Greece ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

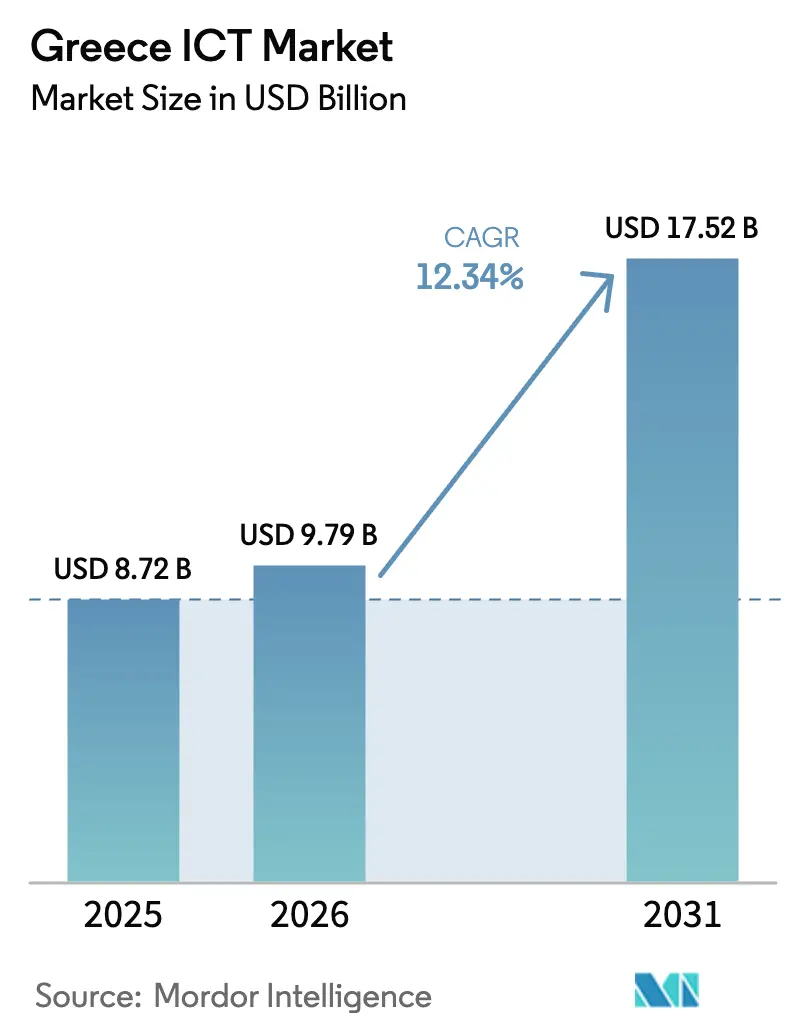

| Base Year Market Size (2025) | USD 8.72 Billion |

| Market Size (2026) | USD 9.79 Billion |

| Market Size (2031) | USD 17.52 Billion |

| Growth Rate (2026 - 2031) | 12.34% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Greece ICT Market Analysis by Mordor Intelligence

The Greece ICT market size is expected to grow from USD 8.72 billion in 2025 to USD 9.79 billion in 2026 and is forecast to reach USD 17.52 billion by 2031 at 12.34% CAGR over 2026-2031.

The growth pace exceeds the wider European average because Greece channels 21.4% of its EUR 36.61 billion (USD 24.98 billion) Recovery and Resilience Facility allocation into digital projects, accelerating broadband, cloud, and e-government rollouts[1]European Commission, “Greece's Recovery and Resilience Plan,” commission.europa.eu. Telecommunications infrastructure upgrades, the arrival of hyperscale data centers, and mandatory e-invoicing regulation combine to unlock fresh demand from both enterprises and consumers. International cloud providers invest nearly USD 2 billion in local facilities, shortening latency and relaxing data-sovereignty concerns, while domestic operators push fiber and 5G deeper into rural areas to capture pent-up connectivity needs. At the same time, a maturing startup ecosystem supplies specialized fintech, martech, and AI solutions that help local firms modernize customer engagement and internal workflows.

Key Report Takeaways

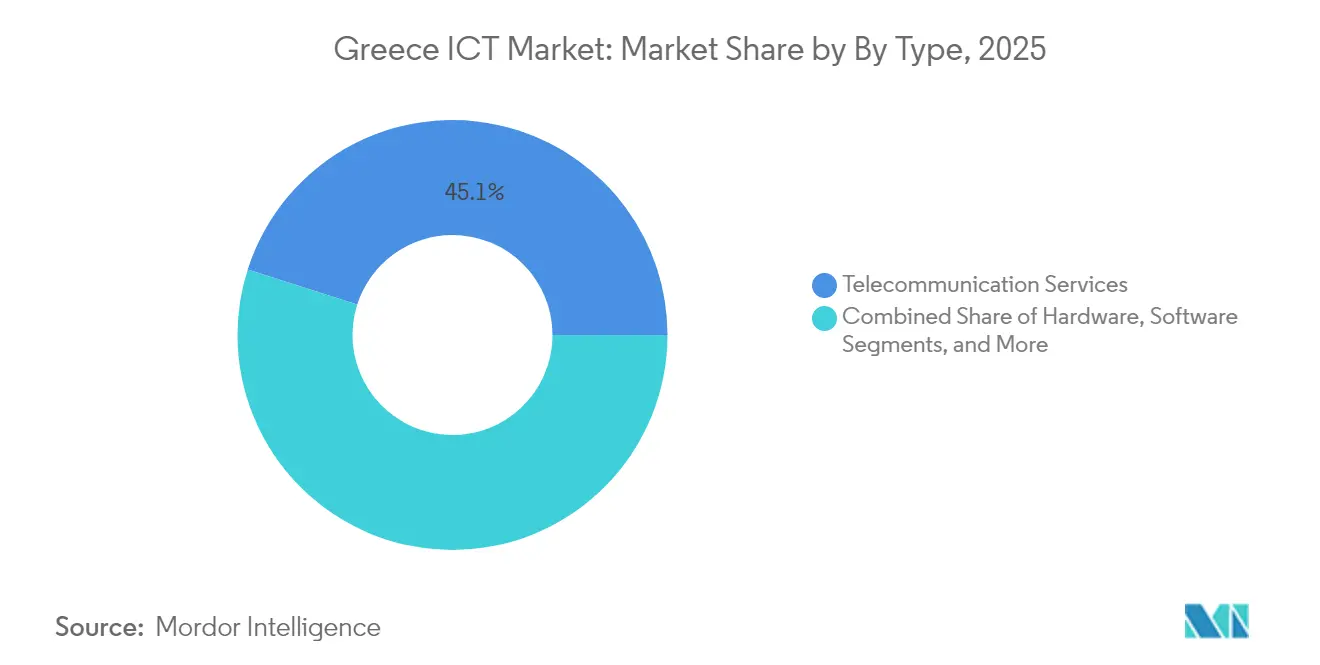

- Telecommunications services led with 45.07% of the Greece ICT market share in 2025.

- Cloud services are projected to grow at a 12.19% CAGR through 2031, the fastest among all service groups.

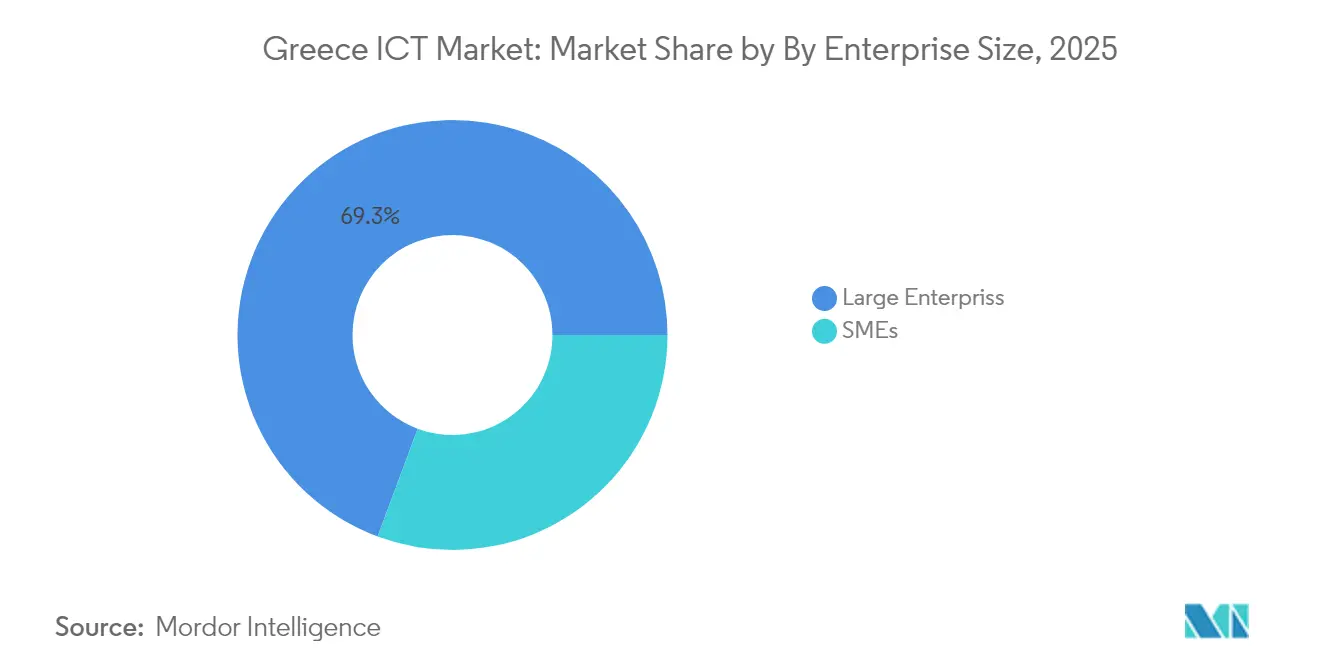

- Large enterprises commanded 69.34% share of the Greece ICT market size in 2025 while small and medium enterprises are advancing at an 10.72% CAGR to 2031.

- Government and public services accounted for 26.18% of the Greece ICT market size in 2025 and retail and e-commerce are expanding at a 13.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G roll-out and private-network pilots | +2.1% | National, with early gains in Athens, Thessaloniki, Patras | Medium term (2-4 years) |

| EU-funded Recovery and Resilience grants for digitalisation | +3.2% | National, concentrated in public sector and rural areas | Short term (≤ 2 years) |

| Near-shoring of pan-European data-centre capacity into Greece | +1.8% | Attica region, with spillover to Northern Greece | Long term (≥ 4 years) |

| Scale-up of Greek start-ups in fintech and mar-tech | +1.4% | Athens metropolitan area, expanding to Thessaloniki | Medium term (2-4 years) |

| Mandatory e-invoicing and e-books for all enterprises (2025) | +2.3% | National, with higher impact on SMEs | Short term (≤ 2 years) |

| Rising demand for sovereign-cloud and cyber-sovereignty solutions | +1.7% | Government sector and critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Roll-out and Private Network Pilots

Greece achieved 76.4% 5G availability by Q2 2025, positioning among Europe's leading markets despite infrastructure legacy challenges.[2]Ookla. "5G Coverage in Europe: Progress Toward Goals Amid Lingering Disparities." July 17, 2025. https://www.ookla.com/articles/europe-5g-q2-2025 Vodafone Greece's EUR 1 billion (USD 1.09 billion) network expansion commitment through 2029 catalyzes enterprise adoption, particularly in manufacturing and logistics sectors, where private 5G networks enable Industry 4.0 applications. The 700 MHz and 3.6 GHz spectrum assignments reach 100% allocation, creating a foundation for mission-critical applications in public safety and emergency services. Private network deployments in ports, airports, and industrial complexes generate premium revenue streams for operators while addressing sovereignty concerns that limit multinational cloud adoption. OTE Group's fiber-to-the-home expansion targeting 2.1 million premises by end-2025 provides essential backhaul infrastructure, positioning Greece as a Mediterranean connectivity hub for North Africa and Middle East traffic routing.

EU-funded Recovery and Resilience Grants for Digitalisation

The EUR 36.61 billion (USD 39.8 billion) Recovery and Resilience Facility allocation transforms Greece's digital infrastructure landscape, with 21.4% dedicated to digital transformation initiatives representing the highest sectoral concentration among EU member states. Public sector digitization projects worth EUR 7.7 billion (USD 8.4 billion) under the Greece 2.0 program accelerate cloud migration and interoperability platform development, creating downstream demand for systems integration and cybersecurity services[3]U.S. Department of Commerce. "Greece Digital Transformation plan." December 6, 2022. https://www.trade.gov/market-intelligence/greece-digital-transformation-plan. SME digital voucher programs targeting 100,000 enterprises generate immediate software licensing and consulting revenues, while educational technology initiatives providing IT devices to 500,000 students from low-income families expand the consumer electronics market. The funding structure's emphasis on measurable milestones and digital performance indicators creates accountability frameworks that ensure sustained technology adoption beyond initial implementation phases. Agricultural digitization projects covering 520+ initiatives demonstrate sector-specific transformation potential, establishing templates for industry-vertical solutions across traditional economic sectors.

Near-shoring of pan-European data-center capacity into Greece

Hyperscalers allocate more than USD 2 billion to Attica and Paiania, attracted by the country’s crossroads location between Europe, Asia, and Africa. Microsoft’s three-facility campus alone will add 300 direct jobs and anchor a local ecosystem of managed-service and cybersecurity partners. Data4 and Lamda Hellix add a multi-tenant space that shortens latency for Balkan and Eastern-Mediterranean clients, enabling compliance-friendly regional cloud zones. Submarine cables such as BlueMed land in Crete and Attica, giving operators diverse routes to Marseille, Palermo, and Tel Aviv. Energy-efficient designs tapping photovoltaic arrays mitigate Greece’s higher electricity prices, turning sustainability into a procurement differentiator for carbon-conscious multinationals.

Scale-up of Greek startups in fintech and martech

Venture funding for Greek startups hit EUR 555 million in 2024, 78% from foreign investors enticed by local engineering talent and lower burn rates than Western Europe. Viva Wallet’s partial sale to JP Morgan for EUR 700 million set a valuation benchmark that validates exit potential for founders and VCs. Conversational-AI vendor Moveo.AI raised EUR 2.3 million to commercialize multilingual customer-service bots, illustrating momentum toward verticalized enterprise applications. Government policies granting angel-investor tax relief and fast-track visas broaden the funnel of early-stage capital and specialized talent. As these startups productize analytics, payment gateways, and advertising-technology stacks, local retailers and banks gain easier access to modern digital-engagement tools without importing expensive bespoke solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population limiting skilled ICT workforce | -2.8% | National, acute in rural areas and smaller cities | Long term (≥ 4 years) |

| Protracted public-sector procurement cycles | -1.5% | Government and public services sector | Medium term (2-4 years) |

| High energy-cost volatility affecting data-centre OPEX | -1.2% | Attica and major metropolitan areas | Short term (≤ 2 years) |

| Persisting regional digital-divide (islands vs mainland) | -0.9% | Greek islands and remote rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population Limiting Skilled ICT Workforce

Greece faces the EU's most severe ICT specialist shortage, with only 2.4% of the workforce employed in technology roles compared to the 4.3% EU average, while demographic trends exacerbate talent scarcity as the working-age population contracts[4]Eurostat. "ICT specialists in employment." May 24, 2024. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=ICT_specialists_in_employment. The Federation of Hellenic Information Technology and Communications Enterprises projects a deficit of 52,000-76,000 qualified professionals by 2030, as universities produce only 64,000-68,000 graduates against demand for 120,000-140,000 new hires. The Thessaly region experiences the most acute shortage, with ICT vacancies 467% above average job categories, forcing companies to compete aggressively for limited talent pools through salary inflation and international recruitment. The skills gap particularly impacts emerging technologies including artificial intelligence, cybersecurity, and cloud architecture, where specialized expertise commands premium compensation that strains SME technology budgets. Government initiatives, including the National Skills Strategy and EU Blue Card programs, attempt to address shortfalls through foreign worker attraction, but bureaucratic complexities limit program effectiveness in meeting immediate industry needs.

High Energy Cost Volatility Affecting Data Center OPEX

Athens electricity prices reached EUR 82.89 per MWh (USD 90.1 per MWh) in 2025, representing a 27% increase that significantly impacts data center operational economics where energy costs constitute 30-60% of total expenses. The volatility creates planning challenges for hyperscale operators who require predictable cost structures for long-term capacity investments, while cooling systems in Greece's Mediterranean climate consume disproportionate energy compared to Northern European facilities. Data center operators increasingly integrate solar photovoltaic systems to achieve energy independence, with Microsoft's Attica facilities designed for near-complete renewable energy self-sufficiency, though initial capital requirements exceed EUR 100 million (USD 109 million) per facility. Grid stability concerns during peak summer months force operators to maintain expensive backup power systems, while renewable energy certificate costs add regulatory compliance expenses that smaller colocation providers struggle to absorb. The energy challenge paradoxically creates competitive advantages for efficient operators who achieve lower power usage effectiveness ratios, potentially consolidating market share among technologically advanced facilities while constraining expansion of legacy infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Telecommunications services anchor connectivity while cloud accelerates adoption

Telecommunications services contributed 45.07% to the Greece ICT market share in 2025, underscoring their foundational role in linking households, enterprises, and data-center backbones. OTE Group’s adjusted EBITDA rose 1.8% to EUR 159.4 million in Q1 2025, powered by 430,000 fiber-to-the-home clients and modest mobile-ARPU gains. Alongside mobile data, fixed broadband upgrades stimulate over-the-top video and cloud backup services that ride the same pipes, turning bandwidth into a cross-sell platform. Meanwhile, cloud services record the fastest trajectory, expanding at a 12.19% CAGR as Microsoft, AWS, and Data4 open local availability zones that shrink latency to single-digit milliseconds. The hybrid pattern emerges: financial institutions and government agencies keep sensitive workloads in private racks, but offload dev-test, analytics, and DR capacity to public cloud nodes, softening capex budgets.

Hardware outlook stabilizes as mandated fiscal devices and POS upgrades spur volume orders from 100,000 merchants before mid-2025. Software growth skews toward subscription models as e-invoicing and myDATA rules compel businesses to implement compliant ERP, accounting, and tax-reporting modules. IT services pivot from traditional break-fix to multi-cloud consulting, managed detection and response, and compliance auditing prompted by the NIS 2 Directive. Collectively, these shifts lift average revenue per user, diversify operator income streams beyond connectivity, and give digital-native startups API hooks into core network functions.

By Enterprise Size: Vouchers and SaaS democratize technology for SMEs

Large enterprises still account for 69.34% of the Greece ICT market size, reflecting their scale, multinational orientation, and early adoption of ERP, analytics, and cybersecurity stacks Flagship projects include the Hellenic Electricity Distribution Network Operator’s smart-grid rollout and National Bank of Greece’s shift to multicloud core banking, each engaging dozens of integrators and niche software vendors. In parallel, SMEs advance at an 10.72% CAGR through 2031 as digital vouchers offset first-year licensing fees for CRM, e-commerce, and collaboration suites. Subscription-priced SaaS lets micro-retailers and logistics brokers embrace omnichannel sales and data-driven inventory with no server footprint, closing operational gaps versus larger rivals.

SMEs spend incrementally on cybersecurity and compliance because e-invoicing mandates expose them to real-time tax auditing. Vendors package endpoint protection, email security, and managed firewall services in bundles sized for 5-50 employees, creating predictable monthly recurring revenue. Large enterprises, by contrast, experiment with AI-assisted coding, generative-design tools, and digital twins to optimize production lines and energy usage. As the two segments converge on cloud-first delivery, solution providers derive economies of scale in support operations and R&D, enabling one codebase to address a broad customer continuum.

By Industry Vertical: Public sector sets the tone, retail scales digital commerce

Government and public services held 26.18% of 2025 spending because the Digital Transformation Bible finances identity, justice, and tax platforms on a national scale. Flagship investments include the DAEDALUS supercomputer with 89 PetaFlops capacity, which will also underpin AI Factory Pharos programs in healthcare imaging and climate modeling. BFSI accelerates in parallel; fintech sandboxes and open-banking APIs prompt incumbents to revamp legacy cores, boosting demand for cybersecurity audits and cloud orchestration. Retail and e-commerce show the fastest trajectory at 13.21% CAGR as omnichannel grocery chains, fashion outlets, and marketplace operators deploy personalization engines and last-mile logistics software to capture online demand shifts.

Manufacturing embraces private 5G networks for real-time quality control and automated guided vehicles, particularly in food processing and shipbuilding clusters around Piraeus. Energy and utilities use IoT sensors and analytics to manage renewable integration and grid stability, aligning with EU decarbonization targets. Healthcare adopts telemedicine portals and electronic health records, leveraging the national e-prescription backbone while layering video consults and AI-driven triage, supported by sustained telemedicine research funding. The diversity of vertical requirements cushions the Greece ICT market against cyclical swings in any single sector.

Geography Analysis

The Attica region around Athens concentrates over two-thirds of new data-center capacity, anchored by submarine cable landings, proximity to government ministries, and the nation’s main international airport. Hyperscale investors favor the area’s fiber density and relatively stable grid, creating spillover demand for construction, electrical engineering, and managed-service contractors that cluster nearby. Thessaloniki follows as a secondary hub focused on software development and business-process outsourcing; however, it also reports the steepest talent deficit, with ICT vacancies 467% above average positions. Local universities collaborate with municipal incubators to retain graduates, but salary competition from Athens and remote-work offers from foreign employers keep churn elevated.

Beyond the mainland, connectivity gaps on Aegean and Ionian islands hinder digital parity, despite the BlueMed cable that now links Crete to international backbones. EU-funded rural broadband projects target 5,000 villages and 320,000 residents, using a mix of fiber, fixed-wireless, and satellite backhaul to overcome rugged terrain. Tourism-dependent islands view cloud-based booking engines and mobile payments as essential to service quality, fueling niche opportunities for satellite-LTE hybrid resellers and edge-caching solutions that optimize content delivery during summer peaks. The persistent divide also spurs local-edge deployments by ferry operators and port authorities that require reliable IoT telemetry independent of variable mainland links.

Emerging clusters in Patras, Ioannina, and Larissa harness university R&D to develop maritime IoT, agri-tech, and renewable-energy management software. Territorial-cohesion incentives grant tax credits and subsidized leases to firms establishing labs outside Athens, gradually decentralizing value creation. Remote work reshapes real-estate demand as developers convert idle industrial buildings into co-working spaces wired with gigabit fiber and redundant power. Greece’s tri-continental position continues to attract content-delivery networks that can serve Eastern Europe, the Middle East, and North Africa from a single latency-optimized node.

Competitive Landscape

The Greece ICT market displays moderate concentration in connectivity: OTE Group, Vodafone Greece, and Nova control more than 80% of telecom revenues, benefiting from nationwide spectrum holdings and entrenched retail channels. Their scale facilitates multi-service bundles that combine fiber, 5G, and pay-TV, but their dominant role also invites regulatory scrutiny aimed at fostering wholesale access for smaller ISPs and MVNOs. In contrast, cloud infrastructure and cybersecurity remain fragmented; hyperscalers battle domestic providers such as Lamda Hellix for colocation clients, while boutique MSSPs carve out compliance-driven niches linked to NIS 2.

Mergers and acquisitions accelerate as global strategics scout Greek engineering talent. Cadence’s USD 1.24 billion purchase of BETA CAE Systems, and Olympia Group’s takeover of ERP vendor Entersoft, spotlight valuation upside for specialty software assets.. Startups benefit from exit precedents that recycle capital into seed funds such as Marathon Venture Capital and Big Pi. Meanwhile, system integrators like Uni Systems and Quest Holdings partner with hyperscalers to resell cloud credits and managed migration services, positioning themselves as compliance translators for regulated clients.

White-space segments abound in maritime logistics, renewable-energy orchestration, and precision agriculture, where Greece’s economic base intersects with digitalization imperatives. Emerging entrants leverage AI, blockchain, and IoT to digitize vessel inspections, predict solar-farm output, and monitor crop health. The government’s sovereign-cloud ambitions could tip some workloads toward domestic champions that meet classified-data standards, intensifying competition between local vendors and multinational providers. Over the next five years, the firms that combine sector-specific IP with secure, scalable infrastructure will capture disproportionate growth.

Greece ICT Industry Leaders

-

Microsoft Corporation

-

Oracle Corporation

-

Alphabet Inc. (Google Cloud Greece)

-

Cisco Systems Inc.

-

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vodafone Greece unveiled a EUR 1 billion (USD 1.09 billion) fiber and 5G build-out plan running through 2029, targeting urban densification and rural coverage parity.

- May 2025: OTE Group reported adjusted Q1 2025 earnings of EUR 159.4 million (USD 173.4 million), citing fiber-to-the-home gains and mobile-service revenue upticks.

- April 2025: The government initiated the DAEDALUS supercomputer project with a EUR 58.9 million (USD 64.1 million) budget and 89 PetaFlops target capacity.

- April 2025: The Amphitheater of the Ministry of Digital Governance hosted the inaugural event for "Pharos – The Greek AI Factory for Accelerating AI Innovation." This event signified the official debut of a bold initiative dedicated to fostering innovation, entrepreneurship, and applied research, all centered around the power of artificial intelligence.

Greece ICT Market Report Scope

Information and communications technology (ICT) is a broad term encompassing information technology (IT) with a focus on integrating telecommunications (both wired and wireless) with computing systems. This integration includes essential components like enterprise software, middleware, storage, and audiovisual tools. The goal is to facilitate users' accessing, storing, transmitting, and effectively utilizing information.

The Report Covers Greece's ICT Market Companies and the Market is Segmented by Type (Hardware, Software, IT Services, Telecommunication Services), by Size of Enterprise (Small and Medium Enterprises, Large Enterprises), by Industry Vertical (BFSI, IT, and Telecom, Government, Retail and E-Commerce, Manufacturing, Energy and Utilities, Other Industry Verticals).

The Report Offers Market Sizes and Forecasts in Value (USD) for all the Above Segments.

| Hardware | Computer Hardwar |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Government and Public Services |

| Retail, E-commerce, and Logisitcs |

| Manufacturing and Industry 4.0 |

| Energy and Utilities |

| Healthcare and Life-Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming anf Esports |

| Other Verticals |

| By Type | Hardware | Computer Hardwar |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | BFSI | |

| Government and Public Services | ||

| Retail, E-commerce, and Logisitcs | ||

| Manufacturing and Industry 4.0 | ||

| Energy and Utilities | ||

| Healthcare and Life-Sciences | ||

| Oil and Gas (Up-, Mid-, Down-stream) | ||

| Gaming anf Esports | ||

| Other Verticals | ||

Key Questions Answered in the Report

How large is the Greece ICT market in 2026 and how fast is it growing?

The market stands at USD 9.79 billion in 2026 and is forecast to expand at a 12.34% CAGR to reach USD 17.52 billion by 2031.

Which segment currently generates the most revenue?

Telecommunications services account for 45.07% of spending, reflecting the foundational role of connectivity in national digitalization.

What is driving the rapid growth in cloud adoption?

Local data-center investments by Microsoft, AWS, and Data4 reduce latency and satisfy data-sovereignty rules, prompting enterprises to migrate workloads at a 12.19% CAGR.

How are government programs influencing ICT demand?

Greece allocates 21.4% of its EUR 36.61 billion Recovery and Resilience funding to digital projects, including public-sector cloud moves and SME technology vouchers.

What talent challenges does the country face?

An ageing workforce produces a projected deficit of up to 76,000 IT specialists by 2030, pressuring salaries and project timelines.

Page last updated on: