Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

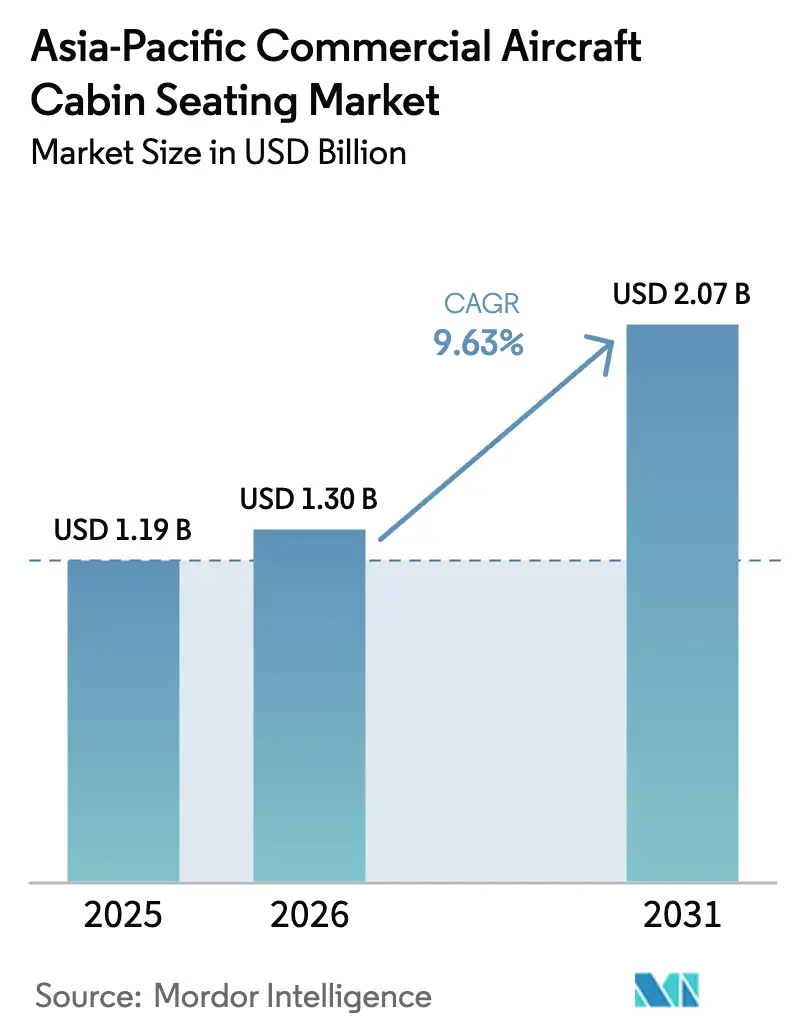

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

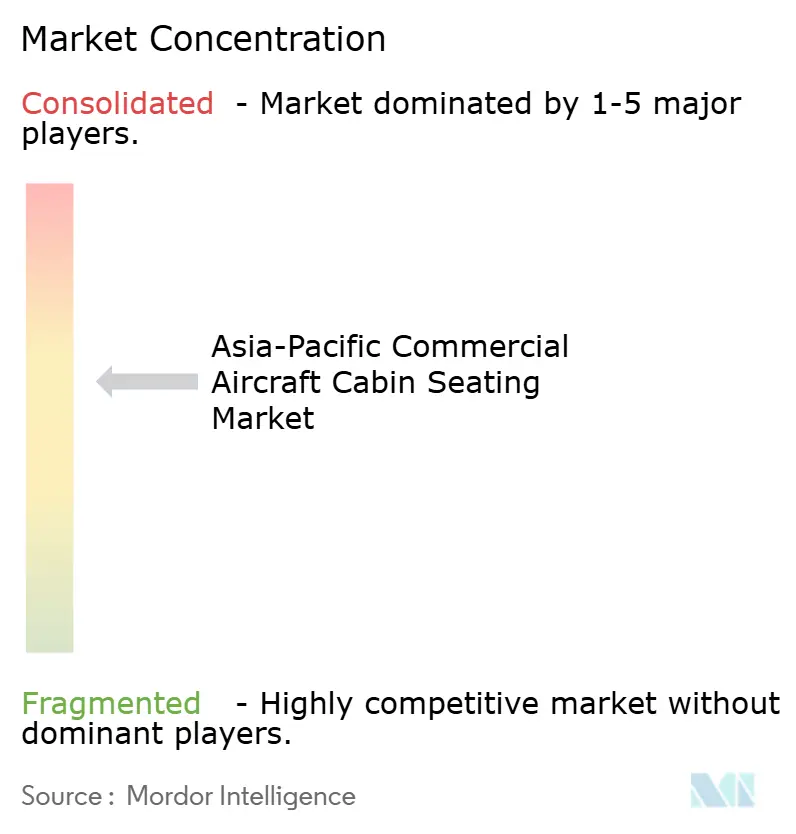

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Commercial Aircraft Cabin Seating Market Analysis by Mordor Intelligence

Asia-Pacific commercial aircraft cabin seating market size in 2026 is estimated at USD 1.30 billion, growing from 2025 value of USD 1.19 billion with 2031 projections showing USD 2.07 billion, growing at 9.63% CAGR over 2026-2031. Narrowbody fleet expansion, cabin differentiation races, and supportive industrial policies propel revenue momentum across linefit and retrofit channels. Suppliers now compete on cabin technology rather than list price, weaving biometric check-in, wireless charging, and IoT diagnostics into seat architecture to lift airline yields. At the same time, premium-cabin investments subsidize economy-class pricing, intensifying demand for lie-flat suites, while composite weight-saving programs align with carriers’ net-zero commitments. Policy mandates in China and India accelerate local supply-chain emergence and reshape long-term competitive dynamics.

Key Report Takeaways

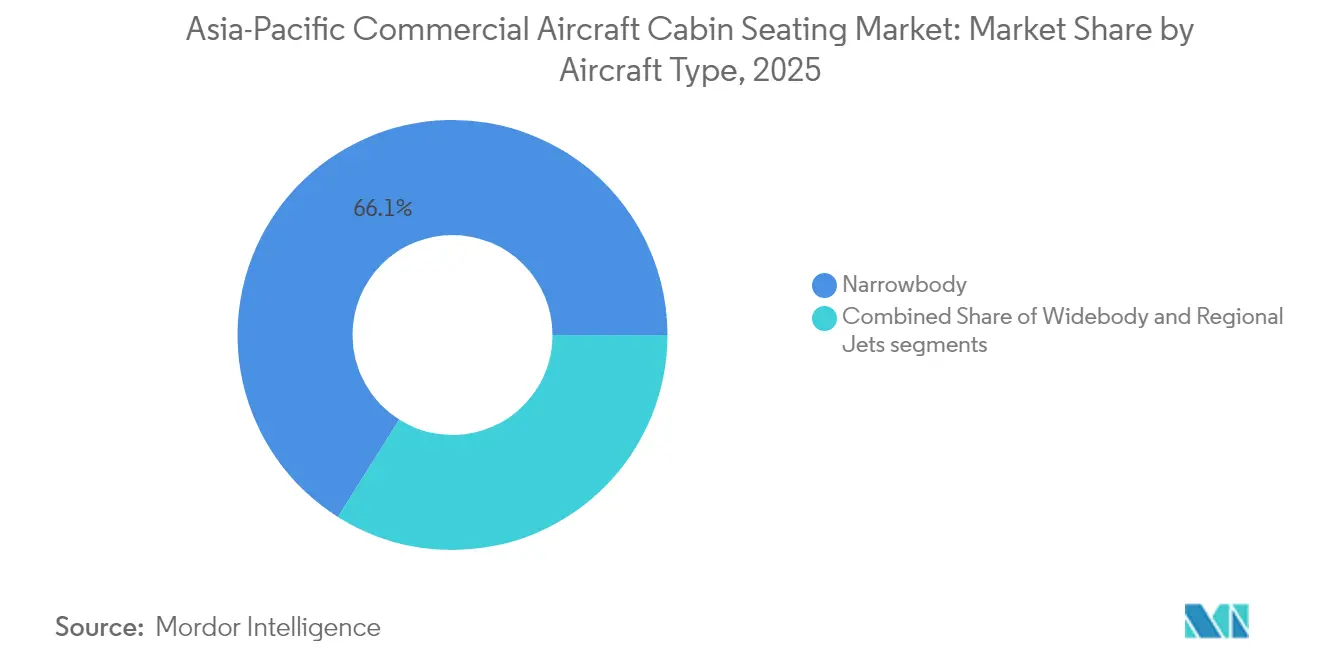

- By aircraft type, narrowbody jets held 66.05% of the Asia-Pacific commercial aircraft cabin seating market share in 2025; widebody retrofit programs are advancing at a 10.14% CAGR through 2031.

- By cabin class, economy seating controlled 44.75% of the Asia-Pacific commercial aircraft cabin seating market size in 2025, while premium economy is set to expand at an 11.05% CAGR to 2031.

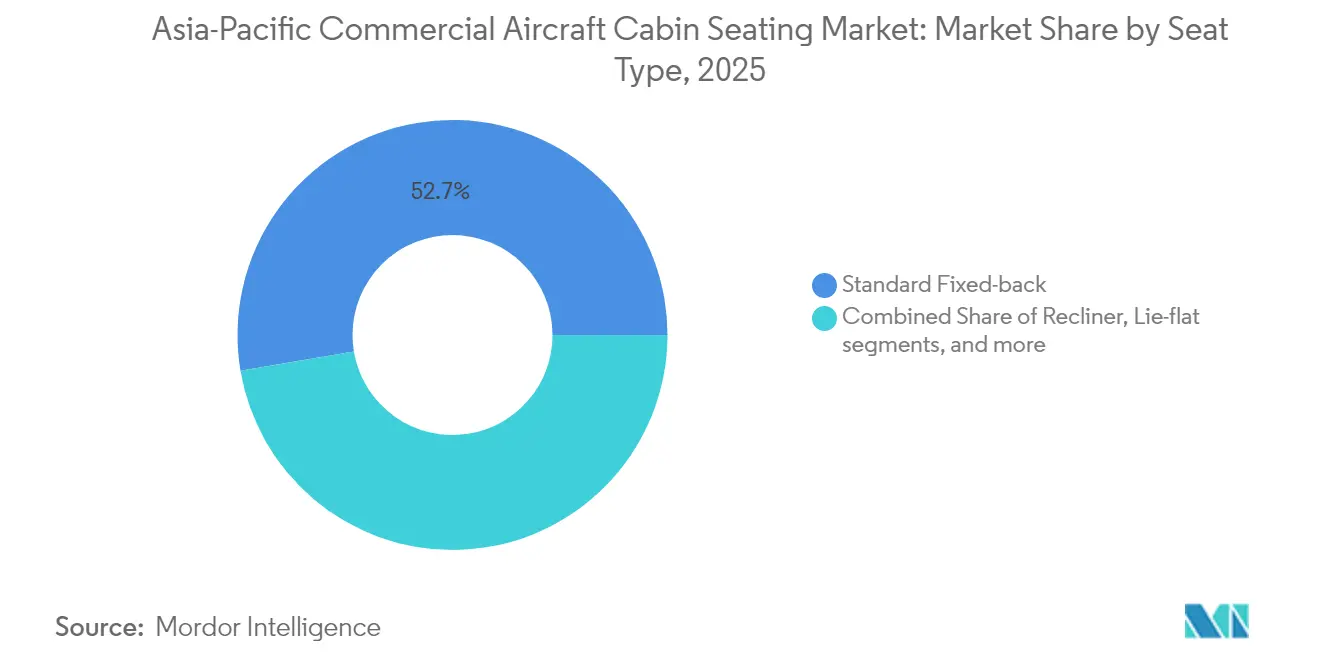

- By seat type, standard fixed-back designs accounted for 52.65% of the Asia-Pacific commercial aircraft cabin seating market size in 2025, and lie-flat products are pacing ahead at a 13.52% CAGR.

- By fit type, linefit installations captured 65.10% of the Asia-Pacific commercial aircraft cabin seating market share in 2025, yet retrofit activities are forecasted to surge at 14.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Commercial Aircraft Cabin Seating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in narrowbody fleet expansion | +2.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Airlines upgrading cabins for passenger-experience differentiation | +2.1% | Japan, Singapore, Australia | Short term (≤ 2 years) |

| Rising disposable income boosting regional air travel | +1.9% | India, Indonesia, Philippines | Long term (≥ 4 years) |

| Government incentives for domestic composite-seat supply chains | +1.6% | China, India | Medium term (2-4 years) |

| Biometric-enabled smart-seat adoption for contact-less services | +1.2% | Singapore, Japan, South Korea | Short term (≤ 2 years) |

| Light-weight seating aligned with airlines’ net-zero targets | +0.8% | Regional | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Narrowbody Fleet Expansion

Boeing predicts that Asia-Pacific airlines will take delivery of 13,560 single-aisle jets by 2043, or 78% of all new aircraft in the region.[1]Boeing Commercial Airplanes, “Commercial Market Outlook 2024-2043,” boeing.com Large orders, such as IndiGo’s 500-plus A320neo-family backlog, drive volume-based seat contracts that favor suppliers with automated, high-throughput lines. Low-cost carriers (LCCs) standardize configurations to reduce maintenance and cabin-cleaning turnaround, creating winner-take-all dynamics on leading aircraft platforms. Seat makers, therefore, emphasize modular designs that meet short-haul economics while offering incremental features like USB-C power and lightweight foams. The single-aisle boom also pulls retrofits forward as airlines accelerate cabin refresh cycles to align older frames with new deliveries and maintain brand consistency across fleets.

Airlines Upgrading Cabins for Passenger-Experience Differentiation

Full-service carriers weaponize cabin ambiance to defend yield premiums against disciplined low-fare rivals. ANA adopted RECARO’s R3 and R4 models to refresh its domestic fleet, citing improved seat pitch and amenity integration.[2]ANA Holdings Inc., “ANA Announces New Seat Selection,” ana.co.jp Singapore Airlines simultaneously rolled out new premium economy hardware and business-class suites, balancing higher capital expenditure with revenue-management gains per seat mile.[3]Singapore Airlines Limited, “Premium Economy and Business Class Upgrades,” singaporeair.com These investments filter down to economy rows, where slimline frames with better lumbar support and Bluetooth audio keep passenger-experience scores high despite dense layouts. Certification pathways under CS-25 force suppliers to intertwine differentiation pushes with rigorous safety testing, yet rapid paybacks on premium-cabin spend reinforce management commitment to continuous upgrades.

Rising Disposable Income Boosting Regional Air Travel

India’s domestic traffic hit 154 million passengers in 2024, a 13% year-on-year surge backed by expanding middle-class incomes and route liberalization.[4]Directorate General of Civil Aviation India, “Passenger Traffic Statistics 2024,” dgca.gov.in As budget carriers tapped secondary airports and island connectors, Indonesia and the Philippines posted similar volume spikes.[5]Ministry of Transportation Indonesia, “Aviation Infrastructure Development,” kemenhub.go.id This tidal demand prizes affordable, durable seats engineered for high cycle counts and lower maintenance budgets. Seat vendors now co-create designs with carriers to stretch warranty mileage and embed easy-swap covers, aligning reliability with tight cost envelopes. Financing packages, including power-by-the-hour seat leases, allow cash-constrained airlines to adopt technology upgrades without up-front hits to balance sheets.

Government Incentives for Domestic Composite-Seat Supply Chains

Beijing’s 60% domestic content rule on C919 programs and New Delhi’s 20% Production-Linked Incentive subsidy for aerospace parts are rewriting sourcing maps.[6]Commercial Aircraft Corporation of China, “C919 Program Update,” comac.cc International seat brands respond through joint ventures and licensed production, pairing design patents with local assembly to clear content hurdles. Certification streamlining for indigenous suppliers cuts approval cycles by 20-30%, eroding legacy vendors’ traditional time-to-market edge. For Tier-2 fabric and foam producers, policy carrots enable rapid scale-up that narrows price gaps with imported alternatives, forcing incumbents to revisit Asian supply-heavy balance strategies and deepen regional engineering footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain disruptions for aluminum and foam materials | −1.8% | China manufacturing hubs | Short term (≤ 2 years) |

| Certification delays under evolving CS-25 and CCAR rules | −1.2% | Global | Medium term (2-4 years) |

| Limited MRO capacity for composite-seat repair | −0.9% | Southeast Asia, India | Medium term (2-4 years) |

| Cabin densification curbing premium-seat retrofits | −0.7% | LCC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions for Aluminum and Foam Materials

Regional aluminum tariffs and petrochemical shortages lengthen seat lead times to 18 weeks, forcing suppliers to build inventory buffers and hedge input costs. Parallel foam raw-material volatility raises working-capital exposure and complicates pricing predictability for airlines finalizing cabin programs months in advance. Quality-assurance teams now screen secondary vendors and invest in batch-level traceability to prevent compliance setbacks, but those checks add cost and delay. Airlines react by clustering orders around dual-qualified seat models, squeezing niche suppliers who cannot guarantee multi-region sourcing resilience.

Certification Delays Under Evolving CS-25 and CCAR Rules

EASA’s latest CS-25 amendments expand dynamic test matrices and cybersecurity validations, prolonging certification to roughly 30 months. China’s CCAR deviations require separate test campaigns, duplicating engineering spend and fragmenting resource allocation for multinational programs. Smart seats with embedded sensors and wireless chargers must also clear heightened electromagnetic-interference thresholds, adding six to 12 months to approval clocks. Smaller design houses face disproportionate strain, as fixed certification fees consume larger chunks of total R&D budgets, nudging them toward alliances or platform licensing deals with bigger incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrow-Bodies Anchor Fleet Growth

The Asia-Pacific commercial aircraft cabin seating market size attributed to narrowbody jets reached USD 786 million in 2025 and is on course to surpass USD 1.39 billion by 2031 on a 10.07% CAGR. This dominance flows from LCC expansion and mainline carriers deploying A320neo and B737 MAX families across point-to-point links. The Asia-Pacific commercial aircraft cabin seating market share for widebodies continues to edge down as airlines favor twin-aisle efficiency over sheer capacity. However, lucrative retrofit contracts on B787s and A350s sustain premium-cabin spending. Suppliers targeting single-aisle programs emphasize high-rate automated lines, fast-change upholstery, and platform-specific mounting rails to keep pace with OEM delivery schedules. In contrast, widebody opportunities revolve around differentiated materials and privacy suites that justify six-figure price tags per triple-seat block.

Regional aircraft garner modest volumes, yet the segment remains necessary for archipelago missions in Indonesia and secondary city connectors in Australia. Range-enhanced variants such as the A220 are blurring boundaries between regional and mainline economics, prompting seat makers to craft hybrid products that match narrowbody weight restrictions while delivering widebody-style amenities. Suppliers that can straddle all three aircraft categories secure risk-diversification advantages, but capital allocation gravitates toward single-aisle programs where yearly output volumes underpin economies of scale.

By Cabin Class: Premium Economy Gains Altitude

Economy retained the largest slice of 44.75% in 2025 in the Asia-Pacific commercial aircraft cabin seating market. Yet, premium economy is the fastest-growing segment, climbing 11.05% annually due to rising discretionary incomes. Airlines view the cabin as a sweet-spot product that upsells price-sensitive business travelers without cannibalizing lie-flat yields. The Asia-Pacific commercial aircraft cabin seating market share for business-class seats remains stable. Still, configuration trends evolve toward 1-2-1 layouts with all-aisle access and sliding doors, pushing average seat cost up by 25-30%. First-class demand dwindles as carriers sunset four-cabin models, redirecting square footage to larger galleys and communal lounges that elevate the brand experience at lower staffing complexity.

For the economy, densification remains a blunt instrument to pare unit costs, yet airlines temper pitch compression with ergonomic foam, articulating seat pans, and in-flight connectivity modules. Premium-economy suppliers integrate calf rests, wider cushions, and individual stowage to distinguish the product tier while preserving dense cabin counts. Revenue-management data shows that a well-priced premium economy seat lifts per-flight contribution margins more effectively than overbook strategies on economy rows, reinforcing management appetite for cabin segmentation.

By Seat Type: Lie-Flat Designs Rapidly Penetrate

The Asia-Pacific commercial aircraft cabin seating market share for standard fixed-back seats stood at 52.65% in 2025, reflecting short-haul density dominance. However, lie-flat adoption logs a robust 13.52% CAGR through 2031 as carriers chase corporate and high-net-worth segments. Recliners upgrade mid-haul comfort on eight-hour missions, yet competitive parity pushes airlines toward full-flat even on selected day flights. Suite-style architecture with sliding doors, privacy wings, and wireless charging represents the apex of the business-class arms race. However, weight penalties and certification hurdles confine widespread rollout to flagship routes. Vendors deploy carbon-fiber spars and bio-foam cushions to shave kilograms and reclaim luggage allowance lost to larger shell structures.

Standard seats remain a volume backbone, and incremental innovation, such as USB-C power, 4-way lumbar, and quick-release dress covers, keeps the product relevant. Suppliers invest in robotized trimming and laser-cutting of cover materials to elevate throughput and consistency without ballooning labor bills. Lie-flat specialists partner with finishers for fine leather and bespoke veneer options, meeting Asian cultural preferences for warm color palettes that mimic hospitality interiors.

By Fit Type: Retrofit Wave Reshapes the Aftermarket

Linefit held 65.10% of the Asia-Pacific commercial aircraft cabin seating market share in 2025. Yet, aftermarket installations are sprinting ahead at a 14.55% CAGR as airlines stretch asset lives and synchronize cabin branding across mixed-age fleets. Retrofit contracts now routinely bundle soft furnishings, lavatories, and connectivity systems, making seats the anchor for holistic cabin refresh packages. Suppliers that field dedicated install teams and maintain spares depots in Bangkok, Hyderabad, and Guangzhou capture schedule-driven airline demand for 10-day turnaround slots. Composite-seat repair lags behind growth, nudging MRO houses into joint ventures with OEMs to import tooling and training programs.

Linefit still delivers integration efficiencies, expanded crash-test certification, digital twin modeling, and OEM warranty coverage that airlines value during growth phases. However, macro headwinds and capital-allocation discipline sway management toward retrofits that deliver immediate customer-experience gains without new-aircraft cash burn. Seat makers, therefore, design modular upgrade kits, arm caps, meal tables, and privacy wings compatible with legacy tracks, enabling phased investment instead of complete row swaps.

Geography Analysis

China commands the largest revenue pool as state-backed fleet expansion and domestic content mandates funnel seat demand to local joint ventures while ensuring a steady backlog for Western partners that transfer tooling know-how. India is the fastest climber; Production-Linked Incentive rebates and LCC fleet additions boost the Asia-Pacific commercial aircraft cabin seating market size tied to the subcontinent by more than 10.8% annually through 2031. Japan’s mature carriers channel spending into premium-cabin overhauls, leveraging partnerships such as ANA’s R3/R4 upgrades for brand differentiation on trunk routes.

Southeast Asia remains the single-aisle epicenter, with Indonesia, Vietnam, and the Philippines reinforcing high-frequency networks prioritizing quick-turn, slimline seats. Singapore’s hub orientation spurs early adoption of biometric-enabled smart seats, with carriers leading trials to streamline boarding flows. South Korea’s tech-forward culture yields receptive customers for IoT-connected cabins, and domestic vendors feed the supply chain with electronic modules adhering to strict cyber-resilience standards. Australia, marked by long stage lengths, prioritizes extra-pitch economy and recliner business seats on narrow-bodies linking remote cities to major capitals.

Competitive Landscape

The Asia-Pacific commercial aircraft cabin seating market exhibits moderate concentration. Collins Aerospace, Safran, and RECARO significantly share regional revenue, leveraging deep catalog breadth and global support centers. They defend share through incremental R&D, evidenced by Collins’ USD 16 million Northern Ireland expansion aimed at low-weight composites and next-gen foam chemistries. Safran focuses on vertical integration, internalizing kitting and dress-cover production to soften aluminum and fabric price swings. At the same time, RECARO secures multi-year block orders from IndiGo and other high-volume Asia-Pacific carriers.

Tier-2 challengers, Thompson Aero Seating, STELIA Aerospace, and Acro, exploit niche opportunities in lie-flat and premium-economy cabins, achieving double-digit revenue growth through flexible engineering cells and shorter internal sign-off cycles. Local entrants in China and India leverage policy nudges to win 5-7-year supply slots on domestic aircraft programs, gradually eroding Western incumbents’ share in the cost-sensitive economy seat segment. Collaboration models shift from traditional license-manufacture deals toward co-design partnerships where intellectual-property ownership is shared, accelerating localization of critical foam, rail, and comfort system sub-assemblies.

Smart seating and sustainability stand out as white-space arenas. Vendors pilot Bluetooth-enabled cushions broadcasting pressure analytics to crew tablets, and bio-based upholstery lines claim 20% lower life-cycle emissions. MRO expansions, such as GMF AeroAsia’s new Singapore alliance, aim to alleviate backlog, yet capacity tightness persists, granting seat OEMs leverage to bundle repair services with initial sale contracts.

Asia-Pacific Commercial Aircraft Cabin Seating Industry Leaders

Expliseat S.A.S.

JAMCO Corporation

Thompson Aero Seating Limited (Aviation Industry Corporation of China)

Safran SA

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: STELIA Aerospace launched the next-generation RENDEZ-VOUS® business class seat, which offers enhanced luxury, flexibility, and comfort features.

- October 2024: Collins Aerospace expanded its executive aircraft seating facility in Medley, Florida. The USD 2 million investment doubled the facility's upholstery production floor space to 30,000 square feet and added new machining equipment that improved production efficiencies, enhanced capabilities, and reduced material waste.

- February 2024: Acro Aircraft Seating showcased its Innovares slimline series at AIX 2024, touting 15% weight savings for LCC cabins.

- January 2024: Collins Aerospace injected USD 20 million into its Northern Ireland R&D hub to accelerate sustainable seat materials and high-rate retrofit solutions.

Asia-Pacific Commercial Aircraft Cabin Seating Market Report Scope

By Aircraft Type

| Narrowbody |

| Widebody |

| Regional Jets |

By Cabin Class

| First Class |

| Business Class |

| Premium Economy Class |

| Economy Class |

By Seat Type

| Standard Fixed-back |

| Recliner |

| Lie-flat |

| Suite/Full-privacy |

By Fit Type

| Linefit |

| Retrofit |

By Geography

| China |

| India |

| Japan |

| Indonesia |

| Singapore |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Aircraft Type | Narrowbody |

| Widebody | |

| Regional Jets | |

| By Cabin Class | First Class |

| Business Class | |

| Premium Economy Class | |

| Economy Class | |

| By Seat Type | Standard Fixed-back |

| Recliner | |

| Lie-flat | |

| Suite/Full-privacy | |

| By Fit Type | Linefit |

| Retrofit | |

| By Geography | China |

| India | |

| Japan | |

| Indonesia | |

| Singapore | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- Product Type - The seats that are integrated into the passenger aircraft and which are made up of a different combination of materials are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms