Kidney Stone Retrieval Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

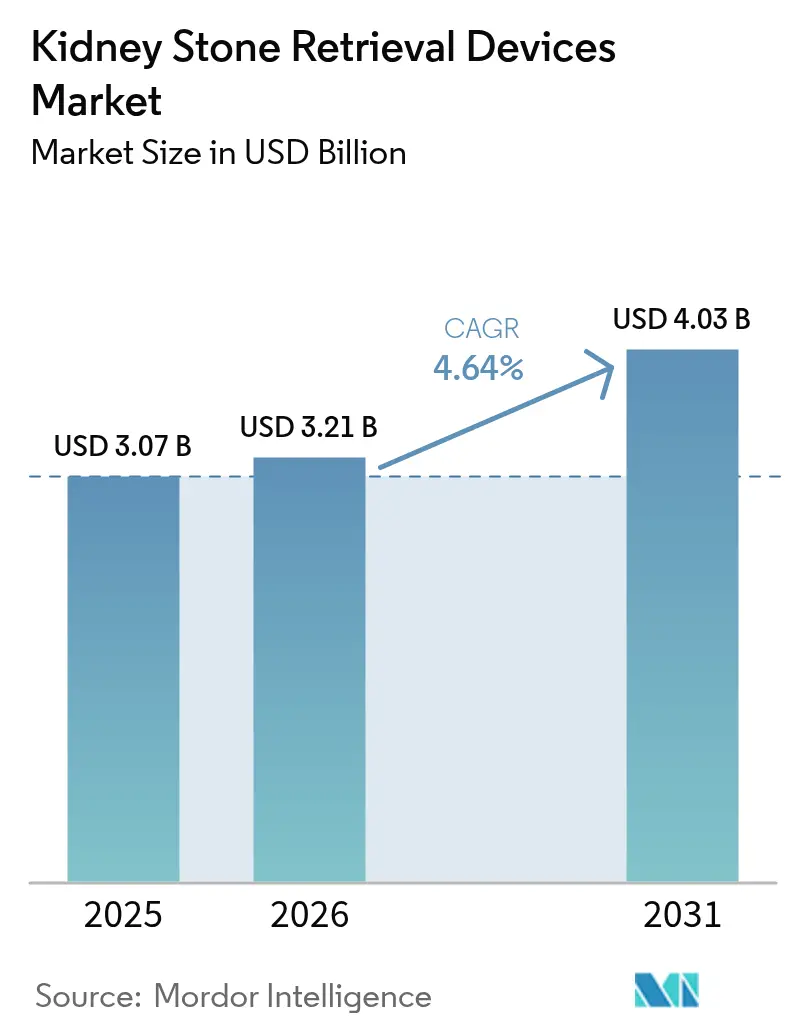

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 4.03 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kidney Stone Retrieval Devices Market Analysis by Mordor Intelligence

The kidney stone retrieval devices market size is expected to grow from USD 3.07 billion in 2025 to USD 3.21 billion in 2026 and is forecast to reach USD 4.03 billion by 2031 at 4.64% CAGR over 2026-2031. Sustained momentum in the kidney stone retrieval devices market arises from the climbing incidence of urolithiasis in ageing populations, the ongoing shift toward minimally-invasive treatment pathways, and the swift roll-out of single-use flexible ureteroscopes, thulium-fiber lasers, and other purpose-built retrieval accessories. Broader reimbursement—illustrated by CMS transitional pass-through payments for single-use scopes—reduces economic barriers, while outpatient centers capture a rising proportion of routine stone procedure. Competitive intensity in the kidney stone retrieval devices market stays moderate as Boston Scientific, Olympus Corporation, Cook Medical, and other leaders combine hardware innovation, physician training, and geographic expansion to widen procedural reach. Cost headwinds linked to premium digital scopes and volatile nitinol supply chains persist, yet cost-effective single-use options and steadily improving reimbursement dilute downside risk.

Key Report Takeaways

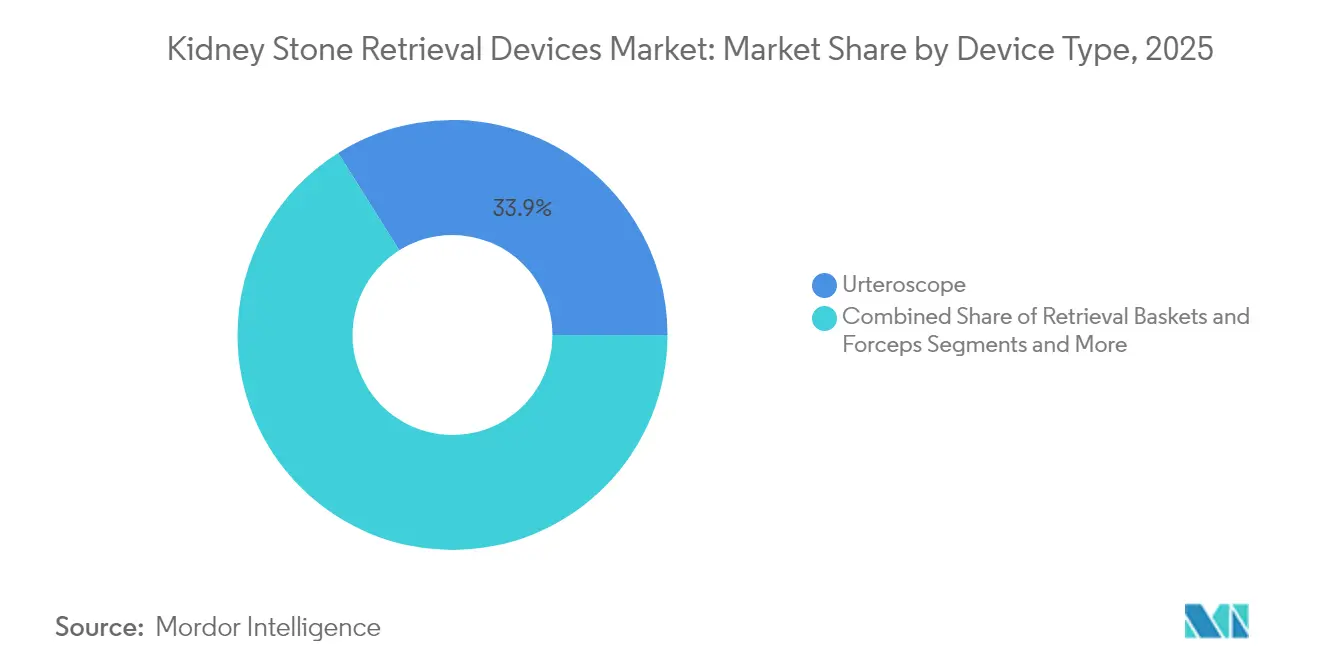

- By device type, ureteroscopes led with 33.92% of the kidney stone retrieval devices market share in 2025, while lithotripters are forecast to expand at a 5.12% CAGR through 2031.

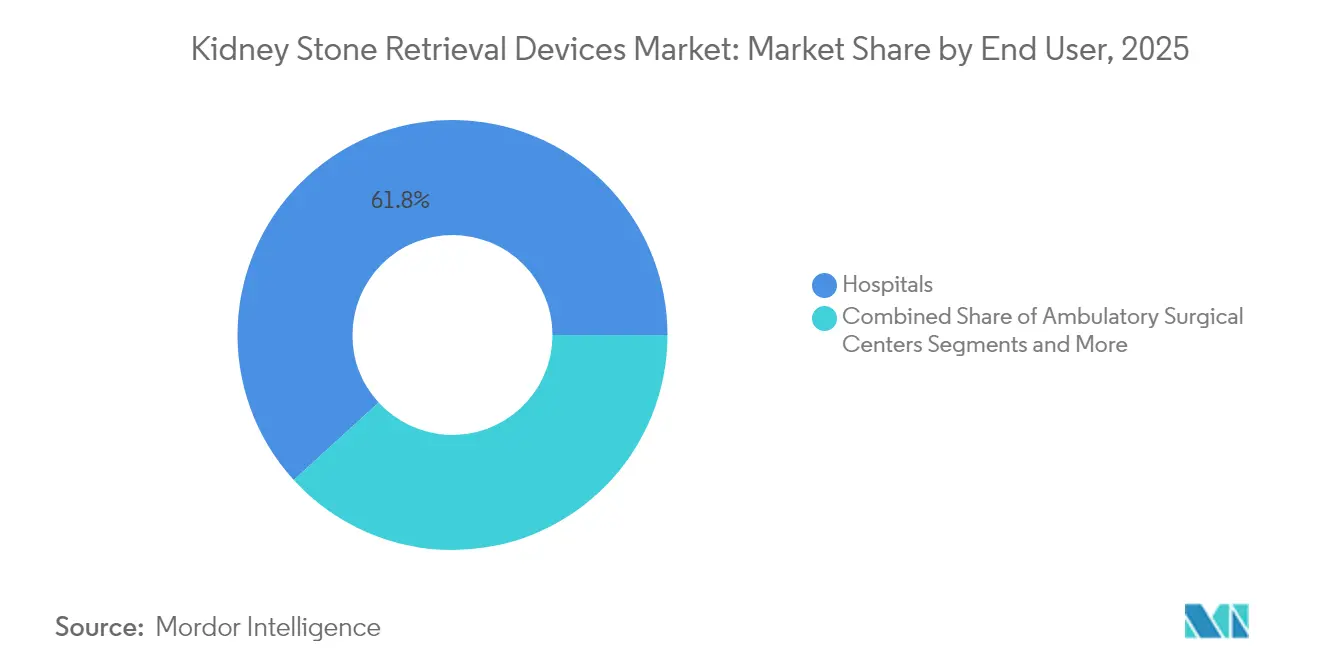

- By end-user, hospitals commanded 61.78% share of the kidney stone retrieval devices market size in 2025; ambulatory surgical centers are advancing at a 6.05% CAGR through 2031.

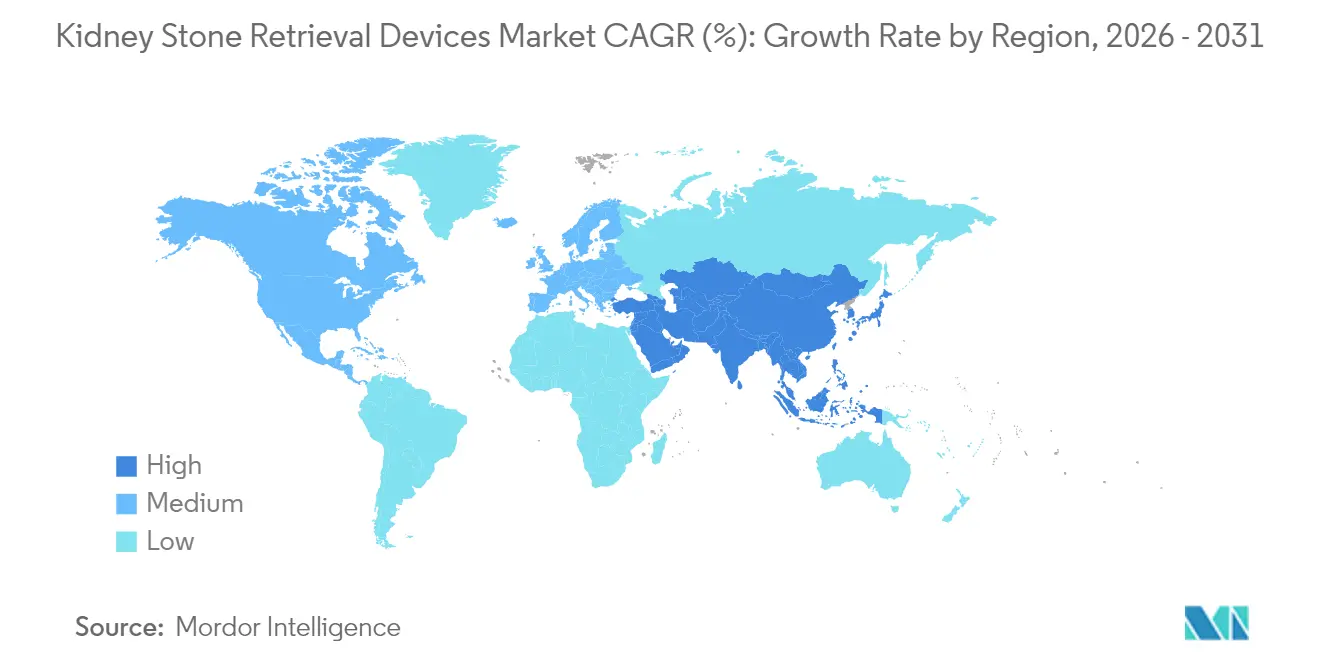

- By geography, North America held 42.12% of the kidney stone retrieval devices market share in 2025, whereas Asia-Pacific is projected to grow the fastest at 6.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kidney Stone Retrieval Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward single-use flexible ureteroscopes | +1.2% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Growing prevalence of urolithiasis in ageing populations | +0.9% | Especially Asia-Pacific | Long term (≥ 4 years) |

| Wider reimbursement for minimally-invasive procedures | +0.8% | North America and EU core; widening in APAC | Medium term (2-4 years) |

| Rapid adoption of thulium-fiber and burst-wave lithotripsy | +0.7% | Developed markets first | Short term (≤ 2 years) |

| AI-assisted endoscopic navigation reducing OR time | +0.5% | Early pilots in North America and Europe | Medium term (2-4 years) |

| ESG pressure favoring low-water, low-radiation techniques | +0.3% | Initially EU; gradually worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward single-use flexible ureteroscopes

Clinical evidence shows that single-use scopes remove reprocessing costs, cut cross-contamination risk, and deliver comparable stone-free outcomes to reusable equivalents. Per-case expenditure ranges from USD 1,300–3,180, making them economical for facilities handling fewer than 50 cases annually. Boston Scientific’s LithoVue platform spearheads adoption, while Olympus will introduce its first single-use ureteroscope in Europe in H2 FY2025. CMS transitional pass-through payments under code C1747 bolster the kidney stone retrieval devices market by improving outpatient economics.

Wider reimbursement for minimally-invasive procedures

Medicare recognizes ureteroscopic lithotripsy as reasonable and necessary, and CMS recently assigned Category I CPT codes to Olympus’s iTind system, signaling willingness to remunerate validated innovation[1]Source: Centers for Medicare & Medicaid Services, “National Coverage Determination for Kidney Stone Treatment,” cms.gov. Field reimbursement managers and ROI calculators from Boston Scientific help providers navigate billing, smoothing adoption paths in the kidney stone retrieval devices market .

Rapid adoption of thulium-fiber and burst-wave lithotripsy

Thulium-fiber lasers shorten operative time by 20% and save USD 69 per case versus holmium:YAG systems. Japanese case series recorded basketing times of 7 minutes compared with 21 minutes for legacy lasers while maintaining equal stone-free rates. Compact consoles needing only standard outlets suit smaller clinics and expand the kidney stone retrieval devices market.

AI-assisted endoscopic navigation reducing OR time

More than 69 studies highlight AI benefits in stone recognition and outcome prediction. Early robotic flexible ureteroscopy platforms achieved 93.48% stone-free rates for stones <4 mm in initial clinical use. AI-ready optics increase differentiation inside the kidney stone retrieval devices market, yet regional data-governance gaps and uneven digital literacy slow mainstreaming[2]Source: APACMed, “Realizing the Value of AI in MedTech within Asia Pacific,” apacmed.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of digital ureteroscopes | -0.8% | Global; steeper in emerging markets | Medium term (2-4 years) |

| Device-related infection and encrustation risk | -0.6% | Global with variable oversight | Short term (≤ 2 years) |

| Shortage of endourology specialists | -0.5% | Low- to middle-income nations, rural zones | Long term (≥ 4 years) |

| Supply-chain dependence on nitinol | -0.4% | Concentrated supplier base worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital cost of digital ureteroscopes

Reusable flexible scopes cost USD 50,000–150,000 and require supporting lasers and imaging stacks exceeding USD 200,000, delaying ROI for resource-constrained sites. Single-use scopes shift cost to operating budgets but can top USD 3,000 per case at low volume, complicating procurement decisions in the kidney stone retrieval devices market.

Device-related infection and encrustation risk

Stent encrustation risk rises after prolonged dwell times, sometimes demanding secondary surgeries. The FDA issued a class I recall on a renal-aspiration system in 2025, underscoring regulatory vigilance in the kidney stone retrieval devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Ureteroscopes Extend Their Lead

The ureteroscope segment accounted for 33.92% of the kidney stone retrieval devices market share in 2025, which translated to roughly USD 1.04 billion of the 2025 kidney stone retrieval devices market size. Dominance stems from the instrument’s essential role in visualising and accessing calculi throughout the urinary tract, while recent upgrades in digital imaging and smaller outer diameters improve manoeuvrability and patient safety. Single-use digital ureteroscopes accelerate volume growth because hospitals can eliminate repair downtime, reprocessing expense and cross-contamination risk. Reusable fleets remain relevant in high-volume academic centres that can amortise reprocessing infrastructure and secure multiyear service contracts. Retrieval baskets and guidewires move in parallel since every ureteroscopic case requires at least one ancillary tool for fragment extraction or device placement.

Lithotripters represent the fastest-growing device class with a projected 5.12% CAGR to 2031, led by thulium-fibre laser consoles that deliver faster fragmentation with lower retropulsion than holmium:YAG systems medical.olympusamerica.com. Compact footprint, standard-outlet power requirements and embedded safety controls allow smaller ambulatory sites to adopt high-energy lasers that once belonged only in tertiary theatres. Access sheaths with suction ports shorten operative time by lowering intrarenal pressure and clearing debris in real time, a benefit that dovetails with advanced laser performance. Manufacturers are layering artificial-intelligence algorithms on top of digital video streams to automate stone detection and propose optimal laser settings, adding another point of differentiation in the kidney stone retrieval devices market. Environmental sustainability also shapes buying criteria; vendors now highlight recyclable packaging and lower water consumption during scope cleaning to align with hospital ESG goals.

By End-User: Hospitals Anchor Demand while Ambulatory Centres Accelerate

Hospitals generated 61.78% of the kidney stone retrieval devices market size in 2025, or around USD 1.9 billion, thanks to 24/7 capability, multidisciplinary backup and access to capital for premium optics. Emergency departments funnel acute renal-colic cases directly into surgical suites, underpinning steady baseline volumes. Academic centres also serve as early adopters of AI-ready scopes and simulation tools, influencing regional referral patterns. Budget committees increasingly scrutinise total cost of ownership, leading many systems to deploy mixed fleets: reusable scopes for predictable high-volume lists and single-use models for infectious or anatomically complex cases. Vendor service bundles that combine training, predictive maintenance and data dashboards help hospitals optimise asset utilisation and justify capital expense.

Ambulatory surgical centres (ASCs) are the fastest-growing channel with a 6.05% CAGR to 2031, propelled by CMS transitional pass-through payments that offset disposable scope costs and align reimbursement with outpatient economics. Same-day discharge, flexible scheduling and lower facility fees appeal to payers and patients alike, shifting straightforward sub-2 cm stones away from inpatient settings. ASCs favour single-use scopes because the devices remove the need for costly reprocessing rooms and biofilm-monitoring protocols. Specialty urology clinics move in a similar direction, often leveraging group-purchasing contracts or mobile laser-rental services to control overhead. The migration of routine procedures to outpatient venues broadens geographic access, fosters price competition and cements the kidney stone retrieval devices market as an integral component of value-based care pathways.

Geography Analysis

North America controlled 42.12 % of the kidney stone retrieval devices market in 2025, buoyed by comprehensive payer coverage and high surgeon density. Medicare reimbursement for transurethral lithotripsy and CMS pass-through payments for single-use scopes solidify procedural economics. Boston Scientific reported 23.5 % Urology segment growth in Q1 2025 as hospitals and ASCs upgraded to digital single-use platforms. Canada mirrors this trend under provincial funding, although capital constraints lengthen purchasing cycles for AI-ready consoles.

Asia-Pacific represents the fastest-growing region, expanding at a 6.86 % CAGR through 2031. Rising prevalence, urbanisation and improving insurance penetration fuel procedure volumes. China’s national data show a decisive tilt toward ureteroscopic treatment; Japan leads in thulium-fiber laser utilisation, and India’s private-insurance growth unlocks demand for cost-effective single-use scopes. Governments pursue Access-Capability-Trust frameworks to harmonise device approvals, upskill surgeons and build digital infrastructure—steps vital for sustained expansion of the kidney stone retrieval devices market.

Europe exhibits steady growth, supported by Medical Device Regulation compliance and ESG-weighted procurement criteria. Olympus is set to launch its first single-use ureteroscope in H2 FY2025, catering to hospitals aiming to reduce cross-infection and water consumption. Training deficits loom as the Simulator Availability Index for ureteroscopy trainers declined in recent surveys, hinting at potential workforce bottlenecks doi.org. South America and the Middle East participate through technology-transfer partnerships, whereas Africa faces financing hurdles and remains an untapped frontier of the kidney stone retrieval devices market.

Regulatory Landscape

In the United States, many kidney stone retrieval accessories and endourology tools used in ureteroscopic stone management (such as ureteral stone dislodgers/baskets) fall under FDA Class II controls and commonly follow the 510(k) premarket notification pathway, requiring demonstration of substantial equivalence to predicate devices. Recent clearances in 2026 highlight ongoing regulatory throughput for both disposable retrieval tools and emerging lithotripsy modalities, including FDA 510(k) clearances for SonoMotion's Break Wave device (January 2026) and a subsequent Special 510(k) update (April 2026), as well as a 510(k) clearance in April 2026 for Zhejiang Soudon Medical Technology Co., Ltd. for a disposable stone extraction basket.

In Europe, kidney stone retrieval devices are governed by the Medical Devices Regulation (MDR) (EU) 2017/745, which places heavier emphasis on comprehensive technical documentation, clinical evaluation, and post-market clinical follow-up (PMCF). The MDR transition continues to influence manufacturer compliance planning, with increased scrutiny on areas central to this market such as sterilization validation, biocompatibility, and performance data for nitinol or metal-based instruments used in retrieval baskets, guidewires, and access systems.

Value Chain Analysis

The value chain spans specialized raw materials and components (notably nitinol for memory-alloy baskets, PTFE and other low-friction polymers for liners and tubing, and stainless steel for support elements) through precision manufacturing and assembly steps such as extrusion of polymer shafts, coating (hydrophilic/low-friction), and cleanroom assembly aligned with ISO 13485 quality systems. For many retrieval baskets, access sheaths, and guide sheaths, tight process control is critical to ensure torque response, kink resistance, and consistent opening/closure behavior of distal retrieval elements.

OEM/ODM production plays a meaningful role in scaling capacity for disposable and semi-disposable product lines, while branded device companies differentiate via system integration (single-use ureteroscopes, suction-enabled access sheaths, and ancillary retrieval tools), physician training, and service support. Distribution typically runs through direct sales to hospitals and ambulatory surgical centers for capital and procedural ecosystem products, alongside tendering and group purchasing for high-throughput consumables; supply risk remains most visible around specialty alloys (including nitinol) and coating/sterilization throughput that can constrain lead times for single-use portfolios.

Competitive Landscape

The kidney stone retrieval devices market is moderately consolidated. Boston Scientific commands leadership with its LithoVue single-use digital ureteroscope, reinforced by robust reimbursement support and data-monitoring tools. Olympus follows with its SOLTIVE SuperPulsed Laser and forthcoming single-use scope. Cook Medical, KARL STORZ and Dornier MedTech complete the leading cohort, each supplying complementary products—access sheaths, imaging towers, or shock-wave systems.

Strategic deals illustrate dynamic competition. Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular-intervention assets widens its catheter-based therapeutic arsenal . KARL STORZ’s proposal to purchase robotic-surgery firm Asensus underscores growing interest in flexible robotics and AI integration. Emerging players such as Calyxo and EndoTheia pursue niche differentiation—continuous-aspiration evacuation and steerable stone baskets respectively—offering hospitals new avenues to boost stone-free results

Beyond hardware, vendors vie in sustainability credentials, training ecosystems and digital-analytics services. Initiatives range from carbon-neutral manufacturing roadmaps to cloud dashboards that benchmark scope utilisation—features increasingly decisive in tender evaluations inside the kidney stone retrieval devices market.

Kidney Stone Retrieval Devices Industry Leaders

Boston Scientific Corporation

Becton, Dickinson and Company

Cook Medical

Olympus

STORZ MEDICAL AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening around non-invasive and lower-acuity care pathways that reduce dependence on operating room time and anesthesia, supported by recent regulatory progress for new lithotripsy approaches. In January 2026, SonoMotion received FDA 510(k) clearance for its Break Wave device for urinary stone fragmentation (with an additional Special 510(k) clearance in April 2026), providing a concrete example of office-oriented, ultrasound-based fragmentation technology moving through mainstream regulatory gates. This creates room for device vendors to build complementary retrieval and fragment-management workflows that reduce residual fragments, including combinations of fragmentation tools with retrieval baskets, guidewires, and access platforms.

Within ureteroscopy-driven care, procurement is shifting from standalone instruments to integrated systems that target stone-free outcomes and intrarenal pressure management during retrograde intrarenal surgery. Market activity around suction-assisted ureteral access sheaths and single-use digital ureteroscopes supports opportunities for bundled offerings across scopes, suction-enabled access, and retrieval accessories that simplify setup for ambulatory surgical centers and help standardize procedures. Updated 2026 urolithiasis guidance from professional bodies such as the AUA and EAU reinforces minimally invasive decision pathways by stone size and location, creating a clearer framework for hospitals and ASCs to align equipment standardization, training, and consumable utilization across ureteroscopes, lithotripters, and retrieval tools.

Recent Industry Developments

- March 2026: Boston Scientific received US FDA 510(k) clearance for the Asurys Fluid Management System for irrigation and distention during endoscopic urologic procedures, including ureteroscopy. The clearance strengthens procedure-room workflow offerings adjacent to ureteroscopes and retrieval accessories, and supports vendors competing on end-to-end ureteroscopy ecosystems rather than standalone instruments.

- September 2025: Dornier MedTech America announced full US commercial launch of the Dornier Hoover Flexible and Navigable Suction Ureteral Access Sheath (FANS) and the Dornier Axis II Slim single-use ureteroscope. The launch expands the installed base for suction-assisted ureteroscopy workflows, increasing pull-through demand for compatible baskets, guidewires, and ancillary retrieval devices used to finish cases with fewer residual fragments.

- November 2024: EndoTheia announced successful completion of a first-in-human clinical trial of its FlexStone Basket, an independently steerable kidney stone retrieval device, in partnership with Nissha Medical Technologies. The clinical milestone advances steerable retrieval concepts aimed at improving access to difficult calyces, adding competitive pressure on legacy basket designs and encouraging differentiation in maneuverability and stone engagement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from devices used by clinicians to locate, fragment, and retrieve urinary stones during kidney stone procedures, across hospital and outpatient care settings, and reported in USD.

Scope exclusions: We exclude diagnostic imaging equipment, oral drug therapies for stone dissolution, and non-device home care products that do not directly enable stone fragmentation or retrieval.

Segmentation Overview

- By Device Type

- Ureteroscopes

- Retrieval Baskets & Forceps

- Lithotripters

- Ureteral Stents

- Dilators & Access Sheaths

- Guidewires

- By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty & Urology Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to anchor the demand pool and the care setting mix before we build the numeric model. We typically start from public health and procedure signals such as urolithiasis prevalence and treatment setting shifts, and then map them to device usage patterns (for example, how often a ureteroscopy case uses a basket, sheath, guidewire, or stent).

For this, we rely on non-paywalled sources such as CDC and NIH publications for disease and utilization indicators, CMS fee schedules and outpatient policy updates, WHO health statistics for broad demographic baselines, and peer-reviewed urology journals for clinical practice patterns and technology adoption. Trade association websites and conference proceedings are also reviewed for standards language and device category definitions, followed by company annual reports, investor presentations, and press releases to understand product mix and geographic exposure. Where needed, we consult paid subscriptions for company financials and intelligence, patent databases, and import-export shipment views to sense-check supply and pricing direction. These desk sources are illustrative, and many other public documents were also used to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work is used to verify procedure-level device usage and the price ladder across reusable and single-use tools, which often shifts by facility type and purchasing contracts. We interview urologists, procurement heads, ambulatory surgery center operators, and device distributors across major regions so assumptions from desk work can be corrected, and then the model can be closed with realistic utilization and pricing ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 42% |

| Mid tier: 60% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 15% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where procedure volumes and care setting splits are reconstructed from public utilization signals, and then translated into device demand using typical per-procedure consumption. The totals are corroborated with selective bottom-up approximations, such as sampled average selling price (ASP) times units for key device groups, distributor feedback on category throughput, and supplier revenue mix checks, and then adjusted where the two views do not align.

In practice, the model leans on a small set of fingerprints that are easy to track each year. These include urolithiasis prevalence trends, the share of cases treated with ureteroscopy versus lithotripsy or PCNL, shifts toward outpatient sites, adoption rates for single-use versus reusable ureteroscopes, and observed ASP movement for baskets, access sheaths, guidewires, and stents as hospitals renegotiate contracts. Where a country lacks clean procedure reporting, we bridge gaps using proxy indicators like population age mix, specialist density, and regional procedure rates shared by clinical respondents.

For forecasting, we use scenario analysis supported by a light multivariate view, where procedure growth, outpatient migration, and single-use penetration are treated as the main drivers, and pricing is stepped based on expected mix and tender behavior. Assumptions are kept explicit so changes in reimbursement, infection-control preferences, or new laser adoption can be translated into a revised volume and ASP path without rebuilding the model from scratch.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model output and independent signals, such as procedure growth direction, facility adoption narratives, and reported product mix shifts discussed in public filings. Large variances are flagged, and we revisit the underlying drivers, including unit intensity per case, price bands by setting, and currency conversions, before the market totals are signed off.

A second analyst review is completed to confirm that inputs, math, and written assumptions match, and that regional totals reconcile with the global roll-up. Reports are refreshed annually, and interim updates are triggered when material events occur, such as policy changes affecting outpatient reimbursement or major technology adoption shifts. Before delivery, a final pass is done so clients receive the most current view that can be supported by traceable inputs and repeatable checks.

Mordor Intelligence's Kidney Stone Retrieval Devices Market Size Compared With Other Published Estimates

Published market sizes for kidney stone retrieval devices often do not match because the counting rules differ, even when the titles look similar. The most common reasons are what device categories are bundled into the total, which care settings are assumed to drive growth, and how pricing is updated when the mix shifts toward single-use tools.

In our build, the biggest swing factors are the year-specific FX conversion timing, the way ASPs are stepped for reusable versus single-use ureteroscopes and their accessories, and whether procedure-driven demand checks are revisited after reimbursement or outpatient policy moves, which is why Mordor Intelligence treats refresh and validation as part of the sizing step and not a one-time setup.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.07 B (2025) | |

| Industry Consultancy A | USD 2.94 B (2024) | Uses an earlier base year and may carry forward pricing with a flatter progression, which can understate mix-driven ASP lift from single-use adoption and premium accessory attach rates. |

| Industry Publisher B | USD 3.07 B (2025) | Matches the headline year but can differ on scope boundaries, where some totals include adjacent urology disposables more broadly, and FX timing assumptions are not always stated, making cross-region aggregation less transparent. |

The spread across the figures is mainly explained by when prices and currencies are refreshed and how tightly device revenues are linked back to procedure demand in ureteroscopy, lithotripsy, and PCNL. By keeping those assumptions visible and re-checking them against real-world utilization signals, the final number remains easier to audit and to update when market conditions change.

Key Questions Answered in the Report

What is the current kidney stone retrieval devices market size?

The kidney stone retrieval devices market size reached USD 3.21 billion in 2026 and is forecast to grow to USD 4.03 billion by 2031.

Which procedure dominates global stone-removal volumes?

Ureteroscopic lithotripsy dominates, owing to its minimally-invasive nature, high stone-clearance rates and short recovery times.

Why are ambulatory surgical centers expanding fast?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Global Kidney Stone Retrieval Devices Market?

CMS pass-through payments for single-use scopes improve outpatient economics, helping ASCs record a 6.05 % CAGR through 2031.

Which region offers the highest growth rate?

Asia-Pacific is projected to expand at a 6.86 % CAGR through 2031 on rising disease prevalence, healthcare spending and technology adoption.

How is sustainability shaping purchasing decisions?

European and increasingly global tenders score device vendors on carbon footprint, water use and recyclability, rewarding companies with clear ESG roadmaps.

Page last updated on: