Murumuru Butter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

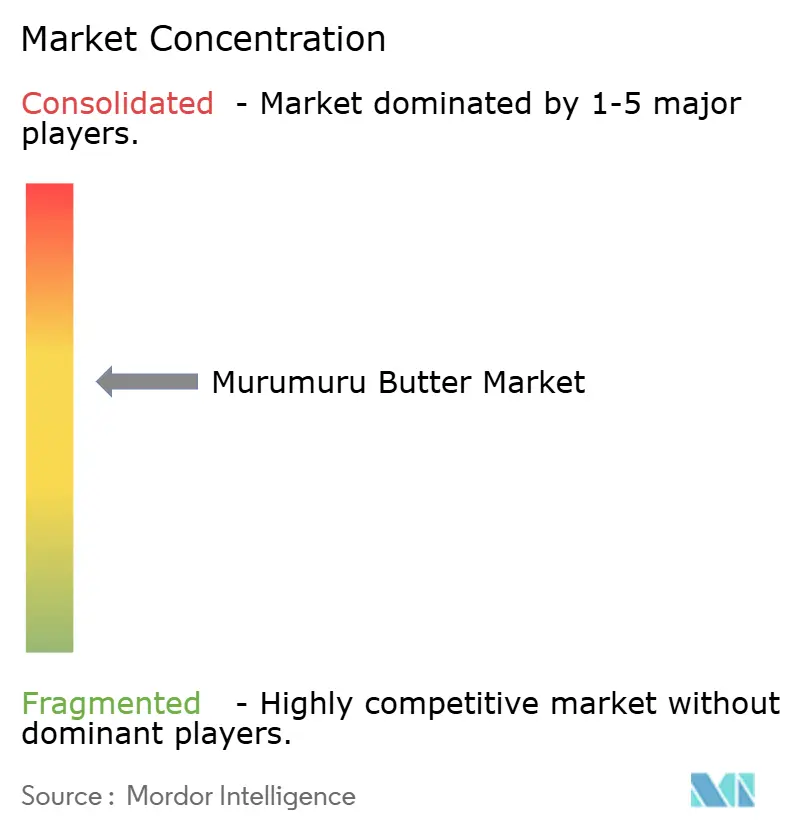

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Murumuru Butter Market Analysis by Mordor Intelligence

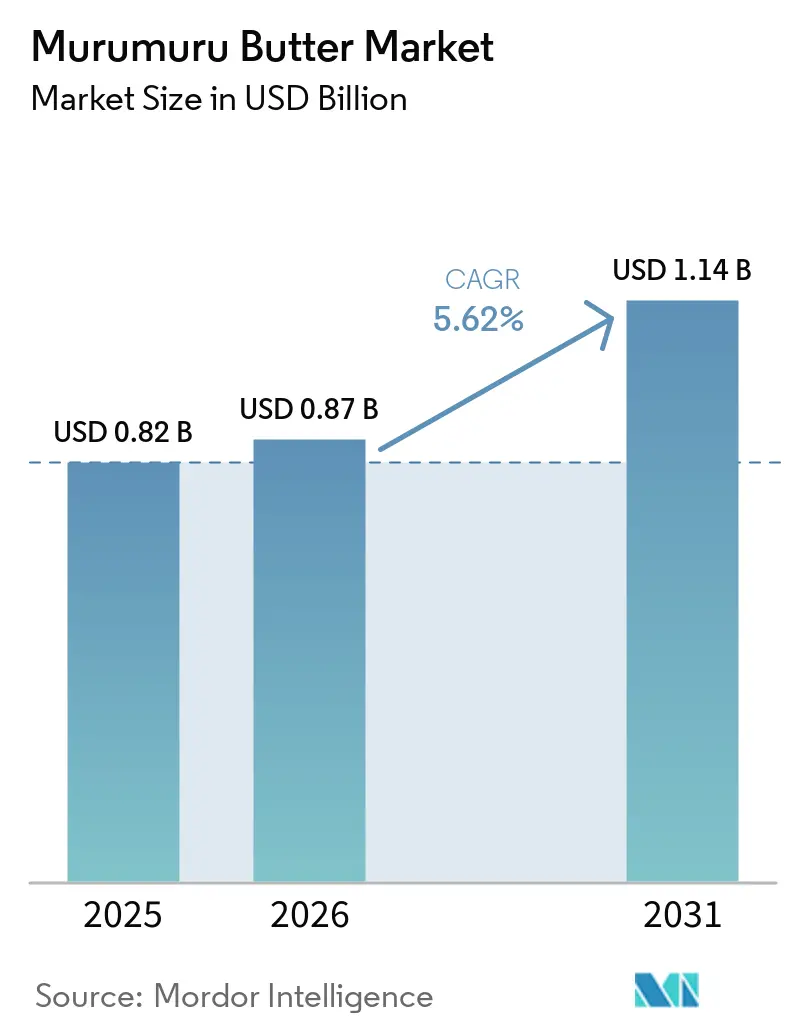

The Murumuru butter market size is projected to expand from USD 0.82 billion in 2025 and USD 0.87 billion in 2026 to USD 1.14 billion by 2031, registering a CAGR of 5.62% between 2026 and 2031. This Amazon-sourced emollient has transitioned from niche botanical curiosity to a formulation staple as brands chase clean-label differentiation while navigating tightening clean-label beauty norms in Europe under Cosmetics Regulation 1223/2009[1]Source: European Union, "Regulation (EC) No 1223/2009 of the European Parliament and of the Council," health.ec.europa.eu. Brands rely on murumuru’s 44-56% lauric acid and 24-32% myristic acid profile to deliver slip and occlusion comparable to synthetics while meeting vegan and silicone-free claims. Its growing popularity is further driven by rising consumer demand for sustainable, ethically sourced ingredients in personal care products. Murumuru butter is increasingly incorporated into hair care formulations for its ability to restore moisture, reduce frizz, and enhance shine. Supply, however, hinges on seasonal wild harvests in Brazil’s Médio Juruá basin, exposing the Murumuru butter market to climate volatility.

Key Report Takeaways

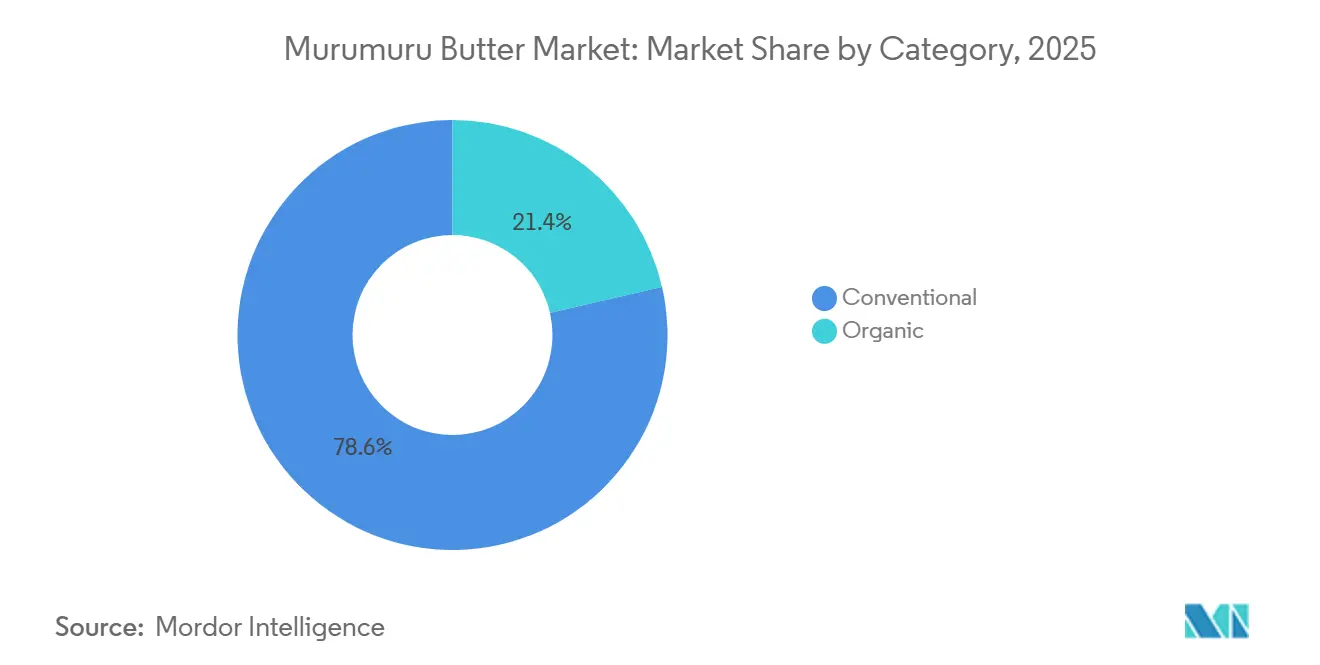

- By category, the conventional segment led with 78.58% of the murumuru butter market share in 2025, while the organic segment is forecast to post an 8.71% CAGR through 2031.

- By form, refined/deodorized butter led with 62.12% market share in 2025, and unrefined (virgin) butter is projected to grow at 7.78% CAGR over 2026-2031.

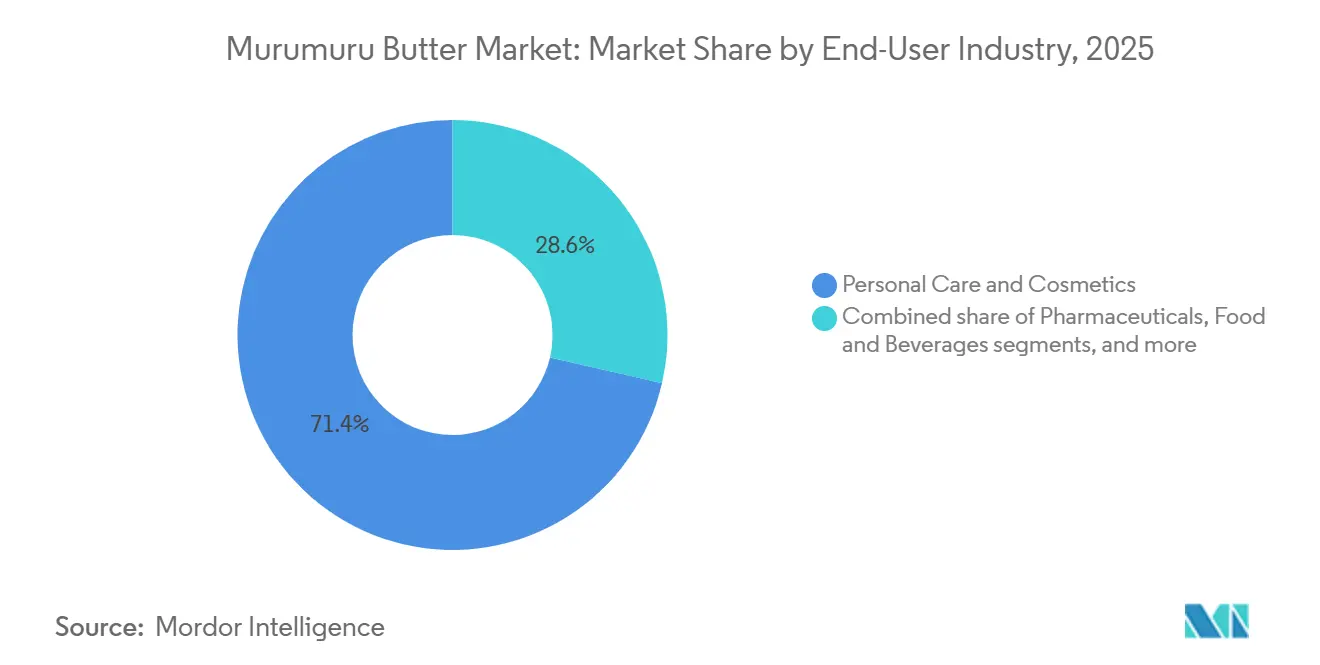

- By end-user industry, personal care and cosmetics accounted for 71.39% of the 2025 market share, and food and beverages are advancing at a 6.04% CAGR to 2031.

- By distribution channel, offline distribution channels captured 68.17% of the 2025 market share, while online channels are expanding at 7.09% CAGR through 2031.

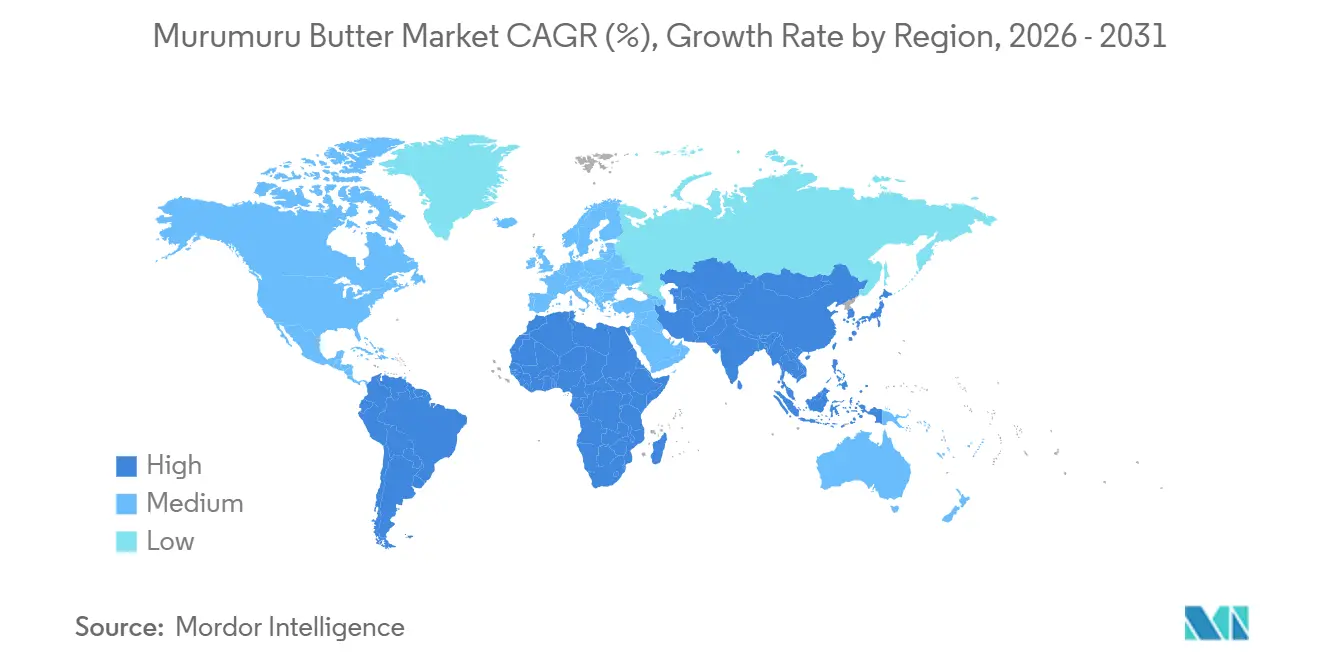

- By geography, North America accounted for 37.63% of the 2025 market share, whereas Asia-Pacific is poised for the fastest 8.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Murumuru Butter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural and organic personal-care ingredients | +1.2% | Global, with premium concentration in North America and Europe | Medium term (2-4 years) |

| Growing consumer preference for clean-label and chemical-free beauty products | +0.9% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Increasing use of personalized and multi-use beauty products | +0.7% | North America, Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of e-commerce and direct-to-consumer beauty channels | +1.0% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Higher consumer awareness of the benefits of botanical emollients | +0.8% | Europe, North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Growing adoption in high-performance haircare and skincare products | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and organic personal-care ingredients

The rising demand for natural and organic personal-care ingredients is driving luxury hair and skin care brands to increasingly adopt murumuru butter as a replacement for silicones and petroleum-based emollients. Its appeal is further enhanced by its potential for dual certification under COSMOS, NATRUE, and USDA Organic standards, which establish minimum organic content thresholds that wild-harvested Amazonian ingredients readily meet. This aligns with the growing consumer preference for eco-friendly and ethically sourced products. Brands are leveraging the natural provenance of murumuru butter to command price premiums over conventional variants, particularly in European markets, where certifications such as Ecocert and Soil Association seals significantly influence purchasing decisions. Additionally, the increasing awareness of the environmental impact of synthetic ingredients has led to a structural shift in the market, with consumers actively seeking products that align with sustainability goals.

Growing consumer preference for clean-label and chemical-free beauty products

Clean-label positioning has migrated from food to beauty. According to a 2024 survey by the British Standards Institution, 64% of global consumers favor natural ingredients, and 70% are willing to pay more for ethically sourced products[2]Source: British Standards Institution, “Natural and Organic Cosmetics Insights,” bsigroup.com. Growing consumer preference for clean-label, chemical-free beauty products has significantly boosted demand for murumuru butter. Its fatty-acid profile, dominated by medium-chain saturated fats, delivers emollient and occlusive functions without parabens, phthalates, or synthetic polymers that trigger consumer skepticism. The ingredient's melting point allows solid-balm formats that eliminate the need for liquid emulsifiers, a formulation simplicity that resonates with transparency-focused shoppers. This dynamic is accelerating in North America, where California's Toxic-Free Cosmetics Act bans specific synthetic fragrance compounds from 2025 onward, and in the European Union, where France enacted legislation to phase out per- and polyfluoroalkyl substances (PFAS) in cosmetics by 2026-2027[3]Source: California Government, "Toxic-Free Cosmetics Act, A.B. 2762," ca.gov.

Increasing use of personalized and multi-use beauty products

Personalized beauty formulations, exemplified by platforms such as BIOS, Qualia, Ash+Stone, LILIXIR, and CALLŌ, are increasingly incorporating murumuru butter for its multifunctional slip, barrier-repair, and sensory attributes that adapt seamlessly across hair, skin, and lip applications. The ingredient's solid-to-liquid phase transition at body temperature enables anhydrous stick formats that eliminate the need for preservative systems, offering a design advantage for custom-batch production where shelf-life predictability is critical. Multi-use products reduce SKU complexity and align with minimalist consumption trends; for instance, a single murumuru-based balm can function as a cuticle treatment, flyaway tamer, and cheekbone highlighter, consolidating three purchase occasions into one. This versatility is particularly valued in direct-to-consumer models, where shipping economics favor concentrated, high-margin items. The trend also intersects with biotechnology innovation, as brands explore fermentation-derived actives, such as regenerative exosomes and postbiotics, that pair with murumuru's lipid matrix to enhance penetration and efficacy, enabling differentiated claims that justify premium pricing.

Higher consumer awareness of the benefits of botanical emollients

Educational campaigns by ingredient suppliers and certification bodies have significantly enhanced consumer awareness of the benefits of botanical emollients. Murumuru butter, in particular, has gained recognition for its high lauric and myristic acid content, which strengthens the skin barrier and improves moisture retention, offering a natural alternative to synthetic emollients. Additionally, its medium-chain fatty acids confer antimicrobial and anti-inflammatory properties, which dermatology influencers on social media platforms have increasingly highlighted. This growing awareness has driven demand, especially in European and North American markets, where consumers are more informed about the advantages of botanical ingredients. Meanwhile, Asia-Pacific markets are in the early stages of adoption, presenting opportunities for suppliers to collaborate with local retailers and dermatology associations to educate consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain instability due to dependence on seasonal wild harvesting in remote Amazon regions | -0.8% | Global, sourcing concentrated in Brazil's Amazonas and Pará states | Short term (≤ 2 years) |

| Competition from low-cost alternate natural butters | -0.5% | Global, price-sensitive segments in all regions | Medium term (2-4 years) |

| ESG-related scrutiny of biodiversity sourcing and traceability | -0.4% | Europe and North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| High raw material and procurement costs | -0.6% | Global, acute in regions with complex logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply chain instability due to dependence on seasonal wild harvesting in remote Amazon regions

Murumuru palms fruit once annually, concentrating harvest activity into narrow windows that coincide with Amazonian rainy seasons. During these periods, river transport, the primary logistics mode in regions like Medio Jurua, becomes highly unpredictable, leading to delays and increased costs. Climate volatility further exacerbates this supply chain fragility, as irregular weather patterns can disrupt both harvesting and transportation schedules. Additionally, reliance on wild harvesting in remote Amazon regions limits scalability, as murumuru fruit availability is subject to natural cycles and environmental conditions. In contrast, competing ingredients, such as shea butter from West African cooperatives or coconut oil from Southeast Asia, benefit from year-round harvest cycles and well-established export infrastructure. These factors provide buyers with greater supply predictability and cost efficiency, making murumuru butter less competitive in terms of reliability and scalability.

ESG-related scrutiny of biodiversity sourcing and traceability

The European Union Deforestation Regulation (EUDR), which imposes due diligence obligations, requires geo-location coordinates and proof of deforestation-free sourcing for all forest-risk commodities, including cosmetic ingredients[4]Source: European Commission, “Regulation on Deforestation-Free Products,” environment.ec.europa.eu. Wild-harvested murumuru often lacks the plantation-style GPS precision that regulators demand, compelling suppliers to invest in advanced traceability systems such as plot-level mapping, satellite monitoring, and blockchain-enabled tracking. These measures significantly increase operational costs, particularly for small cooperatives in remote Amazon regions. Furthermore, certification schemes like the Union for Ethical BioTrade (UEBT), FairWild, and Rainforest Alliance provide frameworks to address biodiversity sourcing and traceability concerns. However, adoption remains inconsistent due to high audit costs, limited technical expertise, and logistical challenges. This creates a fragmented market where certified murumuru products command higher premiums, while uncertified supplies face diminishing demand amid growing ESG-related scrutiny from buyers and regulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Certification Drives Fastest Expansion

Conventional murumuru butter accounted for 78.58% of the market value in 2025, highlighting its dominance in mass-market haircare conditioners, body lotions, and soap bases, where cost per kilogram drives formulation decisions. This segment maintains its volume leadership by catering to industrial buyers, soap manufacturers, and contract formulators who prioritize consistent supply and competitive pricing over the additional costs associated with certification. However, the conventional segment faces margin pressures from private-label competition and commodity substitution. In contrast, organic-certified players benefit from certification barriers that require multi-year investments in traceability infrastructure and auditor relationships, deterring new entrants and sustaining pricing power for established players.

Organic-certified variants are projected to grow at a CAGR of 8.71% through 2031, driven by brands seeking COSMOS, NATRUE, and USDA Organic certifications that enable access to specialty offline channels and justify price premiums. The growth of organic murumuru is uneven across regions. European markets, where consumers show a strong preference for organic-certified personal care products, dominate certified volumes. In North America, demand is concentrated in natural and specialty retail channels, such as Whole Foods and independent beauty boutiques. Meanwhile, adoption in the Asia-Pacific region lags due to lower consumer awareness of certification marks and price sensitivity in mass-market segments.

By Form: Unrefined Variants Capture Premium Positioning

Refined/deodorized murumuru butter accounted for 62.12% of the 2025 market share, driven by its neutral scent profile and extended shelf life, which suit mass-market formulations requiring 24-36 months of stability under variable storage conditions. Refining processes, typically involving alkali neutralization, activated carbon bleaching, and steam deodorization, strip the ingredient's characteristic nutty aroma and reduce free fatty acid content, preventing rancidity and color shifts that complicate quality control in large-batch production. Industrial buyers favor refined murumuru for its formulation predictability and compatibility with synthetic fragrances, which would clash with the unrefined variant's inherent scent.

Unrefined (virgin) murumuru is expanding at 7.78% CAGR through 2031, propelled by clean-beauty advocates who equate minimal processing with superior nutrient retention and authenticity, even though peer-reviewed evidence for differential efficacy remains limited. Unrefined murumuru's growth is concentrated in artisanal and direct-to-consumer brands that leverage cold-press extraction and minimal filtration as marketing differentiators, often pairing the ingredient with storytelling around traditional Amazonian knowledge and single-origin provenance.

By End-User Industry: Food and Beverage Applications Accelerate

Personal care and cosmetics led the murumuru butter market with 71.39% share in 2025, reflecting the ingredient's established use in hair conditioners, leave-in treatments, body butters, lip balms, and barrier-repair creams, where its emollient and occlusive properties deliver immediate sensory payoff. In personal care, haircare products leverage murumuru's slip coefficient and heat-protection attributes, appealing to consumers managing chemically treated or heat-styled hair. Skincare applications are expanding as brands formulate overnight masks and barrier-repair serums that pair murumuru's lipid matrix with ceramides, niacinamide, and peptides to address compromised skin from retinoid use or environmental stressors. Lip care is a niche but high-margin segment, and murumuru's melting point enables anhydrous balm formats that eliminate preservative systems and align with clean-label positioning.

Food and beverage applications are forecast to grow at 6.04% CAGR through 2031 as edible-grade murumuru enters confectionery coatings, plant-based dairy analogs, and functional-food formulations targeting satiety and medium-chain triglyceride (MCT) delivery. The ingredient's lauric acid content mirrors coconut oil's fatty-acid profile, offering formulators a differentiated origin story for products positioning around Amazonian superfoods. Murumuru butter is gaining traction in premium chocolate formulations, where its smooth texture and unique melting properties enhance mouthfeel and flavor release. In plant-based dairy alternatives, murumuru butter is being explored as a fat source in vegan cheeses and spreads, providing a creamy texture and rich taste. Pharmaceutical uses, primarily in topical ointments, suppositories, and controlled-release matrices, leverage murumuru's biocompatibility and solid-to-liquid phase transition.

By Distribution Channel: Digital Platforms Reshape Purchase Journeys

Offline commanded 68.17% of murumuru butter market value in 2025, anchored by specialty beauty retailers, natural-product stores, pharmacies, and department-store cosmetics counters, where tactile evaluation, such as texture, scent, and absorption speed, drives purchase decisions for unfamiliar ingredients. Brick-and-mortar channels also provide immediate gratification and eliminate shipping costs, advantages that sustain foot traffic despite e-commerce encroachment. The offline segment retains advantages in impulse purchases, gift sets, and demographics skeptical of online beauty shopping, yet its growth trajectory lags digital channels that offer superior data capture, personalization, and geographic reach without the fixed costs of retail footprints.

Online is expanding at a 7.09% CAGR through 2031, fueled by online retailers such as Amazon, TikTok Shop's discovery-to-conversion integration, and direct-to-consumer brands that bypass wholesale margins to invest in content marketing and subscription models. Digital platforms excel at storytelling; brands deploy geo-tagged imagery of Amazonian cooperatives, third-party traceability dashboards, and influencer testimonials that emphasize murumuru's exotic provenance and ethical sourcing. Online channels also enable sample-first strategies that reduce risk perception; customers receive trial sachets of murumuru-enriched formulations, lowering the barrier to trial for ingredients lacking mainstream recognition. Subscription pricing, monthly deliveries of haircare or skincare kits featuring murumuru, locks in recurring revenue and improves customer lifetime value.

Geography Analysis

North America held 37.63% of the murumuru butter market value in 2025, with the United States driving demand through clean-beauty adoption, regulatory shifts under the FDA's Modernization of Cosmetics Regulation Act (MoCRA), and California's Toxic-Free Cosmetics Act that bans specific synthetic compounds from 2025 onward. These mandates push formulators toward botanicals with established safety profiles. Canada's natural-product retail infrastructure, anchored by chains such as Well.ca and independent health-food stores, provides distribution for murumuru-based SKUs targeting eco-conscious consumers willing to pay premiums for Amazonian provenance. Mexico's beauty market, though smaller, is expanding as rising middle-class incomes and cross-border e-commerce from United States platforms introduce murumuru-enriched products to urban centers.

Asia-Pacific is forecast to expand at 8.26% CAGR through 2031, the fastest among all regions, propelled by China and India's beauty market. Consumers are prioritizing the provenance of premium ingredients over brand heritage, a behavioral shift that murumuru suppliers can leverage through education partnerships with retailers and dermatology influencers. Lush's January 2026 entry into India via Myntra, featuring over 150 SKUs with murumuru-based products prominently positioned, signals confidence in the market's willingness to adopt unfamiliar Amazonian ingredients when paired with digital storytelling and experiential retail. Japan's beauty consumers, known for ingredient literacy and willingness to trial novel botanicals, represent a high-value segment, while Australia's natural-product retail infrastructure and proximity to Asia-Pacific supply chains position it as a regional hub.

Europe's regulatory environment creates compliance complexity that favors established suppliers with traceability infrastructure. Italy and France's natural cosmetics market prefer organic-certified personal care, underscoring demand density that absorbs murumuru's cost premium. Germany, the United Kingdom, and the Netherlands serve as distribution hubs, with Clariant's expansion of Beraca ingredient availability across the DACH region (Germany, Austria, Switzerland) illustrating how suppliers leverage European logistics networks to serve fragmented national markets. Spain's clean-beauty segment is emerging, driven by younger demographics and social-media influence, yet Southern and Eastern European markets remain price-sensitive, limiting murumuru penetration to premium tiers.

Competitive Landscape

The murumuru butter market is moderately concentrated, reflecting a bifurcated structure where vertically integrated majors such as Natura &Co, Citróleo Group, Clariant (via Beraca and Lucas Meyer Cosmetics acquisitions), control upstream Amazonian sourcing and downstream specialty-active formulation, while smaller ingredient houses and distributors compete on traceability documentation, fair-trade premiums, and regional logistics. Clariant's April 2024 acquisition of Lucas Meyer Cosmetics for USD 810 million consolidated its position, with expertise in bio-functional actives, and cross-selling murumuru-based formulations into Lucas Meyer's customer base. Natura's vertical integration extends to community partnerships; its May 2025 inauguration of a solar-powered agro-industry in Ilha das Cinzas processes murumuru, ucuuba, and patauá from 470 families, embedding social impact into supply-chain economics.

Emerging opportunities center on food-grade murumuru for plant-based dairy and confectionery applications, pharmaceutical formulations leveraging its biocompatibility for topical drug delivery systems, and home-care products targeting waterless formats, where murumuru's solid-to-liquid phase transition enables anhydrous stick designs. Additionally, its high lauric and myristic acid content is gaining traction in premium hair care formulations, particularly for leave-in conditioners and anti-frizz treatments. Artisanal brands are also capitalizing on murumuru's natural appeal, with blockchain traceability initiatives such as Lush's plot-level mapping of its 100-hectare Marajó Island reforestation initiative, commanding premiums from transparency-focused consumers.

Technology adoption is uneven; while Natura and Clariant invest in satellite monitoring and geo-location databases to satisfy compliances, smaller cooperatives lack capital for digital infrastructure, creating a competitive divide where certified, traceable murumuru captures premium channels and uncertified volumes face shrinking buyer pools. Strategic patterns reveal a shift from commodity positioning to differentiated actives. Suppliers are bundling murumuru with complementary Amazonian ingredients, such as cupuaçu and açaí, to create proprietary formulations that resist commoditization. Advancements in processing technologies, such as cold-press extraction and enzymatic refinement, are enhancing the quality and shelf stability of murumuru butter.

Murumuru Butter Industry Leaders

-

Clariant

-

Akoma International UK Limited

-

Lush Retail Ltd.

-

Jarchem Industries Inc.

-

Natura &Co

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lush entered the Indian market via a partnership with Myntra (owned by Bilberry Brands), offering over 150 products, including murumuru-based haircare and skincare formulations.

- February 2026: Lush launched a Paddington-themed collaboration incorporating unrefined murumuru butter alongside Peruvian Brazil nut oil and sacha inchi oil sourced from Candela Peru, bundling multiple Amazonian ingredients to create differentiated narratives around ethical sourcing and traditional knowledge. The limited-edition line targets premium gift segments and reinforces Lush's positioning around fair-trade botanicals.

- February 2026: Natura &Co inaugurated a solar-powered agro-industry in Ilha das Cinzas, Marajó Island, designed in partnership with WEG to process murumuru, ucuuba, and patauá from 470 families. The facility's renewable-energy infrastructure reduces processing costs and carbon footprint, aligning with Natura's 2030 Commitment to Life targets of net-zero emissions and 95% renewable ingredients.

- October 2025: IMCD acquired Dong Yang FT, a South Korean specialty-ingredients distributor with approximately EUR 34 million in annual revenue, to strengthen its Asia-Pacific footprint in beauty and personal-care markets. Transaction closure is expected in the first quarter of 2026, adding regional logistics capabilities and customer relationships that facilitate murumuru market entry across South Korea and neighboring markets.

Global Murumuru Butter Market Report Scope

Murumuru butter is a highly moisturizing, nutrient-rich fat derived from the seeds of the Astrocaryum murumuru palm tree native to the Amazon rainforest. Renowned for its high lauric acid content, it is used in skincare and haircare to deeply hydrate, seal in moisture, and promote shine without being greasy.

The murumuru butter market is segmented by category, form, end-user industry, distribution channel, and geography. Based on category, the market is segmented into organic and conventional. Based on form, the market is segmented into unrefined (virgin) and refined/deodorized. Based on end-user industry, the market has been segmented into personal care and cosmetics, pharmaceuticals, food and beverage, home care products, biofuels and industrial, and others. Based on distribution channels, the market has been segmented into offline distribution channels and online distribution channels. Based on geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and volume (Tons).

| Organic |

| Conventional |

| Unrefined (Virgin) |

| Refined/Deodorized |

| Personal Care and Cosmetics | Hair Care Products |

| Skin Care Products | |

| Lip Care Products | |

| Others | |

| Pharmaceuticals | |

| Food and Beverages | |

| Home Care Products | |

| Biofuels and Industrial | |

| Others |

| Online distribution channels |

| Offline distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Form | Unrefined (Virgin) | |

| Refined/Deodorized | ||

| By End-User Industry | Personal Care and Cosmetics | Hair Care Products |

| Skin Care Products | ||

| Lip Care Products | ||

| Others | ||

| Pharmaceuticals | ||

| Food and Beverages | ||

| Home Care Products | ||

| Biofuels and Industrial | ||

| Others | ||

| By Distribution Channel | Online distribution channels | |

| Offline distribution channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Murumuru butter market in 2031?

The murumuru butter market is projected to reach USD 1.14 billion by 2031, reflecting a 5.62% CAGR from 2026 to 2031.

Which region will add the most Murumuru butter market size through 2031?

Asia-Pacific is forecast to deliver the highest incremental growth, expanding at an 8.26% CAGR on the back of Chinese and Indian demand.

Which segment commands the largest Murumuru butter market share today?

Personal care and cosmetics accounted for 71.39% of 2025 market share.

Why are organic grades growing faster than conventional ones?

Organic-certified murumuru satisfies COSMOS and NATRUE audits that retailers now treat as entry tickets, driving an 8.71% CAGR for certified grades.

Page last updated on: