Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

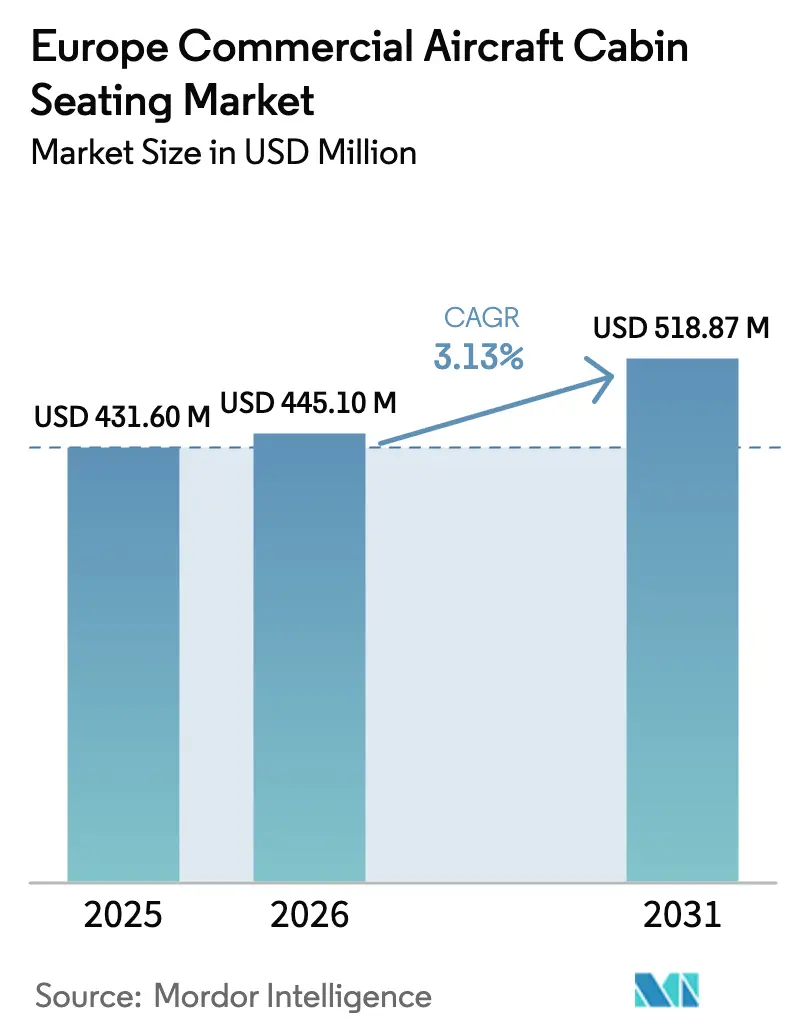

| Base Year Market Size (2025) | USD 431.6 Million |

| Market Size (2026) | USD 445.1 Million |

| Market Size (2031) | USD 518.87 Million |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Commercial Aircraft Cabin Seating Market Analysis by Mordor Intelligence

The Europe Commercial Aircraft Cabin Seating Market size was valued at USD 431.6 million in 2025 and estimated to grow from USD 445.1 million in 2026 to reach USD 518.87 million by 2031, at a CAGR of 3.13% during the forecast period (2026-2031).

The European commercial aircraft seating market is experiencing a significant transformation driven by sustainability initiatives and technological advancements. Manufacturers are increasingly focusing on developing lightweight, non-metallic materials for seat construction to support airlines' fuel efficiency goals and environmental commitments. This shift has resulted in remarkable innovations, with new-generation commercial aircraft seats demonstrating a 30-40% weight reduction compared to previous models. Additionally, other aircraft interior components are following this trend, with modern LED lighting systems offering 40% weight savings over traditional incandescent fixtures while providing enhanced illumination and energy efficiency.

The industry is witnessing a substantial evolution in seating design and passenger comfort features, particularly in premium cabins. Airlines are investing in enhanced seating structures that offer improved ergonomics, adjustable features, and increased personal space. Major European carriers are implementing innovative seating solutions that incorporate advanced materials, smart technology integration, and modular designs. These developments reflect the industry's response to changing passenger preferences and the growing demand for premium travel experiences, with airlines introducing features such as full-flat beds, direct aisle access, and enhanced privacy options.

A notable trend in the market is the increasing preference for narrowbody aircraft configurations, which accounted for 82% of total aircraft deliveries in the region during 2017-2022. This trend is expected to continue with significant orders from major carriers, as evidenced by recent procurement decisions including Rostec's order for 250 aircraft, Ryanair's 200 aircraft order, and Wizz Air's commitment to 102 narrowbody aircraft. These orders reflect the industry's strategic shift toward more efficient and flexible fleet compositions that can serve both short-haul and medium-haul routes effectively.

The market is characterized by extensive fleet modernization initiatives and technological integration in aircraft cabin interiors. Airlines are implementing comprehensive cabin upgrade programs that encompass not only seating but also related systems and amenities. The industry is expected to see the delivery of approximately 2,647 new aircraft through 2030, with 2,354 being narrowbody aircraft, indicating a strong focus on fleet renewal and expansion. These new deliveries are incorporating advanced seating systems with improved materials, enhanced connectivity features, and sophisticated passenger comfort technologies, reflecting the industry's commitment to improving the overall travel experience while maintaining operational efficiency.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Commercial Aircraft Cabin Seating Market Trends and Insights

The main reasons for market growth are the expansion of the fleet and the increased demand for passenger air travel in Europe

- Europe was the second-largest region with the highest air passenger traffic in 2022. Air passenger traffic in Europe reached 1.05 billion in 2022, up by 11% from 2017. Airlines are concentrating on growing their fleet sizes to meet the rising demand for air travel, which may result in a significant increase in the demand for new aircraft in Europe.

- Between 2017 and 2022, a total of 1,206 new aircraft were delivered to Europe, and another 2,647 new jets are anticipated to be delivered between 2023 and 2030. During the historic period, new jet deliveries in Europe amounted to around 25% of global commercial aircraft deliveries. A number of factors may contribute to the increasing number of deliveries during the forecast period, such as LCC’s business innovation to increase passenger load factors, reduce competitive costs, and create an organizational structure that satisfies the demand for travelers with a limited budget while creating distinctly affordable market opportunities. On this note, a total of 1,206 jets were delivered during this period, of which 990 were narrowbody aircraft.

- As of June 2023, around 3,000+ Airbus aircraft were delivered in the region, with major deliveries by A320ceo, A320neo, A321ceo, and A321neo aircraft in the narrowbody segment, and A330-300 and A350-900 in the widebody segment. Several major airlines in Europe, such as Ryanair, Lufthansa, Wizz Air, Aeroflot Group, Air France-KLM, and EasyJet, have a backlog of over 1,600 aircraft, including a mix of narrowbody and widebody jets. Such factors are expected to aid the growth of the commercial aircraft cabin interior market in the future.

The growth in air passenger traffic is expected to be supported by the increasing demand for domestic and international air travel

- The gradual relaxation of travel restrictions in various European countries in 2022 made travel within the continent much easier than during the COVID-19 pandemic. Due to this trend, international demand soared, with passengers unable to travel during the lockdowns eager to fly abroad once again instead of taking domestic vacations. In 2022, air passenger traffic in the whole of Europe reached 1.3 billion, a growth of 8% compared to 2021. The United Kingdom, Germany, and Spain accounted for 36% of the total air passenger traffic in Europe and, hence, may generate more demand for new aircraft compared to other European countries over the coming years. European airlines have also been responsible for carrying almost 40% of global international air passengers.

- European airport traffic grew by 247% in the first six months of 2022 compared to 2021, resulting in an additional 660 million passengers handled across the continent. The United Kingdom, the Netherlands, Turkey, and Germany, which have some of the countries with the busiest airports, recorded a significant rise in passenger traffic in H1 2022. In August 2022, passenger traffic in the top five European airports increased by 68.1% but remained -17.5% below pre-pandemic August 2019 levels, mainly due to continued travel restrictions in Asia. A similar increase in air passenger traffic was observed at airports in the Rest of Europe in August 2022. Commercial air traffic declined from Ukrainian airports, and airports in Belarus and Russia recorded declining passenger volumes as well since the beginning of the Russia-Ukraine War. The air passenger traffic is expected to surge by 31% during 2023-2030, with increased demand in domestic and international aviation.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- The economic development initiatives implemented in the European Union are expected to aid the GDP per capita income growth

- The major OEMs in the market, Boeing and Airbus, are expected to increase their deliveries during 2023-2030, leading to a balanced number of aircraft backlogs

- The surge in the number of passengers has aided the expenditure on aviation infrastructure, with the upgradation of existing airports and the construction of new airports expected in Europe

- The primary source of revenue for aircraft manufacturers is commercial aircraft orders placed with major airlines

- Factors such as recovery in air travel and substantial aircraft orders being placed by various airlines are driving the growth of the market

- Airlines are planning to reduce aircraft fuel consumption in order to reduce the overall aircraft weight

Segment Analysis: Aircraft Type

Narrowbody Segment in Europe Commercial Aircraft Cabin Seating Market

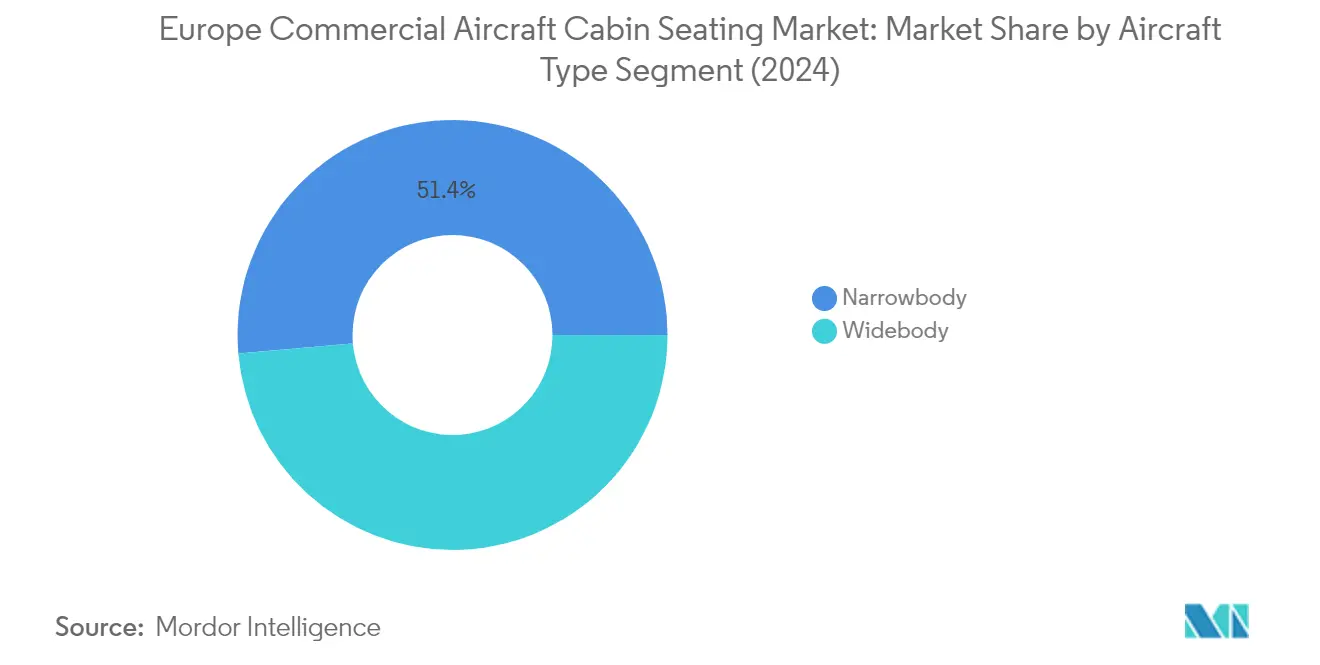

The narrowbody segment dominates the European commercial aircraft cabin seating market, accounting for approximately 50.42% of the total market value in 2025. This dominance is primarily driven by the increasing adoption of narrowbody aircraft by low-cost carriers across Europe for domestic and short-haul international routes. The success of these aircraft is attributed to their operational efficiency and flexibility in fleet management, particularly in serving underserved markets where the frequency of airline services is comparatively lower than conventional routes. Major European airlines, including Air France, British Airways, and Lufthansa, are focusing on enhancing passenger experience by installing lighter, more comfortable aircraft seating configurations with improved headrests in their narrowbody fleet. The segment's growth is further supported by significant orders from carriers like Rostec (250 aircraft), Ryanair (200 aircraft), and Wizz Air (102 narrowbody aircraft), demonstrating the strong market preference for these aircraft types.

Widebody Segment in Europe Commercial Aircraft Cabin Seating Market

The widebody segment is projected to exhibit the fastest growth in the European commercial aircraft cabin seating market, with an expected growth rate of approximately 3.92% during 2025-2031. This accelerated growth is driven by airlines' increasing focus on improving passenger experience for long-haul routes, where widebody aircraft are predominantly utilized. Major carriers are implementing innovative seating solutions, as evidenced by Lufthansa's introduction of the 'Allegris' concept, offering suites with closing doors in both First and Business classes for their new A350 and B787-9 aircraft. The segment's growth is further supported by significant technological advancements in aircraft seating configurations, exemplified by STELLIA Aerospace's launch of their new OPERA business class seat for the Airbus A350 and B787. Airlines are increasingly investing in premium seating configurations for their widebody fleet to enhance passenger comfort on ultra-long routes, driving the demand for sophisticated commercial aircraft seating solutions.

Europe Commercial Aircraft Cabin Seating Market Geography Segment Analysis

Germany represents a cornerstone of the European commercial aircraft seats market, commanding approximately 17.62% of the total market value in 2025. The country's aviation sector has demonstrated remarkable resilience through its emphasis on passenger experience and aircraft cabin interior innovations. Major German carriers, particularly Lufthansa, have been at the forefront of implementing cutting-edge seating solutions across their fleet. The airline's commitment to enhancing passenger comfort is evident in their implementation of the 'Allegris' concept, which introduces suite-style seating with closing doors in both first and business classes. German airlines have shown particular attention to customization and technological integration in their seating solutions, incorporating features such as individually adjustable armrests, ambient mood lighting, and advanced entertainment systems. The country's strong manufacturing base and presence of leading seat suppliers have further strengthened its position in the market. The focus on sustainable and lightweight seating solutions aligns well with Germany's broader aviation industry goals of reducing carbon emissions and operating costs.

Turkey's strategic geographical position as a bridge between Europe and Asia has catalyzed its emergence as a rapidly growing market in the aviation seating sector, with a projected growth rate of approximately 5.74% from 2025 to 2031. The country's aviation sector has been undergoing significant transformation, driven by ambitious fleet expansion plans and modernization initiatives. Turkish airlines are increasingly focusing on enhancing passenger comfort through innovative seating solutions, particularly in their new aircraft deliveries. The country's position as a major transit hub has influenced airlines to invest in premium seating options, especially for long-haul routes. Turkish carriers have been particularly active in adopting new seating technologies that optimize cabin space while maintaining passenger comfort. The emphasis on fuel efficiency has led to increased demand for lightweight seating solutions, contributing to the market's growth. The country's aviation infrastructure development and growing domestic manufacturing capabilities have further strengthened its position in the aircraft seating market.

The United Kingdom maintains a significant presence in the European aircraft interior market, driven by its robust aviation sector and innovative approach to passenger comfort. British carriers have been particularly proactive in implementing new aircraft seating configurations that maximize both comfort and cabin space efficiency. The country's airlines have shown a strong preference for premium seating solutions, especially in their long-haul fleet, reflecting the high proportion of business and premium leisure travelers. British manufacturers and suppliers have been instrumental in developing advanced seating technologies, contributing to the market's technological evolution. The focus on sustainable aviation has led to increased adoption of eco-friendly seating materials and designs. Airlines in the UK have been particularly innovative in their approach to cabin layout and seating configuration, often serving as early adopters of new seating technologies. The presence of major aircraft interior manufacturing facilities and research centers has further strengthened the UK's position in the market.

France's position in the commercial aircraft cabin seating market is characterized by its strong aerospace manufacturing heritage and innovative approach to cabin interior design. The country's airlines have been pioneers in implementing advanced seating solutions, particularly in premium cabin classes. French carriers have demonstrated a strong commitment to passenger comfort through their seating choices, often opting for customized solutions that reflect their brand identity. The presence of major aerospace manufacturers and suppliers has facilitated the rapid adoption of new seating technologies and materials. French airlines have been particularly focused on optimizing cabin space while maintaining high comfort standards, leading to innovative seating configurations. The country's emphasis on design aesthetics has influenced seating solutions that combine functionality with visual appeal. The strong research and development infrastructure in France continues to drive innovations in aircraft seating technology.

The commercial aircraft cabin seating market in other European countries demonstrates diverse trends and requirements, reflecting the varied nature of their aviation sectors. Countries such as Spain, the Netherlands, Switzerland, and the Nordic nations have shown increasing focus on passenger comfort and cabin innovation. These markets are characterized by their emphasis on efficient space utilization and sustainable seating solutions. Regional airlines in these countries often opt for seating configurations that balance comfort with operational efficiency. The presence of both full-service and low-cost carriers in these markets has led to diverse seating requirements, from premium configurations to high-density arrangements. These countries have also been active in adopting new seating technologies and materials that enhance passenger experience while meeting stringent safety and environmental standards. The aviation sectors in these regions continue to evolve, driven by changing passenger preferences and operational requirements.

Competitive Landscape

Top Companies in Europe Commercial Aircraft Cabin Seating Market

The European commercial aircraft cabin seating market is characterized by continuous product innovation focused on lightweight designs, enhanced passenger comfort, and sustainability features. Companies are investing heavily in research and development to create commercial aircraft seats that reduce fuel consumption while maximizing passenger experience through ergonomic designs and premium materials. Operational agility is demonstrated through the establishment of strategic manufacturing facilities and service centers across key European locations, enabling quick responses to customer demands. Strategic partnerships with airlines and aircraft manufacturers have become increasingly important, particularly for line-fit seat installations on new aircraft deliveries. Market leaders are expanding their product portfolios through both organic growth and strategic acquisitions, with a particular focus on developing solutions for both narrowbody and widebody aircraft configurations.

Consolidated Market Led By Global Players

The European commercial aircraft cabin seating market exhibits a highly consolidated structure dominated by established global players with extensive manufacturing capabilities and comprehensive product portfolios. These major players leverage their strong relationships with aircraft manufacturers, extensive certification expertise, and well-established supply chains to maintain their market positions. The market is characterized by high entry barriers due to stringent regulatory requirements, substantial capital investments needed for research and development, and the importance of long-term relationships with aircraft manufacturers and airlines. The presence of specialized regional players adds a layer of competition, particularly in specific market segments such as economy class seating for narrowbody aircraft.

The market has witnessed significant merger and acquisition activity, with larger companies acquiring specialized manufacturers to expand their technological capabilities and market reach. These consolidation moves have helped companies achieve economies of scale, enhance their product offerings, and strengthen their position in key European markets. The trend towards consolidation is driven by the need to offer comprehensive seating solutions across all aircraft types and cabin classes, as well as the importance of maintaining strong financial capabilities to support ongoing research and development efforts.

Innovation and Customer Relations Drive Success

For incumbent players to maintain and increase their market share, focus needs to be placed on developing innovative seating solutions that address the evolving needs of airlines and passengers. This includes investing in lightweight materials, enhanced comfort features, and customization options that allow airlines to differentiate their offerings. Building strong relationships with aircraft manufacturers for line-fit installations and maintaining robust aftermarket support networks are crucial success factors. Companies must also demonstrate their commitment to sustainability through eco-friendly materials and manufacturing processes, while maintaining competitive pricing structures that help airlines optimize their operating costs.

Contenders looking to gain ground in the market need to focus on identifying and exploiting niche opportunities, particularly in emerging segments such as premium economy seating and specialized solutions for narrowbody aircraft. Success in the market requires developing strong technical capabilities, obtaining necessary certifications, and building relationships with key stakeholders in the aviation industry. The ability to offer innovative financing solutions and flexible delivery terms can help newer players compete effectively. Additionally, companies need to carefully monitor regulatory changes related to safety standards and environmental requirements, as these can create opportunities for market entry or expansion through innovative compliance solutions. The integration of aircraft seat components and aircraft seat cushion technologies can further enhance product differentiation and customer satisfaction.

Europe Commercial Aircraft Cabin Seating Industry Leaders

Collins Aerospace

Jamco Corporation

Recaro Group

Safran

Thompson Aero Seating

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2022: Recaro Aircraft Seating was selected by KLM Royal Dutch Airlines (KLM), Transavia France, and Netherlands-based Transavia Airlines to outfit new Airbus aircraft with economy class seats.

- June 2022: STELIA Aerospace and AERQ to collaborate on Cabin Digital Signage integration of OPERA seats for the A320neo family.

- May 2022: Thompson Aero Seating launches next generation VantageXL.

Europe Commercial Aircraft Cabin Seating Market Report Scope

Narrowbody, Widebody are covered as segments by Aircraft Type. France, Germany, Spain, Turkey, United Kingdom are covered as segments by Country.By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Seat Class

| First Class and Business Class |

| Premium Economy Class |

| Economy Class |

By Fit Type

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Material

| Composites |

| Aluminum Alloys |

| Steel and Other Alloys |

| Advanced Thermoplastics |

By Country

| United Kingdom |

| France |

| Germany |

| Spain |

| Italy |

| Russia |

| Rest of Europe |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Seat Class | First Class and Business Class |

| Premium Economy Class | |

| Economy Class | |

| By Fit Type | Original Equipment Manufacturer (OEM) |

| Aftermarket | |

| By Material | Composites |

| Aluminum Alloys | |

| Steel and Other Alloys | |

| Advanced Thermoplastics | |

| By Country | United Kingdom |

| France | |

| Germany | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe |

Market Definition

- Product Type - The seats that are integrated into the passenger aircraft and which are made up of a different combination of materials are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms