Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

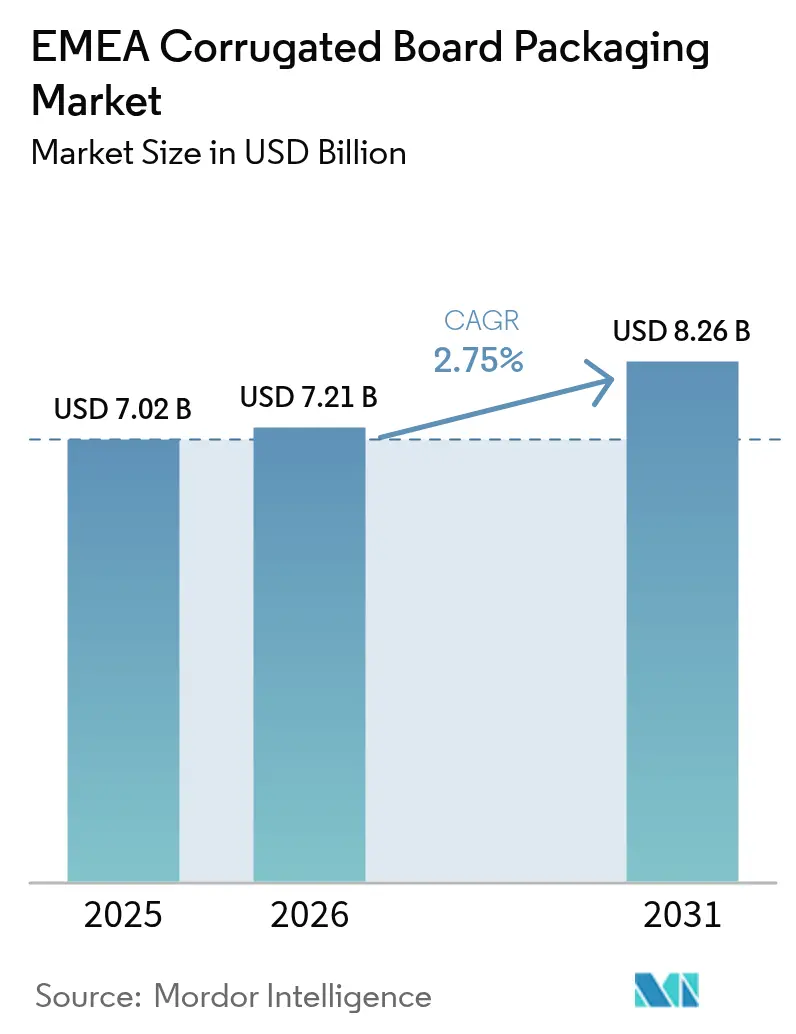

| Base Year Market Size (2025) | USD 7.02 Billion |

| Market Size (2026) | USD 7.21 Billion |

| Market Size (2031) | USD 8.26 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

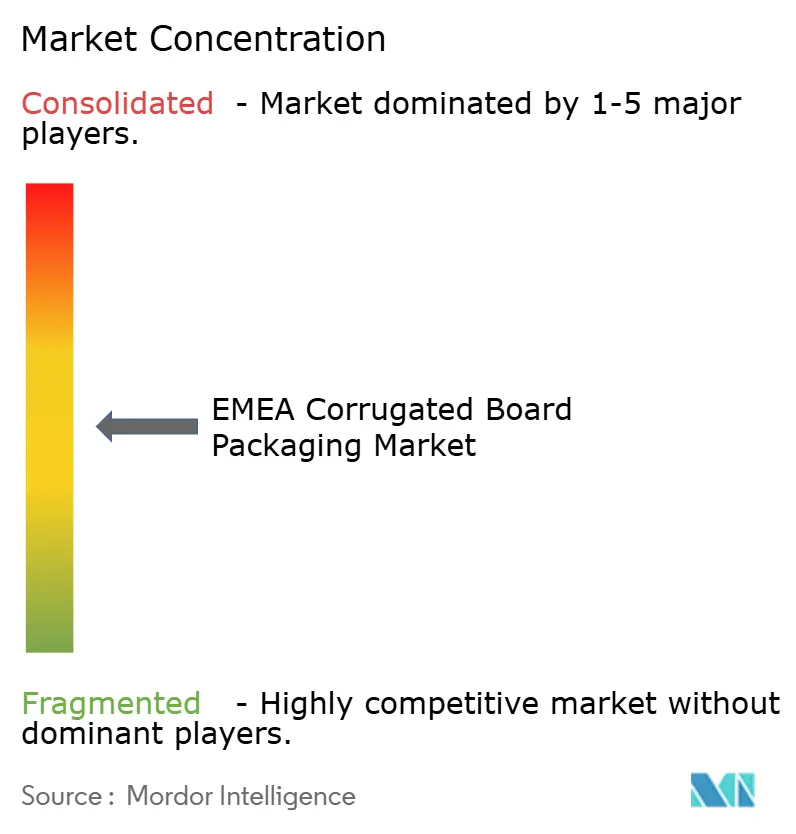

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EMEA Corrugated Board Packaging Market Analysis by Mordor Intelligence

EMEA corrugated board packaging market size in 2026 is estimated at USD 7.21 billion, growing from 2025 value of USD 7.02 billion with 2031 projections showing USD 8.26 billion, growing at 2.75% CAGR over 2026-2031. This measured expansion reflects a mature infrastructure that is upgrading for e-commerce parcel flows, EU sustainability mandates, and energy-efficiency retrofits. Heightened regulatory pressure from the Packaging and Packaging Waste Regulation favors fiber-based substrates, while volatile prices for energy, old corrugated cardboard (OCC), and kraftliner constrain aggressive capacity additions. Consolidation, highlighted by International Paper’s USD 9.9 billion purchase of DS Smith, underpins restructuring toward vertically integrated mill-to-box models that defend margins in an inflationary cost environment. Africa’s urban retail boom and Middle Eastern diversification agendas add incremental volume, but Europe remains the demand anchor and the technology hub for coating, digital printing, and AI-based right-size packaging solutions. The EMEA corrugated board packaging market is thus balancing defensive cost control with selective growth bets in fast-moving, sustainability-linked niches.

Key Report Takeaways

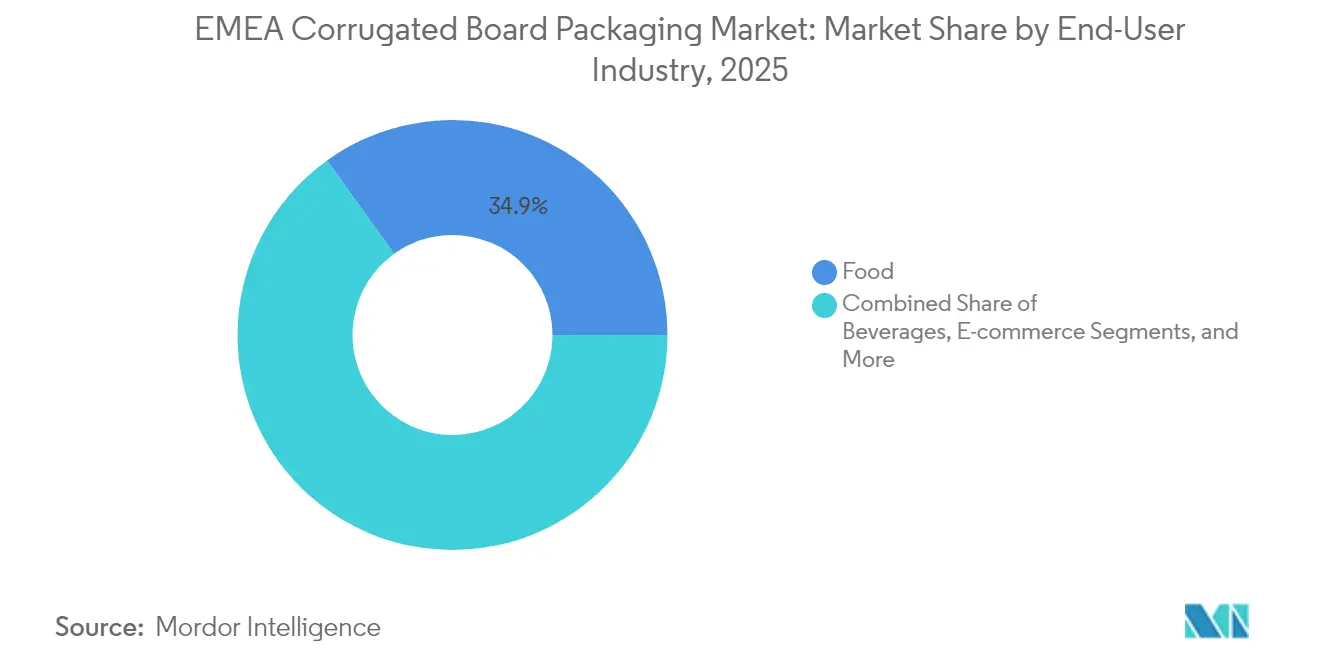

- By end-user industry, food packaging led with a 34.92% revenue share in 2025, while e-commerce applications are advancing at a 4.12% CAGR through 2031.

- By flute type, C-Flute captured 31.95% of the 2025 pie, whereas F/N microflute configurations are set to expand at 3.82% CAGR.

- By board construction, single wall accounted for 38.87% of sales in 2025; triple wall is forecast to post a 3.29% CAGR to 2031.

- By printing technology, flexography held 28.02% share in 2025, and digital printing is registering the fastest 4.73% CAGR.

- By geography, Europe commanded 81.78% of 2025 demand, yet Africa records the swiftest 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

EMEA Corrugated Board Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding e-commerce parcel volumes | +0.8% | Europe core, expanding to MEA cities | Medium term (2-4 years) |

| EU PPWR-driven demand for recyclable packaging | +0.6% | Europe, spillover to MEA markets | Long term (≥ 4 years) |

| Fresh produce cold-chain shift to fiber crates | +0.4% | Western Europe early adopters | Medium term (2-4 years) |

| AI-enabled right-size packaging adoption | +0.3% | EU pilots, MEA trials | Short term (≤ 2 years) |

| Water-based barrier coatings replacing trays | +0.2% | Europe core, tech transfer to MEA | Medium term (2-4 years) |

| EU CBAM incentives for local recycled liner | +0.2% | Europe, indirect MEA effect | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding e-commerce parcel volumes

Online retail added new corrugated demand streams as cross-border transactions in the EU climbed 23% in 2024. Parcel formats favor protective designs, extra branding space, and fit-to-product geometry, all of which command premium unit prices. Urban fulfillment hubs now prefer agile sheet plants over large suburban complexes, pushing converters to deploy modular corrugators with rapid changeovers. Brands such as Zalando demonstrated 15% material savings and improved print aesthetics after switching to custom-sized water-based coated boxes in 2024. Steady growth in same-day delivery further accelerates the EMEA corrugated board packaging market, translating parcel velocity into reliable order backlogs for local plants.

EU PPWR-driven demand for recyclable packaging

The 2024 regulation mandates 90% recycling rates for corrugated formats by 2030 and elevates average recycled fiber content benchmarks to 85%. Corrugated already delivers 88%, giving it a compliance head-start over plastic substrates. Producers with advanced de-inking systems are locking in price premiums for high-whiteness recycled liner. The policy also nudges Middle Eastern and African subsidiaries of European brands toward fiber adoption to maintain uniform sustainability claims. As a result, the EMEA corrugated board packaging market embeds regulatory pull rather than subsidy push, curbing risk profiles for new investments.

Fresh produce cold-chain shift to fiber-based crates

Moisture-resistant coatings enable corrugated crates to withstand humidity without delamination, supplanting returnable plastic and wood. Dutch flower exporters eliminated 40% of plastic crates in 2024, cutting logistics costs by 25% and divorcing supply chains from costly back-haul loops. Produce shippers in Spain and Italy now specify fiber crates that integrate into municipal curbside recycling, satisfying retailer zero-waste commitments. The pattern is mirrored in North African vegetable corridors serving EU supermarkets. Cold-chain expansion therefore becomes a throughput catalyst for the EMEA corrugated board packaging market.

AI-enabled right-size packaging adoption

Corrugators equipped with on-demand digital cut-score systems and learning algorithms reduce void fill, improve cube utilization, and trim freight emissions. The European Patent Office logged 127 AI-centric packaging patents in 2024. [1] European Patent Office, “Patent Applications in Packaging Technology 2024,” Epo.org Early adopters negotiate service-based contracts, charging clients on a cost-per-saved-gram basis, creating novel revenue pools. Capital intensity is sizable, but higher order margins and client stickiness offset payback periods. The technology is scaling from flagship distribution centers to regional hubs, lifting average selling prices in the EMEA corrugated board packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OCC and kraftliner price volatility | -0.5% | Global, pronounced in Europe | Short term (≤ 2 years) |

| Substitution by reusable/flexible formats | -0.3% | Europe core, emerging MEA | Medium term (2-4 years) |

| Energy-price shock hitting corrugator OPEX | -0.4% | Europe core, limited MEA | Medium term (2-4 years) |

| War-related mill outages in Eastern Europe | -0.2% | Eastern Europe, spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OCC and kraftliner price volatility

OCC prices swung 35% in 2024, compressing gross margins for converters locked into annual contracts. [2]Confederation of European Paper Industries, “Raw Material Price Index 2024,” Cepi.org Hedging mechanisms have limited liquidity, forcing mid-tier box plants to renegotiate pass-through clauses or risk solvency. Kraftliner also tracks pulp and energy costs, injecting unpredictability into input budgets. The turbulence intensifies consolidation as scaled integrators leverage broader fiber baskets and currency hedges, while smaller independents exit or specialize. Such swings subtract 0.5 percentage points from the projected CAGR for the EMEA corrugated board packaging market.

Energy-price shock hitting corrugator OPEX

EU industrial electricity prices climbed 28% in 2024. Corrugators respond by installing high-efficiency steam recovery, variable-frequency drives, and biomass boilers. Capex payback stretches when energy markets cool, deterring investment timetables. Plants in Poland, Hungary, and Romania gain relative advantage due to lower wholesale rates, prompting production re-shoring from high-cost Western hubs. The shock therefore weighs on competitiveness yet seeds a longer-run technology refresh in the EMEA corrugated board packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Resilient Food Shipments Meet Digital Retail Surge

The food segment generated a dominant 34.92% share of the EMEA corrugated board packaging market in 2025, anchored in agricultural exports, ambient grocery, and chilled ready-meals. Producers value corrugated’s capacity to absorb condensation without losing compressive strength, fulfilling stringent hygiene standards while supporting brand visibility through high-resolution graphics. Lightweight crates with water-based coatings now penetrate deli and bakery aisles, displacing PET clamshells. The e-commerce channel exhibits the fastest 4.12% CAGR to 2031, driven by direct-to-consumer grocery boxes, fashion returns logistics, and electronics deliveries. Packaging needs here skew toward quick-set locks, rip-tabs, and integrated returns tape that shrink fulfillment labor costs. Synergies arise when food brands cross-list on online marketplaces, requiring dual-purpose SKUs that protect perishables and present attractively on the doorstep, thereby reinforcing share gains for the EMEA corrugated board packaging market.

A stable beverage sub-segment demands reinforced section dividers to shield glass and aluminum multipacks, with inventory switching toward post-consumer recycled liner to meet corporate carbon pledges. Personal care and cosmetics lines select microflute boxes that blend structural integrity with near-offset print quality, uplifting unboxing theatrics. Industrial parts now adopt fold-to-fit die-cuts that replace plywood, lowering weight and easing customs clearance. Electrification in automotive components invites antistatic coatings for battery modules, adding premium value layers without heavy material additions.

By Flute Type: Strength Versus Shelf Appeal

C-Flute maintained 31.95% share in 2025 for its all-round cushioning and stacking competencies, making it a default choice for case-ready foods and durable goods. However, microflute variants (F and N) are growing 3.82% annually on the strength of superior print registration and slimmer wall thickness that cuts freight costs. Specialty converters pair microflute with high-white liners, targeting luxury chocolates, personal electronics, and point-of-sale trays. A-Flute persists in heavy-duty agriculture bins for melons and root vegetables that face vertical stacking in cold stores. B-Flute wins when precise die-cut scoring is needed for shelf-ready displays. E-Flute straddles cartonboard and corrugated territories, servicing small appliances and specialty teas that crave tactile stiffness. This diversification of flute profiles diversifies SKUs and spreads capex across corrugators, sustaining innovation momentum in the EMEA corrugated board packaging market.

Material science developments allow hybrid flute combinations where an E/B double wall mates print surface with crush resistance, giving converters modular setups to serve both e-commerce apparel and industrial spares without switching board suppliers. The approach elevates customer retention, especially when paired with AI pattern libraries that recommend flute mixes from product weight databases.

By Board Type: Light Wall Economics Confront Heavy Wall Performance

Single wall boards delivered 38.87% of 2025 shipments thanks to their lean fiber usage and satisfactory edge crush specifications for standard distribution networks. New high-performance liners allow basis-weight downgrading without sacrificing compression metrics, thus improving cost-to-strength ratios. Triple wall boards, expanding at 3.29% CAGR, find uptake in white-goods packaging, automotive subassemblies, and bulk-chemicals plastic drums. Multinationals now replace timber crates on trans-Mediterranean lanes with triple wall corrugated that folds flat on the backhaul, cutting container repositioning fees. Double wall remains the middle ground, useful for moderate weight combined with branding surfaces, while single face proves valuable for void-fill pillows in high-velocity parcel hubs.

Circularity targets exert fresh pressure to lighten designs, leading to computational board engineering that simulates corrugation angles and fiber orientation. The advances further entrench the EMEA corrugated board packaging market as a materials engineering ecosystem rather than a commodity craft.

By Printing Technology: Flexo Dominance Meets Digital Customization

Flexography accounted for 28.02% of printed square meters in 2025 because it remains cost-efficient on runs above 20,000 units. Continuous improvements in anilox engraving and sleeve changeover shorten wash-up downtime, reinforcing its economic edge. Digital printing, however, grows 4.73% per year, catalyzed by demand for serialized graphics, seasonal promotions, and subscription box personalization. The technology closes the gap on per-unit cost at volumes below 5,000, making it ideal for microbrands and regional e-grocers. Hybrid lines integrate inkjet heads on flexo stations, letting converters switch mid-shift without re-rigging. Litho-lamination maintains a niche in premium spirits and beauty cartons requiring photorealistic imagery. Screen printing holds for functional layers such as moisture barriers and smart-label antennas. Investments in digital front-end workflow and variable data algorithms illustrate how the EMEA corrugated board packaging market is embracing software-driven print ecosystems.

Geography Analysis

Europe set the tone for the EMEA corrugated board packaging market by absorbing 81.78% of 2025 demand and fielding cutting-edge regulatory frameworks that reward recyclable substrates. Germany, France, and the United Kingdom together account for over half of regional volume, driven by consumer packaged goods manufacturing and dense e-commerce parcel flows. Consolidation echoes across the continent: International Paper merging with DS Smith and Mondi buying Schumacher converters reshape the supplier map, while the CBAM overlay amplifies the relative appeal of local recycled liner. Eastern European mills in Poland and the Czech Republic gain share as near-shore fiber sources because they blend lower energy tariffs with EU compliance credentials, feeding Western box plants that optimize logistics radiuses around 500 km.

Africa contributes a modest baseline today yet delivers the fastest 4.42% CAGR through 2031, powered by Nigeria’s population growth, Egypt’s Suez-centric trade corridors, and South Africa’s organized retail. Modern retail chains standardize pallet configurations, compelling suppliers to shift from shrink film bundles to die-cut corrugated trays. Cold-chain investments for pharmaceuticals and strawberries create niches for barrier-coated boards capable of withstanding humid docks at Mombasa and Durban. Local mills face fiber scarcity, stimulating imports of recycled containerboard from Iberian and Italian mills, which in turn capitalize on excess capacity. Public-private recycling partnerships emerge in Nairobi and Accra, exerting spillover benefits on the broader EMEA corrugated board packaging market.

The Middle East bridges the two continents with energy-cost advantages critical for steam-intensive corrugators. Saudi Arabia’s Vision 2030 industrial clusters and the United Arab Emirates’ e-commerce free zones catalyze plant expansions targeting food, consumer electronics, and fresh flower re-exports. Turkey positions itself as a transcontinental hub feeding both European supermarkets and North African processors. Regional converters invest in photovoltaic roofs and gas-turbine cogeneration to soften exposure to global gas swings. Combined, these dynamics diversify the revenue base and cushion cyclicality in the EMEA corrugated board packaging market.

Regulatory Landscape

In Europe, Regulation (EU) 2025/40 on packaging and packaging waste (PPWR) entered into force on 11 February 2025 and applies from 12 August 2026, replacing the prior Packaging and Packaging Waste Directive 94/62/EC after a transition period. For corrugated board packaging placed on the EU market, the PPWR raises compliance requirements around recyclability, labeling, and technical documentation, pushing converters and brand owners to formalize declarations of conformity and supply-chain data capture.

Implementation detail has kept tightening. The European Commission issued interpretive guidance on 10 June 2026 (OJ C/2026/3084) to support consistent application across Member States. Outside the EU, Middle East harmonization efforts are visible through standards bodies such as the GCC Standardization Organization, which adopted GSO 2825:2026 on 30 April 2026 and includes technical requirements for paper and cardboard packaging for specific end uses such as animal feed, adding another layer of specification management for exporters serving GCC markets.

Value Chain Analysis

The EMEA corrugated board packaging value chain begins with recovered fiber (OCC) collection and sorting, virgin pulp and kraftliner inputs, and chemical additives used in strength and barrier solutions. These feed containerboard mills, which are followed by corrugators that convert liner and medium into sheetboard and finished cases. Vertical integration is a defining feature across Europe: groups such as Mondi and Smurfit WestRock operate mill-to-box networks to stabilize input availability and manage cost volatility, while independent converters often depend on sheet feeders and open-market containerboard procurement.

A parallel supply route comes from specialist sheetboard suppliers such as Progroup AG, which focuses on supplying corrugated sheetboard to independent packaging converters rather than competing broadly in finished boxes. Trade-press evidence points to a tighter supply environment shaped by consolidation and operating discipline: European containerboard production in 2025 fell 1.6% and stayed below 2021 levels, while import penetration reached record levels in 2025, driven by low-priced arrivals from China, Indonesia, and Turkey. This has increased emphasis on procurement contracts, lead-time reliability, and price management, and it has pushed converters to balance security of supply with exposure to imported grades when domestic price hikes are delayed (as noted in Italy, where implementation of announced containerboard increases was postponed into July 2026).

Competitive Landscape

The landscape is moderately consolidated. Vertical integration dominates strategy, as players link recycled liner mills with sheet-feeding corrugators to hedge OCC cost volatility. International Paper’s absorption of DS Smith introduced a pan-European platform that leverages U.K. and Italian recycling assets to supply German and French box plants. Smurfit Kappa counters with EUR 20 million (USD 23.39 million) earmarked for fast-response converting cells that shorten lead times in e-commerce boxes. Mondi, after acquiring Schumacher sites, deploys smart warehouse management systems that slash finished-goods inventory days, strengthening price discipline.

Smaller, innovation-led firms target white spaces in digital printing and barrier-coated trays. THIMM Group’s water-based coatings substitute greaseproof plastic trays for pizza chains, while VPK Group’s Product Carbon Footprint Calculator embeds emission data into quotes, meeting brand audits at the RFQ stage. Competitive advantage, therefore, tilts toward data-rich service models rather than sheer capacity. Vertical sustainability claims-FSC forestry, PEFC sourcing, ISO 14064 carbon-accounting-become table stakes in tenders. The evolving playbook positions the EMEA corrugated board packaging market as a battleground where scale efficiencies intersect with niche agility.

EMEA Corrugated Board Packaging Industry Leaders

Smurfit WestRock

Mondi plc

International Paper Company

Saica S.A.

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity sits at the intersection of PPWR compliance execution (applying from 12 August 2026) and productivity-driven modernization. Converters with scalable documentation systems, material traceability, and design-for-recycling capabilities can support brand owners that need uniform EU-market compliance across multi-country operations. Investments in automation and right-size packaging can also help convert regulatory pressure into differentiated service offerings.

Capital deployment across Europe further indicates where capability upgrades are being prioritized. DS Smith announced a DKK 100 million investment in March 2026 to expand and upgrade its Grenaa, Denmark packaging facility, including an advanced rotary die-cutting line that lifts capacity by 15 million square meters annually, aligned with e-commerce-ready formats and faster changeovers. Smurfit WestRock announced a EUR 600 million investment programme across French operations in June 2026 focused on modernization and decarbonization, while Eastern Europe continues to attract new build activity such as Grembox starting construction of a Bytom, Poland site (PLN 110 million) aimed at commissioning in 2027. Together, these moves highlight opportunities in high-speed converting, microflute and premium print runs, and barrier-coated solutions for cold-chain and food applications, where supply security and lead times have become more valuable following consolidation.

Recent Industry Developments

- July 2026: Smurfit WestRock confirmed the closure timeline for its SSK paper mill in Birmingham, UK, effective 27 July 2026. The move removes higher-cost paper capacity from the regional network and reinforces the shift toward footprint optimization alongside targeted investment in core converting and packaging sites.

- June 2026: Smurfit WestRock announced a EUR 600 million investment programme across its French operations over three to five years to modernize assets and advance decarbonization. The commitment concentrates capital into efficiency and sustainability upgrades that can improve cost position and strengthen supply reliability for large FMCG and e-commerce customers in Western Europe.

- February 2025: International Paper finalized its USD 9.9 billion acquisition of DS Smith, creating a larger integrated platform across Europe with combined recycling, paper, and converting assets. The transaction intensified consolidation dynamics and increased the role of mill-to-box integration in managing OCC and energy volatility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market means the value of corrugated board packaging sold and used across EMEA, counted where corrugated packaging is supplied for packing, shipping, and distribution needs across end-user industries.

Scope exclusions: Folding cartons and other non-corrugated paper packaging formats are not counted unless they are part of a corrugated board packaging structure.

Segmentation Overview

- By End-User Industry

- Food

- Processed Foods

- Fresh Food and Produce

- Beverages

- E-commerce

- Electrical and Electronics

- Personal Care and Cosmetics

- Other End-User Industries

- Food

- By Flute Type

- A-Flute

- B-Flute

- C-Flute

- E-Flute

- F/N Microflute

- Other Flute Types

- By Board Type

- Single Face

- Single Wall

- Double Wall

- Triple Wall

- By Printing Technology

- Flexography

- Digital Printing

- Litho-lamination

- Screen Printing

- Other Printing Technologies

- BY Geography

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for the market model and to keep assumptions realistic at a country and sub-region level inside EMEA. We relied on public sources that explain packaging demand and paperboard supply patterns, such as Eurostat manufacturing and trade series, the UN Comtrade database, national statistics offices across Europe and MEA, and the European Commission policy pages covering packaging and recycling requirements.

To link packaging consumption to activity, we also reviewed disclosures and publications from industry associations and standards bodies, plus peer-reviewed papers on corrugated materials, recycling rates, and performance by flute and board structure. Company annual reports, investor presentations, and reputable business press were used to understand capacity moves, price direction, and end-market exposure, then those signals were cross-checked against paid subscriptions that support company financials, patent lookups, and shipment-level import and export views where applicable. These sources are illustrative, and other public datasets and documents were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was run to pressure-test the desk inputs and close gaps on how corrugated board packaging demand is split by end-use and by format choices (including flute preference and board construction). We spoke with packaging converters, raw-material-linked stakeholders, distributors, and large buyers across key EMEA corridors, then used those conversations to confirm pricing logic, utilization direction, and substitution behavior during cost swings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | |

| Mid tier: 45% | Functional/Unit leaders: 40% | |

| Smaller Players: 20% | Managers: 42% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where packaging demand is reconstructed from end-market output and trade flows, then converted into corrugated packaging value using price and mix inputs. In practice, we map major corrugated demand pools across food and beverage, e-commerce shipments, consumer goods, and industrial goods, then apply market-specific share and usage rates so the final number stays connected to real consumption.

To keep totals grounded, we corroborate the model with selective bottom-up approximations, such as roll-ups from a sample of converter revenues, channel checks on average selling price movement, and country-level volume indicators when available. Key inputs include kraftliner and recycled containerboard price direction, old corrugated containers (OCC) availability trends, manufacturing output and retail activity signals, e-commerce parcel growth indicators, and changes in recycling and packaging compliance expectations in Europe and parts of MEA. Forecasting uses scenario analysis supported by a simple multivariate regression on the most stable demand drivers, and then the forecast path is adjusted based on what interviewees expect for pricing, mix shifts between flute types, and capacity utilization.

Where direct datapoints are missing for smaller markets, gaps are handled using proxy indicators (such as closely linked industrial production or import patterns) before normalization so country totals roll up cleanly to EMEA without double counting.

Data Validation & Update Cycle

Validation is done by triangulating the model against independent signals, including trade movement consistency, board and paper price cycles, and whether end-market activity trends can realistically support the implied packaging demand. Outliers are flagged when a country result moves faster than its underlying drivers, then assumptions are revisited, and if needed, respondents are re-contacted to explain the variance.

Before sign-off, outputs go through step-by-step analyst reviews that check unit logic, currency conversion timing, and whether mix and price changes are applied consistently across the time series. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp fiber cost moves, regulatory changes, or major capacity additions. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Emea Corrugated Board Packaging Market Estimate Compared With Other Published Estimates

Published market sizes for EMEA corrugated board packaging often vary because the scope is not always aligned, and the pricing and mix assumptions can be updated at different times. Differences also come from how countries are grouped under EMEA, and whether the estimate is tied to packaging consumption signals or mainly to production-side indicators.

In many cases, the spread is explained by what gets counted inside corrugated packaging (for example, whether only finished corrugated packaging sales are counted, or whether broader paper packaging and converting services are pulled in), and by how quickly fiber and energy driven pricing is assumed to normalize. Another common gap driver is refresh cadence, where an estimate can lag the latest OCC and kraftliner price movement and the latest end-use demand shifts. For this reason, the 2025 base year value is anchored to consumption and sales checks and then re-validated through interview feedback, which is a modeling choice used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.02 B (2025) | |

| Industry Association A | USD 6.40 B (2025) | This figure appears to apply a narrower scope that emphasizes converter output in selected countries, and it can understate cross-border shipments and imported packaging used by large buyers. |

| Trade Journal B | USD 8.10 B (2025) | This estimate likely uses a broader definition that blends corrugated packaging with adjacent paper packaging activities, and it may assume a higher average selling price progression during fiber and energy cost volatility. |

Looking across the table, the main reason for the range is not one single math step, but a mix of scope choices and how pricing is carried through the base year. When we hold geography and product coverage steady, then tie the value build to end-use demand signals with practical checks on price and mix, the resulting market size becomes easier to trace and repeat over time.

Key Questions Answered in the Report

What is the current value of the EMEA corrugated board packaging market?

The market is worth USD 7.21 billion in 2026 and is projected to reach USD 8.26 billion by 2031.

Which end-use segment uses the most corrugated packaging in EMEA?

Food applications dominate with 34.92% share, bolstered by cold-chain produce and grocery shipments.

Why is digital printing growing in corrugated packaging?

Brands want mass customization for e-commerce and seasonal campaigns, pushing digital print to a 4.73% CAGR.

How are EU regulations affecting packaging choices?

The PPWR and CBAM favor recyclable, locally produced fiber solutions, shifting volume away from plastics and imports.

Which geography is expanding fastest within EMEA?

Africa is growing at 4.42% CAGR due to urbanization and modern retail infrastructure.

Page last updated on: