Aircraft Windows And Windshields Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

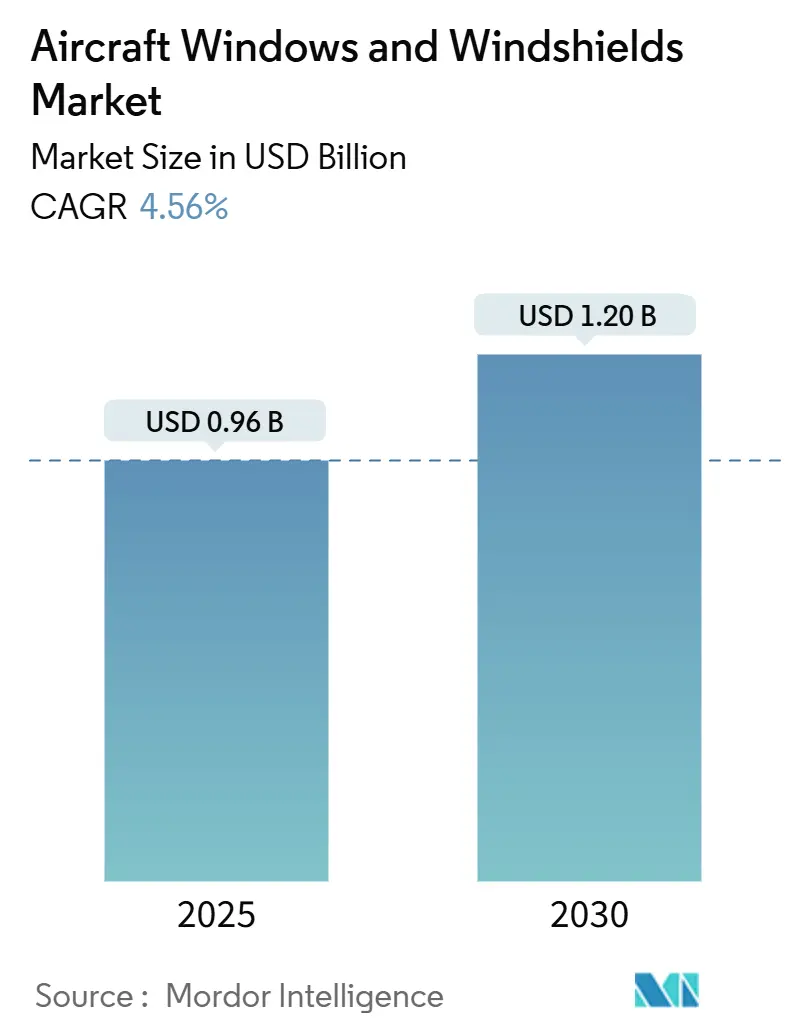

| Market Size (2025) | USD 0.96 Billion |

| Market Size (2030) | USD 1.20 Billion |

| Growth Rate (2025 - 2030) | 4.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Windows And Windshields Market Analysis by Mordor Intelligence

The aircraft windows and windshields market size reached USD 0.96 billion in 2025 and is forecasted to expand at a 4.56% CAGR to USD 1.20 billion by 2030, reflecting persistent growth in global commercial aviation and the robust replacement cycle of aging fleets. Current demand is anchored in two parallel revenue streams: original-equipment fitments for the accelerating build-rates of new jets and a steadily enlarging aftermarket supported by longer aircraft service lives. Boeing’s outlook for 43,975 deliveries through 2043 and Airbus’s projection of 43,420 deliveries over 2025-2044 signal a prolonged production up-cycle, lifting OEM volumes across every transparency category. Cabin windows, already the largest transparency segment, benefit from airline retrofits that improve passenger comfort, while cockpit windshields are advancing through head-up display (HUD) integration and stricter impact-resistance standards. Material innovation is reshaping the competitive landscape as polycarbonate grades post the fastest gains in weight-reduction merits. Moderate supplier concentration persists because certification hurdles lock in incumbents, even as smart-window technologies create premium opportunities for agile entrants.

Key Report Takeaways

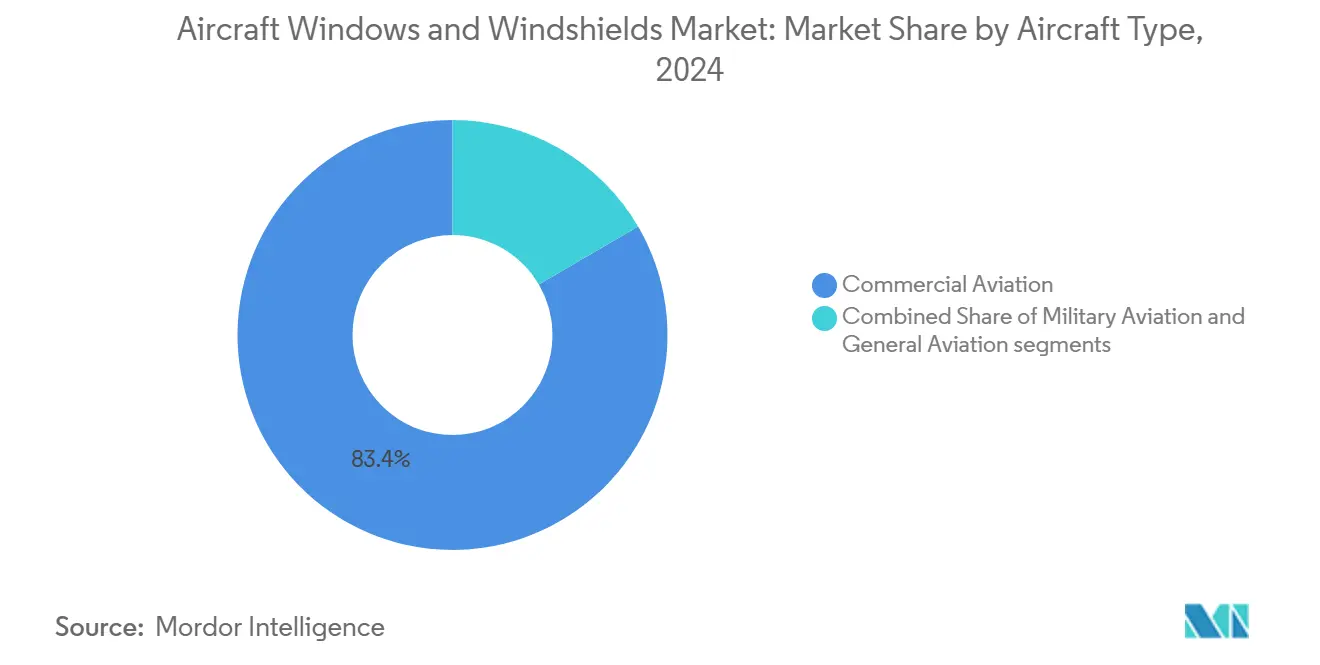

- By aircraft type, commercial aviation held 83.42% of the aircraft windows and windshields market share in 2024 and is progressing at a 5.12% CAGR to 2030.

- By transparency type, cabin windows captured 63.44% revenue share in 2024, while cockpit windshields are advancing at a 5.42% CAGR through 2030.

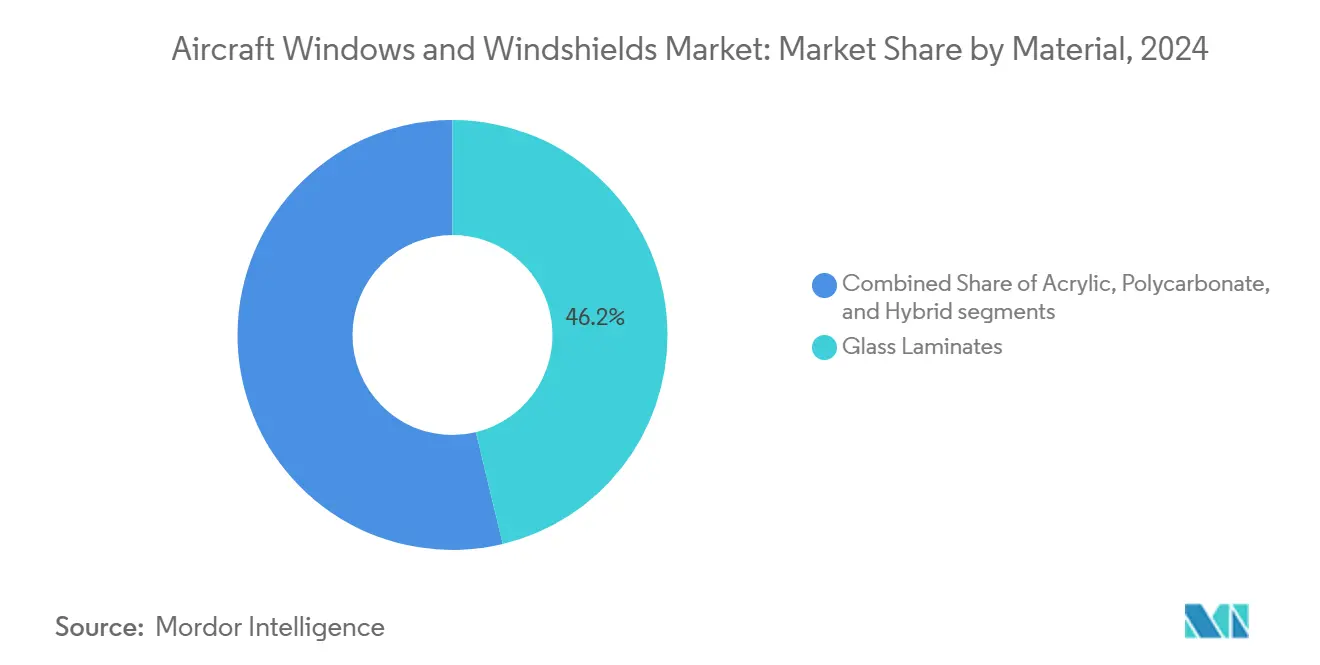

- By material, glass laminates commanded a 46.24% share of the aircraft windows and windshields market in 2024, whereas polycarbonate is projected to grow at a 6.21% CAGR between 2025 and 2030.

- By end market, OEM channels accounted for 58.76% of the 2024 value, yet the aftermarket is forecasted to expand at a 6.37% CAGR to 2030.

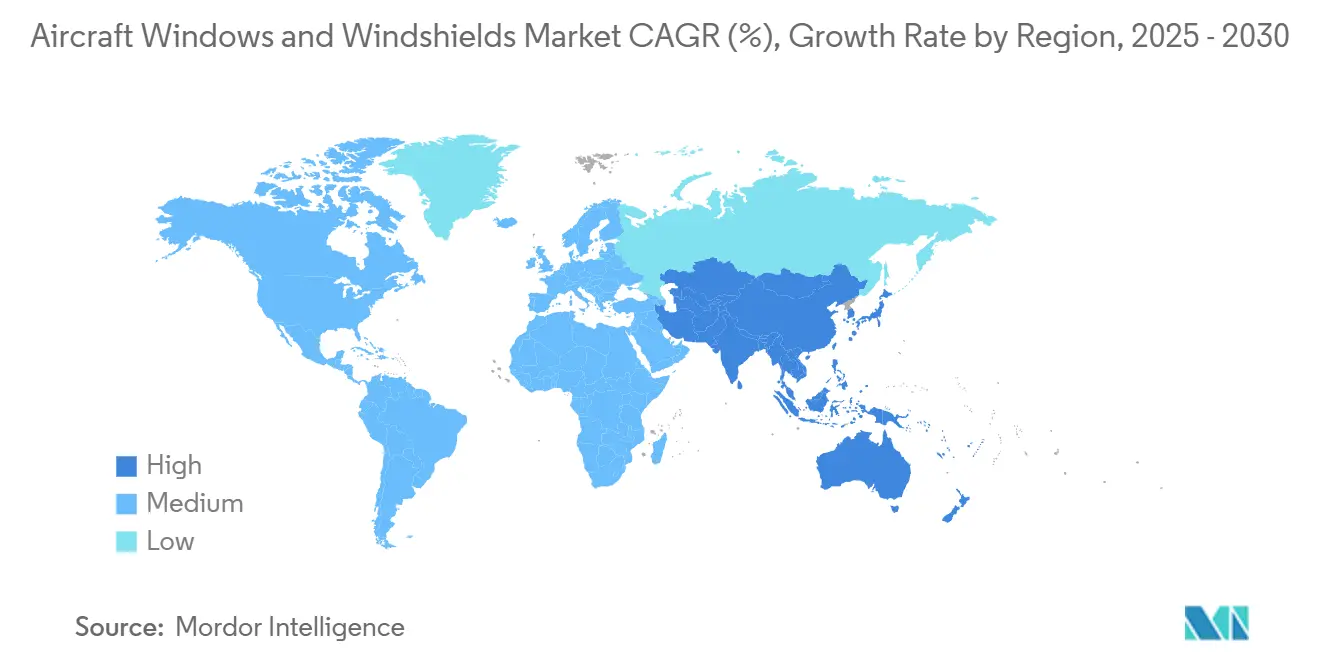

- By geography, North America led with a 37.65% share in 2024; Asia-Pacific is expected to post the fastest 6.12% CAGR through 2030.

Global Aircraft Windows And Windshields Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of the global commercial aircraft fleet | +1.8% | Global with APAC and Middle East leading | Medium term (2-4 years) |

| Replacement demand from aging narrowbody aircraft platforms | +1.2% | North America and Europe core, spillover to APAC | Short term (≤ 2 years) |

| Increasing demand for maintenance and retrofitting of aircraft transparencies | +0.9% | Global, concentrated in mature markets | Long term (≥ 4 years) |

| Advancements in lightweight, durable window materials for fuel efficiency | +0.7% | Global, early adoption in premium segments | Medium term (2-4 years) |

| Rising integration of smart window technologies in modern aircraft cabins | +0.5% | North America and Europe early adoption, APAC following | Long term (≥ 4 years) |

| Enhanced safety requirements driving development of impact resistant glazing systems | +0.4% | Global, regulatory influence from FAA and EASA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of the Global Commercial Aircraft Fleet

Surging fleet requirements are the primary engine for the aircraft windows and windshields market. Airbus estimates 19,500 new jets for Asia-Pacific alone by 2043, equal to 46% of global demand. Boeing’s corresponding global forecast of 43,975 deliveries underlines a decade-long production boom that lifts transparency volumes across narrowbody and widebody categories. Narrowbody programs account for roughly 68% of projected deliveries, locking in high-volume demand for standard cabin windows. Meanwhile, Middle East carriers are expanding fleets at 5.1% annually through 2035, adding further weight to OEM orderbooks.[1]Zawya, “Middle East fleet to expand at 5.1% annually,” zawya.com These trajectories create a durable supplier baseline, especially those aligned with Airbus and Boeing single-aisle build-rates.

Replacement Demand from Aging Narrowbody Aircraft Platforms

Airlines are cycling out older narrowbody variants to capture up to 25% fuel-burn savings available from next-generation models. Airbus projects 18,930 aircraft will replace legacy jets through 2044, ensuring a large pool of aftermarket transactions for certified transparencies. Component MRO revenue is already running ahead of pre-pandemic levels, rising at 4.3% CAGR compared with 0.6% for airframe heavy checks, a trend that elevates demand for cockpit windshield repairs and cabin-window retrofits.[2]Solomon Partners, “Global Aviation Aftermarket Report 2024,” aviationpros.com Programs like PPG’s FAA-approved A320 sliding-window repair service illustrate how incumbents retain share by bundling certification expertise with cost-saving solutions.

Increasing Demand for Maintenance and Retrofitting of Aircraft Transparencies

Used Serviceable Material (USM) volumes grew roughly 50% year-on-year in 2024 as carriers pursued leaner operating costs, and transparencies occupy a visible share of the USM basket. The aftermarket, equal to 41.24% of the 2024 value, is projected to outpace OEM deliveries because inspection cycles for optical clarity and structural health are tightening under FAA Advisory Circular 25.775-1. Automation initiatives such as Saint-Gobain’s glass-line software with Schneider Electric cut downtime and lift product consistency, enabling faster retrofit program turnaround. PMA penetration remains low at roughly 2% of aftermarket spend, but offers airlines 30 to 40% price relief, carving a potential entry lane for new technology vendors that secure approvals.

Advancements in Lightweight, Durable Window Materials for Fuel Efficiency

Airlines scrutinize every kilogram of weight, so polycarbonate formulations that reduce mass while meeting bird strike benchmarks are in high demand. Polycarbonate’s 6.21% CAGR exceeds any other material class, delivering impact strength and fuel-saving weight cuts. Research into electrochromic polymers has demonstrated optical contrast up to 97% with thermal stability beyond 400 °C, opening pathways to multifunctional transparencies that fuse dimming, UV filtering, and thermal control in one assembly. Gentex, already supplying electronically dimmable windows for the B787, ships more than 50 million devices annually, showing that the aerospace-grade smart-window scale is commercially viable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged certification and regulatory approval timelines | -0.8% | Global, FAA and EASA jurisdictions most affected | Long term (≥ 4 years) |

| Volatility in aerospace grade raw material prices | -0.6% | Global with supply-chain concentration risks | Short term (≤ 2 years) |

| Capacity limitations in global ITO and gold coating deposition facilities | -0.4% | Global, concentrated in specialized plants | Medium term (2-4 years) |

| Escalating cybersecurity requirements for sensor integrated aircraft windows | -0.2% | North America and Europe regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged Certification and Regulatory Approval Timelines

Extended certification loops slow product refresh cycles and raise development costs, reducing the velocity at which innovations penetrate the aircraft windows and windshields market. Documentation for Supplemental Type Certificates (STCs) can stretch 9-12 months, discouraging smaller entrants that lack deep compliance teams. The complexity is higher for smart windows because they must satisfy both structural and cyber-hardening criteria. Consequently, OEMs gravitate toward established suppliers, limiting competition and moderating price pressures.

Volatility in Aerospace-Grade Raw Material Prices

Fluctuating prices of aerospace-grade glass, polycarbonate resins, and conductive coatings strain margins, particularly for long-duration OEM contracts that lock pricing two to three years ahead. Supply-chain concentration in specialty ITO and gold-coating facilities exacerbates exposure, forcing manufacturers to hedge costs or renegotiate clauses mid-contract. Periods of sudden price spikes can delay retrofit programs as operators defer non-essential maintenance, temporarily slowing aftermarket momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Commercial Aviation Drives Market Leadership

The commercial segment is projected to rise at a 5.12% CAGR through 2030 as Airbus and Boeing single-aisle backlogs swell. Narrowbody programs lead by volume due to burgeoning short-haul networks, yet widebodies deliver higher dollar content per shipset because of larger cockpit and passenger-window acreage. Though budget cycles cap growth, military fleets keep a stable baseline, benefiting from rotorcraft life extension and special-mission conversions.

Commercial deliveries dominate 83.42% of the market share because airlines in North America and Asia-Pacific prioritize fleet renewal for operating-cost advantages. The aircraft and windshields market continues attracting retrofit spending as low-cost carriers (LCCs) upgrade cabins and introduce LED-backlit shadeless windows for branding impact. Business-jet and emerging eVTOL platforms provide an innovation sandbox, with panoramic polycarbonate domes and augmented-reality displays under test, but still a modest revenue slice.

By Transparency Type: Cabin Windows Lead with Cockpit Innovation

Cabin windows accounted for 63.44% of the aircraft windows and windshields market size in 2024, reflecting their high volume across single-aisle and twin-aisle programs. Growth remains solid as carriers retrofit standard windows with dimmable or larger-aperture variants to lift Net Promoter Scores.

Although representing a smaller denominator, cockpit windshields are forecast to be the fastest-growing transparency at 5.42% CAGR because head-up display interfaces and advanced heating grids mandate new designs. The aircraft windows and windshields market benefits as regulations on bird-strike survivability tighten, encouraging early replacement cycles. Other transparencies, such as emergency exits, retain a consistent niche, governed largely by mandatory inspection calendars rather than discretionary upgrades.

By Material: Glass Laminates Maintain Leadership Despite Polycarbonate Growth

Glass laminates held a 46.24% share in 2024 but are losing incremental share to polycarbonates, which promise double-digit weight savings. High-strength glass remains essential for cockpit zones where thermal gradients and impact loads are most severe, sustaining its prime position.

Polycarbonate panels, advancing at a 6.21% CAGR, unlock weight reductions that translate into lower fuel burn, a priority aligned with airline decarbonization commitments. Because of their lower cost, acrylic grades remain entrenched in general aviation and rotorcraft formats. Hybrid multilayer solutions emerge as a bridge technology that blends glass scratch-resistance with polycarbonate toughness, underpinning the next wave of R&D within the aircraft windows and windshields market.

By End Market: OEM Dominance with Aftermarket Acceleration

Due to steadfast jetliner production rates, OEM shipments represented 58.76% of 2024 revenue. However, the aftermarket is moving faster at 6.37% CAGR, driven by aging fleets whose average age exceeds 11 years in several regions.

Safety mandates require regular transparency inspections for optical haze and micro-cracks, stimulating replacement sales. Airlines increasingly select FAA-approved repaired units and PMA parts when available, highlighting a subtle but steady shift toward cost-optimized sourcing. Therefore, the aircraft windows and windshields market balances high-margin replacement work with volume-driven OEM lines, creating a diversified revenue outlook for incumbents and new entrants.

Geography Analysis

North America held 37.65% of global revenue, reflecting entrenched manufacturing clusters and a dense airline network. Absolute growth is modest, but aftermarket intensity is high because the region fields one of the oldest flying fleets.

Asia-Pacific is the breakout geography, expanding at 6.12% CAGR on the back of an unprecedented aircraft pipeline that calls for 19,500 new jets by 2043.[3]Airbus, “2024 Global Market Forecast,” airbus.com Europe commands a mature yet technology-rich base, supporting high-value exports of tempered glass laminates and electrochromic sub-assemblies. At the same time, Middle East carriers continue to up-gauge fleets, sustaining widebody transparency demand. South America and Africa trail in current volume but offer long-run potential once airport infrastructure and financing frameworks deepen.

Competitive Landscape

Supplier concentration is moderate: the top five players collectively hold more than 50% share. PPG Industries leads through a USD 300 million aerospace backlog and a globe-spanning repair-station network that keeps it close to airline hubs. Saint-Gobain leverages cross-sector glazing expertise, recently introducing automation that halves commissioning times in flat-glass production lines.[4]Glass on Web, “Schneider Electric & Saint-Gobain Automation Initiative,” glassonweb.com

Technology differentiation is sharpening. Gentex dominates electrochromic windows, having shipped tens of millions of dimmable devices. Vertical integration is the prevailing strategy: leaders bring coating deposition, autoclave lamination, and certification testing in-house to protect intellectual property and shorten lead times.

Aircraft Windows And Windshields Industry Leaders

PPG Industries, Inc.

Gentex Corporation

The NORDAM Group LLC

Saint-Gobain Aerospace (Saint-Gobain Group)

GKN Aerospace Services Limited (Melrose plc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gentex Corporation unveiled next-generation dimmable glass products for aerospace, featuring larger active areas and improved switching speed.

- January 2025: Delta Air Lines and Airbus broadened their cooperation on sustainable aviation fuel (SAF) and UpNext technology demonstrators.

- March 2024: MIT announced a nano-stitching technique to reinforce composite laminates, improving crack resistance for future windows.

Global Aircraft Windows And Windshields Market Report Scope

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| Cabin Windows |

| Cockpit Windshields |

| Others |

| Glass Laminates |

| Acrylic |

| Polycarbonate |

| Hybrid |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By Transparency Type | Cabin Windows | ||

| Cockpit Windshields | |||

| Others | |||

| By Material | Glass Laminates | ||

| Acrylic | |||

| Polycarbonate | |||

| Hybrid | |||

| By End Market | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the aircraft windows and windshields market in 2030?

The aircraft windows and windshields market is forecasted to reach USD 1.20 billion by 2030, supported by a 4.56% CAGR.

Which aircraft segment drives the highest demand for transparencies?

Commercial jets lead demand, accounting for 83.42% share in 2024 and continuing to grow as Airbus and Boeing single-aisle programs scale.

Why are polycarbonate transparencies gaining popularity?

Polycarbonate offers significant weight reduction and superior impact resistance, fueling a 6.21% CAGR that outpaces traditional glass laminates.

Which region is expected to grow fastest for aircraft windows and windshields?

Asia-Pacific is projected to rise at 6.12% CAGR through 2030, buoyed by requirements for 19,500 new aircraft.

How are smart windows influencing transparency specifications?

Electronically dimmable windows enhance passenger comfort and operational efficiency, prompting airlines to retrofit cabins and OEMs to integrate the technology on new builds.

What restrains rapid adoption of new transparency technologies?

Lengthy certification cycles and emerging cybersecurity standards add cost and time, discouraging smaller suppliers from quick market entry.

Page last updated on: