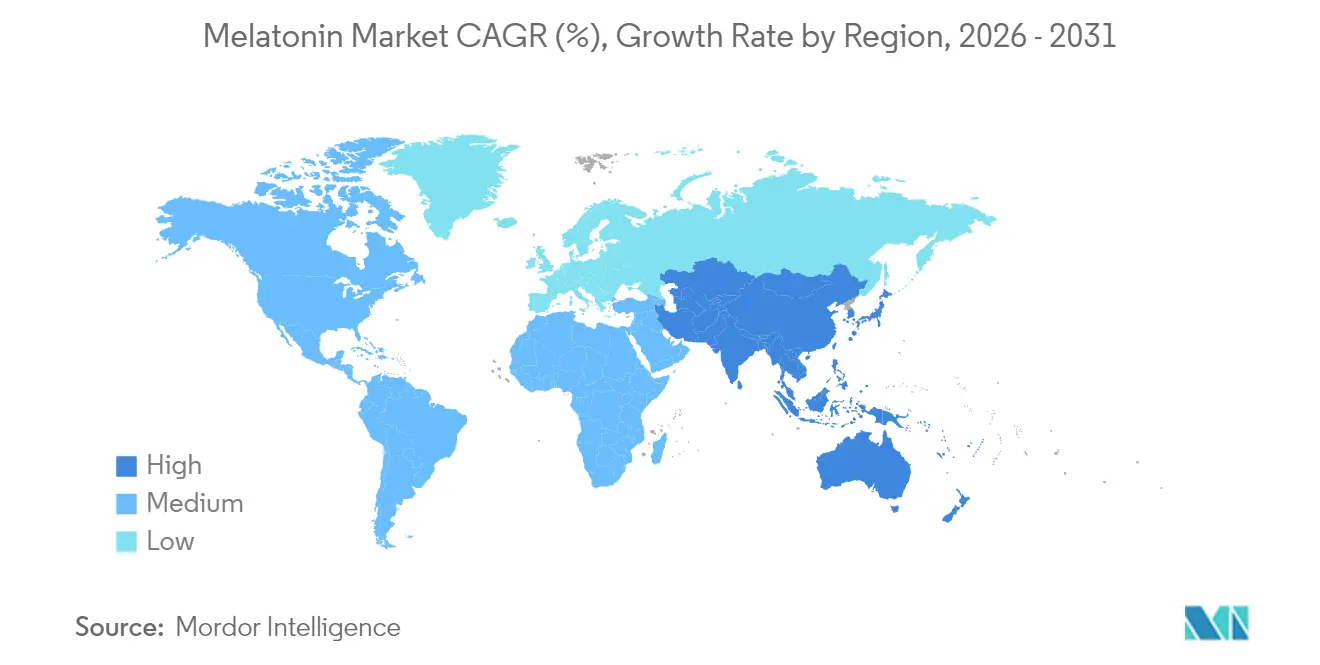

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

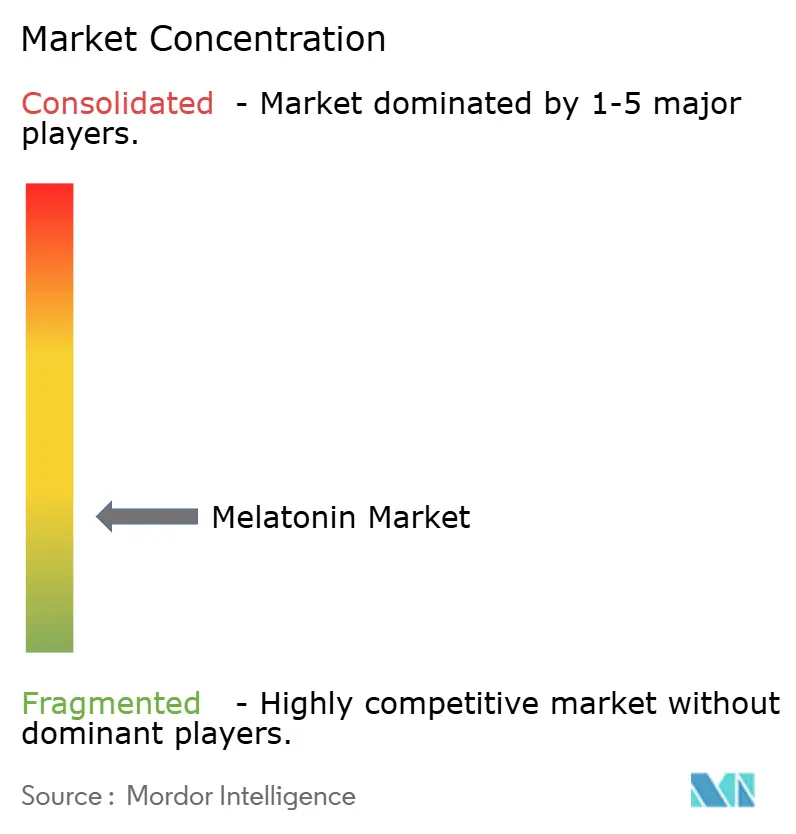

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Melatonin Market Analysis by Mordor Intelligence

The Melatonin Market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 2.07 billion in 2026 to reach USD 3.22 billion by 2031, at a CAGR of 9.28% during the forecast period (2026-2031). The expansion is propelled by prescription growth for circadian-rhythm disorders, synthetic-biology cost breakthroughs that lower manufacturing expenses, and regulatory liberalization in high-growth regions. Synthetic melatonin’s 55.67% 2024 share anchors cost efficiency, while gummies outpace tablets on the back of consumer demand for palatable dosing formats. Prescription-only pediatric protocols, orphan-drug designations, and specialized extended-release delivery systems elevate medical uptake. Meanwhile, agricultural post-harvest applications open non-traditional demand channels that diversify revenue streams within the melatonin market.

Key Report Takeaways

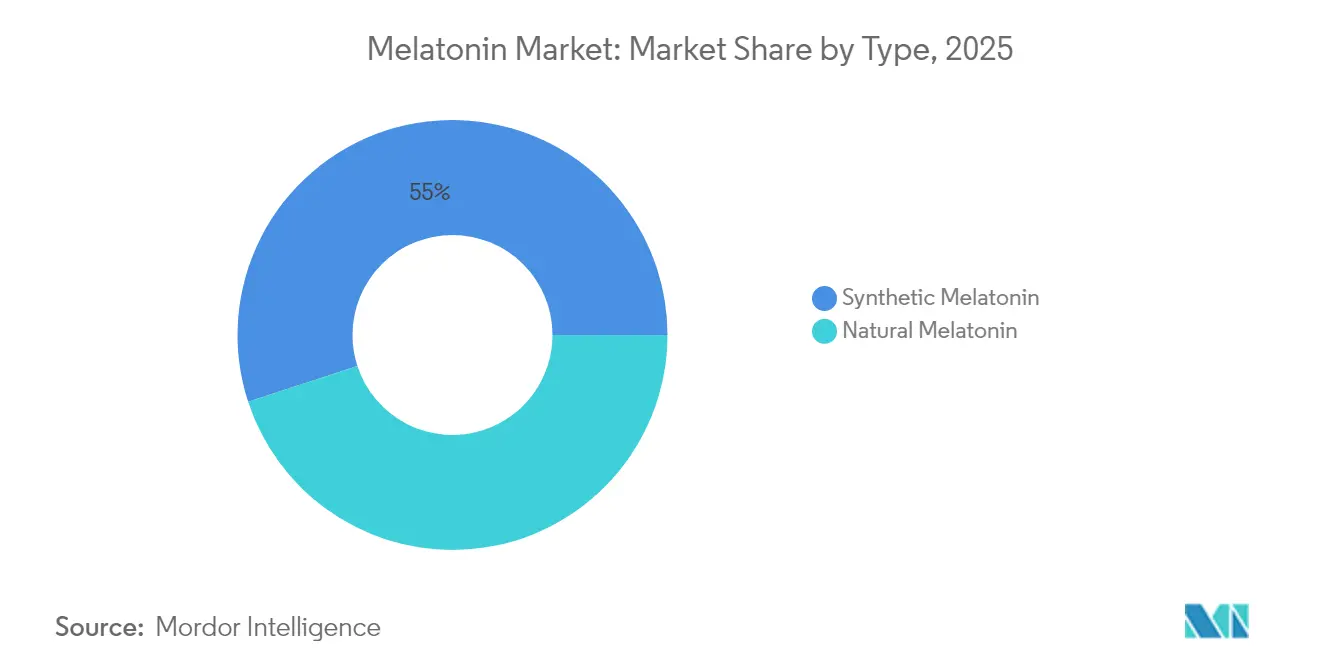

- By type, Synthetic melatonin led with 55.02% melatonin market share in 2025 and is forecast to expand at a 9.96% CAGR through 2031.

- By dosage form, Tablets retained 45.10% revenue share in 2025, while gummies recorded the fastest 9.74% CAGR through 2031.

- By formulation, Immediate-release products accounted for 63.30% of the melatonin market size in 2025; extended-release solutions are projected to rise at 10.32% CAGR to 2031.

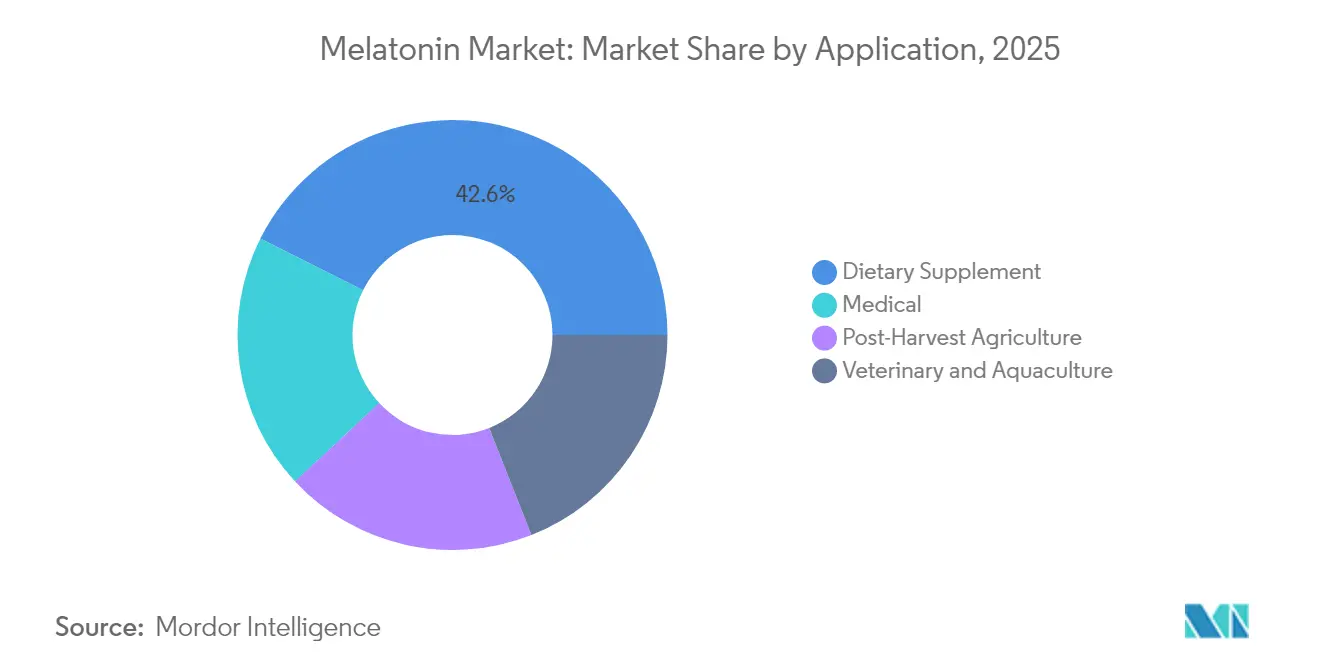

- By application, Dietary supplements captured 42.60% of the melatonin market size in 2025; medical applications post the highest 11.88% CAGR through 2031.

- By geography, North America commanded 38.20% of the melatonin market share in 2025, whereas Asia-Pacific is poised for a 9.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Melatonin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prescription uptake for circadian-rhythm disorders | 2.8% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Pediatric Atrial Septal Defect (ASD) sleep-management protocols | 1.9% | North America, EU, expanding to APAC | Long term (≥ 4 years) |

| Demand for "clean-label" plant-derived melatonin | 1.5% | North America and EU primarily | Short term (≤ 2 years) |

| Synthetic-biology cost breakthroughs | 2.1% | Global manufacturing hubs | Medium term (2-4 years) |

| Agricultural post-harvest anti-bruising use cases | 0.9% | Global agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prescription Uptake for Circadian-Rhythm Disorders

Accelerating prescription volumes validate melatonin’s transition from over-the-counter supplement to reimbursable pharmaceutical solution. Pediatric prescriptions in the United Kingdom rose 245% over nine years, mirroring FDA orphan-drug designations for non-24-hour sleep-wake disorder that expand insurance coverage pathways. European guidance now names melatonin first-line therapy for childhood sleep-onset insomnia, and products such as tasimelteon highlight pipelines targeting blind patients and shift-work populations.

Pediatric ASD Sleep-Management Protocols

Randomized trials consistently show that melatonin shortens sleep-onset latency and raises total sleep time in autism spectrum disorder cohorts with minimal adverse reactions. The prolonged-release product Slenyto earned EU approval for children with ASD, while Stanford clinical guidelines recommend 3-10 mg dosages before bedtime. This therapeutic confidence accelerates adoption across pediatric neurology practices, reinforcing long-term medical demand across the melatonin market.

Demand for “Clean-Label” Plant-Derived Melatonin

Consumers scrutinize supplement labels, spurring interest in phytomelatonin extracted from cherry, rice, and other botanical sources. Laboratory tests found 11 of 13 commercial products carried 5-68% less melatonin than indicated, motivating premium payments for traceable plant-based alternatives. Agricultural-biotech firms are engineering high-melatonin crops, while brands leverage “clean-label” credentials to differentiate in the crowded melatonin market.

Synthetic-Biology Cost Breakthroughs

Engineered Escherichia coli strains now synthesize 1.13 mg/L melatonin from L-tryptophan, lowering costs by up to 30% against chemical routes. Fermentation optimization—glucose control, nitrogen management, and pH at 6.5-7.2 pushes yields further. These efficiencies reinforce synthetic melatonin’s dominance and underpin forecast margin stability through 2030.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening maximum-dosage regulations | -1.8% | EU, expanding to North America | Short term (≤ 2 years) |

| Clinical safety concerns in long-term use | -1.2% | Global, particularly pediatric markets | Medium term (2-4 years) |

| Raw-material price spikes for indole feedstocks | -0.7% | Global manufacturing hubs, Asia-Pacific core | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Maximum-Dosage Regulations

The Council for Responsible Nutrition now requires child-deterrent packaging after pediatric emergency-room visits tied to melatonin rose 420% from 2009 to 2020[1]Council for Responsible Nutrition, “Child-Deterrent Packaging Standards,” crnusa.org. France’s ANSES caps daily dosage at 2 mg and advises high-risk groups to avoid supplements, while an emerging EU framework seeks harmonized labeling. These measures increase compliance costs and may slow new-product timelines, especially for gummy formats favored by children.

Clinical Safety Concerns in Long-Term Use

WHO VigiBase lists 35,479 adverse-event reports, with 21 potential safety signals including tic onset and growth retardation that warrant further study. Pediatric sleep specialists call for expanded sleep-hygiene programs before prescribing and push regulators to standardize long-term monitoring. Precautionary sentiment could temper high-dose formulation roll-outs and dampen growth in sensitive sub-populations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Synthetic Dominance Drives Cost Efficiency

Synthetic melatonin accounted for a 55.02% melatonin market share in 2025 as pharmaceutical buyers prioritize batch-to-batch consistency and price advantages. Synthetic-biology gains, such as E. coli fermentation that halves manufacturing costs, support a 9.96% CAGR outlook, maintaining scale economies integral to the melatonin market. Natural melatonin, although pricier, appeals to consumers pursuing “clean-label” positioning and may see upside as agricultural biotechnology improves crop yields.

The melatonin industry continues investing in precision fermentation lines that limit solvent use and shrink carbon footprints. Regulatory bodies, keen on sustainability metrics, increasingly view microbial methods favorably. Meanwhile, phytomelatonin supply chains experiment with enzyme-assisted extraction to lift purity, yet still struggle to match synthetic volumes.

By Dosage Form: Gummies Disrupt Traditional Tablets

Tablets delivered 45.10% of 2025 revenue as clinicians prefer fixed-dose accuracy and established pharmacopoeia standards. Gummies, however, grow 9.74% annually, propelled by flavor, chewability, and rising pediatric demand. The melatonin market size for gummies is on track to double by 2030, though new child-proof mandates elevate packaging expenses.

Liquid drops and capsules meet niche needs such as titratable pediatric dosing and vegetarian shell preferences. Extended-release tablets, featuring dual-layer designs, mitigate melatonin’s short half-life to enhance sleep maintenance and could shift share away from immediate-release presentations.

By Formulation: Extended-Release Innovation Accelerates

Immediate-release products held 63.30% melatonin market size in 2025 yet extended-release lines chart 10.32% CAGR as pharmacokinetic enhancements gain prescriber confidence. Bilayer tablets achieve 7-hour plasma coverage with a peak at 3 hours; clinical data show improved sleep maintenance relative to quick-release counterparts.

Nanocarriers and ocular gels surface in research and development pipelines, seeking higher bioavailability for neuroprotective indications. Cost remains a hurdle, but price premiums are offset by reduced dosing frequency and better compliance. As patents on delivery technology accumulate, innovators can shield margins while broadening therapeutic scope inside the melatonin market.

By Application: Medical Segment Outpaces Supplements

Dietary supplements commanded 42.60% of melatonin market size in 2025, sustained by easy retail access and wellness trends. Yet medical prescriptions grow at 11.88% yearly, underpinned by FDA orphan-drug incentives and ASD-focused formulations that outperform sedatives on efficacy and safety.

Veterinary reproductive aids and aquaculture stress reducers gain traction, while post-harvest crop protection introduces melatonin into ag-input portfolios. Supplement makers confront potency deviations and stricter testing, nudging a segment shift toward clinically validated, higher-margin pharmaceutical channels.

Geography Analysis

North America retained a 38.20% melatonin market share in 2025, thanks to mature retail infrastructure and payer acceptance of prescription formulations. Rising pediatric prescribing and OTC uptake sustain steady revenue, though new CRN labeling rules raise cost overhead. Extended-release innovations and ASD protocols are key catalysts that help offset compliance spend.

Asia-Pacific is the fastest-growing territory, posting a 9.88% CAGR. China’s revised health-food code now fast-tracks melatonin claims for sleep support, spurring domestic brand launches and cross-border e-commerce. Japan links higher dietary melatonin intake to lower liver cancer risk, feeding functional-food product pipelines. Regulatory openness plus middle-class wellness spending positions the region as the next volume driver within the melatonin market.

Europe presents a mixed picture: Germany and Austria welcomed pediatric ADHD formulation Mellozzan, while France’s ANSES remains cautious, capping dosage and advising susceptible groups to abstain. New Zealand’s 2025 OTC decision, allowing up to 5 mg pharmacy sales, signals gradual liberalization in other OECD states.

Competitive Landscape

The melatonin market features high fragmentation: legacy supplement houses, prescription-drug developers, and synthetic-biology startups all contest for share. Natrol dominates U.S. retail with cGMP plants and rigorous purity testing, supporting brand trust among pharmacists and consumers. Nature’s Bounty leverages omnichannel distribution and gummy innovations, yet faces added compliance costs under child-proof rules.

Melatonin Industry Leaders

Natrol

Nature’s Bounty

Church & Dwight Co., Inc.

Jamieson Vitamins

Pharmavite

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Natrol launched Time Release Melatonin gummies in 3 mg and 10 mg strengths featuring dual-action delivery to aid sleep onset and maintenance.

- June 2023: Nature’s Bounty introduced Sleep3 Gummies, combining L-theanine, quick-release, and time-release melatonin for adults with occasional sleeplessness.

Global Melatonin Market Report Scope

Melatonin is a natural adrenaline produced by the pineal gland to regulate the body's circadian cycle. Most sleep-related diseases like insomnia, interrupted sleep phase syndrome, jet lag, and others are treated with melatonin supplementation. The melatonin market is segmented by type, application, and geography. By type, the market is segmented into natural melanin and synthetic melanin. By application, the market is segmented into medical, and dietary supplements. The report also covers the market size and forecasts for extruded polystyrene in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Natural Melatonin |

| Synthetic Melatonin |

| Tablets |

| Capsules |

| Gummies |

| Liquid Drops |

| Others |

| Immediate-Release |

| Extended-Release |

| Medical |

| Dietary Supplement |

| Veterinary and Aquaculture |

| Post-Harvest Agriculture |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Natural Melatonin | |

| Synthetic Melatonin | ||

| By Dosage Form | Tablets | |

| Capsules | ||

| Gummies | ||

| Liquid Drops | ||

| Others | ||

| By Formulation | Immediate-Release | |

| Extended-Release | ||

| By Application | Medical | |

| Dietary Supplement | ||

| Veterinary and Aquaculture | ||

| Post-Harvest Agriculture | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the melatonin market?

The melatonin market stands at USD 2.07 billion in 2026 and is forecast to reach USD 3.22 billion by 2031.

Which segment is growing fastest within the melatonin market?

Medical applications post the highest 11.88% CAGR as prescriptions rise for circadian-rhythm and pediatric ASD disorders.

How large is the synthetic melatonin segment?

Synthetic variants hold 55.02% melatonin market share in 2025 thanks to cost-efficient microbial production advances.

Which region will lead growth through 2031?

Asia-Pacific is projected to expand at a 9.88% CAGR on the back of regulatory liberalization and growing middle-class supplement demand.

What key regulation will shape product strategy?

Council for Responsible Nutrition rules mandating child-deterrent packaging and stricter labeling will influence new-product costs and formulation choices in North America and potentially Europe.

Page last updated on: