Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Personal Development Market is Segmented by Instrument (Books, Online Courses and E-Learning Platforms, Mobile Apps and Software Tools, Workshops, Seminars and Retreats, and More), Delivery Mode (Digital / Remote, In-Person, and Hybrid), End User (Individual Consumers, Corporate / Enterprise, Educational Institutions, and More), Focus Area (Leadership and Management Skills Mental Health and Mindfulness, and More), and Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

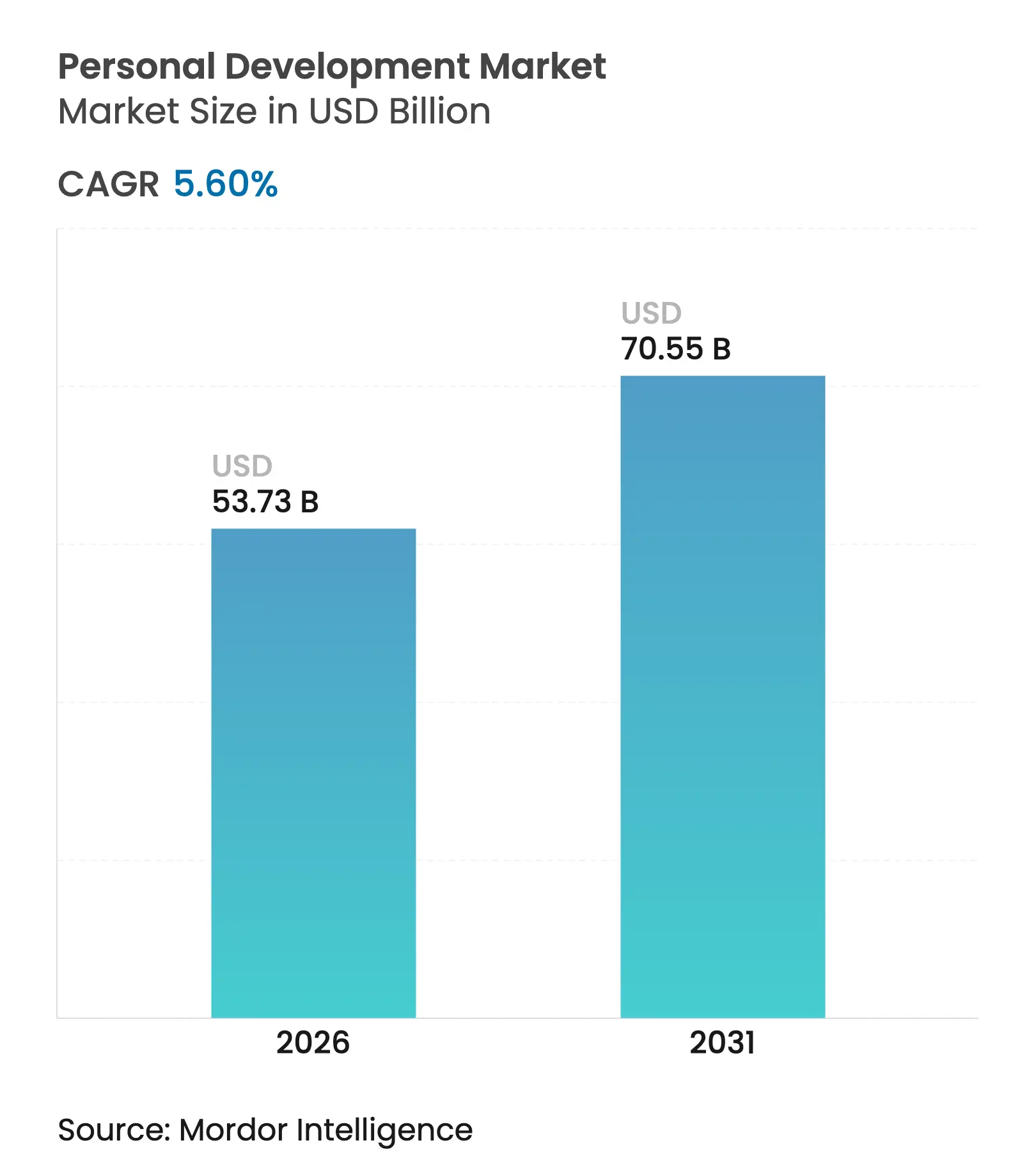

| Market Size (2026) | USD 53.73 Billion |

| Market Size (2031) | USD 70.55 Billion |

| Growth Rate (2026 - 2031) | 5.60 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Personal development market size in 2026 is estimated at USD 53.73 billion, growing from 2025 value of USD 50.88 billion with 2031 projections showing USD 70.55 billion, growing at 5.60% CAGR over 2026-2031. Demand momentum comes from individuals who view continuous self-improvement as a hedge against job displacement and from employers that treat people-centric skills as a strategic asset. Digital transformation is lowering delivery costs, while artificial-intelligence engines now personalise content sequencing and conversational coaching at scale. Corporate buyers are shifting budget from technical training toward leadership, communication and mental-wellness curricula that improve retention, engagement and productivity. North America remains the largest regional buyer set, yet faster expansion in Asia-Pacific signals a re-balancing of growth over the next five years.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analyis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Mobile-first e-learning apps

Mobile-first e-learning apps

| +1.2% | Asia-Pacific leads | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Asia-Pacific leads

|

Impact Timeline

:

Medium term (2-4 years)

|

Corporate LandD pivot to soft skills

Corporate LandD pivot to soft skills

| +1.8% | North America and EU core | Long term (≥ 4 years) | |||

Gen-Z demand for financial-wellness content

Gen-Z demand for financial-wellness content

| +0.9% | North America spreading wider | Short term (≤ 2 years) | |||

Insurance reimbursement for mental-wellness coaching

Insurance reimbursement for mental-wellness coaching

| +1.1% | North America primarly | Medium term (2-4 years) | |||

Global mental-health cover reimbursing coaching

Global mental-health cover reimbursing coaching

| +0.8% | Developed markets first | Long term (≥ 4 years) | |||

Creator-economy monetisation tools

Creator-economy monetisation tools

| +0.7% | Global | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Corporate L and D budgets shift to soft-skill training

Organisations are re-allocating learning spend toward emotional intelligence, leadership and collaboration programmes as automation erodes the value of routine technical tasks. Buyers increasingly judge offerings on behavioural outcomes rather than course volume, rewarding vendors that supply analytics dashboards, competency baselines and ROI metrics. Flexible subscription contracts aligned to head-count let chief learning officers avoid capital expenditure peaks. These factors stimulate recurring revenue for providers able to prove measurable impact on retention and productivity.

Mobile-first e-learning platform proliferation

Smartphone ubiquity is reshaping consumption patterns by enabling micro-learning sessions delivered through push notifications, streak tracking and social leader boards. Providers optimise for low-bandwidth environments, offline downloads and local-language voice-overs to penetrate emerging markets. The approach appeals to younger cohorts with fragmented schedules, lifting engagement while widening reach beyond desktop-centric geographies. Platform operators leverage freemium entry points and in-app subscriptions to convert scale into predictable cash flows.

Insurance reimbursement expansion for mental-health coaching

Approval of Health Savings Account and Flexible Spending Account eligibility for qualified coaching sessions changes the economic calculus for many households. Coaching purchases become reimbursable expenses rather than discretionary spend, broadening access among cost-sensitive users and lending institutional legitimacy to the practice. Providers respond by hiring credentialed coaches and deploying secure documentation workflows that satisfy billing compliance rules. Employers integrate coaching into broader health benefits to curb stress-related absenteeism [1]Wave Life, “Mental Health Coaching Covered by HSA and FSA,” wave.life.

Gen-Z surge in financial-wellness content demand

Younger workers, burdened by debt and volatile income streams, are prioritising practical money-management skills. Content creators blend short-form explainers with interactive budgeting tools and lightweight investing simulators. Partnerships between learning platforms and fintech apps allow a seamless jump from education to action, creating affiliate revenue streams while addressing holistic self-improvement goals.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Market saturation and content commoditisation

Market saturation and content commoditisation

| -0.8% | North America and EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Low completion rates in self-paced courses

Low completion rates in self-paced courses

| -1.2% | Global | Short term (≤ 2 years) | |||

Algorithmic gatekeeping raises acquisition cost

Algorithmic gatekeeping raises acquisition cost

| -0.6% | Global | Short term (≤ 2 years) | |||

Rising copyright litigation on AI-generated content

Rising copyright litigation on AI-generated content

| -0.4% | Developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Market saturation and content commoditisation pressures

An explosion of low-cost courses in popular categories erodes pricing power for incumbent providers. To avoid pure price competition, vendors differentiate through proprietary frameworks, evidence-based methodology and tightly defined niches. Consolidation is likely where smaller players lack resources to maintain marketing visibility on search engines and app stores.

Low completion rates in self-paced learning models

Learners often abandon stand-alone courses once initial motivation fades, reducing lifetime value and harming word-of-mouth referrals. To counter attrition, platforms inject gamified milestones, accountability pods and live cohort sessions that layer human interaction over digital content. Hybrid approaches blend self-paced flexibility with structured check-ins to keep users on track and to improve outcome metrics that corporate buyers require.

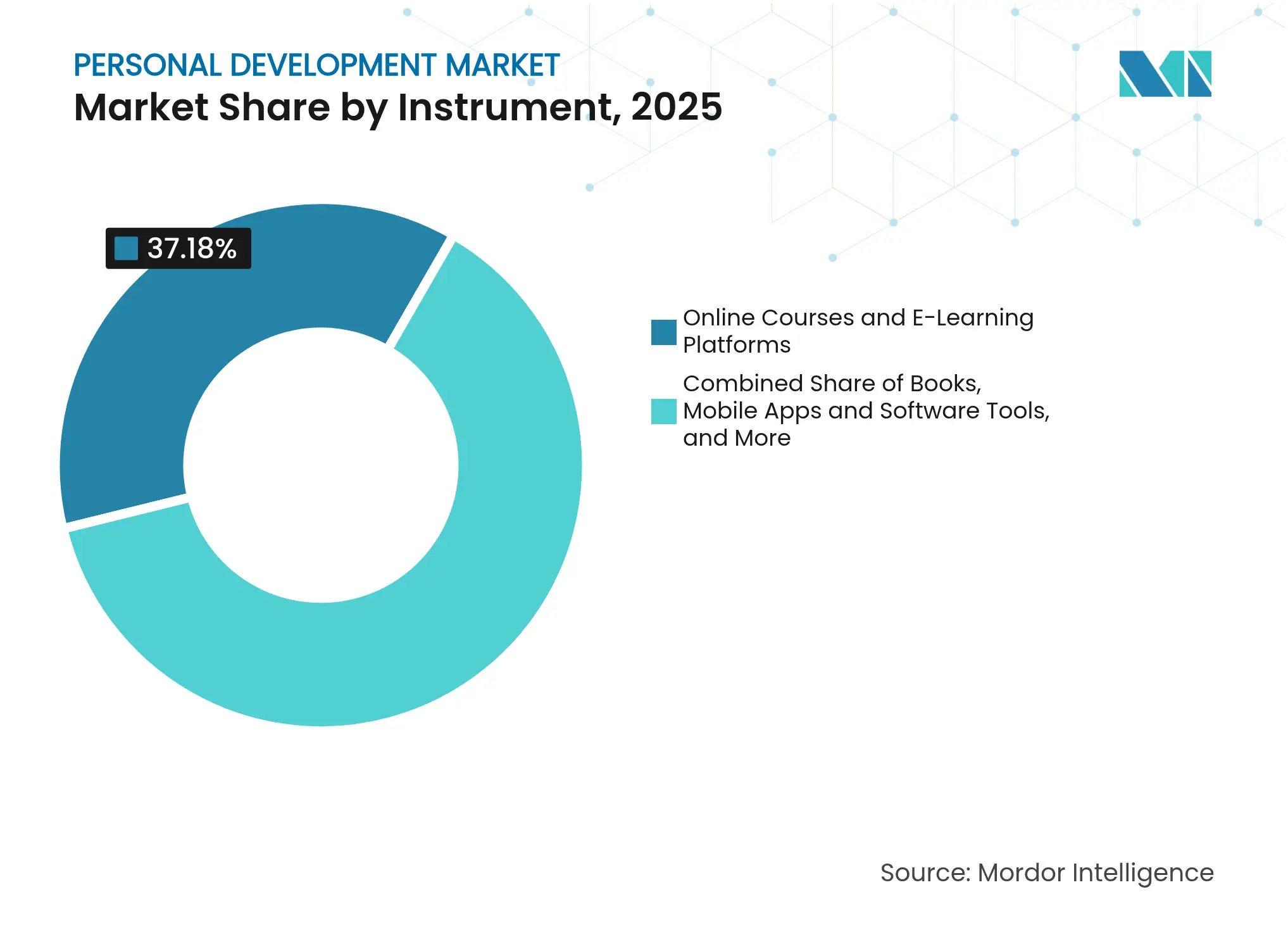

By Instrument: Digital platforms extend scale advantage

Online courses and e-learning platforms held 37.18% of personal development market share in 2025, establishing web-based formats as the primary distribution channel for skill-building resources. Mobile apps post the quickest 18.82% CAGR outlook, aided by smartphone penetration and user preference for micro-learning sessions. Print books hold a shrinking niche among readers who still value deep, linear learning journeys. Workshop-based retreats and live seminars cater to premium segments that seek immersive experiences, networking and direct feedback. Coaching services benefit from the insurance reimbursement trend and from employers sourcing scalable mentoring solutions. Vendors increasingly bundle asynchronous modules with live instructor sessions, producing a blended value proposition that merges reach with personalisation. AI-powered chatbots now deliver just-in-time prompts, nudging users to complete reflective exercises and log behavioural changes. This hybridisation preserves the cost advantage of digital scale yet keeps the human element that drives accountability. Providers that perfect such combinations are positioned to capture a larger slice of personal development market size over the forecast horizon.

A second vector of innovation is the emergence of virtual-reality practice environments. Simulated negotiation tables or public-speaking stages let learners rehearse high-stakes scenarios with immediate feedback on tone, posture and pacing. Although still a small revenue contributor, VR showcases the convergence of experiential and digital modalities that could redefine instrumentation categories. Intellectual-property ownership of these immersive assets creates defensible moats against copy-cat offerings, helping combat content commoditisation.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Mode: Hybrid overtakes pure digital on engagement

Digital and remote channels generated 71.45% of 2025 revenue as lockdown-driven adoption cemented online learning habits. Yet signs of fatigue appear when complex behavioural change requires sustained practice and peer feedback. Hybrid delivery, clocking a 10.48% CAGR, inserts live facilitation, manager coaching and cohort interaction into otherwise self-directed curricula. For leadership topics, this blend boosts application rates once learners return to the workplace, increasing perceived value for enterprise buyers. Pure in-person formats continue to serve niche uses such as executive retreats, team-building boot camps and certification programmes subject to regulatory oversight.

Data analytics enable providers to orchestrate the balance between asynchronous modules and synchronous touch points. Dashboards track micro-engagement signals so facilitators can schedule timely interventions that prevent drop-off. The model also supports geographic expansion because one coach can serve multiple time-zones while localisation remains concentrated at the content layer. As a result, hybrid solutions are projected to capture a growing proportion of personal development market size, especially inside large multinationals seeking global consistency with local cultural relevance.

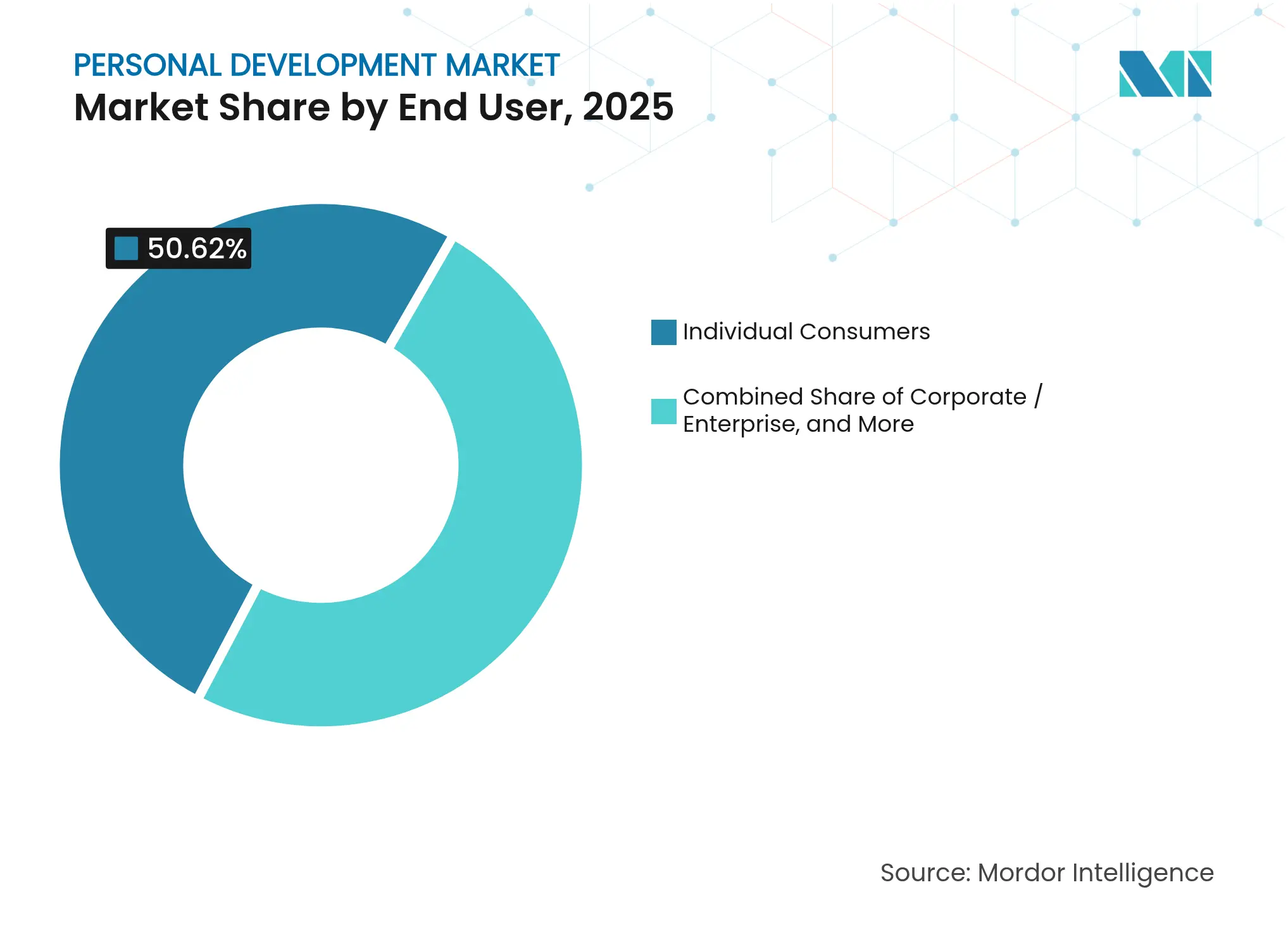

By End User: Enterprise momentum reshapes revenue mix

Individual consumers contributed 50.62% to 2025 demand, yet enterprise clients represent the fastest-growing pool with a 9.78% CAGR through 2031. Employers use coaching and soft-skill curricula to improve engagement scores and to avert costly turnover. Procurement teams favour platform licences that integrate with HR information systems for single-sign-on, usage analytics and competency mapping. Educational institutions embed personal-development micro-credentials into degree pathways to strengthen graduate employability. Government and non-profits apply the same frameworks to upskill civil servants and community leaders.

The convergence of business-to-consumer and business-to-business models pushes providers to build tiered pricing. Freemium entry points attract individuals, while enterprise versions add administrative dashboards, curated pathways and compliance monitoring. Vendors that master both channels lower customer-acquisition costs by converting engaged users into corporate champions, thereby expanding their personal development market share without proportional increases in marketing spend.

Note: Segment shares of all individual segments available upon report purchase

By Focus Area: Mental health ascends alongside leadership mainstay

Leadership and management skills held the largest 23.05% revenue share in 2025, reflecting steady corporate investment in succession pipelines. Mental health and mindfulness programmes, however, record the briskest 11.47% CAGR as employers tackle stress-induced productivity losses and insurance reimbursement widens access. Career-development content such as interview preparation, networking strategy and personal branding remains a staple for early-career professionals. Financial-wellness modules are surging on platforms that cross-sell budgeting tools and investment literacy alongside mindset coaching, deepening engagement while diversifying revenue sources. Spirituality and purpose-centric offerings occupy a smaller but loyal customer base that seeks alignment between work, values and societal impact.

To sustain differentiation, providers anchor each focus area in evidence-based methodology, outcome measurement and certified facilitator networks. The practice shields them from margin erosion as generic content floods free channels. As a result, premium positioning within high-growth sub-segments is expected to lift the overall personal development market size even if base pricing pressures persist elsewhere.

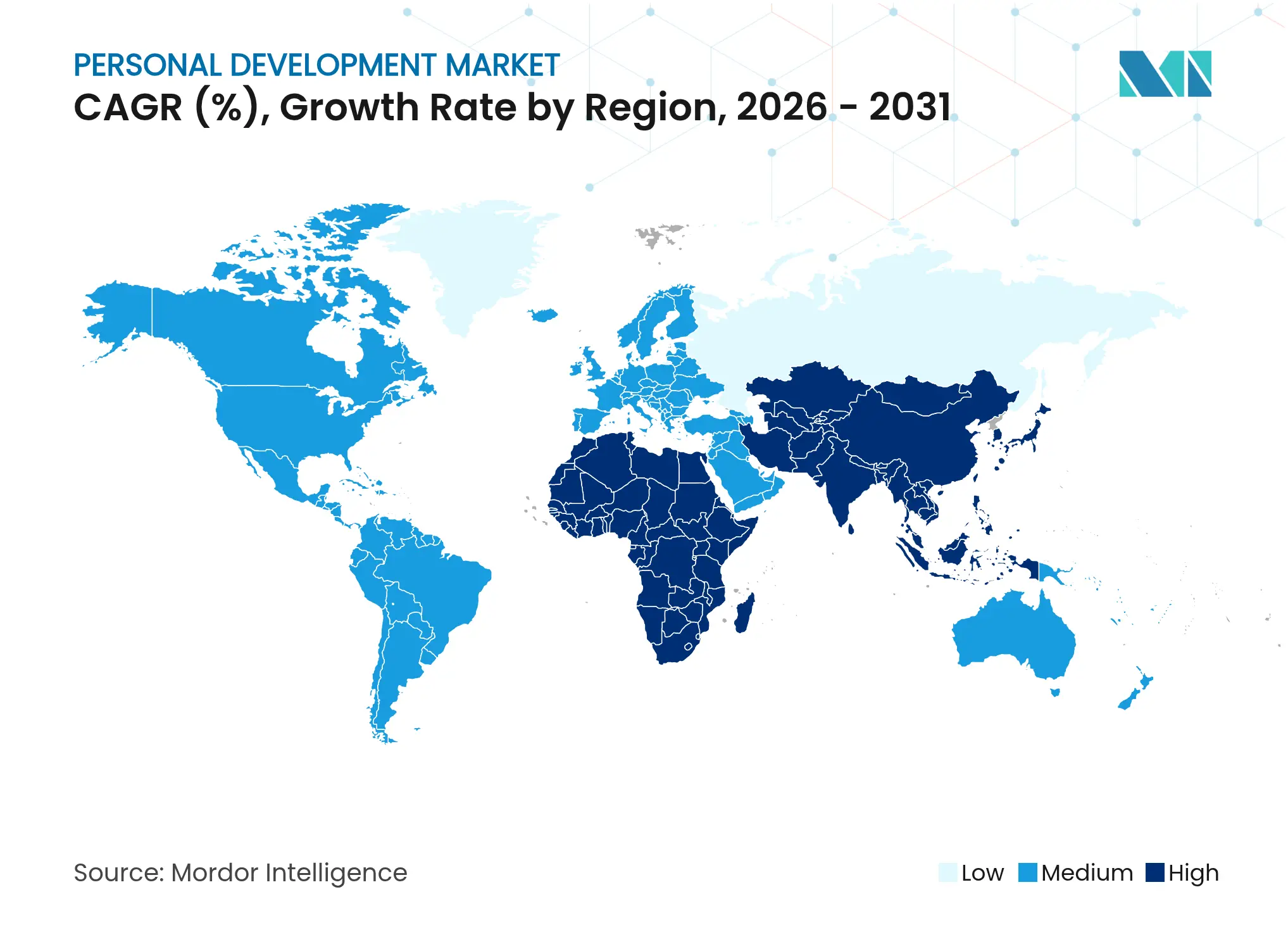

North America accounted for 34.92% of 2025 revenue thanks to entrenched corporate learning budgets, high disposable income and regulatory frameworks that allow Health Savings Account reimbursement for qualified coaching services. Enterprises embed wellness stipends and learning wallets into compensation packages, driving predictable subscription uptake for large platform vendors. The region’s saturated segments, however, face intensified competition, prompting incumbents to pursue niche specialisation or mergers that offer scale synergies.

Asia-Pacific delivers the fastest 9.31% CAGR to 2031, supported by rising middle-class incomes and government-backed digitisation drives. Smartphone-first internet access suits micro-learning formats, while cultural emphasis on education fosters willingness to pay for upskilling. Localisation remains critical as language diversity and national certification standards dictate content adjustments. Indonesia and India illustrate the trajectory: leap-frogging desktop infrastructure, learners consume snack-sized lessons during commuting hours, accelerating mobile app adoption. Providers employing regional joint ventures navigate payment-system complexities, bolstering trust through local-office presence and culturally attuned marketing.

Europe presents a mature yet steady environment. General Data Protection Regulation compliance elevates data-security standards, imposing cost hurdles on smaller entrants but reinforcing consumer trust for established platforms. Emphasis on work-life balance drives corporate wellness spending, though expansive social safety nets temper out-of-pocket consumer purchases. The multilingual landscape necessitates translation and voice-over investment, encouraging partnerships with regional content studios. As skills shortages widen in technology and healthcare, governments co-fund reskilling initiatives, generating public-private procurement opportunities that add incremental volume to personal development market size.

Market Concentration

The industry remains fragmented, with no single player controlling a dominant share. Coursera, one of the largest platforms, posted USD 695 million in 2024 revenue, yet still commands a single-digit slice of overall personal development market share [2]Jeff Maggioncalda, “Coursera Reports Fourth Quarter and Full Year 2024 Results,” Coursera, coursera.org. Competition spans traditional educational publishers, specialist coaching firms, wellness-app developers and enterprise software providers embedding learning modules into larger suites.

Technology constitutes the chief differentiation lever. Vendors deploy recommendation engines that tailor pathways based on psychometrics, usage data and career goals. Automated writing or speech feedback cuts facilitator costs, widening the margin gap over purely human-delivered services. Content libraries now integrate interactive case simulations, scenario branching and AI avatars able to role-play negotiation, interview or conflict-resolution situations. Providers racing to patent such engines hope to lock in enterprise accounts through switching-cost barriers.

Strategic moves reflect this scramble. TELUS Health deepened its wellness footprint by purchasing Workplace Options for USD 500 million in May 2025, adding counselling and employee assistance expertise [3]TELUS Health, “TELUS Health Acquires Workplace Options for $500 M,” telus.com. CoachHub raised fresh debt in December 2024 to fund international expansion and to refine its machine-learning coach-matching algorithm. Meanwhile, niche players such as Conquer Your Limits introduced lifetime-membership bundles that front-load cash flows while promising perpetual content updates, demonstrating creative monetisation approaches beyond monthly subscriptions.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Market Definitions and Key Coverage

According to Mordor Intelligence, our study defines the personal development market as the total yearly revenue earned from books, digital learning tools, mobile apps, live workshops, and coaching or mentoring services that help individuals improve skills, mindset, or well-being. These offerings are tracked globally across consumer, corporate, and institutional buyers.

Scope Exclusions: We exclude therapeutic counseling, accredited degree programs, and workplace-only compliance training.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview platform founders, certified coaches, human-resource directors, and bookstore chains across North America, Europe, and Asia-Pacific. These conversations validate pricing ladders, program completion rates, and the share of corporate learning budgets flowing into self-improvement.

Desk Research

We begin with a wide sweep of publicly available, high-credibility sources such as the United Nations SDG data hub, OECD adult-learning statistics, U.S. Bureau of Labor Statistics spending surveys, and patent libraries from Questel. Company 10-Ks, investor decks, and association portals like the International Coaching Federation supply granular spend and enrollment clues.

Trade data from Volza, news archives in Dow Jones Factiva, and regional education ministries help us size cross-border book shipments, app adoption, and training budgets. This list is illustrative; many additional documents feed our files before any numbers are locked.

Market-Sizing & Forecasting

We construct a top-down model that starts with consumer spending and corporate L&D outlays reported by governments and industry bodies, which are then split by penetration rates for key instruments. Results are cross-checked with selective bottom-up supplier roll-ups and sampled average selling price multiplied by volume checks to close gaps.

Key variables that drive the model include smartphone literacy, per-capita discretionary income, corporate training spend per employee, average course price, and time spent on learning apps. A multivariate regression projects each driver, and scenario analysis tests upside or downside shifts.

Data Validation & Update Cycle

Every draft passes anomaly checks and peer review. Variances above preset thresholds trigger re-contacts. Reports refresh once each year, and we issue interim notes if regulatory shifts or major acquisitions cause material change, so clients always receive our latest view.

Why Our Personal Development Baseline Earns Trust

Benchmark comparison

Published estimates often differ because providers pick unique service baskets, convert currencies differently, or revisit models at uneven intervals. Our disciplined scope, annual refresh, and driver-based forecasts keep the baseline steady yet responsive.

Key gap drivers include competitor focus on narrower sub-segments, unverified price points, or inclusion of wellness therapies that we purposely exclude. Our analysts also revisit exchange and inflation factors quarterly, something several publishers skip.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 50.88 billion (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 48.40 billion (2024) | Global Consultancy A | Covers coaching only and freezes average prices for the full forecast period | ||

USD 50.42 billion (2024) | Trade Journal B | Adds mindfulness retreats, inflating totals beyond our definition | ||

USD 46.73 billion (2024) | Industry Association C | Uses single-year FX rates and omits digital app revenues |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.