Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

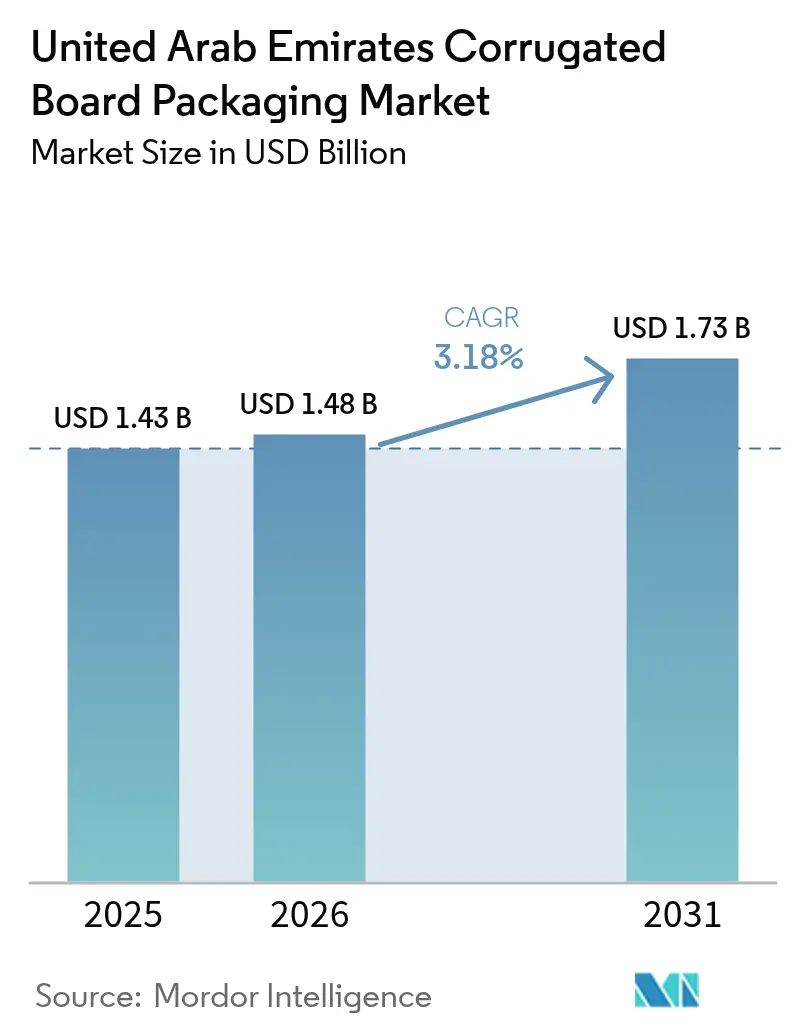

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Corrugated Board Packaging Market Analysis by Mordor Intelligence

The United Arab Emirates corrugated board packaging market size was valued at USD 1.43 billion in 2025 and estimated to grow from USD 1.48 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 3.18% during the forecast period (2026-2031). Strategic economic diversification, a USD 8.6 billion manufacturing sector, and a national ambition to lift non-oil exports by 50% collectively underpin stable demand for transit, retail, and premium corrugated solutions. Dubai’s transshipment role, handling 75% of national maritime traffic, multiplies packaging volumes as goods flow through re-export channels. In tandem, food processing output of 5.96 million t and rapid e-commerce expansion intensify the need for durable, high-graphics boxes. Brand owners further accelerate the adoption of digital printing and lightweight substrates to cut freight costs and elevate shelf appeal. Government customs exemptions on machinery and raw materials and competitive energy tariffs attract regional and global converters to scale local capacity.

Key Report Takeaways

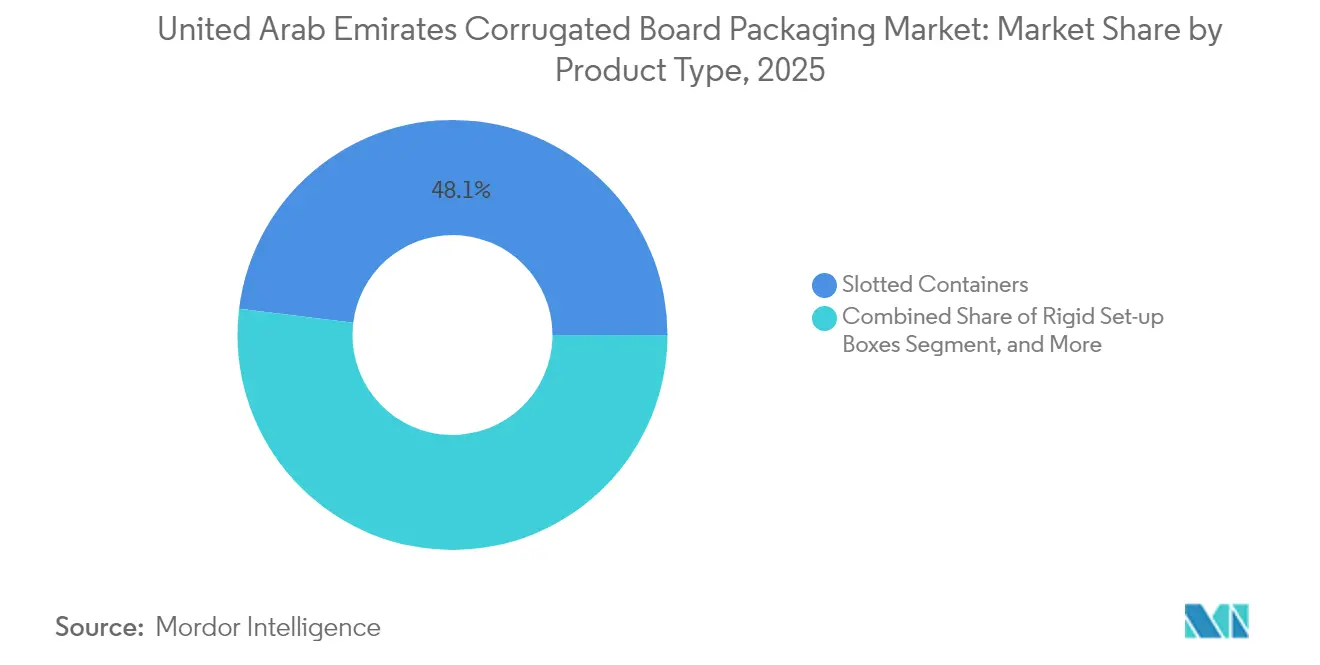

- By product type, slotted containers led with 48.05% of the United Arab Emirates corrugated board packaging market share in 2025; rigid set-up boxes will advance at a 5.34% CAGR to 2031.

- By end-user, food accounted for 32.20% of the United Arab Emirates corrugated board packaging market size in 2025, while e-commerce is forecast to expand at a 4.78% CAGR through 2031.

- By board construction, single-wall commanded 58.00% share of the United Arab Emirates corrugated board packaging market size in 2025, and triple-wall is projected to grow at 4.32% CAGR to 2031.

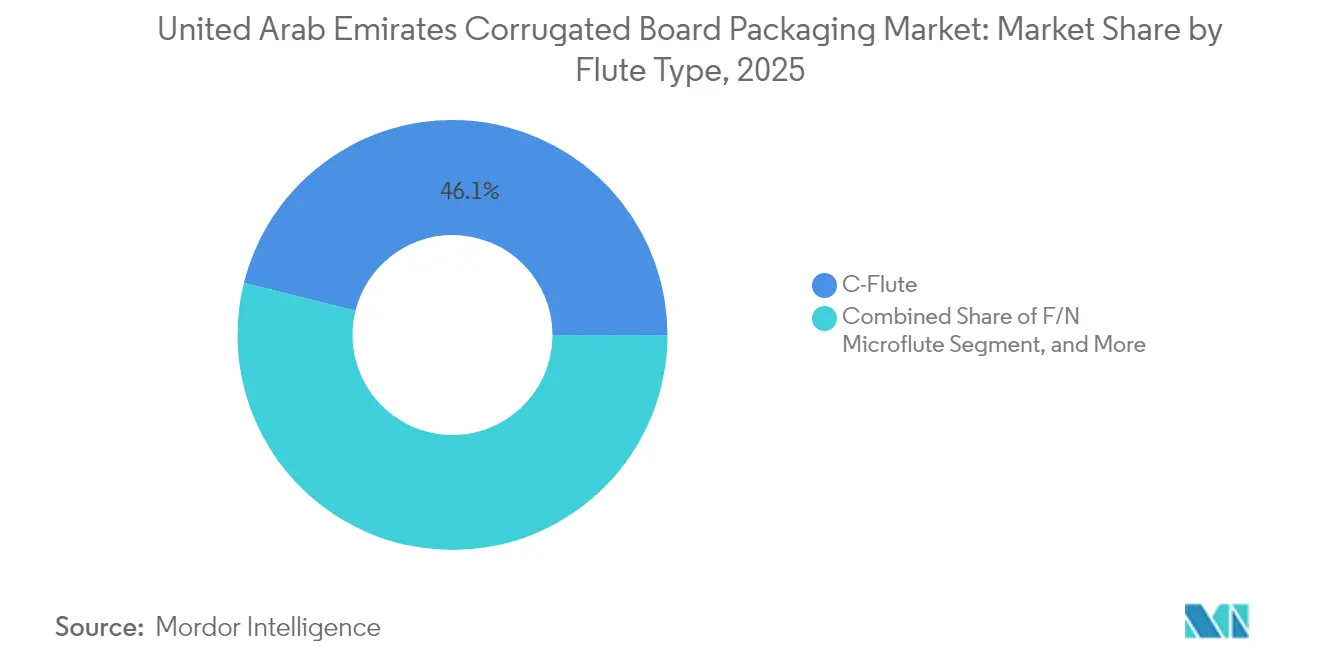

- By flute type, C-flute captured 46.10% of the United Arab Emirates corrugated board packaging market share in 2025; F/N microflute is poised for 4.74% CAGR through 2031.

- By printing technology, flexography held 38.10% share of the United Arab Emirates corrugated board packaging market size in 2025, whereas digital printing is rising at a 4.96% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Corrugated Board Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom driving high-volume transit packaging | +0.8% | National (Dubai & Abu Dhabi focus) | Short term (≤ 2 years) |

| Light-weighting and high-graphics printing in FMCG and electronics | +0.6% | National; GCC spillover | Medium term (2-4 years) |

| Regulatory push for plastic substitution with recyclable board | +0.5% | National; GCC alignment | Long term (≥ 4 years) |

| Logistics corridor expansion around Jebel Ali Port | +0.4% | Dubai-centric; Northern Emirates | Medium term (2-4 years) |

| Mars Mission and aerospace supply chains needing high-strength boxes | +0.2% | National; advanced zones | Long term (≥ 4 years) |

| Rapid growth of dark-store grocery start-ups | +0.3% | Urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom Driving High-Volume Transit Packaging

Online retail has re-shaped order fulfillment, with food e-commerce sales climbing to USD 1.07 billion in 2023 and grocery turnover reaching USD 36.5 billion in 2022. [1]U.S. Department of Agriculture FAS, “Food Processing Ingredients Annual,” APPS.FAS.USDA.GOV International Paper’s USD 40 million investment to upgrade European e-commerce lines signals global recognition of transport-intensive parcel formats. Because Dubai handles roughly 61% of GCC-bound cargo, corrugated demand multiplies as shipments are repacked for regional delivery. Dark-store grocery chains favor right-sized, rapid-assembly boxes that protect chilled items during last-mile runs. The United Arab Emirates corrugated board packaging market, therefore, benefits from higher unit counts per order and from value-added design services that enhance unboxing experiences.

Light-weighting and High-Graphics Printing in FMCG and Electronics

Digital presses now permit personalized graphics with run lengths tailored to promotion cycles, pushing digital printing to a 5.21% CAGR. [2]Billerud, “Digital Print – Personalised Corrugated Packaging Can Be the Future,” BILLERUD.COM Brands in the electronics and FMCG sectors leverage lighter microflute boards to lessen freight expense while preserving structural integrity. Automated warehouses and smart recycling lines financed under the USD 8.6 billion manufacturing agenda favor thinner substrates that run efficiently through high-speed conveyors. Packaging thus evolves from commodity containers to marketing assets that reinforce premium positioning at the point of delivery. The United Arab Emirates corrugated board packaging market increasingly revolves around collaborative structural design and variable data printing expertise.

Regulatory Push for Plastic Substitution with Recyclable Board

Government climate objectives, including a 2050 circular manufacturing roadmap, incentivize the adoption of fiber-based packaging. Alpha Emirates processes 84,000 t of recovered paper yearly, supporting recycled-content corrugated capacity. Anti-dumping duties on select paperboard imports demonstrate policymakers’ readiness to shield local mills from injurious pricing. Food processors, totaling about 2,000 firms, shift toward corrugated formats that satisfy GCC traceability and environmental labeling rules. As regulatory traction converges with recycling infrastructure, fiber-based formats gain share at the expense of single-use plastic crates.

Logistics Corridor Expansion Around Jebel Ali Port

Ongoing port deepening and free-zone warehousing upgrades sustain demand for heavy-duty bulk shippers and high-stacking strength boxes. Gulf Paper Manufacturing Company’s forthcoming 70,000 t capacity addition inside Jebel Ali Free Zone underscores the pull of proximity to export lanes. Large multinationals such as Smurfit Westrock, which booked USD 9.577 billion from its Europe-MEA-APAC division in 2024, align capacity planning to tap surging containerboard flows through Dubai. Efficient customs clearance and bonded logistics clusters further cement the United Arab Emirates’ role as a packaging gateway for the wider Middle East.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile kraftliner import prices and freight surcharges | -0.7% | National | Short term (≤ 2 years) |

| Fibre-quality inconsistency in domestic recycling streams | -0.4% | Industrial zones | Medium term (2-4 years) |

| Competition from returnable plastic crates in fresh produce | -0.3% | Food distribution centers | Medium term (2-4 years) |

| Aseptic-grade demands in pharma limit corrugated uptake | -0.2% | Pharma clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Kraftliner Import Prices and Freight Surcharges

The United Arab Emirates relies heavily on imported kraftliner, exposing converters to global price spikes that erode margins. Graphic Packaging’s 2024 sales slide to USD 8.807 billion, blamed partly on pulp and freight swings, mirrors pressure felt by local sheet feeders. [3]Graphic Packaging Holding Company, “Full-Year 2024 Results,” INVESTORS.GRAPHICPKG.COM Smurfit Westrock likewise flagged higher recovered fiber and energy costs, with delayed pass-through to box pricing. Customs exemptions help, yet cannot neutralize currency and bunker fuel volatility. Converters hedge through dual-sourcing and lightweighting, but price turbulence still clips the United Arab Emirates corrugated board packaging market growth rate.

Fibre-Quality Inconsistency in Domestic Recycling Streams

Although recycling capacity expands, variability in collected grades forces expensive cleaning and blending steps. Alpha Emirates’ 84,000 t mill illustrates commendable scale but still struggles with mixed-paper contamination. Gulf Paper’s 50,000 t annual waste-paper recovery runs into similar purity gaps, affecting runnability and box strength. Investment in optical sorters and AI-enabled inspection is underway, yet full standardization remains several years out. Until then, mill gate rejects and imported semi-chemical fluting fill supply gaps, trimming sustainable content targets for the United Arab Emirates corrugated board packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Packaging Drives Innovation

Rigid set-up boxes, though niche, are predicted to register the fastest 5.34% CAGR, reflecting rising demand for luxury electronics, confectionery, and gifting formats. Slotted containers preserved a 48.05% share of the United Arab Emirates corrugated board packaging market size in 2025, largely because they remain the universal choice for bulk shipping. Rigid set-up designs capitalize on high-graphics wraps and tactile finishes that command shelf premiums, enabled by digital print workflows and short fabrication cycles. Emirates Printing Press demonstrates local proficiency in folding carton and rigid set-up conversion, allowing brand owners to localize premium packs without long lead times.

Volume-driven die-cut containers and five-panel folders cater to e-commerce and electronics fulfillment, where easy assembly and precise fit reduce cushioning expense. Product innovation also extends to heavy-duty tray-lid formats for aerospace parts tied to the Mars program. As national export ambitions accelerate, specifications increasingly favor performance-engineered corrugated over generic brown boxes, ensuring the United Arab Emirates corrugated board packaging market maintains a balanced mix of mass and premium SKUs.

By End-User Industry: E-Commerce Reshapes Demand Patterns

Food processors consumed 32.20% of all corrugated in 2025, buoyed by 5.96 million t of domestic output spanning bakery, dairy, and savory snacks. E-commerce, however, will outpace every other vertical with a 4.78% CAGR as online grocery, fashion, and electronics retailers switch from plastic mailers to right-sized fiber boxes. Platform operators demand rapid art changes, serialized barcodes, and ship-ready tear strips, which favor digitally printed microflute. Beverage, personal care, and electrical goods, meanwhile, exploit high-strength double-wall cases to minimize damage claims during regional re-export runs.

Industrial, pharmaceutical, and petrochemical users add steady volume through anti-static liners, humidity shields, and tamper-evident tapes. Taken together, these mixed use-cases anchor steady base demand while permitting converters to diversify revenue. The United Arab Emirates corrugated board packaging market, therefore, exhibits both scale and specialization, hedging economic swings in any single vertical.

By Board Construction: Structural Innovation Meets Performance Demands

Single-wall maintained a 58.00% share of the United Arab Emirates corrugated board packaging market size in 2025, thanks to cost efficiency and adequate stacking strength for most FMCG cases. Triple wall is forecast to record a 4.32% CAGR, driven by aerospace payload, heavy machinery spares, and bulk chemical bag-in-box shipments that need compressive strength without weight penalties. Double wall satisfies intermediate loads for electronics and auto parts, offering a compromise between board weight and crush resistance.

Gulf Paper Manufacturing Company’s investment plan targets multi-wall capacity, betting on regional infrastructure and construction exports that require heavier grades. Logistics customers increasingly map board design to pallet patterns and container heights, engaging converters in value engineering to lower total landed cost. In sum, board construction choice is becoming a strategic lever for shippers, reinforcing demand for diversified sheet-feeding in the United Arab Emirates corrugated board packaging market.

By Flute Type: Microflute Technology Gains Traction

C-flute dominated with 46.10% share in 2025, prized for cushioning and stacking across food staples. F/N microflute is projected to advance at 4.74% CAGR as shelf-ready packs, gift boxes, and subscription parcels prioritize surface print quality and slim profiles. B-flute stays popular for wine, beverages, and mid-range appliances, where the balance between print area and rigidity is key. E-flute carves a niche in cosmetics and OTC pharma where point-of-sale display and tactile finishes matter.

Digital presses from Billerud show optimal results on microflute, aligning visual storytelling and inventory reduction. Recycled fiber input from Alpha Emirates, once refined, meets caliper needs for all flute combinations, strengthening domestic supply security. Consequently, flute selection is no longer a one-size gamble; it is data-driven, enabling converters in the United Arab Emirates corrugated board packaging market to tailor SKU-specific performance.

By Printing Technology: Digital Revolution Transforms Capabilities

Flexography retained 38.10% market share in 2025 on the back of long runs for beverages and staples. Digital printing, though, is rising at a 4.96% CAGR as SKU proliferation and seasonal campaigns require agile artwork swaps. Hybrid presses combining inkjet heads with inline die-cutting shrink order-to-delivery windows to as little as 24 hours, critical for flash promotions and influencer-driven product drops. Screen and offset methods survive for specialty gift attire and low-porosity coated liners.

Emirates Printing Press deploys both conventional and digital units, giving customers a continuum of cost-to-volume options. Variable QR codes, anti-counterfeit inks, and augmented-reality triggers are increasingly printed on high-touch packs in e-commerce, giving digital an edge. Investment payback is improved by reduced plate charges and minimized waste, catalyzing broader digital penetration in the United Arab Emirates corrugated board packaging market.

Geography Analysis

Dubai anchors demand by channeling 75% of the nation’s maritime traffic through Jebel Ali, translating to high throughput for export cartons, pallet bins, and reefer liners. The emirate also re-exports 61% of GCC-bound cargo, creating double-handling opportunities for value-added repacking. Abu Dhabi complements with aerospace clusters and state-backed manufacturing zones that stipulate advanced multi-wall grades for defense, aviation, and Mars-mission payload kits. Incentive programs granting duty-free machinery import and subsidized utilities lure global sheet integrators to both emirates, cementing their lead within the United Arab Emirates corrugated board packaging market.

Sharjah and Ajman leverage proximity to Dubai but differentiate through SME-oriented industrial estates offering quick-turn sheet-plant services for local confectionery, printing, and personal-care producers. Ras Al Khaimah adds mineral and cement exports, driving bulk bag-in-box and high-burst corrugated pallet surrounds. Government anti-injury duties on under-priced imports protect mills in all emirates, encouraging capex in recycling sortation and energy-efficient pulping.

Nationally, the USD 1 trillion transport infrastructure plan underscores packaging’s role in safeguarding value during multimodal transfers. Harmonized GCC labeling codes further integrate United Arab Emirates output into neighboring markets. As a result, regional converters position facilities within one-day truck distance of both seaport and desert hinterland to optimize freight and service lead times. Geography thus amplifies the resilience and growth prospects of the United Arab Emirates corrugated board packaging market.

Competitive Landscape

International groups dominate scale-driven containerboard but partner with regional players for market intimacy. Smurfit Westrock’s USD 9.577 billion Europe-MEA-APAC earnings equip it with procurement clout and R&D funding to push high-performance liners into the United Arab Emirates. Middle East Paper Company and Gulf Paper Manufacturing Company counter with responsive lead times, Arabic labeling fluency, and relationships inside free zones. Strategic thrusts focus on lightweighting, recycled content, and digital front-end services.

Technology is the new battleground. Billerud licenses modular inkjet engines to converters seeking personalized campaigns, while Alpha Emirates back-integrates into recovered-fiber sorting for circular credentials. E-commerce specialists experiment with glue-free crash-lock bases that cut pack time by 30%. Sustainability seals, carbon-footprint calculators, and blockchain traceability emerge as service differentiators beyond board price. The result is a moderately concentrated yet innovation-intensive United Arab Emirates corrugated board packaging market where collaboration often trumps outright rivalry.

M&A activity remains selective after Smurfit WestRock’s 2024 mega-deal, with local sheet-plants instead favoring JV structures inside free zones to scale without heavy balance-sheet stretch. Investors monitor freight cost volatility and fiber supply as key risk determinants. Overall, competitive dynamics balance scale efficiency with agile customization, aligning with the diversified demand base of the United Arab Emirates corrugated board packaging market.

United Arab Emirates Corrugated Board Packaging Industry Leaders

Arabian Packaging Co. LLC

World Pack Industries LLC

Universal Carton Industries LLC

Queenex Corrugated Carton Factory LLC

Falcon Pack Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Smurfit Westrock completed the merger of Smurfit Kappa and WestRock, listing on NYSE and LSE and expanding paper-based packaging reach into roughly 40 countries.

- May 2025: Middle East Paper Company posted Q1 2025 financials, reinforcing its trajectory in regional corrugated capacity scaling.

- April 2025: Ministry of Economy renewed industrial benefits, duty-free inputs and low energy tariffs, bolstering cost competitiveness for domestic converters.

- January 2025: Emirates Printing Press refreshed its website, showcasing folding-carton and rigid-box capabilities to capture premium segment growth.

United Arab Emirates Corrugated Board Packaging Market Report Scope

Corrugated board packaging is a flexible and economical way to safeguard and transport various goods. Its key advantages, such as lightweight, biodegradability, and recyclability, make it an essential component in modern life. The study tracks key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The UAE corrugated board packaging market is segmented by product type (slotted containers, die-cut containers, five-panel folder boxes, set up boxes, and other product types) and end-user industry (food, beverage, electrical goods, personal care and household care, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Slotted Containers |

| Die-cut Containers |

| Five-Panel Folder Boxes |

| Rigid Set-up Boxes |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Electrical and Electronics |

| Personal and Home Care |

| E-commerce |

| Other End-user Industries |

By Board Construction

| Single Face |

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Type

| C-Flute |

| B-Flute |

| E-Flute |

| F/N Microflute |

| Other Flute Types |

By Printing Technology

| Flexography |

| Digital |

| Other Printing Technologies |

| By Product Type | Slotted Containers |

| Die-cut Containers | |

| Five-Panel Folder Boxes | |

| Rigid Set-up Boxes | |

| Other Product Types | |

| By End-User Industry | Food |

| Beverage | |

| Electrical and Electronics | |

| Personal and Home Care | |

| E-commerce | |

| Other End-user Industries | |

| By Board Construction | Single Face |

| Single Wall | |

| Double Wall | |

| Triple Wall | |

| By Flute Type | C-Flute |

| B-Flute | |

| E-Flute | |

| F/N Microflute | |

| Other Flute Types | |

| By Printing Technology | Flexography |

| Digital | |

| Other Printing Technologies |

Key Questions Answered in the Report

How large is corrugated packaging demand in the United Arab Emirates today?

The United Arab Emirates corrugated board packaging market size is USD 1.48 billion in 2026 and is projected to reach USD 1.73 billion by 2031.

Which segment is growing fastest through 2031?

E-commerce packaging is forecast to post a 4.78% CAGR, outpacing every other end-user segment.

What board construction is most common for everyday shipping cartons?

Single wall accounts for 58.00% of current volume due to its balance of cost and performance.

How are sustainability policies influencing material choices?

Government targets for a circular economy and anti-plastic measures are shifting demand toward recycled-content corrugated solutions.

Which technology is disrupting traditional flexography?

Digital inkjet printing is rising at a 4.96% CAGR, enabling personalized graphics and fast turnaround times.

Why are kraftliner prices a critical issue for converters?

The nation relies on imported kraftliner, so freight surcharges and global pulp swings directly hit input costs, trimming margins and elevating price volatility.

Page last updated on: