Croatia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.91 Billion |

| Market Size (2030) | USD 2.18 Billion |

| Growth Rate (2025 - 2030) | 2.58% CAGR |

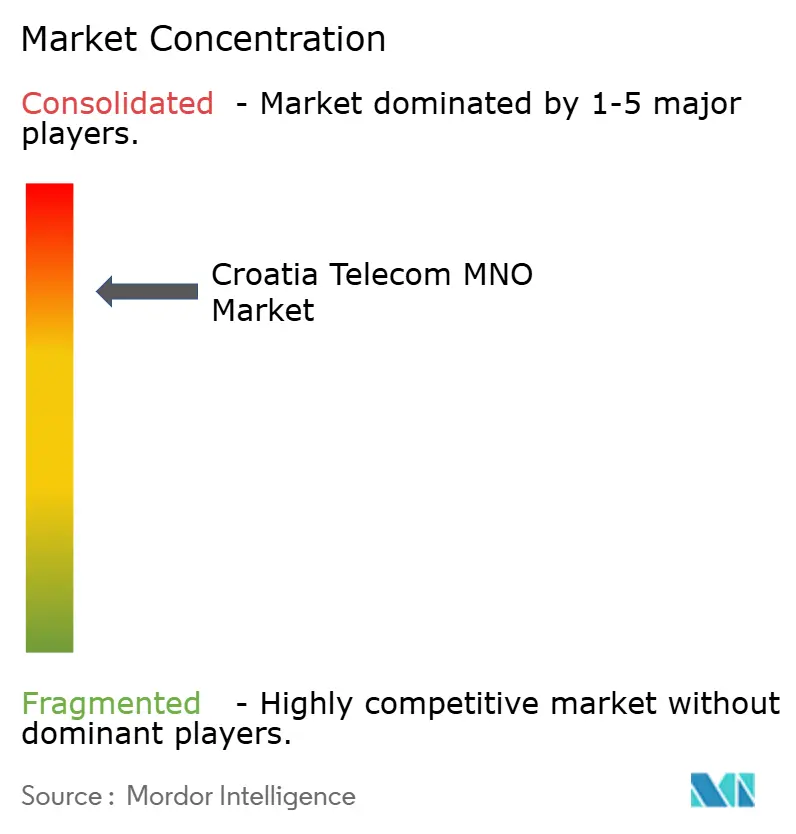

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia Telecom MNO Market Analysis by Mordor Intelligence

The Croatia Telecom MNO Market size is estimated at USD 1.91 billion in 2025, and is expected to reach USD 2.18 billion by 2030, at a CAGR of 2.58% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 5.69 million subscribers in 2025 to 6.39 million subscribers by 2030, at a CAGR of 2.34% during the forecast period (2025-2030). Mobile operators are refocusing on data-centric bundles as 5G standalone coverage expands and enterprise demand for managed IoT connectivity accelerates. Spectrum secured in the 2021 multiband auction underpins this capacity build-out, although EU wholesale price caps temper near-term revenue growth. [1]HAKOM, “5G Network in Croatia,” hakom.hr Seasonal tourism surges lift mobile ARPU each summer, while EU-backed rural fiber rollouts enlarge the addressable broadband base. Submarine cable landings on the Adriatic coast further reposition the country as a regional transit node for Balkan–Mediterranean data flows.

Key Report Takeaways

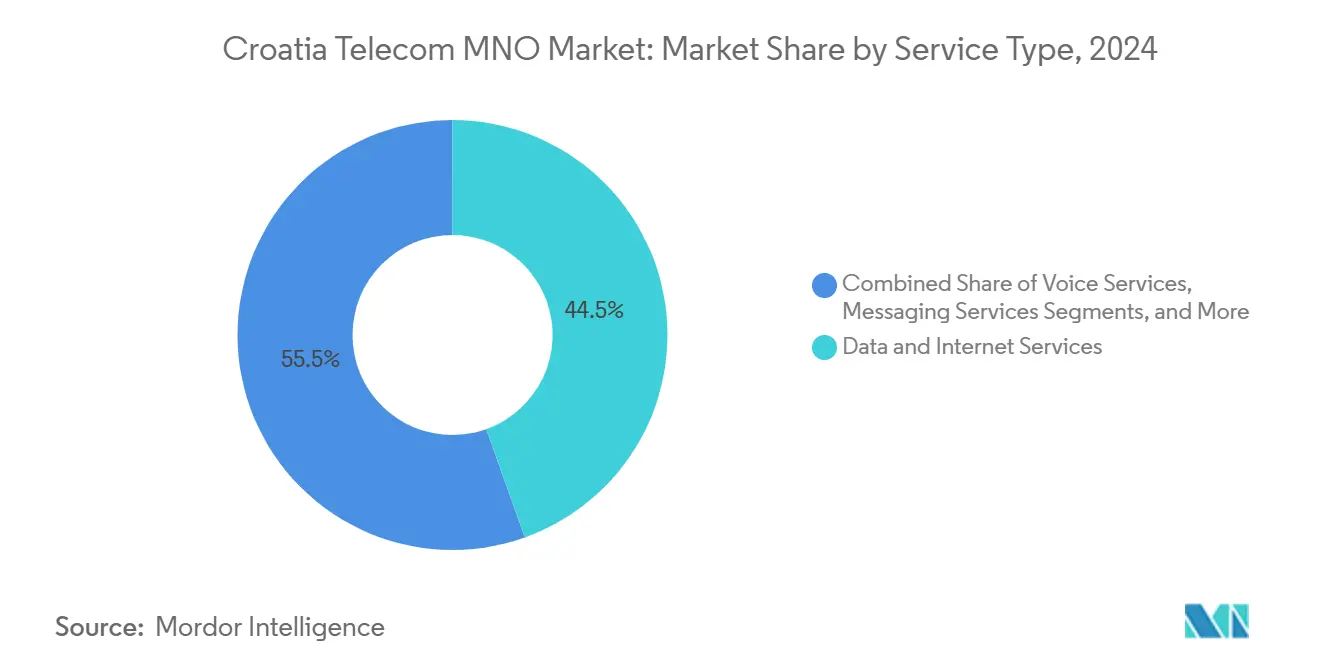

- By service type, data and internet services captured 44.53% of Croatia telecom MNO market share in 2024 and IoT and M2M services are forecast to expand at a 3.87% CAGR through 2030.

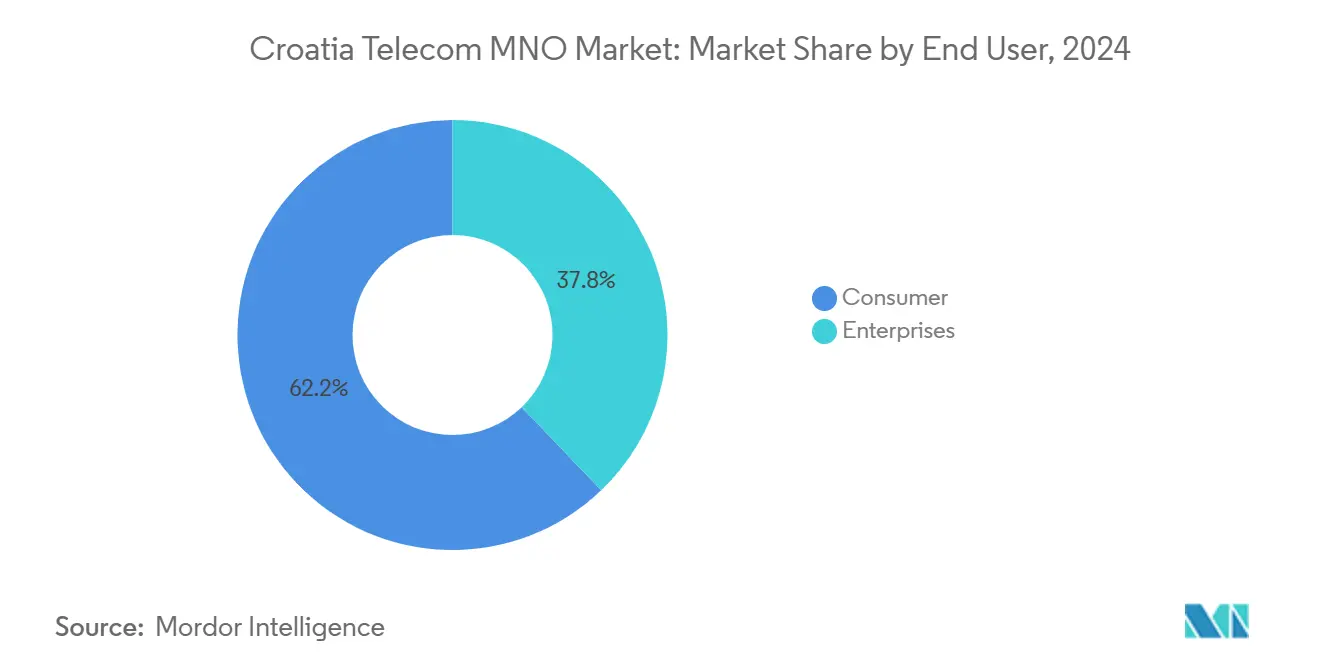

- By end user, consumer subscriptions accounted for 62.17% of Croatia telecom MNO market share in 2024, and enterprise subscriptions are projected to advance at a 2.92% CAGR to 2030.

Croatia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Mobile Data Consumption with 5G Rollout | +0.8% | Zagreb, Split, Rijeka | Medium term (2-4 years) |

| Fixed-fiber Broadband Expansion via EU Funds | +0.6% | Rural counties, Primorje-Gorski Kotar, Istria | Long term (≥ 4 years) |

| Enterprise IoT Connectivity Demand | +0.4% | Industrial zones and ports | Medium term (2-4 years) |

| Government Spectrum Auctions Enabling Capacity | +0.3% | Nationwide | Short term (≤ 2 years) |

| Tourism-driven Seasonal Bandwidth ARPU Uplift | +0.2% | Dubrovnik, Split, coastal resorts | Short term (≤ 2 years) |

| Balkan Submarine Cable Transit Opportunities | +0.1% | Adriatic landing stations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile Data Consumption with 5G Rollout

Average monthly mobile data use in Croatia is tracking upward from 14 GB in 2022 toward a projected 75 GB by 2030 as video streaming and social media dominate traffic profiles. [2]Hrvatski Telekom, “Best Mobile Network Confirmed,” t.ht.hr The switch-off of 3G in January 2025 freed spectrum that has already bolstered 4G capacity and expedited 5G standalone coverage. Operators have introduced tiered premium bundles that monetize network slicing and latency-sensitive gaming add-ons. This shift lifts blended ARPU even in a subscriber-saturated environment. Network vendors are jointly trialing dual-mode cores that consolidate 4G EPC and 5G cores, which reduces opex and accelerates feature rollouts.

Fixed-fiber Broadband Expansion via EU Funds

A EUR 101.4 million rural broadband scheme, financed by the Recovery and Resilience Facility, will deliver open-access fiber capable of 100 Mbps symmetrical speeds across underserved counties. [3]Vecernji List, “EU Approves Croatian NGA Plan,” vecernji.hr Implementation through state-owned Odašiljači i veze guarantees equal wholesale access for all three MNOs, lowering capital intensity and supporting convergent bundles. The RuNe cross-border build in Istria and Primorje-Gorski Kotar illustrates how regional cooperation pools funding and engineering capabilities. Fiber backhaul makes small-cell densification for 5G economically viable and reduces latency on enterprise VPN circuits. The program narrows Croatia’s historical gap to the EU average in NGA coverage.

Enterprise IoT Connectivity Demand

Industrial automation, logistics tracking, and smart-city pilots are anchoring a fresh revenue stream for operators. Televend, a Croatian engineering export, remotely manages over 250,000 vending machines worldwide through embedded SIMs and cloud dashboards. [4]Orange Business, “IoT Connects Vending Machines,” orange-business.com Rijeka’s container terminal uses a private 5G standalone slice for crane telemetry, asset tracking, and emission monitoring, proving the ROI case for ultra-reliable links. Municipal platforms such as Dubrovnik’s “smart street” project leverage NB-IoT sensors for parking and traffic optimization. Enterprises pay a meaningful premium over consumer tariffs because service-level guarantees and secure APNs are mandatory. EU digitalization grants covering SMEs accelerate adoption in manufacturing clusters.

Government Spectrum Auctions Enabling Capacity

The 2021 multiband auction awarded contiguous 700 MHz, 3.6 GHz, and 26 GHz licenses to all three network operators, generating HRK 359 million (USD 47.9 million) for the treasury HAKOM.HR. Licence conditions mandate defined rural population coverage ratios within five years, aligning commercial rollout with policy goals. Low-band 700 MHz assets extend indoor and rural reach at low incremental cost, while millimeter-wave blocks support enterprise fixed-wireless substitutes and campus networks. The transparent auction process prevented spectrum hoarding, maintaining competitive balance. Forthcoming 6 GHz harmonization could inject fresh capacity and bolster long-term traffic growth forecasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated Mobile Penetration | -0.5% | Urban clusters | Long term (≥ 4 years) |

| EU Wholesale Price Regulation Pressure | -0.4% | Nationwide | Medium term (2-4 years) |

| Demographic Decline and Emigration | -0.3% | Rural eastern counties | Long term (≥ 4 years) |

| Energy-price Volatility on Network OPEX | -0.2% | Energy-intensive base-station mix | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturated Mobile Penetration

Active SIM density surpassed 119% in 2024, leaving limited room for organic subscriber growth. Operators therefore pivot to wallet-share strategies anchored on data bundles, device leasing, and convergent fixed-mobile propositions. Ongoing population decline compounds this ceiling, with forecasts showing a fall from 3.86 million residents in 2022 to 3.31 million by 2050. The ageing demographic skews usage toward lower-value voice and basic data plans. Rural depopulation intensifies the cost-revenue imbalance on low-density towers, challenging return on capital.

EU Wholesale Price Regulation Pressure

Roam-Like-at-Home rules slashed intra-EU retail and wholesale rates, cutting average operator ARPU by 9.1% since full implementation. Croatia feels this pinch acutely during the peak tourist season when inbound roamers previously yielded premium per-GB margins. Upcoming BEREC reviews signal further downward pressure on interconnect and intra-EU communication caps. Operators absorb higher energy and spectrum amortization costs without the historical pricing levers, squeezing EBITDA margins and delaying some rural coverage upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive IoT Transformation

Data and Internet services held a 44.53% Croatia telecom MNO market share in 2024, reflecting consumers’ preference for high-speed mobile broadband bundles. Average revenue per user rose during summer peaks as operators packaged unlimited data with tourist SIM offers. In contrast, voice and SMS revenue continued a mild decline as over-the-top apps displaced legacy communications. IoT and M2M lines, though still nascent, logged the fastest growth and are expected to post a 3.87% CAGR to 2030, aided by NB-IoT and LTE-M coverage in industrial corridors.

The segment mix underpins stable earnings diversification. Content partnerships with streaming platforms anchor premium data tiers, while wholesale backhaul to MVNOs monetizes spare capacity. Submarine cable routes landing on the Adriatic promise to enlarge the wholesale customer base further. Operators are integrating secure IoT cloud platforms to capture higher-margin device management fees.

By End User: Enterprise Growth Outpaces Consumer Maturity

Consumer subscriptions represented 62.17% of Croatia telecom MNO market share in 2024, but usage growth has plateaued because penetration exceeds 100%. Enterprise lines, although smaller in number, are forecast to record a 2.92% CAGR through 2030 because digitalization funding spurs demand for managed connectivity, SD-WAN, and private 5G slices. Port operators, manufacturers, and logistics firms require deterministic quality of service, which justifies pricing at a 1.5-to-2-times premium over standard consumer ARPU.

Cross-selling convergent mobile-fixed-cloud bundles raises switching costs for corporates and offsets margin compression in mass retail. Network slicing, available following standalone 5G cores, enables time-critical control for automated production lines. Operators continue to invest in SOC centers and edge data facilities to meet enterprise latency and security expectations and to capture incremental revenue from analytics and smart-building applications.

Geography Analysis

Coastal counties such as Dubrovnik-Neretva and Split-Dalmatia absorb three to four times their off-season traffic during the June-to-September tourist surge. Operators deploy temporary cell-on-wheel clusters and dynamic spectrum sharing to protect user experience and unlock ARPU uplift. Inland, Zagreb remains the largest revenue pool, combining dense residential neighborhoods with the country’s principal business district. The city also serves as the national testbed for early 5G standalone features, including massive MIMO deployments on the 3.6 GHz band.

Rural counties historically lagged in broadband speeds, but EU co-funded fiber projects are closing this divide. Once completed, these networks will allow operators to migrate DSL households to gigabit plans and backhaul 5G small cells at lower latency. Eastern Slavonia presents the steepest demographic headwinds because sustained emigration reduces addressable lines, although agricultural IoT pilots could restore incremental connectivity demand. The Croatia telecom MNO market size attributable to rural areas is therefore expected to stabilize rather than decline as data consumption per user compensates for fewer users.

The Adriatic shore is emerging as a Mediterranean switching point following Sparkle’s GreenMed cable landing in 2024. Additional express links being negotiated between Albania and Egypt would permit low-latency traffic routing to Middle Eastern content hubs. This positioning may elevate wholesale transit revenue to a mid-single-digit share of total mobile service revenue by 2030. Harmonized cross-border regulation under the Digital Single Market agenda would further integrate Croatia into regional backbone grids, though that benefit hinges on timely spectrum coordination with neighboring states.

Competitive Landscape

Croatia’s mobile services industry is a three-player oligopoly. Hrvatski Telekom leads with a 46% mobile SIM share and reported network quality scores of 888.2 in 2024 field tests. The operator’s January 2025 3G shutdown freed refarmed 900 MHz and 2100 MHz blocks that now support 4G capacity and extend 5G coverage. A1 Croatia serves roughly 2 million customers and leverages convergent cable and mobile assets to retain high-value households; its EBITDA margin improved to 37% in 2024 on disciplined pricing.

Telemach Croatia positions on aggressive pricing and rapid 5G build-out, claiming 98.9% population coverage by end-2024. Parent United Group’s scale advantages in content procurement enable differentiated video bundles that attract cord-cutting youth cohorts. Operators differentiate less on technology as access parity rises and more on customer-experience metrics, bundling OTT streaming and cloud storage to lock in contracts.

Investment intensity remains high because 700 MHz coverage obligations and urban millimeter-wave densification both demand sustained capex. Consolidation talk occasionally surfaces, yet antitrust hurdles remain significant because any tie-up among the three incumbents would risk market dominance. Instead, selective asset purchases prevail, such as tower-company carve-outs that recycle capital for radio upgrades. Over the forecast horizon, enterprise private-network solutions, low-orbit satellite backhaul and edge-cloud collaborations with Hyperscalers are expected to redraw competitive lines, handing an early-mover advantage to operators that scale secure IoT platforms fastest.

Croatia Telecom MNO Industry Leaders

Hrvatski Telekom

A1 Croatia

Telemach Croatia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hrvatski Telekom completed Croatia’s first national 3G network shutdown, reallocating spectrum to bolster 4G and 5G capacity.

- January 2025: Hrvatski Telekom announced a 3% tariff adjustment from March 2025 to fund annual network modernization exceeding EUR 200 million.

- July 2024: Hrvatski Telekom activated a 5G standalone network at the Rijeka container port to enhance industrial IoT operations.

- May 2024: HAKOM confirmed Hrvatski Telekom retained top position in national mobile network quality benchmarking.

Croatia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current size of the Croatia telecom MNO market?

The market generated USD 1.91 billion in mobile service revenue during 2025 and is on track to reach USD 2.18 billion by 2030.

Which service category holds the largest share?

Data and Internet services accounted for 44.53% of Croatia telecom MNO market share in 2024, reflecting strong demand for mobile broadband.

Which segment is growing fastest?

IoT and M2M connections are projected to post a 3.87% CAGR through 2030 as enterprises roll out smart-factory, port and city solutions.

How saturated is Croatia’s mobile subscriber base?

SIM penetration exceeded 119% in 2024, so operators now focus on boosting ARPU through premium data bundles and convergent offers.

Why did Hrvatski Telekom shut down its 3G network?

The shutdown freed low-band spectrum to improve 4G coverage and accelerate nationwide 5G rollout while cutting legacy network costs.

What is the outlook for enterprise revenue?

Enterprise lines are forecast to expand at a 2.92% CAGR as EU digitalization grants and private 5G projects drive demand for guaranteed-quality connectivity.

Page last updated on: