Global Kidney Function Tests Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

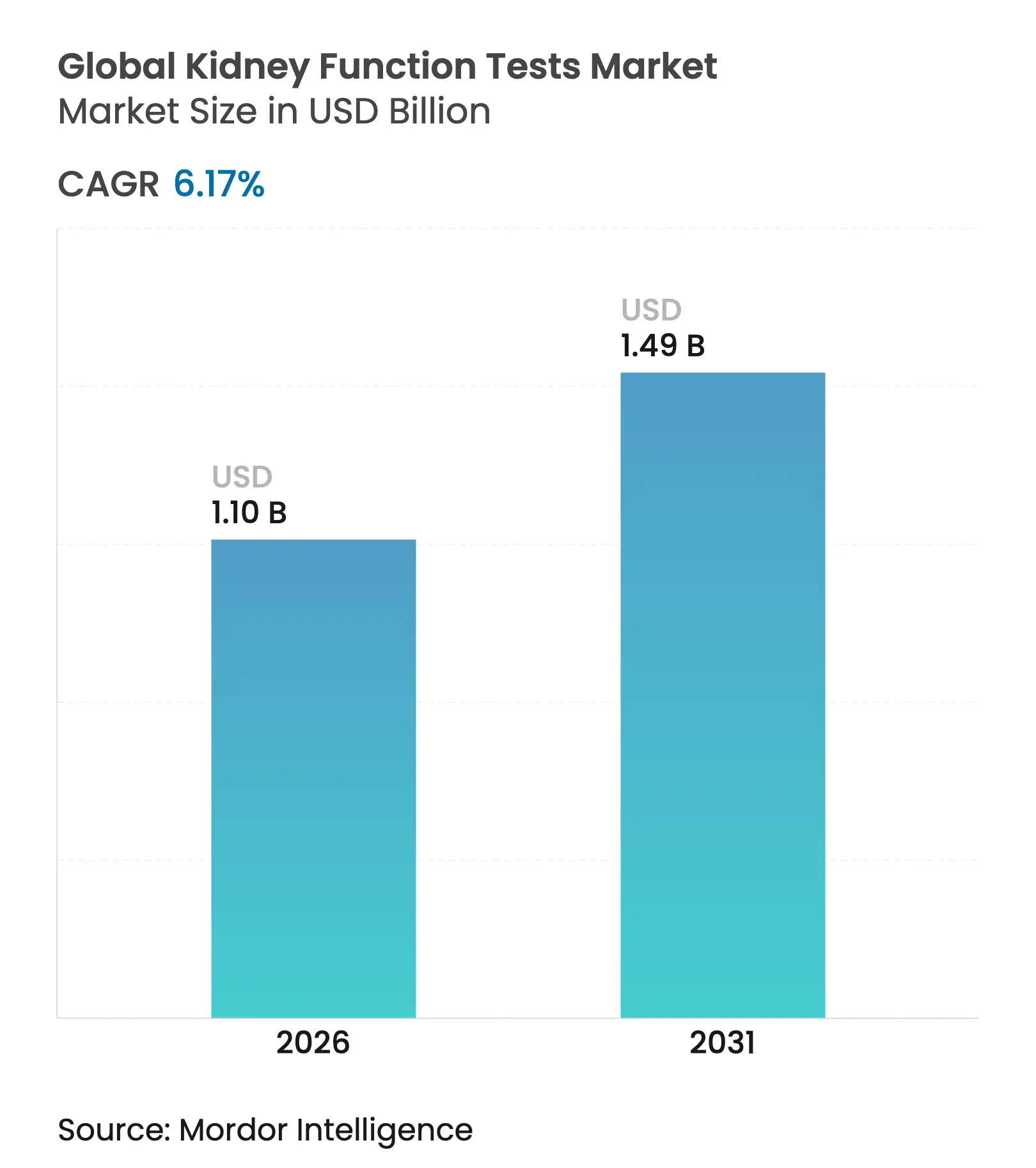

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 6.17 % CAGR |

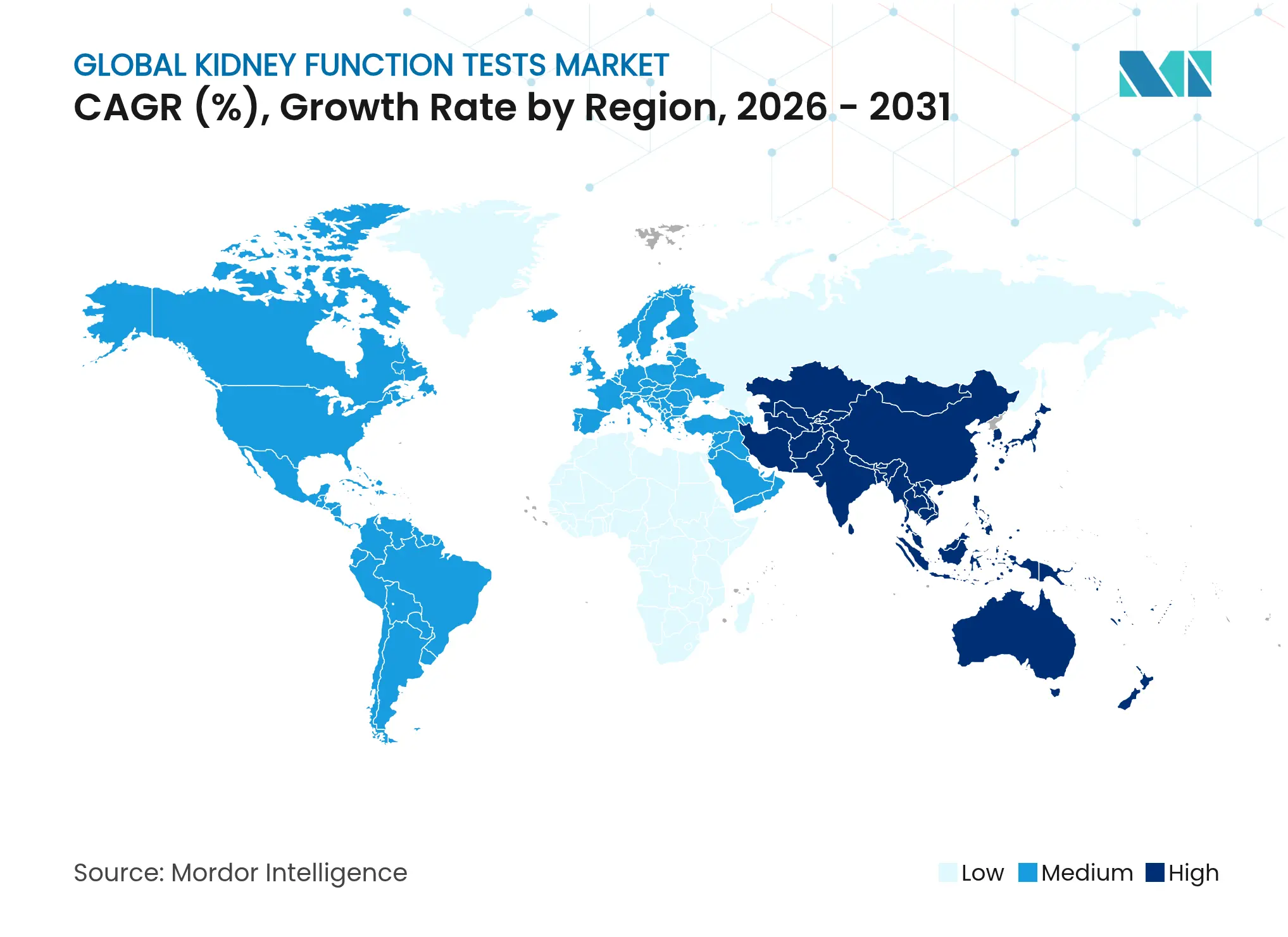

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

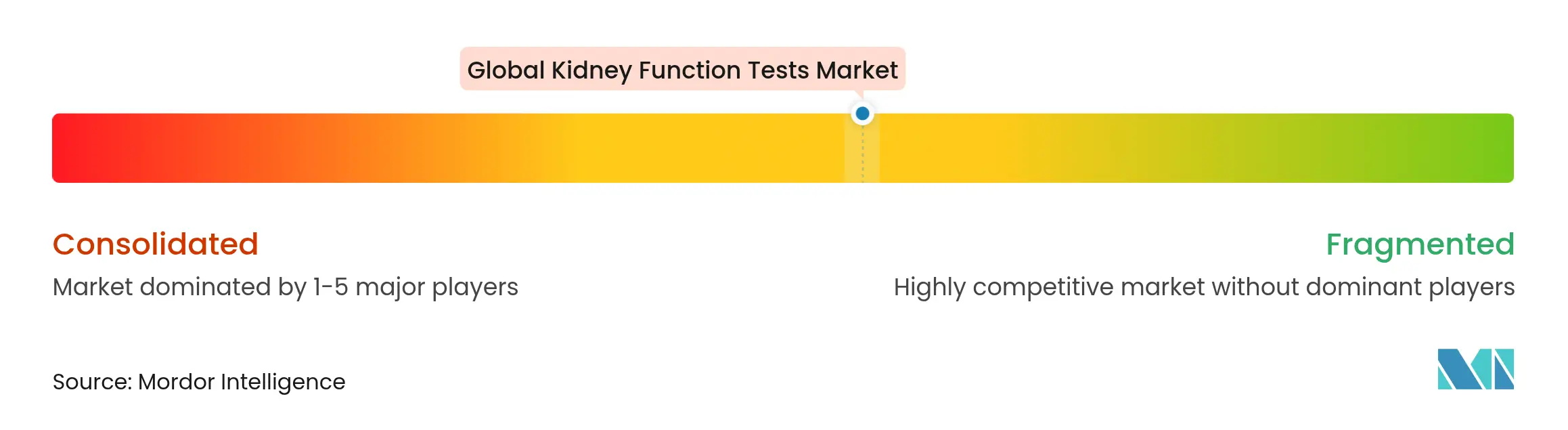

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Global Kidney Function Tests Market Analysis by Mordor Intelligence

Kidney function test market size in 2026 is estimated at USD 1.1 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD 1.49 billion, growing at 6.17% CAGR over 2026-2031. This growth links directly to a worldwide chronic kidney disease (CKD) burden that already exceeds 850 million people, with diabetes and hypertension acting as the principal catalysts. Point-of-care (POC) diagnostics, artificial-intelligence (AI) decision support, and home-based monitoring are reshaping test demand by moving assessments closer to patients. Government-backed screening initiatives such as expanded Medicare coverage for home dialysis and inclusion of oral-only drugs in the End-Stage Renal Disease (ESRD) bundle are reinforcing the shift toward decentralized testing models. Asia-Pacific exhibits the fastest regional momentum, while North America retains scale leadership because of comprehensive reimbursement and advanced diagnostic infrastructure. Against this backdrop, consolidation among conventional diagnostics firms and rapid entry by smartphone-based platforms are intensifying competition and forcing suppliers to differentiate through automation, multi-analyte panels, and clinical-decision software.

Key Report Takeaways

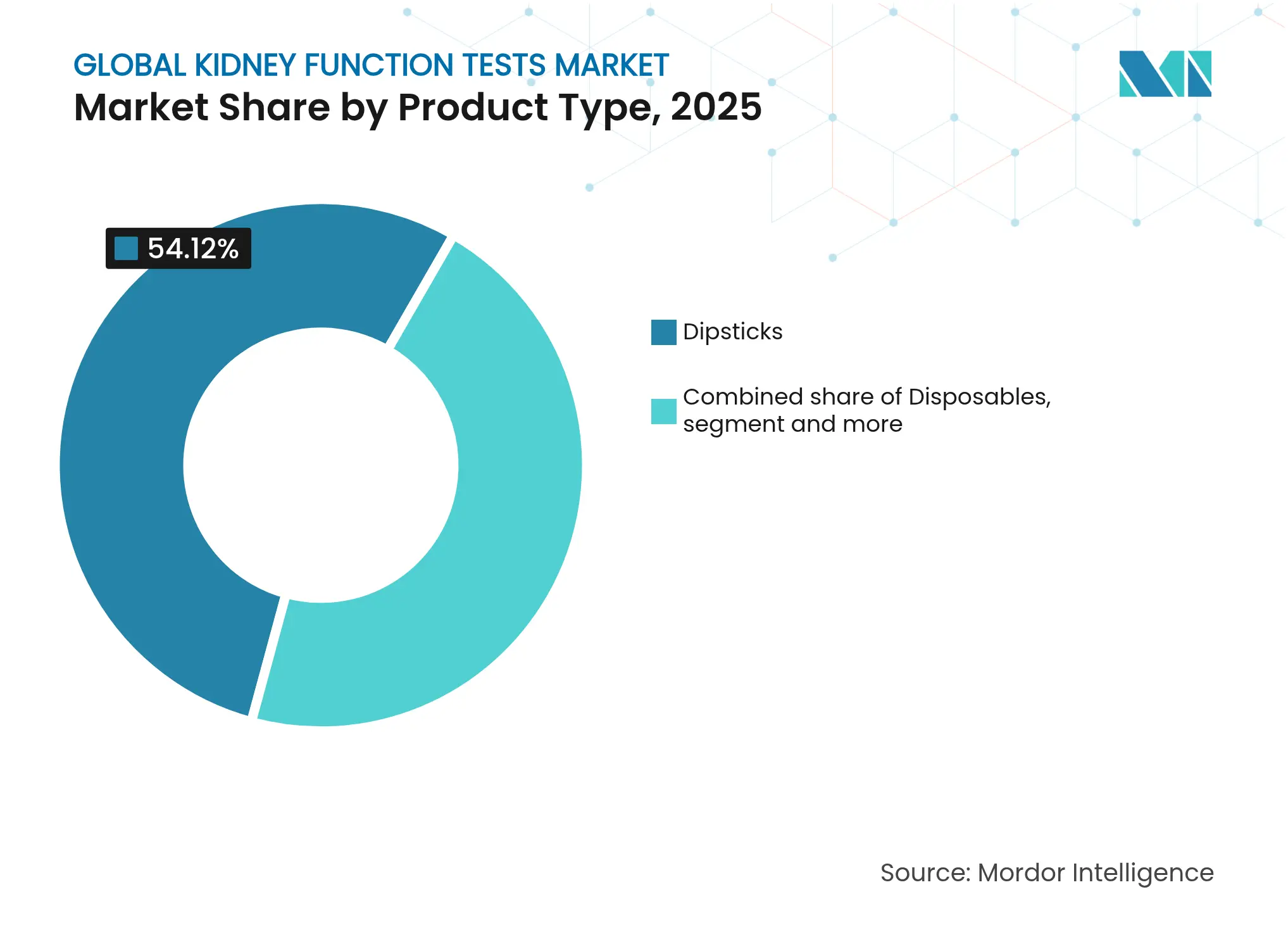

- By product type, dipsticks held 54.12% of kidney function tests market share in 2025; reagents are projected to advance at a 7.24% CAGR through 2031.

- By test type, urine testing accounted for 61.75% share of the kidney function tests market size in 2025, whereas blood-based assays are expanding at 6.95% CAGR between 2026-2031.

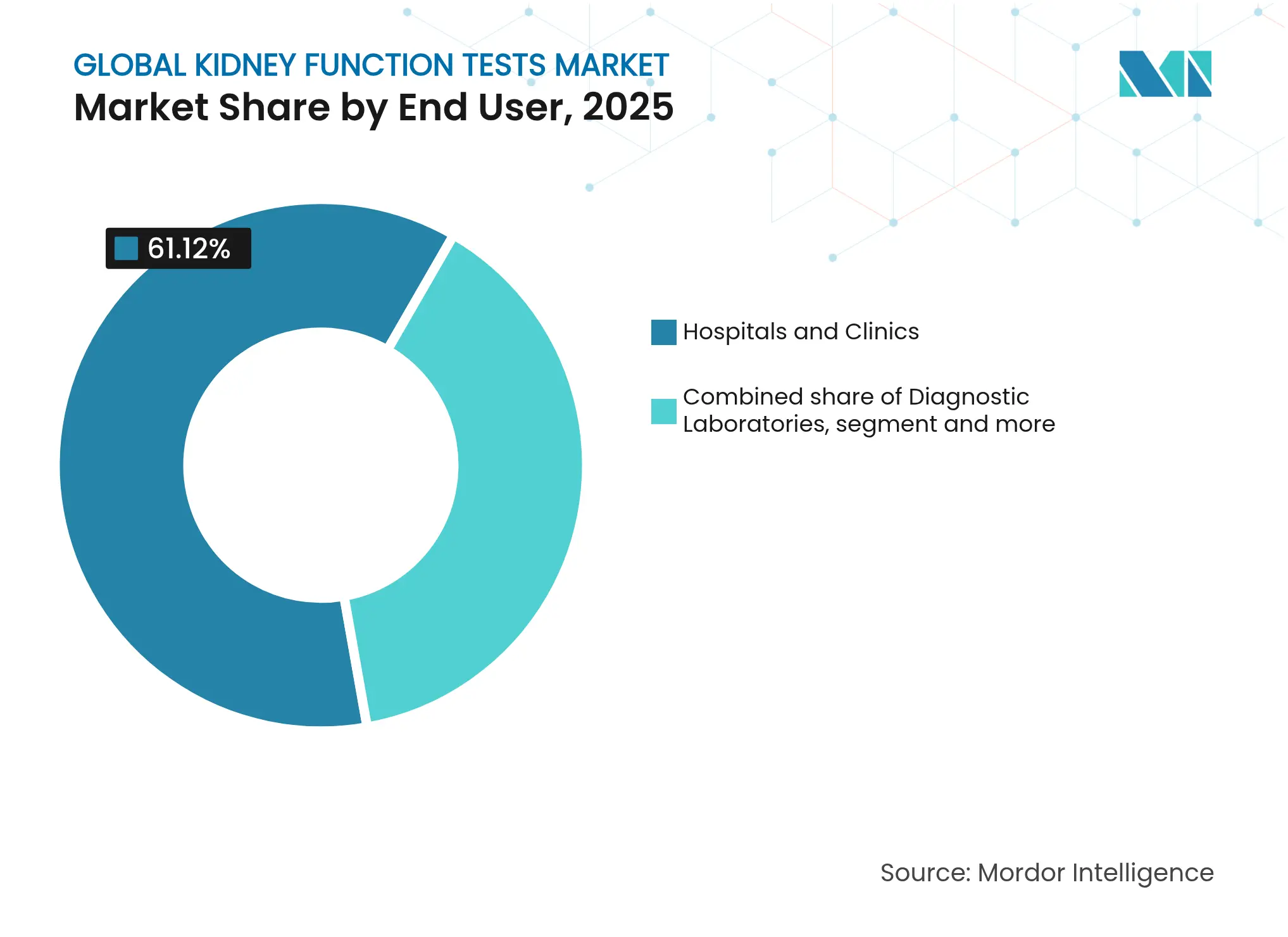

- By end user, hospitals and clinics controlled 61.12% revenue share in 2025; home and POC settings represent the fastest-growing channel at 7.63% CAGR to 2031.

- By testing settings, central-lab based accounted for 70.62% share of the kidney function tests market size in 2025, whereas point-of-care is expanding at 7.86% CAGR between 2026-2031.

- By geography, North America captured 43.05% of kidney function tests market share in 2025; Asia-Pacific is forecast to post the highest 8.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kidney Function Tests Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of chronic kidney disease Rising prevalence of chronic kidney disease | +1.8% | Global, strongest in APAC and MEA | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, strongest in APAC and MEA | Impact Timeline:Long term (≥ 4 years) |

Growing diabetes & hypertension burden Growing diabetes & hypertension burden | +1.5% | Global, especially North America and Europe | Medium term (2-4 years) | |||

Government-backed CKD screening programs Government-backed CKD screening programs | +1.2% | North America, Europe, selected APAC economies | Medium term (2-4 years) | |||

Automation & POC technology advances Automation & POC technology advances | +1.0% | Global, early uptake in developed regions | Short term (≤ 2 years) | |||

Multi-omics plus AI biomarker panels Multi-omics plus AI biomarker panels | +0.8% | Initially North America and Europe, widening globally | Long term (≥ 4 years) | |||

Wearable and home-monitoring kidney sensors Wearable and home-monitoring kidney sensors | +0.6% | North America and Europe, progressive APAC penetration | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising prevalence of chronic kidney disease (CKD)

CKD now affects 13.4% of the global population, and health systems are scaling screening to stem dialysis demand. The Philippines extended its ACT NOW program to 12 provinces, providing more than 1 million free urine albumin-creatinine ratio tests.[1]Philippine News Agency, “ACT NOW for CKD Expands to 12 Provinces,” pna.gov.ph In India, the CITE study uncovered a 32% CKD prevalence among people living with type 2 diabetes, with risk increasing sharply after age 60 and a 10-year disease duration. Such evidence is pushing both high-income and emerging markets to adopt scalable, low-cost kidney function testing outside traditional laboratories. The kidney function tests market therefore benefits from predictable demand as public health agencies standardize screening protocols.

Growing diabetes & hypertension burden

The American Diabetes Association’s 2024 clinical guidance recommends annual albuminuria and estimated glomerular filtration rate (eGFR) evaluations for every adult with type 2 diabetes. Alignment with quality measures such as HEDIS and MIPS is rewarding providers who systematically test high-risk patients. Proteomics International commercialized PromarkerD in Australia, a blood test that flags diabetic kidney disease up to four years before symptom onset. These policies and tools channel patients toward proactive monitoring, ensuring steady growth in the kidney function tests market.

Government-backed CKD screening programs

More than 40 members of the U.S. Congress urged the Preventive Services Task Force to issue federal CKD screening recommendations in 2025. India’s Pradhan Mantri National Dialysis Program is scaling capacity for 3.4 crore dialysis sessions annually, underpinning test demand. CMS has embedded a Kidney Health Evaluation measure into multiple quality-reporting programs, mandating annual eGFR and urine ACR in adults with diabetes. Japan’s national claims database shows CKD diagnoses in 43.5% of patients when quantitative proteinuria results are available compared with only 5.9% when no protein data are captured. Such mandates reinforce routine testing and remove volume risk for suppliers.

Automation & POC technology advances

Healthy.io’s smartphone-based platform combines computer vision and colorimetry to convert a standard phone camera into a quantitative urinalysis tool, broadening access to home testing. Nova Biomedical’s FDA-cleared Stat Profile Prime Plus can deliver an 11-parameter panel, including creatinine and urea, from 90 µL of blood. An AI-enabled mobile urine-strip reader achieved 98.7% nitrite and 97.3% glucose detection accuracy, demonstrating near-laboratory performance outside central labs. These advances improve accuracy, cut turnaround, and lower staff skill requirements, amplifying adoption across pharmacies, community health centers, and patient homes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of analyzers & consumables High cost of analyzers & consumables | -1.4% | Global, especially LMICs and smaller clinics | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, especially LMICs and smaller clinics | Impact Timeline:Medium term (2-4 years) |

Stringent regulatory & reimbursement hurdles Stringent regulatory & reimbursement hurdles | -1.1% | Worldwide, most acute in North America and Europe | Long term (≥ 4 years) | |||

Lack of standardisation for novel biomarkers Lack of standardisation for novel biomarkers | -0.8% | Global, felt first in developed markets | Medium term (2-4 years) | |||

Supply-chain fragility for critical reagents Supply-chain fragility for critical reagents | -0.6% | APAC, MEA, South America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High cost of analyzers & consumables

Annual medical expenses for renal replacement therapy in Asia range from USD 2,901 to USD 18,668, while hemodialysis averages USD 23,358 per patient, underlining the need for cost-effective screening.[2]Cost Effectiveness and Resource Allocation, “Economic Burden of Renal Replacement Therapy in Asia,” resource-allocation.biomedcentral.com The FDA warned in March 2025 of bloodline shortages for hemodialysis equipment that could persist through early fall 2025. Ugandan clinicians cite price barriers, supply shortages, and weak infrastructure as primary obstacles to CKD testing. High capital costs thus impede analyzer placement in low-resource facilities, tempering uptake of some advanced platforms in the kidney function tests market.

Stringent regulatory & reimbursement hurdles

The FDA’s phased regulation of laboratory-developed tests began in 2024 with mandatory medical-device reporting and will culminate in full pre-market review by 2028. Demonstrating clinical utility for algorithms like KidneyIntelX remains a prerequisite for CMS payment approval, extending commercialization timelines. In Europe, transplantation stakeholders are navigating new advanced-therapy guidelines that add compliance steps for diagnostics used in donor evaluation. Meanwhile, private insurers in the United States reimburse dialysis at roughly triple Medicare rates, distorting incentives and complicating coverage expectations for novel tests. These dynamics lengthen time-to-market and raise capital needs for entrants.

Segment Analysis

By Product Type: Dipstick Leadership Endures While Reagents Accelerate

Dipsticks contributed 54.12% of kidney function tests market share in 2025 due to their low price, ease of use, and compatibility with routine urinalysis workflows. Demand spans hospital wards, outpatient clinics, and school health programs, anchoring baseline volumes. Reagents, however, are projected to expand at a 7.24% CAGR through 2031 as laboratories migrate toward automated, high-throughput chemistry platforms that cut technician time and improve analytical precision. The kidney function tests market size for reagents is forecast to increase alongside adoption of microfluidic cartridges and multi-analyte chemistry packs that bundle albumin, cystatin C, and β2-microglobulin into single runs. Disposables sit between these poles, benefiting from higher test counts yet experiencing price competition from generic suppliers.

Innovation revolves around reagent chemistry. Siemens Healthineers introduced an albumin-creatinine ratio test that delivers quantitative results within minutes and can process small urine volumes, making it suitable for pediatric and geriatric use. Multi-omics research has identified 32 circulating proteins linked to CKD progression, driving demand for specialized reagent panels able to detect multiplexed biomarkers. Procurement teams increasingly prioritize supplier packages that pair analyzers with proprietary reagent kits to guarantee calibration integrity. This bundling fortifies switching costs and sustains revenue visibility across the kidney function tests market.

Note: Segment shares of all individual segments available upon report purchase

By Test Type: Urine Dominance Persists, Blood Panels Gain Pace

Urine-based assays represented 61.75% of kidney function tests market size in 2025, reflecting their non-invasive nature and entrenched clinical guidelines. Micro-albumin testing is becoming a routine annual check for patients with diabetes or hypertension, while dipstick urinalysis remains the first-line screen in occupational and military health programs. Blood-based assays are forecast to grow 6.95% CAGR, underpinned by micro-sample technologies that require only finger-stick volumes. BD’s capillary collection device delivers sample integrity comparable with venous draws, helping laboratories integrate creatinine and cystatin C into comprehensive metabolic panels.

Serum creatinine remains central to eGFR calculations, yet cystatin C is gaining traction for older adults because it is less influenced by muscle mass. Research covering 675 serum and 542 urine metabolites significantly associated with renal function indicates looming expansion beyond classical markers. For suppliers, multi-analyte kits that combine both fluids offer cross-selling synergies, pushing margin growth in the kidney function tests market.

By End User: Home and POC Settings Form the New Growth Core

Hospitals and clinics generated 61.12% of 2025 revenue owing to centralized nephrology services, but home and POC environments are forecast to post a 7.63% CAGR through 2031. The shift gained traction during the COVID-19 pandemic, when health systems observed the operational value of remote monitoring. Stanford engineers designed a smartphone-assisted urinalysis device achieving 99.9% glucose detection accuracy, underscoring the viability of home testing at scale. Wearable bioimpedance sensors embedded in patches or belts provide continuous kidney status feedback and integrate with tele-nephrology portals.

Diagnostic laboratories hold steady demand because they run high-complexity assays such as metabolomic profiling and serve as confirmatory reference centers. Meanwhile, retail health channels are embedding POC creatinine readers like the Nova Max Pro that delivers an eGFR estimate in 30 seconds. The kidney function tests market therefore bifurcates into high-throughput core labs and high-accessibility decentralized sites, each requiring tailored reagent and device strategies.

Note: Segment shares of all individual segments available upon report purchase

By Testing Setting: Central Labs Retain Scale, Point-of-Care Surges

Central laboratories accounted for 70.62% revenue in 2025 because they bundle kidney markers with chemistry panels, manage data integration, and exploit economies of scale. Yet POC testing is expected to grow 7.86% CAGR across pharmacies, GP offices, and community clinics. The MyACR system employs colorimetric spectroscopy to realize 100% sensitivity and specificity in identifying severe nephropathy, and automatically transmits results to clinicians, neutering the logistical lag between sample collection and therapeutic action. Concurrently, lateral-flow cartridges detecting uromodulin and osteopontin are widening the analyte spectrum beyond albumin and creatinine.

Central laboratories are responding by layering proteomic and metabolomic services that require mass-spectrometry infrastructures, thereby preserving relevance for complex diagnostics. Hybrid models, where specimens are collected near patients and then shipped for central processing, merge convenience with analytical breadth. This multi-channel architecture underpins sustained volume growth in the kidney function tests market.

Geography Analysis

North America held 43.05% kidney function tests market share in 2025 on the back of mandated annual kidney health evaluations for adults with diabetes under CMS quality programs. Payers in the region reimburse both central-lab and POC assays, anchoring predictable revenue for suppliers. The United States also spearheads wearable diagnostics; prototype artificial-kidney belts leverage bioimpedance sensors and AI to produce real-time GFR estimates, spurring demand for companion confirmatory tests. Canada’s provincial health agencies are funding CKD screening in Indigenous communities, broadening addressable volume, while Mexico’s Seguro Popular upgrades include public dialysis centers that integrate on-site creatinine testing.

Asia-Pacific constitutes the fastest-expanding geography, projected at an 8.34% CAGR through 2031. China approved MediBeacon’s transdermal GFR monitor in 2025, marking the region’s openness to advanced diagnostics. India’s national dialysis scheme finances three weekly treatments for below-poverty-line patients and automatically triggers pre-dialysis creatinine checks, driving reagent volumes. Rising diabetes prevalence, coupled with expanding private insurance penetration, positions Indonesia, Thailand, and Vietnam as high-growth sub-markets within the kidney function tests market.

Europe maintains stable expansion as the KDIGO 2024 guidelines plus European Renal Best Practice commentary harmonize CKD management pathways. Nova Biomedical’s CE-marked Max Pro meter delivers creatinine and eGFR in 30 seconds at POC sites across the European Union, illustrating regulatory momentum toward decentralized diagnostics. Eastern European countries leverage EU structural funds to upgrade nephrology labs, balancing regional disparities. The Middle East and Africa face infrastructural constraints, yet Gulf Cooperation Council states are investing in dialysis centers that incorporate on-site urinalysis rooms. African union development grants are earmarked for portable creatinine readers that operate without continuous power. South America’s urbanization and lifestyle shifts fuel CKD prevalence; Brazil’s public health agency recently piloted pharmacy-based albumin-creatinine strip testing in São Paulo clinics. Collectively these regional vectors ensure the kidney function tests market continues its balanced growth narrative, combining volume uptake in emerging economies with technology-driven value expansion in mature ones.

Competitive Landscape

Market Concentration

The kidney function tests market shows moderate fragmentation. Abbott, Roche, and Siemens Healthineers preserve leading positions by bundling platforms, reagents, and informatics services. Roche’s cobas chemistry line gained an AI-driven eGFR algorithm update during 2025, enhancing performance in elderly populations. Siemens Healthineers scaled its Atellica CI Analyzer to mid-volume labs, pairing it with integrated albumin-creatinine reagents to lock in consumable revenue.

Consolidation is quickening. Quest Diagnostics agreed in February 2025 to acquire Fresenius Medical Care’s kidney-testing assets, enabling vertical integration with its renal patient service centers. MediBeacon secured USD 35 million growth capital to commercialize its transdermal GFR device globally, forging distribution alliances with dialysis chains. Meanwhile, startups such as Healthy.io target home-monitoring niches through smartphone imaging that requires no proprietary hardware, challenging incumbents on convenience.

Technology differentiation is the second axis of rivalry. Companies like NxGen Biomics employ multi-omics discovery to assemble biomarker panels that can predict rapid eGFR decline years in advance, positioning them for companion-diagnostic partnerships with pharma. Central-lab leaders counter by embedding liquid-handling robotics and cloud analytics into next-generation analyzers, lifting throughput to 2,000 tests per hour. White-space opportunities appear in low- and middle-income countries where reagent sachets compatible with off-grid POC readers can open new customer segments. Supply-chain fragility, however, pressures smaller vendors that lack dual-sourcing for critical chemicals. Larger firms are therefore establishing regional reagent fill-finish sites to localize production and hedge logistics risk, reinforcing scale advantages inside the kidney function tests market.

Global Kidney Function Tests Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Healthy.io acquired Labrador Health to enhance its at-home testing capabilities, combining biochemistry, microfluidics, and computer-vision technologies to deliver lab-grade results for chronic kidney disease monitoring in home settings.

- February 2025: Quest Diagnostics agreed to acquire Fresenius Medical Care’s kidney testing assets, consolidating its position in the specialized kidney diagnostics market.

- February 2025: MediBeacon’s Transdermal GFR System received device approval in China, expanding access to non-invasive kidney function assessment technology in the world’s largest healthcare market.

- May 2024: Thermo Fisher launched the CXCL10 test for kidney transplant patient monitoring, expanding biomarker options for post-transplant care management.

Table of Contents for Global Kidney Function Tests Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising prevalence of chronic kidney disease (CKD)

- 4.2.2Growing diabetes & hypertension burden

- 4.2.3Government-backed CKD screening programs

- 4.2.4Automation & POC technology advances

- 4.2.5Multi-omics + AI early-diagnosis biomarker panels

- 4.2.6Adoption of wearable & home-monitoring kidney sensors

- 4.3Market Restraints

- 4.3.1High cost of analyzers & consumables

- 4.3.2Stringent regulatory & reimbursement hurdles

- 4.3.3Lack of clinical standardisation for novel biomarkers

- 4.3.4Supply-chain fragility for critical reagents in LMICs

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Dipsticks

- 5.1.2Disposables

- 5.1.3Reagents

- 5.2By Test Type

- 5.2.1Urine Tests

- 5.2.1.1Urine Protein Tests

- 5.2.1.2Creatinine Clearance Tests

- 5.2.1.3Micro-albumin Tests

- 5.2.2Blood Tests

- 5.2.2.1Serum Creatinine Tests

- 5.2.2.2eGFR / Glomerular Filtration Rate Tests

- 5.2.2.3Blood Urea Nitrogen Tests

- 5.3By End User

- 5.3.1Hospitals and Clinics

- 5.3.2Diagnostic Laboratories

- 5.3.3Home and Point-of-Care Settings

- 5.3.4Others

- 5.4By Testing Setting

- 5.4.1Central-Lab Based

- 5.4.2Point-of-Care

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Abbott Laboratories

- 6.3.2F. Hoffmann-La Roche Ltd.

- 6.3.3Siemens Healthineers

- 6.3.4Sysmex Corporation

- 6.3.5Beckman Coulter Inc. (Danaher Corporation)

- 6.3.6Nova Biomedical

- 6.3.7Thermo Fisher Scientific

- 6.3.8Arkray Inc.

- 6.3.977 Elektronika Kft

- 6.3.10ACON Laboratories Inc.

- 6.3.11Randox Laboratories

- 6.3.12Quest Diagnostics

- 6.3.13Laboratory Corporation of America Holdings

- 6.3.14URIT Medical Electronic Co. Ltd

- 6.3.15bioMérieux SA

- 6.3.16Alfa Wassermann Diagnostic Technologies

- 6.3.17Bio-Rad Laboratories

- 6.3.18Ortho-Clinical Diagnostics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Kidney Function Tests Market Report Scope

As per the scope of the report, kidney function tests are simple procedures that generally use either blood or urine to help identify issues in the kidneys. The kidney function tests market is segmented by Product Type (Dipsticks, Disposables, and Reagents), Test Type (Urine Test (Urine Protein Tests, Creatinine Clearance Tests, and Microalbumin Tests), and Blood Tests (Serum Creatinine Tests, Glomerular Filtration Rate Tests, and Blood Urea Nitrogen Tests), End User (Hospitals and Clinics, Diagnostic Laboratories, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.