Hemodialysis Vascular Grafts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

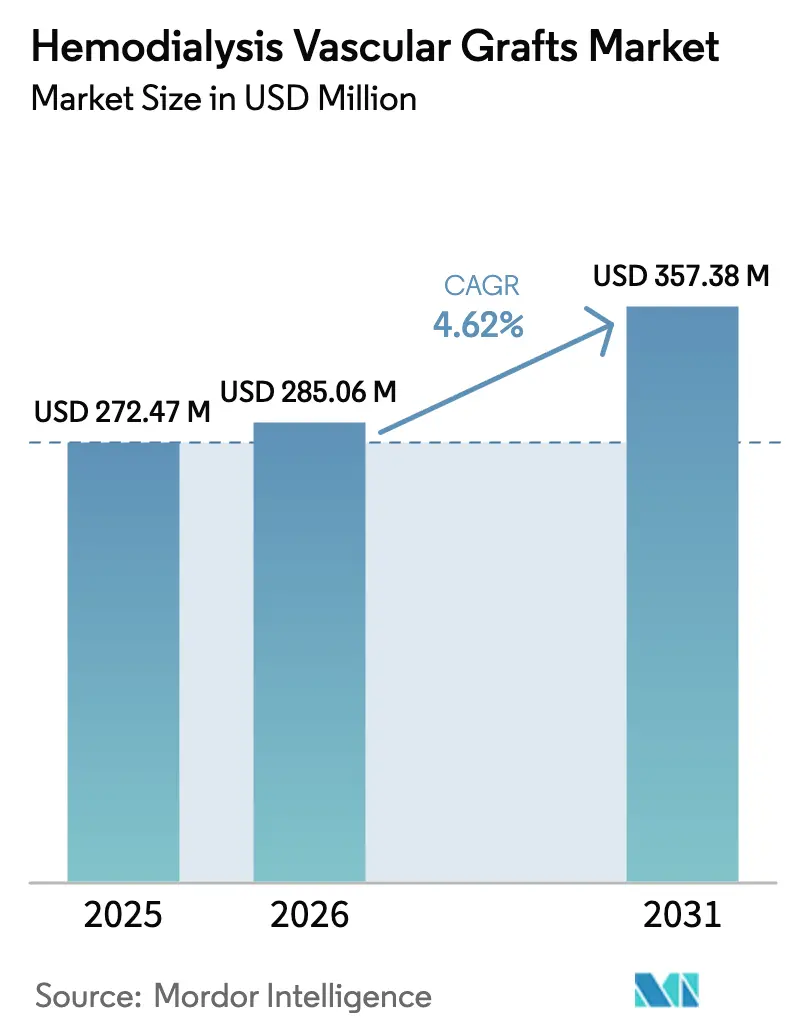

| Market Size (2026) | USD 285.06 Million |

| Market Size (2031) | USD 357.38 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemodialysis Vascular Grafts Market Analysis by Mordor Intelligence

hemodialysis vascular access grafts market size in 2026 is estimated at USD 285.06 million, growing from 2025 value of USD 272.47 million with 2031 projections showing USD 357.38 million, growing at 4.62% CAGR over 2026-2031. Rising chronic kidney disease (CKD) prevalence, which affected 673 million people in 2024, is enlarging the dialysis patient pool and sustaining demand for reliable vascular access. Economic incentives such as Medicare’s USD 273.82 per-treatment End-Stage Renal Disease (ESRD) Prospective Payment System (PPS) base rate reinforce the need for durable, low-maintenance grafts[1]Source: Centers for Medicare & Medicaid Services, “Calendar Year 2025 End-Stage Renal Disease Prospective Payment System Final Rule,” cms.gov. Technological differentiation is intensifying: early-cannulation expanded polytetrafluoroethylene (ePTFE) designs, heparin-bonded coatings, and tissue-engineered vessels are key innovation fronts. Market participants are also responding to a “Fistula First, Catheter Last” clinical environment by positioning grafts as rapid back-up options for high-risk patients whose fistulas fail to mature.

Key Report Takeaways

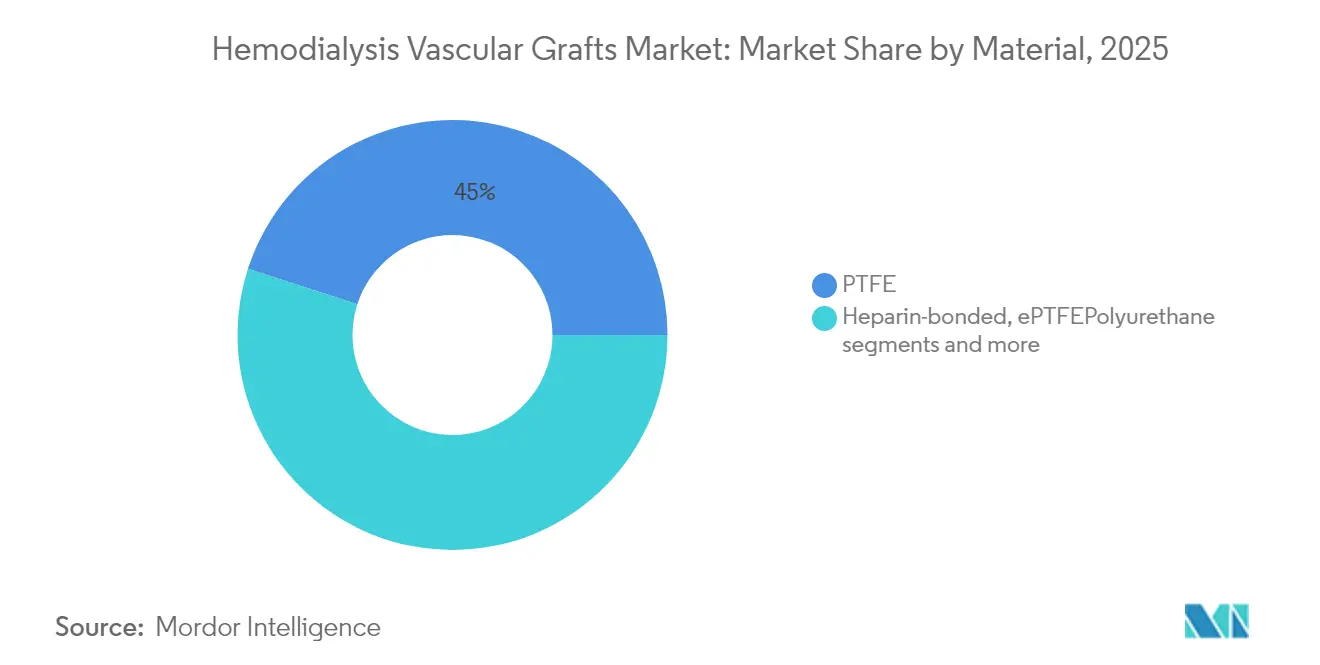

- By material, PTFE led with 45.02% of hemodialysis vascular access grafts market share in 2025, while biosynthetic materials are forecast to expand at a 4.96% CAGR through 2031.

- By configuration, conventional grafts held 68.42% revenue share in 2025, whereas early-cannulation variants are projected to rise at a 5.52% CAGR to 2031.

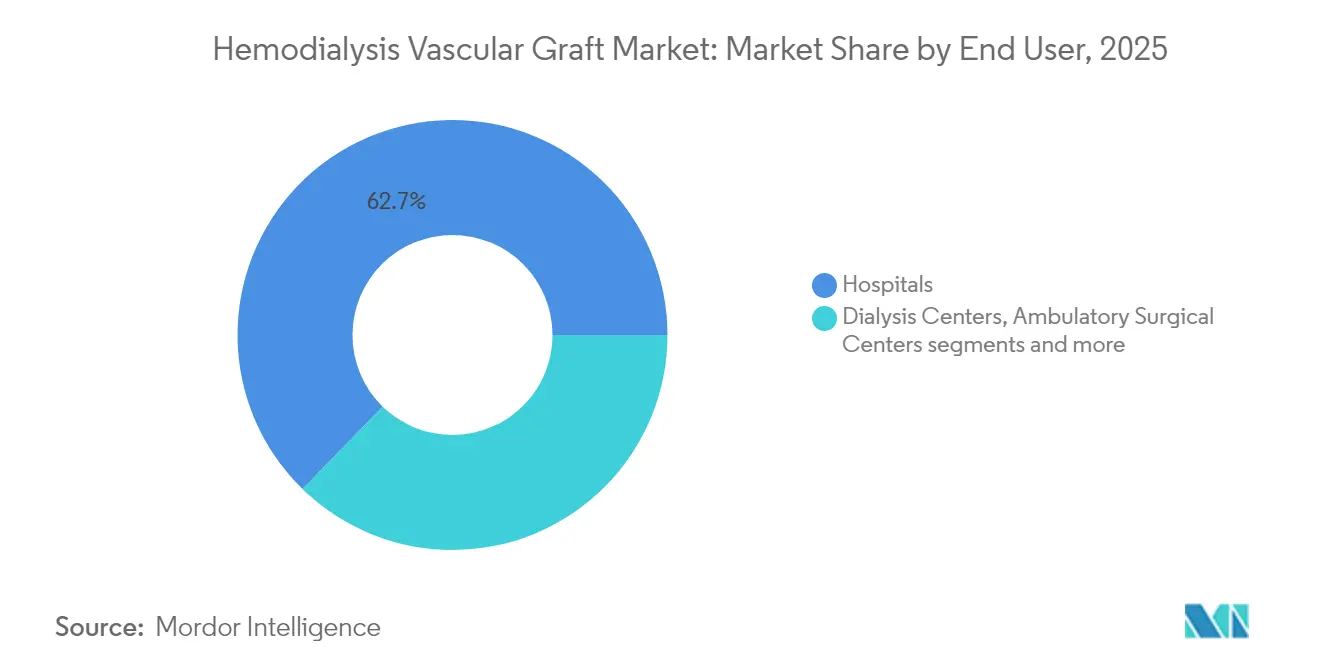

- By end user, hospitals accounted for 62.71% of the hemodialysis vascular access grafts market size in 2025; dialysis centers show the fastest growth at a 5.71% CAGR.

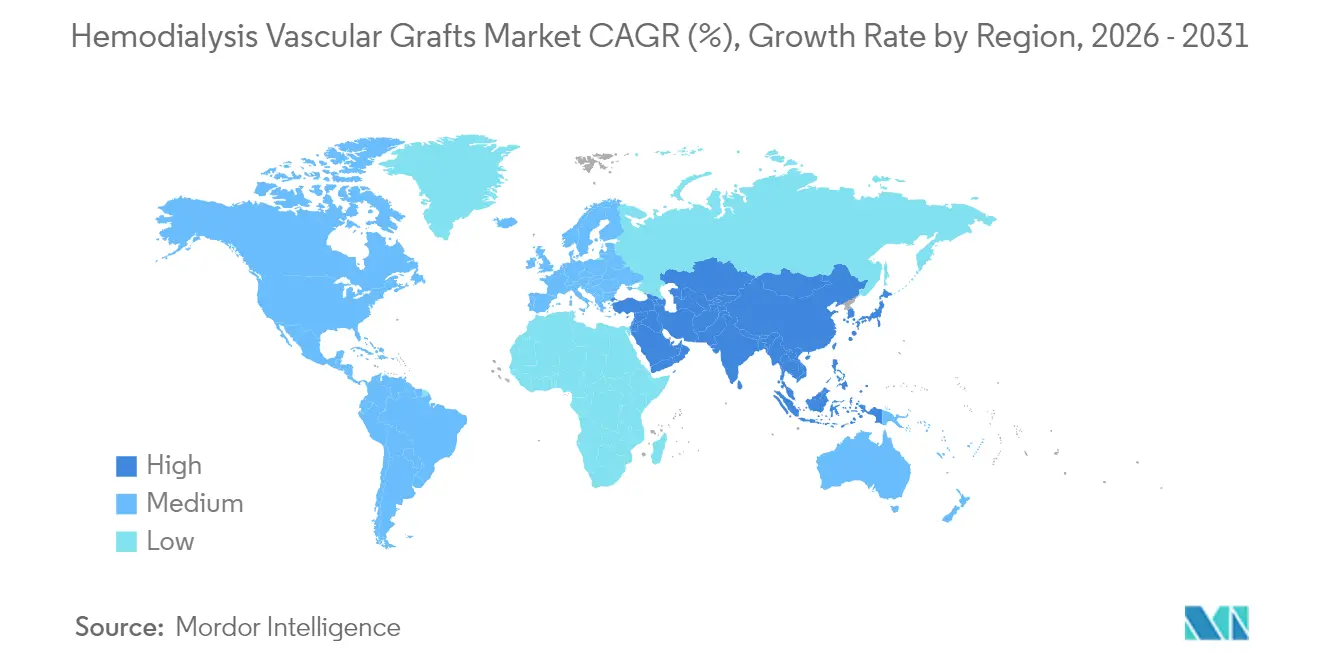

- By geography, North America commanded 37.10% share of the hemodialysis vascular access grafts market in 2025, but APAC is poised for the quickest expansion at a 6.63% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hemodialysis Vascular Grafts Market Trends and Insights

Driver Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CKD prevalence & dialysis patient pool | +1.2% | Global, strongest in APAC & MEA | Long term (≥ 4 years) |

| Increasing adoption of early-cannulation ePTFE grafts | +0.8% | North America & EU; spreading to APAC | Medium term (2-4 years) |

| Technology shift toward heparin-bonded & bio-active coatings | +0.6% | Global, led by developed markets | Medium term (2-4 years) |

| Hospital consolidation driving bulk purchasing | +0.4% | North America & EU | Short term (≤ 2 years) |

| Medicare policy creating graft back-up demand | +0.5% | United States | Medium term (2-4 years) |

| Pipeline micro-porous silk fibroin grafts | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CKD prevalence & dialysis patient pool

Global CKD prevalence climbed to 673 million cases in 2024, accompanied by higher mortality and disability-adjusted life years, especially in low-sociodemographic regions. High fasting plasma glucose accounts for roughly one-third of CKD-related deaths, indicating diabetes as a key demand driver for dialysis grafts in emerging markets. Earlier ultrasound-based CKD detection is enlarging the eligible patient base before end-stage progression. Together, these epidemiological shifts underpin sustained expansion of the hemodialysis vascular access grafts market.

Increasing adoption of early-cannulation ePTFE grafts

Gore’s ACUSEAL graft achieved 73% successful cannulation within 24 hours post-implantation, reducing catheter exposure and infection risk [2]Source: Gore Medical, “ACUSEAL Vascular Graft,” goremedical.com . Japanese cohort data reported 88.8% assisted-primary patency at 3 months, confirming clinical durability. Hospitals value the ability to initiate dialysis rapidly without central venous catheters, a factor accelerating early-cannulation uptake.

Technology shift toward heparin-bonded & bio-active coatings

Gore’s PROPATEN vascular graft reduced occlusion risk by 50% among critical limb ischemia patients, illustrating how surface-bound heparin improves thromboresistance. Preclinical research shows nitric-oxide-releasing bilayer grafts that foster endothelial healing while curbing smooth-muscle proliferation. Such innovations enhance long-term patency, shaping competitive strategy.

Hospital consolidation driving bulk purchasing

Integrated delivery networks negotiate volume contracts that favor suppliers offering end-to-end vascular access solutions. Teleflex’s EUR 760 million acquisition of BIOTRONIK’s Vascular Intervention unit exemplifies portfolio broadening to satisfy large health-system buyers. Vendors able to supply data-backed value propositions gain leverage in bundled procurement negotiations

Restraint Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High intervention cost vs. fistula | -0.70% | Global, strongest in cost-sensitive markets | Medium term (2-4 years) |

| Reimbursement cuts on dialyzer bundle (U.S.) | -0.50% | United States | Short term (≤ 2 years) |

| Rising antimicrobial resistance | -0.40% | Global, higher in hospital settings | Medium term (2-4 years) |

| 3D-printed personalized grafts post-2030 | -0.30% | Developed markets initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High intervention cost vs. fistula

Arteriovenous fistulas remain the economic benchmark, with Brazilian registry data showing graft usage at only 2.6% compared with 73.8% fistulas in 2024. Medicare’s bundled ESRD payment structure incentivizes low-cost access modalities, dampening graft adoption unless new devices can prove fewer re-interventions

Rising antimicrobial resistance → higher infection risk

Bloodstream infections occurred in 17.5% of chronic hemodialysis patients in 2024, with gram-negative organisms responsible for 46.3% of cases. Multidrug-resistant pathogens complicate treatment, elevating the clinical burden associated with synthetic grafts relative to autogenous fistulas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PTFE Dominance Faces Biosynthetic Innovation

PTFE claimed 45.02% of 2025 revenues, underlining its long-standing clinical integration and manufacturing scalability. The hemodialysis vascular access grafts market size for PTFE is forecast to reach USD 161.27 million by 2031, expanding at a steady pace as proprietary surface modifications, such as Gore’s STRETCH and ACUSEAL, bolster performance. In contrast, biosynthetic and tissue-engineered vessels such as Humacyte’s acellular tissue-engineered vessel (ATEV) are projected to grow at 4.96% CAGR, supported by December 2024 FDA approval for vascular trauma and promising Phase 3 dialysis data. Mechanical attributes of silk-fibroin scaffolds mirror native vessels, strengthening the case for biologic options.

Biosynthetic progress is reshaping supplier roadmaps yet scale-up hurdles remain. Regulatory scrutiny of living-cell constructs lengthens time-to-market, and higher unit costs could constrain early uptake in price-sensitive regions. Nevertheless, early adopters are testing off-the-shelf tissue-engineered grafts for patients who lack suitable veins, signalling future share gains for biologics within the hemodialysis vascular access grafts market.

By Configuration: Early-Cannulation Gains Despite Conventional Leadership

Conventional grafts retained 68.42% revenue share in 2025, reflecting surgeon familiarity and entrenched operating-room protocols. Early-cannulation designs, however, are forecast to deliver a 5.52% CAGR through 2031. The hemodialysis vascular access grafts market share held by early-cannulation variants could exceed 30% by the end of the decade as facilities prioritise catheter avoidance. Clinical evidence shows ACUSEAL enabling dialysis within 24 hours while maintaining 78% secondary patency at 12 months.

Adoption barriers include higher upfront device costs and learning curves, yet total cost-of-care analysis increasingly favours early access because catheter infections prolong hospital stays. Policymaker focus on home dialysis and outpatient care further strengthens the value proposition for grafts that become functional quickly, underpinning growth momentum in this configuration segment.

By End User: Hospital Dominance Shifts Toward Dialysis Centers

Hospitals captured 62.71% of 2025 revenues owing to surgical placement capabilities and complex patient management needs. The hemodialysis vascular access grafts market size attributable to hospitals is projected to reach USD 221.88 million by 2031, but their share will erode modestly as dialysis centers, expanding at 5.71% CAGR, increase procedural volumes. Center-based growth reflects decentralised care models; facilities are investing in in-house access maintenance to reduce costly hospital referrals.

Ambulatory surgical centers are gaining traction for same-day graft placements, and policy moves to boost home dialysis broaden the clinical settings requiring dependable graft options. Vendors offering streamlined training and post-operative support can capitalise on this transition across end-user categories.

Geography Analysis

North America held 37.10% of the hemodialysis vascular access grafts market in 2025, supported by Medicare’s PPS and widespread adherence to “Fistula First, Catheter Last” guidelines. The presence of innovation hubs and accelerated FDA pathways promotes early adoption of heparin-bonded and early-cannulation designs. Merit Medical’s WRAPSODY endoprosthesis, commercialised in January 2025, illustrates ongoing domestic device advancement with a 70.1% target-lesion primary patency rate at 12 months.

APAC is forecast to expand at 6.63% CAGR to 2031, driven by large CKD populations and improving reimbursement in China, India, and Southeast Asia. Yet disparities persist; high treatment costs in lower-income countries limit utilisation, while Japan and South Korea represent mature high-value markets. Terumo’s Puerto Rico manufacturing expansion, announced in 2024, positions the firm to serve both North American and fast-growing APAC demand efficiently.

Europe remains steady, supported by coordinated reimbursement systems that favour technologies with proven clinical value. The continent’s push toward home dialysis aligns with early-cannulation adoption trends. Latin America and the Middle East & Africa offer niche growth pockets, yet constrained health budgets and lower graft penetration temper short-term prospects. Overall, regional variability emphasises the necessity of tailored commercial strategies within the hemodialysis vascular access grafts market.

Competitive Landscape

The market presents moderate concentration, with W.L. Gore & Associates, Terumo Corporation, and B. Braun Melsungen anchoring global supply through proprietary ePTFE chemistries, heparin-bonding expertise, and expansive distribution. Gore’s portfolio spans STRETCH, ACUSEAL, and PROPATEN, enabling surgeons to match graft type to patient risk profile. Terumo’s vascular closure innovations support a complementary access hardware offering, enhancing account penetration. B. Braun’s 2024 launch of Heparin Sodium 2,000 units in saline shows the firm’s commitment to adjunct therapies that preserve graft patency bbraunusa.com.

Tissue-engineering entrants pose disruption potential. Humacyte’s FDA-cleared acellular vessel and planned Investigational New Drug (IND) filing for small-diameter coronary use expand the technology’s addressable market humacyte.gcs-web.com. 3D-bioprinted grafts achieved functional blood flow in 2025 preclinical models, foreshadowing long-term competitive pressure on synthetic demand nature.com.

M&A activity is elevating entry barriers. Teleflex’s EUR 760 million acquisition of BIOTRONIK’s devices and Merit Medical’s USD 120 million Biolife deal underscore the value of scale and product-line breadth. Suppliers combining devices, coatings, and ancillary hemostatic products can better meet integrated delivery network requirements, thereby consolidating share within the hemodialysis vascular access grafts market.

Hemodialysis Vascular Grafts Industry Leaders

W. L. Gore & Associates, Inc.

Vascudyne, Inc.

LeMaitre

Getinge AB

CryoLife, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for about EUR 760 million, broadening its interventional portfolio.

- January 2025: Humacyte announced plans to file an IND for a small-diameter acellular tissue-engineered vessel in coronary bypass.

- January 2025: Merit Medical began US rollout of the WRAPSODY Cell-Impermeable Endoprosthesis after December 2024 FDA approval

Global Hemodialysis Vascular Grafts Market Report Scope

As per the report's scope, hemodialysis vascular grafts or arteriovenous (AV) grafts are medical devices used to connect an artery and a vein in people who need hemodialysis. They are designed to be durable, provide adequate blood flow rates for efficient dialysis, and resist infection and clotting.

The hemodialysis vascular grafts market is segmented by raw material and geography. By raw material, the market is segmented into polyester, polytetrafluoroethylene, polyurethane, and biological materials. By biological material, the market is segmented into human saphenous & umbilical veins and tissue-engineered materials. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| PTFE |

| Heparin-bonded ePTFE |

| Polyurethane |

| Biosynthetic |

| Biological / Tissue-engineered |

| Early-cannulation |

| Conventional |

| Hospitals |

| Dialysis Centers |

| Ambulatory Surgical Centers |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Material | PTFE | |

| Heparin-bonded ePTFE | ||

| Polyurethane | ||

| Biosynthetic | ||

| Biological / Tissue-engineered | ||

| By Configuration | Early-cannulation | |

| Conventional | ||

| By End User | Hospitals | |

| Dialysis Centers | ||

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hemodialysis vascular access grafts market?

The market stood at USD 285.06 million in 2026 and is forecast to reach USD 357.38 million by 2031.

Which material leads the hemodialysis vascular access grafts market?

PTFE accounts for the largest revenue share at 45.02% in 2025, benefiting from decades of clinical use.

Why are early-cannulation grafts gaining popularity?

They allow dialysis to start within hours of implantation, lowering catheter-related infection risks and hospital costs.

Which region is growing fastest in this market?

Asia-Pacific is projected to expand at a 6.63% CAGR through 2031 due to rising CKD incidence and improving reimbursement.

How does antimicrobial resistance affect graft adoption?

Increasing infections by multidrug-resistant organisms elevate complication risks, pressuring manufacturers to enhance antimicrobial coatings.

What years does this Hemodialysis Vascular Grafts Market cover, and what was the market size in 2025?

In 2025, the Hemodialysis Vascular Grafts Market size was estimated at USD 285.06 million. The report covers the Hemodialysis Vascular Grafts Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Hemodialysis Vascular Grafts Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: