Aircraft Door Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

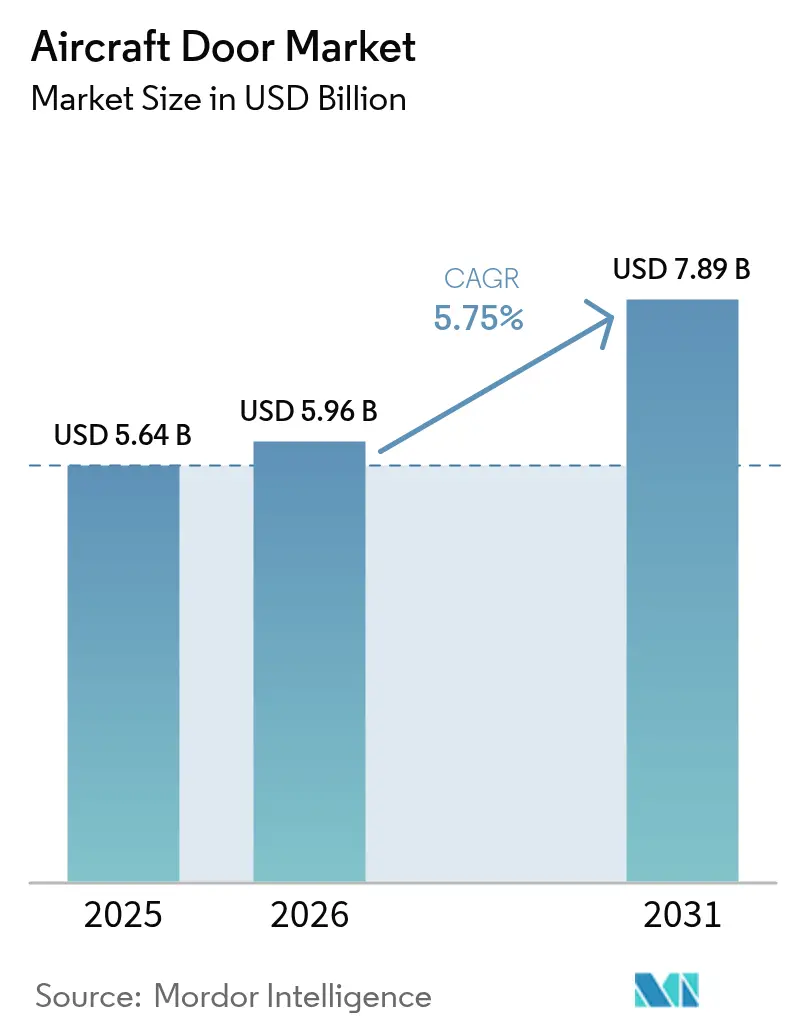

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 7.89 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Door Market Analysis by Mordor Intelligence

The aircraft door market size was valued at USD 5.64 billion in 2025 and estimated to grow from USD 5.96 billion in 2026 to reach USD 7.89 billion by 2031, at a CAGR of 5.75% during the forecast period (2026-2031). Growth has been anchored in record commercial backlogs at Airbus and Boeing, as well as the expansion of global fleets, and stricter safety expectations that prompt airlines to upgrade their door systems. Rising eVTOL production plans, an aftermarket surge linked to an aging global fleet, and the pivot toward electric actuation have further lifted demand. North American dominance rests on its deep OEM and MRO base, while Asia-Pacific’s supply-chain investments signal the next demand wave. Meanwhile, composite designs that reduce door weight by 20%, combined with real-time monitoring mandated by regulators, are reshaping product specifications.[1]Federal Aviation Administration, “Airworthiness Directives; The Boeing Company Airplanes,” faa.gov

Key Report Takeaways

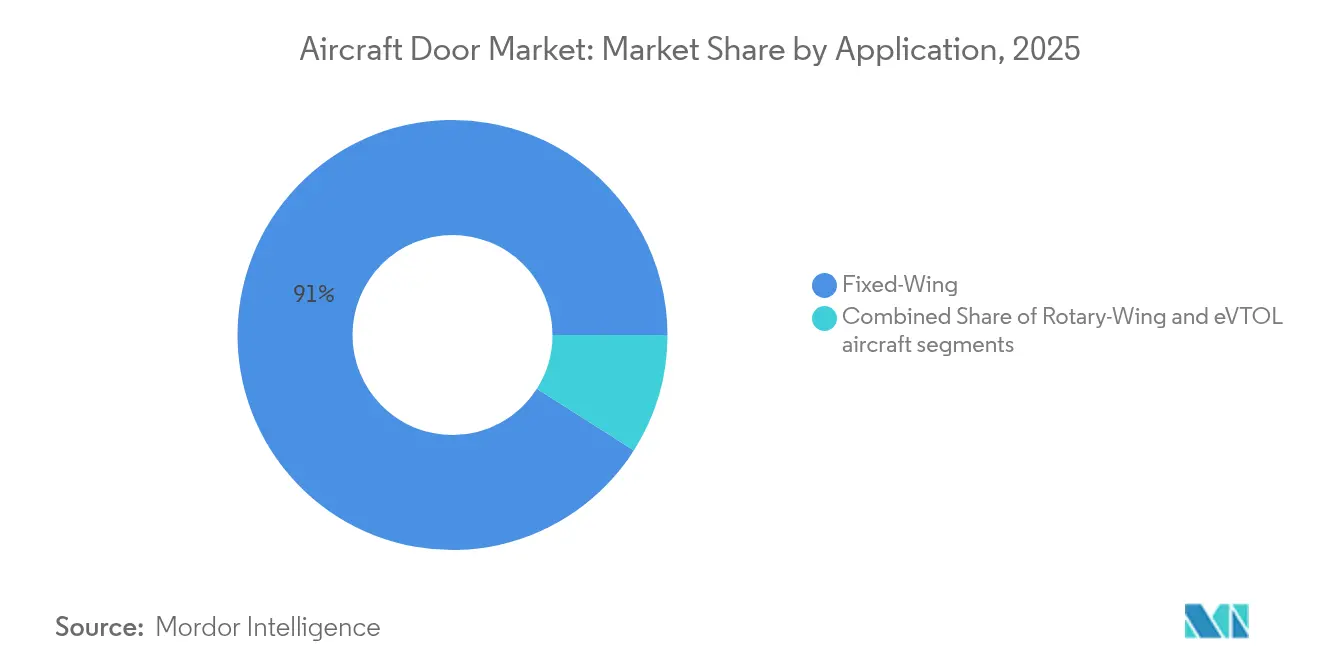

- By application, fixed-wing aircraft doors held 90.98% of the market share in 2025, while the eVTOL segment is projected to grow at an 8.06% CAGR to 2031.

- By door type, passenger doors accounted for 45.52% of the aircraft door market size in 2025 and are projected to advance at a 5.36% CAGR through 2031.

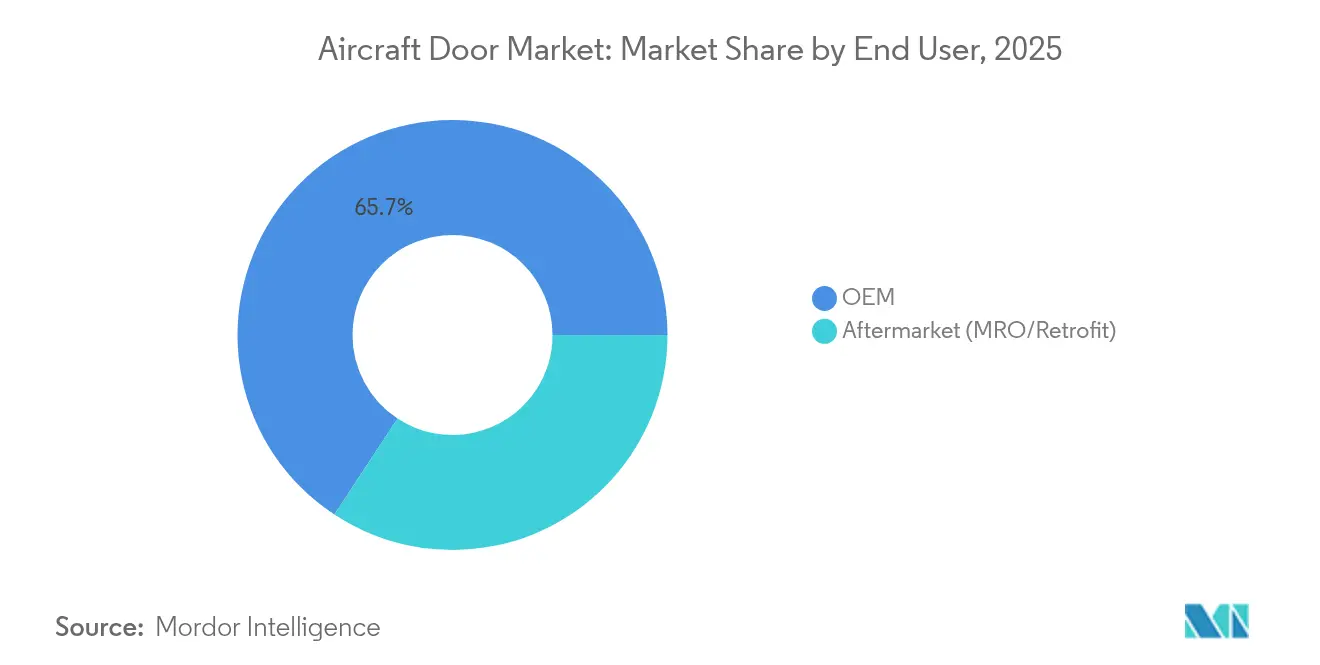

- By end use, the OEM segment accounted for 65.74% of revenue in 2025, while the aftermarket is expected to expand at a 6.22% CAGR between 2026 and 2031.

- By mechanism, hydraulic systems maintained a 52.15% share in 2025; however, the electric mechanisms are forecasted to rise at a 6.84% CAGR through 2031.

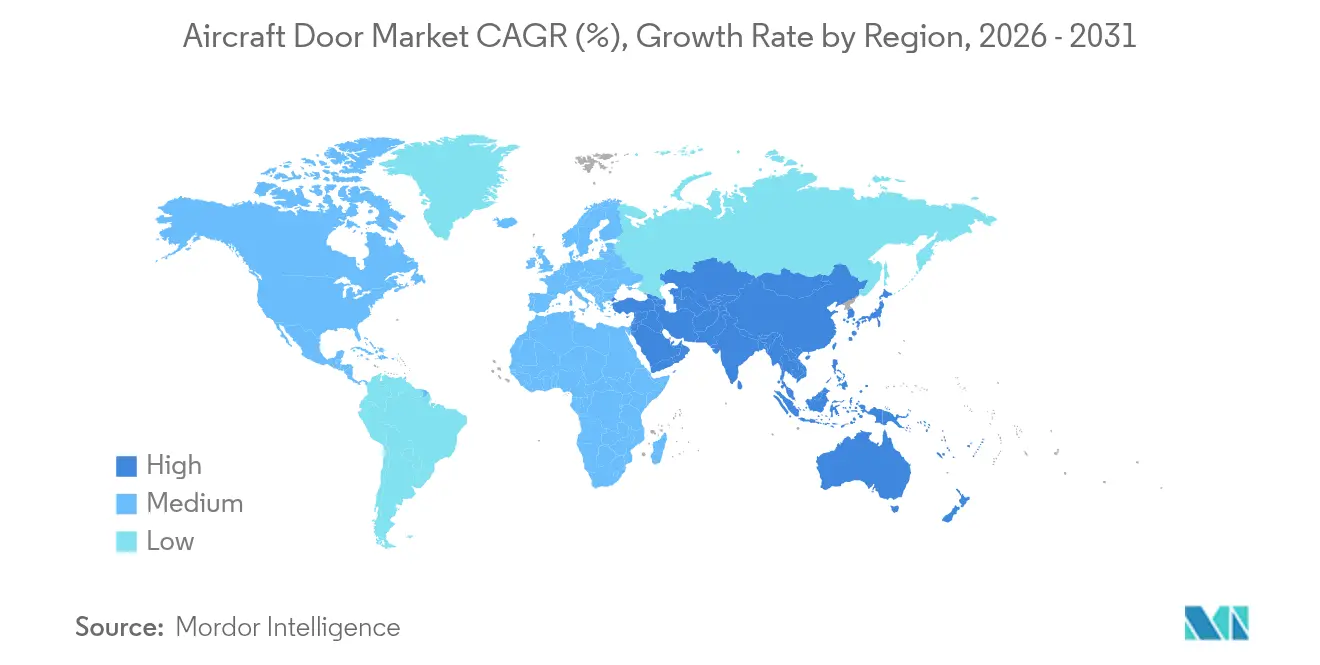

- By geography, North America accounted for 37.88% of the 2025 revenue; the Asia-Pacific region is projected to post the fastest growth, with a 6.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Door Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and aircraft deliveries surge | +1.8% | Global (Asia-Pacific, North America) | Long term (≥ 4 years) |

| Lightweight composite adoption for fuel-efficiency | +1.2% | Global (North America, Europe) | Medium term (2-4 years) |

| Stricter passenger-safety and evacuation mandates | +0.9% | Global (North America, Europe) | Short term (≤ 2 years) |

| Passenger-to-freighter conversion boom | +0.7% | Global (Asia-Pacific, North America) | Medium term (2-4 years) |

| Urban-air-mobility (eVTOL) door innovations | +0.5% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Aging-fleet MRO door replacements | +0.4% | Global (regions with older fleets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion and Aircraft Deliveries Surge

The record number of unfilled orders, 8,658 at Airbus and 5,595 at Boeing in late 2024, created multi-year visibility for the aircraft door market. The backlog would take approximately 14 years to clear at current build rates, prompting suppliers to secure long-term capacity. Airbus projected more than 42,000 deliveries over 20 years, forcing door suppliers to expand their factories and adopt faster production methods, such as Fraunhofer IWU’s four-hour thermoplastic process, which yields 4,000 doors annually.[2]Fraunhofer IWU, “New Concept for Materials and Production Drastically Reduces Manufacturing Time for Aircraft Doors,” iwu.fraunhofer.de MRO providers have followed suit, with facilities adding taller hangar doors to handle widebody traffic.

Lightweight Composite Adoption for Fuel-efficiency

Advanced CFRP and thermoplastic composites cut door weight by up to 20%, trimming fuel burn and extending maintenance intervals. Collins Aerospace's one-piece thermoplastic door demonstrated a production cut from 110 hours to 4 hours by replacing mechanical fasteners with welding.[3]Collins Aerospace, “Future of Flight,” collinsaerospace.com Hexcel's rapid-curing HexPly M51 prepreg supports higher takt rates while retaining structural integrity. These materials integrate easily with electric actuators, reinforcing the industry's move toward a more electric aircraft (MEA) architecture.

Stricter Passenger-safety and Evacuation Mandates

After a 2024 door-panel incident, the FAA placed Boeing under heightened oversight and issued directives covering lavatory and cargo door latches. The NTSB followed with urgent inspection recommendations for B757 door latches. Operators now adopt real-time latch-status sensors and predictive alerts that flag anomalies before gate departure. These requirements pulled passenger doors into the spotlight and accelerated retrofit activity for older fleets.

Passenger-to-freighter Conversion Boom

Over the past two decades, the expected 750 P2F conversions have lifted demand for large cargo doors that withstand high-cycle pressurization. Although narrowbody conversions are expected to decrease to fewer than 50 in 2025, widebody slots remain premium-priced. Door installation alone can reach USD 6.1 million on narrowbody frames and more than USD 14 million on widebody frames, cementing cargo doors as a high-value aftermarket niche.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High R&D and certification cost barrier | -0.8% | Global (more impact in emerging markets) | Medium term (2-4 years) |

| Raw-material price and supply-chain volatility | -0.6% | Global (regions with constrained supply chains) | Short term (≤ 2 years) |

| Lengthy regulatory approval cycles | -0.5% | Global (North America, Europe) | Medium term (2-4 years) |

| Heightened OEM risk-aversion post door-failure incidents | -0.4% | Global (North America) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High R&D and Certification Cost Barrier

Enhanced FAA scrutiny multiplied testing protocols and raised prototype costs, discouraging smaller entrants. Each material or actuation shift invites new certification pathways, lengthening programs, and tilting bargaining power toward large tier-1 integrators that can spread compliance expense across wide product lines.

Raw Material Price and Supply-chain Volatility

Aerospace-grade carbon fiber shortages in 2024-2025 forced door programs to dual-source resins and stockpile longer-lead items. Quality lapses increased as suppliers rushed to clear backlogs, necessitating additional inspection steps. These moves raised working-capital needs and tempered margin expansion for new-technology doors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Demand Split Between Legacy Fleets and Urban Air Mobility

The fixed-wing segment held 90.98% of the aircraft door market share in 2025, primarily driven by narrowbody aircraft, which comprised 62% of the global fleet. That dominance is likely to widen as airlines favor single-aisles for medium-haul routes. Business and general aviation expanded as private travel stayed resilient, encouraging MRO upgrades. Military programs offered steady volumes because US defense spending reached USD 886 billion in 2024.

The eVTOL segment’s 8.06% CAGR has attracted new entrants, such as Eve Air Mobility, which has selected Latecoere as its door supplier for deliveries starting in 2026. Certification frameworks now include vertical take-off constraints that require lighter, wider apertures and intuitive locking. As these aircraft integrate electric propulsion, demand for doors compatible with distributed power management will accelerate.

By Door Type: Passenger Experience Drives Fastest Growth

Passenger doors captured 45.52% of 2025 revenue, led by wide single-leaf designs that simplify evacuation and cabin seating flow. Passenger doors are expected to advance at a 5.36% CAGR to 2031 as airlines retrofit them with sensors and noise-dampening panels. Cargo doors ranked next, backed by P2F conversions and express-parcel trade, which spurred the development of wide apertures capable of handling ULD pallets. Emergency exits gained attention following mid-flight events, triggering latch design overhauls.

Service, utility, and cockpit doors filled niche requirements but benefited from the migration to composite materials. A growing share of the aircraft door market incorporates origami-inspired folding designs, such as the Zen Privacy Door, which simplifies assembly and reduces the number of parts.

By End Use: Aftermarket Narrows the Gap with OEM Production

As Airbus and Boeing pushed line rates higher, OEM deliveries still generated 65.74% of 2025 revenue, yet slots remain short. Fraunhofer IWU’s automated process hinted at profound cycle-time reductions, signalling efforts to protect market lead times. The aircraft door market size for OEM production is expected to expand with backlog clearance, although rate-ramp pressure may put a squeeze on margins.

Aftermarket work is expected to grow at a 6.22% CAGR. The average global fleet age reached 13.4 years in 2025, triggering the need for hinge and seal replacements. The FAA directive on B737 lavatory doors alone affects 2,612 aircraft. Cargo door retrofits in P2F conversions can account for a third of the total conversion expense, underscoring the aftermarket value.

By Mechanism: Electric Mechanism Rises From Niche to Mainstream

Hydraulic systems accounted for 52.15% of the revenue in 2025, primarily due to their ruggedness and legacy certification. Electric mechanisms, growing at a 6.84% CAGR, align with more-electric aircraft agendas and remove fluid-leak risks.

Hybrid systems combine hydraulic power for primary loads and electric drives for fine positioning, striking a balance between redundancy and weight targets. Pneumatic systems stayed niche, suited to regional climate-controlled cargo bays.

Geography Analysis

North America accounted for 37.88% of the 2025 revenue for the aircraft door market, supported by Boeing, a robust MRO network, and sustained defense budgets. FAA directives often set global precedents, so domestic suppliers refine their products first and then export them to other countries. The region's airline fleets had a higher average age, which led to increased aftermarket door replacements. eVTOL certification timelines in the United States drove domestic door suppliers to produce prototypes that pass rotary and fixed-wing criteria.

Asia-Pacific posted the fastest 6.63% CAGR outlook. China's domestic traffic recovery, India's Make-in-India initiative, and A220's door contract with Dynamatic Technologies shifted supply chains eastward. Regional fleets skew young but are growing quickly; door OEMs are establishing in-region composite lay-up plants to reduce logistics costs. Japan's push for fully automated passenger boarding bridges illustrates how airport infrastructure synchronizes with door technology.

Europe remained a technology driver, anchored by Airbus' final-assembly lines and its leadership in sustainable aviation. EASA's emphasis on composite flammability and crashworthiness standards increased certification burdens, indirectly supporting European materials firms. The market share of European composite suppliers in the aircraft door market is expected to rise as demand for thermoplastics increases. Middle East and Africa expanded capacity via Gulf carrier freighter orders, adding large cargo door opportunities that complement regional maintenance hubs.

Competitive Landscape

The aircraft door market featured a moderately consolidated field of tier-1 integrators with vertical capabilities that span concept, build, and service. Safran and Collins Aerospace leveraged avionics and cabin-systems portfolios to offer doors with embedded sensors. At the same time, Latecoere balanced structural expertise with composite know-how across several Airbus and eVTOL programs. Partnerships between airframe OEMs and research institutes accelerated the adoption of thermoplastics; Airbus and Fraunhofer IWU reduced cycle time from 110 hours to 4 hours, positioning thermoplastic doors as mainstream by the end of the decade.

Mergers continued to reshape supplier tiers. Boeing’s exploration of acquiring Spirit AeroSystems could vertically integrate the B737 and B787 door lines, consolidating bargaining power and possibly prompting Airbus to diversify its sourcing. Regional champions matured; India’s Dynamatic Technologies moved from sub-assemblies to complete door packages on the A220, signaling OEM confidence in emerging-market suppliers.

White-space prospects included electric actuation kits for legacy fleets, predictive maintenance software that ties door sensor data to component life prediction, and tailored door modules for eVTOL cabins. Saab’s composite escape doors for the B787 and Mitsubishi Heavy Industries’ automated boarding bridges underscored how adjacent infrastructure solutions feed design priorities.

Aircraft Door Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

LATECOERE S.A

Elbit Systems Ltd.

Premium AEROTEC GmbH (Airbus SE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fraunhofer IWU unveiled an automated thermoplastic door production line that reduces build time from 110 to 4 hours, enabling the production of 4,000 doors annually.

- April 2024: Eve Air Mobility expanded its supplier contracts for its electric vertical takeoff and landing (eVTOL) aircraft, adding four new names. KRD Luftfahrttechnik GmbH (KRD) was contracted to provide its KASIGLAS® polycarbonate windows, while Latecoere will supply the aircraft's doors. Meanwhile, both RALLC and Alltec were contracted to supply fuselage components.

- February 2024: Airbus awarded Dynamatic Technologies a contract to manufacture A220 passenger, cargo, and service doors in India.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global aircraft door market as the value generated from new-build and replacement passenger, service, cargo, emergency-exit, landing-gear, and cockpit doors installed on fixed-wing commercial, regional, business, military, and rotorcraft platforms. Aftermarket retrofit kits and maintenance parts are included where they carry a discrete door bill-of-materials.

Scope Exclusion: Cabin interior partitions, lavatory doors, and jet-bridge boarding bridges are outside the market scope.

Segmentation Overview

- By Application

- Fixed-Wing

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- Business and General Aviation

- Business Jets

- Light Aircraft

- Military Aviation

- Combat Aircraft

- Transport Aircraft

- Special Mission Aircraft

- Commercial Aviation

- Rotary Wing

- Commercial Helicopter

- Military Helicopter

- eVTOL Aircraft

- Fixed-Wing

- By Door Type

- Passenger

- Cargo

- Emergency Exit

- Service/Utility

- Landing Bay

- Cockpit

- By End Use

- OEM

- Aftermarket (MRO/Retrofit)

- By Mechanism

- Hydraulic

- Electric

- Pneumatic

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed air-framer engineering managers, MRO planners across North America, Europe, and Asia-Pacific, and supply-chain directors at door subsystem vendors. These conversations validated typical ship-set pricing, clarified adoption timelines for electric actuation, and benchmarked regional aftermarket failure rates that do not surface in public datasets.

Desk Research

We began by mapping fleet inventories, deliveries, and backlogs from sources such as ICAO traffic databases, IATA fleet factbooks, EASA and FAA airworthiness directives, and UN Comtrade customs codes for HS 8803 door assemblies. Trade association yearbooks (AIA, ASD-Europe) and open access journals covering aerostructure composites enriched our material and cost baselines. Financial filings and investor decks from listed Tier-1 door integrators provided pricing corridors, while D&B Hoovers and Dow Jones Factiva offered supplemental company intelligence. The sources listed here are illustrative; many additional publicly available references supported data collection and cross-checks.

Market-Sizing & Forecasting

A combined top-down fleet-in-service reconstruction and bottom-up supplier roll-up was adopted. We first linked annual production, retirement, and utilization hours to door demand pools, then overlaid representative average selling prices drawn from procurement disclosures. Bottom-up triangulation sampling OEM framework agreements, MRO invoice data points, and channel checks adjusted totals where disclosure gaps existed. Key model drivers include aircraft build rates, active fleet age mix, composite penetration in large doors, regulatory evacuation time targets, electric actuation adoption curves, and regional defense procurement outlays. A multivariate regression with ARIMA error correction projected each driver, delivering 2025-2030 values that were stress tested with scenario analysis for supply-chain disruption odds.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review that flags variance beyond predefined thresholds versus historical trend corridors, trade data, and interview feedback. We refresh every twelve months, and we trigger interim updates when OEM order books, regulatory directives, or raw-material shocks alter the baseline.

Why Mordor's Aircraft Door Baseline Commands Reliability

Published figures often diverge because firms vary door typology, include or exclude retrofits, and apply distinct price curves before currency translation.

Key gap drivers in rival estimates stem from narrower segment coverage, omitting landing-gear doors, optimistic composite cost deflation, and less frequent dataset refreshes that ignore the 2024 narrow-body production rebound.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.64 B (2025) | Mordor Intelligence | - |

| USD 6.30 B (2025) | Global Consultancy A | Excludes military helicopters; applies higher ASP escalation |

| USD 5.77 B (2024) | Industry Analyst B | Uses 2019 fleet retirement ratio; limited primary validation |

| USD 5.22 B (2024) | Trade Journal C | Omits aftermarket; price points sourced solely from press releases |

In sum, our disciplined scope selection, mixed-method modeling, and annual refresh cadence give decision-makers a balanced, transparent baseline that traces every figure to verifiable variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the aircraft door market by 2031?

The market is forecasted to reach USD 7.89 billion by 2031, witnessing a 5.75% CAGR.

Which application segment is growing the fastest?

EVTOL programs are slated to post an 8.06% CAGR between 2026 and 2031.

How large is the aftermarket opportunity?

The aftermarket segment is projected to expand at 6.22% CAGR, driven by a fleet age of 13.4 years and regulatory retrofit mandates.

Why are electric actuation systems gaining traction?

Electric drives reduce weight, eliminate hydraulic fluid risks, and align with more-electric aircraft architectures, supporting a 6.84% CAGR.

Which region will outpace others through 2031?

Asia-Pacific is expected to deliver the quickest 6.63% CAGR, buoyed by fleet growth in China and India and new door manufacturing contracts.

What impact could Boeing’s potential Spirit AeroSystems deal have?

The acquisition would vertically integrate key door production lines, likely reshaping supplier dynamics and sourcing strategies across the market.

Page last updated on: