Corrugated Beverage Carrier Board Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

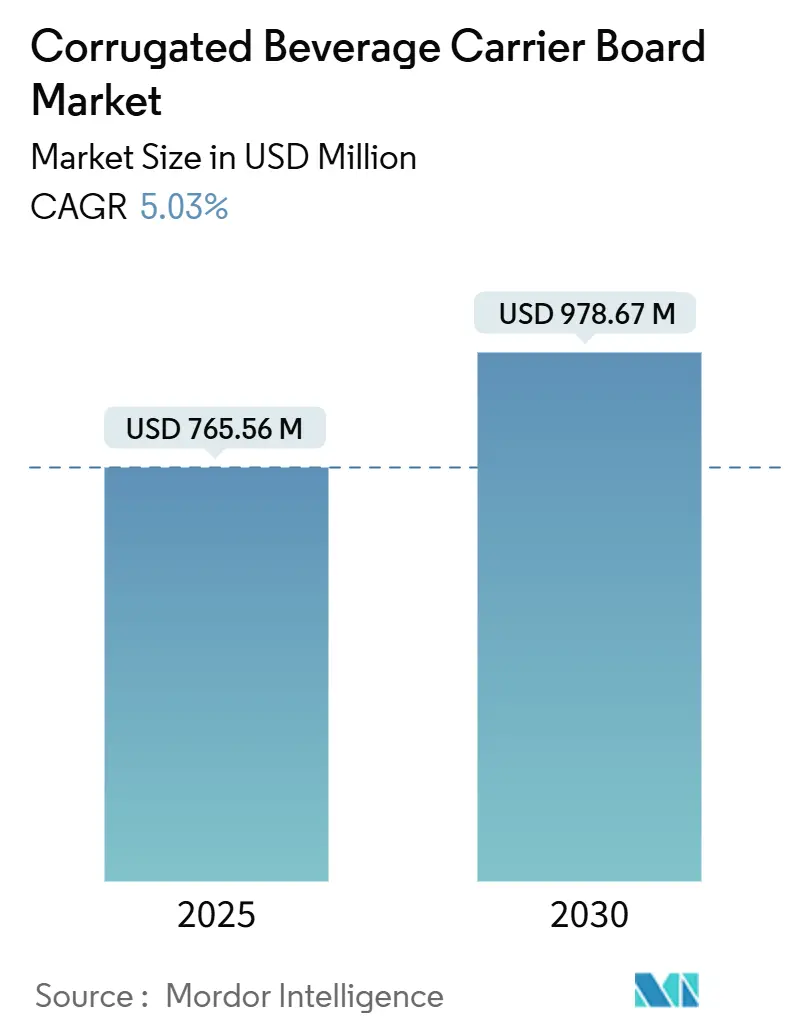

| Market Size (2025) | USD 765.56 Million |

| Market Size (2030) | USD 978.67 Million |

| Growth Rate (2025 - 2030) | 5.03% CAGR |

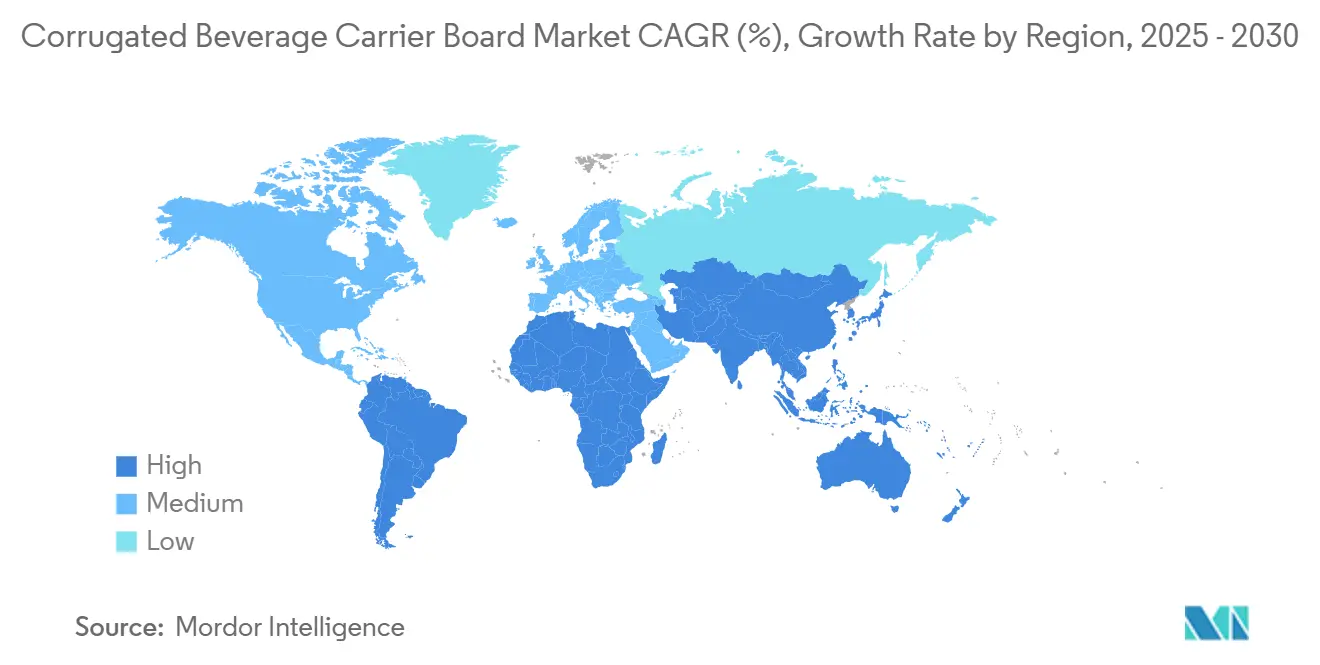

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Beverage Carrier Board Market Analysis by Mordor Intelligence

The corrugated beverage carrier board market size stands at USD 765.56 million in 2025 and is forecast to advance to USD 978.67 million by 2030 at a 5.03% CAGR. Strong demand for sustainable multi-pack formats, ongoing premiumization in craft beverages, and e-commerce shipping specifications combine to lift volumes, while recycled-content mandates accelerate the migration away from plastic carriers. North America anchors present sales thanks to its mature brewery network and strict packaging rules, yet Asia-Pacific delivers the sharpest growth as brand owners expand regional filling capacity and modern retail formats. Hybrid kraft/white-top boards post the fastest grade gains because they blend shelf impact with structural strength, and flexible converting lines unlock economical short production runs that suit rising SKU variety. Producers use vertical integration and mill modernization programs to soften recycled linerboard price swings and to meet looming PFAS-free adhesive deadlines, positioning the corrugated beverage carrier board market for steady, value-driven expansion.[1]United States Department of Agriculture Foreign Agricultural Service, “European Union Finalizes New Rules for Packaging and Packaging Waste Reduction,” FAS.USDA.GOV

Key Report Takeaways

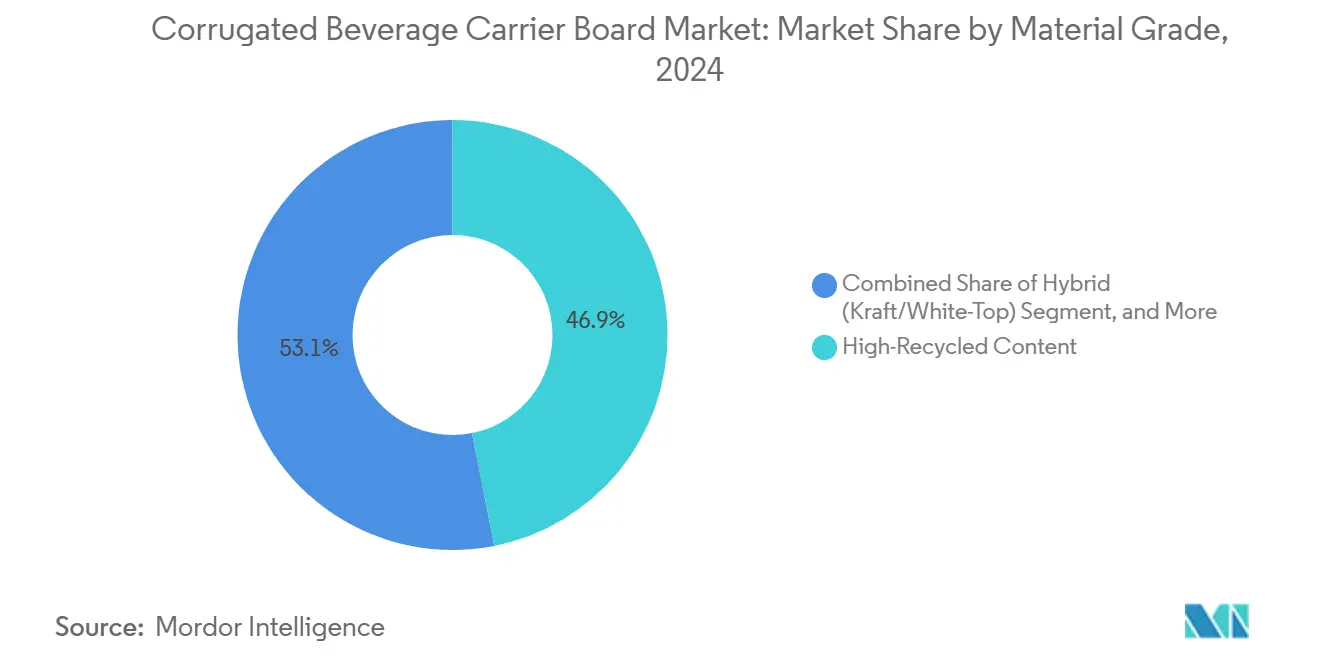

- By material grade, high-recycled content captured 46.89% of the corrugated beverage carrier board market share in 2024.

- By beverage type, the corrugated beverage carrier board market size for the dairy and plant-based drinks segment is projected to grow at a 6.07% CAGR between 2025-2030.

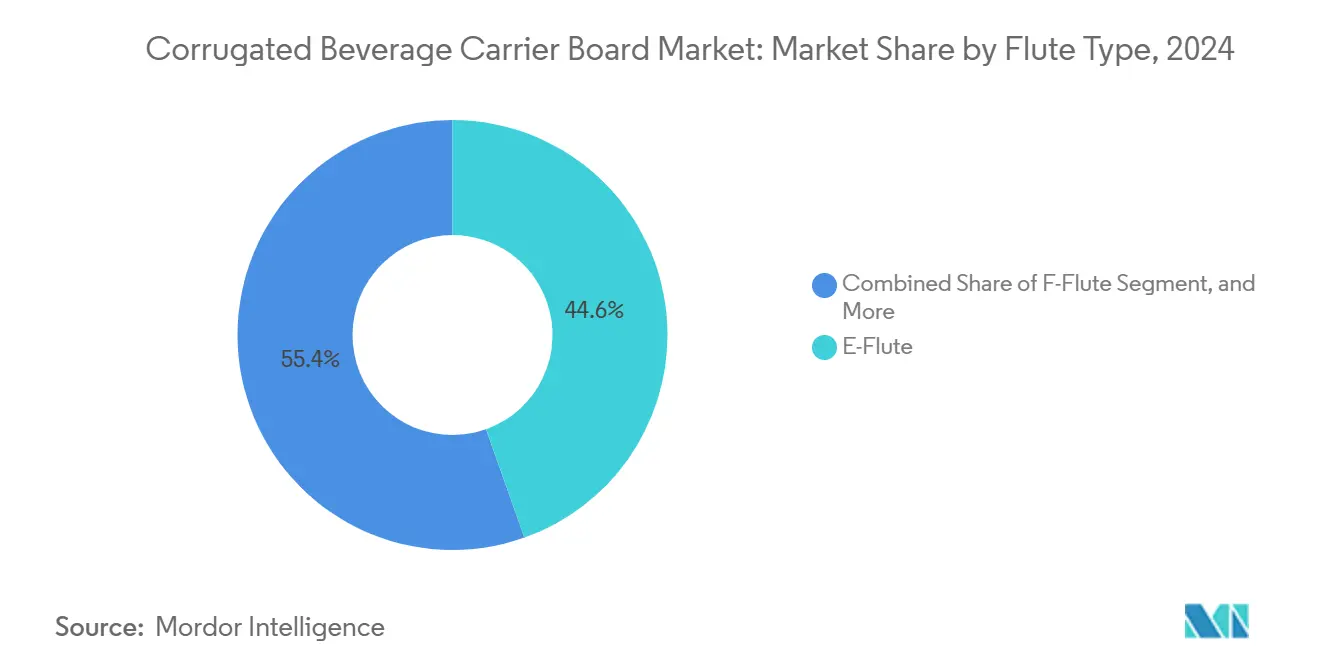

- By flute type, E-flute captured 44.56% of the corrugated beverage carrier board market share in 2024.

- By end-user, the corrugated beverage carrier board market size for the co-packers segment is projected to grow at a 6.54% CAGR between 2025-2030.

- By geography, North America captured 31.96% of the corrugated beverage carrier board market share in 2024.

Global Corrugated Beverage Carrier Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising craft-beer multi-pack demand | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Growth in on-the-go beverage consumption | +0.8% | Global, with urban concentration | Short term (≤ 2 years) |

| Sustainability push and plastic substitution | +1.5% | EU leading, North America following | Long term (≥ 4 years) |

| Emerging-market beverage capacity expansion | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Short-run multipack machinery adoption | +0.4% | North America and EU | Medium term (2-4 years) |

| E-commerce beverage shipping requirements | +0.6% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Craft-Beer Multi-Pack Demand

Craft breweries lean on expressive packaging to capture shelf attention, and multi-packs have become their favored vehicle for volume growth. Corrugated carriers enable high-color graphics and withstand cold-chain condensation better than molded pulp inserts. Manufacturers tap hybrid kraft/white-top blends to supply the rigidity needed for heavier glass formats alongside premium print surfaces. Glass bottle output is set to reach 14,731.3 million units by 2030, underscoring sustained premiumization.[2]BG Container Glass, “One Report 2023,” BGC.CO.TH Strong craft positioning allows converters to charge for specialty coatings and moisture barriers that boost margins while keeping fibers recyclable.

Growth in On-the-Go Beverage Consumption

Urban consumers buy smaller, portable packs that travel from convenience stores to transit hubs, subjecting carriers to frequent handling. Corrugated designs now integrate finger-holes, easy-open tear lines, and tamper indicators without sacrificing compression strength. Australia’s rule to achieve 100% recyclable packaging by 2035 accelerates the redesign of grab-and-go multipacks. Rapid urbanization in Asian capitals further scales unit demand, prompting converters to localize their footprint and optimize logistics to shorten delivery cycles for high-volume retailers.

Sustainability Push and Plastic Substitution

The European Parliament’s 2024 directive establishes ambitious recycling targets and deposit-return systems that make traditional plastic yokes less viable. Brand owners pivot to corrugated solutions that already reach curbside recovery rates above 80%. WestRock reports 96% of its portfolio as recyclable, underpinned by 4.7 million tons of recovered fiber usage. As FDA rules strike PFAS from food contact, corrugated boards gain a regulatory edge over plastic coated carriers, channeling fresh R&D toward bio-based barrier sprays and closed-loop fiber systems.

Emerging-Market Beverage Capacity Expansion

Brewery and bottling plant investments in India, China, and Southeast Asia raise local demand for reliable multipacks. China produced 47.58 million kiloliters of beverage alcohol in 2023, and India’s packaging sector is on track for USD 204.81 billion in value by 2025. Domestic corrugators add high-speed lines to capture surging volumes and to meet local-content rules that favor in-country sourcing. For multinationals, long-term supply contracts lock in board grades that balance recycled content with export stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled linerboard price volatility | -0.8% | Global, acute in North America | Short term (≤ 2 years) |

| Competition from molded-fiber/plastic carriers | -0.6% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Beverage lightweighting lowers board calipers | -0.4% | Global, led by cost-conscious segments | Long term (≥ 4 years) |

| PFAS adhesive-content regulatory pressure | -0.3% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recycled Linerboard Price Volatility

The Producer Price Index for recyclable corrugated paper dropped 12.2% between October 2024 and January 2025, eroding finished-board pricing stability. Seasonal wastepaper collection swings, export demand shifts, and energy cost fluctuation exacerbate mill margin management. Producers institute quarterly price-adjustment clauses and hedge pulp futures to protect earnings, but frequent recalibration strains converter–brand relationships.

Competition from Molded-Fiber/Plastic Carriers

Molded fiber can form sculpted inserts that cradle premium bottles, and its global market could hit USD 15.57 billion by 2034. Life-cycle data show plastic carriers often weigh less than paper, lowering freight costs. Corrugated makers counter by bundling design services and by showcasing carbon-footprint reductions enabled through high-recycled fiber ratios and curbside recovery visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Grade: Sustainability Drives Recycled Uptake

High-recycled content boards captured nearly half of 2024 shipments, reflecting retailer scorecards and brand emissions targets. Hybrid kraft/white-top variants grow fastest because they overlay a bleached printable face on recycled mediums. Virgin kraft remains essential for export-ready multi-packs that face humid maritime holds. The corrugated beverage carrier board market size for hybrid grades is forecast to widen rapidly, supported by procurement policies that specify minimum 90% FSC-certified fiber. Commodity PPI data signal ongoing price gaps that encourage blended structures yet keep total conversion costs competitive.

Growing brand spend on packaging aesthetics raises ink-laydown demands, and white-top liners achieve sharper color contrast than natural brown. Recycled content improvements narrow historic tensile gaps; Rochester Institute of Technology testing shows today’s recycled liner compression values within 8% of virgin equivalents.[3]Rochester Institute of Technology, “Physical Properties of Linerboards,” RIT.EDU Market education campaigns reassure beverage producers that high-recycled formulas deliver shelf-life parity, supporting a virtuous cycle of fiber recovery.

By Beverage Type: Beer Retains Core Volume, Dairy Surges

Beer’s 33.21% share underscores the format’s deep roots in six-pack merchandising. Craft labels lean on tactile carrier textures and foil accents to justify premium pricing. Conversely, dairy and plant-based drinks accelerate on health and protein trends that line refrigerators across Asia and Europe. The corrugated beverage carrier board market share for dairy increments swiftly as lactose-free and oat-based brands switch from shrink film to fully recyclable fiber wraps to align with retailer plastic pledges.

Carbonated soft drinks still ship in high volumes but face caliper reductions as bottle weights fall. Spirit and wine brands adopt micro-flute carriers that present a luxury aesthetic and incorporate tamper-proof tabs needed for controlled-substance logistics. Water multi-packs in price-sensitive outlets use plain brown E-flute trays wrapped by minimal film, blending cost control with recyclability.

By Flute Type: E-Flute Commands, F-Flute Climbs

E-flute’s 1.6 mm profile balances crush strength and board economy, making it the default for four- to eight-unit beverage carriers. F-flute outpaces peers because its 1 mm thickness permits sharper offset lithography and fuller shelf facings without increasing case weight. The corrugated beverage carrier board market size expansion in F-flute aligns with premium craft launches targeting boutique retailers.

B-flute, at 2.5 mm, stays relevant for export beer pallets and glass growler packs that demand extra cushioning. C-flute sees niche use where long dwell times in warehouses invite stacking loads beyond 900 pounds. Modern inline corrugators allow mid-shift flute changeovers that keep plant utilization high even as order profiles fragment.

By End-User: Breweries Dominate but Co-Packers Accelerate

Breweries secured 36.42% of 2024 demand through direct sourcing contracts with integrated box plants. Their brand marketing cycles call for frequent artwork refreshes that digital pre-print boards now support. Co-packers post the top CAGR because emerging beverage startups outsource filling and packaging to preserve capital; these service providers favor versatile converting vendors who manage fluctuating run lengths.

Soft-drink bottlers negotiate long-term pricing to shield against kraft pulp hikes, reinforcing their scale advantage. Dairy processors command moisture-scored boards to endure chilled distribution. Wineries and distillers desire embossing and metallic inks that convey premium cues and deter counterfeits in duty-free channels.

Geography Analysis

North America led 2024 sales with 31.96% share as expansive craft brewery networks and state deposit laws favor sturdy recyclable carriers. United States converters leverage vertical integration to steady fiber supply and to innovate coatings that survive cold-chain condensation. Canada’s eco-logo procurement and Mexico’s export corridors jointly lift regional tonnage. Smurfit Westrock’s USD 400 million synergy plan illustrates the capital scale deployed to streamline mills and logistics.

Asia-Pacific records the quickest 5.98% CAGR as urbanization widens modern trade channels and beverage SKUs. India’s MSME-heavy packaging sector consolidates, opening market entry windows for multinational box makers seeking greenfield plants near new breweries. Chinese alcohol output gains underline latent demand for multi-pack solutions that meet both domestic recycling quotas and export quality flags. Japan and South Korea keep a premium orientation, adopting micro-flutes and aqueous inks to satisfy discerning consumers.

Europe sits between mature volume and regulatory dynamism. The EU’s 65% recycled-content rule embedded in Regulation 2025/40 cements corrugated boards’ compliance credentials. Germany’s Reinheitsgebot beer heritage drives steady high-spec packaging orders, while the United Kingdom’s craft renaissance values bespoke short runs. Southern wine economies favor premium white-top carriers that travel safely from vineyard to global shelves. Circular-economy funding streams further subsidize closed-loop fiber collection infrastructure, lifting recovery rates and lowering virgin pulp reliance.

South America and the Middle East & Africa register smaller bases yet rising consumer class expansion fuels beverage manufacturing investments. Regional corrugators partner with global breweries to localize carrier designs that reflect cultural motifs while remaining export compliant.

Competitive Landscape

Industry consolidation proceeds at a measured pace. The merger creating Smurfit Westrock brings unrivaled geographic coverage and a stated USD 400 million synergy capture, propelling integrated cost advantages in fiber procurement and mill utilization. International Paper generated USD 18.9 billion net sales in 2023, of which USD 15.6 billion stemmed from industrial packaging, underscoring scale benefits that mitigate pulp volatility.

Graphic Packaging devoted USD 1 billion to a recycled paperboard mill in Texas, signaling long-term confidence in fiber-based beverage solutions. Regional independents differentiate through rapid lead times, digital print services, and light-asset models that suit craft producers. Strategic themes include vertical integration, renewable-energy-powered mills, and PFAS-free adhesive rollouts that anticipate global compliance shifts.

Partnerships with molded-fiber specialists surface as converters hedge against material substitution. Technology tie-ups in digital corrugation and robotics streamline line changeovers, slashing setup by 60% and enabling profitable micro-runs.

Corrugated Beverage Carrier Board Industry Leaders

Smurfit Westrock PLC

Graphic Packaging International LLC

Mondi PLC

International Paper Company

Georgia-Pacific LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA declared 35 PFAS food-contact notifications inactive, setting a June 2025 compliance deadline.

- February 2025: Smurfit Westrock posted USD 319 million full-year 2024 net income with USD 4.7 billion adjusted EBITDA following its merger integration.

- January 2025: Graphic Packaging brought its USD 1 billion recycled board plant in Waco online, bolstering sustainable capacity.

- December 2024: International Paper closed its Orange, Texas containerboard mill to optimize product mix.

Global Corrugated Beverage Carrier Board Market Report Scope

| Virgin Kraft |

| High-Recycled Content |

| Hybrid (Kraft/White-Top) |

| Beer |

| Carbonated Soft Drinks |

| Juice and Functional Drinks |

| Dairy and Plant-based |

| Water |

| Wine and Spirits |

| F-Flute |

| E-Flute |

| B-Flute |

| C-Flute |

| Breweries |

| Soft-Drink Bottlers |

| Wineries and Distilleries |

| Dairy Processors |

| Co-packers and Other End-user |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Grade | Virgin Kraft | ||

| High-Recycled Content | |||

| Hybrid (Kraft/White-Top) | |||

| By Beverage Type | Beer | ||

| Carbonated Soft Drinks | |||

| Juice and Functional Drinks | |||

| Dairy and Plant-based | |||

| Water | |||

| Wine and Spirits | |||

| By Flute Type | F-Flute | ||

| E-Flute | |||

| B-Flute | |||

| C-Flute | |||

| By End-user | Breweries | ||

| Soft-Drink Bottlers | |||

| Wineries and Distilleries | |||

| Dairy Processors | |||

| Co-packers and Other End-user | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global demand for corrugated beverage carriers be in 2030?

It is projected to reach USD 978.67 million, reflecting a 5.03% CAGR from 2025.

Which region is expanding fastest for beverage carrier boards?

Asia-Pacific posts the quickest 5.98% CAGR, fueled by new bottling capacity and rising disposable income.

Why are hybrid kraft/white-top grades growing so quickly?

They merge recycled content with a printable white face, satisfying both sustainability targets and brand graphics needs while advancing at a 6.12% CAGR.

What is the main competitive threat to corrugated carriers?

Molded-fiber inserts and lightweight plastic carriers challenge premium segments, although regulatory plastic curbs temper their growth.

How are suppliers addressing PFAS adhesive restrictions?

Converters are testing water-based and bio-based binding systems that comply with FDA rules effective mid-2025, ensuring food-contact safety without fluorochemicals.

Which flute profile dominates beverage multi-packs?

E-flute holds about 44.56% share due to its balance of strength, printability, and material efficiency.

Page last updated on: