Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

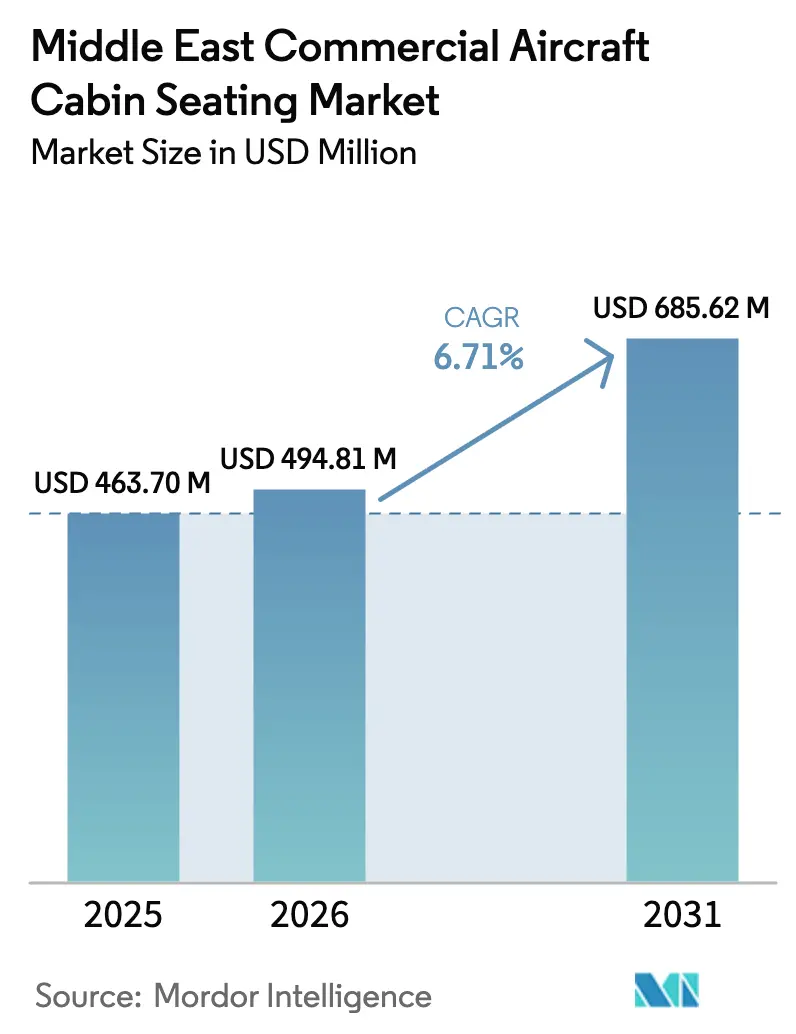

| Base Year Market Size (2025) | USD 463.70 Million |

| Market Size (2026) | USD 494.81 Million |

| Market Size (2031) | USD 685.62 Million |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

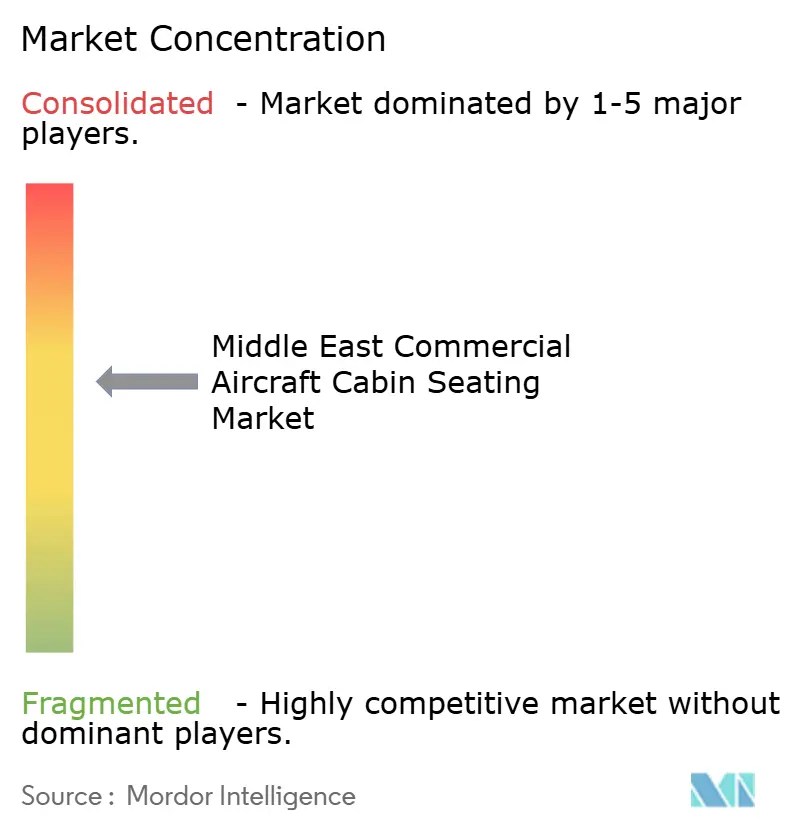

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Commercial Aircraft Cabin Seating Market Analysis by Mordor Intelligence

The Middle East commercial aircraft cabin seating market size is expected to grow from USD 463.70 million in 2025 to USD 494.81 million in 2026 and is forecast to reach USD 685.62 million by 2031 at 6.71% CAGR over 2026-2031. Government-funded airport expansions across Saudi Arabia and the United Arab Emirates, along with the rapid rise of low-cost carriers (LCCs), sustain high linefit demand, while widebody fleet renewal and retrofit programs channel incremental revenue for premium seating suppliers. Airlines intensify product differentiation through privacy-focused suites and premium economy cabins, and seat makers respond with lightweight composite structures that help carriers meet stringent fuel efficiency targets. Supply-chain vulnerabilities, particularly for foam and actuator components, lengthen delivery lead times and pressure airline capital expenditure schedules. Even so, the Middle East commercial aircraft cabin seating market benefits from the region’s hub status on intercontinental routes and resilient government support for tourism-led economic diversification, anchoring growth prospects beyond global aviation cycles.

Key Report Takeaways

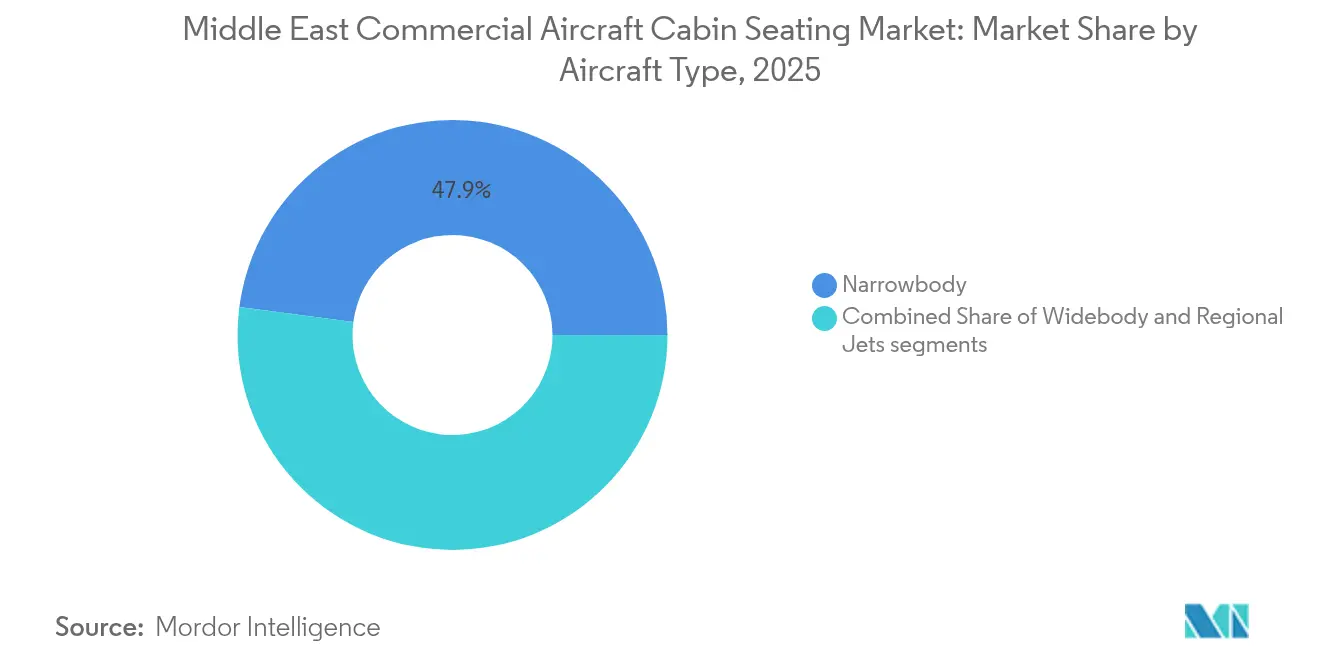

- By aircraft type, narrowbodies held 47.92% of the Middle East commercial aircraft cabin seating market share in 2025, and widebodies are projected to record the fastest CAGR at 7.28% to 2031.

- By cabin class, the economy accounted for a 54.63% share of the Middle East commercial aircraft cabin seating market in 2025, and the premium economy is forecasted to expand at an 8.05% CAGR through 2031.

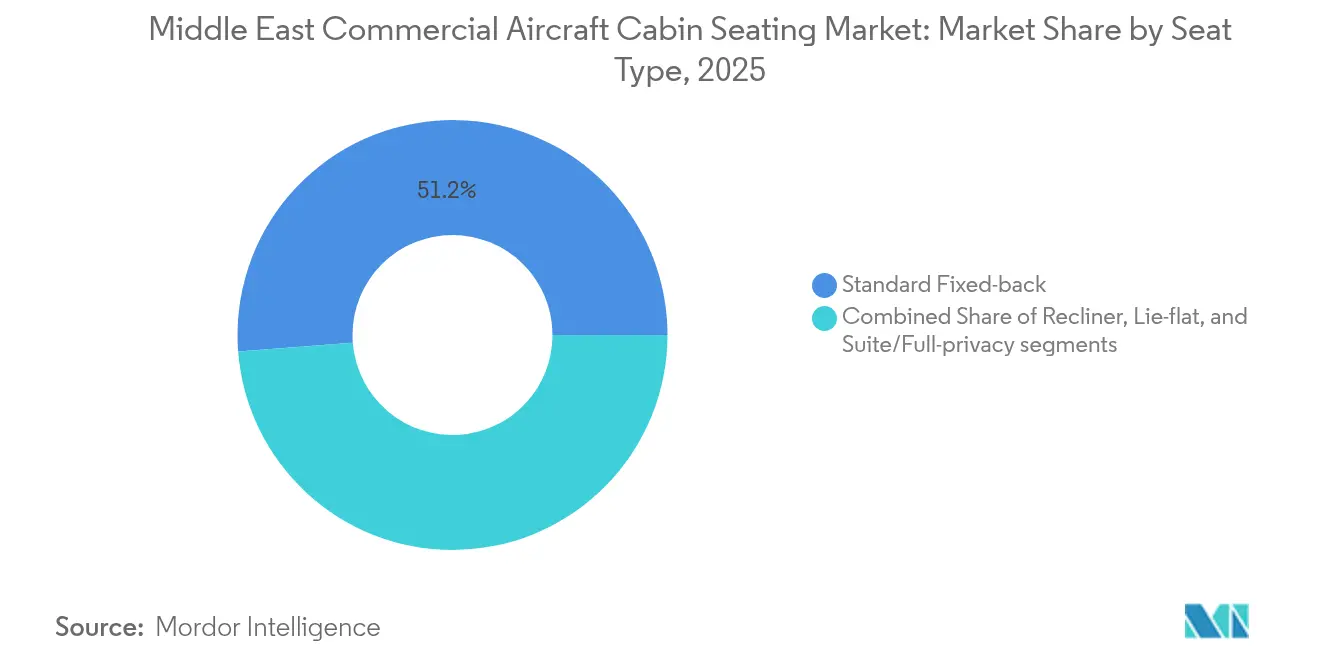

- By seat type, fixed-back designs captured a 51.22% share in 2025, whereas suite configurations are expected to grow at a 10.62% CAGR to 2031.

- By fit type, linefit installations accounted for 68.74% of 2025 revenues, while retrofits are expected to increase at a 8.84% CAGR.

- By geography, the United Arab Emirates is expected to account for 58.21% of the regional market share in 2025. In comparison, Saudi Arabia is projected to grow at a CAGR of 11.25%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Commercial Aircraft Cabin Seating Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of LCCs | +1.5% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Fleet renewal programs amid fuel-efficiency targets | +1.2% | Region-wide; strongest in UAE and Saudi Arabia | Long term (≥4 years) |

| Rising premium-economy retrofits | +0.8% | Gulf carriers; spillover to other Middle East markets | Short term (≤2 years) |

| Increase in the number of government-backed aviation hubs | +0.7% | UAE and Qatar | Long term (≥4 years) |

| Lightweight composite seat certification advances | +0.6% | Global suppliers serving Middle East carriers | Medium term (2-4 years) |

| OEM-seatmaker risk-sharing partnerships | +0.5% | Global; concentrated around major hub operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of LCCs

Budget airlines such as flynas, Air Arabia, and flydubai escalate fleet orders and favor 174-180-seat narrowbody layouts that maximize density, so volume demand for durable fixed-back economy units rises markedly.[1]flynas, “Fleet Expansion and Route Development Strategy,” FLYNAS.COM Seat makers that deliver modular platforms with quick-change cushions and integrated USB-C charging capture orders because carriers seek faster turnarounds and ancillary-revenue features. The government targets to link 250 overseas destinations by 2030 and amplify seat procurement pipelines, especially for high-frequency regional pairs.[2]General Authority of Civil Aviation, “Saudi Aviation Sector Growth Statistics,” GACA.GOV.SA Lightweight composite frames help carriers cut fuel burn while preserving seat-count economics, satisfying cost discipline in the low-fare model. As network breadth expands, airlines retrofit earlier deliveries to align cabin standards, generating follow-on aftermarket opportunities for certified suppliers.

Fleet Renewal Programs Amid Fuel-Efficiency Targets

Gulf carriers accelerate widebody refresh cycles to reach 15-20% fuel-burn improvements, and seating contracts bundle carbon-fiber structures with weight-optimized dress covers that shave kilograms per passenger.[3]Emirates, “Cabin Retrofit and Fleet Modernization Program,” EMIRATES.COM Emirates has earmarked USD 3 billion for cabin upgrades, including next-generation seats that integrate titanium seat legs and recycled-content plastics to meet sustainability pledges. EASA ETSO-C127c certification underpins supplier qualification, so incumbents with test-facility capacity hold an advantage. Network planners quantify fuel savings in kilogram-kilometer metrics. ROI thresholds favor weight reduction products and revenue upside through ancillary services such as Bluetooth-enabled in-seat ordering. New-build B787 and A350 deliveries thus embed premium-economy and suite installations from the outset, supporting steady linefit demand.

Rising Premium-Economy Retrofits

Premium economy generates 30-40% higher yield than standard economy, and Gulf carriers accelerate rollouts to monetize latent willingness to pay among corporate and VFR segments.[4]Qatar Airways, “Premium Economy and Fleet Expansion Plans,” QATARAIRWAYS.COM Retrofit lines in Dubai and Doha convert widebody cabins within sixteen-day groundings, swapping 3-3-3 economy blocks for 2-4-2 premium layouts with 38-42-inch pitch and calf-rest leg supports. Seat suppliers integrate seat-mounted amenity stowage, privacy wings, and enlarged meal-tray arms to elevate perceived value while limiting additional cabin weight. The Middle East commercial aircraft cabin seating market registers a surge in retrofit engineering services, including monument re-certification and LOPA updates, as airlines squeeze incremental revenue out of mid-life hulls. Response from loyalty programs is positive, boosting load factors on long-haul sectors and validating further rollouts.

Government-Backed Aviation Hubs

Mega-hub strategies rely on seamless passenger experience, so authorities direct capital toward premium seating products that reinforce brand perception.[5]Saudi Press Agency, “Saudi Arabia Announces $50 Billion Airport Infrastructure Investment,” SPA.GOV.SA Dubai’s USD 35 billion airport expansion raises peak departure banks, translating into more aircraft seat capacity requirements. Doha’s focus on high-yield connecting traffic prompts Qatar Airways to specify privacy-oriented suites on flagship routes, easing competitive pressure against Asian and European rivals. Government funding insulates carriers from short-term oil-price shocks, supporting sustained procurement cycles. For suppliers, proximity to free-zone logistics hubs reduces lead times for linefit shipsets, mitigating tax and customs frictions that affect other regions. Overall, hub-oriented policy guarantees predictable, multi-year seating demand across cabin classes.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery delays of aircraft programs | −0.9% | Global impact; acute in Middle East due to big orders | Short term (≤2 years) |

| Supply-chain bottlenecks in foam and actuators | −0.6% | Global manufacturing; regional installation delays | Medium term (2-4 years) |

| Volatile jet-fuel prices impacting capex | −0.7% | Region-wide | Short term (≤2 years) |

| Cabin-density regulations limiting seat-counts | −0.4% | Region-wide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Delivery Delays of Aircraft Programs

Extended lead-times at Boeing and Airbus shift narrowbody and widebody deliveries by 12-18 months, freezing scheduled seat-installation windows and deferring supplier revenue recognition. Middle East carriers with sizable order backlogs, Emirates, Qatar Airways, and Saudia, face downstream capacity gaps, compelling them to stretch utilization of older cabins or lease interim lift. Seat makers incur inventory-holding costs for partially completed shipsets awaiting airframe availability, increasing working-capital requirements and dampening margin profiles. Airlines mitigate disruption by accelerating retrofit programs, but retrofit slots compete with heavy-maintenance visits, straining MRO capacity. The logjam tempers near-term growth yet sets up a delivery bulge in 2027-2028 that could test supplier throughput limits.

Supply-Chain Bottlenecks in Foam and Actuators

Regulatory-grade polyurethane foam faces raw-material shortages linked to chemical-safety restrictions, and semiconductor scarcity delays electromechanical actuator shipments, extending component lead-times to 20 weeks. Seat OEMs either use dual-source materials, trigger fresh certification cycles, or redesign products to fit available substitutes, inflating non-recurring engineering expenses. Airlines encounter higher unit prices and limited spec flexibility, sometimes accepting lower-feature seat builds to avoid aircraft-on-ground scenarios. In response, Collins Aerospace and Safran expand vertical integration into foam and motion-control sub-assemblies, though ramp-up requires capex and workforce training. Persistent shortages modestly suppress the Middle East commercial aircraft cabin seating market CAGR until global semiconductor capacity catches up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Widebody Growth Outpaces Narrowbody Volume

The widebody slice of the Middle East commercial aircraft cabin seating market posted a 7.28% forecast CAGR, outstripping narrowbody volume even though narrowbodies retained 47.92% market share in 2025. Widebody demand aligns with Gulf carriers’ long-haul strategies and premium-cabin differentiation, notably their A350 and B787 fleets, which feature next-generation suites and self-contained suites. Narrowbody momentum rests on short-haul frequency and LCC expansion; contract awards for A320neo and B737 MAX programs fill fixed-back economy pipelines at Safran and RECARO. Regional jets remain a niche market but serve point-to-point links, unable to sustain larger aircraft.

Fleet planners justify widebody retrofit budgets because each upgraded seat unlocks fare premiums that are multiple times higher than those of narrowbody aircraft, or, at the same time, 1-2% weight savings translate into sizable kerosene cost offsets on ultra-long segments. Conversely, narrowbody rnarrowbodycus on slimline economy refreshes, integrated power, and cabin lighting harmonization that boost ancillary revenue. EASA and GACA alignment on certification streamlines supplier ship-sets across aircraft categories, reinforcing cross-program commonality strategies.

By Cabin Class: Premium Economy Drives Revenue Optimization

Economy seating still dominates value because it fills the majority of cabin real estate, capturing 54.63% of the Middle East commercial aircraft cabin seating market share in 2025. Airlines apply slimline designs with 28-31-inch pitch to sustain breakeven load factors on price-sensitive routes. Yet premium-economy growth at 8.05% CAGR underpins revenue mix shifts, as carriers slot 24-40 seats per widebody to capture higher yields without the service complexity of lie-flat business beds.

Premium-economy furniture features recliner-type mechanisms, wider armrests, and adjustable calf rests, yet weighs only marginally more than base economy units due to composite sidewalls and magnesium hard goods. Fleet retrofits drive the Middle East commercial aircraft cabin seating market size for premium economy at Emirates, Etihad, and Saudia. Business-class seating upholds brand stature on flagship routes but delivers steadier, not hyper-growth, volumes. First-class installations are typically boutique, featuring six to eight suites per aircraft; they nonetheless drive high-margin engineering services and sensor-enabled seat controls.

By Seat Type: Suite Configurations Lead Innovation

Fixed-back economy units held a 51.22% share in 2025, yet suite-style seats registered the highest trajectory at 10.62% CAGR, reflecting Gulf carriers’ pursuit of exclusivity on long-haul corridors. Suite designs now feature floor-to-ceiling privacy doors, 32-inch video screens, and VR-enabled window displays, redefining the top of the product pyramid. Recliner seats support premium-economy footprints, optimizing comfort within conventional seat tracks. Meanwhile, lie-flat business products are evolving to herringbone layouts with increased aisle access and shoulder space, striking a balance between density and comfort.

R&D centers in Toulouse, Hamburg, and Dubai iterate composite shell geometries that compress weight without sacrificing stiffness. Suppliers equip suites with integrated wireless charging, OLED mood lighting, and predictive maintenance sensors that transmit usage data via aircraft-health monitoring systems. The Middle East commercial aircraft cabin seating market size for suite and privacy products is expected to grow from USD 50 million in 2025 to USD 91.6 million in 2031, driven by multi-shipset retrofit contracts across Emirates’ B777 fleet.

By Fit Type: Retrofit Acceleration Drives Aftermarket Growth

Linefit dominated with a 68.74% share in 2025 because every new aircraft requires certified seating at delivery, and OEM-approved seat catalogues reduce airline engineering workload. However, retrofit CAGR of 8.84% outpaces baseline growth as carriers bridge delayed deliveries and refresh complex products ahead of global events such as Expo 2030 Riyadh. Airlines gauge retrofit ROI through fare-premium premiums and maintenance downtime trade-offs; modular seat kits and plug-and-play IFE harnesses cut aircraft-on-ground time to fewer than 18 days.

Collins Aerospace’s retrofit partnership with Saudia exemplifies the trend, covering economy slimline replacements and business-class lie-flat upgrades bundled with lavatory refurbishments. Retrofit providers bundle STC engineering, parts kitting, and on-site installation supervision, generating service pull-through beyond the initial seat sale. The Middle East commercial aircraft cabin seating market share for retrofit work is poised to edge above 35% by 2031 as backlogs unwind and OEM deliveries stabilize.

Geography Analysis

The United Arab Emirates anchors the Middle East commercial aircraft cabin seating market through Emirates and Etihad, which operated more than 300 aircraft in 2025 and holds expansive retrofit and linefit pipelines. Dubai International’s USD 35 billion infrastructure program reinforces fleet growth, funneling demand toward premium suite and lie-flat products that align with brand standards. Suppliers establish regional distribution hubs in the Dubai South Free Zone, mitigating customs frictions and enabling rapid spares delivery to MRO partners.

Saudi Arabia is the fastest-growing seat market, underwritten by a USD 50 billion airport expansion plan and Vision 2030 targets for 330 million passengers annually. Flynas’ narrowbody orderbook anchors bulk economy-seat volume, while Saudia’s widebody retrofits introduce premium economy cabins along religious tourism trunk routes. Riyadh’s new King Salman International Airport amplifies future linefit seating demand, and localized airworthiness oversight, harmonized with EASA, accelerates certification cycles for seat suppliers.

Qatar retains an outsized influence relative to its population because Qatar Airways deploys a young widebody fleet with high suite density, driving continuous development of privacy-oriented business products. The carrier’s forthcoming B777-9 introduction will set new benchmarks for first-class suites featuring floor-to-ceiling doors and smart-glass panels. Israel and smaller Gulf states add supplemental growth through flag-carrier modernization and regional tourism programs, favoring cost-effective slimline seating with integrated power and tablet holders. Across the region, free-trade zones and tax concessions encourage global suppliers to establish regional stocking positions, improving time-to-market metrics and reinforcing customer proximity.

Government policy across the Middle East mandates adherence to ICAO Annex 8 and EASA safety norms, ensuring uniform seat-certification protocols. Harmonized regulatory environments reduce non-recurring engineering costs for suppliers and streamline airline procurement cycles. Collectively, these geographic factors position the Middle East commercial aircraft cabin seating market as resilient to global economic swings, sustaining compounded growth through 2030.

Competitive Landscape

Safran, Collins Aerospace, and RECARO command the most extensive installed base, leveraging multi-year catalog positions at Airbus and Boeing to secure recurring line-fit volumes. Safran’s Z200 slimline platform underpins flynas’ A320neo deliveries, integrating smart cushions and USB-C power to meet the needs of an LCC. Collins Aerospace differentiates itself through full-service retrofit packages that combine seat, galley, and lavatory upgrades, as evidenced by Saudia’s cabin overhaul schedule. RECARO focuses on weight-optimized economy and premium economy products, utilizing titanium cross-beams and composite seatbacks.

Emerging players like Geven, ZIM, and Thompson Aero Seating carve out a share in the premium economy and business segments by offering flexible customization around seat track footprints. Technological white spaces include sensor-enabled seat health monitoring, biocidal upholstery fabrics, and additive-manufactured seat parts that enable rapid spare replacement. Certification expertise remains a barrier; incumbent suppliers operate in-house dynamic-test sleds and flammability labs that accelerate ETSO approvals. The competitive arena thus exhibits moderate concentration, with long-term airline relationships and regulatory capital requirements limiting fragmentation.

New entrants are pursuing niche opportunities in lightweight foam chemistry and integrated wireless charging; however, scale challenges persist due to recurring qualification costs. M&A continues as a route to capability acquisition, as ZIM’s purchase of HAECO Cabin Solutions broadens product reach from economy to business class. Over the forecast horizon, competitive intensity will hinge on supply-chain resilience; firms that control upstream materials and actuator production are likely to improve their market position.

Middle East Commercial Aircraft Cabin Seating Industry Leaders

Elevate Aircraft Seating LLC

Expliseat S.A.S.

Safran SA

Collins Aerospace (RTX Corporation)

RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: flynas signed a memorandum of understanding (MoU) with Safran to equip 60 A320neo aircraft with Z200 economy seats featuring smart cushions, device holders, and power-supply ports.

- April 2025: Thompson Aero Seating secured a contract with Thai Airways for 32 shipsets of Vantage business-class seats for A321neo deliveries scheduled in late 2025.

- April 2025: Geven announced economy and premium-class seat contracts with Turkish Airlines and Frontier Airlines, leveraging Essenza SE and the Comoda platform.

- October 2024: RECARO Aircraft Seating hosted its 13th Global Supplier Day, spotlighting recycled-content material initiatives.

Middle East Commercial Aircraft Cabin Seating Market Report Scope

By Aircraft Type

| Narrowbody |

| Widebody |

| Regional Jet |

By Cabin Class

| Economy |

| Premium Economy |

| Business |

| First |

By Seat Type

| Standard Fixed-back |

| Recliner |

| Lie-flat |

| Suite/Full-privacy |

By Fit Type

| Line-fit |

| Retrofit |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Israel |

| Rest of Middle East |

| By Aircraft Type | Narrowbody |

| Widebody | |

| Regional Jet | |

| By Cabin Class | Economy |

| Premium Economy | |

| Business | |

| First | |

| By Seat Type | Standard Fixed-back |

| Recliner | |

| Lie-flat | |

| Suite/Full-privacy | |

| By Fit Type | Line-fit |

| Retrofit | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Israel | |

| Rest of Middle East |

Market Definition

- Product Type - The seats that are integrated into the passenger aircraft and which are made up of a different combination of materials are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms