Finland Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.03 Billion |

| Market Size (2026) | USD 5.25 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

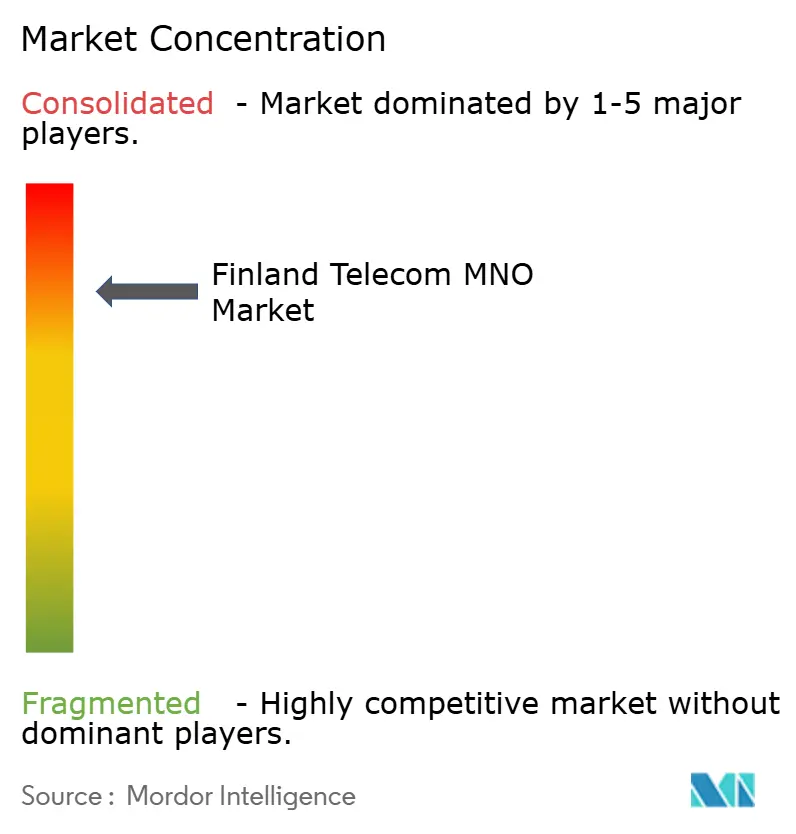

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finland Telecom MNO Market Analysis by Mordor Intelligence

The Finland Telecom MNO Market size market is expected to grow from USD 5.03 billion in 2025 to USD 5.25 billion in 2026 and is forecast to reach USD 6.49 billion by 2031 at 4.33% CAGR over 2026-2031.

The growth outlook is anchored in Finland’s 98.3% nationwide 5G household coverage, its world-leading 63.3 GB monthly per-capita mobile data usage, and the country’s sustained fiber roll-outs financed in part by EU Recovery and Resilience funds. [1]5G Observatory, “5G Observatory Quarterly Report June 2024,” 5gobservatory.eu Rapid 5G migration, an unlimited-data culture that supports premium ARPU tiers, and surging private 5G campus deployments in manufacturing and healthcare bolster long-run revenue visibility. Intensifying network-quality competition among Elisa, Telia Finland, and DNA drives investment in standalone 5G cores, edge computing, and energy-efficient RAN upgrades. At the same time, data-center expansion by Hyperscalers such as Google increases enterprise back-haul demand, while Finland’s 6G research ecosystem positions operators for next-generation revenue streams. Margin pressure from energy inflation and spectrum fees, plus looming “fair-use” regulation on unlimited plans, creates counterweights that operators address through renewable power sourcing, network sharing, and selective price increases.

Key Report Takeaways

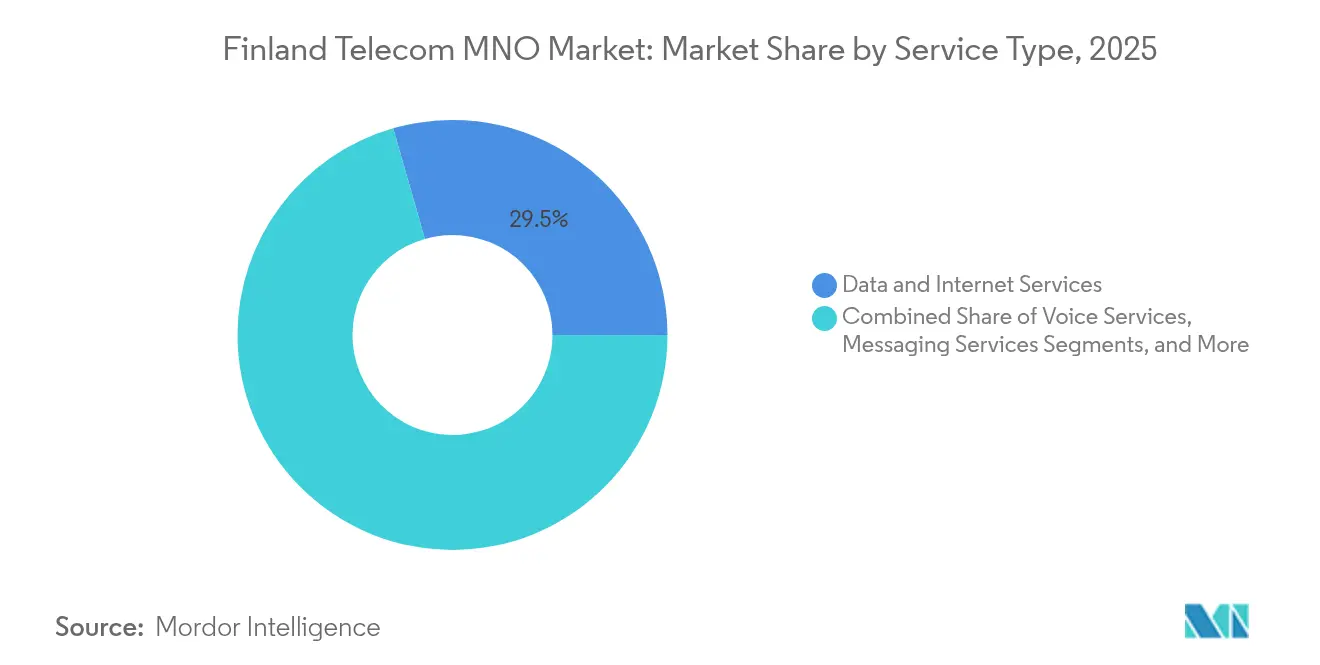

- By service type, data and Internet services led with 29.45% of Finland telecom MNO market share in 2025. IoT and M2M services are projected to expand at a 4.41% CAGR to 2031, the fastest within service categories.

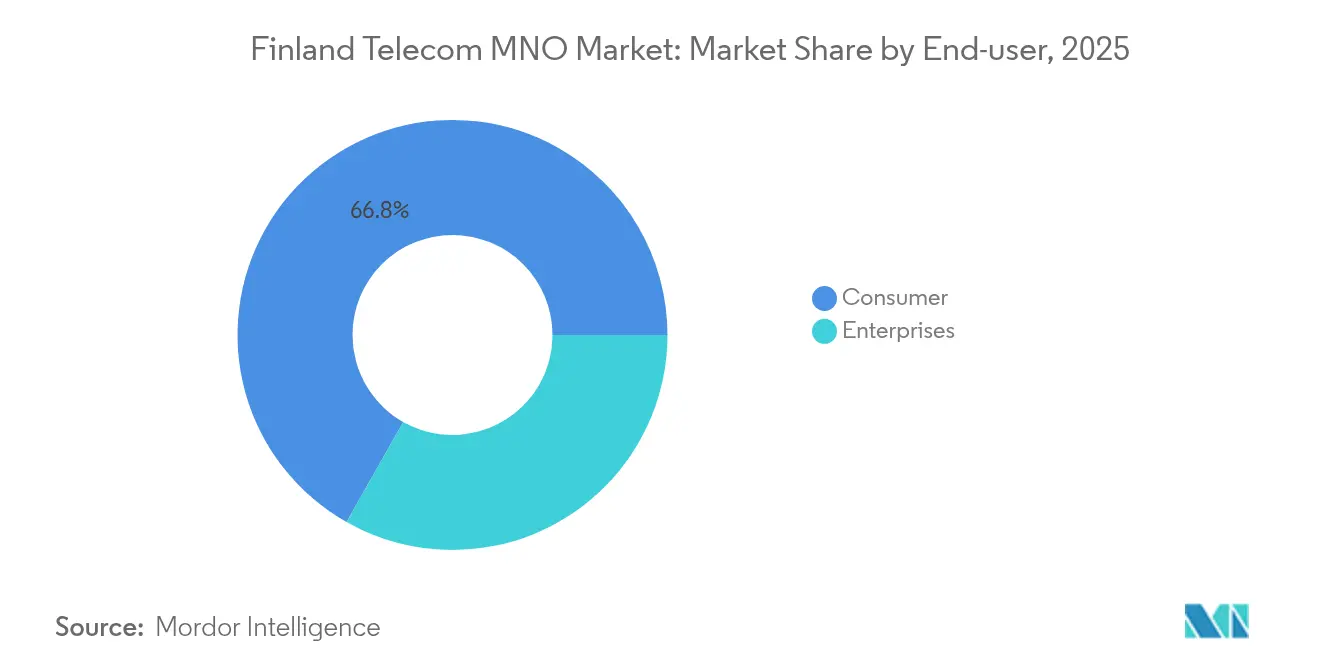

- By end user, the consumer segment accounted for 66.80% of the Finland telecom MNO market size in 2025. The enterprise segment is forecast to advance at a 4.65% CAGR between 2026-2031, outpacing consumer growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Finland Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-out and spectrum re-farming | +1.2% | National, urban areas | Medium term (2-4 years) |

| Unlimited-data culture boosts usage and ARPU | +0.8% | National, urban areas | Short term (≤ 2 years) |

| EU Recovery and Resilience funds for digital infra | +0.6% | National, rural focus | Medium term (2-4 years) |

| Private 5G campus networks in manufacturing | +0.4% | Regional, industrial clusters | Long term (≥ 4 years) |

| Finland’s 6G research ecosystem attracts vendors | +0.3% | National, R&D hubs | Long term (≥ 4 years) |

| Data-center boom raises enterprise back-haul need | +0.5% | Regional, data-center sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G roll-out and spectrum re-farming

Finland’s award of 700 MHz spectrum in 2016, followed by 3.5 GHz and 26 GHz auctions, enabled operators to switch off 3G and refarm low-band assets for 5G by 2024. The resulting 98.3% household 5G coverage improves capacity economics and supports premium pricing for differentiated latency-sensitive services. Elisa’s nationwide standalone 5G core launched in 2025 showcases network slicing readiness, allowing industrial clients to order dedicated throughput for production lines. This first-mover advantage cements Finland’s reputation as a European test bed for early 5G use cases. [2]Traficom, “Telecommunications Register,” traficom.fi

Unlimited-data culture boosts usage and ARPU

Operators have turned uncapped mobile plans into a revenue engine by segmenting heavy users into higher-priced tiers. Monthly per-capita consumption of 63.3 GB ranks first globally, yet Telia Finland recorded 8% mobile ARPU growth in 2024, proving value migration rather than commoditization. Traffic concentration among the top user deciles lets carriers engineer networks around predictable peak loads while monetizing premium add-ons like cloud gaming acceleration and 5G-SA slicing. The model also mitigates churn because data ceilings no longer differentiate rivals.

EU Recovery and Resilience funds for digital infrastructure

The Finnish Recovery and Resilience Plan allocates EUR 32 million to rural broadband. Combined with operator capex, total 2023 fixed-network investment jumped 88% to EUR 385 million, lifting fiber availability to 68% of households. Access to 1 Gbps services reached 75% of homes in September 2024, narrowing the urban-rural divide. Improved connectivity supports remote work, e-health, and smart agriculture, slowing rural population decline that previously weighed on traffic volumes.

Private 5G campus networks in manufacturing

EDZCOM’s 26 live private LTE/5G networks, plus Nokia–Rockwell Automation pilots, illustrate demand for ultra-reliable wireless inside factories. Use cases span autonomous mobile robots, digital twins, and condition-based maintenance. Operators increasingly supply spectrum leasing, SIM lifecycle management, and hybrid public-private roaming to capture enterprise spend that would otherwise bypass the Finland telecom MNO market. [3]DNA Plc, “DNA’s 5G Network Reaches 96% of Finns,” dna.fi

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated subscriber base limits organic growth | -0.7% | National | Short term (≤ 2 years) |

| High energy and spectrum costs pressure margins | -0.5% | National | Medium term (2-4 years) |

| Rural youth out-migration lowers voice traffic | -0.3% | Rural regions | Long term (≥ 4 years) |

| Forthcoming “fair-use” regulation on unlimited plans | -0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturated subscriber base limits organic growth

SIM penetration hovers well above 130% of the population, leaving scant headroom for net adds. Telia Finland shed 16,000 mobile lines in Q2 2024, even as service revenue rose, underlining the pivot from volume to value. Competition has thus shifted to quality of service differentiation, fixed–mobile convergence bundles, and IoT connections. Operators target enterprise verticals where penetration remains low, such as smart logistics and health wearables, to offset stagnant consumer numbers. [4]GuruFocus, “Telia Company Q2 2024 Earnings Call Highlights,” gurufocus.com

High energy and spectrum costs pressure margins

Finland’s cold climate reduces site-cooling bills, yet electricity accounts for a rising share of opex as 5G densification adds radios. Each carrier also pays spectrum instalments and an information-society levy of 0.135% of telecom turnover. DNA and Telia trial photovoltaic-plus-battery systems and heat reuse to curb costs, but long-run profitability still depends on automated RAN energy-saving software and wholesale dark-fiber access for back-haul cost control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data supremacy underpins IoT momentum

Data and Internet offerings captured 29.45% of Finland telecom MNO market share in 2025 on the back of the nation’s unmatched 63.3 GB average monthly usage. Voice and SMS continued their structural decline as OTT apps displaced legacy services, while fiber expansion bolstered OTT video and cloud gaming take-up. IoT and M2M services will post a 4.41% CAGR to 2031 as manufacturers deploy predictive maintenance, asset tracking, and computer-vision quality control. The Finland telecom MNO market size for IoT SIMs is forecast to reach 59.1 million connections by 2031, equal to 10× Finland’s population, creating scale benefits for core signaling infrastructure. DNA and Telia have broadened their NB-IoT and LTE-M footprints to support battery-powered sensors, whereas Elisa focuses on 5G RedCap for mid-bandwidth industrial cameras.

Second-generation OTT and Pay-TV bundles gain traction as 68% of households sit within fiber coverage, letting operators upsell gigabit fixed-wireless access in rural communities where trenching costs remain prohibitive. High-capacity packages include parental controls and zero-rated local streaming, a differentiator amid homogeneous mobile tariffs. Other services, such as cloud PBX and secure SD-WAN, leverage the same core network, offering margin-accretive cross-selling opportunities to SMEs.

By End User: Enterprises ignite private network wave

Consumer lines still dominate with 66.80% of the Finland telecom MNO market size in 2025, but growth is modest as penetration edges toward saturation. Operators thus emphasize load-balanced plans, device financing, and content bundles to elevate ARPU. In contrast, enterprise subscriptions will expand at a 4.65% CAGR through 2031, propelled by Industry 4.0 adoption and campus private 5G roll-outs. Hospitals such as Oulu University Hospital employ standalone 5G slices for tele-surgery, while logistics hubs deploy 5G drones for inventory audits, validating mission-critical wireless. The Finland telecom MNO market size for enterprise e-SIM fleet management is expected to surpass USD 229.4 million in 2031, underscoring monetization beyond connectivity alone.

Operators adopt network-as-a-service models where enterprises rent throughput profiles and edge compute resources per hour, mirroring cloud-service pricing. Consumer and enterprise workloads coexist on shared infrastructure via network slicing, preserving cost efficiency while enforcing SLA segregation. This architecture aids operators in extracting incremental revenue from premium latency tiers without duplicating physical assets.

Geography Analysis

Finland’s dense 5G footprint places metropolitan Helsinki, Tampere, and Turku among Europe’s fastest median download speeds above 380 Mbps. Rural Lapland lags but benefits from EU-funded fiber back-haul that feeds high-power 5G macro cells, improving spectral efficiency. The Finland telecom MNO market size for northern provinces rose 3.7% in 2025 after years of stagnation, reflecting improved digital inclusion. Cross-border fiber with Sweden via GlobalConnect’s 3-petabit link strengthens Finland’s role as a Baltic data gateway, lowering latency to Frankfurt and Warsaw. This attracts hyperscale data-center traffic, raising wholesale IP transit revenues.

Industrial clusters along the west coast, notably Ostrobothnia, command early private 5G adoption as manufacturing constitutes 17% of regional GDP. MNOs partner with local utilities for pole-sharing, reducing deployment cost per square kilometer by 22%. Eastern regions encounter demographic headwinds; youth out-migration suppresses voice traffic yet creates opportunity for fixed-wireless access that substitutes absent cable networks. EU cohesion funds further finance remote base-station solarization, aligning with Finland’s 2035 carbon-neutrality target and lowering long-run opex.

Competitive Landscape

Finland exhibits an oligopolistic structure where the top three carriers control 89% of subscriptions, driving disciplined pricing behavior. Elisa maintains leadership through early standalone 5G rollout and award-winning customer care, while Telia Finland leverages pan-Nordic operations to secure enterprise contracts that bundle cross-border connectivity. All three invest in massive MIMO upgrades and mmWave trials to prepare for 6G. Infra sharing remains limited to rural passive towers, reflecting each operator’s preference to own differentiated radio assets in urban areas.

Vendor dynamics shift as Nokia completes its acquisition of Infinera, promising high-capacity optical back-haul that dovetails with Elisa’s 25G PON trials. Ericsson supplies mid-band radios for Telia, while Huawei’s presence has receded due to security policies, leading DNA to diversify toward Samsung open-RAN pilots. Private-network specialists add competitive tension; Boldyn Networks’ acquisition of EDZCOM injects an independent wholesale model for campus 5G, prompting incumbents to co-market slice-based offers to defend share. Carriers also explore green financing to fund zero-carbon base-station retrofits, tying tariff structures to ESG metrics valued by Finnish consumers.

Finland Telecom MNO Industry Leaders

Elisa Oyj

Telia Finland Oyj

DNA Plc (Telenor)

Ålcom (Ålands Telekommunikation Ab)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: DNA’s Nasdaq Helsinki-listed bond matured, ending standalone financial disclosure obligations while integration into Telenor Group reporting continues.

- February 2025: Boldyn Networks deployed a private 5G network at Oulu University Hospital, expanding private-network use beyond manufacturing.

- November 2024: Google purchased land in Muhos and Kajaani for EUR 27 million to expand Finnish data-center capacity under a EUR 1 billion investment pledge.

- September 2024: Traficom reported fiber networks passed almost 2 million homes, lifting household coverage to 68% and highlighting regional speed disparities.

Finland Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The Finnish telecom market includes an in-depth trend analysis based on connectivity, such as fixed networks, mobile networks, and telecom towers. Telecom services are segmented into voice services (wired and wireless), data and messaging services, and OTT and PayTV services. Several factors, including an increasing demand for 5G, will likely drive the adoption of telecom services in Finland over the coming years.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and Pay-TV Services |

| Other Services (VAS, Roaming, Enterprise and Wholesale) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and Pay-TV Services | |

| Other Services (VAS, Roaming, Enterprise and Wholesale) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Finland telecom MNO market in 2026?

The market is valued at USD 5.25 billion in 2026 and is set to grow at a 4.33% CAGR to 2031.

Which service segment leads revenue?

Data and Internet services lead with 29.45% share, thanks to Finland’s world-leading mobile data consumption.

Why are enterprises the fastest-growing user group?

Private 5G campus networks for manufacturing and healthcare drive a 4.65% CAGR in enterprise subscriptions through 2031.

Which operator offers the best overall mobile experience?

DNA ranked first in Opensignal’s May 2025 report with a score of 80.8.

How does EU funding influence rural connectivity?

EUR 32 million in Recovery and Resilience funds accelerated fiber roll-outs, lifting household fiber coverage to 68% in 2024.

What risks threaten operator margins?

Rising energy prices and ongoing spectrum instalments raise operating costs despite revenue gains.

Page last updated on: