Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

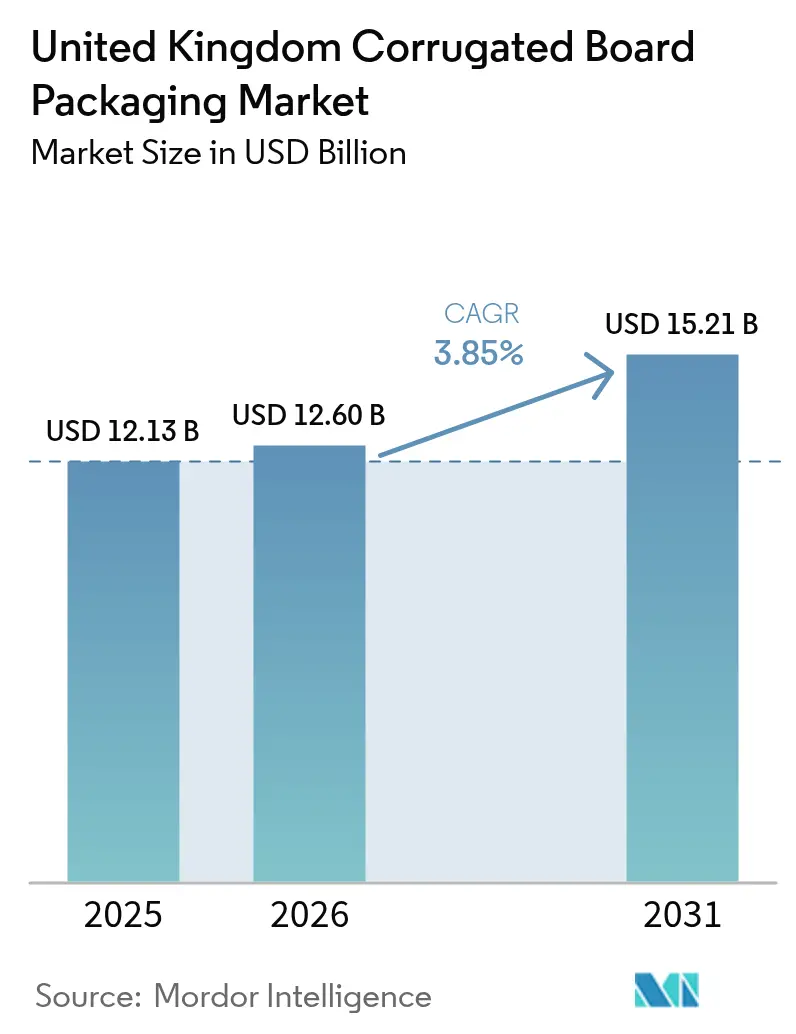

| Base Year Market Size (2025) | USD 12.13 Billion |

| Market Size (2026) | USD 12.6 Billion |

| Market Size (2031) | USD 15.21 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

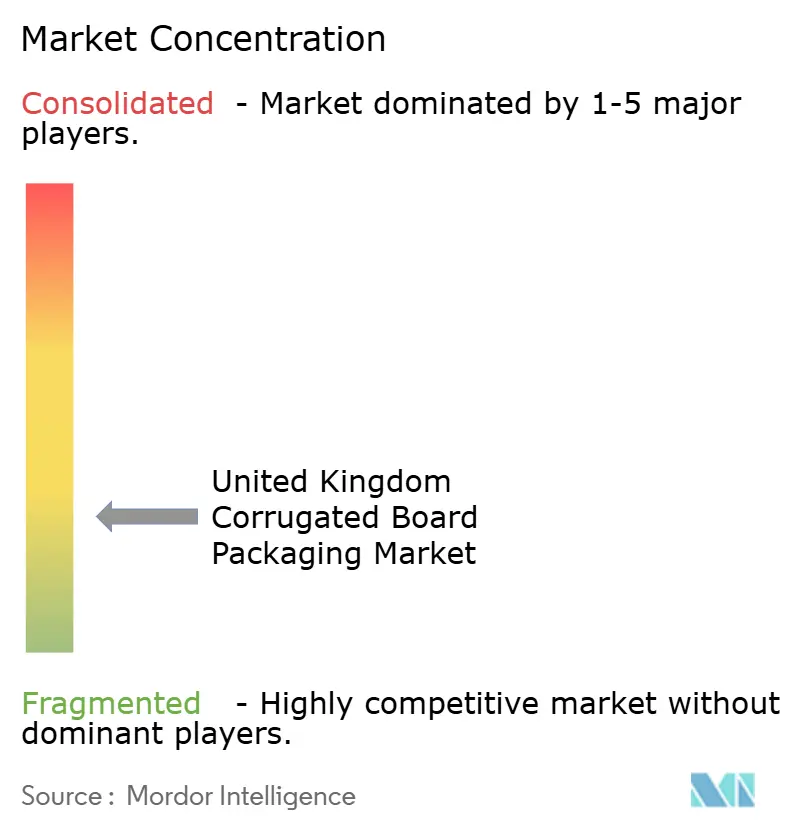

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Corrugated Board Packaging Market Analysis by Mordor Intelligence

The United Kingdom corrugated board packaging market size in 2026 is estimated at USD 12.6 billion, growing from 2025 value of USD 12.13 billion with 2031 projections showing USD 15.21 billion, growing at 3.85% CAGR over 2026-2031. Consistent demand from e-commerce fulfillment, regulatory incentives favoring fiber solutions, and cost-optimized lightweight fluting technology collectively underpin this trajectory. The sector benefits from Extended Producer Responsibility (EPR) rules that transfer end-of-life costs to producers, spurring a decisive shift away from single-use plastics and reinforcing the material-recovery leadership already enjoyed by corrugated substrates. Brand owners also lean on the format’s recyclability and print versatility to elevate shelf presence, while converters pursue energy-efficiency upgrades to soften the blow of volatile utility prices. Intensifying consolidation, capped by International Paper’s acquisition of DS Smith, expands integrated capacity, raises the industry’s operating scale, and pressures mid-tier participants to carve defensible niches. Against this backdrop, moderate growth signals a maturing yet still opportunity-rich environment in which technology investments, circular-economy credentials, and proximity-based service models shape competitive advantage.

Key Report Takeaways

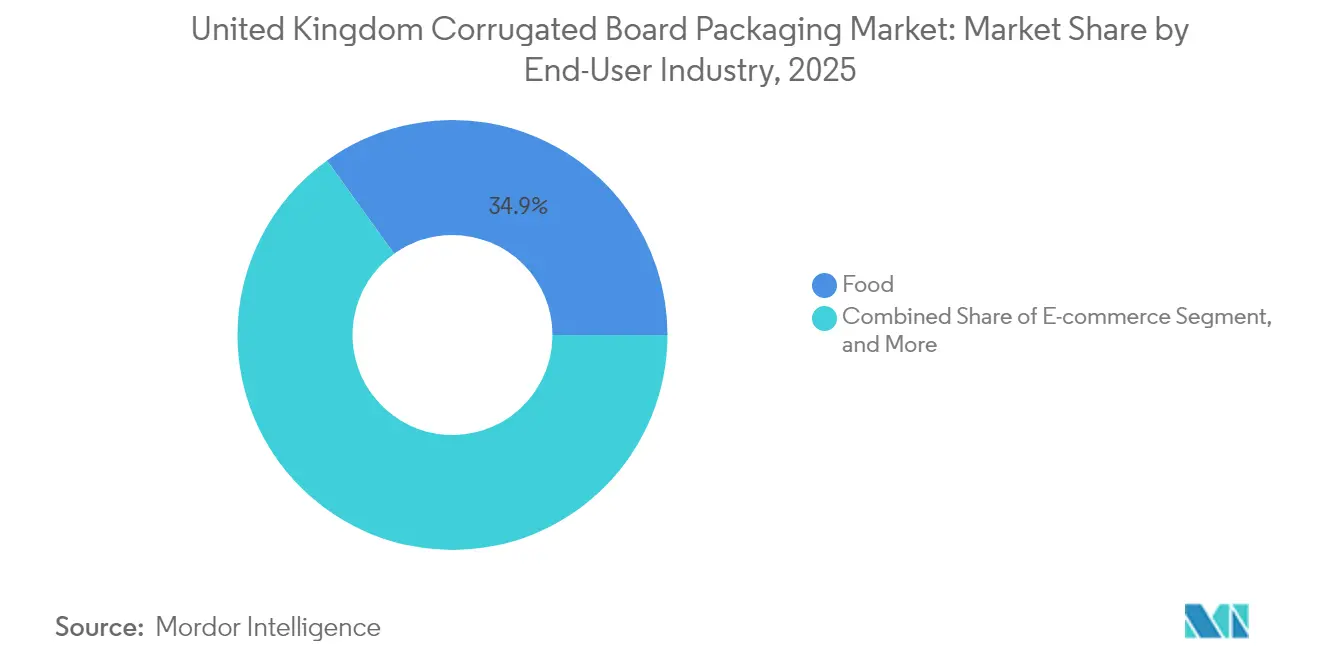

- By end-user industry, food applications commanded 34.92% of the United Kingdom corrugated board packaging market share in 2025, while e-commerce is set to accelerate at a 5.16% CAGR to 2031.

- By flute type, C-Flute held the lead with a 31.74% share in 2025; F/N Microflute is forecast to expand the fastest at a 4.80% CAGR through 2031.

- By board construction, single-wall designs accounted for 38.88% of the market in 2025, but triple-wall configurations are projected to post the strongest growth, advancing at a 4.82% CAGR over the outlook period.

- By printing process, flexography represented 28.02% of revenue in 2025, whereas digital printing is poised for a 5.04% CAGR on the back of customization and short-run demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Corrugated Board Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment volume surge | +1.2% | Nationwide, strongest in London, Manchester, Birmingham hubs | Medium term (2-4 years) |

| Retailer shift to shelf-ready packaging | +0.8% | All major retail corridors | Short term (≤ 2 years) |

| Substitution away from single-use plastics | +0.6% | Nationwide | Long term (≥ 4 years) |

| Cost-optimized lightweight fluting technology | +0.5% | Midlands and North England manufacturing belts | Medium term (2-4 years) |

| AI-enabled box-on-demand systems | +0.4% | Southeast England tech clusters | Long term (≥ 4 years) |

| Carbon-footprint labeling mandates | +0.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfillment Volume Surge

Online retail requires about 30% more protective packaging per parcel than traditional channels, elevating corrugated demand as parcel counts climb. [1]Office for National Statistics, “Retail Sales: January 2025,” ons.gov.uk United Kingdom e-commerce sales leapt 15.8% in 2024, locking in behavioral shifts that spread across categories ranging from apparel to small electronics. Converters integrate AI-driven box-on-demand equipment that trims material use by up to 25% without sacrificing strength, enabling right-sized shipping solutions that control dimensional-weight charges. Direct data feeds from e-commerce storefronts into manufacturing execution systems cut inventory holdings and sharpen response times, a decisive advantage for brands targeting premium unboxing experiences. Specialized converters riding this wave often stress digital printing, enabling variable graphics and event-driven campaigns at minimal setup cost.

Retailer Shift to Shelf-Ready Packaging

Major grocery chains such as Tesco and ASDA broadened shelf-ready mandates across ambient aisles, reducing in-store labor by up to 50% and slashing damage rates during restocking.[2]British Retail Consortium, “Shelf-Ready Packaging Guidelines Updated,” brc.org.uk Corrugated designs featuring perforations and easy-open tear strips satisfy the mixed need for shipping resistance and rapid presentation. Collaboration among brands, retailers, and converters intensifies because display geometry, case counts, and stacking integrity must harmonize. Smaller regional converters build loyalty through fast prototyping and local service, whereas national players extract value from die-cutting scale and high-capacity flexo presses. The payoff for successful participants is higher unit revenue from premium structural features and higher end-of-aisle compliance.

Substitution Away from Single-Use Plastics

EPR levies averaging GBP 400-600 per tonne on plastic packaging widen the cost gap versus corrugated fiber, stimulating rapid material switch-outs in fresh produce trays, beverage carriers, and multi-packs. Improved barrier coatings and moisture-tolerant liners now allow corrugated boxes to withstand chilled-chain humidity, unlocking addressable volumes in fruit, vegetable, and ready-meal channels. Research partnerships between board mills and chemical suppliers focus on water-based coatings that maintain recyclability while repelling condensation. Retailers increasingly display fiber-based solutions as visible proof of sustainable commitment, pushing peer competitors to follow suit. Manufacturers that invested early in specialty coating lines now hold a technological moat that commands premium pricing.

Cost-Optimized Lightweight Fluting Technology

Advanced F- and N-flute profiles trim fiber by 15-20% yet keep compression strength intact, a direct response to both input-price inflation and carbon-reduction targets. Precision corrugators and next-generation starch adhesives allow tighter flute pitches that flatten board caliper without compromising edge-crush requirements. Logistics advantages cascade from lighter boxes that increase pallet yields and reduce freight emissions. Capital intensity, however, rises: plants must install laser-controlled gap monitoring and enhanced pre-heater sections. Well-capitalized multinationals can absorb these outlays, while many independent plants collaborate with OEMs to retrofit step-change upgrades. Rapid adoption continues wherever volumetric shipping tariffs drive cost avoidance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-tightening recycled paper availability | -0.7% | Nationwide, severe in dense urban areas | Short term (≤ 2 years) |

| Energy-price volatility pressuring mill margins | -0.5% | Scotland and North England manufacturing corridors | Medium term (2-4 years) |

| Labor shortages in United Kingdom logistics | -0.4% | National distribution networks, worst in Southeast | Short term (≤ 2 years) |

| Import competition from Eastern Europe | -0.3% | Ports and major distribution centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Re-tightening Recycled Paper Availability

Paper Recovery Note (PRN) values broke two-decade highs at GBP 180-200 per tonne in 2024, exposing the imbalance between collection output and mill intake. [3]Confederation of Paper Industries, “Recycling Factsheets,” paper.org.uk Contamination in mixed municipal streams erodes fiber quality, forcing converters either to hunt costlier sorted grades or import recovered paper from continental suppliers. Integrated producers respond by acquiring collection fleets and sorting facilities, securing feedstock, and reducing spot-market exposure. Smaller independents, lacking such scope, endure episodic downtime or raise finished-box prices, risking share loss. Currency volatility adds another cost layer when euro-denominated imports rise against sterling, complicating procurement hedges.

Energy-Price Volatility Pressuring Mill Margins

Quarter-on-quarter swings of 25-40% in industrial electricity tariffs during 2024 rocked operational budgets for energy-intensive corrugators. Producers scramble to sign long-term power-purchase agreements tied to renewable projects that promise cost stability and carbon credits. Investment in combined heat-and-power (CHP) plants at select mills is already trimming energy bills by up to 30% and shaving Scope 1 emissions, yet CAPEX hurdles remain steep. Facilities unable to lock in predictable rates risk cash-flow drag and reduced maintenance budgets, hastening the retirement of antiquated equipment. In parallel, energy audits spotlight compressed-air leaks and sleeve-roll inefficiencies, highlighting no-regret savings that management teams now prioritize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Food Dominance Drives Sustainability Innovation

Food applications represented 34.92% of the United Kingdom corrugated board packaging market in 2025, reflecting entrenched dependence on fiber-based transit packaging across produce, ambient grocery, and beverage supply chains. The segment’s growth remains linked to substitution away from hard-to-recycle plastics, especially for fresh fruit trays incorporating moisture-resistant coatings. Retail take-up accelerates as supermarkets showcase the recyclability narrative to shoppers, locking in volume for converters with barrier-treatment capacity. E-commerce, though smaller, is forecast to advance at a 5.16% CAGR, buoyed by direct-to-consumer shipping formats that often demand burst strength equal to transit boxes but refined graphics aimed at end-user unboxing. The United Kingdom corrugated board packaging market size for e-commerce shipments is projected to balloon alongside parcel counts, supplying profitable short-run work to plants outfitted with digital presses.

Packagers serving beverages maintain steady momentum through multi-pack carriers, exploiting flexo’s high-speed capability for promotional branding aligned with sporting and holiday calendars. Electronics and personal-care niches, while comparatively modest in tonnage, deliver higher revenue per square meter due to anti-static liners and premium printing. End-use diversification thus cushions overall demand against cyclical swings in any single consumption category, a strategic hedge embraced by larger integrated players.

By Flute Type: Microflute Innovation Challenges Traditional Configurations

C-Flute holds a 31.74% slice of the United Kingdom corrugated board packaging market share, beloved for its balanced cushioning and print surface. Yet F/N Microflute is stealing the spotlight with a projected 4.80% CAGR; its ultra-thin profile allows finer graphics while shaving dimensional weight, an attribute highly prized in parcel networks where carriers bill by volume. The United Kingdom corrugated board packaging market size allocated to microflute designs is set to rise as apparel and cosmetic shippers demand Instagram-ready presentation without superfluous airspace.

A- and B-Flute grades remain essential for heavy or fragile SKUs where drop-test performance eclipses cube-optimization needs. E-Flute, positioned between display aesthetics and structural integrity, thrives in shelf-ready formats whose outer facing must double as a merchandising panel. Ongoing flute diversification complicates inventory planning, prompting converters to deploy digital twin software that simulates performance at varying grammages before committing paper. The winners balance wide flute arsenals with agile changeovers, minimizing downtime and scrap.

By Board Type: Triple-Wall Gains Ground in Heavy-Duty Applications

Single-wall constructions accounted for 38.88% of total volume in 2025, thanks to competitive price points and a broad utility span. Triple-wall, while currently niche, registers the best forward momentum at a 4.82% CAGR, largely because e-commerce players seek robust solutions able to protect high-value consumer durables through multi-node distribution. The United Kingdom corrugated board packaging market size for triple-wall formats should therefore outpace average industry expansion, even if its share remains below one-tenth of aggregate tonnage by 2031.

Double-wall clings to relevance where mid-grade stacking strength suffices, think beverages, DIY tools, and moderate-weight groceries, allowing retailers to sidestep the weight premium of triple-wall. Single-face sheets thrive as inner wraps and dunnage that shield molded plastic or metal parts from abrasion. Specialty honeycomb cores, while outside the mainstream, attract automotive OEMs looking for impact absorption at lighter weight than plywood crates. Board-type variation demands converters refine scheduling logistics, as thicker builds require slower corrugator speeds and extended drying cycles.

By Printing Technology: Digital Revolution Transforms Customization

Flexography captured 28.02% of revenue in 2025, propelled by its low ink cost and rapid setup for high-throughput runs. Yet digital presses, inkjet, and electrophotographic alike- are forecast for a 5.04% CAGR, carving share by enabling batch sizes as low as one while still meeting brand-color standards. The United Kingdom corrugated board packaging market size is attributed to digital output expanding each time a direct-to-consumer brand pivots from generic brown kraft to full-bleed graphics shipped within 48 hours.

Litho-laminated topsheets continue to own premium point-of-sale displays where photographic rendering and gloss varnish are non-negotiable. Screen printing occupies a smaller but defensible corner servicing tactile varnish and scent-release applications. Hybrid architectures combining flexo pre-print with late-stage digital personalization attract marketers that run national campaigns followed by region- or event-specific overlays, compressing lead times and inventory. Plants adding digital capacity must retrain operators on RIP workflows and ICC color profiling, an investment increasingly viewed as table stakes rather than speculative.

Regulatory Landscape

The United Kingdom corrugated board packaging market operates under the Producer Responsibility Obligations (Packaging and Packaging Waste) Regulations 2024, with amendments introduced via the 2025 Amendment Regulations taking effect from 1 January 2026. Under the extended producer responsibility (EPR) framework, obligated producers must report packaging data, meet recycling obligations (including via PRNs/PERNs), and pay household packaging waste disposal fees, which increases the need for accurate material classification for paper and board formats.

From 2026, PackUK serves as the scheme administrator for EPR delivery, linking compliance outcomes to producer cost through administration, data validation, and fee-setting processes. Regulatory definitions also tighten for fiber-based composite and paper/board packaging from 1 January 2026, including a 5% mass threshold for plastic layers in paper-based packaging, affecting how coated and laminated corrugated solutions are treated within obligations. In July 2026, PackUK announced a 1 September 2026 resubmission deadline for 2025 packaging data to support 2026/27 fee calculations and Notices of Liability, reinforcing the importance of aligning internal data systems and specifications management with regulator timelines.

Value Chain Analysis

The United Kingdom corrugated board packaging value chain starts with fiber procurement (virgin kraft and recovered paper), followed by containerboard manufacturing, corrugated sheet production, and conversion into cases, shelf-ready packs, and protective packaging. Integrated groups combine paper mills, corrugators, and converting sites, while independent converters and sheet plants purchase containerboard or sheets and compete through responsiveness, structural design, and print capability; trade bodies such as the Confederation of Paper Industries (CPI) and the Sheet Plant Association (SPA) support sector guidance on compliance and operating practices.

Logistics and proximity to demand centers matter because corrugated packaging is bulky and freight-sensitive. Operational models that co-locate board production and conversion, including the Packaging Park approach used by eCorrugated Ltd and Prowell Ltd, reduce transport distances and emissions while shortening lead times for retail and e-commerce customers. Investment in converting throughput and automation also shapes competitiveness, illustrated by Fencor Packaging Groups Manor Packaging site operating a high-speed line capable of 10,000 boxes per hour (announced June 2026), which improves service for short lead-time, higher-mix jobs as supply chains respond to EPR-driven material efficiency requirements.

Competitive Landscape

Early 2025 reshaped industry hierarchy when International Paper sealed its GBP 5.8 billion (USD 7.2 billion) purchase of DS Smith, forging a top-tier player with global revenue above USD 28 billion and roughly 65,000 employees. Integration plans slot 500,000-600,000 tonnes of United Kingdom containerboard into the buyer’s mill system, elevating internal supply coverage toward 90% and targeting USD 514 million in synergies by year 4. The move squeezes mid-tier converters on procurement leverage and selling prices, compelling some to forge supply alliances or focus on high-complexity niche runs.

Smurfit WestRock, itself fresh from a trans-Atlantic merger, reported USD 7.5 billion in Q4 2024 net sales and signaled a USD 400 million synergy capture by end-2025, underscoring the scale economics now setting the competitive pace. VPK Packaging deepened its United Kingdom reach by investing in Fencor Packaging, a specialist in design-led corrugated solutions, evidence that smaller yet agile groups can still create value by targeting bespoke requirements outside commodity grades. Antalis Packaging’s acquisition of The Packaging Company extends the distributor-converter hybrid model, amplifying service intensity across the Midlands.

Strategic themes concentrate on vertical integration to guarantee fiber supply, coupled with digital workflows that shrink design-to-market lead times demanded by direct-to-consumer brands. Capital expenditures gravitate toward energy-saving corrugators, AI-driven predictive maintenance, and digital printing fleets that process variable artwork without plate changes. Sustainability credentials escalate in customer audits, pushing ISO 14001 and FSC chain-of-custody certification from “nice-to-have” to mandatory. In this evolving arena, converters incapable of matching the capital pace or of differentiating through service risk margin erosion and potential buy-out.

United Kingdom Corrugated Board Packaging Industry Leaders

Smurfit WestRock

International Paper Company

Mondi plc

GWP Group Ltd.

Belmont Packaging Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EPR administration through PackUK, including the operational focus for 2026 to 2027 and progress on fee design, ties packaging design choices more directly to producer costs. This creates room for corrugated suppliers that can deliver verifiable recyclability, clearer material classification (including coated or composite paper-based structures), and data-ready specifications that make customer reporting easier. Lightweight lightweight fluting and right-sizing solutions also fit with producer efforts to reduce obligated tonnage while keeping enough transit protection for e-commerce and shelf-ready formats.

Capacity additions and technology upgrades give converters practical paths into higher-service segments, including short runs, complex die-cuts, and fast-turn retail-ready packs. Eren Holdings completion of the Shotton Paper Mill redevelopment in Flintshire, Wales (including a 750,000 tpa containerboard machine and a corrugating facility for 110,000 tonnes of boxes per annum, completed June 2026) and Sheard Packagings completion of investment in a third Gopfert rotary die cutter with a fourth Bahmuller gluer line scheduled to arrive in June 2026 at its Yorkshire facility support that shift. On the demand side, retailer shelf-ready requirements (e.g., Tesco and ASDA mandates) and continued growth in UK online retail activity create additional work for converters that combine design services, rapid prototyping, and variable graphics through digital printing workflows.

Recent Industry Developments

- June 2026: Eren Holding completed the Shotton Paper Mill redevelopment in Flintshire, Wales, adding a 750,000 tpa containerboard machine and a corrugating facility sized for 110,000 tonnes of boxes per year. This step increases domestic integrated supply options for UK corrugated packaging buyers and strengthens local availability of liner and fluting for converters.

- April 2026: Smurfit WestRock launched a consultation process on the future of its Birmingham SSK paper mill, a site supplying about 200,000 tonnes of fluting and liner to the UK and Irish corrugated market. The action forms part of a wider asset optimization program and can alter regional sourcing and lead-time planning for downstream corrugated packaging producers.

- October 2024: VPK Packaging invested in Fencor Packaging Group, reinforcing its presence in the United Kingdom corrugated sector. The move supports expansion into design-led, bespoke corrugated solutions and increases competitive intensity for independent converters focused on higher-complexity work.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, we treat the market as the total value of corrugated board packaging sold for use in the United Kingdom, covering boxes and related corrugated formats used to protect, ship, and handle goods across industries.

Scope exclusions (not counted): non-corrugated paper packaging (such as folding cartons), plastic protective packaging, and return logistics services that are not sold as corrugated packaging value.

Segmentation Overview

- By End-User Industry

- Food

- Processed Foods

- Fresh Food and Produce

- Beverages

- E-commerce

- Electrical and Electronics

- Personal Care and Cosmetics

- Other End-User Industries

- Food

- By Flute Type

- A-Flute

- B-Flute

- C-Flute

- E-Flute

- F/N Microflute

- Other Flute Types

- By Board Type

- Single Face

- Single Wall

- Double Wall

- Triple Wall

- By Printing Technology

- Flexography

- Digital Printing

- Litho-lamination

- Screen Printing

- Other Printing Technologies

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the UK demand and supply context that sits behind corrugated packaging usage. We rely on public industry and trade signals such as packaging and paperboard statistics from UK government sources (for example, ONS), trade flow series from HMRC, and customs or trade datasets that show paper and paperboard movements.

To keep assumptions realistic, we also review sources such as the Confederation of Paper Industries publications, corrugated industry fact sheets from trade bodies, peer reviewed papers on paper and board recycling rates, and public policy documents tied to packaging waste and Extended Producer Responsibility. Company annual reports, investor presentations, and reputable press are used to sense check capacity adds, major contract wins, and pricing comments. We also use paid subscriptions only where they add structure, including company financials and patent databases, plus an import and export shipment level database when a trade check is needed. The sources listed here are illustrative, and many other public references are used to clarify, validate, and fill gaps during the work.

Primary Interviews and Surveys

Primary inputs come from interviews and short surveys with packaging converters, paper and board participants, distribution focused stakeholders, and large packaging buyers across key UK end use categories like food, beverages, and e-commerce. We use these conversations to confirm what is truly being purchased as corrugated board packaging, validate price movement logic, and test how demand changes with shipment intensity and retail fulfillment patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 58% | Functional/Unit leaders: 30% | |

| Smaller Players: 16% | Managers: 58% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up mix that can be repeated with practical data. The top-down side reconstructs the UK corrugated packaging value pool by linking packaging demand to end use shipment intensity and fulfillment needs, and then applying price levels that reflect what buyers actually pay in the market.

To keep the model grounded, we track variables that typically move the category, such as UK manufacturing and retail activity signals, e-commerce parcel and delivery intensity proxies, paper and board input cost direction, recycled fiber availability cues, and observed shifts in packaging mix toward lighter or stronger board grades. Those inputs are then corroborated with selective bottom-up approximations, like sampled average selling price ranges from interviews, converter revenue context from public filings, and channel checks on how pricing and volumes moved across common box formats. Where company disclosures are incomplete, gaps are handled through ratio based allocation using production mix cues and buyer procurement patterns shared in interviews.

Forecasts are developed using scenario analysis. In the base case, we follow expected demand from key end users and a realistic price path that reflects energy and fiber cost direction. We then test the forecast against expert expectations for run rates, utilization sentiment, and procurement behavior to avoid overreacting to short term price spikes.

Data Validation & Update Cycle

Outputs are checked in several steps before numbers are finalized. We compare results with independent signals like trade direction, public packaging policy timelines, and the consistency of implied prices against interview ranges, and then we flag sharp jumps that do not fit the demand story.

A second analyst review is done to check formulas, units, and year to year movements, followed by a final logic review that challenges the main assumptions and sensitivities. When variance is high or a new event changes the outlook, we re-contact selected participants to retest the key inputs before sign-off. Reports are refreshed annually, with interim updates for material changes, and a last pass completed close to delivery so the latest updated view is provided.

Mordor Intelligence's United Kingdom Corrugated Board Packaging Market Size Compared Against Other Published Estimates

Published market sizes for UK corrugated board packaging can look far apart, even when the studies are describing the same industry in broad terms. The usual drivers are differences in what gets counted as corrugated packaging value, how price changes are treated through the base year, and whether the estimate is tied to real demand signals or mainly to broad packaging totals.

Some published figures appear to include a wider paper packaging basket or add adjacent services, which lifts the total. In Mordor Intelligence, value is counted only for corrugated board packaging sold for use in the United Kingdom, and the pricing path is validated through interviews and cross checks rather than being carried forward from a single index.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.13 B (2025) | |

| Industry Platform A | USD 19.06 B (2024) | This estimate is materially higher, and the spread is typically explained when broader corrugated packaging plus adjacent paper packaging formats are grouped together, and when pricing is carried forward from a high inflation year without enough buyer side validation. |

| Manufacturing Directory B | USD 8.29 B (2026) | This figure is closer to manufacturing turnover style sizing, which can undercount packaging value sold into the UK when parts of the value chain sit outside a narrow manufacturing definition or when trade and conversion flows are not fully reconciled. |

The table shows that the largest gaps come from what is included around corrugated board packaging and how pricing is converted into value across years. By keeping the scope limited to corrugated board packaging sales and then testing volumes and prices against multiple UK demand signals, our estimate stays traceable to clear inputs and can be rechecked when conditions change.

Key Questions Answered in the Report

How large is the United Kingdom corrugated board packaging market in 2026?

It stands at USD 12.6 billion, with a 3.85% CAGR projected to lift value to USD 15.21 billion by 2031.

Which end-user contributes the greatest volume?

Food categories lead with 34.92% of 2025 revenue thanks to broad grocery and produce needs.

What segment is growing the fastest?

E-commerce packaging shows the strongest momentum, tracking a 5.16% CAGR through 2031.

How is digital printing influencing packaging supply?

Digital presses enable low-volume, high-graphic jobs, fueling a 5.04% CAGR in that technology segment.

Why are triple-wall boards gaining traction?

Rising parcel weights and extended delivery distances push demand for triple-wall’s enhanced protection, supporting a 4.82% CAGR in that construction.

What key regulation is shifting material choices?

Extended Producer Responsibility fees on plastics spur brand owners to adopt corrugated alternatives for cost and sustainability advantages.

Page last updated on: