Software Development Outsourcing Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Market Size (2026) | USD 618.38 Billion |

| Market Size (2031) | USD 977.04 Billion |

| Growth Rate (2026 - 2031) | 9.60% CAGR |

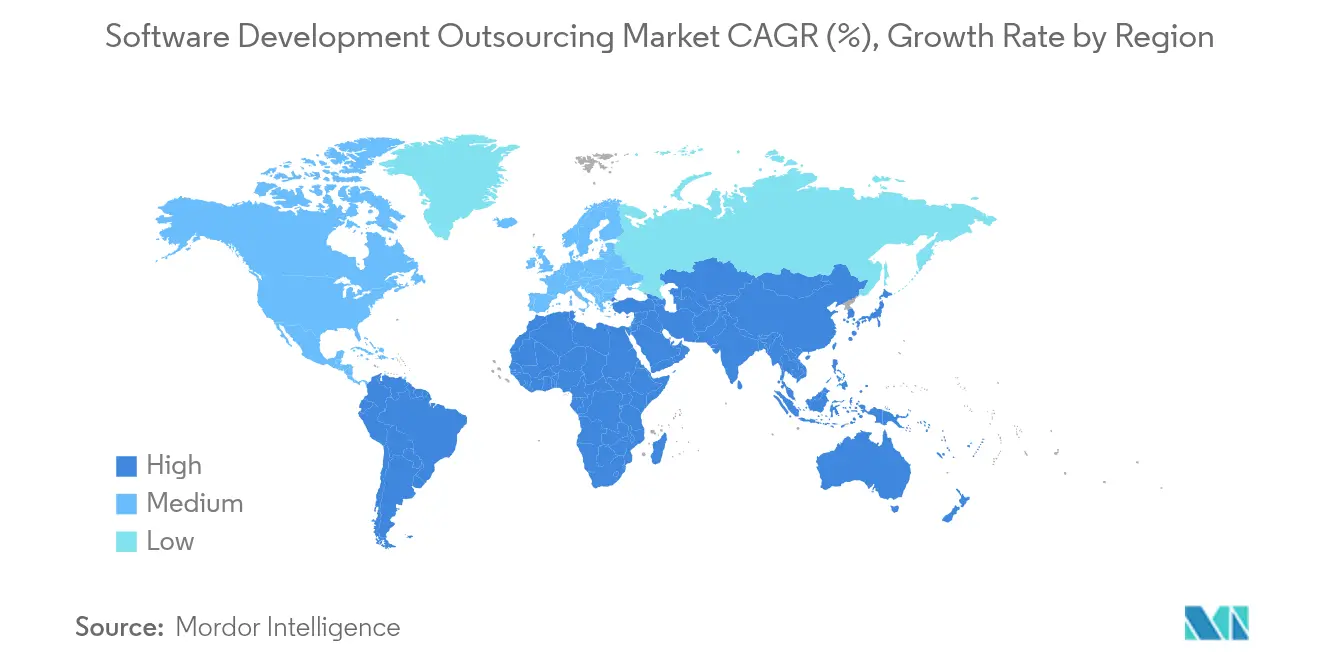

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Development Outsourcing Market Analysis by Mordor Intelligence

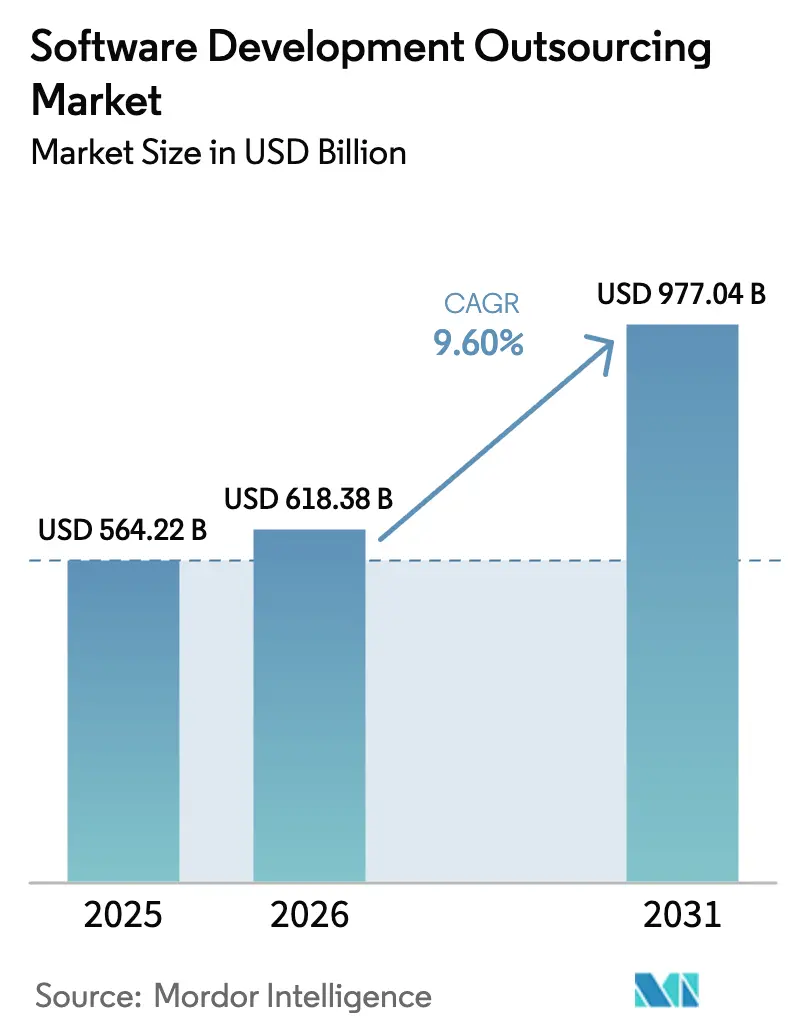

Software development outsourcing market size in 2026 is estimated at USD 618.38 billion, growing from 2025 value of USD 564.22 billion with 2031 projections showing USD 977.04 billion, growing at 9.60% CAGR over 2026-2031. Surging demand for external digital-engineering expertise, rapid generative-AI adoption, and the persistent shortage of senior technologists in OECD economies keep contracting pipelines robust. Enterprises that once viewed outsourcing purely as a cost lever now use it to secure scarce AI, cybersecurity, and cloud-native skills, compress product launch cycles, and meet strict regulatory timelines. Providers are, in turn, shifting from traditional project staffing toward value-based partnerships built around outcome guarantees, near-real-time collaboration, and strong data-sovereignty controls. The industry’s resilience is further underpinned by a healthy geographic spread of delivery hubs that cushions macro-economic shocks and by mid-market firms entering the buyer pool as consumption-based cloud services reduce the need for large‐scale internal IT teams. [1]U.S. Department of Homeland Security, “Artificial Intelligence Strategic Plan,” dhs.gov

Key Report Takeaways

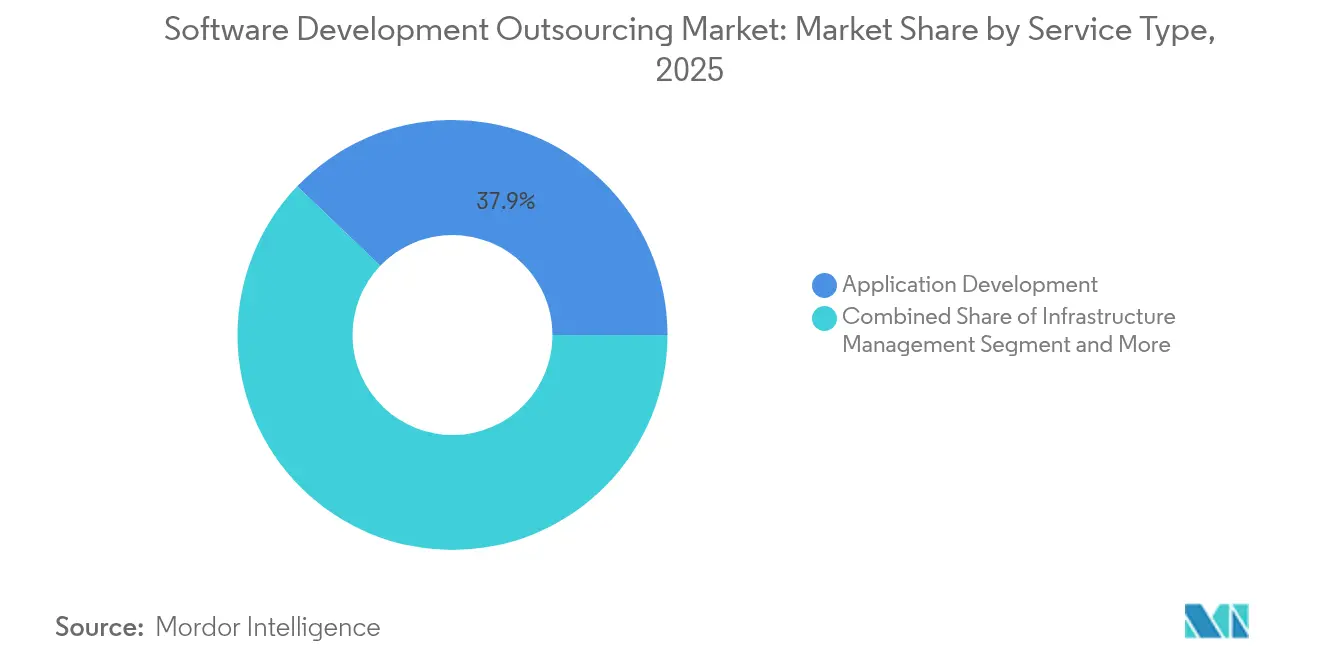

- By service type, Application Development led with 37.85% of software development outsourcing market share in 2025; Product Development is projected to expand at a 12.62% CAGR to 2031.

- By organisation size, Large Enterprises held 70.95% of the software development outsourcing market in 2025, while Small and Medium Enterprises show the highest forecast CAGR at 11.25% through 2031.

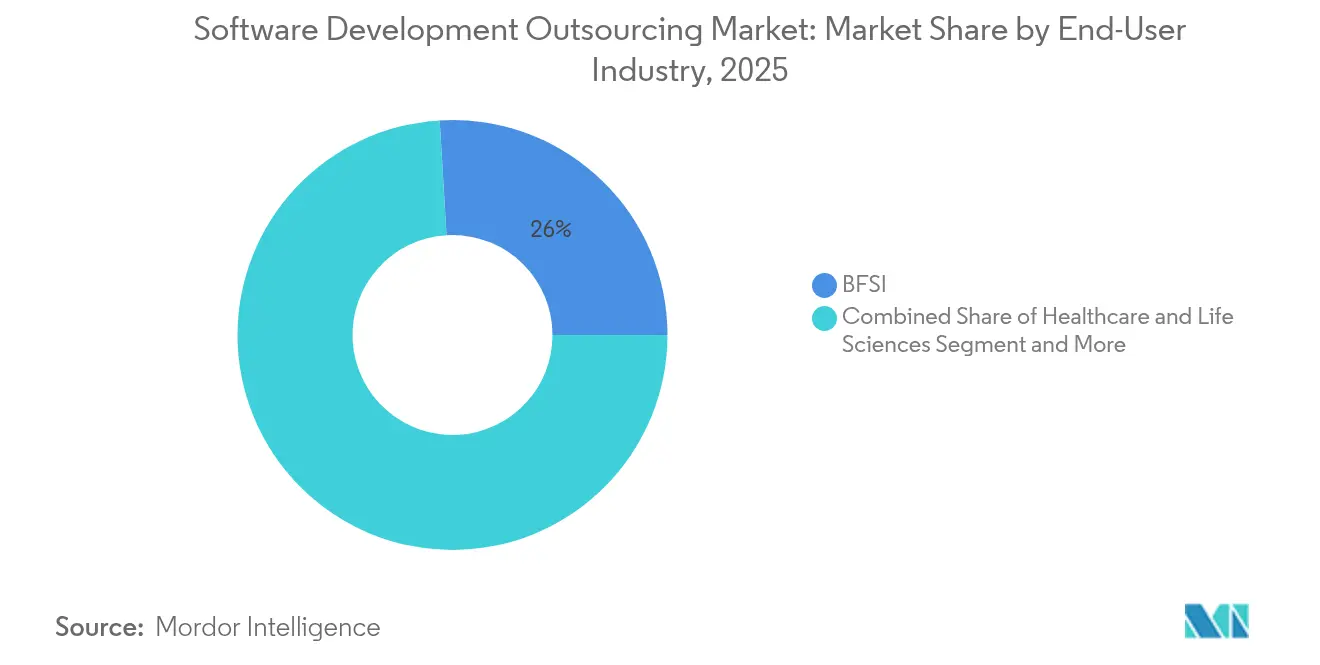

- By end-user industry, Banking, Financial Services & Insurance captured 25.95% revenue share in 2025; Healthcare & Life Sciences is expected to advance at a 12.85% CAGR to 2031.

- By outsourcing model, offshore accounted for 51.85% of the software development outsourcing market size in 2025; Near-shore is set to grow at a 13.95% CAGR between 2026-2031.

- By geography, Asia-Pacific retained the largest regional footprint with 31.75% share in 2025, whereas the Middle East & Africa region is poised for the fastest growth at 13.20% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software Development Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-efficiency pressure on CIO budgets | 2.10% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Digital-transformation acceleration post-GenAI | 2.80% | Global, led by North America, spreading to APAC & Europe | Short term (≤ 2 years) |

| Scarcity of senior engineering talent in OECD nations | 1.90% | North America & Europe primarily, spillover to Australia | Long term (≥ 4 years) |

| Cloud-native adoption among mid-market firms | 1.40% | Global, with early adoption in North America & Northern Europe | Medium term (2-4 years) |

| AI-pair-programming productivity boost | 1.60% | Global, concentrated in tech-forward markets | Short term (≤ 2 years) |

| Near-shore legislation incentives in CEE & LatAm | 0.90% | Central & Eastern Europe, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Acceleration Post-GenAI

Generative AI has recast buying criteria: 87% of North American engineering leaders in 2025 already fund GenAI pilots, and vendors capable of embedding large-language-model toolchains into secure pipelines command premium rates. EPAM projects that 80% of the development life cycle will involve GenAI touchpoints by year-end, potentially raising individual-developer productivity by as much as 75%. Government analyses echo the efficiency gains: the US Department of Homeland Security pegs code-generation lift between 20-50%, particularly in documentation and test-case creation. Buyers thus prioritise partners able to deploy gated AI frameworks, manage prompt-engineering risks, and guarantee model-output traceability. For providers, this shift expands addressable revenue pools from staff augmentation to enterprise-scale AI enablement services.

Cost-Efficiency Pressure on CIO Budgets

Macro-economic caution has tightened discretionary IT outlays, yet board-level mandates to sustain digital programmes remain. North American CIO surveys show double-digit budget cuts in back-office modernisation but a simultaneous 11% rise in AI-driven initiatives. Indian tier-one vendors recorded sub-2% revenue upticks in early FY 2026 as clients slowed renewals, forcing suppliers to prove ROI through automation, FinOps, and outcome-based billing. Providers offering bundled managed services with guaranteed savings see faster deal closures than those competing on labour-rate arbitrage alone.

Scarcity of Senior Engineering Talent in OECD Nations

The US entered 2025 with 1.4 million unfilled technology roles against only 400,000 annual computer-science graduates, translating to USD 162 billion in foregone output. Similar gaps exist across Western Europe, particularly for AI/ML, cyber-defence, and cloud-platform architects. Enterprises now outsource not for wage savings but to secure scarce capabilities, often integrating near-shore squads as core product teams. Immigration-policy tweaks and STEM-education investments will take several years to ease shortages, keeping outsourcing demand elevated.

Cloud-Native Adoption Among Mid-Market Firms

More than half of firms with under USD 1 billion revenue run over 10 Kubernetes clusters, yet 75% report operational complexity they cannot manage in-house. Outsourcers offering site-reliability engineering, GitOps automation, and managed container security capitalise on this gap. The mid-market’s preference for subscription pricing and rapid MVP cycles aligns with vendor platforms that bundle DevSecOps tooling and 24×7 support, fuelling steady contract volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty & residency mandates | -1.80% | Europe, China, emerging markets with strict data laws | Long term (≥ 4 years) |

| Persistent IP-security concerns | -1.20% | Global, heightened in North America & Europe | Medium term (2-4 years) |

| Wage inflation in Tier-1 offshore hubs | -0.90% | India, Philippines, Eastern Europe | Short term (≤ 2 years) |

| Talent poaching & attrition risk post-remote-work | -0.70% | Global, concentrated in major outsourcing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty & Residency Mandates

Cross-border data rules tighten yearly. The EU Cloud Services Scheme now stipulates that sensitive workloads must stay within EU-accredited facilities, while China’s March 2024 regulations impose security reviews on outbound data transfers overseen by the Central Internet Security and Informatization Committee. Providers lacking local data-centre footprints must form joint ventures, raise capital for regional buildouts, or cede business. Multinationals, meanwhile, split architectures into regional micro-services—adding cost and governance overhead that slows contract signoffs. [2]Central Cyberspace Affairs Commission, “Regulation on Cross-Border Data Transfer,” cac.gov.cn

Persistent IP-Security Concerns

US manufacturers lose up to USD 600 billion annually to intellectual-property theft, underscoring heightened scrutiny of vendor cyber-hygiene. Generative-AI workflows exacerbate risk because training data, prompt logs, and model artefacts all represent valuable IP. Enterprises insist on zero-trust network architectures, secure-coding certifications, and continuous security monitoring. Smaller providers that cannot invest in top-tier defences face relegation to non-critical work or exclusion from request-for-proposal (RFP) shortlists. [3]Machine Design, John McCloy, “The High Cost of IP Theft,” machinedesign.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Innovation Demand Diversifies Spend

Application Development secured 37.85% software development outsourcing market share in 2025 thanks to evergreen demand for tailored digital-experience projects. Clients increasingly request AI-embedded feature sets, driving ticket sizes higher and necessitating full-stack squads fluent in modern LLM frameworks. Yet Product Development’s 12.62% forecast CAGR signals a pivot toward strategic co-creation models where vendors assume joint roadmap ownership. Software development outsourcing market size for Product Development is projected to reach USD xx billion by 2031, reflecting enterprises’ willingness to outsource innovative core offerings alongside support workloads. Infrastructure Management remains resilient as multicloud complexity rises, and Testing & Quality Assurance gains fresh relevance: AI-generated code augments volume but requires sophisticated test-orchestration pipelines.

The automation of Level 1 support threatens the Software Maintenance & Support segment, pressing providers to re-train staff for higher-value SRE tasks. Consulting Services show healthy momentum due to AI-strategy engagements, cyber-risk assessments, and value-stream mapping. Vendors differentiating through proprietary GenAI accelerators report contract-value uplifts; Sonata Software documented a 20% cut in document-retrieval times and a 50-60% drop in enquiry-resolution latency for telecom and travel clients, respectively.

By Organisation Size: Democratization Spurs SME Uptake

Large Enterprises anchored 70.95% of 2025 revenue, leveraging mature vendor-management offices and global capability centres. Nevertheless, SMEs’ 11.25% CAGR through 2031 underlines a structural change in procurement behaviours. Pay-as-you-go cloud services and modular APIs level the playing field, letting smaller firms purchase bite-sized sprints rather than long-term staff augmentation deals. The software development outsourcing market now sees regional providers launching fixed-price productised offerings—such as MVP-in-a-Sprint or DevOps-as-a-Service—that cap costs and simplify governance. OECD reports still find an adoption gap versus large enterprises, but outcome-based pricing models and marketplace platforms narrow this divide each quarter.

SME buyers gravitate toward near-shore partners for time zone alignment and cultural affinity, a trend especially visible across Central Europe and Latin America. Providers that package cybersecurity hardening and regulatory templates see faster conversions, as resource-constrained SMEs rely on external expertise to pass compliance audits.

By End-User Industry: Healthcare Fastest, BFSI Largest

Banking, Financial Services & Insurance retained 25.95% revenue share by sustaining multiyear digital-core transformations and relentless regulatory mandates. The segment continues to invest in AI-driven risk scoring, embedded finance, and real-time payments. Conversely, Healthcare & Life Sciences shows 12.85% CAGR to 2031, the fastest among tracked verticals. Software development outsourcing market size for healthcare is projected to nearly double as hospitals modernise electronic health records and biopharma firms deploy AI-aided drug-discovery platforms. ITRex Group’s web-based medical imaging solution, for instance, boosts diagnostic throughput and underlines the outsourcer’s role in clinical innovation.

Media & Telecommunications, Retail & E-commerce, and Manufacturing hold stable growth trajectories, each shaped by sector-specific digital-experience imperatives. Providers that present domain accelerators—such as pre-trained telco language models or industrial-IoT analytics kits—win wallet share over generic competitors.

By Outsourcing Model: Policy-Backed Near-Shore Uptick

Offshore hubs like India and the Philippines still control 51.85% of spend, yet wage inflation and currency shifts compress their cost advantage. Government policy fuels near-shore momentum: Mexico’s Plan Mexico offers USD 1.5 billion in tax breaks for tech investors, while Romania’s programmer-tax exemptions lower total cost of engagement for EU buyers. Consequently, the near-shore slice is expanding at 13.95% CAGR, and some European banks now cap offshore exposure at 50% of external headcount to de-risk geopolitical volatility.

On-shore outsourcing quietly gains relevance for regulated workloads. National cyber-resilience directives encourage in-country delivery for critical infrastructure projects, giving rise to hybrid models where vendors split execution across domestic and near-shore teams.

Geography Analysis

Asia-Pacific delivered the largest slice of 2025 revenue at 31.75%, anchored by India’s mature export engine and China’s fast-scaling domestic demand. Providers in Bengaluru, Hyderabad, and Ho Chi Minh City increasingly bundle AI-accelerators into fixed-price contracts, offsetting wage inflation with higher value. Software development outsourcing market share for Asia-Pacific could moderate slightly by 2031 as buyers diversify sources; however, absolute intake grows on the back of emerging hubs in Vietnam and the Philippines.

North America commands premium contract value thanks to complex AI, cyber-security, and regulatory compliance assignments. US-based clients show rising interest in dual-shore models: core product squads remain onshore or near-shore, while commoditised feature work shifts to APAC. Buyers emphasise deliverable-based pricing and transparent velocity metrics, forcing vendors to adopt advanced DevOps telemetry for real-time performance reporting.

The Middle East & Africa represents the fastest-growing region at 13.20% CAGR. Ghana’s partnership with the UAE to build a USD 1 billion innovation hub illustrates the region’s ambition to develop AI-engineering and data-labelling ecosystems. Saudi Arabia’s Vision 2030 directs multibillion-dollar investments toward semiconductor fabs and AI-research centres, driving outsourcing demand for cloud-native platform builders. Regional governments further sweeten the proposition with zero-tax technology zones and subsidised digital-skilling programmes.

Competitive Landscape

The market remains moderately fragmented: the top five vendors hold under 45% combined revenue, yielding intense competition for large transformation deals. Incumbents—Accenture, TCS, IBM, Cognizant, and Infosys—retain scale advantages, extensive client rosters, and deep regulatory know-how. Their 2025 strategies centre on enterprise-grade generative-AI platforms, proprietary DevOps toolchains, and upskilling programmes that target 100,000+ engineers annually.

Specialised challengers carve profitable niches. EPAM and Globant cultivate AI-native delivery models, while cybersecurity-focused firms like NCC Group secure IP-heavy workloads. Near-shore providers in Poland and Mexico highlight time zone compatibility and EU/US data-protection compliance to win projects previously routed to Asia.

Consolidation accelerated in 2025. Capgemini’s USD 3.3 billion purchase of WNS sought to blend business-process expertise with intelligent automation, signalling that scale plus AI depth will define future leaders. HCLTech’s partnership with OpenAI underscores the arms-race for exclusive-model access. Vendors unable to fund proprietary AI R&D face either acquisition or niche specialisation.

Software Development Outsourcing Industry Leaders

Accenture plc

Tata Consultancy Services Limited

Cognizant Technology Solutions Corporation

Infosys Limited

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Capgemini acquires WNS for USD 3.3 billion to embed agentic-AI into business-process services.

- July 2025: HCLTech forms strategic collaboration with OpenAI to bolster AI-powered delivery offerings.

- July 2025: Ghana and the UAE sign a USD 1 billion MoU to create a tech and innovation hub for 11,000+ global firms.

- May 2025: Infosys moves to buy The Missing Link and MRE Consulting, expanding cyber-security and energy-sector reach.

Global Software Development Outsourcing Market Report Scope

Software development outsourcing involves enlisting a third-party service provider to undertake software development projects. These services can encompass everything from creating software tailored for your company to overseeing business operations or even developing and maintaining software solutions for your clientele.

The software development outsourcing market is segmented by service type (media relations, digital and social media PR, crisis communication, event management, and content development), by end-user industry (BFSI, consumer good and retail, government and public sector, entertainment, IT & telecom, healthcare, hospitality, and food and beverage).

| Infrastructure Management |

| Application Development |

| Testing and Quality Assurance |

| Product Development |

| Software Maintenance and Support |

| Consulting Services |

| Small and Mid-sized Enterprises (SMEs) |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Media and Telecommunications |

| Retail and E-commerce |

| Manufacturing and Industrial |

| On-shore |

| Near-shore |

| Offshore |

| Agile / Scrum |

| DevOps / Continuous Delivery |

| Waterfall and Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Infrastructure Management | |

| Application Development | ||

| Testing and Quality Assurance | ||

| Product Development | ||

| Software Maintenance and Support | ||

| Consulting Services | ||

| By Organisation Size | Small and Mid-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | ||

| Media and Telecommunications | ||

| Retail and E-commerce | ||

| Manufacturing and Industrial | ||

| By Outsourcing Model | On-shore | |

| Near-shore | ||

| Offshore | ||

| By Development Methodology | Agile / Scrum | |

| DevOps / Continuous Delivery | ||

| Waterfall and Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the software development outsourcing market?

The market is valued at USD 618.38 billion in 2026 and is forecast to reach USD 977.04 billion by 2031.

Which service segment is growing the fastest?

Product Development is set to expand at a 12.62% CAGR through 2031 as buyers seek innovation-led engagements.

Why are SMEs increasing their outsourcing spend?

Cloud-native tools and outcome-based pricing models lower entry barriers, helping SMEs access enterprise-grade engineering talent while capping costs.

How is generative AI changing outsourcing contracts?

GenAI shifts demand toward vendors that can embed large-language-model toolchains into secure delivery pipelines, raising productivity and enabling premium pricing.

Which geography offers the highest growth potential?

The Middle East & Africa region shows the fastest forecast CAGR at 13.20%, buoyed by large-scale government technology investments.

What are the main risks to outsourcing growth?

Data-sovereignty mandates, IP-security concerns, and wage inflation in traditional offshore hubs can temper growth if providers fail to adapt service models.

Page last updated on: