Africa Aircraft Seating Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

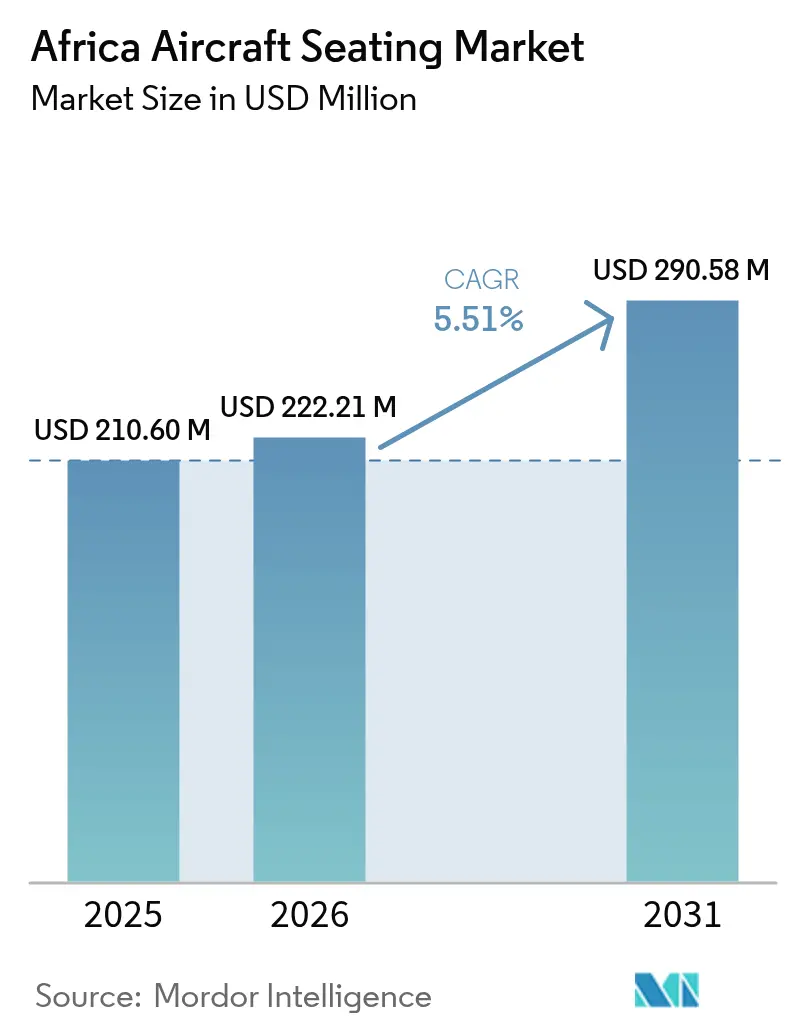

| Base Year Market Size (2025) | USD 210.60 Million |

| Market Size (2026) | USD 222.21 Million |

| Market Size (2031) | USD 290.58 Million |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

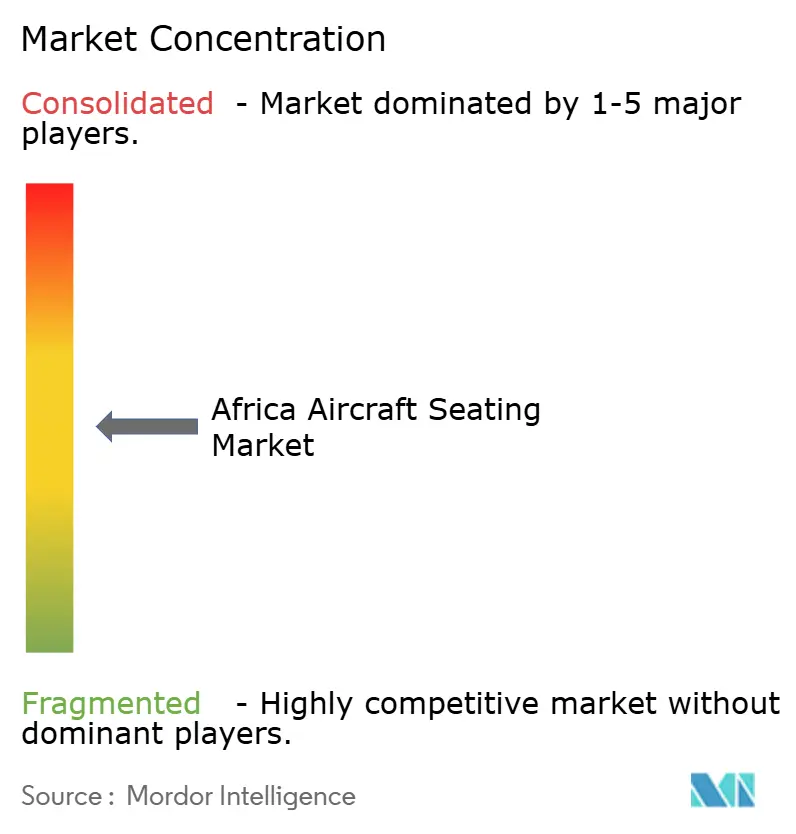

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Aircraft Seating Market Analysis by Mordor Intelligence

The Africa aircraft seating market size was valued at USD 210.60 million in 2025 and estimated to grow from USD 222.21 million in 2026 to reach USD 290.58 million by 2031, at a CAGR of 5.51% during the forecast period (2026-2031). Narrow-body deliveries for high-frequency intra-African routes, premium cabin retrofits on long-haul fleets, and rising defense procurement across North and West Africa are the primary drivers of growth. Ethiopian Airlines, FlySafair, Royal Air Maroc, and Kenya Airways are replacing their heavier legacy seats with composite models to reduce fuel consumption and comply with emerging emissions regulations. Military transport and special-missions helicopters ordered by Nigeria, Egypt, and South Africa feature high-value troop and ejection seats, which increase revenue per unit compared to commercial economy lines. Meanwhile, supply chain pressures persist, as import duties of 15 to 25% and 45-60 day ocean freight lead times inflate landed costs by 20 to 30% compared to Europe or Asia. Operators are therefore expanding local MRO capacity in Johannesburg and Addis Ababa to shorten downtime, lower logistics bills, and secure faster certification windows.

Key Report Takeaways

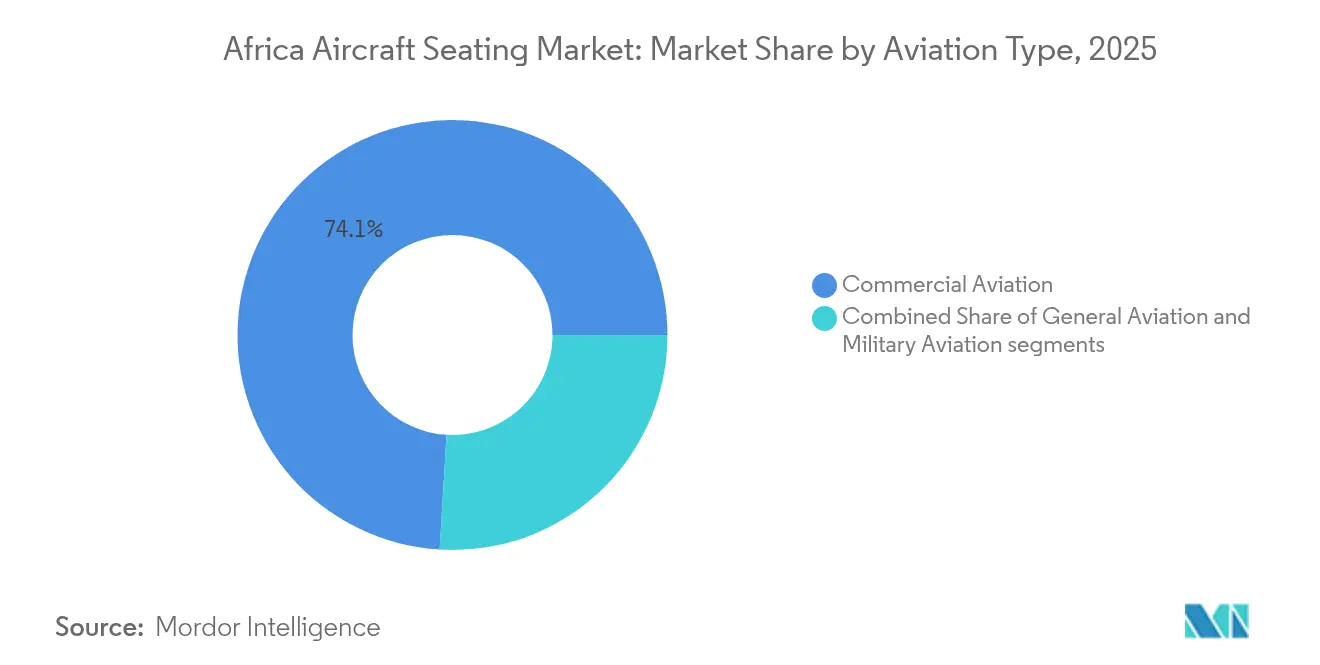

- By aviation type, commercial aviation led with 74.05% of the Africa aircraft seating market share in 2025, while military aviation is forecasted to advance at a 7.06% CAGR to 2031.

- By seat class, economy class commanded 67.88% share of the Africa aircraft seating market size in 2025, and business class is set to expand at a 7.36% CAGR through 2031.

- By fitment, line-fit accounted for 58.20% revenue in 2025, and retrofit programs are projected to rise at a 6.12% CAGR between 2026 and 2031.

- By seat material, upholsteries and seat covers held a 52.02% share in 2025, while structure materials are expected to climb at a 6.78% CAGR to 2031.

- By country, South Africa retained a 46.10% share in 2025, and Ethiopia is forecasted to post a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Aircraft Seating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising single-aisle fleet expansion across African carriers | +1.2% | Ethiopia, South Africa, Morocco | Medium term (2-4 years) |

| Growth of low-cost carrier (LCC) networks driving high-density economy-class demand | +0.9% | South Africa, Kenya, Nigeria | Short term (≤ 2 years) |

| Fleet modernisation favouring lightweight, fuel-efficient seat designs | +1.1% | Pan-African | Medium term (2-4 years) |

| Increasing passenger traffic and route liberalization | +0.8% | 37 SAATM signatories | Long term (≥ 4 years) |

| Under-served intra-African premium-cabin demand at new hub airports | +0.7% | Ethiopia (Addis Ababa), South Africa (Johannesburg), Egypt (Cairo) | Medium term (2-4 years) |

| Emerging African seat-component manufacturing and MRO clusters | +0.5% | South Africa, Ethiopia, Morocco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Single-Aisle Fleet Expansion Across African Carriers

Single-aisle jets form the backbone of the Africa aircraft seating market as Ethiopian Airlines operates 140 aircraft and holds firm orders for 11 B777-9s plus options for additional B737 MAX narrowbodies. Royal Air Maroc has retrofitted its B737-800s with Recaro SL3510 seats, adding two economy rows per aircraft without extending the fuselage length.[1]Acro Communications Team, “FlySafair Selects Series 9 Seats,” Acro Aircraft Seating, acro.aero Kenya Airways leased five B737-800s to replace deferred widebody orders, proving that frequency now trumps capacity on regional routes. Load factors averaged 74% in Q3 2024, so carriers are adopting 28-29 inch pitch layouts that demand high-durability yet low-cost seats priced near USD 3,000 per unit. Seat OEMs able to supply slimline models within 12-week lead times gain a competitive edge on these programs.

Growth of Low-Cost Carrier Networks Driving High-Density Economy-Class Demand

FlySafair operates 28 B737 aircraft and chose Acro Series 9 seats in September 2025, trimming seat weight by 15% and pushing capacity to 186 seats per jet. Fares on Johannesburg-Cape Town routes now undercut intercity bus tickets, so dense cabins are critical to sustain a cost per available seat kilometer of less than ZAR 0.50 (USD 0.03). Air Arabia Africa operates 174-seat A320s from Casablanca to Agadir, offering fares 30-40% lower than those of Royal Air Maroc, which nudges incumbents toward similar seat counts. Fastjet’s 156-seat A319s in Zimbabwe generate ancillary revenue through seat selection, baggage, and priority boarding, helping to offset thin yields. LCC penetration is still below 10% of African capacity, leaving ample runway for dense economy cabins as SAATM rules take hold.

Fleet Modernization Favoring Lightweight, Fuel-Efficient Seat Designs

Recaro’s 8.5-kilogram R1 seat cut Ethiopian’s A350 operating empty weight by 1,200 kilograms per frame in 2024. South African Airways specified similar composite seats on 12 A350-900 orders to save 2,000 kilograms and reduce fuel burn by 1.5% on Johannesburg-New York services. Collins Aerospace unveiled the MAYA concept seat with recycled aluminum and bio-foams that reduce lifecycle emissions by 30%. Expliseat’s 4-kilogram TiSeat holds EASA CS-25 approval, but its USD 5,000 price remains a hurdle for African carriers focused on near-term cash preservation. Weight savings translate directly into added cargo or passenger payload on short runways prevalent across the continent.

Increasing Passenger Traffic and Route Liberalization

SAATM removed bilateral limits for 37 countries, lowering the average intra-African fares by 18% between 2019 and 2024, and lifting Q3 2024 passenger numbers by 11.2% year-over-year. Ethiopian Airlines launched 15 new intra-African routes in 2024, using 154-seat B737-800s to feed its Addis Ababa hub. Kenya Airways reopened the Nairobi-Mogadishu route using 96-seat E190s to test demand ahead of potential B737 upgrades. Liberalized skies stimulate incremental demand for roughly 2,500 to 3,000 new economy seats per year, assuming 150-seat frames and sustained 75% load factors. That volume underpins a steady replacement cycle even without a surge in aircraft orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import duties and logistics costs for seat systems | -0.8% | Nigeria, Kenya, Tanzania | Short term (≤ 2 years) |

| Limited access to aircraft financing and FX volatility | -0.6% | Nigeria, Kenya, Ethiopia | Medium term (2-4 years) |

| Certification bottlenecks across fragmented CAAs | -0.5% | Kenya, Nigeria, Morocco, Tanzania | Medium term (2-4 years) |

| Skilled-labour shortage for cabin-retrofit programmes | -0.4% | Pan-African excluding South Africa and Ethiopia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Duties amd Logistics Costs for Seat Systems

Nigeria levies a 20% import duty plus 7.5% VAT on seats, which increases the cost of a 150-seat retrofit from USD 450,000 to approximately USD 574,000, extending the break-even point beyond five years.[2]Nigeria Customs Board, “Import Duty Tariff 2024,” Nigeria Customs Service, customs.gov.ng Kenya’s 25% tariff on cabin furnishings, coupled with USD 1,200 per ton handling fees at Nairobi, doubles the air-freight rate seen in Johannesburg. Ocean transit from Europe to Lagos or Mombasa averages 45-60 days, and vessel dwell times of 21 days invite demurrage charges that add 10-15% to total landed cost. Ethiopian Airlines enjoys a customs waiver on aviation imports, so its seat costs align with European benchmarks, giving Addis-based MRO units a 15 to 20% price advantage over rivals in Kenya and Nigeria. Persistent bottlenecks prompt carriers to ferry aircraft to Johannesburg or Addis for seat swaps, incurring extra downtime and ferry costs.

Limited Access to Aircraft Financing and FX Volatility

Kenya Airways posted a KES 23 billion net loss in FY 2024, following a 15% depreciation of the KES against USD, which led to increased lease costs for its B737 and B787 fleets. South African Airways paused A350 deliveries in 2024 when export credit agencies withheld guarantees due to sub-investment-grade ratings. Air Peace deferred three B777-300ERs as the naira weakened from NGN 460 to NGN 1,500 per dollar between 2020 and 2024, opting instead for wet-lease capacity. Most seat contracts are denominated in EUR or USD, yet airlines collect fares in local currencies that depreciated 12-18% in 2024, widening the currency mismatch. Afreximbank’s USD 44 million facility to CIAF Leasing covers aircraft hulls but excludes cabin retrofits, leaving seat makers without receivables-backed credit options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aviation Type: Military Procurement Outpaces Commercial Growth

Military procurement is slated to expand at a 7.06% CAGR, surpassing the average growth rate of the Africa aircraft seating market as Nigeria, Egypt, and South Africa add transport aircraft and special-mission helicopters. Nigeria’s Air Force received six AW109s and ordered 12 AW139s with 12-troop cabins, while Egypt integrated 24 Rafales fitted with Martin-Baker ejection seats. Ejection seats can cost USD 150,000 to USD 250,000 each, so the African aircraft seating market benefits disproportionately from even modest fighter deliveries. Commercial aviation still controls almost three-quarters of revenue due to Ethiopian Airlines’ 140-unit fleet and Royal Air Maroc’s B787-9 acquisitions. Regional jets, such as Embraer E190s and CRJ900s, keep thin routes viable, but the median seat life is expected to reach 15 years by 2027, spurring retrofit interest across both sectors.

A second growth lever is helicopter seating for offshore oil and humanitarian missions in Angola, Nigeria, and Mozambique. Crashworthy troop benches, vibration-damped cushions, and quick-release seat tracks carry price premiums over civil economy chairs, lifting the Africa aircraft seating market share for defense suppliers. Growth in military and civil air transport, therefore, yields parallel demand profiles: high-volume, narrowbody seats for passenger carriers, and high-margin, specialty seats for air forces.

By Seat Class: Premium Cabins Capture Connecting Traffic

Business class leads growth at 7.36% CAGR as Addis Ababa, Johannesburg, and Cairo position themselves as long-haul hubs. Ethiopian Airlines selected Safran Z400 suites for its B777-9s, featuring a 78-inch pitch and direct aisle access, aligning with the standards of its Gulf rival. South African Airways selected Collins Super Diamond for its A350-900s to regain its premium share on trans-Atlantic routes. Premium cabins yield up to five times the revenue of economy cabins per square meter, justifying retrofit cycles every 8-10 years despite capital constraints. At the other end, economy class still occupies 67.88% of installed seats in 2025, and carriers like FlySafair favor 28-inch pitch configurations to keep load factors above 80%.

The Africa aircraft seating market size gains additional upside from emerging premium economy sections. Ethiopian’s B787-9s feature 21 premium-economy seats, priced 40% above standard economy, targeting price-sensitive business travelers who avoid full-fare business class. First class remains a sub-2% niche limited to a handful of B777 fleets, indicating that the future mix will skew toward three-class layouts dominated by lie-flat business and dense economy cabins.

By Fitment: Retrofit Programs Gain Traction

Linefit still represented 58.20% of 2025 revenue as Boeing and Airbus delivered factory-equipped seats for Ethiopian Airlines and Royal Air Maroc. Yet retrofit demand is set to rise at a 6.12% CAGR because carriers prefer extending airframe life over committing to new orders amid currency volatility. Ethiopian spent USD 180 million retrofitting 10 B777-300ERs with Safran suites in 2024, completing the work within a four-week downtime window at its Addis Ababa facility. Kenya Airways plans a 2026 retrofit of eight 787-8s, aiming for a 15% weight cut in economy seats. Certification remains a hurdle: Kenya’s CAA requires 12-18 months to validate changes, compared to 6-9 months in Europe, which prolongs payback periods.

Line-fit programs will persist for long-haul fleet renewals, but retrofit’s share rises as used-aircraft imports accelerate. Aircraft retiring from US and European fleets enter Africa with seats nearing the end of life, triggering immediate replacement projects. This dynamic underpins the Africa aircraft seating market as airlines juggle liquidity limits with passenger experience upgrades.

By Seat Material: Composites Drive Weight Reduction

Structural materials are forecast to grow at 6.78% as airlines seek to reduce the weight of economy seats to under 9 kilograms, aiming to trim fuel costs that account for 35-40% of operating expenses. Recaro’s carbon-fiber seatbacks saved Ethiopian 1,200 kilograms per A350 in 2024, improving range and payload margins. Collins’ MAYA concept, which blends recycled aluminum and bio-foam, is under review by South African Airways for future A350 deliveries. Expliseat’s titanium-carbon TiSeat promises a 4-kilogram weight but carries a premium that LCCs have yet to accept. Suppliers who deliver lightweight seats at traditional price points will likely dominate upcoming bids, particularly as jet fuel prices rise.

Upholsteries and seat covers, which still account for 52.02% of the spend in 2025, are evolving toward antimicrobial and bio-based textiles. Ultrafabrics’ SkyLeather weighs 25% less than bovine hides and comes with a five-year antimicrobial guarantee, having already been selected by Ethiopian for B777 retrofits. Muirhead’s silver-ion-treated leather debuted on Royal Air Maroc B787s in 2024. Volar Bio fabric, derived from sugarcane polymers, is awaiting its first African launch customer, marking a significant shift in the sector’s focus toward sustainability.

Geography Analysis

South Africa retained 46.10% of the Africa aircraft seating market in 2025 due to FlySafair’s domestic network and South African Airways’ pending A350 fleet. Johannesburg hosts Lufthansa Technik and Safran MRO shops that can install up to 200 seats per month, drawing retrofit business from Botswana, Namibia, and Mozambique. Certification takes 9-12 months under the South African CAA, which is faster than most regional peers, thereby minimizing revenue downtime for operators.

Ethiopia is the fastest-growing market, with a 6.98% CAGR through 2031, as Ethiopian Airlines expands its fleet to 11 B777-9s featuring Safran Z400 suites and leverages its duty-free import waiver. The Addis MRO complex serviced 25 third-party carriers in 2024, generating USD 180 million in revenue and capturing retrofit work that Nigeria and Kenya lost due to longer customs cycles.

Egypt, Nigeria, Kenya, and Morocco collectively account for roughly 37.65% of the African aircraft seating market size. EgyptAir’s B777-300ER retrofit plan is pending foreign-exchange approval, highlighting currency risk even in large markets. Air Peace seeks additional B777s but leans on wet leases until naira volatility stabilizes. Kenya Airways prioritizes B737 leases over capital-intensive wide-body seats, while Royal Air Maroc utilizes slimline retrofits to increase B737 capacity by 7%. The rest of Africa, led by Angola and Tanzania, accounts for approximately 9.25% of demand, with financing access being the primary constraint rather than seat availability.

Regulatory Landscape

Aircraft seating supplied into Africa is governed through national civil aviation authorities (CAAs) that commonly accept or reference FAA and EASA certification baselines for seats and associated cabin materials. Seat designs and modifications are typically supported by approvals aligned to the EASA CS-ETSO/ETSO C127 series and FAA methodologies for dynamic testing (including 16g test approaches described in FAA AC 20-146A), alongside transport-category airworthiness requirements (for example, CS-25 fire blocking and flammability expectations) used as compliance anchors for fitment and retrofit work.

Within Africa, oversight and acceptance pathways differ by country, which adds validation steps for the same seat shipset or STC across multiple CAAs (for example, SACAA in South Africa, KCAA in Kenya, and TCAA in Tanzania). South Africa also anchors parts manufacturing and maintenance controls through SACAA requirements such as Parts Manufacturing Approval (ZA-PMA) and Part 145 provisions that require traceable release documentation (for example, FAA 8130 or EASA Form 1) for Class II components, tightening controls on untraceable cabin components used in line maintenance and retrofit programs.

Value Chain Analysis

The Africa aircraft seating value chain starts with global seat OEMs and Tier-2 suppliers providing seat structures (aluminum, composites, titanium), cushions and foams, textiles and leather covers, seat actuation and fittings, and certification documentation (TSO/ETSO, flammability and dynamic test substantiation). Seats reach African airlines through line-fit channels (airframer supply chains) and through aftermarket channels that bundle shipsets, kitting, installation engineering, and certification support for retrofits. Local value capture is concentrated in MRO and cabin refurbishment activities, with hubs such as Johannesburg and Addis Ababa handling installation, re-covering, repairs, and seat swaps that reduce ferry time and help mitigate long ocean-freight cycles for inbound components.

Supply constraints and logistics costs keep lead times and landed costs elevated, so airlines and suppliers increasingly use regional assembly, repair, and stocking strategies. A notable upstream shift is the Emirates and Safran Seats MoU (18 November 2025) to build a 20,000 to 25,000 square meter seat manufacturing and assembly facility in Dubai (target completion Q4 2027). The effort is aimed initially at retrofit seat output, with later expansion toward line-fit, which supports nearer-to-market production and shorter replenishment loops for operators serving Africa from Middle East hubs.

Competitive Landscape

Global OEMs, such as Safran SA, Collins Aerospace (RTX Corporation), Recaro Holding GmbH, Thompson Aero Seating Ltd, and Geven SpA, hold a prominent share of line-fit contracts, giving the African aircraft seating market a moderate concentration profile. Safran secured the first African B777X business-class win when Ethiopian selected Z400 suites in 2025. Recaro delivered four B787-9 ship-sets to Royal Air Maroc in 2024 and filed 14 composite-seat patents in the same year, aiming to cut lead times to 10 weeks. Collins Aerospace focuses on sustainability with its MAYA seat, banking on future carbon-pricing regimes to justify higher upfront costs.

Regional specialists fill niches. Acro locked in FlySafair’s 28-aircraft program by guaranteeing delivery within 12 months and a 15% weight cut versus legacy aluminum frames. Expliseat targets ultra-low-cost carriers with the 4-kilogram TiSeat but has yet to secure an order in Africa due to its USD 5,000 price tag. Certification remains a barrier: Kenya, Nigeria, and Morocco each mandate separate validations that add 6 to 12 months and raise costs for new entrants, favoring incumbents with established local engineering hubs.

Opportunities include premium-economy retrofits for intra-African long-haul connectors and lightweight seats for regional jets where 8-kilogram composites could extend range by up to 80 nautical miles. OEMs that bundle seats with financing or offset import duties through local assembly stand to increase their share.

Africa Aircraft Seating Industry Leaders

Safran SA

Collins Aerospace (RTX Corporation)

Recaro Holding GmbH

Thompson Aero Seating Ltd. (Aviation Industry Corporation of China)

Geven SpA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Retrofit and cabin life-extension programs represent a practical whitespace where airlines pursue fuel and weight benefits while managing financing and FX constraints. In the report scope, carriers are executing or planning premium and narrow-body programs (for example, Ethiopian Airlines seat retrofit spend and Kenya Airways planned 2026 787-8 retrofit). Import-duty friction in markets such as Nigeria and Kenya also supports a stronger case for routing more work through established hubs (Johannesburg and Addis Ababa), along with suppliers that can provide certified repair, re-covering, and exchange pools to reduce AOG exposure.

A second opportunity area is building closer regional supply and MRO capability for cabin interiors that can serve Africa-bound fleets via Middle East and North Africa corridors. Steps that reinforce this direction include the Emirates and Safran Seats plan to localize seat manufacturing and assembly in Dubai (MoU signed November 2025) and the establishment of new cabin interior MRO capacity in the wider region, such as Regent Aerospace partnering with Kuwait Airways in February 2026 to create a cabin interior MRO hub focused on seat refurbishment and life-extension. These initiatives align with the need to shorten 45 to 60 day ocean freight cycles and reduce the total downtime economics of seating retrofits for African operators.

Recent Industry Developments

- April 2026: flyadeal finalized its seat supplier selections for its Airbus A330-900neo cabins, choosing Geven for premium economy and Jiatai for economy. The decision adds incremental widebody shipset demand and strengthens Geven's footprint in the region, supporting commonality-driven procurement across Middle East and Africa networks.

- November 2025: Emirates and Safran Seats signed an MoU to establish a 20,000 to 25,000 square meter aircraft seat manufacturing and assembly facility in Dubai, with operations targeted by Q4 2027. The project shifts part of the seat supply chain closer to regional retrofit demand, helping airlines manage delivery bottlenecks and reduce reliance on long inbound logistics lanes for cabin interior shipsets.

- February 2024: Saudia contracted Collins Aerospace for new seat installations on its upcoming Boeing 787 fleet (with deliveries starting from early 2026) and for a retrofit program covering existing Airbus A330 and Boeing 777 fleets through late 2027. The multi-fleet scope expands Collins Aerospace's installed base for premium seating in the region and signals continued demand for both line-fit and retrofit seat capacity across widebody operations that connect into African routes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of aircraft passenger seats supplied for aircraft operated within Africa, including line-fit supply for deliveries and retrofit or replacement demand tied to cabin upgrades.

Scope exclusions: we exclude non-seat cabin interior items, such as galleys, lavatories, and in-flight entertainment systems, and we exclude non-aviation passenger seating.

Segmentation Overview

- By Aviation Type

- Commercial Aviation

- Widebody

- Narrowbody

- Regional Jets

- General Aviation

- Business Jets

- Commercial Helicopters

- Military Aviation

- Combat

- Transport

- Special Mission

- Helicopters

- Commercial Aviation

- By Seat Class

- First Class

- Business Class

- Premium Economy Class

- Economy Class

- By Fitment

- Linefit

- Retrofit

- By Seat Material

- Cushion Materials

- Structural Materials

- Upholsteries and Seat Covers

- By Country

- South Africa

- Egypt

- Ethiopia

- Nigeria

- Kenya

- Morocco

- Rest of Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and to put practical guardrails around the model before we finalized the numbers. We referred to public aviation indicators and traffic series from sources such as ICAO publications, IATA releases, World Bank air transport statistics, and airport or civil aviation authority updates from major African markets.

To connect flying activity to seating demand, we also reviewed aircraft delivery and fleet-in-service signals, plus safety and certification context from sources such as FAA and EASA publications. Trade statistics and customs releases were used where seat and seating-part categories could be observed at a high level. We used company filings, investor presentations, and reputed aviation press to understand cabin refresh timing and retrofit intensity. Select paid subscriptions covering company financials and patent intelligence were used only where they helped validate directionally important assumptions. The desk sources listed here are illustrative only, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm assumptions that are not consistently available in public datasets, especially retrofit cadence, cabin layout changes, and price movement by seat class. We spoke with a mix of aircraft operators, MRO and cabin retrofit participants, and component-side experts across Africa, so outliers from a single country or airline type would not distort the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 16% | |

| Mid tier: 56% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 52% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build, where the Africa-based fleet in service and planned deliveries are translated into seat-shipset needs by aircraft category, then adjusted for retrofit and replacement demand. We corroborate the totals with selective bottom-up approximations, such as sampled seats per aircraft combined with indicative price bands by cabin class, which helps us catch overstatement when mix assumptions drift.

A few inputs drive most of the model outcomes, so we kept them simple and traceable. These include deliveries and retirements, average seat count per airframe type, cabin class mix shifts (economy versus premium layouts), refurbishment timing that often aligns with heavier maintenance visits, and pricing direction linked to materials and certification-driven design updates. When country-level indicators were thin, we filled gaps using subregional fleet utilization and traffic growth as proxies, then rebalanced the output using expert feedback.

For forecasting, we used scenario analysis so the outlook can reflect faster or slower fleet renewal, uneven route recovery, and MRO capacity constraints. The final growth path was aligned to expert consensus on airline expansion plans and cabin upgrade timing, and then checked for year-to-year realism rather than only matching the end-year value.

Data Validation & Update Cycle

Model outputs were cross-checked against independent aviation signals, including fleet counts, delivery schedules, passenger traffic direction, and typical cabin upgrade cycles. If an assumption created a sharp step change that could not be explained by deliveries, maintenance cadence, or pricing movement, we reworked it and re-tested. We also ran a second analyst review before sign-off.

Reports are refreshed annually, and interim updates are made when material events occur, such as major aircraft orders, changes in fleet grounding status, or clear shifts in retrofit activity. Before delivery, an analyst completes a fresh pass so the shared numbers reflect the latest available data and the most recent validation calls.

Mordor Intelligence's Africa Aircraft Seating Market Sizing Compared With Other Published Estimates

Published market sizes for aircraft seating can differ even when the topic sounds the same, because the underlying geography and what gets counted as seating demand are not always consistent. Differences also show up when one estimate assumes aggressive fleet recovery, or when pricing is applied using a single average that ignores cabin mix and retrofit share.

The main gap comes from regional blending, where Mordor Intelligence keeps the value Africa-only and ties demand to local fleet activity plus retrofit timing, instead of scaling down a Middle East and Africa number that is influenced by Gulf widebody cabin spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 210.60 M (2025) | |

| Global Consultancy A | USD 450.00 M (2024) | Uses a Middle East and Africa total rather than Africa-only, and the base year differs, which shifts currency timing and the starting fleet and retrofit assumptions. |

| Trade Journal B | USD 710.00 M (2025) | Reports a Middle East and Africa regional value inside a global roll-up, so Africa can be overstated if cabin class mix and retrofit demand are applied using broad regional averages. |

Across the figures, the biggest driver is whether Africa is sized directly from its fleet and maintenance-led retrofit signals, or inferred from a wider region and then adjusted. Once scope and demand construction are kept consistent, the remaining differences usually come from cabin mix assumptions and how price movement is carried into the base year.

Key Questions Answered in the Report

What is the projected value of the Africa aircraft seating market by 2031?

The Africa aircraft seating market is forecasted to reach USD 290.58 million by 2031, reflecting a 5.51% CAGR from 2026.

Which seat class is expected to grow fastest in African fleets?

Business class is set to expand at 7.36% CAGR as carriers retrofit widebodies with lie-flat suites.

Why are retrofit programs gaining traction among African airlines?

Retrofits allow carriers to extend aircraft life and reduce fuel burn without large capital outlays, driving a 6.12% CAGR in retrofits through 2031.

How do import duties affect seating costs in Nigeria?

A combined 27.5% duty and VAT raise the landed price of a 150-seat narrowbody retrofit by around USD 124,000, lengthening payback periods.

Which country is forecasted to be the fastest-growing seat market?

Ethiopia leads with a 6.98% CAGR due to fleet expansion and duty-free import policies.

What materials are airlines adopting to reduce seat weight?

Carriers favor carbon-fiber seatbacks and titanium frames that cut weight to below 9 kilograms per economy seat, saving up to 1.5% in fuel use.

Page last updated on: