Cyprus ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 1.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cyprus ICT Market Analysis by Mordor Intelligence

The Cyprus ICT Market size was valued at USD 0.91 billion in 2025 and is estimated to grow from USD 0.93 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 1.92% during the forecast period (2026-2031).

The measured expansion reflects government-led modernization funded by the Digital Agenda 2030, continued fibre-to-the-home and 5G build-outs, and an ambitious EU eIDAS roll-out that elevates demand for qualified trust services. Investment momentum is strongest in IT services and cybersecurity, while hardware refresh cycles remain muted as enterprises migrate to cloud subscriptions. Competitive intensity is heightened by Cyta’s network-first strategy, PrimeTel’s submarine-cable play, and a cluster of global gaming studios that anchor demand for low-latency infrastructure. Key risks for the Cyprus ICT market include a limited domestic DevOps talent pool, high electricity tariffs for data-center operators, and a two-tier connectivity gap between urban and rural areas.

Key Report Takeaways

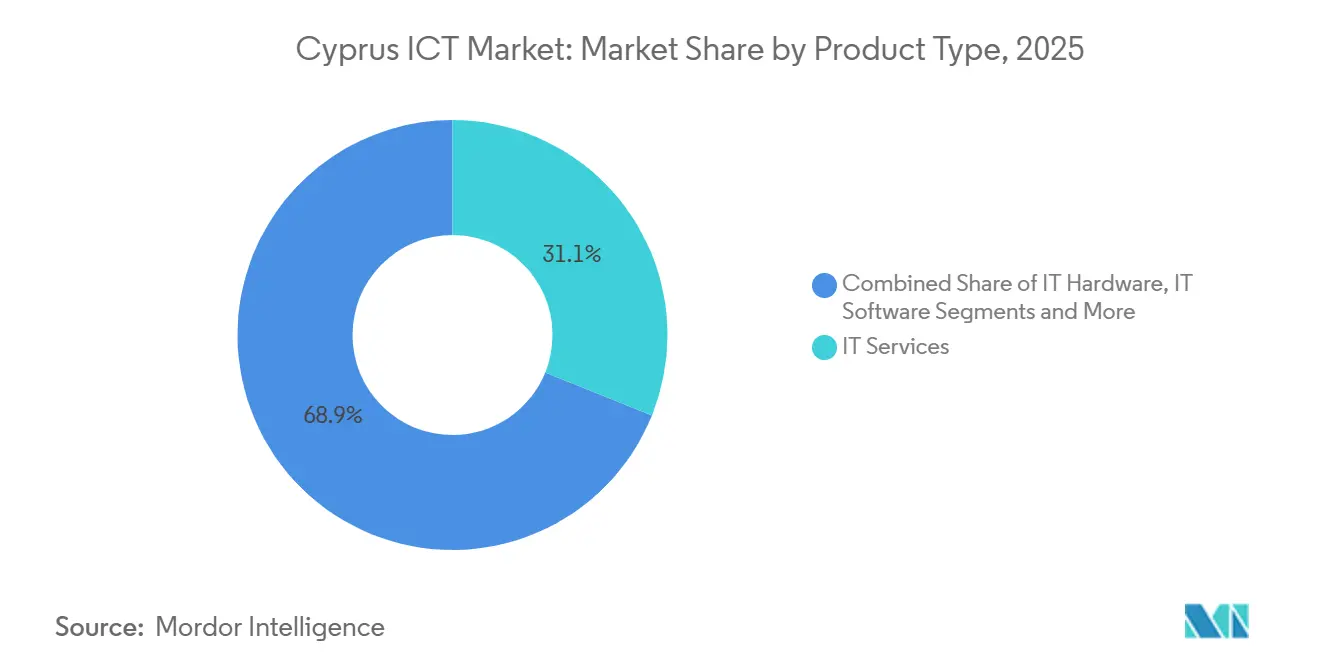

- By product type, IT services led with 31.10% revenue share in 2025, while IT security is forecast to post the fastest 3.50% CAGR through 2031.

- By enterprise size, large enterprises held 63.20% of spending in 2025, yet small and medium enterprises are projected to expand at a 2.10% CAGR to 2031.

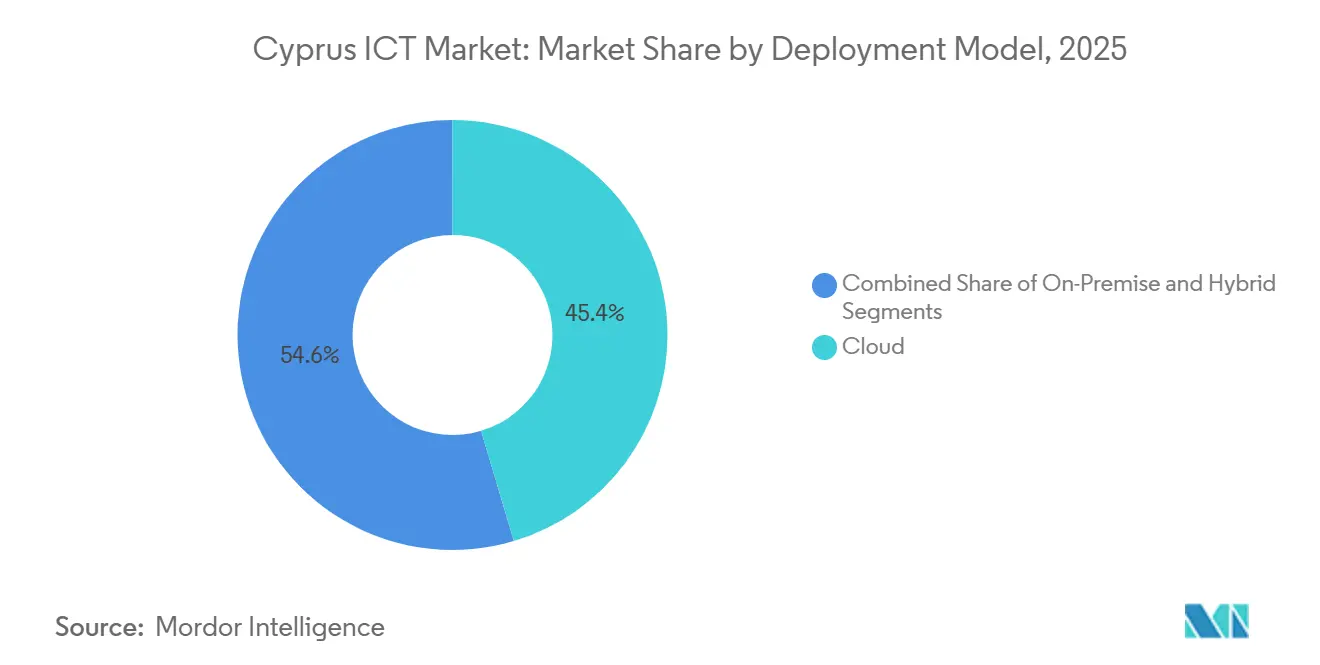

- By deployment model, cloud captured 45.39% share of the Cyprus ICT market size in 2025 and is advancing at a 2.88% CAGR through 2031.

- By industry vertical, government and public administration accounted for a 24.30% share of the Cyprus ICT market size in 2025, while gaming and esports is growing at a 4.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Cyprus ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed Cyprus Digital Agenda 2030 funding commitments | +0.5% | Cyprus-wide, focus on Nicosia and Limassol | Medium term (2-4 years) |

| Accelerated fibre-to-the-home roll-out and 5G spectrum auctions | +0.4% | Urban and suburban zones | Short term (≤ 2 years) |

| EU eIDAS-driven demand for trust and cyber-security services | +0.3% | Nationwide cross-border use cases | Short term (≤ 2 years) |

| Near-shoring of Mediterranean disaster-recovery data centers | +0.2% | Nicosia, Limassol, Larnaca | Long term (≥ 4 years) |

| Tourism industry pivot to smart-experience platforms | +0.2% | Coastal resort zones | Medium term (2-4 years) |

| Shipping and maritime digital twin adoption in Limassol Port | +0.1% | Limassol Port corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Cyprus Digital Agenda 2030 Funding Commitments

The EUR 988.4 million Digital Agenda represents 2.96% of national GDP and lifts public demand for cloud-based e-government services. Annual allocations to the Deputy Ministry rise to EUR 172.8 million in 2026, encouraging procurement of single-sign-on platforms, open-data portals, and network upgrades. Connectivity receives 60% of the budget, ensuring gigabit targets advance even as rural builds slip into 2028 because of right-of-way disputes. Skills funding captures only 15% of the envelope, implying network capacity could outstrip workforce readiness in the short run. As infrastructure rolls out faster than talent upskilling, managed-service providers gain an opening to bridge skills gaps for the Cyprus ICT market.

Accelerated Fibre-to-the-Home Roll-out and 5G Spectrum Auctions

Cyta reached 100% 5G population coverage in 2024 and extended fibre to 77.1% of premises, backed by more than USD 238 million annual capital outlays[1]Source: Cyta, “Annual Report 2022,” cyta.com.cy. PrimeTel’s HAWK cable adds 4 Tbps of external capacity that positions Cyprus as a Mediterranean transit node[2] Source: PrimeTel, “HAWK Submarine Cable,” primetel.com.cy . Nonetheless, 76% of fibre coverage is still concentrated in major cities, leaving rural municipalities on legacy co-axial networks. The Cyprus ICT market benefits from superior urban bandwidth, yet the rural lag restrains use cases that rely on symmetrical uploads such as cloud back-ups and real-time collaboration.

EU eIDAS-Driven Demand for Trust and Cyber-Security Services

Notification of the national eID at High assurance level catalyzes spending on hardware security modules, ISO 27001 data centers, and managed SOC offerings. Digital Identity Wallets mandated for 2026 accelerate integration work for mobile credentials and biometric modules. Enterprises unable to staff 24/7 detection teams contract MSSPs, expanding the security pie inside the Cyprus ICT market while tightening compliance deadlines under NIS2.

Near-Shoring of Mediterranean Disaster-Recovery Data Centers

Sixteen colocation sites now operate on the island, many marketed as secondary sites for European banks and fintechs seeking seismic diversification. New submarine paths and modest corporate tax rates improve the value proposition, although electricity costs stay among the highest in the EU and lift total ownership costs. Data-center investment therefore skews toward low-duty-cycle disaster recovery instead of compute-intensive AI workloads, a nuance that tempers long-term upside yet still contributes incremental growth for the Cyprus ICT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Constrained domestic talent pool in advanced cloud DevOps | −0.3% | Nicosia and Limassol tech hubs | Medium term (2-4 years) |

| Fragmented SME base with low ICT budgets | −0.2% | Nationwide retail and hospitality segments | Short term (≤ 2 years) |

| Legacy co-ax infrastructure outside urban corridors | −0.1% | Mountainous communities | Long term (≥ 4 years) |

| Elevated cost of electricity for data-center operations | −0.2% | All island data centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Constrained Domestic Talent Pool in Advanced Cloud DevOps

Only 49.5% of citizens had basic digital skills in 2024, and 89% of firms cited staff shortages as the top barrier to digital adoption. Government training grants remain fragmented across agencies, so private programs like Wargaming Forge fill gaps only within the gaming vertical. Enterprises in the Cyprus ICT market backfill shortages with remote contractors, yet higher wage bids from distributed teams inflate project costs. The scarcity also nudges firms toward low-code platforms, potentially reducing long-term flexibility as vendor lock-in rises.

Fragmented SME Base with Low ICT Budgets

SMEs represent the numeric majority of Cypriot businesses yet spend unevenly on technology. Although 94% invested in digital tools during 2024, budgets remain modest and episodic[3]Source: Eurostat, “Electricity Prices for Non-household Consumers H1 2025,” ec.europa.eu . Many rely on manual workflows and view cloud subscriptions as operating expenses rather than strategic investments. Voucher schemes and EU co-funded grants have begun to shift perceptions, but uptake is slow outside tourism and retail. Limited pooled demand keeps average deal sizes small, lowering the near-term revenue ceiling for vendors targeting the Cyprus ICT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services and Security Take Divergent Paths

IT services held the largest 31.10% Cyprus ICT market share in 2025 as public digitalization and tourism upgrades fueled system-integration contracts. IT security is forecast to record a 3.50% CAGR through 2031, underlining rising compliance outlays for eIDAS and NIS2. Hardware demand stays muted because cloud uptake reduces on-premise server refreshes, while software subscriptions in ERP and CRM sustain mid-single-digit growth. Fibre and 5G roll-outs keep communication services revenue flat as legacy voice declines offset data gains.

Enterprises continue reallocating budgets away from capital purchases toward outcomes-based managed services. Gaming studios in Limassol and Nicosia need specialized support for multiplayer orchestration and anti-cheat analytics, spawning niche consultancies. As public-sector contracts bundle connectivity, cloud access, and SOC monitoring, integrators with multi-disciplinary skill sets consolidate share inside the Cyprus ICT market.

By End-User Enterprise Size: SME Digitalization Accelerates from a Low Base

Large enterprises controlled 63.20% of 2025 spending, but SME outlays will climb faster at a 2.10% CAGR. Voucher incentives and simplified cloud on-boarding schemes reduce barriers, yet 70% of smaller firms still grapple with network-quality issues and 87% cite energy costs as restraints. Low-code SaaS remains the preferred entry point because it minimizes upfront cash.

A bifurcated pattern persists. Big organizations negotiate volume discounts and deploy hybrid architectures, whereas SMEs depend on turnkey cloud packages that trade customizability for speed. As skills initiatives scale, broader SME adoption could unlock a sizeable incremental pool, positioning the Cyprus ICT market for steadier gains beyond 2028.

By Deployment Model: Cloud Extends Lead Despite Data-Sovereignty Concerns

Cloud models already account for 45.39% of spending and will rise at a 2.88% CAGR. High electricity tariffs dilute on-premise economics, tipping cost calculus toward pay-as-you-go resources even for conservative sectors. Hybrid remains attractive for latency-sensitive or regulated workloads, yet EU Data Act portability rules lower switching costs and embolden multi-cloud strategies.

Gaming companies rely on overseas hyperscale regions for real-time servers, so lower submarine-cable latency could spur local edge-deployment opportunities. As fibre routes diversify and direct southern-Europe links improve, the Cyprus ICT market may evolve into an edge node for ultralow-latency workloads.

By End-User Industry Vertical: Government Anchors Demand, Gaming Drives Growth

Government and public administration contributed 24.30% of 2025 value through large digital-identity, broadband, and open-data projects. Gaming and esports is projected as the fastest climber with a 4.20% CAGR, supported by Wargaming, GDEV, and other studios scaling headcount and revenue. BFSI invests heavily in core banking refreshes and PSD2 compliance, while retail modernizes omnichannel stacks and logistics analytics.

Energy utilities channel outlays into smart-grid telemetry and advanced metering to absorb renewable generation. Healthcare slowly advances electronic records integration, limited by legacy system fragmentation. Maritime digital twins in Limassol port remain pilot-scale but indicate a future vertical upswing for the Cyprus ICT market once smart-port mandates mature.

Geography Analysis

ICT spending is heavily concentrated in the Nicosia-Limassol-Larnaca corridor, which accounted for roughly 85% of 2025 outlays. Nicosia hosts most government agencies and data centers, while Limassol has become the gaming and fintech nexus thanks to deep talent pools and port logistics. Larnaca positions itself as a disaster-recovery hub with new submarine-cable landing stations and lower real-estate prices.

Peripheral regions struggle with connectivity gaps. Rural SMEs in Troodos and the Paphos hinterland endure upload speeds below 30 Mbps, undermining cloud adoption and remote work. The EUR 72.5 million National Broadband Plan aims to extend fibre nationally by 2027, but timeline slippage could widen the digital divide.

Tourism zones along Ayia Napa and Protaras already deploy IoT guest-experience platforms that demand robust Wi-Fi back-haul, reinforcing the connectivity imperative. High power tariffs further complicate rural data-center economics, explaining why colocation clusters remain near urban fiber POPs. Over time, improved renewable integration and grid interconnections could balance regional disparities in the Cyprus ICT market.

Competitive Landscape

Cyta retains an estimated 40-45% share of telecom revenue by combining 100% 5G coverage with 77.1% fibre reach and multi-year managed-service bundles. PrimeTel differentiates through the HAWK submarine cable and an ISO 27001 data center, appealing to global enterprises needing low-latency Mediterranean routes.

Cablenet focuses on residential broadband and small-business plays in secondary cities. International software leaders such as Microsoft, Oracle, SAP, and Cisco sell through local integrators Logicom and Epic, while boutique firms address gaming-specific infrastructure and analytics.

White-space opportunities emerge in vertical SaaS for hospitality, maritime logistics, and gaming back-end services. Cybersecurity faces intense vendor jockeying because eIDAS and NIS2 compress buying cycles and expand compliance scope. Managed SOC offerings gain traction among mid-market firms that cannot staff internal teams. As talent scarcity endures, vendors able to bundle training, implementation, and support should keep winning share inside the Cyprus ICT market.

Cyprus ICT Industry Leaders

Cyprus Telecommunications Authority

Epic Ltd

Cablenet Communication Systems Public Company Ltd

PrimeTel Public Company Ltd

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Deputy Ministry confirmed EUR 172.8 million 2026 budget allocation, a 3.2% rise over 2025, sustaining Digital Agenda road-map funding.

- November 2025: Cyta announced a power purchase agreement targeting 100% renewable energy coverage for network and data-center facilities by 2027.

- July 2025: Khazna Data Centers signed an agreement to explore a 20 MW hyperscale campus in Larnaca, citing submarine-cable density and corporate-tax certainty.

- March 2025: The Energy Regulatory Authority finalized network-tariff rules that add fixed fees on self-generation, impacting on-site solar economics for data centers.

Cyprus ICT Market Report Scope

ICT, an umbrella term encompassing Information Technology (IT), covers a wide array of communication technologies. These include wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and various media applications. Collectively, these technologies empower users to store, access, transmit, retrieve, and manipulate information in digital formats.

The Cyprus ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, and Communication Services), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (On-premise, Cloud, and Hybrid), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, and Gaming and Esports). Market Forecasts are Provided in Terms of Value (USD).

| IT Hardware |

| IT Software |

| IT Services |

| IT Infrastructure |

| IT Security |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Products Type | IT Hardware |

| IT Software | |

| IT Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services | |

| By End-User Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-premise |

| Cloud | |

| Hybrid | |

| By End-User Industry Vertical | Government and Public Administration |

| BFSI | |

| Energy and Utilities | |

| Retail, E-commerce and Logistics | |

| Manufacturing and Industry 4.0 | |

| Healthcare and Life Sciences | |

| Oil and Gas (Up-, Mid-, Down-stream) | |

| Gaming and Esports | |

| Other Verticals |

Key Questions Answered in the Report

How large will the Cyprus ICT market become by 2031?

The market is expected to reach USD 1.02 billion by 2031 after expanding at a 1.92% CAGR over 2026-2031.

Which segment is growing the fastest within Cyprus technology spending?

Gaming and esports leads with a projected 4.20% CAGR, outpacing all other verticals through 2031.

What share of spending do large enterprises command?

Large enterprises accounted for 63.20% of 2025 outlays, reflecting strong budgets in government, banking, and gaming.

Why are electricity costs a concern for data-center investors?

Non-recoverable taxes push industrial electricity tariffs to the second-highest level in the EU, eroding operating margins for colocation sites.

Page last updated on: