Crypto Wallet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

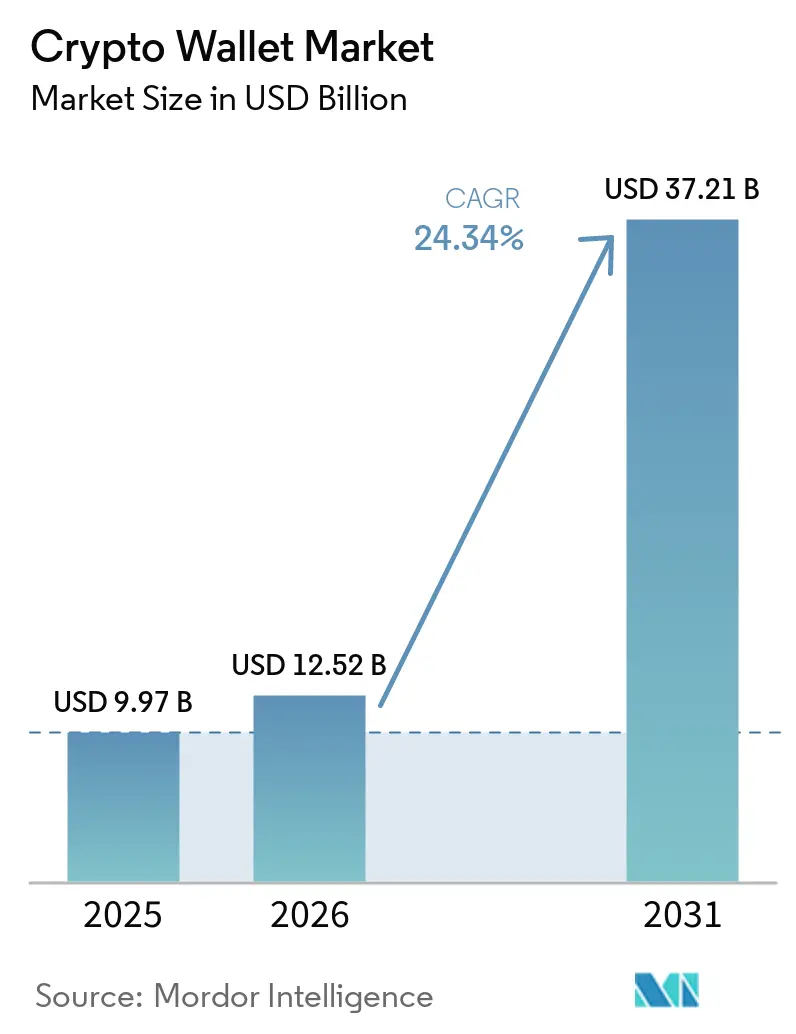

| Market Size (2026) | USD 12.52 Billion |

| Market Size (2031) | USD 37.21 Billion |

| Growth Rate (2026 - 2031) | 24.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crypto Wallet Market Analysis by Mordor Intelligence

The Crypto wallet market size is projected to be USD 9.97 billion in 2025, USD 12.52 billion in 2026, and reach USD 37.21 billion by 2031, growing at a CAGR of 24.34% from 2026 to 2031. Growth is being shaped by a shift away from retail speculation alone and toward broader wallet use in treasury management, cross-border settlement, and automated on-chain operations. Stablecoin settlement is expanding wallets' role beyond token storage and trading, making wallet infrastructure more relevant to mainstream payments and capital flows. Institutional participation is also changing product design, with stronger demand for audited controls, multi-party approval models, and regulated custody connectivity. At the same time, self-custody demand remains strong among retail users who want direct access to DeFi, swaps, and Web3 applications, which keeps software wallets central to user acquisition. Security incidents still restrain adoption, but they are also pushing premium demand toward hardware signing, transaction simulation, and seedless recovery models.

Key Report Takeaways

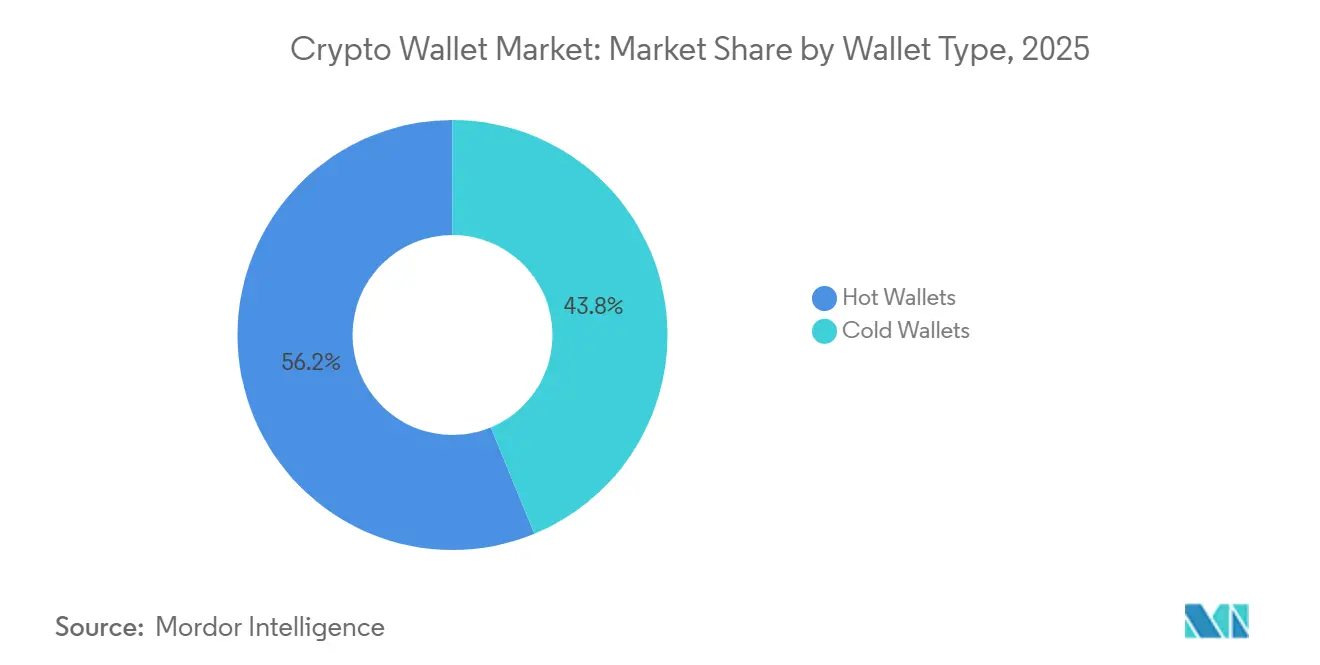

- By wallet type, hot wallets led with 56.23% revenue share of the crypto wallet market in 2025, while cold wallets are forecast to expand at a 25.74% CAGR through 2031.

- By application, trading accounted for a 44.28% share of the crypto wallet market in 2025, while peer-to-peer payments are advancing at a 25.34% CAGR through 2031.

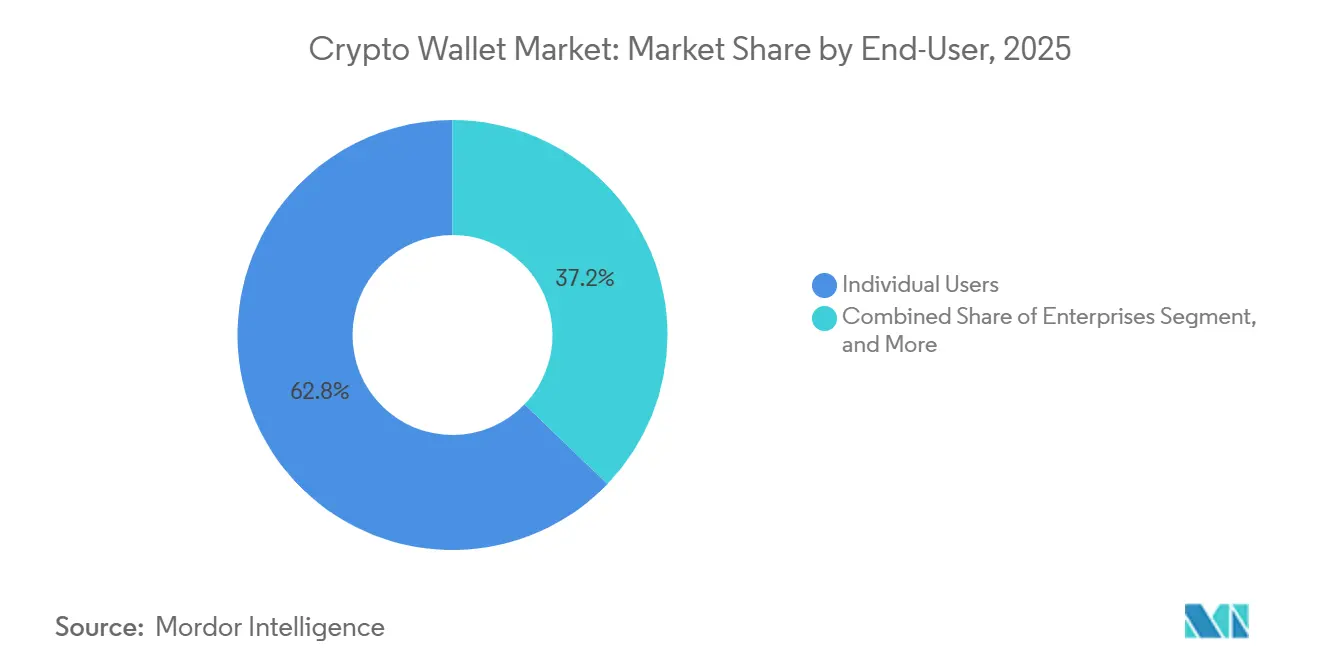

- By end user, individual users accounted for 62.81% of the demand of the crypto wallet market in 2025, while enterprises posted the highest projected CAGR of 35.54% through 2031.

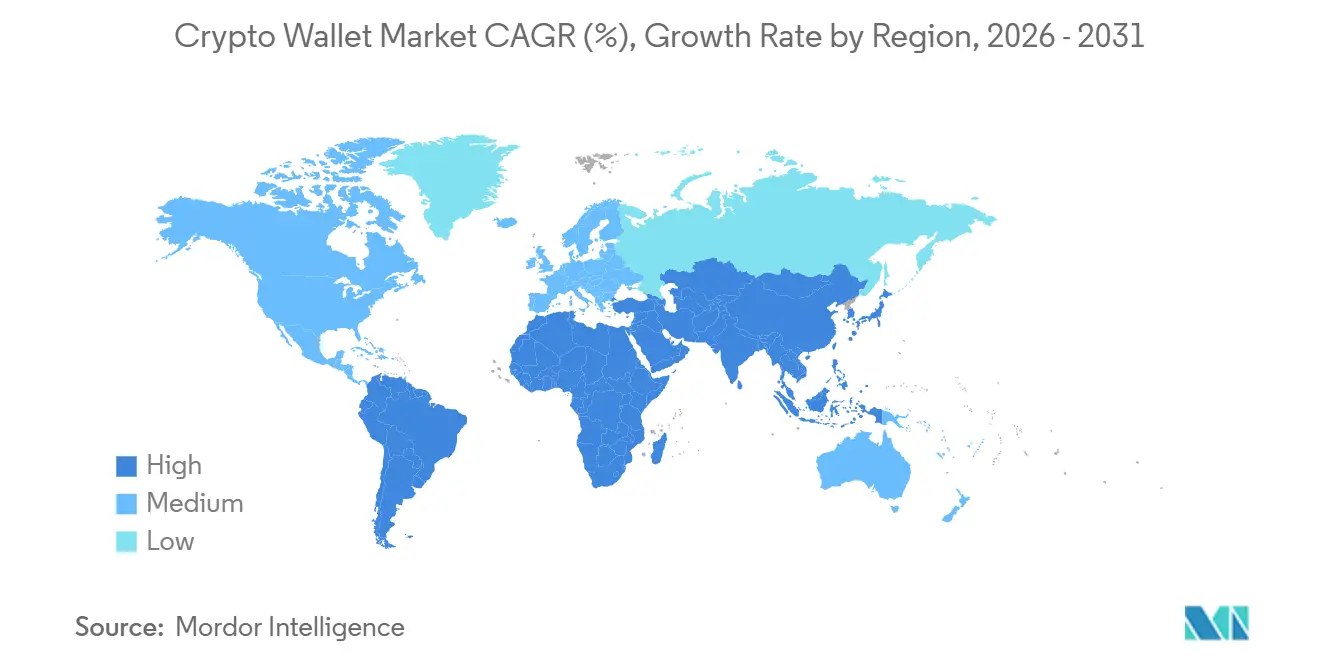

- By geography, Asia-Pacific accounted for 36.81% of the crypto wallet market's revenue in 2025 and is also the fastest-growing regional segment, with a 25.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Crypto Wallet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding DeFi and Web3 Participation | +5.2% | Global, with intensity in APAC and North America | Medium term (2-4 years) |

| Rising Institutional and Treasury Adoption | +4.6% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Stablecoin-Based Remittance and Payments Utility | +4.0% | APAC, South America, Africa, Middle East core | Short term (≤ 2 years) |

| Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion | +3.4% | APAC, Middle East and Africa, South America | Short term (≤ 2 years) |

| Account Abstraction and Seedless Recovery Reducing User Friction | +2.8% | Global, concentrated in EVM-compatible ecosystems | Medium term (2-4 years) |

| AI-Agent and Machine-Wallet Demand | +2.2% | North America and APAC core, early stage globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding DeFi and Web3 Participation

DeFi has become a major structural driver of demand for the crypto wallet market, as wallets are now the primary interfaces for swaps, staking, liquidity provision, and access to tokenized assets. Activity is no longer concentrated in experimental retail use, as wallet-linked execution is increasingly tied to broader on-chain financial activity and a wider set of applications. Embedded swap activity via wallet providers rose meaningfully in 2025, reinforcing the wallet's role as a transaction layer rather than a passive storage tool. Tokenized real-world assets also expanded sharply by 2025, underscoring the need for custody interfaces that support compliant ownership, auditable movement, and direct user control. As more users interact with DeFi directly from wallet environments, the crypto wallet market is seeing stronger monetization opportunities through swaps, routing, and premium security features. This is why the crypto wallet market continues to benefit when wallet-native execution gains share relative to exchange-native execution.

Rising Institutional and Treasury Adoption

Institutional buying has become a major driver of the crypto wallet market because treasury use requires stronger controls than consumer trading. Public company participation widened further by 2026, and Strategy Inc. alone held 818,869 BTC as of May 11, 2026, which illustrates how treasury-scale adoption can reshape wallet demand and custody architecture. A Coinbase institutional survey released in 2025 found that more than 75% of respondents planned to increase their digital asset allocations in 2025, and 84% were already using or considering stablecoins, pointing to broader demand for regulated wallet infrastructure. The institutional requirement is moving beyond simple hot-and-cold separation toward multi-party computation, policy controls, and regulated settlement connectivity, which raises the value of enterprise wallet platforms. U.S. accounting and custody changes also widened the addressable base for banks and licensed providers, which supports a larger long-term opportunity for the crypto wallet market. As these buyers enter, the crypto wallet market is becoming more service-led and compliance-led, not only feature-led.

Stablecoin-Based Remittance and Payments Utility

Stablecoin payment flows are expanding the crypto wallet market by giving wallets a direct role in remittances, payroll, and business settlements. A consortium study covering 33 stablecoin payment firms recorded USD 136 billion in stablecoin payments between January 2023 and August 2025, with an annualized run rate of USD 122 billion by August 2025, including USD 76 billion annualized in B2B flows alone. The Federal Reserve stated in March 2026 that payment stablecoins are a credible form of money for cross-border infrastructure, and its analysis linked higher remittance costs with higher USDT and low-value BTC flows, which supports wallet adoption in expensive corridors.[1]Kyungmin Kim, Romina Ruprecht, and Mary-Frances Styczynski, “Payment Stablecoins and Cross-Border Payments: Benefits and Implications for Monetary Policy Implementation,” FEDS Notes, federalreserve.gov BIS research also identified large-scale cross-border USDC and USDT activity, reinforcing the role of wallets in everyday transfers rather than solely in speculative turnover. This matters for the crypto wallet market because payment and remittance use cases increase transaction frequency and create retention that is less tied to token price cycles. It also broadens the crypto wallet market in emerging regions, where transfer costs and local currency pressures make stablecoin wallets more practical.

Mobile-First Onboarding and Fiat-to-Crypto Rails Expansion

Mobile-first onboarding remains an important support for the crypto wallet market because most new users in high-growth countries enter the market on phones, not desktops. The strongest adoption pattern is evident in markets where wallets connect to local payment rails, reducing the steps between fiat funding and on-chain use. This matters because conversion depends less on awareness and more on whether the user can complete funding and first use with minimal friction. The Zengo and Onramper partnership announced in November 2025, which added access to more than 130 local payment methods, illustrates how wallet providers are widening local on-ramp coverage to improve activation across South America, Southeast Asia, and Africa. As more providers build around local payment behavior, the crypto wallet market is becoming more regional in distribution strategy, even while infrastructure remains global. This is also helping the crypto wallet market keep mobile wallets ahead in revenue, even as desktop-linked workflows remain important for advanced DeFi usage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Private Key and Seed Phrase Complexity | -3.2% | Global, more pronounced in emerging markets and among new users | Short term (≤ 2 years) |

| Rising Phishing, Drainers, and Wallet Exploits | -2.8% | Global, peak risk in high-liquidity DeFi ecosystems | Short term (≤ 2 years) |

| Fragmented Self-Custody Compliance and Travel Rule Burden | -1.9% | North America and Europe, spill-over to APAC and Middle East and Africa | Medium term (2-4 years) |

| Hardware Wallet Cost Inflation and Secure-Element Supply Risk | -1.4% | Global, concentrated in mature economies and institutional buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Private Key and Seed Phrase Complexity

Private key and seed phrase management remains a basic friction point for the crypto wallet market because fund recovery still depends on user behavior that feels unfamiliar to most consumers. The risk is not only technical difficulty but also the permanent loss scenario that can result from a simple mistake or poor backup practices. ThreatFabric disclosed the Crocodilus Android malware in 2025, and the attack used fake urgent backup prompts to trick users into revealing wallet phrases directly on compromised devices. In response, the crypto wallet market is moving toward account abstraction, smart wallets, and recovery models that reduce direct phrase handling, and Ethereum.org reported more than 26 million ERC-4337 smart wallet deployments with over 170 million UserOperations by April 2026.[2]Ethereum Foundation, “Account Abstraction,” Ethereum.org, ethereum.org Even so, migration takes time because existing users must be re-educated while new users must learn a different security model from the start. Until that transition becomes more standard, the crypto wallet market will continue to face a usability ceiling among less experienced users.

Rising Phishing, Drainers, and Wallet Exploits

Phishing and interface-level attacks are constraining the crypto wallet market because they target the exact layer where users approve transactions and trust what they see. State Street cited the February 2025 Bybit hack, in which USD 1.5 billion was stolen through a compromised multisig interface, as a clear example that front-end weaknesses can defeat even hardware-anchored setups. Blockaid documented in April 2026 that wallet drainers were using fake revoke sites and social media impersonation to exploit victims, showing how quickly attack methods are adapting to user behavior rather than protocol bugs. This threat pattern raises customer acquisition costs because providers must invest more in simulation tools, warning systems, and clear signing. It also changes how users choose products, which is pushing the crypto wallet market toward premium security features as a point of differentiation. As long as phishing remains the most visible risk, the crypto wallet market will grow with a higher premium on verification, education, and transaction transparency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wallet Type: Institutional Capital Pulls Cold Wallets Into Growth Lead

Hot wallets accounted for 56.23% of revenue in 2025, keeping them at the center of the crypto wallet market as the most practical option for daily trading, DeFi access, and frequent swaps. Their lead reflects the continued preference for internet-connected wallets when users need immediate execution, dApp connectivity, and simple portfolio movement. Mobile, web, and desktop hot wallets each still serve distinct user groups, with mobile favored for daily transfers and browser-linked setups preferred for deeper DeFi activity. The convenience advantage remains strong, which is why hot wallets have maintained the broadest commercial reach in the crypto wallet industry. Hot wallets also benefit from wallet-native transaction growth, as users can now swap, bridge, and interact with protocols without returning to centralized exchange interfaces.

Cold wallets are the fastest-growing type, with the crypto wallet market size for cold wallets projected to expand at a 25.74% CAGR through 2031. That growth reflects institutional treasury buying, higher sensitivity to counterparty risk, and stronger demand from users holding larger balances for longer periods. Strategy Inc.'s treasury position highlights why large holders increasingly depend on cold storage architecture for asset segregation and approval control. Hardware providers responded with more advanced products in 2025, including Ledger Nano Gen5 and Trezor Safe 7, both of which pushed security and usability improvements further into the mainstream. A hybrid model is now common, in which software wallets handle daily activity and hardware signers protect reserve balances, reshaping how the crypto wallet market is monetized across device and software layers. Paper wallets remain a minor and declining niche because they offer limited verification, poor usability, and little alignment with current compliance expectations.

By Application: Trading Keeps Scale While Payments and Remittance Use Expand

Trading retained 44.28% of application revenue in 2025, making it the largest use case in the crypto wallet market and keeping execution features at the center of competition. This position reflects the ongoing shift of swaps and derivative access into wallet interfaces, where users can route activity without relying on centralized exchanges. The addition of perpetual trading and access to prediction markets by leading wallet brands in 2025 and 2026 also shows how providers are trying to capture more high-frequency activity at the wallet layer. Trading, therefore, remains the main revenue anchor in the crypto wallet market, especially for active users who value speed, routing, and chain connectivity. It also explains why consumer-facing wallet brands still compete heavily on app experience and integrated financial tools.

Peer-to-peer payments are the fastest-growing application, with the crypto wallet market size for this segment projected to rise at a 25.34% CAGR through 2031. The main support comes from stablecoin settlement, where lower-cost transfers are drawing activity away from traditional remittance channels in high-friction corridors. BIS research on cross-border stablecoin flows and the World Bank remittance cost benchmark together support the view that wallet-based transfer models are solving a real price problem for small-value users. Merchant payments and e-commerce are also maturing, supported by large payment ecosystems and rising stablecoin-linked card usage. DeFi and Web3 access remains an important application because every new protocol connection increases session frequency and keeps the wallet central to on-chain behavior. This mix means the crypto wallet market is becoming less dependent on trading alone and more balanced across payments, commerce, and application access.

By End-User: Commercial Demand Becomes the Main Revenue Upgrade Path

Individual users accounted for 62.81% of end-user demand in 2025, keeping retail users as the volume base of the crypto wallet market. This segment still matters because self-custody, swaps, staking, and Web3 access all depend on broad user participation and familiarity with apps. Consumer brands such as Ledger, Trezor, Phantom, and Exodus continue to shape awareness, design expectations, and first-use experiences across the crypto wallet market. Retail behavior also continues to influence the direction of software integration, especially around mobile access, browser connectivity, and recovery design. Even with stronger enterprise growth, the consumer layer remains the part of the crypto wallet industry that drives brand mindshare and product discovery.

Enterprises are the fastest-growing end-user segment, with the crypto wallet market for this segment projected to grow at a 35.54% CAGR through 2031. This growth is important because commercial demand tends to carry higher transaction values and a stronger willingness to pay for approvals, reporting, and policy controls. The segment includes small and medium enterprises using wallets for payroll, accounts payable, and treasury movement, as well as larger entities that require programmable governance and secure settlement flows. BitGo's federally chartered bank structure and regulated trust positioning also show how service depth is becoming a key differentiator for enterprise buyers. Financial institutions and fintechs are entering through licensing and infrastructure partnerships, while merchants and payment providers are accelerating stablecoin wallet integration through card and settlement networks. Web3 developers remain a smaller segment, but they continue to influence architecture through embedded wallet SDKs and programmable account needs.

Geography Analysis

Asia-Pacific held 36.81% of the crypto wallet market share in 2025 and is also the fastest-growing region, with a 25.24% CAGR through 2031. That combination shows that the crypto wallet market in Asia-Pacific is not growing from a small base, but from deep and broad user demand. India remained the global leader in crypto adoption through 2025, and the country also recorded USD 338 billion in on-chain transaction volume, which supported its leading position. Japan and South Korea added a different layer of demand, with regulatory progress, high trading intensity, and stronger stablecoin usage supporting regional wallet activity. Pakistan and Vietnam also moved toward more formal policy recognition in 2025, which supports the next wave of regional wallet adoption in remittance-heavy and mobile-first markets. This mix keeps Asia-Pacific at the center of the crypto wallet market across both retail and professional use.

North America and Europe remained the main poles of institutional demand in the crypto wallet market during 2025 and 2026. In North America, the United States benefited from clearer, more stable direction on stablecoins and market structure, which reduced some of the hesitation around custody integration and regulated access. Strategy Inc.'s May 2026 filing noted that major banks, including Morgan Stanley, Goldman Sachs, and Citigroup, had announced bitcoin trading, custody, and lending services, reflecting a more normalized institutional environment. In Europe, full MiCA enforcement in 2026 and related reporting rules raised the operating bar for providers by increasing authorization, record-keeping, and disclosure requirements.[3]European Commission, “Commission Delegated Regulation (EU) 2025/1140,” Official Journal of the European Union, eur-lex.europa.eu That favors larg, nd better-capitalized firms gradually reshaping the crypto wallet market in Europe toward fewer providers with stronger compliance capacity.

South America, the Middle East, and Africa added a different demand profile to the crypto wallet market, with stablecoins playing a more functional role in treasury preservation, merchant settlement, and cross-border transfers. South American adoption is supported by local-currency pressure, and a consortium study showed that Colombian companies using USD-pegged stablecoins materially reduced inflation losses on treasury funds, while USDC captured a large share of stablecoin volume in Argentina. Brazil also improved the operating environment in 2025 through secondary rules under its Virtual Assets Law, which enabled wallet providers to gain greater market participation. In the Middle East and Africa, the UAE is positioning itself as a premium institutional hub, while sub-Saharan Africa recorded more than 50% year-over-year growth in on-chain transaction volumes in 2025, led by retail transfers below USD 10,000. Together, these regions are expanding the crypto wallet market through practical payment use cases rather than solely on trading demand.

Competitive Landscape

The crypto wallet market has a clear multi-tier structure, with institutional infrastructure providers, hardware specialists, and software wallet brands each competing on different capabilities. BitGo, Fireblocks, and Cobo focus on regulated custody, approval controls, and settlement connectivity, while Ledger, Trezor, Tangem, and other device makers compete on physical security and form factor. Software brands such as Phantom, Exodus, Zengo, Argent, Zerion, and SafePal compete more heavily on chain support, usability, and embedded financial services. This structure means the crypto wallet market is fragmented by product model, even when a few brands dominate mindshare in their own categories. It also explains why competition is increasingly shifting from basic wallet access toward full platform design.

Platform expansion was one of the clearest competitive themes in 2025 and 2026 across the crypto wallet market. Ledger transferred stewardship of the Clear Signing initiative to the Ethereum Foundation in May 2026, and the working group includes Trezor, Fireblocks, MetaMask, and WalletConnect, which shows a coordinated move toward open transaction-legibility standards. Ledger also expanded product depth with Wallet 4.0 and access to perpetual trading, pushing its offering beyond device-led security alone.[4]Ledger, “Release Notes Q1, 2026: Trade Different via Ledger Wallet 4.0,” Ledger, ledger.com Exodus closed its USD 175 million acquisition of Monavate and Baanx on May 1, 2026, which brought card-program management and stablecoin settlement infrastructure into its self-custody stack. BitGo strengthened its institutional position through federally chartered banking status and off-exchange settlement connectivity, reinforcing the service moat around its regulated custody. These moves show that the crypto wallet market is rewarding breadth of service as much as product security.

The crypto wallet market also has clear white spaces where competition is still emerging. AI-agent wallet infrastructure is one of them, and Coinbase launched Agentic Wallets in February 2026 to support autonomous AI systems on the x402 protocol. Commercial treasury and payroll tools are another area, because enterprise demand is rising faster than the supply of purpose-built wallet platforms. Mid-market institutional buyers also occupy a useful gap between retail hardware signers and large enterprise MPC suites, leaving room for hybrid providers with simpler yet still controlled solutions. Consolidation is already visible, and eToro's acquisition of Zengo in April 2026 shows that established fintech firms prefer to buy self-custody capability rather than build it slowly from scratch. That pattern suggests the crypto wallet market will remain active on M&A as platform providers race to control both custody and financial access layers.

Crypto Wallet Industry Leaders

Ledger SAS

Trezor Company s.r.o.

Phantom Technologies, Inc.

BitGo Holdings, Inc.

Exodus Movement, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ledger SAS transferred stewardship of the Clear Signing (ERC-7730) initiative to the Ethereum Foundation, establishing a neutral open standard to eliminate blind-signing risks across the industry. The working group includes Trezor, Fireblocks, MetaMask, and WalletConnect, with implications for global user protection standards.

- May 2026: Exodus Movement, Inc. closed its USD 175 million acquisition of Monavate and Baanx from W3C Corp on May 1, 2026, integrating card-program management and stablecoin-settlement infrastructure into its self-custody wallet stack. The company also announced a multi-year partnership as the UFC's official payments partner.

- April 2026: BitGo, Inc. announced on April 23, 2026, the integration of OKX into its Go Network Off-Exchange Settlement solution, enabling U.S. institutional clients to trade on OKX while assets remain in BitGo Bank and Trust's federally chartered cold custody, reducing counterparty exposure and pre-funding requirements.

- April 2026: eToro Group Ltd. announced the acquisition of Zengo Ltd. on April 15, 2026, to expand self-custodial crypto capabilities and bridge traditional brokerage with on-chain DeFi infrastructure, integrating Zengo's MPC keyless architecture into eToro's 38 million-user platform.

Global Crypto Wallet Market Report Scope

The Crypto Wallet Market comprises software-based and hardware-based solutions that enable users and organizations to securely store, manage, transfer, receive, and interact with cryptocurrencies and blockchain-based digital assets. Crypto wallets function as interfaces for managing cryptographic keys, executing blockchain transactions, accessing decentralized finance (DeFi) applications, participating in Web3 ecosystems, managing digital assets such as NFTs, and enabling crypto-based payments and remittances.

The Crypto Wallet Market Report is Segmented by Wallet Type (Hot Wallets, and Cold Wallets), Application (Trading, Peer-To-Peer Payments, Remittance, Merchant Payments and E-Commerce, and DeFi and Web3 Access), End-User (Individual Users, Enterprises, Crypto-Native Institutions, Financial Institutions and Fintechs, Merchants and Payment Providers, and Web3 Studios and Developers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hot Wallets |

| Cold Wallets |

| Trading |

| Peer-To-Peer Payments |

| Remittance |

| Merchant Payments and E-Commerce |

| DeFi and Web3 Access |

| Individual Users |

| Enterprises |

| Crypto-Native Institutions |

| Financial Institutions and Fintechs |

| Merchants and Payment Providers |

| Web3 Studios and Developers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Wallet Type | Hot Wallets | ||

| Cold Wallets | |||

| By Application | Trading | ||

| Peer-To-Peer Payments | |||

| Remittance | |||

| Merchant Payments and E-Commerce | |||

| DeFi and Web3 Access | |||

| By End-User | Individual Users | ||

| Enterprises | |||

| Crypto-Native Institutions | |||

| Financial Institutions and Fintechs | |||

| Merchants and Payment Providers | |||

| Web3 Studios and Developers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 to 2031 outlook for crypto wallet revenue?

The Crypto wallet market is projected to grow from USD 12.52 billion in 2026 to USD 37.21 billion by 2031, at a CAGR of 24.34%.

Which region is leading crypto wallet demand?

Asia-Pacific led with 36.81% of revenue in 2025 and is also the fastest-growing regional segment, with a 25.24% CAGR through 2031.

Why are cold wallets growing faster than hot wallets?

Cold wallets are expanding at a 25.74% CAGR because institutional buyers and larger holders want stronger isolation, long-duration custody, and more controlled approval flows.

Which application is growing fastest in wallet usage?

Peer-to-peer payments is the fastest-growing application at a 25.34% CAGR, supported by rising stablecoin use in remittance and settlement corridors.

What is driving commercial demand for wallet platforms?

Enterprises are projected to grow at a 35.54% CAGR as enterprises adopt wallets for treasury, payroll, accounts payable, and B2B settlement with stronger audit and policy controls.

How is competition changing among wallet providers?

Competition is moving beyond storage and signing toward broader platforms, including regulated custody links, card and settlement services, clear-signing standards, and AI-agent wallet capabilities.

Page last updated on: