Global Renal Dialysis Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

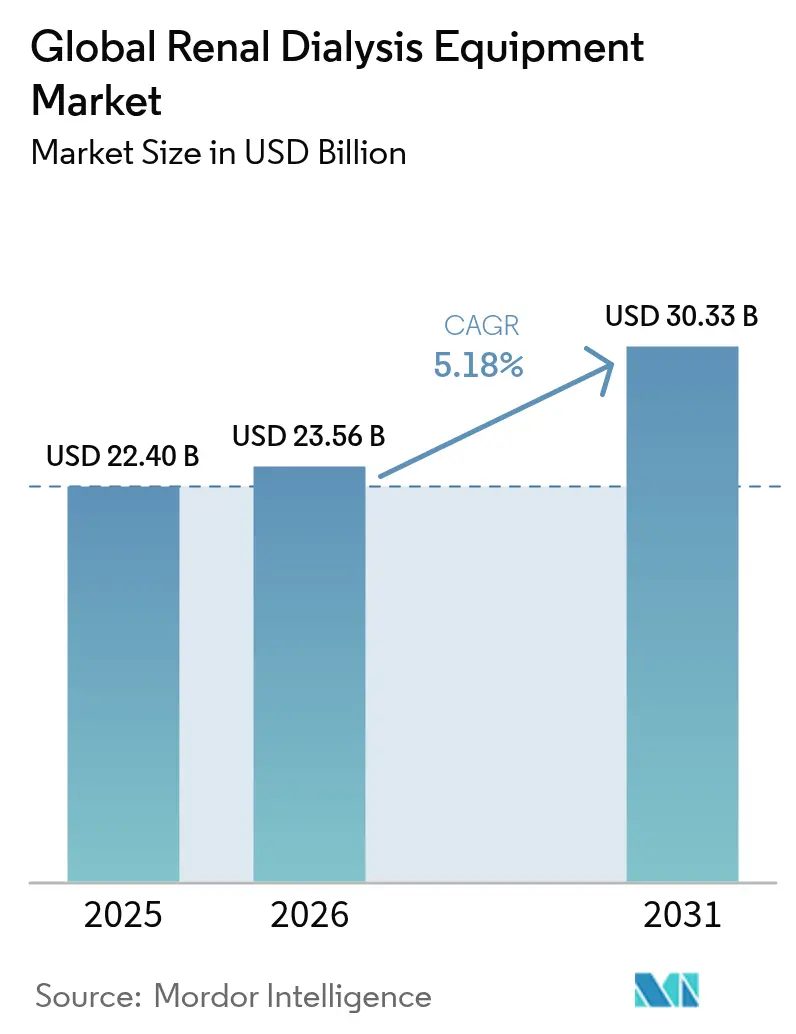

| Market Size (2026) | USD 23.56 Billion |

| Market Size (2031) | USD 30.33 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Renal Dialysis Equipment Market Analysis by Mordor Intelligence

The renal dialysis equipment market size is expected to grow from USD 22.40 billion in 2025 to USD 23.56 billion in 2026 and is forecast to reach USD 30.33 billion by 2031 at 5.18% CAGR over 2026-2031. Demographic aging, rising diabetes prevalence, and chronic kidney disease (CKD) incidence are sustaining demand, while Medicare’s 2025 End-Stage Renal Disease (ESRD) payment update and similar reimbursement reforms worldwide are accelerating a shift from in-center delivery models to home-based care. Leading manufacturers are introducing compact, water-efficient machines that lower infrastructure needs, and service providers are investing in AI-enabled predictive maintenance to minimize downtime and improve clinical outcomes. Supply-chain resilience and environmental sustainability have become strategic priorities following recent raw-material shortages and tougher regulations on single-use plastics. Concurrently, capital inflows into wearable and portable sorbent-based devices point to a medium-term transition toward patient-centric, resource-light treatment paradigms.

Key Report Takeaways

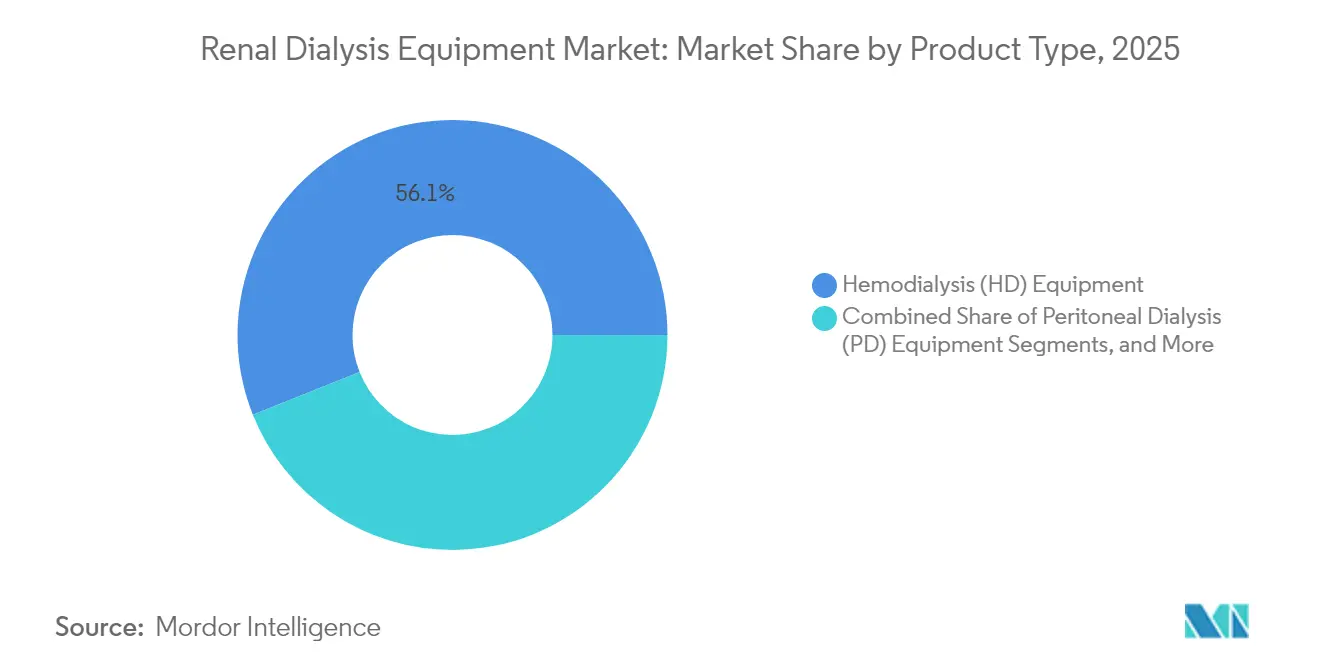

- By product type, hemodialysis equipment led with 56.05% of renal dialysis equipment market share in 2025, while peritoneal dialysis equipment is projected to rise at a 6.42% CAGR through 2031.

- By application, hemodialysis accounted for 81.65% share of the renal dialysis equipment market size in 2025; peritoneal dialysis applications are expected to grow at a 6.19% CAGR to 2031.

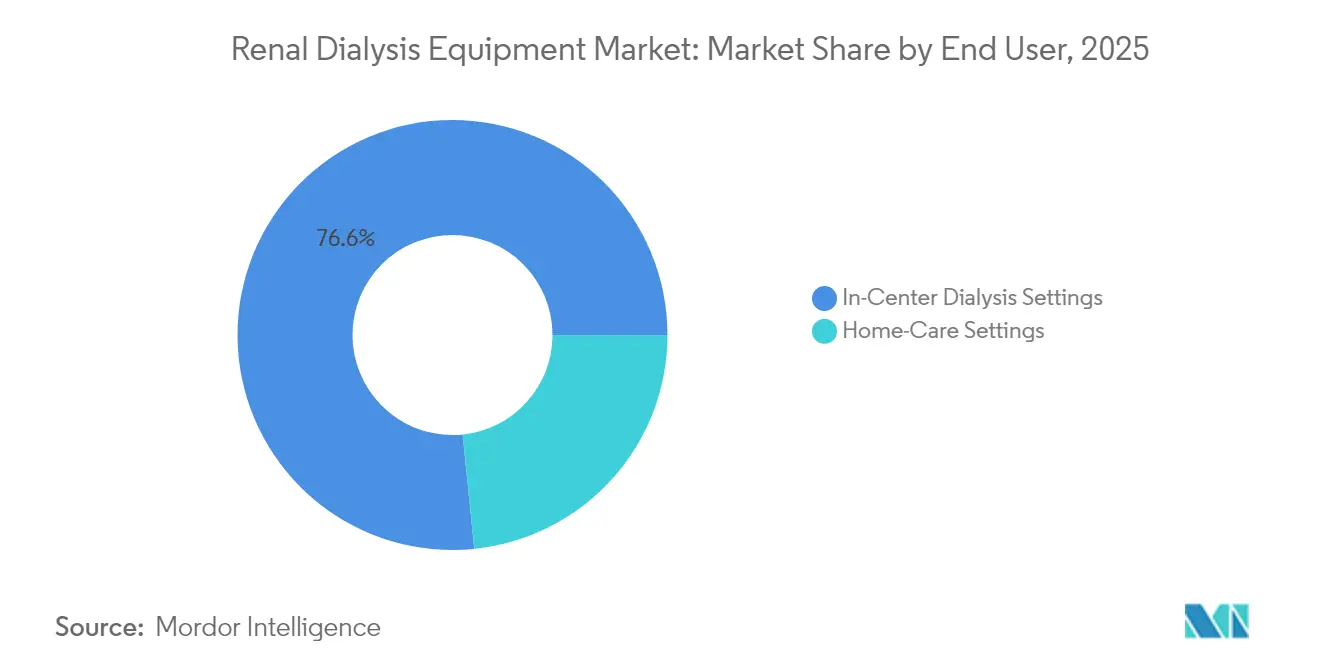

- By end user, in-center settings commanded 76.62% revenue share in 2025; the home-care segment is forecast to expand at 5.88% CAGR between 2026-2031.

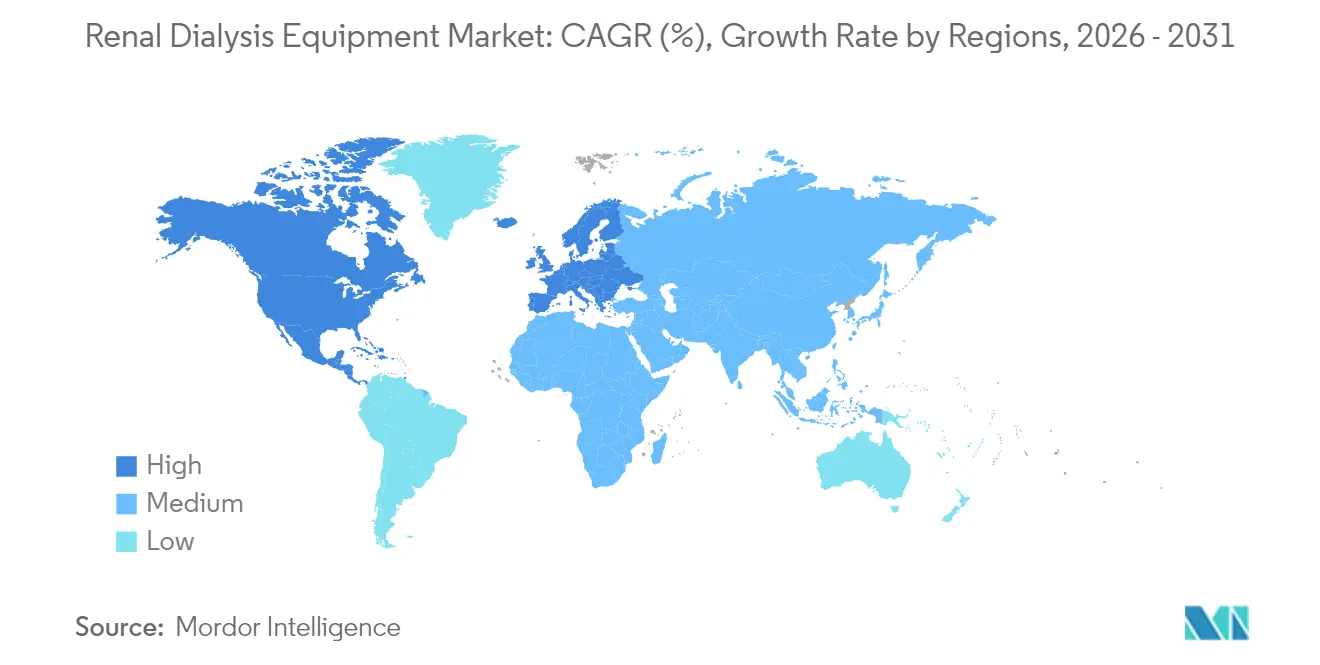

- By geography, North America held 43.02% of the renal dialysis equipment market in 2025, whereas Asia-Pacific is poised to register the fastest 6.86% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Renal Dialysis Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for peritoneal dialysis | +1.2% | Global; strongest in Asia-Pacific and Latin America | Medium term (2-4 years) |

| R&D spending for next-generation equipment | +0.8% | North America & Europe; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Increasing CKD prevalence | +1.5% | Global; highest burden in low- and middle-income regions | Long term (≥ 4 years) |

| Adoption of portable sorbent-based systems | +0.7% | North America & Europe | Medium term (2-4 years) |

| AI-enabled predictive maintenance | +0.4% | Developed markets with advanced infrastructure | Medium term (2-4 years) |

| Net-zero, water-less dialysis technologies | +0.6% | Global; priority in water-scarce regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Peritoneal Dialysis

Peritoneal dialysis use is rising as clinical evidence confirms survival rates comparable to in-center hemodialysis and highlights lower infection exposure for patients treated at home. The United States Renal Data System (USRDS) reported a 70% jump in incident home-dialysis starts between 2012 and 2022, supported by Medicare’s 2025 ESRD Treatment Choices Model incentives [1]US Renal Data System, “2024 USRDS Annual Data Report,” usrds.nih.gov. Latin America illustrates the trend, with Mexico accounting for one-quarter of the world’s peritoneal population. Nonetheless, access gaps driven by limited surgical training and patient education persist in several regions. Clinical societies now recommend early modality education to lift adoption, and device makers are launching automated cyclers that simplify set-up and monitoring.

Growth in R&D Expenditure for New Dialysis Products

Top manufacturers have earmarked multi-year R&D budgets to upgrade dialysis platforms. Fresenius Medical Care secured FDA clearance for its 5008X system, which delivers high-volume hemodiafiltration and targets replacement of legacy machines [2]U.S. Food and Drug Administration, “510(k) Clearance K230145: 5008X Hemodialysis System,” fda.gov. Vantive, the newly spun-out Baxter kidney-care entity, plans USD 1 billion of investment over five years to commercialize portable and implantable technologies. Academic groups add momentum: the University of Portsmouth demonstrated predictive-maintenance algorithms that cut machine downtime by 30%, while Seoul National University is advancing nano-electrokinetic pumps for compact peritoneal units. Funding programs such as KidneyX have awarded USD 17 million since 2023, ensuring a steady pipeline of projects.

Increasing Prevalence of Chronic Kidney Disease (CKD)

CKD affected 37 million Americans in 2025, and epidemiological reviews recorded 18.99 million new global cases in 2019, reflecting a sustained burden that underpins renal dialysis equipment market growth. Diabetes and hypertension remain leading risk factors; the CDC estimates Medicare spent USD 87.2 billion on CKD in 2024, nearly 8% of its budget. Low-income countries face the sharpest rise in incidence yet lack adequate therapy capacity, creating sizable white-space opportunities for cost-optimized devices. Modeling studies forecast CKD-related deaths to top 1.81 million by 2030, ensuring demand for dialysis and transplantation outpaces supply.

Adoption of Portable Sorbent-Based Dialysis Systems

Portable systems that regenerate dialysate through sorbent cartridges dramatically reduce water consumption and infrastructure costs. Quanta Dialysis Technologies’ SC+ platform received FDA clearance for home use with flow rates equal to in-center machines while operating on standard tap water. Clinical testing shows pulsatile push-pull flows enhance solute clearance by 10-15%, and facilities benefit from faster room turnover and lower utility bills. Investor confidence surged after Quanta’s USD 245 million Series D round, enabling global scale-up and acute-care applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complications and risks during dialysis | -0.8% | Global; higher impact in developing regions | Short term (≤ 2 years) |

| Reimbursement limitations in emerging markets | -1.2% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Volatile supply of medical-grade resins | -0.6% | Global; acute in North America & Europe | Short term (≤ 2 years) |

| Regulatory scrutiny on single-use plastics | -0.4% | Europe & North America; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complications & Risks Associated with Dialysis Procedures

Safety alerts issued by the FDA in 2024 detailed toxic-compound leaching from silicone tubing in pediatric circuits, prompting rapid redesigns and material substitutions fda.gov. Vascular-access infection remains a leading cause of hospitalization; the CMS ESRD Measures Manual showed that catheter use correlated with higher sepsis rates than arteriovenous fistulas. Peritoneal dialysis peritonitis is declining but continues to deter clinicians in settings with limited training. These complications inflate treatment costs and can delay therapy initiation, slowing overall equipment uptake.

Reimbursement Limitations in Emerging Markets

The Clinical Journal of the American Society of Nephrology found that 90% of surveyed governments reimburse maintenance dialysis but that payment rates track closely with national GDP, leaving substantial gaps in Asia-Pacific and parts of Africa. Registry data reveal renal replacement therapy prevalence closely mirrors gross national income, confirming financial access as the primary hurdle. Because the highest CKD growth occurs where reimbursement is weakest, manufacturers must tailor lower-cost models, localize production, and partner with charities to unlock demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hemodialysis Platforms Remain Dominant While Peritoneal Equipment Gains Momentum

Hemodialysis machines, water-treatment systems, and ancillary disposables accounted for 56.05% of renal dialysis equipment market share in 2025 underpinned by decades of installed infrastructure and clinician familiarity. The 5008X high-volume hemodiafiltration unit is expected to refresh fleets across major U.S. providers, signaling sustained investment in conventional platforms. In contrast, peritoneal dialysis cyclers are forecast to post a 6.42% CAGR, buoyed by payer incentives and advances in user-friendly interfaces. Automated cyclers equipped with remote telemetry are expanding uptake among elderly and rural patients, and new biocompatible solutions are reducing peritonitis rates. Concentrates and solutions also benefit from CMS policy changes that bring oral phosphate binders into the bundled payment, enlarging adjunct revenue streams.

Peritoneal equipment momentum is strongest in Mexico, China, and the United States, where transitional care units guide candidates through modality selection. Supply-chain tightness for plastic bloodlines and cartridges spotlighted the need for multi-source procurement strategies, yet manufacturers with vertically integrated resin capacity are navigating disruptions better than peers. Sustainability targets are accelerating a shift to recyclable cartridges, and research consortia are trialing plant-based polymers for dialyzer housings. As home uptake rises, after-sales service and 24-hour technical support emerge as key competitive differentiators.

By Application: Conventional Hemodialysis Leads but Home-Based Modalities Accelerate

Conventional in-center hemodialysis retained 81.65% of the renal dialysis equipment market size in 2025, reflecting worldwide standardization of thrice-weekly regimens. AI-driven sensors within modern machines now adjust ultrafiltration in real time, lowering hypotension events and aligning with quality metrics. Short-daily and nocturnal variants are growing from a small base, supported by outcome data indicating superior fluid management and patient-reported quality of life.

Peritoneal dialysis applications, although smaller, are set to expand at 6.19% CAGR. Continuous ambulatory peritoneal dialysis (CAPD) dominates Latin American practice, whereas automated peritoneal dialysis (APD) gains traction in developed economies. The 2024 USRDS report showed that 45.6% of U.S. clinics still lack home-dialysis certification, offering a large conversion pool once training barriers are removed. Emerging telehealth platforms allow nephrologists to review real-time data and intervene proactively, raising confidence in home care.

By End User: Facility-Based Care Prevails as Home-Care Growth Outpaces

In-center facilities captured 76.62% revenue in 2025, supported by economies of scale and immediate clinical oversight. Fresenius Medical Care and DaVita, through vertical integration, standardize protocols and consolidate procurement, reinforcing their purchasing power. Hospital-based units treat higher-acuity patients and maintain larger proportions of peritoneal cases due to surgical resources.

Home-care settings, though nascent, are predicted to grow 5.88% annually. The Medicare home-dialysis payment adjustment and FDA clearance of machines that run on tap water lower entry hurdles. Transitional training programs report conversion rates above 40%, indicating patient willingness when education is structured. Remote monitoring platforms feeding into electronic health records facilitate regulatory compliance and early adverse-event detection.

Geography Analysis

North America retained 43.02% of the renal dialysis equipment market in 2025 thanks to robust reimbursement, extensive clinic networks, and rapid device approvals. Medicare spent USD 75 billion on CKD beneficiaries in 2024, and CMS raised the ESRD base rate to USD 273.82 in 2025, directly boosting provider capital budgets . Canada’s single-payer model guarantees nationwide dialysis coverage, while Mexico leads peritoneal usage globally due to sustained policy backing. Although Hurricane-related disruptions to a key North Carolina dialyzer plant exposed supply‐chain concentration, FDA emergency-use authorizations enabled alternative sourcing, prompting manufacturers to diversify footprints.

Europe constitutes the second-largest region, characterized by strict environmental directives that favor low-water, low-waste systems. National health services in Germany, France, and the United Kingdom fund universal access, and the European Renal Association promotes cross-border clinical guidelines to harmonize quality standards. Italy’s nephrology society published a ten-step green framework in 2024, encouraging dialyzer reprocessing and renewable-energy adoption within clinics. Regulatory updates aligning ISO 23500 water-purity limits with AAMI guidelines are pushing vendors to upgrade filtration modules across the installed base.

Asia-Pacific is the fastest-growing territory at a projected 6.86% CAGR. Japan records the world’s highest ESRD prevalence and maintains sophisticated reimbursement for thrice-weekly in-center hemodialysis. China and India face a 66% access gap, representing the largest latent demand pool. Government-led insurance expansions, private-equity investment in dialysis chains, and public-private partnerships for rural outreach are narrowing disparities. Australia and South Korea showcase near-universal coverage and are early adopters of tele-monitored home systems. Multinationals are increasingly establishing localized assembly plants to meet price-sensitive segments and qualify for procurement tenders.

Competitive Landscape

The renal dialysis equipment market is highly concentrated. Fresenius Medical Care and DaVita collectively treat 69% of U.S. patients at 65% of facilities, and Fresenius supplies a significant share of machines to its own sites, reinforcing vertical control. Fresenius’s acquisition of NxStage strengthened its home-hemodialysis roster, while DaVita leverages analytics to optimize capacity utilization. Baxter completed a USD 3.8 billion carve-out of its kidney-care arm, Vantive, allocating USD 1 billion to accelerate wearable and implantable technologies, a move that could reshape competitive dynamics by 2028.

Emerging challengers center on portability and user simplicity. Outset Medical’s Tablo integrates water purification and supports acute and chronic settings, enabling hospitals to deploy dialysis beyond dedicated units. Quanta’s SC+ delivers clinic-grade performance in a trolley-size footprint and has accumulated more than 1 million treatment hours worldwide. Device makers are also courting sustainability: Nipro introduced dialyzers with reduced-carbon membranes, and B. Braun is piloting recyclable cartridge programs that aim to cut plastic waste by 40% per treatment.

Strategic alliances are proliferating. Fresenius partnered with Nvidia in 2025 to embed AI workflows that detect coagulation anomalies before alarms trigger, while Baxter signed a memorandum with Tencent to integrate tele-monitoring into its automated peritoneal cyclers for the Chinese market. Suppliers are pairing equipment with cloud analytics, consumable subscriptions, and patient-education apps to lock in long-term revenue and differentiate beyond hardware specifications.

Global Renal Dialysis Equipment Industry Leaders

Fresenius Kabi AG

Baxter International, Inc.

Nikkiso Co, Ltd.

Nipro Corporation

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Four Square Medical Center, Coimbatore, launched the Dimi Home Dialysis Machine, a RO-free system engineered for residential use.

- October 2024: Nephro Care India Ltd. and NIT Silchar unveiled a prototype AI-enabled smart hemodialysis machine expected to lower treatment costs by up to 75%.

- March 2024: Nipro Medical Corporation introduced the SURDIAL DX Hemodialysis System to the United States.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the renal dialysis equipment market as all new machines and disposables that directly perform hemo or peritoneal dialysis for chronic or acute kidney failure patients, valued at the point of first sale from the manufacturer. This includes standalone hemodialysis units, peritoneal cyclers, associated water treatment modules, bloodline systems, dialyzers, and patient specific fluid cartridges. Devices for continuous renal replacement therapy that share identical filtration architecture are also counted.

Scope Exclusions: Rental services, procedure fees, dialysis chairs, and general hospital equipment are not included.

Segmentation Overview

- By Product Type

- Hemodialysis (HD) Equipment

- Dialysis Machines

- Dialyzers

- Bloodlines & Tubing Sets

- Water Treatment Systems

- Peritoneal Dialysis (PD) Equipment

- Automated PD Cyclers

- Portable PD Devices

- Concentrates & Solutions

- Other Accessories

- Hemodialysis (HD) Equipment

- By Application

- Hemodialysis

- Conventional HD

- Short-Daily HD

- Nocturnal HD

- Peritoneal Dialysis

- CAPD

- APD

- Hemodialysis

- By End User

- In-Center Dialysis Settings

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Multiple semi structured interviews with nephrologists, procurement managers, and aftermarket engineers across North America, Europe, and high growth Asian economies allowed us to stress test uptake rates for home dialysis, validate import statistics, and gather realistic ASP corridors. Continuous e surveys with patient advocacy groups further clarified modality preferences and replacement intervals.

Desk Research

We began with publicly available anchors, kidney disease prevalence tables from the WHO, ESRD counts from the USRDS and ERA Registry, import export codes for 901890 and 842129 under UN Comtrade, and tariff filings from major customs unions because they report verifiable shipment or patient numbers. Trade association briefs from the International Society of Nephrology, safety alerts from the FDA MAUDE database, and patent families retrieved through Questel helped us map technological diffusion and replacement cycles. Our team then tapped paid repositories such as D&B Hoovers for company revenue splits and Dow Jones Factiva for pricing news. These sources illustrate market volume baselines, typical average selling prices, and procurement trends; many additional references were consulted beyond those listed here.

Market Sizing and Forecasting

We modeled the market top down, first projecting the treated ESRD population by country and multiplying by dialysis modality penetration and machine to patient ratios; results were cross checked bottom up with sampled supplier shipments and channel checks before final calibration. Critical variables include chronic kidney disease prevalence, machine service life, average annual treatment sessions, home based adoption shares, public reimbursement ceilings, and median machine ASP movements. A multivariate regression links these drivers to historical revenue to forecast through 2030, and scenario analysis adjusts for reimbursement shocks or technology breakthroughs.

Data Validation and Update Cycle

Outputs pass a three layer review, analyst, senior analyst, and domain lead. Variances beyond ±5% versus fresh shipment or registry data trigger model reruns. We refresh every twelve months, with interim updates when regulatory or recall events materially alter demand.

Why Mordor's Renal Dialysis Equipment Baseline Stands Reliable

Published figures often diverge because players choose different device groupings, price definitions, and update rhythms. We disclose our device only lens, current ASP stack, and yearly refresh so decision makers instantly see what is and is not inside the number.

Key gap drivers include some publishers rolling consumables and multiyear service contracts into equipment revenue, others excluding home care cyclers, and a few converting sales using spot exchange rates instead of fiscal year averages, inflating totals in volatile currency periods. Our disciplined scoping and mid year currency reconciliation limit such swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.17 B (2024) | Mordor Intelligence | - |

| USD 98.51 B (2024) | Global Consultancy A | Bundles machines with fluids and maintenance services; bases totals on hospital spend proxies |

| USD 19.52 B (2024) | Industry Publisher B | Uses factory gate prices and omits home dialysis systems from scope |

In sum, Mordor's transparent device list, patient based demand pool, and dual validation steps produce a balanced baseline that clients can trace back to tangible variables and replicate with limited resources, something broader or narrower lenses cannot guarantee.

Key Questions Answered in the Report

How big is the Global Renal Dialysis Equipment Market?

The Global Renal Dialysis Equipment Market size is expected to reach USD 23.56 billion in 2026 and grow at a CAGR of 5.18% to reach USD 30.33 billion by 2031.

What is the current Global Renal Dialysis Equipment Market size?

In 2026, the Global Renal Dialysis Equipment Market size is expected to reach USD 23.56 billion.

Who are the key players in Global Renal Dialysis Equipment Market?

Fresenius Kabi AG, Baxter International, Inc., Nikkiso Co, Ltd., Nipro Corporation and B. Braun Melsungen AG are the major companies operating in the Global Renal Dialysis Equipment Market.

Which is the fastest growing region in Global Renal Dialysis Equipment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Renal Dialysis Equipment Market?

In 2025, the North America accounts for the largest market share in Global Renal Dialysis Equipment Market.

What years does this Global Renal Dialysis Equipment Market cover, and what was the market size in 2025?

In 2025, the Global Renal Dialysis Equipment Market size was estimated at USD 23.56 billion. The report covers the Global Renal Dialysis Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Renal Dialysis Equipment Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: