Continuous Renal Replacement Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

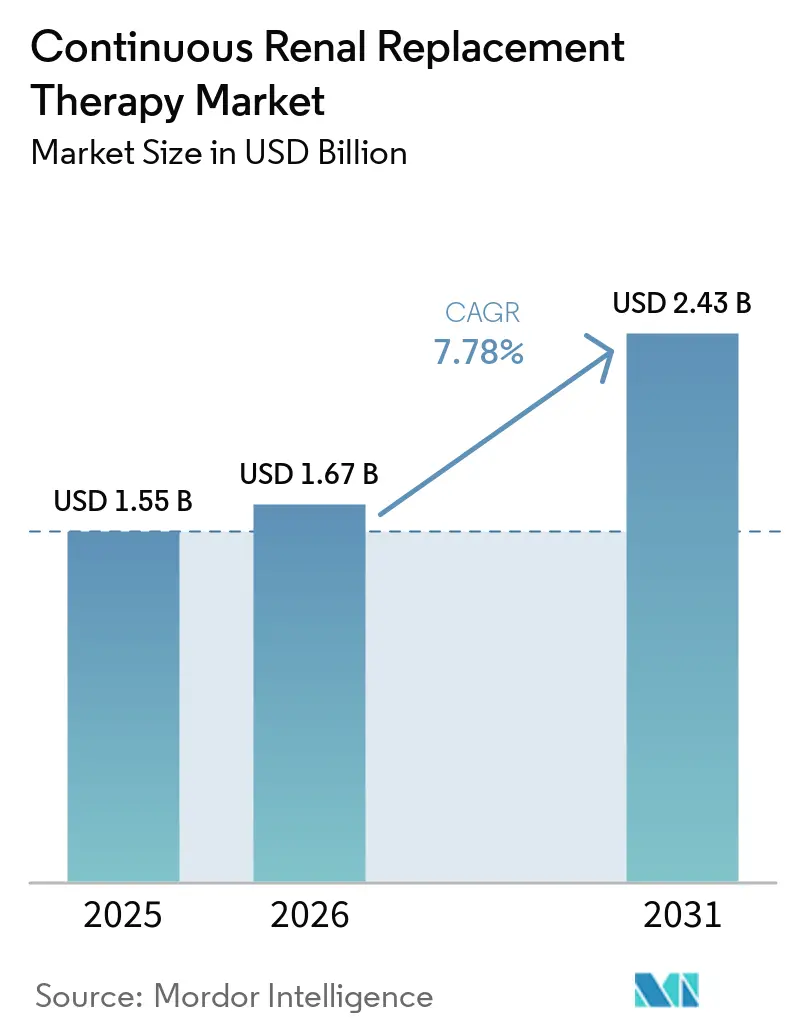

| Market Size (2026) | USD 1.67 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Continuous Renal Replacement Therapy Market Analysis by Mordor Intelligence

The continuous renal replacement therapy market size is projected to be USD 1.55 billion in 2025, USD 1.67 billion in 2026, and reach USD 2.43 billion by 2031, growing at a CAGR of 7.78% from 2026 to 2031. Uptake is propelled by the rising burden of acute kidney injury in aging, multi-morbid intensive-care populations, steady advances in membrane biocompatibility and regional citrate anticoagulation that lengthen filter life, and faster device clearances through emergency-use pathways.

Key Report Takeaways

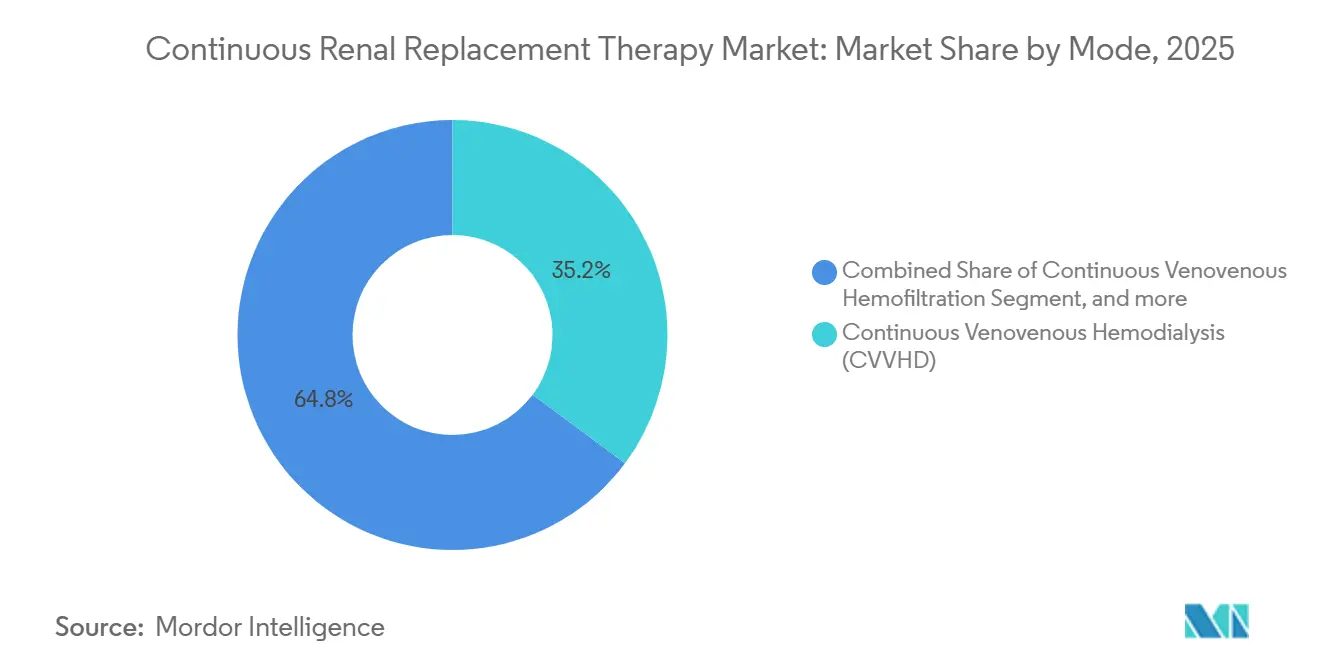

- By mode, Continuous Venovenous Hemodialysis retained 35.18% of the continuous renal replacement therapy market share in 2025, while Continuous Venovenous Hemodiafiltration is forecast to expand at a 10.22% CAGR through 2031.

- By product type, dialysate and replacement fluids accounted for a 43.21% share of the continuous renal replacement therapy market size in 2025; catheters and ancillaries are advancing at a 9.65% CAGR to 2031.

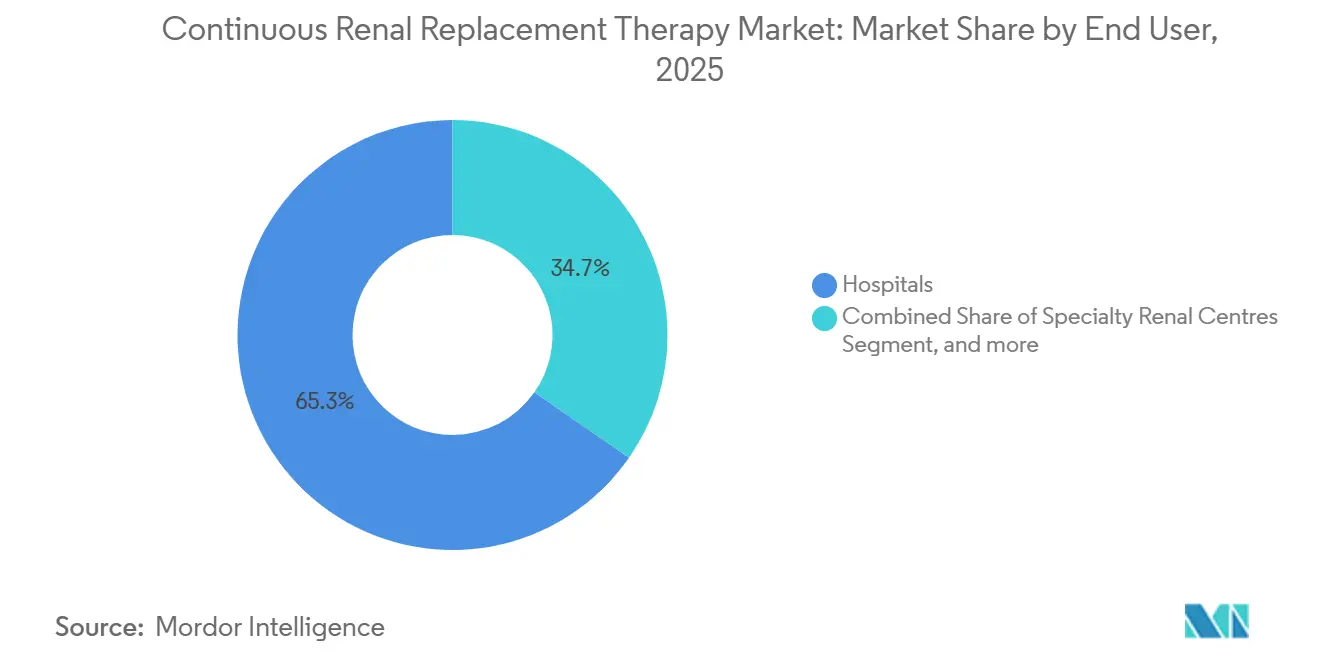

- By end user, hospitals captured 65.32% revenue in 2025 and ambulatory surgical centers represent the fastest-growing channel with a 9.12% CAGR over 2026-2031.

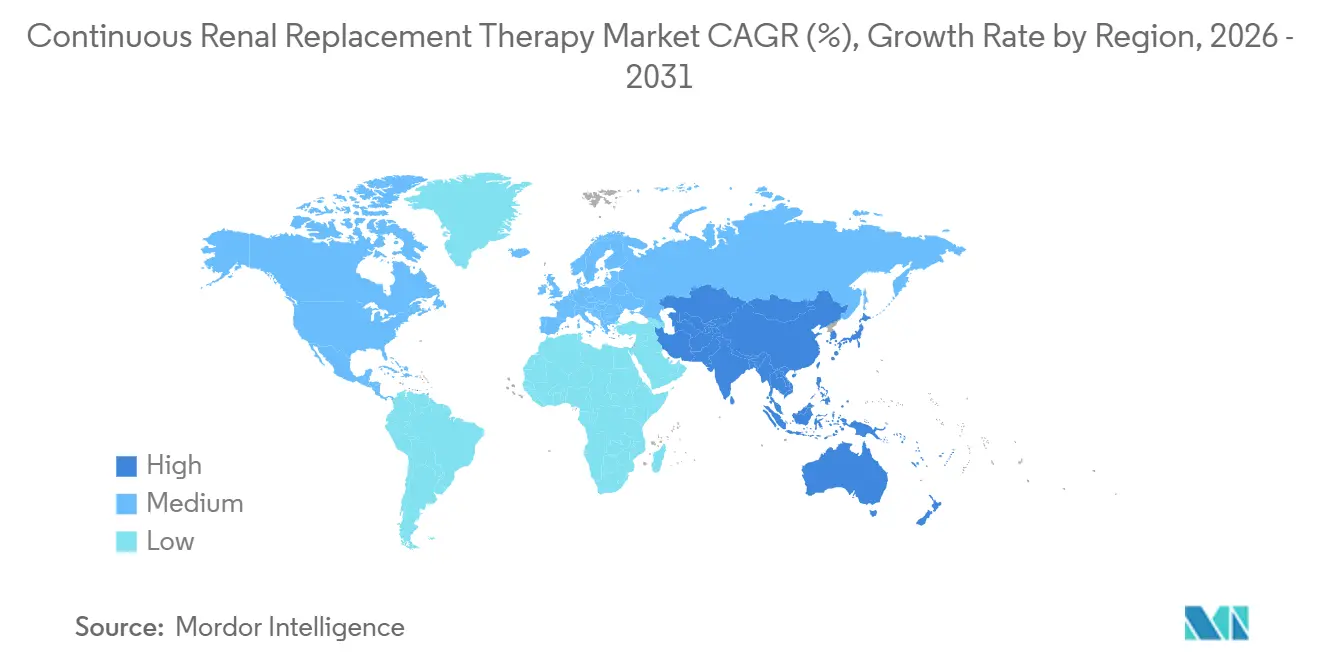

- By geography, North America retained 44.15% revenue share in 2025, and Asia-Pacific is projected to record a 10.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Continuous Renal Replacement Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of AKI among aging ICU cases | +2.1% | North America, Europe most acute | Long term (≥ 4 years) |

| Continuous innovation in CRRT hardware & fluids | +1.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Sepsis-related multi-organ dysfunction | +1.5% | Asia-Pacific, Middle East-Africa | Short term (≤ 2 years) |

| ICU bed additions in emerging economies | +1.3% | Asia-Pacific core, spill-over to MEA, S. America | Long term (≥ 4 years) |

| Emergency-use-authorization pathways | +0.7% | United States, EU, selected APAC | Short term (≤ 2 years) |

| Regional citrate anticoagulation adoption | +0.4% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of AKI Among Aging, Multi-Morbid ICU Populations

Acute kidney injury complicated 22.3% of all intensive-care admissions in 2025 as median patient age edged past 68 years and nearly half of the cohort carried diabetes or chronic kidney disease[1]Daniel Johnson, “ICU Admissions Complicated by AKI in 2025,” ccforum.com. Polypharmacy intensifies exposure, with patients on five or more nephrotoxic agents facing triple the AKI risk. Because the global population over 65 will swell to 1.6 billion by 2030, this demand driver is structural rather than cyclical. Hospitals in higher-income settings have therefore embedded CRRT consoles inside general ICUs rather than nephrology units, cutting transfer delays and lifting 28-day survival by about eight percentage points. Regulation exerts little influence here since AKI care is guided chiefly by clinical practice rather than device mandates.

Continuous Innovation in CRRT Hardware, Membranes & Fluids

Polyethersulfone-polysulfone blends with enlarged surface areas raised middle-molecule clearance 15% between 2024 and 2025, enabling single-modality cytokine removal for CAR-T and severe COVID-19 patients. Baxter’s Prismaflex HF1400, cleared in March 2025, carries a hydrophilic coating that extends median filter life to 96 hours under citrate, trimming consumable expense 30%. Fresenius’ multiFiltrate PRO, launched in Europe in June 2025, adds optical sensors that flag hemolysis or air within two seconds, addressing a legacy safety gap. Concurrently, bicarbonate-buffered fluids with moderated sodium now dominate, curbing hypernatremia during prolonged therapy. Adherence to the stricter ISO 23500-5:2025 biocompatibility rules lifts development costs yet ensures lower endotoxin exposure.

Sepsis-Related Multi-Organ Dysfunction Expanding CRRT Utilization

Sepsis represented 31% of ICU admissions in 2025, and nearly half of those patients progressed to AKI within 72 hours. The 2024 surviving-sepsis guidelines raised CRRT to class IIa status for refractory fluid overload, pushing initiation rates up 22% across Western centers[2]Martin Smith, “Surviving Sepsis Campaign 2024 Guidelines,” icm-journal.com. High-cutoff hemofilters and hemoadsorption cartridges now target patients with median IL-6 titers of 850 pg/mL, well beyond non-septic ranges, yielding a 14% 30-day survival benefit in European registry work. Clinically, the driver is most powerful in Asia-Pacific and MEA where sepsis incidence is almost double North America’s baseline.

ICU Bed Additions and Acuity Upgrades in Emerging Economies

China installed 28,000 new ICU beds in 2025 to reach 142,000, yet its 3.9-per-100,000 ratio remains below U.S. density. India earmarked USD 1.2 billion for 15,000 Level-II beds by 2027, each specified for CRRT. Saudi Arabia’s Vision 2030 plan funds 4,500 ICU beds with mandatory CRRT capability. New units target nurse-to-patient ratios of 1:2 and align with ISO norms, accelerating local uptake of continuous renal replacement therapy market solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy and capital costs versus IHD | –1.2% | South America, MEA, South Asia | Medium term (2-4 years) |

| Shortage of CRRT-trained nurses & technicians | –0.9% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| Supply-chain fragility for sterile dialysate | –0.5% | Episodic shocks in North America & Europe | Short term (≤ 2 years) |

| ISO 23500 compliance burden for mid-tier firms | –0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy and Capital Costs Versus Intermittent RRT

A single CRRT day typically consumes USD 1,200–2,500 in disposables, dwarfing the USD 400–800 cost for intermittent hemodialysis. Equipment adds another USD 40,000–70,000 per machine, while reimbursement often fails to close the gap; U.S. DRG-based payments leave many hospitals at a loss on complex AKI admissions[3]Centers for Medicare & Medicaid Services, “DRG Payment Rates for AKI,” cms.gov. In India, the public scheme pays USD 600 per session against a USD 1,000 outlay, limiting penetration. Latin America and Sub-Saharan Africa face even steeper affordability cliffs where out-of-pocket health spend tops 40%.

Global Shortage of CRRT-Trained Critical-Care Nurses & Technicians

The United States entered 2026 short nearly 78,000 critical-care nurses, with ICU turnover running 18.7% a year. Only 38% of hospitals offer formal CRRT training, leaving skill levels patchy. Germany and the United Kingdom post double-digit vacancy rates, while China’s nurse-to-ICU-bed ratio lingers at 1.8:1. Vendors reply with predictive-control consoles, but regulators remain wary of full closed-loop autonomy in life-support devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode: Hybrid Modalities Move Center Stage

CVVHD held a 35.18% slice of the continuous renal replacement therapy market in 2025, but CVVHDF’s 10.22% CAGR signals a decisive turn toward mixed convective-diffusive clearance. The diffusion-only ceiling at 15 kDa means CVVHD misses inflammatory mediators; CVVHDF captures them without sacrificing small-solute control. Vendors facilitate the switch with consoles that auto-calculate replacement-fluid flow, easing bedside complexity. Japan’s reimbursement premium for CVVHDF, 15% above CVVHD as of March 2025, reinforced uptake.

Centers that prize ultrafiltration for cardiorenal syndrome still favor CVVH, yet its share is eroding because CVVHDF delivers equivalent fluid removal with tighter potassium control. Slow Continuous Ultrafiltration remains a niche tool for gentle volume extraction. Regulatory acknowledgment of CVVHDF as a distinct modality forces manufacturers to meet higher benchmarks for convective performance, spurring membrane innovation that should keep CVVHDF ahead through 2031.

By Product Type: Consumables Dominate, Smart Catheters Surge

Dialysate and replacement fluids accounted for 43.21% of the continuous renal replacement therapy market size in 2025 and remain the primary profit engine, thanks to their razor-and-blade economics. Catheters and ancillaries, however, are growing faster at 9.65% CAGR as antimicrobial coatings and step-tip geometries cut bloodstream infections 40% and recirculation under 5%.

Hemofilters with cytokine-adsorbing polymers command premium pricing, especially in sepsis care, while RFID-embedded bloodline sets reduce waste in high-volume centers. Breakthrough-device designation for Teleflex’s Arrow CRRT catheter in September 2025 exemplifies regulator support for infection-averse designs and positions catheters as the standout growth pocket within consumables.

By End User: Acuity Migrates Toward Ambulatory Settings

Hospitals retained 65.32% of 2025 global revenue, yet ambulatory surgical centers are climbing 9.12% CAGR on the back of bundled-payment models that penalize readmissions. Specialty renal centers are also adding CRRT to manage acute-on-chronic flares among stage-4 CKD patients, leveraging existing dialysis infrastructure for 20% lower costs versus hospital ICUs.

Outpatient expansion hinges on regulatory flexibility; only 14 U.S. states permit CRRT outside hospitals as of early 2026. The United Kingdom’s draft guidance allowing nurse-led ambulatory CRRT under remote physician oversight could accelerate Europe’s shift. Home-based evaluations of Quanta’s SC+ platform underscore the longer-term goal of portable, low-flow therapy for stable fluid-overloaded patients.

Geography Analysis

North America generated 44.15% of 2025 revenue, propped up by 9.7 ICU beds per 100,000 residents and widespread citrate protocols that shave USD 900 from per-episode disposables. Growth is moderating as bed additions slow and nurse shortages curtail capacity. Canada’s CAD 240 million upgrade fund helps offset delayed equipment cycles, whereas Mexico’s public hospitals largely rely on intermittent dialysis, limiting penetration.

Asia-Pacific remains the fastest climber at a 10.98% CAGR through 2031. China’s order that all tertiary hospitals deploy CRRT by December 2026 and India’s USD 1.2 billion ICU upgrade plan are central catalysts. Japan’s strict reimbursement caps keep cost pressure high, forcing efficiency gains. Australia’s approval of four new systems in 2025 signals an appetite for technological diversity.

Europe maintains a sizable share, buoyed by EMA adaptive approvals that shorten launch cycles and NHS-brokered volume discounts that cut consumable prices 12%. Southern Europe still trails Northern peers on ICU density but will add 6,000 beds by 2028 with EU structural money. The Middle East is propelled by Saudi Vision 2030, while South America struggles with currency depreciation that inflates imported-consumable costs.

Competitive Landscape

Fresenius Medical Care, Medtronic, B. Braun, and others together control a significant share of the continuous renal replacement therapy market, leveraging installed bases and proprietary consumables. Fresenius locks in clients through 40,000 multiFiltrate consoles worldwide, reaping 70% gross margins on fluids and filters, though antitrust regulators are watching exclusivity clauses. Baxter completed its kidney-care spin-off (Vantive) in April 2025, a move that sharpened R&D focus but briefly disrupted supply chains and ceded share to B. Braun.

Smaller innovators are tilting the field. Cytosorbents’ hemoadsorption cartridge targets cytokine removal and now exceeds 180,000 global uses. Quanta Dialysis Technologies’ SC+ portable unit positions the company for home-CRRT trials and promises 40% per-session savings. SeaStar Medical’s selective cytopheretic device, granted breakthrough status in August 2025, seeks to modulate neutrophils without systemic anticoagulation. New ISO 23500 mandates elevate compliance costs, favoring diversified players but potentially squeezing niche entrants into partnerships or acquisitions.

Continuous Renal Replacement Therapy Industry Leaders

Asahi Kasei Medical Co., Ltd

B. Braun Melsungen AG

Fresenius Medical Care AG & Co. KgaA

Infomed SA

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SWS Medical announced that its flagship blood purification platforms, including the SWS-4000 and SWS-6000 series hemodialysis machines, as well as the SWS-5000 series continuous renal replacement therapy (CRRT) equipment, have achieved certification under the European Union Medical Device Regulation (EU MDR 2017/745).

- December 2025: Nephrodite Inc. reported successful multi-day large-animal testing of its Holly implantable renal replacement system.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the continuous renal replacement therapy (CRRT) market as the total annual value of systems, hemofilters, dialysate and replacement fluids, tubing sets, and single-use disposables deployed for 24-hour extracorporeal blood purification in hemodynamically unstable patients with acute kidney injury across hospital critical-care settings worldwide.

Scope exclusion: devices or consumables designed solely for chronic home hemodialysis are not counted.

Segmentation Overview

- By Mode

- Continuous Venovenous Hemodialysis (CVVHD)

- Continuous Venovenous Hemofiltration (CVVH)

- Continuous Venovenous Hemodiafiltration (CVVHDF)

- Slow Continuous Ultrafiltration (SCUF)

- By Product Type

- Dialysate & Replacement Fluids

- Hemofilters & Adsorptive Cartridges

- Bloodline Sets & Tubes

- Catheters & Ancillaries

- CRRT Systems / Monitors

- By End User

- Hospitals

- Specialty Renal Centres

- Ambulatory Surgical Centres

- Home- & Field-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with critical-care clinicians, renal nurses, procurement heads, and regulatory reviewers across North America, Europe, and leading Asian economies. Insights on consumable run-rates, typical therapy days per patient, and price adjustments during COVID-era shortages were used to refine model coefficients and to vet secondary findings.

Desk Research

We began with open datasets from bodies such as the World Health Organization, KDIGO, the International Society of Nephrology, the U.S. CDC, Eurostat, and Japan's MHLW, which outline AKI incidence, ICU bed density, and procedure codes. Product shipment clues came from FDA 510(k) releases, EU MDR filings, and customs trade lines (HS 901890). Financial clues were gathered through 10-Ks, investor decks, and D&B Hoovers; news flow was screened on Dow Jones Factiva; patent velocity was checked on Questel. These sources anchored baseline volumes, price corridors, and regional mix. The list is illustrative; many additional publications aided data checks.

Market-Sizing and Forecasting

A top-down reconstruction starts with country-level AKI ICU admissions, applies clinically validated CRRT penetration ratios, and multiplies by average therapy days and consumables per day. System sales are then tied to replacement cycles. Supplier roll-ups and channel checks provide a selective bottom-up lens that tempers totals. Key variables include ICU bed expansion, sepsis prevalence, average selling prices of hemofilters, fluid-to-blood flow ratios, and regional reimbursement shifts. Forecasts are produced through multivariate regression blended with ARIMA for short-term shocks, after consensus review with primary respondents. Data gaps, such as missing import flows for smaller economies, are bridged by regional proxies adjusted through purchasing-power parity.

Data Validation and Update Cycle

Outputs pass a two-step variance screen versus historical ratios and peer benchmarks; material deviations trigger analyst re-work before sign-off. Reports refresh annually, while major regulatory or macro events prompt interim revisions, and every delivery includes a fresh data sweep.

Why Mordor's Continuous Renal Replacement Therapy Baseline Deserves Trust

Published estimates often diverge because firms pick different product baskets, pricing ladders, and forecast cut-off points.

Key gap drivers include narrower modality coverage in some studies, alternate base-year currency conversions, or optimistic uptake curves for home-based therapies, all factors our framework normalizes before sizing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.55 B (2025) | Mordor Intelligence | - |

| USD 1.25 B (2025) | Global Consultancy A | Excludes dialysate and replacement fluids; uses list prices without regional ASP weighting |

| USD 1.71 B (2025) | Trade Journal B | Adds neonatal home-care kits and projects faster ICU adoption curve |

| USD 1.57 B (2024) | Industry Association C | Older base year and single inflation uplift, limited primary verification |

In sum, the disciplined scoping, dual-angle modeling, and annual refresh cadence applied by Mordor Intelligence give decision-makers a balanced, transparent baseline that traces every dollar back to clear, reproducible drivers.

Key Questions Answered in the Report

How fast will global demand for continuous renal replacement therapy rise through 2031?

Global revenue is forecast to expand at a 7.78% CAGR from 2026 to 2031, reaching USD 2.43 billion.

Which region offers the highest growth runway for continuous renal replacement therapy?

Asia-Pacific leads with a 10.98% CAGR, fueled by ICU bed additions in China, India, and Southeast Asia.

What modality is gaining preference over CVVHD?

Continuous Venovenous Hemodiafiltration is the fastest riser, projected at a 10.22% CAGR owing to superior cytokine clearance.

Why are ambulatory surgical centers adopting CRRT?

Episode-based payment encourages outpatient management, and ambulatory centers can deliver sessions at margins near 12% when filter life exceeds 48 hours.

How do newer anticoagulation protocols impact operating costs?

Regional citrate anticoagulation extends filter life to roughly 72 hours, shaving about USD 900 in disposables per patient episode.

Page last updated on: