Cosmetic Shea Butter Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

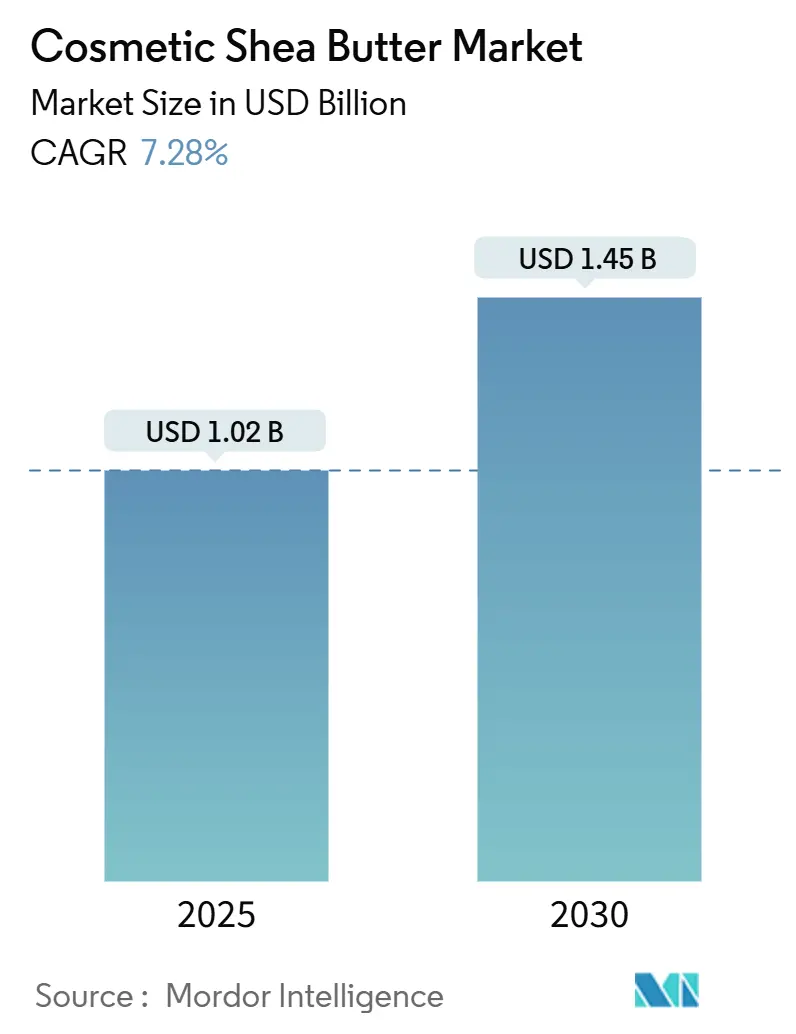

| Market Size (2025) | USD 1.02 Billion |

| Market Size (2030) | USD 1.45 Billion |

| Growth Rate (2025 - 2030) | 7.28% CAGR |

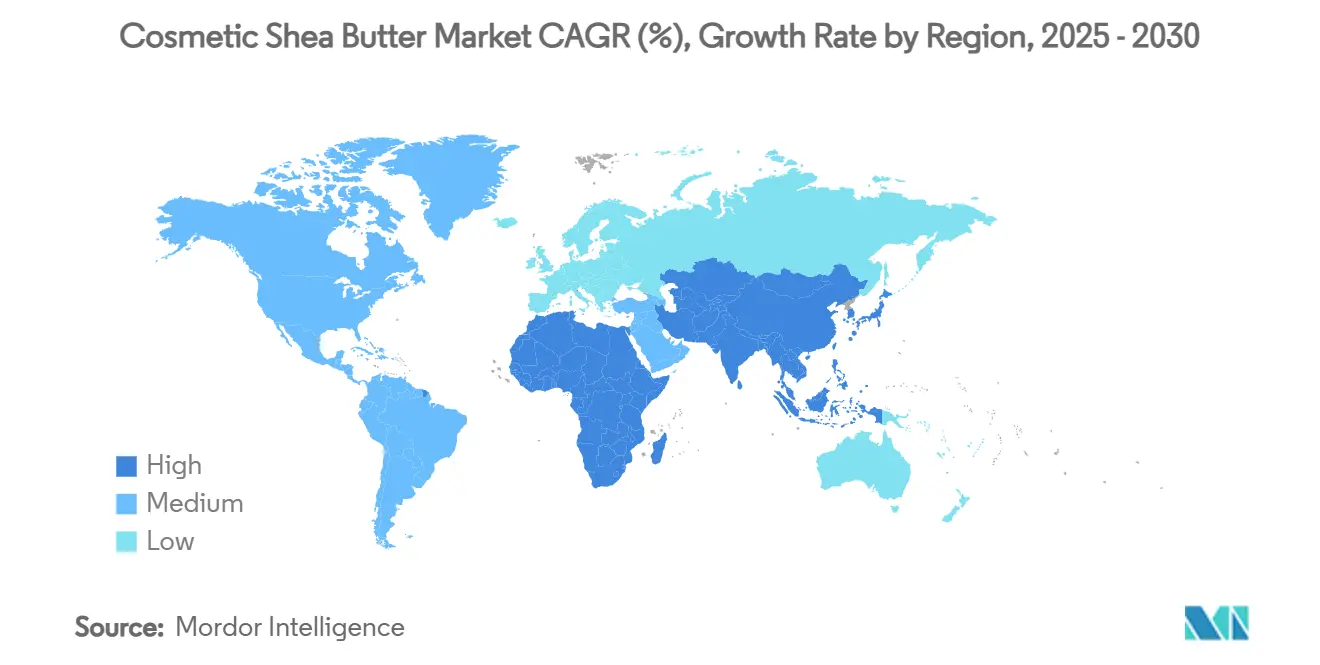

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic Shea Butter Market Analysis by Mordor Intelligence

The global cosmetic shea butter market size, valued at USD 1.02 billion in 2025, is expected to reach USD 1.45 billion by 2030, growing at a CAGR of 7.28% during the forecast period. The market demonstrates robust growth as consumers increasingly prioritize natural and sustainable beauty solutions, positioning shea butter as a fundamental ingredient in premium skincare formulations. This shift in consumer behavior aligns with the broader clean beauty movement, where manufacturers are responding to demands for transparent, environmentally responsible products. The market's development is further strengthened by supportive regulatory frameworks that encourage the use of natural ingredients, while technological advancements in extraction methods ensure the preservation of vital bioactive compounds necessary for effective cosmetic applications. These factors collectively create a favorable environment for market expansion, particularly as beauty brands continue to innovate and develop new product lines incorporating shea butter.

Key Report Takeaways

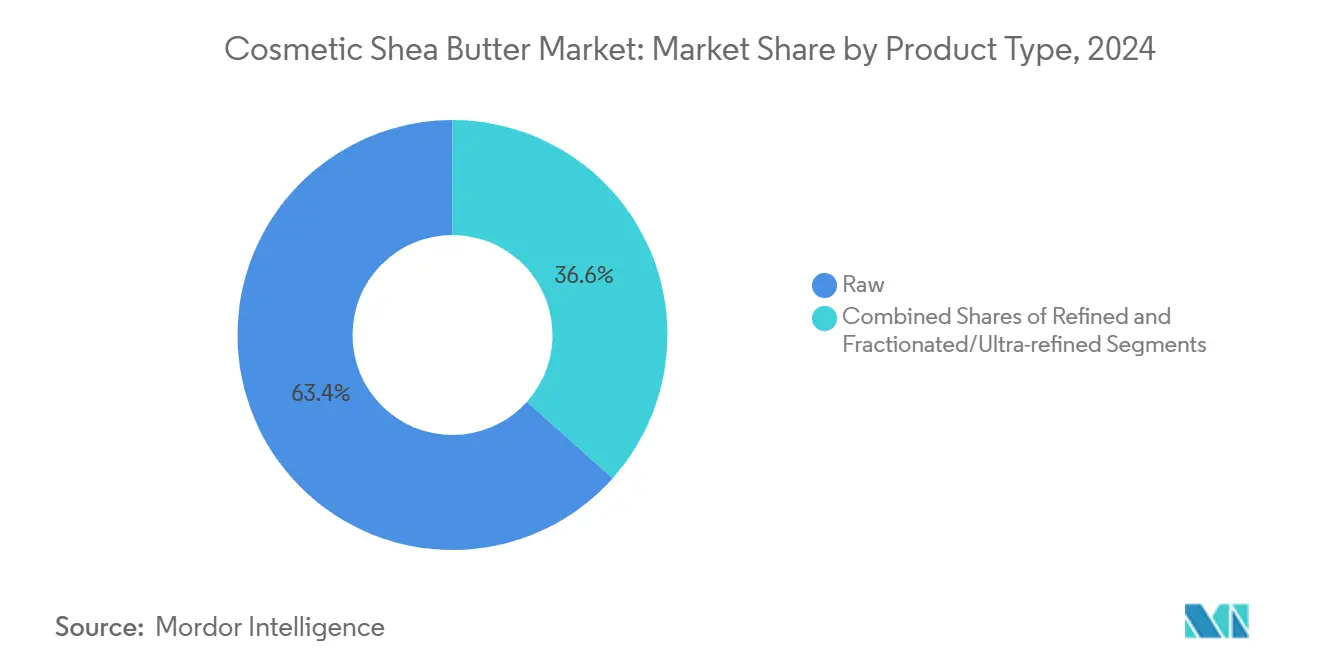

- By product type, raw shea butter led with 63.39% revenue share in 2024, whereas fractionated and ultra-refined grades are projected to expand at an 8.43% CAGR through 2030.

- By nature, conventional variants accounted for 66.13% of 2024 demand, while organic shea butter is poised to grow at an 8.52% CAGR between 2025 and 2030, driven by premium positioning in North America and Europe.

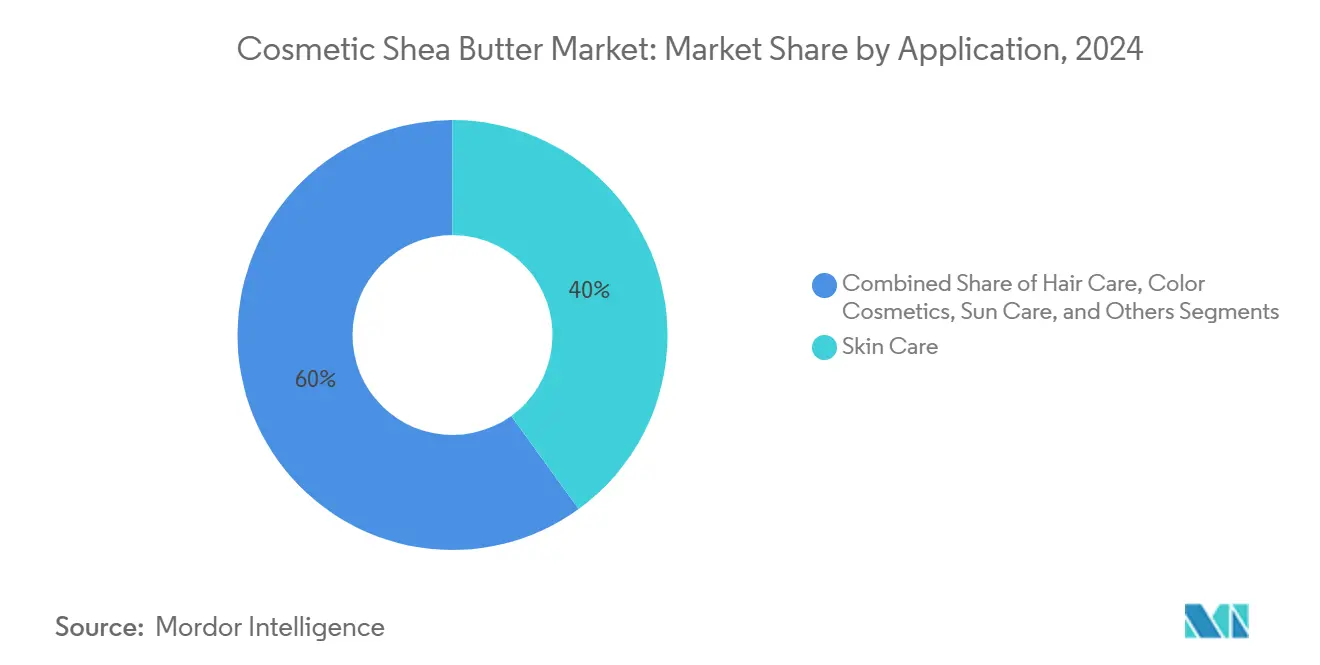

- By application, skincare dominated with 40.01% share in 2024, yet sun-care products are forecast to register an 8.43% CAGR to 2030, reflecting consumer interest in natural UV shields across Asia-Pacific and Latin America.

- By geography, Europe captured 35.92% of 2024 revenue, whereas the Asia-Pacific region is projected to achieve an 8.84% CAGR over the same period

Global Cosmetic Shea Butter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for natural and organic personal care products | +1.8% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Growing popularity of vegan and cruelty-free cosmetic formulations | +1.2% | Global, led by Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Expansion of "clean beauty" and sustainable cosmetics movements | +1.5% | Global, with premium segments in developed markets | Long term (≥ 4 years) |

| Popularity of anti-aging products, with shea butter | +1.1% | Global, with highest penetration in North America and Europe | Short term (≤ 2 years) |

| Advancements in extraction and refining technologies | +0.9% | Global, with technology centers in Europe and emerging applications in Africa | Long term (≥ 4 years) |

| Positive regulatory stance on natural skin care ingredients | +0.8% | North America & EU, with spillover effects globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Natural and Organic Personal Care Products

The growing consumer preference for natural ingredients has transformed cosmetic formulation strategies, with shea butter emerging as a key botanical ingredient that offers both effectiveness and sustainability. The European market recorded shea butter imports worth EUR 95 million in 2023, with France, Germany, and the UK being the primary importers [1]Source: CBI, “Demand for Natural Ingredients for Cosmetics in Europe,” cbi.eu. This increase in demand reflects consumers' heightened awareness of ingredient transparency, as shea butter's historical use in African skincare traditions provides authenticity compared to synthetic alternatives. The trend has expanded beyond premium products into mass-market segments, as mainstream brands incorporate shea butter to address consumer demand for natural formulations. The Swedish cosmetics market, which reached EUR 2 billion in 2020, exemplifies this shift, with 70% of consumers prioritizing ecolabels, generating consistent demand for certified natural ingredients [2]Source: Open Trade Gate Sweden, “The Swedish Market,” kommerskollegium.se.

Growing Popularity of Vegan and Cruelty-Free Cosmetic Formulations

Shea butter has emerged as a fundamental ingredient in ethical cosmetic formulations, driven by increasing consumer demand for plant-based and sustainably sourced beauty products. The ingredient's natural origins and responsible harvesting practices resonate strongly with environmentally conscious consumers in the global beauty market. Major industry player NIVEA has responded to this market shift by integrating shea butter into its comprehensive sustainability framework, setting an ambitious target to achieve 100% sustainable sourcing of renewable ingredients by 2025. Through its partnership with the Global Shea Alliance, NIVEA actively supports 10,000 female shea collectors, demonstrating its commitment to responsible sourcing practices. This emphasis on ethical ingredient procurement serves as a key market differentiator, particularly as consumer purchasing decisions increasingly favor products with vegan certification. Beiersdorf's strategic investment in shea butter sustainability has yielded tangible results, including the successful planting of 20,400 new shea trees and significant improvements in the economic conditions of women in rural collection communities. This approach effectively illustrates how companies can align ingredient sourcing strategies with both commercial objectives and social responsibility goals, creating value across the entire supply chain.

Expansion of "Clean Beauty" and Sustainable Cosmetics Movements

Shea butter has established itself as a fundamental ingredient in clean beauty products, driven by its proven safety record and commitment to environmental sustainability. The Expert Panel for Cosmetic Ingredient Safety's recent assessment validates the safety of shea-derived ingredients when properly formulated to prevent sensitization. The assessment confirms shea butter's widespread adoption across various cosmetic applications, particularly in moisturizing products where it can be used in its pure form. The ingredient's effectiveness is attributed to its natural composition of triterpene esters, delivering both anti-inflammatory and antimicrobial properties to cosmetic formulations. Contemporary fractionation methods have revolutionized shea butter processing, substantially reducing production timeframes while maintaining product integrity and improving environmental performance. As the clean beauty movement continues to prioritize transparency, manufacturers are increasingly seeking traceable shea butter sources, fostering direct relationships with African farming communities to strengthen supply chain integrity and demonstrate social responsibility.

Popularity of Anti-Aging Products, with Shea Butter

Scientific validation of shea butter's anti-aging properties has driven its incorporation into premium skincare products, particularly appealing to mature consumers with substantial disposable income. Research demonstrates that specific compounds extracted from shea fat, particularly triterpene cinnamates and acetates, show significant benefits in reducing inflammation and preventing adverse skin conditions. The unsaponifiable portion of shea butter contains essential bioactive compounds, including cinnamic acid esters, vitamins A and E, and polyphenols, which work together to protect the skin from environmental damage and oxidative stress. Modern enzymatic extraction methods have revolutionized the production process, allowing manufacturers to produce high-quality shea butter while maintaining its beneficial properties. The expanding anti-aging market segment benefits from shea butter's proven effectiveness in supporting natural collagen production and reinforcing the skin's protective barrier. Clinical research has established that shea butter effectively increases the body's natural antioxidant levels and provides substantial protection against sun-related skin damage, making it a versatile ingredient that comprehensively addresses various aging concerns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain vulnerabilities | -1.4% | West Africa production regions, global supply chains | Short term (≤ 2 years) |

| Complex and lengthy certification for organic or fair-trade status | -0.8% | Global, with highest impact in premium market segments | Medium term (2-4 years) |

| Challenges in maintaining freshness and bioactive content | -0.6% | Global, with particular impact on long-distance trade | Short term (≤ 2 years) |

| Stringent cosmetic regulatory requirements | -0.5% | North America & EU, with emerging impacts in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities

The West African shea industry faces significant supply chain challenges that affect global cosmetic manufacturers, impacting both local communities and international businesses. The region's variable climate patterns and limited infrastructure create substantial difficulties in maintaining consistent product quality and meeting delivery commitments. In Northern Ghana, numerous women rely on shea butter production as their primary source of income, employing traditional processing methods that result in quality variations across batches, creating challenges for cosmetic manufacturers' standardization efforts. The supply chain operations are particularly constrained by the remote locations of collection areas and inadequate transportation networks, especially during seasonal changes that restrict access to processing facilities and export markets. The shea tree's extensive maturation period before fruit production poses challenges for long-term supply planning and investment decisions. The declining shea tree population, driven by agricultural expansion and increased farm mechanization, further compounds these industry challenges [3]Source: Merian Institute for Advanced Studies in Africa, “Shea Parklands Face Various Threats,” hypotheses.org. Potential solutions include implementing energy-efficient processing methods and utilizing shea butter by-products as alternative fuel sources to reduce environmental impact. However, these improvements require substantial infrastructure investment and comprehensive technology transfer programs to effectively support and empower local producer communities while ensuring sustainable industry growth.

Complex and Lengthy Certification for Organic or Fair-Trade Status

The organic and fair-trade certification processes for shea butter require extensive validation procedures and involve multiple stakeholders, creating significant barriers for producer communities seeking market entry and premium positioning. Ghana's shea sector faces challenges due to uncoordinated institutional structures, where organizations often prioritize individual interests over collective sector benefits, hindering certification efforts. Research in Ghana's Tamale Metropolis shows that organic shea butter processors earn higher household incomes (GHC 4,192.037) compared to conventional processors (GHC 1,527.883). However, obtaining organic certification requires significant investments in training, documentation, and compliance systems. The certification process spans 18-24 months and includes multiple stages: supply chain traceability, environmental impact assessments, and social compliance verification, each requiring thorough documentation and third-party validation. Fair trade certification further complicates the process by mandating community development programs, price premiums, and democratic decision-making structures, which often conflict with traditional hierarchical systems in producer communities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Raw Dominance Drives Volume Growth

Raw shea butter dominates the market with a substantial 63.39% share in 2024, establishing itself as a fundamental ingredient in the cosmetics industry. This significant market presence is attributed to its versatility in various cosmetic applications and its appeal to manufacturers seeking natural ingredient integration without substantial processing investments. Raw shea butter's market leadership is further strengthened by its ability to retain essential bioactive compounds, while traditional extraction methods continue to produce high-quality ingredients that align with clean beauty formulation requirements.

Refined shea butter occupies a distinct market segment, primarily serving specialized applications that demand specific melting points and extended shelf life characteristics. The market dynamics are evolving with fractionated and ultra-refined variants emerging as the fastest-growing segment, demonstrating an 8.43% CAGR through 2030. This growth is primarily fueled by the increasing demand from premium cosmetic formulations that require precise functional properties, reflecting the industry's shift toward more sophisticated product offerings.

By Nature: Organic Certification Drives Premium Positioning

Conventional shea butter maintains its dominant position with a 66.13% market share in 2024, benefiting from well-established supply chains and competitive pricing structures. The organic segment demonstrates robust growth potential with an anticipated CAGR of 8.52% through 2030, as consumers increasingly demonstrate their readiness to invest in certified sustainable ingredients. The organic segment's expansion is fundamentally driven by growing consumer understanding of the environmental footprint and social implications associated with cosmetic ingredient sourcing, with organic certification serving as a trusted third-party validation of sustainability practices.

Conventional shea butter continues to thrive through optimized procurement processes and lower compliance requirements, enabling manufacturers to maintain competitive pricing for mass-market cosmetic applications. In contrast, organic shea butter production demands a more rigorous approach, encompassing comprehensive supply chain management protocols, including regular soil testing, strict adherence to pesticide-free cultivation practices, and extensive documentation requirements. While these requirements create significant barriers to market entry, they enable producers to command substantial price premiums in developed markets. The IFOAM report examining organic trade opportunities in Africa provides detailed market analysis for strengthening organic shea trade, presenting strategic recommendations for stakeholder engagement to enhance market integrity and foster sustainable growth.

By Application: Skincare Leadership with Sun Care Acceleration

The skincare segment maintains a commanding 40.01% market share in 2024, demonstrating the widespread adoption of shea butter in the industry. This dominance is attributed to shea butter's well-documented moisturizing and anti-inflammatory properties, which effectively address a broad spectrum of skin concerns, from basic hydration needs to advanced anti-aging treatments. The segment's strong position reflects shea butter's exceptional versatility in product formulations, enabling manufacturers to incorporate it into various products, from basic moisturizers to sophisticated serums and targeted treatment solutions.

Hair care represents a substantial secondary application in the market, where manufacturers harness shea butter's natural conditioning and UV-protective properties for both leave-in and rinse-out product formulations. In the color cosmetics segment, producers utilize shea butter's emollient and preservation characteristics to enhance product performance and stability. The sun care segment has emerged as the most dynamic growth area, recording an impressive 8.43% CAGR through 2030, primarily due to increasing consumer awareness and appreciation of shea butter's inherent UV-protective capabilities.

Geography Analysis

Europe continues to dominate the global shea butter market with a commanding 35.92% market share in 2024. The region's market strength builds upon its robust cosmetics manufacturing base, stringent quality control protocols, and environmentally conscious consumers who prioritize ethically sourced natural ingredients. France remains the primary European importer of shea butter and natural ingredients from developing nations, with Germany and the UK maintaining strong import volumes. These markets adhere to strict EU Cosmetics Regulation standards, ensuring product quality and traceability throughout the supply chain. European buyers consistently demonstrate their commitment to transparency, rewarding organic and fair-trade certifications with premium pricing. The regulatory framework, including REACH compliance and limitations on synthetic ingredients, naturally favors ingredients like shea butter, while the European Green Deal further strengthens market demand through its sustainable sourcing requirements.

Asia-Pacific demonstrates exceptional market momentum, achieving an 8.84% CAGR through 2030. This growth stems from significant shifts in consumer behavior, with an expanding middle class showing increased interest in premium beauty products and natural ingredients. The region's diverse markets exhibit growing sophistication in their approach to personal care, embracing the benefits of natural cosmetic ingredients. The Global Shea Alliance actively facilitates direct partnerships between Asia-Pacific cosmetic manufacturers and African producers, enhancing regional trade dynamics while supporting producer communities and ensuring sustainable supply chains.

North America maintains its position as a stable market with established demand patterns for natural and organic cosmetic ingredients. The region's informed consumer base values ingredient safety and environmental responsibility, characteristics that align perfectly with shea butter's natural profile. The implementation of the FDA's Modernization of Cosmetics Regulation Act creates a regulatory environment that benefits established ingredients like shea butter, which has demonstrated safety for cosmetic use at concentrations up to 100%. This combination of regulatory support and educated consumer preferences ensures North America's continued importance in the global shea butter market.

Competitive Landscape

The cosmetic shea butter market demonstrates moderate fragmentation, creating a dynamic environment where both multinational corporations and specialized processors can establish their market presence. Market leaders including AAK AB, Bunge Global SA, and Cargill Incorporated have built strong competitive positions through comprehensive vertical integration and advanced processing capabilities. In contrast, companies like Olvea Group and Vantage Specialty Ingredients have found success by focusing on specialized applications and premium market segments. This diverse market structure accommodates various product requirements, ranging from mass-market moisturizers to sophisticated anti-aging formulations, with each segment demanding specific quality parameters and supply chain solutions.

Companies in the market are increasingly distinguishing themselves through robust sustainability programs and direct relationships with producers. These initiatives include substantial investments in community development programs and certification systems to secure premium market positioning. A notable example is Bunge's implementation of a significant public-private partnership in Ghana, which provides support to more than 2,500 women through the Women Shea Business Cooperative project. This initiative, funded by the German Federal Ministry for Economic Cooperation and Development, demonstrates how strategic supply chain investments can simultaneously strengthen market position and deliver meaningful social impact. The adoption of advanced technology in processing and quality control has emerged as a crucial differentiator, with companies making substantial investments in sophisticated extraction methods, fractionation capabilities, and comprehensive analytical systems to ensure consistent product quality and regulatory compliance. The Expert Panel for Cosmetic Ingredient Safety's thorough evaluation of 13 shea-derived ingredients has established clear regulatory guidelines, benefiting established companies while creating significant barriers for smaller operators with limited technical resources.

The market presents several untapped opportunities, particularly in specialized applications such as sun care formulations, where the natural UV protection properties of shea butter remain underutilized. Additionally, emerging markets offer significant potential for growth, especially in developing local processing capabilities that could enhance value retention within producing regions. These opportunities represent promising areas for market expansion and innovation, allowing companies to capture new value streams while addressing evolving consumer needs.

Cosmetic Shea Butter Industry Leaders

AAK AB

Cargill Incorporated

Olvea Group

Vantage Specialty Ingredients

Bunge Global SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: A new shea processing facility was launched in Ilesha Baruba, Kwara State, by the Initiative for Gender Empowerment and Creativity (IGEC) with support from Estée Lauder Emerging Leaders and Vital Voices Global Partnership The facility aims to empower rural women and youth while boosting high-quality shea butter production for the global cosmetic market

- June 2025: The Global Shea Alliance (GSA), eos Products (Evolution of Smooth), and Water for West Africa launched a strategic partnership to empower women shea processors in Ghana and Côte d’Ivoire. This initiative focuses on improving processing capacity, product quality, clean water access, and sustainable livelihoods to support the global cosmetic shea butter market.

- December 2024: A new shea butter fractionation technology was developed and implemented by Ugandan researchers led by Francis Omujal at the Natural Chemotherapeutics Research Institute. This innovation enhances shea butter quality and output, producing high-value products for cosmetics and personal care while increasing efficiency and reducing energy consumption.

Global Cosmetic Shea Butter Market Report Scope

| Raw |

| Refined |

| Fractionated/Ultra-refined |

| Organic |

| Conventional |

| Skin Care |

| Hair Care |

| Color Cosmetics |

| Sun Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Raw | |

| Refined | ||

| Fractionated/Ultra-refined | ||

| By Nature | Organic | |

| Conventional | ||

| By Application | Skin Care | |

| Hair Care | ||

| Color Cosmetics | ||

| Sun Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global value of cosmetic shea butter in 2025?

The segment stands at USD 1.02 billion in 2025 and is projected to reach USD 1.45 billion by 2030.

Which geography shows the fastest growth for cosmetic shea butter?

Asia-Pacific leads expansion with an 8.84% CAGR forecast for 2025-2030, reflecting rising middle-class demand and digital beauty retail.

Why are premium brands shifting toward organic shea butter?

Certified organic supply commands clear price premiums and aligns with clean-beauty and ESG mandates, helping brands differentiate while meeting strict sourcing standards.

What is driving the rise of shea butter in sun-care formulations?

Shea butter’s naturally occurring cinnamic acid esters provide gentle UV protection, enabling hybrid moisturizers and sticks to claim both hydration and SPF benefits.

What certification hurdles do cooperatives face?

Organic and fair-trade labels require 18–24 months of audits, traceability records, and social-impact programs, creating high upfront costs but unlocking premium pricing once achieved.

Page last updated on: