Application-Level Encryption Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

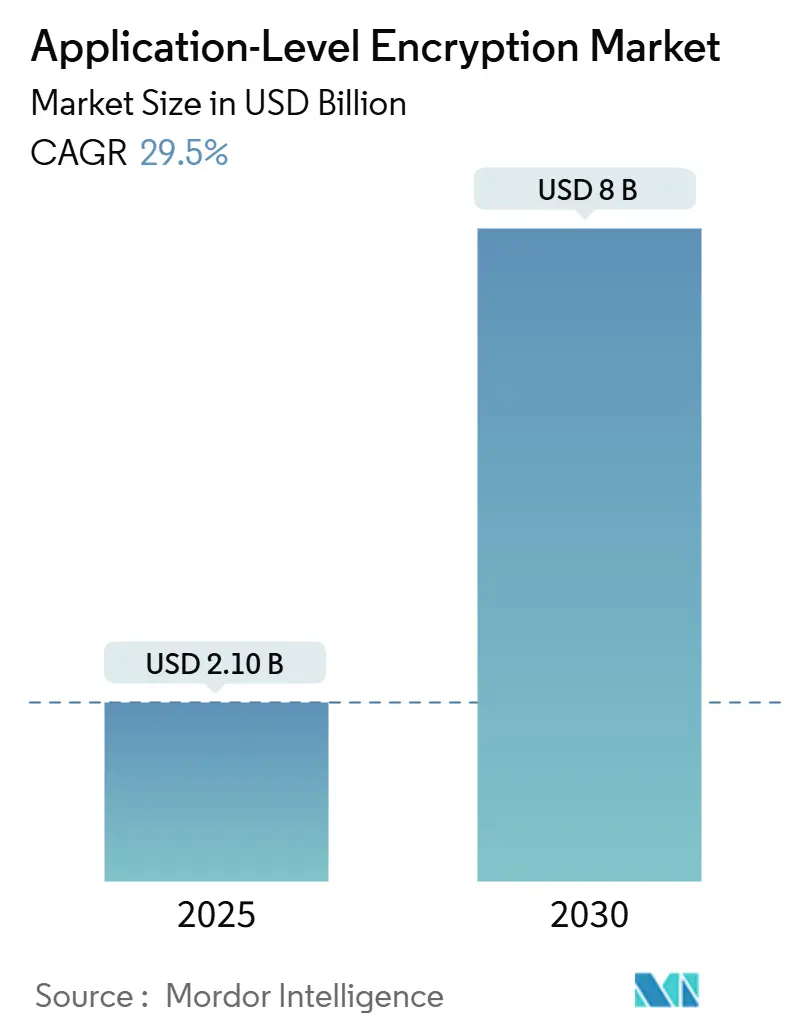

| Market Size (2025) | USD 2.10 Billion |

| Market Size (2030) | USD 8 Billion |

| Growth Rate (2025 - 2030) | 29.50% CAGR |

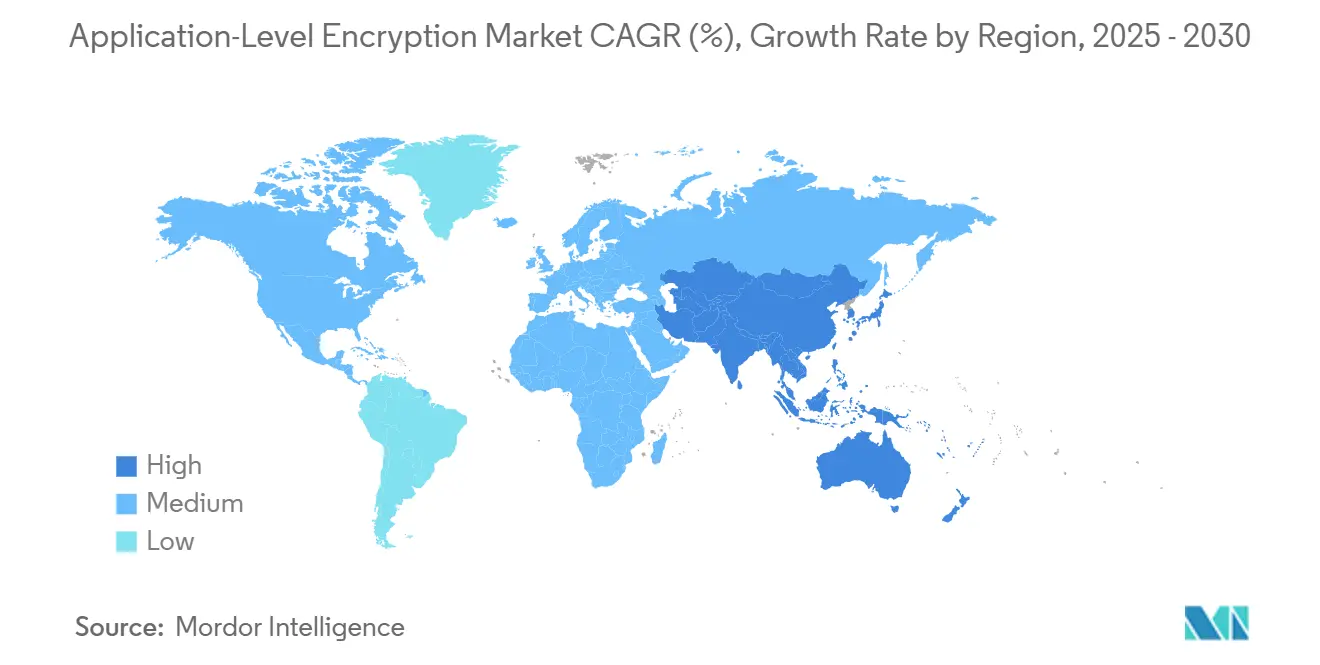

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application-Level Encryption Market Analysis by Mordor Intelligence

The global application-level encryption market size reached USD 2.10 billion in 2025 and is projected to climb to USD 8.00 billion in 2030, reflecting a 29.5% CAGR across the period. Rising adoption of cloud-native architectures, urgent post-quantum readiness, and intensifying data-protection mandates are converging to expand the addressable opportunity for vendors and service providers. Organizations are embedding strong cryptography directly inside modern microservices, relying on integrated hardware acceleration and confidential-computing enclaves to keep latency within service-level objectives. Performance breakthroughs such as Linux 6.10’s AES-XTS boost on AMD Zen 4 cut CPU overhead and reduce objections from latency-sensitive sectors.[1]Michael Larabel, “Linux 6.10 AES-XTS for Disk/File Encryption as Much as 155% Faster for AMD Zen 4 CPUs,” phoronix.com Consolidation is accelerating as identity-security leaders acquire key-management specialists to deliver unified machine-identity and secrets-management offerings, while venture funding fuels innovation in homomorphic and post-quantum implementations.[2]Alibaba Cloud, “Use Multi-Buffer to Accelerate TLS Encryption and Decryption in Envoy,” alibabacloud.com

Key Report Takeaways

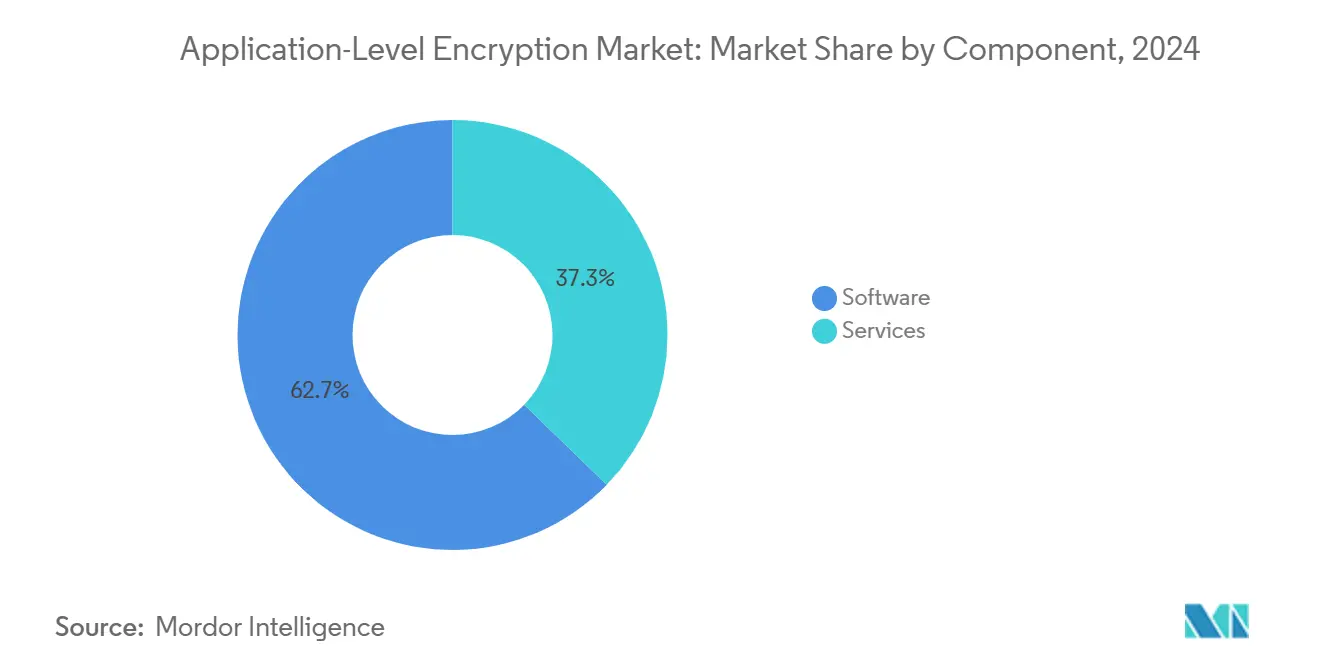

- By component, software led with 62.73% of application level encryption market share in 2024, while ingestible services is projected to grow at an 31.11% CAGR through 2030.

- By deployment, cloud led with 71.93% of application level encryption market share in 2024, and cloud is expanding at a 31.34% CAGR to 2030.

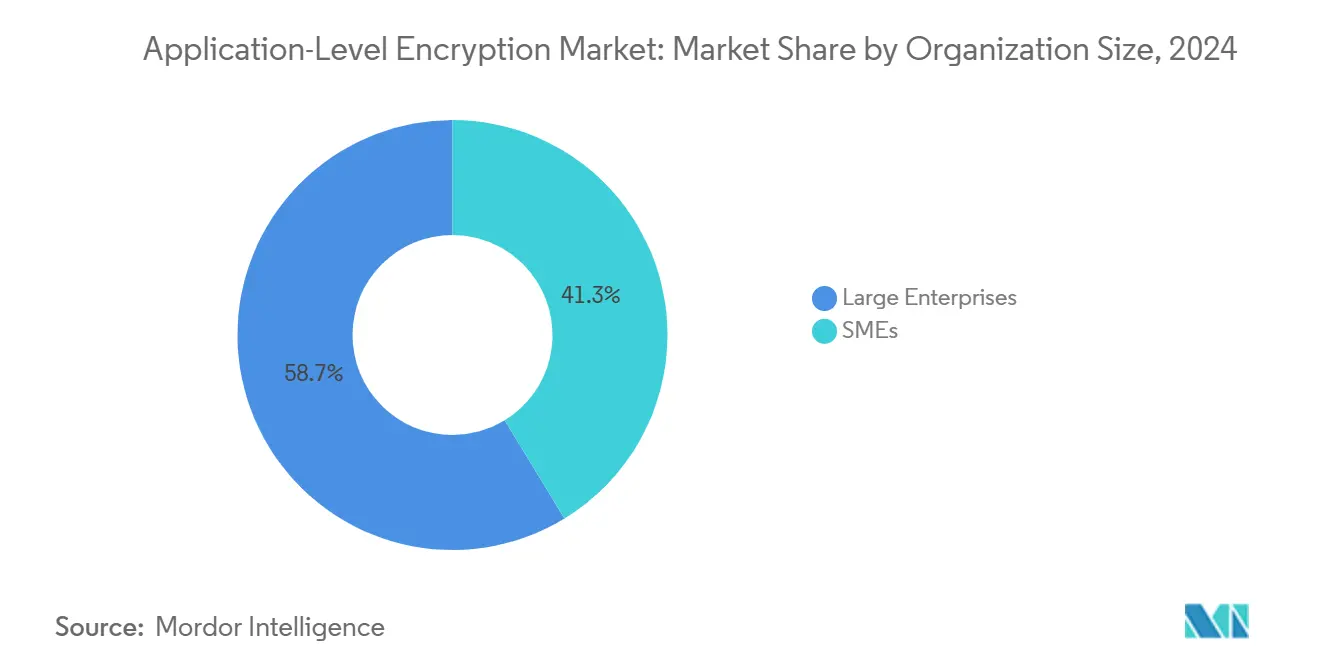

- By organization size, large entrprises led with 62.73% of application level encryption market share in 2024, small and medium enterprises are advancing at a 30.77% CAGR through 2030.

- By end-user industry, BFSI led with 30.82% of application level encryption market share in 2024, and healthcare is expanding at a 30.44% CAGR to 2030.

- By geography, North America accounted for 34.82% share of the application-level encryption market size in 2024, and Asia-Pacific is expanding at a 30.66% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Application-Level Encryption Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth of Cloud-Native Applications | +8.0% | Global, with concentration in North America and APAC | Medium term (2-4 years) |

| Stringent Data-Protection Regulations | +6.2% | Global, led by EU GDPR and expanding to APAC | Long term (≥ 4 years) |

| Surge in Remote Work and BYOD Adoption | +5.8% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Rising Frequency and Sophistication of Data Breaches | +4.1% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Integration of Confidential Computing with App-Level Encryption | +3.7% | North America and EU, early adoption in APAC | Long term (≥ 4 years) |

| Adoption of Homomorphic Encryption APIs for Analytics | +3.2% | North America and EU, research-driven expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Cloud-Native Applications

Container orchestration and service-mesh adoption require encryption that scales elastically, integrates with DevOps pipelines, and aligns with zero-trust networking. Alibaba Cloud demonstrated a 75% jump in requests-per-second when it embedded Intel multi-buffer acceleration for TLS inside Envoy, validating the business case for cryptographic offload within cloud service meshes. Enterprises now demand libraries that secure data in motion, at rest, and in use without forcing developers to re-architect microservices. Standardization of confidential-computing instances across hyperscalers further lifts demand because trusted execution environments complement application-level encryption instead of replacing it. As multicloud deployments mature, encryption that follows the workload becomes a baseline expectation rather than an optional add-on.

Stringent Data-Protection Regulations

Global regulators are stipulating prescriptive technical controls, turning encryption from a best practice into a formal requirement for compliance attestations. European Data Protection Authorities levy multi-million-euro penalties for weak or missing encryption, prompting firms to adopt provably secure application-level controls that survive audits. Healthcare providers face HIPAA updates that insist on encryption in use throughout analytics pipelines, while Asia-Pacific jurisdictions align local laws with GDPR-grade rules. Encryption is now treated as risk insurance because certification programs such as ISO 27001 give explicit credit for strong in-application cryptography during audits, directly influencing vendor selection and customer trust.

Surge in Remote Work and BYOD Adoption

Hybrid work broadens the attack surface, forcing encryption directly into applications rather than relying on perimeter defenses. BYOD policies place sensitive data on unmanaged devices, so client-side encryption and robust key-distribution protocols rise in priority. Research on U.K. SMEs shows that smaller firms still underinvest in advanced controls, yet they are increasingly drawn to managed encryption services that abstract complexity and cut capital expense. SaaS dependence amplifies this trend because cloud services can expose data across multiple locations; client-side encryption mitigates leakage while preserving productivity.

Rising Frequency and Sophistication of Data Breaches

Cybercriminals increasingly target key-material compromise rather than brute-forcing algorithms. Asia-Pacific accounted for nearly one-third of global attacks in 2024, driving regional appetite for layered cryptography that sustains confidentiality even after perimeter failure.[3]Alibaba Cloud, “Use Multi-Buffer to Accelerate TLS Encryption and Decryption in Envoy,” alibabacloud.com Defense-in-depth strategies combine hardware-rooted keys, formal verification of libraries, and cryptographic agility so organizations can swap algorithms in response to new threats without massive code rewrites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Performance Overhead on Mission-Critical Apps | -2.9% | Global, with higher impact in latency-sensitive sectors | Short term (≤ 2 years) |

| Complex Key Management Across Hybrid Environments | -2.4% | Global, particularly affecting multi-cloud deployments | Medium term (2-4 years) |

| Compatibility Challenges with Legacy Systems | -1.8% | North America and Europe, legacy-heavy enterprises | Medium term (2-4 years) |

| Emerging Quantum-Ready Standards Causing Adoption Delays | -1.5% | Global, with early impact in government and defense | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Performance Overhead on Mission-Critical Apps

Encryption adds CPU cycles and latency that can erode user experience in high-frequency trading or real-time analytics. Earlier implementations consumed up to 15% of server compute, triggering pushback from business units. Kernel-level optimizations, such as the AES-XTS uplift in Linux 6.10, now cut overhead by more than half on modern AMD silicon. Confidential-computing co-processors further decouple cryptographic load from application logic. Enterprises increasingly treat performance tuning as an engineering task rather than an adoption blocker.

Complex Key Management Across Hybrid Environments

Key lifecycle governance spans on-premises data centers, multiple clouds, and edge nodes. Companies struggle with rotation cadence, access-policy synchronization, and compliance reporting. The 2024 acquisition of Venafi by CyberArk consolidated secrets management and machine-identity lifecycle into a single control plane, signaling vendor focus on unified key orchestration. Cloud HSM services also standardize rotation and auditing procedures, narrowing the skill gap and easing multi-jurisdiction compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Software Dominance

Software held 62.73% of application-level encryption market share in 2024, reflecting widespread use of libraries and SDKs that embed cryptography inside microservices. Many firms begin adoption through open-source or cloud-native toolkits that integrate with CI/CD workflows. The application-level encryption market size for the software segment is forecast to record a 28.9% CAGR, powered by confidential-computing usage and post-quantum algorithm migration.

Services are advancing at 31.11% CAGR because successful rollouts demand specialized expertise in algorithm selection, threat modeling, and compliance mapping. Managed services relieve SMEs of operational burdens, while global systems integrators package encryption assessments with zero-trust transformations. Post-quantum transition consulting and interoperability testing with legacy PKI systems underpin robust demand for expert services.

By Deployment Mode: Cloud Supremacy Drives Innovation

Cloud deployment accounted for 71.93% of application-level encryption market share in 2024 and will grow 31.34% annually through 2030, underscoring the gravitational pull of elastic cryptography-as-a-service. Hyperscalers bundle hardware enclaves, HSMs, and low-latency API gateways, making cloud the default venue for homomorphic and confidential-computing workloads. The application-level encryption market size for cloud offerings is projected to add USD 4.5 billion between 2025 and 2030.

On-premises usage persists in defense, critical infrastructure, and jurisdictions with rigid data-sovereignty rules. Hybrid models emerge as a pragmatic compromise, retaining root keys on site while outsourcing compute-intensive cryptography to cloud accelerators. Vendor roadmaps increasingly feature policy engines that enforce uniform key governance across all venues.

By Organization Size: SME Adoption Accelerates

Large enterprises still command 58.73% share in 2024, bolstered by regulatory scrutiny and resource capacity. These organizations deploy encryption programmatically across thousands of applications and integrate it with privileged-access management and SIEM systems. For them, algorithm agility and hardware acceleration are top buying criteria.

SMEs are growing fastest at 30.77% CAGR because cloud services now embed turnkey encryption that eliminates heavy up-front investment. Predictable subscription pricing and API-first key management align with limited security headcount. Awareness campaigns by trade associations and insurers that reward encrypted workloads with lower premiums add momentum.

By End-User Industry: Healthcare Emerges as Growth Leader

Banking, financial services, and insurance retained 30.82% share in 2024 due to stringent audit trails and high-value datasets. Institutions deploy layered encryption inside payment rails and trading engines while piloting homomorphic techniques for privacy-preserving risk analytics.

Healthcare posted the highest growth at 30.44% CAGR, fueled by electronic health record expansion, telemedicine, and genomic research. Providers need encryption that respects life-critical latency constraints and supports cross-institution data exchange under HIPAA updates. The application-level encryption market size for healthcare workloads is projected to add USD 1.2 billion by 2030.

Geography Analysis

North America captured 34.82% of application-level encryption market share in 2024, anchored by early cloud adoption, federal funding for post-quantum migration, and concentration of leading vendors. U.S. executive orders that set 2035 deadlines for quantum-safe algorithms spark sizeable multiyear contracts for readiness assessments and pilot deployments. Canada mirrors these dynamics in its financial and public sectors.

Asia-Pacific is the fastest mover with a 30.66% CAGR through 2030 as digital-economy expansion and sovereign data laws converge. China promotes domestic cryptographic standards while investing in RISC-V hardware root-of-trust, creating demand for dual-stack solutions compatible with global and local algorithms. India’s Digital Personal Data Protection Act drives large-scale encryption rollouts across banking and healthcare. Southeast Asian SMEs adopt cloud-delivered encryption to satisfy cross-border commerce compliances without constructing full security operations centers.

Europe maintains steady, regulation-driven growth. GDPR fine patterns incentivize robust in-application encryption, and upcoming AI Act articles require explicit protection for automated decision inputs. Nations prioritize cloud sovereignty, so multi-cloud key orchestration and in-country HSM clusters gain traction. The region also pioneers post-quantum cryptography testbeds through Horizon Europe grants, reinforcing vendor presence.

Competitive Landscape

The field is moderately fragmented. Amazon Web Services, Microsoft, Google, and IBM anchor the high end by embedding encryption toolchains inside cloud control planes; their scale allows bundled compliance reports and no-touch rotation features. Customers favor these integrated offerings when workloads already reside on the respective clouds.

Specialists such as Thales, Fortanix, Baffle, and Protegrity differentiate through algorithm agility, tokenization depth, and compliance automation for regulated verticals. Partnerships with chipset makers unlock hardware acceleration paths that shrink CPU overhead without extra licensing. The 2024 CyberArk-Venafi deal exemplifies consolidation that marries secrets management and machine identity, positioning the combined platform to manage human and non-human credentials under a single policy engine. Start-ups like Zama and PQShield concentrate on homomorphic and post-quantum niches, attracting venture inflows as enterprises budget for long-term algorithm shifts. Overall competition pivots on measurable performance gains, compliance evidence packs, and simplified key orchestration.

Application-Level Encryption Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zama raised USD 73 million Series A to commercialize homomorphic encryption APIs for privacy-preserving analytics.

- December 2024: PQShield secured USD 37 million Series B to accelerate quantum-resistant algorithm deployment.

- October 2024: Netskope bought Dasera, integrating data-security posture management with its SASE platform.

- October 2024: Cyera acquired Trail Security for USD 162 million to add AI-driven DLP to its cloud-data-protection suite.

Global Application-Level Encryption Market Report Scope

| Software |

| Services |

| On-Premises |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare |

| IT and Telecom |

| Retail and E-commerce |

| Government and Defense |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | BFSI | ||

| Healthcare | |||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Government and Defense | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the application-level encryption market in 2030?

It is expected to reach USD 8.00 billion by 2030, expanding at a 29.5% CAGR from 2025.

Which deployment mode is growing fastest within application-level encryption solutions?

Cloud deployment is growing at a 31.34% CAGR as hyperscalers bundle HSMs, confidential-computing instances, and low-latency encryption APIs.

Why are healthcare organizations investing heavily in application-level encryption?

Updated privacy mandates and telemedicine expansion drive healthcare to adopt strong in-application encryption, resulting in a 30.44% CAGR through 2030.

How does post-quantum readiness influence encryption spending?

Federal deadlines and NIST standards are pushing enterprises to upgrade algorithms now, creating demand for consulting and agile key-management platforms.

What performance breakthroughs are reducing encryption overhead?

Linux 6.10 kernel improvements and Intel multi-buffer acceleration inside Envoy cut AES-XTS latency by up to 155%, easing concerns for real-time workloads.

Page last updated on: