Stablecoin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

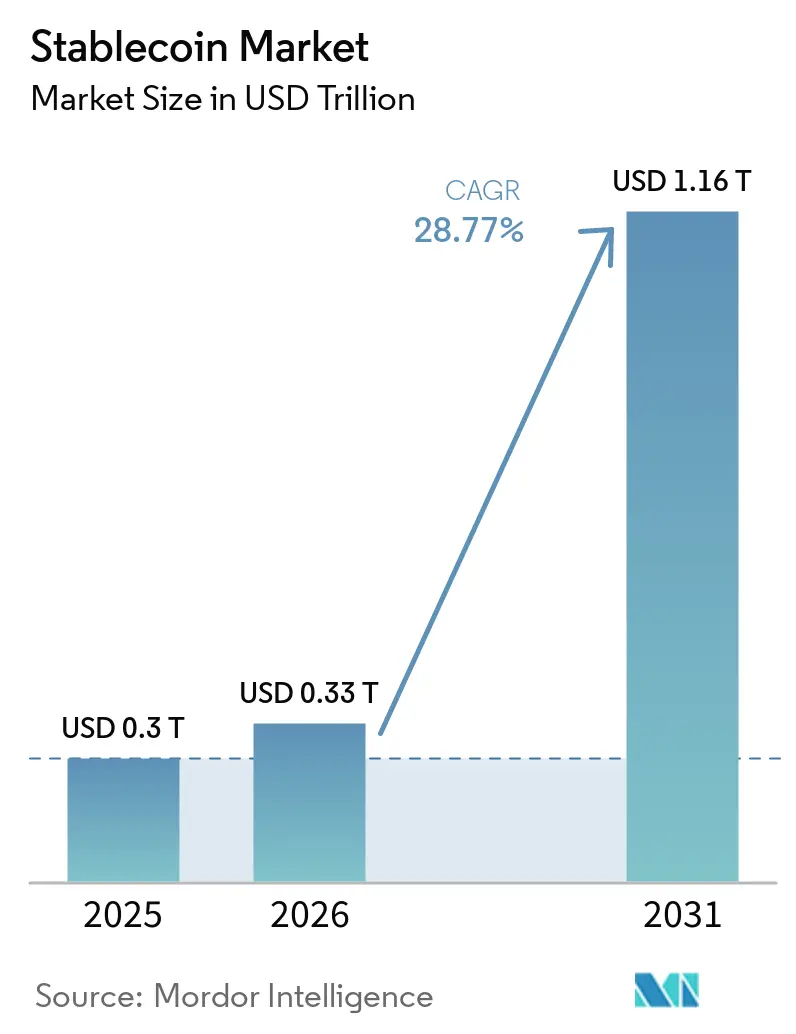

| Market Size (2026) | USD 0.33 Trillion |

| Market Size (2031) | USD 1.16 Trillion |

| Growth Rate (2026 - 2031) | 28.77% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stablecoin Market Analysis by Mordor Intelligence

The Stablecoin Market size is expected to grow from USD 0.3 trillion in 2025 to USD 0.33 trillion in 2026 and is forecast to reach USD 1.16 trillion by 2031 at 28.77% CAGR over 2026-2031.

The stablecoin market is moving from a tool used mainly inside crypto trading into a broader settlement layer for treasury operations, cross-border business payments, and digital commerce. Regulatory progress in the United States and Europe is reducing compliance uncertainty and expanding the potential user base for issuers that meet reserve, disclosure, and governance standards. Enterprise adoption is also becoming more operational in 2026 as treasury platforms and payment providers connect stablecoin settlement to existing business workflows and payout networks. The stablecoin market remains concentrated around the largest issuers, but new products from payment firms, banks, and crypto-native companies are widening the competitive field in regulated and institution-facing niches. Growth still faces limits from concerns about reserve transparency and fragmented licensing, yet those same gaps are creating opportunities for compliant issuers, custody providers, and payment infrastructure firms as implementation moves forward.

Key Report Takeaways

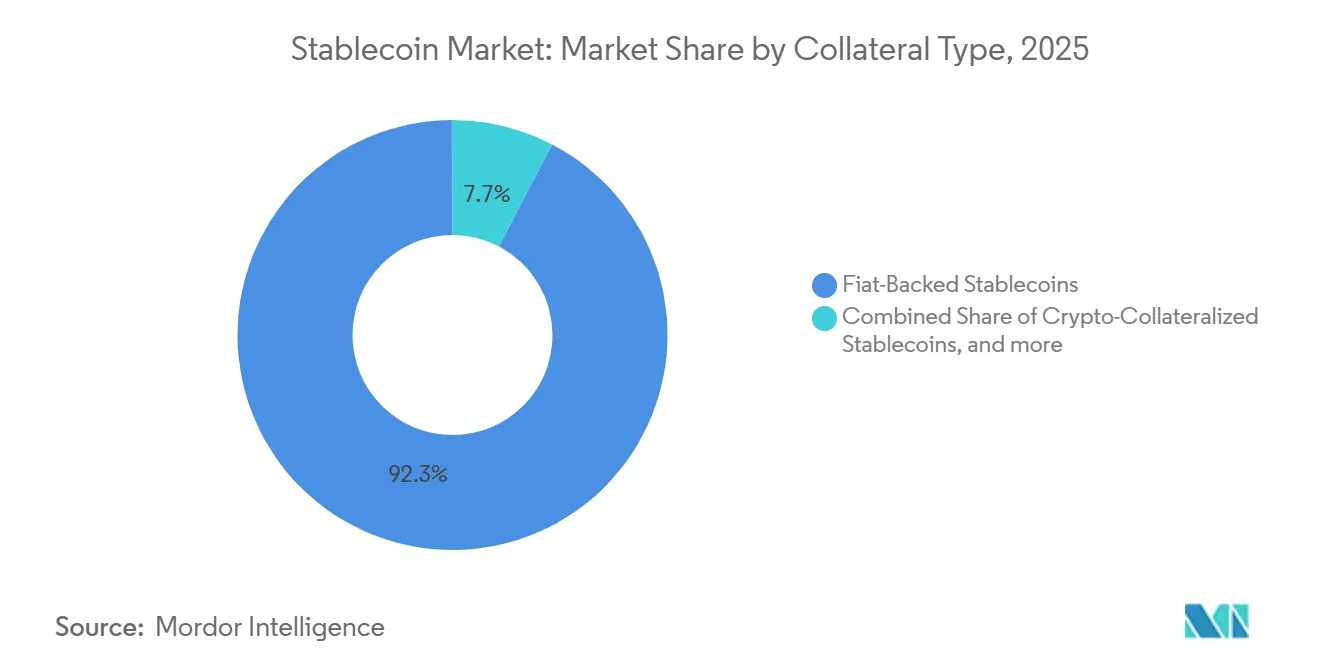

- By collateral type, fiat-backed stablecoins captured 92.3% of the stablecoin market share in 2025, while hybrid and algorithmic formats in the stablecoin market are projected to grow at 44.8% CAGR through 2031.

- By blockchain platform, Tron held a 34.9% share of the stablecoin market in 2025, while layer-2 networks are projected to grow at a 39.5% CAGR through 2031.

- By application, cryptocurrency trading and liquidity management accounted for 47.2% of the stablecoin market share in 2025, while cross-border payments and remittances are projected to grow at a 36.5% CAGR through 2031.

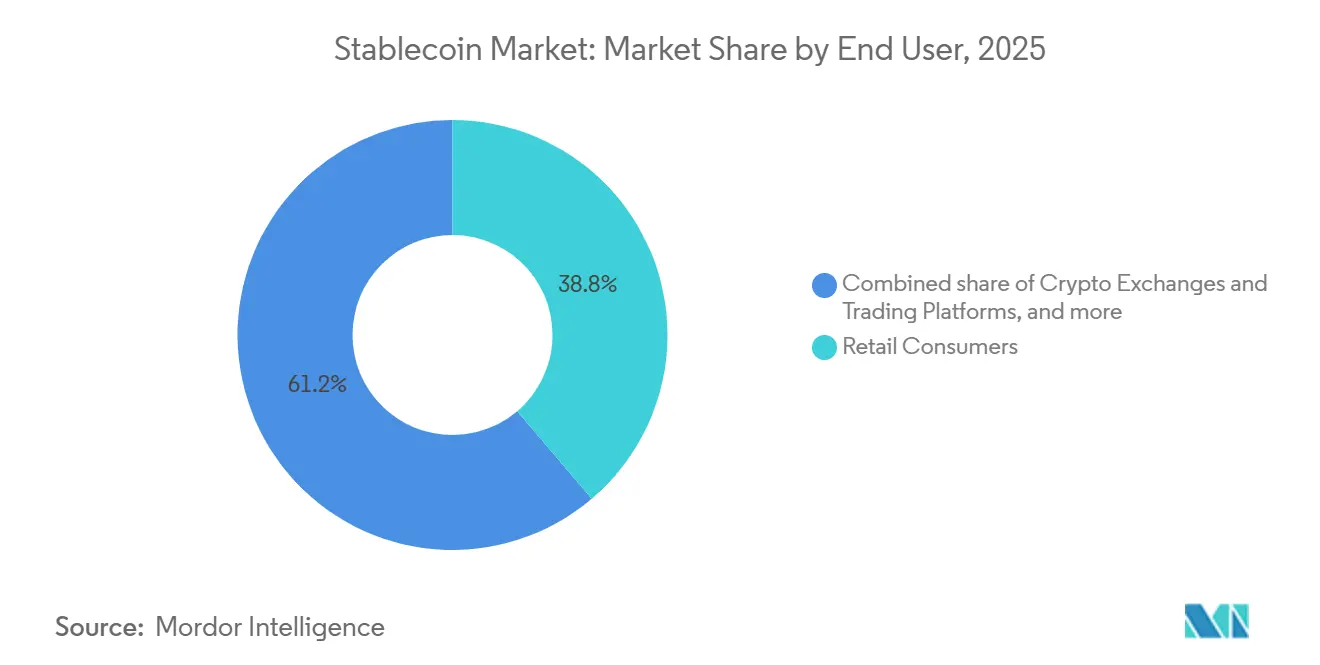

- By end user, retail consumers held 38.8% of the stablecoin market share in 2025, while financial institutions and payment service providers are projected to grow at a 34.2% CAGR through 2031.

- By distribution channel, centralized exchanges accounted for 59.4% of the stablecoin market in 2025, while payment gateways and fintech platforms are projected to grow at a 37.3% CAGR through 2031.

- By geography, Asia-Pacific accounted for 39.6% of the stablecoin market size in 2025, while the Middle East and Africa in the stablecoin market is projected to grow at 35.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stablecoin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Cross-Border Settlement | +5.5% | Global, with concentrated early gains in the Middle East and Africa, South Asia, and Latin America | Short term (≤ 2 years) |

| Liquidity Bridge for Crypto Trading and DeFi | +4.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Regulatory Clarity for Reserve-Backed Stablecoins | +6.2% | North America and Europe, with spillover to the Asia-Pacific and Middle East, and Africa | Short term (≤ 2 years) |

| Treasury Yield Economics Supporting Issuer Scale | +3.9% | North America and Europe | Medium term (2-4 years) |

| On-Chain Treasury and Cash Management for Enterprises | +4.1% | North America, Europe, and core Asia-Pacific, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Synthetic Stablecoin Risk Segmentation and Yield Demand | +3.2% | Global, with early gains in DeFi-active markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Cross-Border Settlement

Cross-border payment friction continues to support the stablecoin market because stablecoin rails can settle at any time and reduce reliance on slower correspondent banking chains. This matters most in corridors where transfer fees, settlement delays, and limited foreign exchange access still make traditional systems costly for both individuals and businesses. The stablecoin market is also benefiting from the fact that corridor economics often matter more than formal rulemaking in early adoption environments, especially where users prioritize speed and cost over product complexity. Circle’s Payments Network reported USD 8.3 billion in annualized transaction volume as of March 31, 2026, after expanding fiat payout connectivity through new corridors, including Brazil and Nigeria[1]Circle, “Nium and Circle to Connect USDC Settlement with Global Payouts,” Circle Pressroom, circle.com. This creates an advantage for issuers and partners that can combine low-cost blockchain routes with dependable local cash-out infrastructure in high-volume remittance and B2B payment corridors.

Regulatory Clarity for Reserve-Backed Stablecoins

Regulatory clarity is a major support for the stablecoin market because institutional users have been waiting for clearer expectations on reserves, attestations, custody, and issuer oversight. The GENIUS Act in the United States and MiCA in Europe are setting the first large-scale compliance framework for payment stablecoins, changing how exchanges, banks, and payment firms evaluate distribution partners. The stablecoin market is now separating more clearly between issuers that meet formal operating standards and those that still rely on regulatory gray areas. That split affects platform listings, enterprise partnerships, and the willingness of large financial institutions to integrate stablecoins into customer-facing products. The practical result is that compliance is becoming a distribution advantage rather than merely a legal requirement, reshaping competitive positioning across the stablecoin market.

On-Chain Treasury and Cash Management for Enterprises

Enterprise treasury adoption is becoming a more visible driver of the stablecoin market in 2026 as firms move from testing to live operating workflows. Kyriba announced a collaboration with Circle on April 28, 2026, to embed USDC into treasury systems, enabling enterprise users to manage liquidity and intercompany settlement within existing finance processes. On June 8, 2026, Ledger and Mantu deployed live stablecoin treasury payment flows inside Kyriba’s Treasury Management System using Fipto’s regulated rails for supplier payments and cross-border intercompany transfers[2]Fipto, “Ledger and Mantu Deploy Enterprise Stablecoin Treasury via Kyriba, Powered by Fipto,” Fipto, fipto.com. The stablecoin market benefits from these deployments because they demonstrate that treasury teams can use round-the-clock settlement without rebuilding their finance stacks from scratch. This use case is also more compliance-sensitive than retail payments, which means regulated issuers and regulated service partners are likely to capture a larger share of future enterprise demand.

Liquidity Bridge For Crypto Trading And DeFi

Crypto trading and DeFi liquidity remain a core growth engine for the stablecoin market because stablecoins still function as the main unit of account and collateral layer across centralized and decentralized trading venues. Quarterly stablecoin trading volume exceeded USD 28 trillion by early April 2026, representing 75% of overall crypto trading volume in the source draft, which shows how deeply stablecoins are embedded in market infrastructure. On-chain transaction volume also expanded sharply through 2025 as collateral reuse, lending activity, and yield strategies kept capital circulating across DeFi protocols. The stablecoin market is also being shaped by infrastructure migration, as major issuers increasingly treat leading Layer-2 networks as permanent venues rather than temporary extensions of mainnet ecosystems. This matters because native issuance on scalable chains can deepen liquidity, reduce friction from bridge risk, and strengthen issuer positioning where DeFi settlement becomes more cost-sensitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reserve Transparency and Redemption Confidence Gaps | -2.1% | Global, most acute in markets without formal issuer oversight | Short term (≤ 2 years) |

| Fragmented Global Licensing and Compliance Burden | -3.8% | Global, particularly Asia-Pacific and Middle East, and Africa, where frameworks are nascent | Medium term (2-4 years) |

| Limited Payments Penetration Beyond Crypto-Native Use | -2.4% | Emerging markets, including South America and Sub-Saharan Africa | Long term (≥ 4 years) |

| Market Concentration Limits New Issuer Network Effects | -1.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reserve Transparency and Redemption Confidence Gaps

Reserve transparency remains a direct limit on the stablecoin market because institutional users still place a high value on clear redemption mechanics, verified reserves, and consistent reporting standards. Even with new regulations, implementation is not yet complete across all major markets, meaning many investors and operating partners still rely on voluntary attestations and uneven disclosure practices. The stablecoin market is therefore developing a quality gap between the largest issuers, which adhere to stronger disclosure standards, and smaller issuers that struggle to consistently demonstrate reserve strength. DeFi protocols are also becoming more selective in their collateral acceptance as on-chain reserve verification tools gain traction, potentially reducing the addressable market for issuers that fail to meet rising transparency expectations. The European Central Bank also warned in July 2025 that differences between United States and European rules could create regulatory arbitrage and raise systemic concerns if under-supervised issuers find indirect access into stricter markets[3]European Central Bank, “From Hype to Hazard, What Stablecoins Mean for Europe,” ECB Blog, ecb.europa.eu.

Fragmented Global Licensing and Compliance Burden

Fragmented licensing adds cost and execution risk to the stablecoin market because issuers and distributors must navigate different reserve rules, issuer categories, disclosure standards, and market access requirements across regions. Asia-Pacific alone reflects this tension, with Singapore advancing a labeled stablecoin framework while other jurisdictions continue to debate permissible issuer structures or tighten restrictions on private stablecoin issuance. The stablecoin market, therefore, rewards scale because large issuers can fund legal, compliance, custody, and reporting infrastructure across multiple regions simultaneously. Smaller challengers face a harder path because cross-border distribution now depends not only on product demand but also on the ability to satisfy multiple supervisory expectations without slowing launch timelines. Europe has also raised the entry bar through MiCA licensing pathways, which support market formalization but can limit the pace at which new entrants expand beyond narrow regional or product niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collateral Type: Fiat Dominance Persists as Yield Structures Gain Institutional Traction

Fiat-backed stablecoins held 92.3% of the market in 2025, indicating that reserve-backed dollar instruments still set the baseline for the stablecoin market. USDT and USDC together accounted for approximately 83% of total supply, while other fiat-backed issuers, such as Paxos with USDP and USDG, PayPal with PYUSD, First Digital Trust with FDUSD, and Ripple with RLUSD, remained more focused on targeted compliance and institutional niches. This pattern shows that trust, liquidity depth, and exchange acceptance still matter more than product variety in the largest part of the stablecoin market. Crypto-collateralized stablecoins such as MakerDAO’s DAI remain structurally important because they continue to serve as core collateral in DeFi lending and trading systems. Commodity-backed tokens, including Tether Gold and Paxos Gold, also benefited from stronger gold prices in 2025, and Tether’s February 2026 USD 150 million purchase of a 12% stake in Gold.com linked tokenized gold distribution more directly to precious metals demand.

Hybrid and algorithmic stablecoins are projected to expand at a 44.8% CAGR through 2031, making them the fastest-growing collateral segment in the stablecoin market. Growth is being driven by demand for yield-bearing structures that offer an alternative to zero-yield reserve-backed models, especially among institutional allocators seeking greater capital efficiency from digital dollar exposure. Ethena’s USDe is a clear example because it uses a synthetic dollar structure built on delta-neutral perpetual derivative positions rather than simple reserve storage. The current generation of synthetic products is materially different from the purely algorithmic formats that failed in 2022, because the newer designs are more risk-segmented and closer in form to structured credit products. Even so, the stablecoin market still faces a policy gap here because regulation has not fully codified how these newer structures should be supervised, leaving room for growth and a clear downside risk if oversight tightens abruptly.

By Blockchain Platform: Tron Anchors Retail Volume While Layer-2 Networks Restructure Settlement Infrastructure

Tron held a 34.9% share in 2025, making it the largest blockchain platform segment in the stablecoin market. That position reflects its very low transaction fees and its role as the preferred route for retail USDT transfers in emerging market corridors across Southeast Asia, Sub-Saharan Africa, and Latin America. The stablecoin market on Tron remains closely tied to payment utility rather than solely to speculation, as many users rely on it as the cheapest available option for routine cross-border transfers. Ethereum still maintained a large position because of its role in institutional DeFi, high-value settlement, and broader application support. Binance Smart Chain and Solana also served distinct user groups, and PYUSD on Solana benefited from sub-cent fees and growing interest from institutional payment processors.

Layer-2 networks are projected to grow at a 39.5% CAGR through 2031, making them the fastest-growing segment of the stablecoin market. The source draft stated that these networks processed more than 1.9 million daily transactions in 2025 and that stablecoins accounted for more than 70% of Layer-2 transaction volume, underscoring the close link between scaling adoption and stablecoin usage. It also stated that Layer-2 adoption reached 85% of Ethereum transaction throughput by late 2025, while Base processed more than 30% of the United States stablecoin transactions through strong USDC volumes. A major operating shift is the move from bridged contracts to native stablecoin issuance on leading Layer-2 networks, and Arbitrum’s migration from USDC.e to native USDC by late 2025 reflected that change. This matters for the stablecoin market because issuers that establish native liquidity early on scalable chains can defend market position more effectively than late entrants that rely on bridge-dependent distribution.

By Application: Trading Leads by Share, Cross-Border Payments Sets the Growth Agenda

Cryptocurrency trading and liquidity management accounted for 47.2% of the stablecoin market in 2025, confirming that trading remained the largest application. Stablecoins continue to serve as the primary quote asset for centralized exchange trading pairs and as a key form of collateral across decentralized finance protocols. DeFi also maintained a strong position because lending, leveraged trading, collateral recycling, and yield provisioning all depend on stable, transferable on-chain dollar units. Treasury and cash management deployments were smaller in volume but stood out as high-value institutional use cases because they reduced reliance on pre-funded accounts and improved settlement speed within business workflows. E-commerce and merchant payments were still in early development, yet the source draft noted that Grey Business processed USD 61.4 million in stablecoin-denominated cross-border B2B transaction volume by mid-2026, with USDC and USDT accounting for the largest share of flows on the platform.

Cross-border payments and remittances are projected to grow at a 36.5% CAGR through 2031, making them the fastest-growing application in the stablecoin market. The source draft stated that stablecoins delivered USD 8.6 billion in remittances to Southeast Asia in the first half of 2025, suggesting active displacement of conventional wire-based transfer models on key corridors. This shift is strategically important because the stablecoin market is expanding into a use case where incumbent financial institutions are more likely to become customers or partners than direct rivals. That creates a path for regulated issuers to operate as infrastructure providers to banks, payment service providers, and treasury platforms rather than compete only in crypto-native channels. MoneyGram and NALA reinforced that direction when they announced a stablecoin-powered payout partnership on April 17, 2026 focused on Africa and Asia corridors with near real-time settlement and lower foreign exchange costs[4]MENA Fintech Association, “MoneyGram and NALA Use Stablecoins for Payouts in Africa and Asia,” MENA Fintech Association, mena-fintech.org.

By End User: Retail Volume Anchors the Base, Institutional Adoption Determines the Trajectory

Retail consumers held 38.8% of the stablecoin market share in 2025, making them the largest end-user segment. That result reflected the large installed base of crypto-native users who continue to use stablecoins as their main unit of account for exchange activity, wallet transfers, and on-chain payments. The source draft also noted that monthly stablecoin transactions rose from 314 million in January 2025 to 3.2 billion in December 2025, indicating that retail adoption was still scaling even as institutional use gained greater visibility. Crypto exchanges and trading platforms continued to account for substantial end-user volume because they remain the core liquidity infrastructure for issuance, trading, and redemption flows. This means the stablecoin market still rests on a large retail and exchange foundation, even while its next growth phase is being shaped by business and institutional adoption.

Financial institutions and payment service providers are projected to grow at a 34.2% CAGR through 2031, which makes them the fastest-growing end-user segment in the stablecoin market. Visa launched USDC settlement for the United States banks in December 2025, and Mastercard expanded its network in 2026 to support 6 regulated stablecoins across 6 blockchains, demonstrating that global payment networks now treat stablecoins as a permanent settlement layer rather than a short-term trial. Enterprises and merchants are also scaling adoption through live treasury and settlement use cases, with Corpay, Ledger, and Mantu all cited in the source draft as examples of real operating deployments in 2026. Government and public sector participation remains early, but central banks in Japan, South Korea, and the UAE are monitoring licensed stablecoin frameworks as both complements to and constraints on future CBDC plans. Developers and Web3 platforms also remain steady users because stablecoins continue to fund protocol liquidity, smart contract collateral, and operational cash movement across decentralized applications.

By Distribution Channel: Centralized Exchanges Dominate, Fintech Platforms Capture the Marginal Dollar

Centralized exchanges held 59.4% share in 2025, which made them the leading distribution channel in the stablecoin market. They remain the primary onboarding route for new users and still account for the largest share of volume because exchange-based trading pairs anchor liquidity and price discovery. Decentralized exchanges also contributed meaningfully through liquidity pools and token swaps, while wallet providers remained the direct interface for peer-to-peer transfers and self-custody. OTC desks and institutional brokers retain a specialized role because they offer large-block execution, pricing discretion, and settlement flexibility that public order books cannot always provide efficiently. The stablecoin market, therefore, still depends heavily on exchange-linked liquidity even as payment and enterprise channels become more important.

Payment gateways and fintech platforms are projected to grow at a 37.3% CAGR through 2031, making them the fastest-growing distribution route in the stablecoin market. Modern Treasury’s integration of USDC on Base showed how businesses can manage on-chain balances alongside ACH, wire, and FedNow activity through a single API layer, using a business flow baseline of USD 400 billion in throughput cited in the source draft. That kind of integration matters because it removes much of the technical friction that previously separated conventional payment operations from blockchain-based settlement. Circle also launched CPN Managed Payments on April 8, 2026, with Thunes, Worldline, and Veem as launch partners, so banks, fintechs, payment service providers, and enterprises can access stablecoin settlement without directly managing digital assets. The stablecoin market gains incremental adoption through these familiar interfaces because enterprises are more likely to use stablecoin settlement when it appears as a feature inside existing payment and treasury software rather than as a separate crypto workflow.

Geography Analysis

Asia-Pacific accounted for 39.6% of the stablecoin market in 2025, making it the largest regional market. The region’s leadership reflects a combination of high remittance activity, active participation in exchanges, mobile-first financial behavior, and early regulatory development across markets such as Singapore, Hong Kong, South Korea, and Japan. Retail USDT flows on Tron remained especially important across Southeast Asian corridors because low transaction fees and easy availability fit the needs of price-sensitive users and cross-border senders. South Korea’s Digital Asset Basic Law remained stalled through mid-2026 because policymakers continued to disagree over which issuer categories should be allowed, delaying local-currency stablecoin issuance and keeping global-dollar stablecoins more prominent in the interim. India, Indonesia, Thailand, Vietnam, and Malaysia also remain important growth markets for the stablecoin market because underbanked populations, smartphone-based finance, and meaningful remittance inflows continue to support adoption.

North America and Europe define the compliance frontier for the stablecoin market because both regions are shaping the rules that institutional users are likely to follow. In the United States, final rules under the GENIUS Act are required by July 18, 2026, with the law taking effect within 120 days after that, which places formal institutional market activation on a late 2026 to early 2027 timeline in the source draft. Tether launched USAT in January 2026 through Anchorage Digital Bank, with reserves held at Cantor Fitzgerald, demonstrating how major issuers are preparing product structures specifically for the United States compliance environment. In Europe, the full MiCA transition period ends on July 1, 2026, and the source draft noted that 10 issuers received formal authorization, while USDT had already been removed from regulated EU platforms by the first quarter of 2025. The European Commission also opened a consultation on May 20, 2026, to review whether MiCA remains fit for purpose, and the source draft noted that euro stablecoins represented EUR 774 million, or USD 835.9 million, versus USD 320 billion for dollar-denominated instruments, highlighting the wide current gap between euro and dollar stablecoin activity.

The Middle East and Africa are projected to grow at a 35.6% CAGR through 2031, which makes it the fastest-growing regional segment in the stablecoin market. High remittance dependence, foreign exchange access constraints, and expanding corridor infrastructure are supporting this rise, especially in markets linked to Dubai’s regulatory environment and broader expatriate payment flows. The stablecoin market is also gaining traction in the UAE as firms seek payment routes that reduce reliance on disrupted correspondent banking channels. At the same time, South America, especially Brazil and Argentina, remains important because dollar-linked stablecoins serve as practical tools in foreign-exchange-constrained settings. Argentina was cited in the source draft as accounting for approximately 46% of local stablecoin volumes, while Brazil’s central bank and fintech ecosystem are exploring links with USDC and the PIX instant payment system, which could open a large institutional corridor during the forecast period.

Competitive Landscape

The stablecoin market is highly concentrated at the issuer level, even though the wider value chain remains more diverse. Tether and Circle together held approximately 83% of the total supply in early 2026, which gave the market a concentrated core despite a growing list of new issuers, payment partners, custody providers, and blockchain networks. Competition is increasingly shaped by distribution access, reserve credibility, and regulatory readiness rather than by simple token issuance alone. Circle’s compliance-led strategy gave it a stronger position in regulated environments after it became the first global issuer to achieve full MiCA compliance in July 2024, which helped support a shift in which USDC’s monthly on-chain transaction volume surpassed USDT in April 2026, as noted in the source draft. The stablecoin market is therefore moving toward a structure where legal readiness and enterprise connectivity matter as much as liquidity scale.

Tether has responded with geographic diversification and broader product expansion, rather than relying solely on its legacy USDT base in the stablecoin market. Its January 2026 launch of USAT for the United States institutional segment, its USD 150 million investment in Gold.com, and its June 2026 gold-backed Visa card partnership with Fasset all show a strategy built around extending reserve formats and widening access points across different user groups. Circle has focused more directly on infrastructure and regulated distribution, including CPN Managed Payments, treasury integrations with Kyriba, and partnerships that connect stablecoin settlement with local payouts. Mastercard’s 2026 expansion to support multiple regulated stablecoins across multiple blockchains also suggests that the network layer is preparing for a multi-issuer settlement model rather than a single-token outcome. This matters because the stablecoin market is increasingly shaped by interoperability, software integration, and institutional usability, rather than just token supply.

White-space opportunities remain most visible in regulated euro stablecoins. Non-USD instruments such as AED, SGD, BRL, and INR-linked products, and programmable payment rails can support AI-native transaction workflows. Circle’s August 2025 launch of Arc, an EVM-compatible Layer-1 built for stablecoin-native finance and AI agent integrations, showed how issuers are already positioning for these next use cases. Custody and operating infrastructure firms such as Anchorage Digital, BitGo, and Fireblocks also play an important gatekeeping role, as they determine which stablecoins meet institutional onboarding standards. The stablecoin market is therefore likely to stay concentrated at the top while becoming more layered underneath, with issuers, custodians, payment networks, and enterprise software providers all competing to control access to the next phase of adoption.

Stablecoin Industry Leaders

Tether Limited

Circle Internet Financial, Inc.

PayPal Holdings, Inc.

Paxos Trust Company, LLC

Ethena Labs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Fipto and Kyriba announced that Ledger and Mantu deployed live stablecoin treasury operations inside Kyriba's Treasury Management System in June 2026, using Fipto's regulated rails—the first production-grade regulated stablecoin treasury deployments within an enterprise TMS platform, covering automated supplier payments and cross-border intercompany transfers. This establishes a replicable blueprint for enterprise treasury adoption of digital payments, stablecoins.

- May 2026: Circle and Nium announced a partnership connecting USDC settlement with last-mile payouts across 190+ countries and 100 currencies. Circle's Payments Network reported USD 8.3 billion in annualized transaction volume as of March 31, 2026, reflecting the rapid institutional scaling of CPN.

- April 2026: Circle launched CPN Managed Payments, a full-stack stablecoin settlement platform enabling PSPs, fintechs, banks, and enterprises to access stablecoin rails without managing digital assets directly, with Thunes, Worldline, and Veem as launch partners. USDC cumulative on-chain settlement volume surpassed USD 70 trillion as of March 2026, with Q4 2025 on-chain volume nearing USD 12 trillion.

- April 2026: Kyriba and Circle announced a collaboration to embed USDC capabilities within Kyriba's treasury management platform, enabling enterprise treasury teams to manage intercompany liquidity and access 24/7 on-chain settlement within existing workflows

Global Stablecoin Market Report Scope

| Fiat-Backed Stablecoins |

| Crypto-Collateralized Stablecoins |

| Algorithmic Stablecoins |

| Commodity-Backed Stablecoins |

| Other Stablecoins |

| Ethereum |

| Tron |

| Binance Smart Chain |

| Solana |

| Layer-2 Networks |

| Other Blockchain Platforms |

| Cryptocurrency Trading and Liquidity Management |

| Cross-Border Payments and Remittances |

| Decentralized Finance |

| E-Commerce and Merchant Payments |

| Treasury and Cash Management |

| Other Applications |

| Retail Consumers |

| Crypto Exchanges and Trading Platforms |

| Financial Institutions and Payment Service Providers |

| Enterprises and Merchants |

| Developers and Web3 Platforms |

| Government and Public Sector Entities |

| Centralized Exchanges |

| Decentralized Exchanges |

| Wallet Providers |

| Payment Gateways and Fintech Platforms |

| OTC Desks and Institutional Brokers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Collateral Type | Fiat-Backed Stablecoins | |

| Crypto-Collateralized Stablecoins | ||

| Algorithmic Stablecoins | ||

| Commodity-Backed Stablecoins | ||

| Other Stablecoins | ||

| By Blockchain Platform | Ethereum | |

| Tron | ||

| Binance Smart Chain | ||

| Solana | ||

| Layer-2 Networks | ||

| Other Blockchain Platforms | ||

| By Application | Cryptocurrency Trading and Liquidity Management | |

| Cross-Border Payments and Remittances | ||

| Decentralized Finance | ||

| E-Commerce and Merchant Payments | ||

| Treasury and Cash Management | ||

| Other Applications | ||

| By End User | Retail Consumers | |

| Crypto Exchanges and Trading Platforms | ||

| Financial Institutions and Payment Service Providers | ||

| Enterprises and Merchants | ||

| Developers and Web3 Platforms | ||

| Government and Public Sector Entities | ||

| By Distribution Channel | Centralized Exchanges | |

| Decentralized Exchanges | ||

| Wallet Providers | ||

| Payment Gateways and Fintech Platforms | ||

| OTC Desks and Institutional Brokers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving stablecoin adoption beyond crypto trading?

The strongest expansion areas are cross-border payments, enterprise treasury, and institution-facing settlement workflows. The stablecoin market size is projected to reach USD 1,155.4 billion by 2031, supported by these newer use cases.

Which collateral type currently leads stablecoins?

Fiat-backed stablecoins led with 92.3% share in 2025. That reflects the continued preference for dollar-pegged, reserve-backed instruments in payments, trading, and treasury activity.

Which blockchain is leading stablecoin activity today?

Tron led with 34.9% share in 2025 because of low transaction costs and strong use in retail remittance corridors. Layer-2 networks, however, are the fastest-growing platform segment at 39.5% CAGR through 2031.

Why are financial institutions becoming more active in stablecoins?

Banks, payment firms, and treasury platforms are adopting stablecoins for faster settlement, better liquidity management, and reduced dependence on pre-funded accounts. Financial institutions and payment service providers are projected to grow at 34.2% CAGR through 2031.

Which region leads current activity and which region is growing fastest?

Asia-Pacific held the largest regional share at 39.6% in 2025. Middle East and Africa is the fastest-growing region, with a projected 35.6% CAGR through 2031.

How concentrated is the issuer landscape?

The issuer layer is highly concentrated, with Tether and Circle together holding approximately 83% of supply in early 2026. That is why the market, even though the broader ecosystem is becoming more diverse.

Page last updated on: